Quick Answer

For most India business receipts, use SWIFT or a bank trade-inward-remittance workflow as the starting rail, collect the purpose code and invoice reference before money moves, and treat NEFT or UPI only as domestic or corridor-specific layers. Keep MTSS for personal inward remittances, not business collections.

Separate cross-border receipt, local settlement, and proof#

If you want to receive international payments in India without month-end confusion, map the rail in the right order. The cross-border leg, the India settlement leg, and the documentary proof are three separate things.

For most business receipts, the cross-border leg is a bank-led wire or inward trade remittance. NEFT, RTGS, or IMPS may appear only after the money is already inside India. UPI can matter, but only in supported acceptance models rather than as a universal replacement for bank receipt from any payer abroad.

This guide stays narrow on India operations: rail choice, admissible use cases, onboarding fields, and the evidence pack you need for reconciliation. If you also control the payer side, read The Best Way to Pay an Indian Development Agency from the US alongside this article.

Start with the rail map, not the provider logo#

The fastest way to create failed receipts is to ask a foreign payer to use a domestic India rail name as if it were the international channel. RBI's NEFT FAQ, updated on September 2, 2024, makes clear that NEFT is India's domestic centralised payment system. It can be used for inward foreign exchange remittances once the payment is already inside the India banking system, but it is not the originating cross-border rail itself.

| Option | Best fit | What it really is | Key ops constraint |

|---|---|---|---|

| SWIFT or bank wire to India | Invoice-led B2B collections and higher-value receipts | The cross-border bank-to-bank leg | You need clean beneficiary, correspondent, and charge instructions before funds move |

| Bank trade inward remittance workflow | Export goods or service receipts into a business account | A bank-managed process for credit plus purpose and document review | Credit can be delayed if purpose code or export documents are incomplete |

| UPI-based international acceptance | Supported merchant flows or foreign-traveller acceptance in India | A corridor-specific acceptance model, not generic remote overseas bank receipt | You need confirmed merchant activation and settlement outputs before go-live |

| MTSS | Personal inward remittances and foreign-tourist scenarios | A personal inward remittance scheme under RBI rules | It is not for trade-related business receipts |

| NEFT or other domestic India transfer | India-side credit or onward domestic movement after receipt | The domestic settlement leg after the international payment reaches India | Do not present it to the overseas payer as the international method |

That separation matters because each lane changes who owns missing data. On a wire, missing beneficiary or correspondent details usually create bank-side repair work. On a trade remittance, missing purpose and documentary fields delay disposal or credit. On UPI, the real risk is promising acceptance your merchant setup does not actually support.

Use SWIFT or a bank trade workflow for most business receipts#

Default business rule: if you invoice clients abroad, start with a bank-led inward receipt path. ICICI's wire transfer guidance describes the flow as a SWIFT-based receipt into India, with remittance tracking, correspondent-bank details by currency, and sender-side routing information. That is the right starting model when the payer is outside India and you need money in an Indian account.

For business collections, ICICI's trade remittances page is even closer to the real operating model. It treats inward trade remittances as export proceeds that are credited after the required purpose and export documents are submitted. That is the right mental model for B2B and export-of-services flows: the money and the documentation clear together.

The same ICICI wire page says inward wires are supported in 41 currencies and are generally received within 1-2 working days. The bank's trade-remittance page says inward trade receipts can be received in 24+ currencies and says funds are credited within 1 hour of receiving disposal instructions and required documents, subject to verification. Treat those as bank-specific checkpoints, not corridor-wide promises. You still need to test the exact account, currency, and document pack your team will actually use.

Use UPI only in supported cross-border acceptance models#

UPI helps only when your acceptance model supports it. NPCI's UPI One World guide is explicit that the product is for inbound travellers, offered to foreign nationals and NRIs from G20 countries, and usable at UPI-enabled merchant locations in India. That can be useful if your payer is physically in India and your merchant acceptance stack supports the flow.

Scope rule: it is not the same as telling any overseas client to pay your UPI ID from abroad. If the customer is remote, ask your PSP, acquirer, or bank to prove the exact corridor, customer experience, settlement account, and dispute handling before you launch. If they cannot do that, keep UPI as a local acceptance option rather than your core international receipt lane.

Treat NEFT as the India-side leg#

When you see NEFT in an inbound setup, it usually describes the India-side credit or onward movement after FX conversion or settlement. RBI's September 2, 2024 FAQ says the system runs 24x7 in half-hourly batches, supports receipt as well as transfer, and uses IFSC plus beneficiary account details. That makes it a practical domestic leg once the international receipt has already been processed.

