Why this matters for platform finance teams#

If you are automating payment reconciliation from invoice to bank, treat it as a control objective, not just a tool sync project. Aim for a traceable path from invoice to bank statement to General Ledger (GL), with explicit matching decisions and a clear process for failures.

Manual reconciliation is repetitive, time-consuming, and harder to sustain as volume grows. In disconnected workflows, payment data, invoices, deposits, and remittance context split across systems. Exceptions pile up, and teams drift back to manual cleanup. Even one misapplied payment can ripple into aging errors, incorrect customer statements, disputes, and a month-end close that slips.

For platform teams, the practical checkpoint is simple: can you trace one payment end to end using structured fields, then explain the final GL outcome? Durable automation depends on rules-based matching for amounts, dates, invoice numbers, and reference codes, plus an audit trail for what matched and what failed.

Success is not just more matches. It is a control chain you can defend at scale, where unresolved items stay visible and close confidence improves because posted outcomes are explainable. For a concrete example, see QuickBooks Online + Payout Platform Integration: How to Automate Contractor Payment Reconciliation.

What to prepare before you automate#

Before you automate, set ownership and data policy first. Reconciliation spans gateways, banks, billing platforms, ERP, and accounting ledgers, and complexity often comes from multi-source data, settlement delays, fees, missing references, and ERP posting logic. Without that foundation, automation may work briefly, then exceptions accumulate and the team falls back to manual cleanup.

Inventory every source and assign an owner#

Start with a full source inventory and a named owner for each source. At minimum, include your payment gateway or PSP, bank feed, ERP, GL, and any separate billing or settlement source.

For each source, define accountability for data quality and exception handling. You should be able to trace a payment across collection, bank movement, and accounting records without cross-team guesswork.

Standardize only the identifiers you can trust#

Standardize match identifiers only where fields are present and reliable across systems. Focus on identifiers and remittance context that consistently travel across your channels and records.

The goal is not to force a universal schema. It is to recognize the same payment consistently across gateways, banks, billing records, and accounting entries. If a field is sourced inconsistently, do not make it a primary match key.

Set system-of-record policy before matching#

Define system-of-record policy before you build matching logic. Payment reconciliation and bank reconciliation are related controls, but they serve different decisions.

Document how each status is owned and how exceptions or overrides are handled. Payment-matched activity should not automatically be treated as bank-confirmed cash unless your policy explicitly allows it. That separation helps reporting, forecasting, and treasury rely on reconciled cash balances.

Define audit evidence before go live#

Set evidence policy before go live, alongside implementation planning, data preparation, and team training. At minimum, keep decision history clear enough to review source records, match outcomes, and manual exceptions without rebuilding evidence ad hoc.

That discipline helps keep automation resilient as exception volume rises. For a step-by-step walkthrough, see Account Reconciliation for Payment Platforms: How to Automate the Match Between Payouts and GL Entries.

Map the invoice to bank data chain#

Write the full chain before you automate, because one payment signal is not the same as end-to-end reconciliation. Keep invoice status, payment status, and bank-confirmed status distinct so reporting reflects cash movement, not just early events.

Document the full invoice-to-bank sequence#

Document the sequence your team must reconcile from start to finish: Invoice generated, payment captured, payment record received, then Bank statement line available for matching. For each handoff, record the system of record and the identifier that must carry through, typically invoice ID, payer reference, and amount.

Your checkpoint is simple: pick a recent payment and confirm one reviewer can trace it from invoice to bank statement line with no hidden context.

Define status meaning by record type#

Define status meaning by record type, not as one blanket status for the whole flow. Use your own labels, but document what each label means for the invoice record, payment record, and bank statement match so teams do not interpret the same word differently. That keeps open invoice and reconciliation reporting stable when events arrive at different times.

Separate early payment signals from bank confirmation#

Treat early payment data as useful, but not automatically final for bank reconciliation. Invoicing and payment execution are often separate systems, so a payment update can arrive before bank confirmation. Set an explicit rule for when payment reconciliation can advance and when bank reconciliation is actually complete.

Map failure points before they hit production#

Map failure points up front, especially where matching depends on payer-entered reference data and amount. In bank-driven flows, weak or incorrect references can force manual matching.

Also define how partial payments are handled so they do not turn into ad hoc adjustments. For exceptions, require a small evidence set, including the payment record, invoice record, and bank statement line when available, before final posting decisions.

You might also find this useful: Invoice Matching Explained: How Platforms Automate 2-Way and 3-Way Matching to Prevent Overpayment.

Choose your reconciliation architecture#

Choose the architecture based on where reconciliation truth can be explained and defended, not just where matching is fastest to turn on. A provider-native setup can be a workable starting point when activity is concentrated and evidence remains complete in one place. As records spread across sources, a broader reconciliation layer often becomes more practical for traceability. Treat that as a heuristic, not a rule.

Score source complexity before choosing tooling#

Score source complexity first. If payment events, bank activity, and posting context stay mostly inside one operational path, native matching can help you automate quickly with less implementation overhead.

If reconciliation already spans multiple providers, entities, or banking paths, native tooling may still help with part of the flow, but you should verify whether it still provides complete control and visibility end to end. Use a practical checkpoint: can your design support direct bank feeds, broad PSP reconciliation, and full audit trail visibility, including higher account count operations such as 20+ accounts?

Verification test: sample recent payments and confirm one reviewer can trace each item from invoice to payment record to bank statement line. The reviewer should reach the same conclusion each time and should not need off-tool context.

Compare architectures against failure modes#

Compare options against failure modes and control needs, not just implementation speed.

| Decision area | Provider-native matching | Orchestrated matching in your own service |

|---|---|---|

| Implementation scope | Can be sufficient when one tool captures most payment and bank context. | Useful when reconciliation requires combining provider, bank, and ERP records. |

| Audit trail transparency | Depends on whether a full trace is visible and exportable across sources. | Centralizes traceability when records are spread across systems. |

| Matching logic quality | Basic date-and-amount matching can miss edge cases. | Configurable matching rules can better handle edge cases. |

| Partial payment handling | Can work, but date-and-amount-only logic is fragile. | Better fit when allocations span multiple receipts or invoices. |

| Batched payment handling | Harder when one deposit reflects bundled PSP settlements. | Better when you need to unpack bundles and preserve invoice-level links. |

| Cleared vs pending visibility | Can become fragmented if teams still stitch multiple tools manually. | Can provide one operating view when designed to consolidate status. |

A common trap is choosing native matching for speed, then assuming it closes bank reconciliation end to end. Bank confirmation is still the external check, and basic date-and-amount matching alone misses edge cases such as partial payments and PSP bundles.

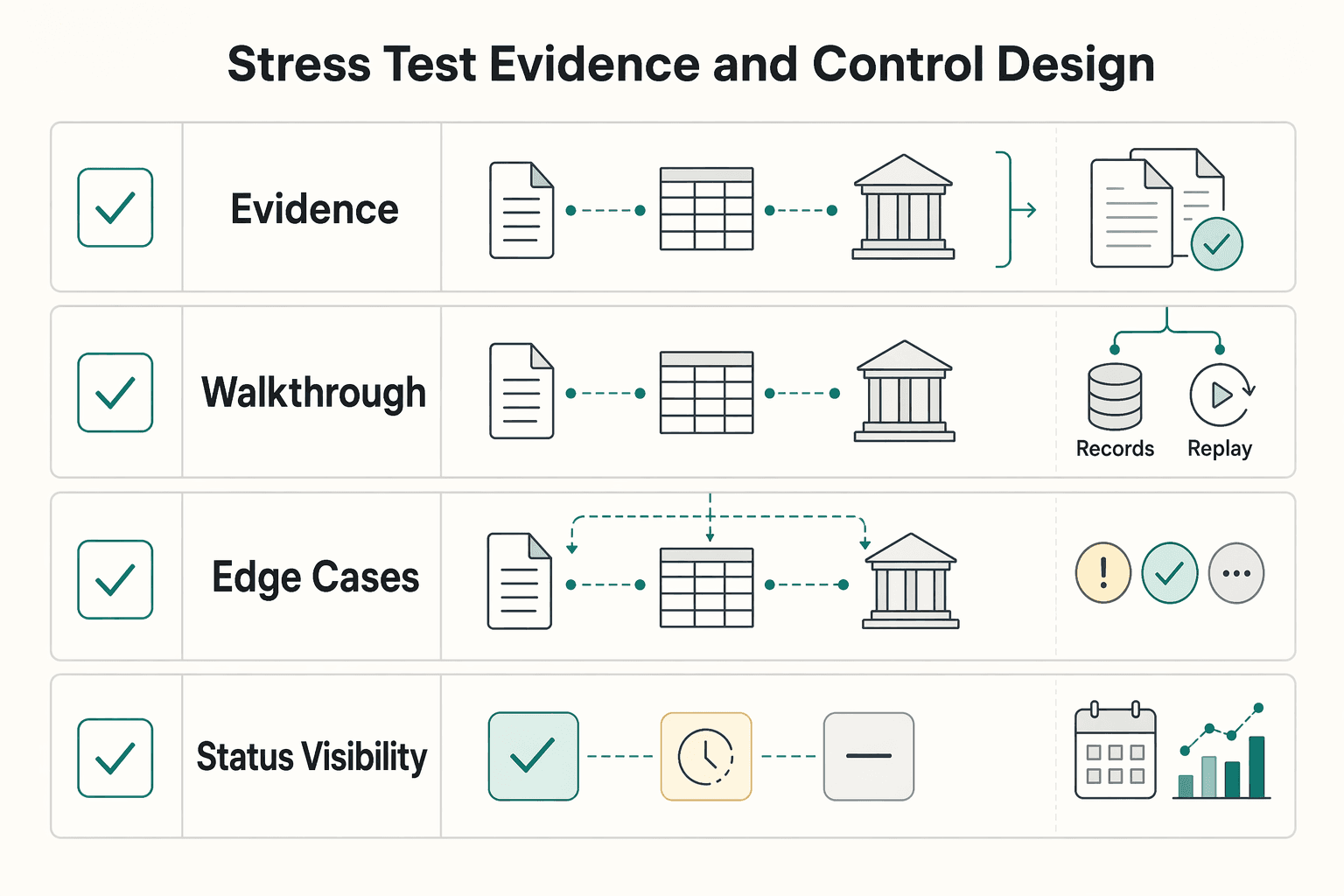

Stress test evidence and control design#

Stress test evidence and controls before you commit. Reconciliation should live with finance records, not in disconnected tools, so define where cleared versus pending status is finalized and reviewed.

| Check | What to confirm |

|---|---|

| Export evidence | Source events, bank links, match decisions, overrides, and rule or config history can be exported |

| Walkthrough | An audit-style walkthrough is traceable end to end from records |

| Edge cases | One partial payment and one batched payment are explainable from system records alone |

| Status visibility | Cleared versus pending visibility appears in one operating view |

Decision test: stay native if it still produces a complete, reviewable evidence trail. If complete evidence only appears after you combine provider, bank, and ERP data yourself, orchestrate deliberately. If teams still have to combine multiple tools manually, the architecture is still fragmented. Before you lock the architecture, review Gruv Docs to align webhook events, idempotent retries, and reconciliation status mapping.

Define matching logic before you scale volume#

Define matching rules and exception paths before volume rises. This is a control point for keeping reconciliation explainable as activity grows, especially when manual intervention scales linearly with transaction volume and small discrepancies can compound before close.

Set matching precedence in writing#

Use one explicit rule order and require each match to show the rule path used. The exact order is up to your data and tooling, but it should be documented, repeatable, and auditable rather than improvised case by case.

Avoid treating any single precedence pattern as universal. Whatever order you choose, make the decision trail visible in system records so a reviewer can explain the result without relying on memory.

Predefine edge-case behavior#

Predefine handling for missing remittance data and other recurring exceptions. Missing remittance details are a known failure point, so these paths need written rules before you scale.

| Scenario | Define in advance | Send to review when |

|---|---|---|

| Missing remittance data | Which matching rules can suggest candidates and what record evidence is required. | The target cannot be identified clearly from records. |

| Ambiguous or conflicting matches | How exceptions are documented and resolved consistently. | Multiple valid targets remain or rule outcomes conflict. |

Tie matching checks to inputs and downstream use#

Document which matching checks are required for each workflow, so reviewers reach the same conclusion on similar cases.

Keep this tied to reconciliation inputs and downstream use. Bank feeds and ERP or GL are direct inputs to reconciliation, and reconciled cash balances feed reporting, forecasting, and treasury.

Add tie-breakers and review gates#

Set deterministic tie-breakers for ambiguous candidates and define a clear boundary between auto match, suggested match, and review-required outcomes. If no rule produces one explainable result, route the item to exception review instead of auto-posting.

This applies whether your tooling is rule-based, AI-driven, or mixed. Review near-miss patterns regularly. Repeated ambiguity often means the rule set or upstream data needs tightening.

If you want a deeper dive, read Payment Reconciliation for Freelancers: How to Match Invoices to Bank Deposits.

Design exception handling with named owners and SLAs#

Exception handling should be a defined workflow step with clear ownership, aging visibility, and audit-ready records, so unresolved items do not drift through close.

Classify exceptions by root cause and owner#

Classify exceptions by why the match failed, then assign each class to one accountable owner. This keeps different issue types from competing in one undifferentiated queue. Each exception record should show class, owner, age, and next action so routing stays consistent as volume grows.

Escalate based on close risk and cutoffs#

Escalate based on close impact, not queue age alone. Payment flows run across schedules, dependencies, file arrivals, and cutoff times, so late files or delayed approvals should trigger exception alerts before close pressure builds. Keep unresolved exceptions visible until the underlying break is cleared.

Set the evidence needed to close an exception#

Resolve exceptions with enough evidence for an independent reviewer to follow the decision path. Your record should connect the triggering reconciliation data, the analyst decision, and the resulting audit log entry. Avoid vague notes that do not explain why the exception was resolved.

Document recovery paths for unmatched deposits and settlement discrepancies#

Unmatched deposits and other settlement discrepancies need explicit recovery paths so ownership and next actions stay clear. Document how these cases move through exception handling, who reviews them, and what status change closes the loop. This prevents a matched-looking ledger state from masking an unresolved break.

Need the full breakdown? Read How Platforms Automate 2-Way and 3-Way Invoice Verification.

Post to the ledger with controls that survive audit#

Only post to the General ledger (GL) from reconciled states. Keep provisional events in operational statuses until your Payment reconciliation and Bank reconciliation states support accounting finality.

Keep provisional events out of the GL#

Treat capture events, settlement notices, and early PSP updates as operational signals, not journal triggers. If cash is not yet confirmed by reconciliation logic, keep the item in a pending or matched-not-posted state instead of posting and unwinding later.

Post from reconciled state, not first arrival. This matters whenever reconciliation is still catching up across systems. For a single source of truth, keep posting connected to your central accounting software or ERP, not side spreadsheets or dashboard exports.

Use a period checkpoint. Compare initial and final balances between bank and accounting records. If balances tie only when provisional items are included, the posting gate is too loose.

Prove retry-safe posting before retries go live#

Retries should not create duplicate Accounts receivable (AR) impact. Do not assume journal posting is retry safe. Test it under replay conditions.

Use a stable posting control across retries and verify how your ERP handles duplicate attempts before go-live.

Control evidence should show what rule triggered, the matching criteria, and whether undo actions were used, with an audit trail that includes method, timestamp, and user. If matcher and poster cannot confirm prior posting status, treat the item as review-required.

Capture reversal paths with source links#

Corrections and undo actions need structured reversals, not free-text notes. Where your system supports it, record counter entries that link back to the original Invoice, relevant Bank statement line, and the rule or decision behind the first post.

Keep evidence together: triggering reconciliation record, matching criteria, journal identifiers, and undo action. When available, export reconciliation artifacts such as Excel or PDF for audit documentation. Treat entries posted outside the primary automation flow as review-required suggestions until validated.

Derive wallet and balance views from journals#

If teams rely on wallet or balance screens for accounting decisions, treat journal-derived balances as the reference and PSP snapshots as operational context.

Run regular comparisons between displayed balances and journal-derived balances for the same period and entity. When they diverge, check data quality breaks first, including inconsistent bank export fields or narration values that can disrupt lookup logic and push work back to manual matching.

Journal-derived views are stronger for audit because they tie to what actually posted to the GL.

Integrate systems in the right order#

A practical sequence is to integrate reconciliation inputs before downstream consumers: stabilize intake and matching first, then connect accounting, then feed reporting. Teams can regress to manual cleanup when exceptions pile up on top of weak joins across payment, invoice, deposit, and remittance data.

Connect source inputs before downstream views#

Start with the records that drive Payment reconciliation and Bank reconciliation: bank feeds, PSP sources, and ERP/GL data. Confirm connector coverage for the paths you actually run before moving downstream. Include direct bank connectivity plus any relevant file or channel variants in scope, for example SFTP and statement formats such as CSV, CAMT, and MT940.

Use a trace test. One sample payment should be followable from source event to Bank statement line without manual patching.

Validate accounting mappings before sync goes live#

Once source intake is stable, connect the accounting target and test mappings and status transitions before enabling automation. Verify that reconciliation states map cleanly to accounting states in a test flow. The failure mode to avoid is drift between operations and accounting that pushes teams back into manual cleanup.

Use extracted document data as input, not proof#

Remittance context is often scattered across emails and attachments. Treat extracted document details as input, then verify them against core reconciliation records before acting on them. Keep matching decisions anchored to reconciled payment, invoice, deposit, and bank record context.

Set control consistency at launch#

Apply launch controls so handling stays consistent across entities and regions. This matters because reconciled cash balances are consumed downstream by reporting, forecasting, and treasury. Keep a compact launch checklist: connector inventory, supported input formats, and mapping signoff.

Pilot the process before full rollout#

Run a controlled pilot before expanding reconciliation automation across customers or channels. Keep it to 4 to 8 weeks and include at least one month-end cycle so you can validate matching and exception handling under real close conditions.

| Pilot element | Guidance |

|---|---|

| Duration | 4 to 8 weeks |

| Close coverage | At least one month-end cycle |

| Goals | 2 to 3 measurable goals |

| Report output | A clear report separates matched items from items needing review |

| Scenario testing | Include incomplete or unclean source data, transactions that do not auto-match, and exceptions that require human review during close |

Choose a cohort that is narrow, real, and predictable#

Set a pilot scope that is small enough to control but realistic enough to learn from. A practical starting point is one transaction channel, or another small cohort that still reflects real workflow behavior.

Keep your accounting or ERP record as the single source of truth while software handles matching and your team handles exceptions. For a sample set, require a clear report that separates matched items from items needing review.

Define pass criteria before the first live run#

Set 2 to 3 measurable goals before launch. At this stage, center pass criteria on whether matching improves, exceptions are manageable, and internal records stay aligned with bank statements.

Do not rely on auto match rate alone. Require a match report that clearly separates matched items from items needing attention. If an item cannot be tied cleanly to the bank-side record, flag it for investigation.

Force edge cases before production volume does#

A pilot has to test failure paths, not just happy-path matching. Include scenario tests for:

- incomplete or unclean source data

- transactions that do not auto-match

- exceptions that require human review during close

For each case, confirm it is surfaced as needing attention and routed through an explicit handling path. Poor or incomplete reconciliations are audit-risk signals, so unresolved items should not be treated as complete.

If the pilot handles both normal flow and forced failures, expand scope. If not, keep the cohort narrow and fix breakpoints before adding entities, channels, or customers.

Related reading: Invoice Verification for Platforms: How to Validate Contractor Bills Before Releasing Payment.

Common failure modes and how to recover#

If your pilot exposed breakpoints, use them. The biggest risk is false certainty: items look matched, queues look active, and month end still shows incomplete proof. Treat the four issues below as guardrails before you expand automation.

| Failure mode | Recovery focus |

|---|---|

| Questionable invoice links | Prioritize exact reference matches and send weaker or fuzzy rules to review unless another source-verified field also agrees |

| Generic exception queue | Split items by root cause and owner, and keep data issues, commercial disputes, and timing gaps separate |

| Settlement treated as cash proof | Hold items provisional until the bank statement line confirms movement |

| OCR used as final proof | Use OCR for extraction, then verify against source records before invoice linkage or downstream posting |

Tighten match approval before GL posting#

High auto match is not a win if it links the wrong Invoice. Prioritize exact reference matches before anything posts to the General ledger (GL).

Use stronger rules first, and treat weaker or fuzzy rules as review candidates unless another source-verified field also agrees. That second check can come from identifiers already present in your ERP or PSP record.

Measure quality with reviewed samples, not match rate alone. If a rule set is creating questionable links, pause posting for those cases and return them to review.

Split the exception queue by root cause and owner#

When exceptions pile up before close, one generic Exception queue can hide what is actually wrong. Classify items by root cause and assign ownership at that level.

Keep data issues, commercial disputes, and timing gaps separate so teams can act on the right problem. Timing items should stay visible, but they should not be mixed with broken data cases.

Your check is operational clarity: open count by class, current owner, and which items block Bank reconciliation or invoice closure. If you cannot answer those quickly, the queue is still too generic.

Hold provisional states until the bank line confirms cash#

Settlement status is not final proof of cash. Keep items provisional until the Bank statement line confirms movement. Timing differences are expected in reconciliation, and settlement speed can vary by rail. Some card flows may settle in 2-3 days, while other rails can be faster or slower.

Use a strict checkpoint: any non-zero unexplained difference, even $1, means proof is incomplete. Do not clear from expected cash alone when bank-side confirmation is missing.

Limit OCR to extraction and verify against source records#

Use OCR as an input signal, not as final linkage proof. OCR-heavy processing can introduce delays and extraction errors, so low-confidence cases still need manual review.

Verify extracted invoice references against source records before invoice linkage or downstream posting. If extraction is ambiguous or conflicts with payment evidence, route to review instead of auto posting.

Keep traceability complete enough to reconstruct decisions, including override handling. If you cannot reconstruct why one payment linked to one invoice, the match is not audit proof.

We covered this in detail in How to Build a Payment Reconciliation Dashboard for Your Subscription Platform.

Measure whether automation is actually working#

Automation is working when internal records and external statements agree on amounts, mismatches are investigated rather than auto-closed, and key impact metrics like speed and cost savings improve without masking risk.

Build a compact scorecard from source records#

Build a scorecard your team can validate from underlying evidence, not only from a matcher dashboard.

| Metric | What it tells you | Verify with |

|---|---|---|

| Match consistency | How much volume is matched with equal amounts | Matched items where internal and external records show equal amounts |

| Open discrepancies | Whether unresolved mismatches are building into close | Items where records do not match, grouped by age |

| Reconciliation speed | Whether automation is reducing cycle time | Time to complete reconciliation or close-related steps |

| Cost impact | Whether automation is lowering reconciliation effort | Cost-to-reconcile trend over time |

Keep the evidence standard strict. Each transaction should have at least two forms of documentation, typically an internal record such as a journal entry and an external statement from a bank or card provider. If amounts do not match, keep the item open for investigation.

Add control metrics that reveal hidden breakage#

Add control checks that show whether quality is improving, including unresolved discrepancies and the types of issues reconciliation is surfacing, such as errors, potential fraud, and unpaid invoices.

Spot check discrepant items and review the evidence chain: the internal record and the external statement. If that chain is hard to reconstruct, control quality is weaker than match-rate reporting suggests.

Report by decision type and recalibrate as payment mix changes#

Report findings in a way decision-makers can act on: unresolved differences, root cause, owner, next action, and blockers to posting or close completion. Treat any real-time-close claim as valid only when bank-side and ledger evidence align.

As payment-channel variety expands, reconciliation becomes more complicated and labor-intensive, so revisit exception categories and controls so new failure patterns do not stay hidden.

Use this copy and paste checklist to launch cleanly#

Lock launch decisions before go live. Prioritize identifiers, exception ownership, and close evidence early.

Confirm sources, owners, and identifiers#

Start by standardizing scope and accountability across PSP, bank feed or bank statement import, ERP, and GL. Assign one owner and one backup reviewer per source, and document the identifiers that must flow across records, including invoice ID, payer reference, settlement reference, and fields in Remittance data.

Use traceability as the checkpoint. Sample a payment and confirm you can follow it across PSP record, bank line, ERP invoice, and GL outcome without outside reconstruction. If references differ and no mapping rule exists, stop and fix that first, because cross-provider formats, identifiers, and timing vary.

Approve edge-case match rules#

Define handling for Partial payment, Batched payment, Overpayment, and missing Remittance data before live volume starts. The goal is consistent control, not perfect prediction.

For each case, set three outcomes: auto match, hold for more evidence, or route to review. For batched deposits, require a clean link to underlying payment records or proof of settlement before closing AR items. When remittance is missing, treat it as a control gap until evidence is complete.

Deploy exception classes and evidence packs#

Treat unmatched items as control risk, not harmless backlog. They can hide duplicates, unexpected fees, or fraud, so each exception class needs a clear owner and review expectation.

At minimum, keep one Audit trail record with:

- source payment event or PSP record

- related bank statement line

- invoice snapshot or AR record

- analyst decision and adjustment note

- adjustment approver and supporting paperwork

This gives you an auditable source of truth. The practical check is simple: a reviewer should be able to see why an item is matched, unmatched, or adjusted without rebuilding context manually.

Complete the pilot before you expand#

Expand only after a narrow pilot proves control quality, not just match volume. Pass criteria should include no unexplained gap between payment reconciliation and bank reconciliation, plus transaction-level status output for every line.

Test failure scenarios deliberately: missing remittance data, delayed bank arrival, duplicate payment risk, and overpayment cases should route to review instead of closing silently. High auto match rates with weak evidence still create close risk.

Publish a weekly scorecard until close is stable#

Run a compact scorecard weekly until close performance is stable. Track match coverage, unresolved exception aging, reopen rate, manual adjustments, and close blockers tied to AR and GL.

Keep the reconciliation report operational: each line should be clearly matched, unmatched, or adjusted, and adjusted lines should show approver plus supporting paperwork. If unmatched or adjusted volume keeps rising, pause expansion and fix root causes before scaling further.

For cash-speed metrics after reconciliation controls are in place, use Track Payment Conversion Rates From Invoice to Settled Cash.

Once your launch checklist is approved, talk with Gruv to confirm module fit, controls, and rollout sequencing for your operating model.

Frequently Asked Questions

What does invoice-to-bank automation include beyond simple bank feed syncing?

A bank feed is only one input. Reliable automation also imports statements, matches imported transactions to ledger entries, and posts residual transactions that are not yet in the ledger. In practice, many teams need a connection layer between payment collection data and accounting records, not just synced statement lines.

How should we handle partial and batched payments without creating false matches?

Handle these cases conservatively. When a bank transaction cannot be mapped clearly to underlying payments, treat it as an exception and send it to manual review instead of forcing an automatic match.

What still needs human review after automation is live?

Human review is still needed for exceptions the system cannot explain cleanly, especially fees, deductions, withholdings, and FX movements. If exceptions start accumulating, that is a sign the process can drift back toward manual cleanup.

Which integrations are mandatory first for a reliable launch?

There is no universal first integration order. Reliable bank reconciliation depends on both external bank data and internal ERP or GL records, because matching requires both sides of the transaction. If payments run through a separate collection system, include that data path so reconciliation keeps operational context.

Can software alone guarantee an accurate month-end close?

No. Automation can reduce manual effort by matching more transactions and suggesting posting accounts, but complex differences can still require manual investigation.

How do we prove reconciliation quality to auditors and leadership?

Use sampled items that trace bank statement activity to ledger matches and residual postings. Pair that with operating metrics like speed and cost impact so leadership can assess practical results as well as control quality.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 6 external sources outside the trusted-domain allowlist.

- mgaleg.maryland.gov/Pubs/BudgetFiscal/2026rs-budget-docs-operati...trusted

- psc.ky.gov/pscecf/2017-00179/slsharp%40aep.com/08282017...trusted

- alternativepayments.io/resources/why-manual-matching-is-a-2025-relicexternal

- cashmanagement.org/bank-reconciliation/the-5-most-common-bank-r...external

- ccmonet.ai/blog/how-do-smes-run-a-pilot-test-for-ai-acc...external

- chaserhq.com/blog/payment-reconciliation-automationexternal

- emagia.com/blog/automatically-match-payments-to-invoicesexternal

- embat.io/account-reconciliation-automation/bank-recon...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: