Quick Answer

Yes, a foreign inward remittance certificate is the bank-issued proof many India-based freelancers and small teams need when a payment may later be used for filing, audit follow-up, or dispute evidence. The article explains that labels can vary by route, including FIRA and e-FIRC, so the practical move is to confirm the issuing AD Category I bank, request the correct document early, and reconcile key fields against invoice and remittance records before treating the payment as closed.

Treat FIRC as part of payment closeout#

Getting paid from abroad is not complete when funds appear as an INR credit. It is complete when you can produce bank-issued proof that matches your invoice and remittance details.

For freelancers and small teams in India, this is where avoidable friction can start. A payment can land on time, then stall at filing or closeout because the supporting document is missing, mislabeled, or not reconciled with the invoice record. A Foreign Inward Remittance Certificate can serve as confirmation that foreign currency was received, but naming is not uniform. One route may return FIRC, another FIRA, another eFIRC, and using only one label across cases can create confusion.

In some routes, documentation is now more digital and less paper-heavy, but that is not a universal rule. Treat each payment as its own check. Confirm issuer, label, and retrieval path before you assume what will be available for that specific receipt.

Use a simple sequence for every overseas receipt:

- Decide the required proof label before payment is due.

- Reconcile key fields on receipt day.

- Archive one complete packet before marking the payment closed.

Before filing any proof, verify the issuer bank, sender name, receipt date, foreign amount, and payment purpose. If one field conflicts with your invoice or remittance record, request correction first and keep the case open.

Keep platform screenshots, emails, and confirmations as support material. They help you trace what happened, but they do not replace a bank-issued inward-remittance document when formal proof is required.

A practical closeout rule runs through this article: do not treat payment receipt and payment closure as the same event. Receipt means money arrived. Closure means your evidence packet is complete, reconciled, and usable if a checker asks for it months later.

Start with the core terms so you do not file the wrong document#

Naming mistakes are a real failure mode. If the label in your file does not match what a checker requested, you can create avoidable back-and-forth even when the payment itself is valid.

| Term | Definition |

|---|---|

| FIRC | Official document issued by an AD Category I bank in India and used as proof of inward foreign-currency receipt |

| FIRA | Label some banks or payment routes use for similar remittance proof |

| e-FIRC | Predominant electronic form of FIRC, especially in service and goods export contexts |

| Physical FIRC | Now typically limited to narrower cases such as FDI or FII |

Term usage varies across institutions. You may see FIRC, FIRA, e-FIRC, credit advice, or other bank-specific labels for inward remittance proof. The right move is not to force one label across all payments. The right move is to capture exactly what was issued for that route.

Use the issuer label exactly, then keep one internal tag so records stay searchable:

- Save the file under the issued document title.

- Add one internal tag such as

inward remittance proof. - Capture issuer name, shown document type, and remittance date together.

- If someone asks for

FIRCspecifically, confirm whetherFIRAis accepted before submission.

This naming discipline helps during handoffs. If your accountant, finance reviewer, or tax advisor opens the folder later, they can see the exact issued label and the internal category. That makes the file easier to review without guesswork.

Final checkpoint: confirm the issuer is an AD Category I bank, then mirror the issued label in your records. For export receipts, FIRC handling may also be reviewed through RBI-linked reporting paths such as EDPMS. If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

Decide if you need FIRC for this payment#

Request proof early when there is any chance the payment will be used beyond internal bookkeeping. If a receipt may be needed for compliance, refunds, claims, or dispute evidence, request FIRC/FIRA (where available) soon after the payment lands.

Your operating pattern should shape how strict you are:

- Solo freelancer with occasional overseas payments: decide per payment and prioritize higher-risk invoices.

- Small agency with recurring cross-border receipts: request proof consistently to avoid backfilling multiple client cycles later.

The tradeoff is simple. Deferring proof requests may reduce immediate admin on low-risk receipts. It also increases backfill risk if the same payment later appears in a filing, refund, or audit follow-up. Early requests add a small amount of work now and reduce recovery work later.

Route details matter. On Wise routes, these documents are usually requested by the recipient. Wise states NOC is only available for business INR transfers (with a business sender and/or recipient when sending to India) and that it can facilitate FIRA issuance through partner banks; NOC is not the same as remittance proof. Wise also describes e-FIRC auto-generation only for eligible receipts through Wise business account details. Email delivery is described within about 3 business days after processing, while other INR transfer types are not eligible for e-FIRC.

Use this pre-close gate on each transaction:

- Could this receipt be needed for filing, refund, or audit evidence?

- Is your route eligible for the exact label you plan to submit?

- Do you know who must request it and where it will be delivered?

- If issuance is delayed, is the rest of your payment packet complete?

A useful habit is to store the answer to those four questions in the same folder as the invoice and payment confirmation. That note becomes your decision record if someone later asks why one payment has immediate proof and another is still pending.

Mandatory triggers can differ by institution and case. Confirm requirements for that payment type with your bank or provider, then store that confirmation with the transaction file.

Know who can issue it and what format you should expect#

Rely on the official record for final filing, not the first downloadable file you see. If issuing authority or official status is unclear, treat the file as provisional until that is confirmed.

Keep informational artifacts and final records separate. Portal exports, previews, and confirmations can help with traceability, but they do not replace the official document your reviewer asked for.

When multiple documents appear in one thread, keep roles distinct. A supporting file is not automatically equivalent to the specific document type requested. If a reviewer requests a specific label, submit that exact type or get written acceptance for an alternative.

If your route provides an electronic file, archive the original and the delivery trace together so origin and timing are easier to verify later.

A common friction point is mixed evidence from different channels. For example, one source may provide a quick confirmation, while the officially recognized record is confirmed later. Keep both, but mark interim files as supporting material until the official record is in place.

Use this filing check before marking a case complete:

- The file is from an official edition, not just an informational prototype or preview.

- If using FederalRegister.gov content, verify it against an official Federal Register edition.

- Save the corresponding official PDF on govinfo.gov when available.

- Treat XML or similar renditions as informational unless they are granted official status.

- Store supporting artifacts separately from the final filing copy.

If one check fails, keep status as pending and resolve that gap before final filing. This avoids rework when records look complete at first glance but rely on a non-official version. Related: The Rise of Embedded Finance: What It Means for Freelance Platforms.

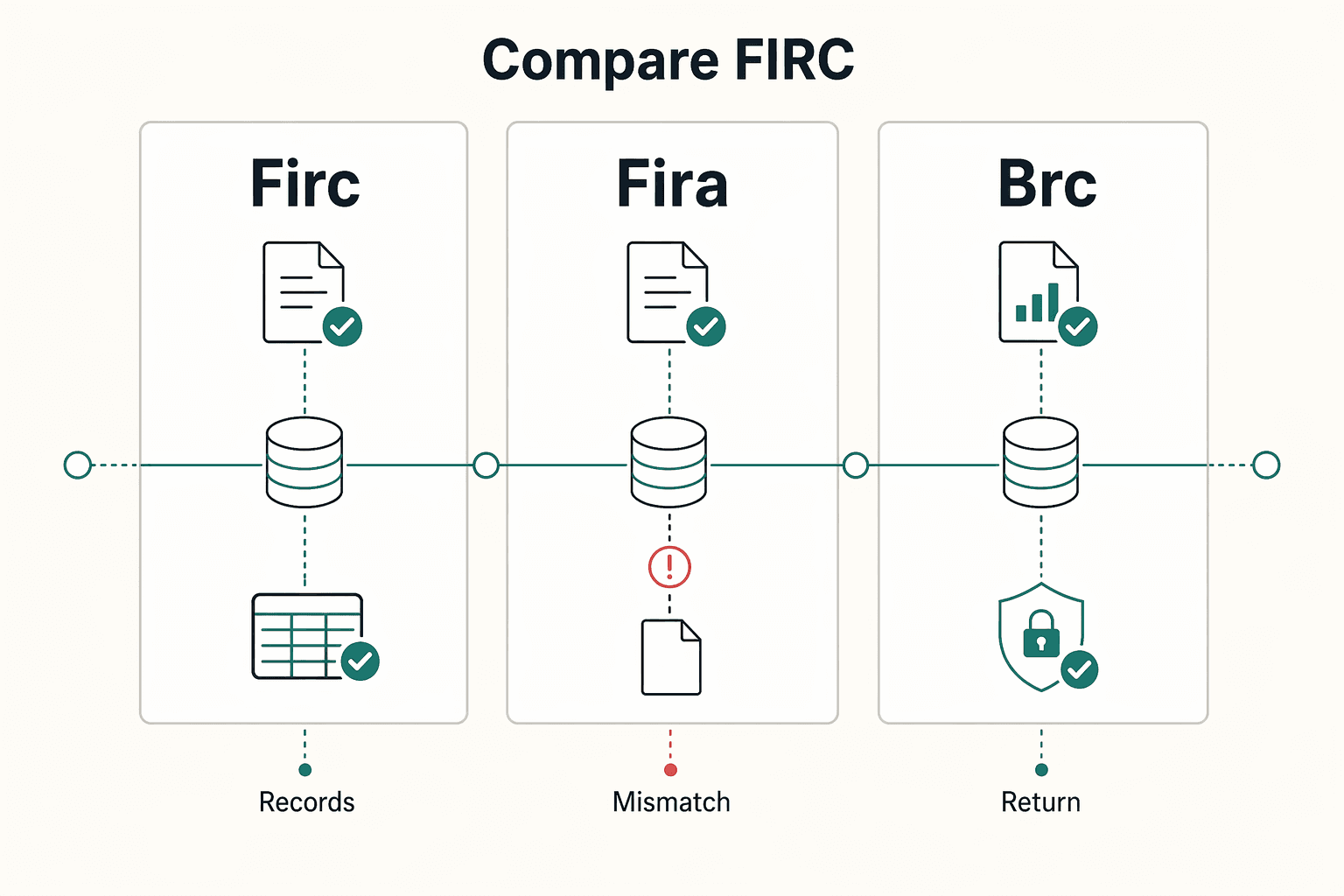

Compare FIRC, FIRA, and BRC before you submit anything#

Do not submit by close-enough logic. If a process asks for one document label, treat that label as binding until the checker confirms an alternative in writing.

| Document | Typical use context | Common confusion | Submission gate |

|---|---|---|---|

| FIRC | Often requested by name in specific checks; in current practice it is more associated with capital-account cases such as FDI than routine export-trade proof | Assumed to apply to every export receipt | Submit when explicitly requested, or secure written approval for an alternative |

| FIRA | Standard proof for export-trade payment documentation | Treated as a universal replacement for every request | Confirm the specific filing step accepts FIRA |

| BRC | Used to show export obligations were met against a shipping bill | Mistaken for generic inward-remittance proof | Match BRC to the shipping bill and the claim path |

A practical context point: some guidance describes a post-2016 shift away from physical FIRC issuance for export receipts, with export documentation increasingly linked to EDPMS records. Teams that still assume paper-first handling often create avoidable review loops.

Think in evidence chains instead of single files. FIRA (or digital IRMs, where accepted) may support GST-facing export documentation, while BRC serves a separate export-realization role tied to shipping-bill-linked obligations.

The key decision rule is to map document purpose before submission. Ask what this step is trying to verify: inward remittance receipt, export realization, or both. Then submit the file that answers that exact question.

Use this gate before submission:

- Capture the exact requested label:

FIRC,FIRA, orBRC. - Verify issuer name and reference number.

- Link it to the invoice and remittance, and to shipping-bill details where relevant.

- If substituting labels, get written acceptance first.

- Store the original file with submission acknowledgement.

One red flag deserves repetition because it causes repeated rework: a generic proof of payment upload without checking the requested label. The payment may be genuine, but a label mismatch can still block processing.

Set up your invoice so payment proof is easy later#

It helps to plan for payment proof at invoice issue, not only when retrieval is urgent.

A Foreign Inward Remittance Certificate (FIRC) is a bank-issued certificate used as proof of international payments. Treat requirement and retrieval as two separate decisions: confirm whether a FIRC is required for the payment, then confirm how your bank provides the certificate (including download/request steps).

Pre-issue checks for your own process:

- Keep invoice details consistent across your records.

- Decide where the matching proof document will be stored with that invoice.

- If the requirement is unclear, flag it and verify with the bank before relying on a fixed workflow.

Volume changes the risk profile. A single mismatch may be easy to fix manually, while repeated mismatches can create avoidable delays.

Before sending or revising the invoice, do a quick self-review as if you were retrieving proof later. If your records are clear and consistent, matching documents is usually simpler.

When edits are needed after issue, add a short change note in the payment folder so old and new versions are easier to distinguish during document requests.

Collect the right evidence pack on payment day#

Payment day is a closure checkpoint, not a clerical afterthought. Mark a receipt complete only after proof is matched and archived with the transaction record.

Build the packet while records are fresh#

Create one folder per client-payment event and collect the full packet while references are easy to trace:

| Packet item | Include |

|---|---|

| Invoice copy | Invoice ID, client name, service description, currency, and amount |

| Transfer confirmation | Remitter name, reference, and transfer date |

| Sender details | As shown in your banking records |

| Bank credit entry | Value date and INR amount |

| Proof file | FIRC or e-FIRC; keep FIRA as preliminary remittance advice when final proof is pending |

Attach files in the order above so any reviewer can follow the payment path from invoice to credited amount without searching across folders. The order helps verification move from invoice intent to remittance evidence, then to bank-issued proof.

Do not close a payment on a transfer screenshot alone. If a filing asks for FIRC, do not substitute another label without written acceptance. For issuance or correction delays, contact the issuing bank early.

Keep one bundle usable for compliance follow-ups#

Your packet should make these fields easy to verify: remittance purpose, foreign amount, conversion basis, and INR credit amount. That keeps the same file usable for GST support and reduces rework in later compliance or audit follow-up.

In many cases, records arrive electronically first. Retrieve the file promptly when available, then verify status by payment instead of assuming every route auto-generates the same document.

To keep follow-up clean, add a short reconciliation note in plain language. Capture whether amounts match, whether label matches request, and whether any correction ticket is open. This single note helps future review because it tells the next person exactly what is complete and what still needs action.

If payer identity appears in more than one variant across files, keep the exact text from each source and note the relationship rather than rewriting names. Consistent raw capture is safer than informal normalization when records are reviewed later.

Store with fixed naming and a hard close rule#

Use immutable filenames by event, for example 2026-03-15_ClientX_INV-2048_USD-1200. If a corrected file arrives, keep the original and append a version suffix such as v2.

Keep version history visible in one folder. Do not overwrite prior files in place. Overwriting hides what changed and makes it harder to explain why a correction was requested.

Do not mark a payment fully closed until:

- The proof file is present.

- Key fields match invoice and bank credit records.

- The complete packet is stored in the event folder.

For teams, assign one owner per payment packet and log handoff when ownership changes. That avoids silent gaps where one person assumes another already requested or verified the final file.

Verify the certificate before you close the client job#

Run a short verification pass before final close. For freelancers and exporters handling overseas payments, foreign-currency receipts can be a hassle, so a quick check can help avoid follow-up later.

Use two simple statuses so handoffs stay clear:

ready: document and records align.needs correction: something is missing, unclear, or inconsistent.

Check the certificate against your invoice packet and internal records. Keep the exact field checklist tied to your own process requirements.

Use a fixed order for the check so reviewers follow the same path each time and can spot mismatches early.

If status is needs correction, keep the case open in the same folder and close only after the updated document and records are reconciled.

A useful habit is to add one line on why status changed from needs correction to ready. That note gives future reviewers context on what changed.

If the same mismatch repeats across payments, it can indicate a checklist gap in intake or invoicing. You might also find this useful: The 'Second Job': Quantifying the Administrative Burden on Freelancers.

Request and retrieve documents by payment route#

Start with route mapping. A practical way to get the right file is to anchor one request thread to one payment event.

Map the route before you open support#

Capture these details before contacting support:

- route type

- payment reference

- remittance date

- payment purpose text

- foreign amount and local credit amount

- requested document label

Open one support thread per payment ID and keep every reply in that payment folder. A single-thread rule helps prevent fragmented history. If the same case is spread across multiple chats or emails, details such as the label request or reference number can get lost, and correction cycles can take longer.

Retrieve by route, then verify the returned file#

Use the provider that handled the payment route as the first support contact, and include the full payment packet in your first message.

For Wise-linked cases, keep transfer records and bank-document requests linked but separate. Include fee and rate details in your request trail; Wise says fees are shown upfront, fees vary by currency, pricing can start from 0.57%, and it uses the mid-market exchange rate.

When the returned document arrives, compare it against your route record before filing. If label, amount, or reference differs from your request, keep status as needs correction and request revision in the same thread.

Do not open a fresh thread for the same correction unless required. Keeping correction history in one place gives support and reviewers a complete timeline and reduces duplicate requests.

Use a short request format support can act on#

Use a compact request template:

- subject line with client name, invoice ID, and payment reference

- remittance date, foreign amount, and local credit amount

- payment purpose text exactly as recorded

- requested document label plus attachments: invoice, transfer confirmation, and bank credit entry

- for Wise-linked transfers, the transfer record with fee and exchange-rate details

Keep wording factual and concise. Support teams can act faster when your request reads like a clear data packet instead of a long narrative.

Before sending, verify that all identifiers in the email body match attachment filenames. That small check cuts down avoidable loops caused by typo-level mismatches.

Handle delays, mismatches, and missing certificates#

Treat unresolved proof as an active exception with owner and next action. Possible failure modes include no document generated or field mismatches against the payment record.

| Escalation path | Article guidance |

|---|---|

| Provider support | Open one ticket per payment reference with remittance date, payer name, foreign amount, INR amount, and requested document label |

| Issuing AD bank | Attach the same reference and prior replies, then request issuance or correction in the same thread |

| Compliance or tax advisor | Involve them when filing dates are close and status is still unresolved |

Keep document identity separate from payment identity. FIRC is a bank-issued inward remittance confirmation. If the returned document label does not match what was requested, keep the case open and request correction instead of relabeling internally.

Escalation can involve multiple parties, depending on where the issue sits:

- Provider support: open one ticket per payment reference with remittance date, payer name, foreign amount, INR amount, and requested document label.

- Issuing

AD bank: attach the same reference and prior replies, then request issuance or correction in the same thread. - Compliance or tax advisor: involve them when filing dates are close and status is still unresolved.

Before each escalation, re-check payer and beneficiary names, remittance date, foreign amount, INR amount, transfer source, purpose text, document label, and issuing bank identity.

If proof is delayed, continue internal reconciliation but keep external submissions gated until status is confirmed. Track each exception as pending document or pending correction, and log ticket ID, owner, and last action date.

A practical escalation discipline helps reduce stress near filing windows. At each handoff, ask one explicit question and record the answer, such as whether a document was generated or whether correction is possible. Keep the response with the payment packet.

Do not close an exception because the payment amount looks correct. Close it only when the requested document label, key fields, and issuer identity are all reconciled.

Keep compliance clean across GST, FEMA, and export reporting#

Use one evidence trail per payment across GST, FEMA, and export checks. Reviews can slow down when purpose coding or key payment descriptors differ across files, even when payment receipt is clear.

Anchor each case to the authorised bank channel and the purpose coding used for that remittance. Inward remittance handling is framed in RBI and FEMA context, so mismatched coding or inconsistent descriptors can trigger avoidable clarification.

Build one reusable packet for every payment. Then keep the same structure each time:

- invoice and contract aligned to billed service

- bank credit record with remittance reference

FIRAore-FIRAfor that payment route- payer and KYC details tied to the same payment

- internal note with purpose text, confirmer, and latest status

Treat that packet as strong support, not automatic approval for every filing step. If a process asks for additional export documentation, verify the current acceptance criteria before submission.

When wording is unclear, confirm against current instructions from the Reserve Bank of India, GST portal, and DGFT before final submission. If instructions still conflict, mark status as pending confirmation and keep the decision note with the payment file.

Review your packet standard whenever transaction patterns change. New countries, new client types, or larger ticket sizes can expose gaps that did not matter in earlier, smaller payment cycles.

The goal is consistency, not volume. One clean packet that aligns across GST, FEMA, and export reporting is more useful than a large folder of unlinked files.

Final checklist to keep every overseas payment audit-ready#

Keep closeout in the same cycle: lock route and issuer before due date, reconcile evidence on receipt day, and archive one complete packet before final closure.

Lock the route before invoice due date#

Many avoidable delays come from route or label confusion. Confirm payment path, issuing institution, and expected proof label before the invoice is due.

- Record route and expected issuer before sending final payment instructions.

- Save bank support contact and remittance reference format with the invoice file.

- Note expected proof label

FIRCorFIRAand do not treat them as automatically interchangeable. - If issuer path or label is unclear, escalate before the due date.

If your team handles multiple clients, keep this checkpoint in your invoice handoff. Route confirmation before due date is usually easier than correction after submission.

Reconcile evidence on receipt day#

When funds arrive, collect and reconcile records immediately. AD banks often request supporting documentation before clearing remittances, so delays here can create avoidable back-and-forth.

Match invoice, sender confirmation, bank credit record, and bank-issued proof in one pass. If using FIRC, verify foreign amount, INR amount, and transfer source against your payment record. If values do not align, request correction and keep the case open.

Add one short reconciliation note to each packet that records status and next action. This note keeps ownership clear and prevents duplicate follow-up.

Archive one audit packet and track exceptions#

Maintain one client-payment packet that can support GST, FEMA, and audit checks without rebuilding history. Retain records for at least 5 years, and keep an exception log until each item is closed.

Track exceptions such as:

- missing bank proof for a received remittance

- label mismatch against checker request, such as

FIRCversusFIRA - amount or transfer-source mismatch pending correction

Do not mark overseas payment complete until the packet is reconciled and archived, or the exception is actively tracked with owner, next action, and target closure date.

If you need one final gate, use this: can another reviewer open the folder and understand the case without asking you for context. If the answer is no, keep it open and finish the packet first. If your case depends on a specific country or program path, Talk to Gruv.

Frequently Asked Questions

What is a foreign inward remittance certificate in one line?

A Foreign Inward Remittance Certificate is a bank-issued document in India confirming that foreign currency was received into an Indian bank account. It is used as inward remittance proof.

What is the practical difference between FIRC, FIRA, and e-FIRC?

They are related labels, but they are not always interchangeable. Naming can vary by bank and payment route, and some flows use adjacent labels such as credit advice or BIRC/eBRC. Confirm acceptance for the specific checker before submission.

Is FIRC mandatory for freelancers in India, or only in specific cases?

Do not assume it is mandatory for every overseas receipt. Requirements can vary by transaction type and bank process. Some guidance also describes a post-2016 shift where traditional FIRC issuance is more tied to capital-account cases such as FDI.

Who issues FIRC, and can I get it online through my bank or provider?

Issuance is bank-led, historically through AD Category I banks. Banks may issue digital versions for some trade or export remittances, but availability and document labels are not uniform across institutions and processes. Confirm process and label for the exact payment route.

What details should I verify on an e-FIRC before I archive it?

Check key transaction fields first, including exchange rate context and payment purpose text. Then verify those details against your records for the same remittance. If any mismatch appears, request correction before final filing.

What should I do if I received foreign payment proof but no FIRC/FIRA?

Keep the transaction packet complete and ask the bank which label is issued for that route. Request the bank-issued file against the same remittance reference. If status remains unclear, mark it pending confirmation instead of assuming equivalence.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 3 external sources outside the trusted-domain allowlist.

- federalregister.gov/documents/2021/01/15/2020-28103/disclosure-o...trusted

- wise.com/help/articles/2655509/whats-a-foreign-inward...trusted

- karboncard.com/blog/what-is-foreign-inward-remittance-certi...external

- veem.com/library/foreign-inward-remittance-certificat...external

- xflowpay.com/firc-foreign-inward-remittance-certificateexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Choosing Embedded Finance for Freelance Platforms With an Operations-First Scorecard

Trend headlines are not a selection method. If you are evaluating embedded finance for freelancers, start with an operations-first scorecard that tests day-to-day execution before you reward product polish.

The 'Second Job': Quantifying the Administrative Burden on Freelancers

Freelancer administrative burden is the recurring non-billable work required to stay compliant, get paid, and keep records defensible. For a solopreneur, these admin tasks often look like freelance productivity drag, not visible client delivery. The goal is not perfection. It is a repeatable weekly process with a fixed time budget.