Your operator rule should be simple: never give an overseas customer pay me by NEFT as the starting instruction. Give them the bank-wire or bank-managed inward-remittance instruction instead, then decide whether the final rupee credit or treasury movement happens through NEFT, RTGS, or no extra domestic leg at all.

Keep MTSS for personal inward remittances only#

Use RBI's MTSS master direction to draw a hard line between personal and business receipts. RBI's direction, updated on November 28, 2025, describes MTSS as a quick and easy way to transfer personal remittances into India. It permits only inward personal remittances such as family maintenance or remittances favouring foreign tourists visiting India.

The same direction also says trade-related remittances, property purchase, investments, and credit to NRE accounts should not be handled through MTSS. It also caps each remittance at USD 2500 and limits a single beneficiary to 30 remittances in a calendar year. So if you are receiving export proceeds, freelancing income, marketplace revenue, or SaaS invoices, MTSS is the wrong lane even if it looks faster at the front end.

Use published numbers as gate checks, not marketing copy#

| Source | Published number or rule | Why you care |

|---|---|---|

| RBI NEFT FAQ updated Sep 2, 2024 | 24x7 operation in half-hourly batches | Confirms NEFT is a domestic credit option, not the cross-border origin rail |

| ICICI inward wire page | 41 currencies and 1-2 working days | Use as a checkpoint for currency coverage and realistic bank timing |

| ICICI trade remittance page | 24+ currencies and 1 hour after disposal instruction and documents, subject to verification | Shows how document readiness changes credit timing on business receipts |

| RBI MTSS direction updated Nov 28, 2025 | USD 2500 cap and 30 remittances per beneficiary per year | Confirms MTSS is a personal inward-remittance lane, not a scalable business rail |

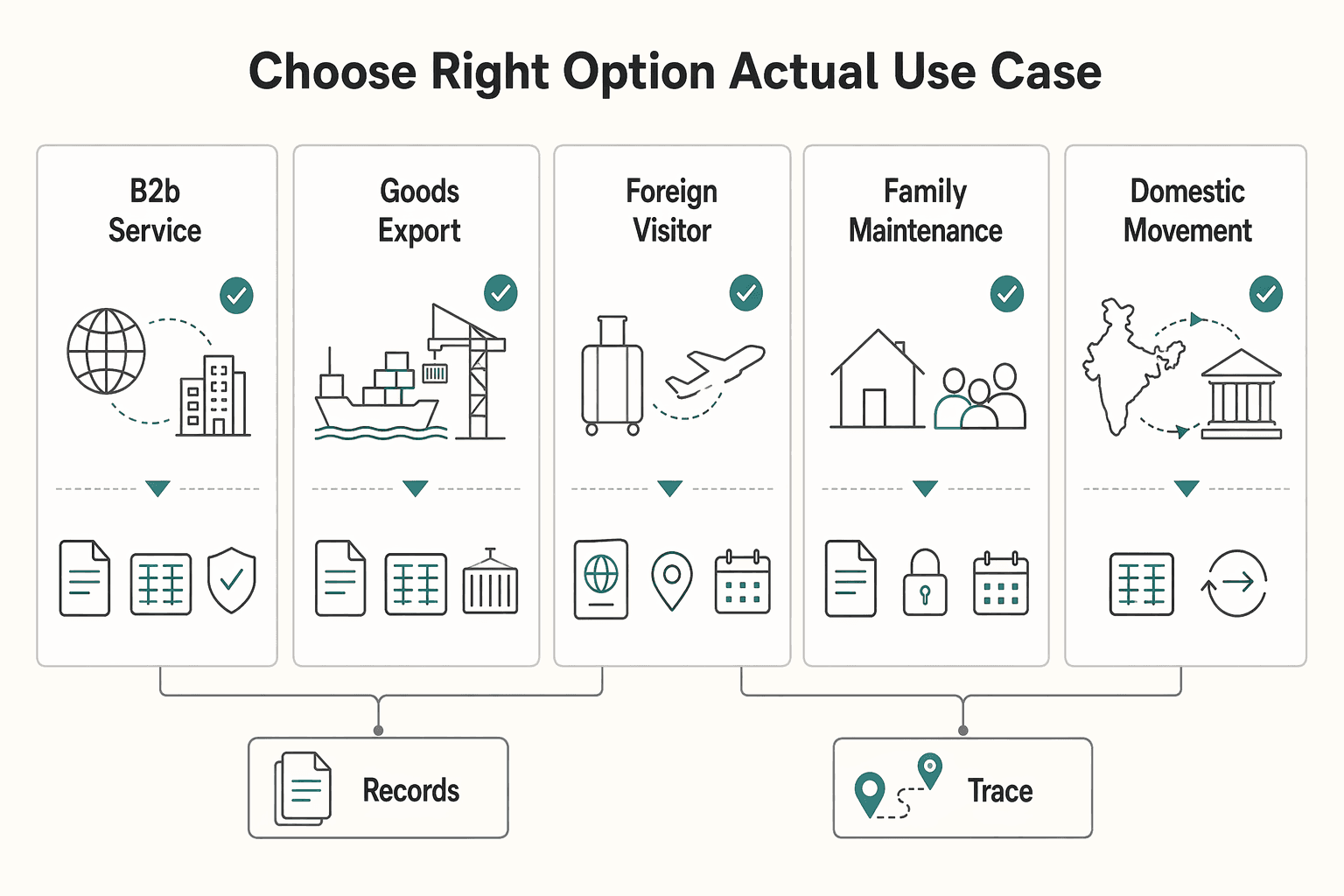

Choose the right option for the actual use case#

Once you stop mixing lanes, the decision becomes operational rather than emotional. Pick the option that gives you the cleanest match between payer intent, bank credit, and documentary proof.

| Use case | Primary rail | Why it fits | What you verify before go-live |

|---|---|---|---|

| B2B service invoice from an overseas client | SWIFT or bank trade inward remittance | Strongest bank trail for invoice-led receipts | Purpose code, sender instructions, charge handling, post-credit proof |

| Goods export receipt | Bank trade inward remittance | Shipping and export documents can be handled in the same workflow | Invoice, shipping documents, disposal instruction, expected bank certificate |

| Foreign visitor paying you in India | Approved UPI acceptance or UPI One World-capable merchant flow | Fast merchant experience when the payer is physically in India | Merchant activation, supported instrument, settlement account, reconciliation export |

| Family maintenance or other personal support | MTSS or bank personal inward remittance | Fits RBI's personal inward remittance rule set | Recipient identity, KYC status, payout method, no trade use |

| Domestic movement after international credit | NEFT or other domestic bank transfer | Traceable India-side routing after the foreign receipt lands | Beneficiary account, IFSC, internal reference, statement matching |

Export and service receipts#

For export of goods or services, behave as though your bank is part of the receivables workflow, because it is. ICICI's trade-remittance guide says inward trade remittances are credited after the required documents and purpose are in place, and it also distinguishes BIRC and FIRC scenarios instead of pretending one certificate covers everything.

Use that as an onboarding standard. If your bank publishes separate timelines for retail wire receipt and trade receipt, keep those flows separate in your playbook. A bank's faster documentary lane for trade inward remittance does not automatically apply to every freelance invoice, and a generic retail inward wire page does not answer export-proof questions for your finance close.

That should change how you onboard customers. Before the first live invoice, decide which bank account will receive the money, which purpose-code family applies, whether finance expects BIRC, FIRC, FIRA, or only inward advice, and how you will link the bank credit to the invoice. If your team still treats this as post-credit cleanup, read What is a Foreign Inward Remittance Certificate (FIRC) and Why It Matters before launch.

Foreign visitors or in-person merchant collection#

If the payer is in India and behaving like a retail or travel customer rather than an overseas accounts-payable team, UPI can be the better experience. But keep the scope narrow. NPCI's July 2, 2024 UPI One World material is about foreign travellers paying merchants in India, not generic remote cross-border invoice settlement.

This means you should use UPI only when your acceptance partner confirms the customer journey and settlement outputs. Ask for a sample settlement file and a dispute escalation path, not just a screenshot of a successful QR payment.

Personal inward remittance is a separate policy lane#

If the money is genuinely family maintenance or another personal inward remittance, do not run it through the same process as export receipts. MTSS and bank personal inward-remittance channels exist for a reason. Keeping that lane separate protects your purpose-code logic, documentary expectations, and tax posture.

Domestic movement after the foreign credit#

Once the foreign money is credited or converted, your domestic movement decision becomes a separate treasury choice. NEFT gives broad availability and traceable UTRs, RTGS can fit higher-value domestic urgency, and some providers may credit the business account directly with no extra domestic leg. Pay Contractors in India With UPI Without Losing Control is useful here, but remember that outbound domestic payout operations are not the same thing as the inbound cross-border receipt.

Build the onboarding pack before the first live receipt#

Before the first payer sends money, give your team a one-page sender instruction sheet and a one-page internal checklist. Both should use the exact fields your bank expects, not a generic notion of bank details.

Use a sender instruction sheet with the real banking fields#

The HDFC inward SWIFT or wire form is a good model because it exposes the real fields: intermediary bank, beneficiary bank, ultimate beneficiary, charge handling, and remittance information plus purpose code. Even if you do not bank with HDFC, the operational lesson is the same: your sender instructions must cover correspondent data, beneficiary identity, and purpose text in one place.

For banks that support correspondent-bank routing by currency, link the sender to the official currency grid rather than emailing ad hoc instructions. ICICI publishes currency-specific correspondent details for this reason. If you skip that step, the sender bank or intermediary bank may reroute the payment, convert it unexpectedly, or ask for repairs after funds are already in flight.

| Field | Why you need it | Where teams go wrong |

|---|---|---|

| Beneficiary legal name | Lets the bank match the receiving account and supporting records | Using a trading name instead of the legal entity |

| Account number and IFSC | Needed for India-side credit or domestic follow-on movement | Sharing only a UPI ID or an account nickname |

| Bank SWIFT or BIC and correspondent details | Routes the foreign leg into the right bank chain | Omitting currency-specific correspondent information |

| Purpose code and plain-English business reason | Supports RBI or FEMA reporting and bank review | Using vague memo text that does not match the invoice |

| Invoice, contract, or shipping reference | Ties the credit to the commercial event you are settling | Leaving the reference only in email threads |

| Charge handling such as OUR, SHA, or BEN | Determines whether the net receipt will match the invoice | Closing receivables on gross amount before fees post |

| Named contact for repair queries | Shortens bank-side exception resolution | No owner for bank questions once funds are in flight |

Purpose code is an input field, not after-the-fact cleanup#

Purpose code is not a filler field. RBI's receipt purpose-code schedule maps receipts by commercial reason, and HDFC's inward-wire form says the bank may hold or return the remittance when a valid purpose code is missing.

Your control is to align three items before money moves: the invoice wording, the internal business description, and the purpose code you expect the bank to see. If those three do not read like the same transaction, expect a query.

Decide charge handling and documentary output before go-live#

Documentation rule: do not promise a customer, accountant, or finance lead a specific document name until your bank confirms the issuance pattern. ICICI says BIRC is used for export proceeds and other remittance scenarios, while FIRC is issued for some inward remittances related to FDI or FII upon request. Other providers may give FIRA, inward advice, or a different bank certificate.

Ask two direct questions before launch: who absorbs intermediary and beneficiary-bank charges, and what proof document will the bank or provider actually issue for this flow? If nobody can answer those before first receipt, the lane is not launch-ready.

- What exact post-credit document will the bank or provider issue for this flow?

- Who absorbs

OUR,SHA, orBENcharge variance if the net credit differs from the invoice? - Does the correspondent-bank path change by currency or sender region?

- Who approves the purpose code and supporting documents before the first live receipt?

Reconcile international receipts in India without firefighting#

Once you start receiving cross-border money, the failure mode is rarely no money arrived. It is money arrived, but finance cannot explain the difference between the foreign amount, the net INR credit, and the invoice that was supposedly settled. Use the same discipline described in How to Automate Payment Reconciliation End-to-End: From Invoice to Bank Statement.

Store both the foreign-leg and India-side references#

Reconciliation rule: keep the sender-bank reference and the India-side credit reference together. ICICI's wire-transfer guidance tells recipients to keep the SWIFT GPI reference or the SWIFT copy or payment reference to track incoming remittances. After credit inside India, you may also get a bank transaction reference or a UTR if there is a domestic bank leg.

You need both. The foreign reference helps during in-flight investigations. The India-side reference is what your finance team uses when matching the bank statement, the ledger, and the evidence pack.

Use one evidence pack per receipt#

- payer legal name and, where available, payer bank name

- invoice or contract reference

- foreign amount and currency

- purpose code and plain-language business reason

- sender-bank or SWIFT reference

- India-side credit reference or UTR

- FX rate, charges, and net credited amount

- bank certificate or inward advice if issued

- named owner and status of any unresolved query

If any of those items live outside the receipt record, you have not actually solved reconciliation. You have only delayed the hunt for missing context.

Use statuses that force action#

Status design matters because international receipts can be delayed, queried, partially credited, or returned. Use states your team can act on instead of a single vague paid label.

| Status | Entry rule | Next action | Close condition |

|---|---|---|---|

| In flight | Sender confirms release or bank sees the incoming message | Monitor the expected credit window using the payment reference | Credit lands or the bank requests more information |

| Bank query or pending docs | Bank asks for purpose, documents, or beneficiary clarification | Send the requested item from the named owner and record what was sent | Bank confirms processing resumed or funds are returned |

| Credited unmatched | Funds landed but the invoice or ledger match is incomplete | Check fees, FX, and payer reference before closing the item | Invoice, receipt, and ledger entry tie off cleanly |

| Returned or repaired | Funds reverse or the bank amends the route | Capture the root cause and update sender instructions | A corrected instruction set is published and the old error is closed |

Close the invoice only after bank credit and match#

Mark the invoice closed only when the receiving-bank credit is visible and matched. SWIFT, NEFT, and provider dashboards are useful for tracking, but none of them substitute for final bank credit plus internal tie-back.

Common mistakes that create preventable exceptions#

Treating NEFT as if it were the international lane#

This creates useless instructions for overseas payers and weak investigations when funds are delayed. Tell the payer to wire to your bank using the exact correspondent and purpose details, then use NEFT only for the domestic leg if it is actually needed.

Promising generic UPI acceptance to remote overseas payers#

UPI can be excellent in the right model, but not every international payer can use it and not every Indian merchant setup can settle it. Keep UPI limited to the exact merchant or corridor model your provider has activated.

Mixing personal receipts and business collections#

When family support, freelance income, export proceeds, and reimbursements all share one informal process, purpose codes drift and evidence gets weak. Separate personal inward remittances from trade receipts from day one.

Ignoring charges until the ledger no longer matches#

OUR, SHA, and BEN change whether the invoice amount equals the net credit. Decide up front who absorbs intermediary and beneficiary-bank deductions, especially on SWIFT chains, and build that rule into collections terms.

Waiting until the bank asks for missing paperwork#

A bank query is not the start of the process. It is the signal that intake failed. Purpose text, invoice references, charge handling, and expected documentary outputs should be decided before the first sender instruction goes out.

Conclusion and launch checklist#

The safest default for India business receipts is straightforward: start with a bank-led cross-border rail, make the purpose code and documentary expectations explicit, and treat UPI or NEFT as supporting rails only when the use case truly fits. If you want more background on the messaging side, see SWIFT Payments for Platform Teams: How International Wire Transfers Work.

- Choose one primary rail per use case instead of mixing business, traveller, and personal flows.

- Publish a sender instruction sheet with SWIFT or correspondent details, beneficiary fields, charge handling, and purpose code.

- Confirm what post-credit proof the bank or provider will issue before first live receipt.

- Store foreign-leg and India-side references in the same receipt record.

- Keep MTSS and other personal inward-remittance lanes out of business collections.

- Run one pilot receipt and reconcile it end to end before you widen volume.

Frequently Asked Questions

Can an overseas client pay me by NEFT?

Not as the starting cross-border instruction. NEFT is a domestic India payment system. For most overseas business payments, the payer should send a bank wire or use a bank-supported inward trade remittance workflow, and NEFT may appear only after the money is already in India.

When does UPI make sense for international receipts in India?

UPI makes sense when your acceptance model explicitly supports it, such as foreign-traveller or corridor-specific merchant acceptance. It should not be assumed to work for every remote payer abroad.

What details should I send to the payer before they transfer funds?

Send the beneficiary legal name, account number, bank name, IFSC where relevant, bank SWIFT or BIC, correspondent-bank details if required, invoice or contract reference, charge handling rule, and the purpose code or business reason the bank expects.

Is MTSS acceptable for freelance or export invoices?

No. RBI's MTSS framework is for inward personal remittances such as family maintenance or remittances favouring foreign tourists. Trade-related business receipts should use a bank-led business or export remittance flow instead.

What should be in my reconciliation pack for each receipt?

Keep the payer name, invoice reference, foreign amount and currency, purpose code, sender-bank or SWIFT reference, India-side credit reference or UTR, FX and fee details, net credited amount, and any bank certificate or inward advice issued for the transaction.

Do I need FIRC, BIRC, or another bank document?

It depends on the flow and the bank. Banks may issue different inward-remittance documents for export proceeds, FDI-related receipts, or platform-led collections. Confirm the exact document name and issuance trigger before you promise it internally or to the payer.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 6 external sources outside the trusted-domain allowlist.

- hdfc.bank.in/content/dam/hdfcbankpws/in/en/personal-banki...external

- icici.bank.in/business-banking/trade-solutions/remittancesexternal

- icici.bank.in/nri-banking/money-transfer/wire-transferexternal

- npci.org.in/uploads/UPI_ONE_WORLD_Brand_Guidelines_dd698...external

- rbi.org.in/Scripts/FAQView.aspxexternal

- rbi.org.in/Scripts/BS_ViewMasDirections.aspxexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: