Quick Answer

Choose an invoice-first transfer workflow to pay indian development agency partners from the US: lock terms before collecting bank details, then run one controlled first transfer with a saved quote, approval record, transfer confirmation, and recipient confirmation. Use card rails only for urgent one-offs, not recurring invoices. Recheck live pricing and credited amounts each cycle, and document the FIRC request path in writing so documentation disputes do not delay the next payment.

Pay an Indian Development Agency Without Cashflow Surprises#

This guide is about paying a software agency in India from the United States without drifting into the wrong topic. It covers invoice-based vendor payments for service work, not salary or stock pages, investment analysis, or unrelated U.S. programs that happen to include the word "Indian."

- Confirm relevance first

Confirm the page topic before you trust it. A .gov domain tells you a page is official, but it does not tell you it is relevant to this payment workflow. In the research set, results included Bureau of Indian Affairs "Fee to Trust Land Acquisitions," Defense "Indian Incentive Program FAQs," and a Senate report page dated July 15, 2025. All of them are reminders to verify topic metadata before you make decisions.

- Center the decisions that affect cash flow

Keep the scope practical: define your payment method, set clear payment terms, and run vendor payments in a way that makes month-end review straightforward. If you cannot explain approval, confirmation, and invoice matching before sending money, stop and fix that process first.

- Treat documentation as part of the payment

Missing documentation can stop processing. One source warning is explicit: incomplete requests are not processed until required documentation is received. Another warns of long waits between submission and payment. Different context, same lesson: define required records and follow-up ownership before the first transfer.

How to Choose the Right Payment Method#

Pick the method you can run cleanly every month, not the one that only looks fastest on the first transfer. This part focuses on invoice-driven international payments between small teams and agencies, not payroll-heavy employer setups or public-market research like P/E ratio or market capitalization.

If you need to pay an overseas agency on a recurring cadence, use these four screens:

- Match the method to the engagement

Businesses have more payment choices than ever, and that can make selection harder, not easier. For recurring, invoice-based work, start with operational fit: can you reliably connect invoice, approval, and payment confirmation every cycle?

- Price the full landed cost, not just the send fee

In cross-border payments, speed and cost both affect cash flow. Compare the whole picture for each option: how much you send, what the recipient is expected to receive, and how clearly the method shows what happened so month-end review stays straightforward.

- Check restrictions before a deadline exposes them

Card-based routes can fail on limits, and those limits vary by bank and by card category. If you are considering a card or debit-card path, confirm limits and setup status before an urgent invoice is due.

- Use a practical comparison lens

Compare payment modes by features, restrictions, and benefits. For recurring vendor invoices, favor methods that are easy to repeat, easy to review, and easy to pull records from later.

For recurring cross-border invoice work, use a simple rule: prioritize predictable record matching and repeatable documentation, then weigh speed. With that in mind, here is how the main options stack up.

Comparison Table for the Best Payment Options#

For recurring U.S.-to-India agency invoices, one practical starting point is a transfer-first route when consistency and reviewability are priorities. Use alternatives when your approval model, vendor mix, or urgency makes that tradeoff worth it.

| Illustrative fit rank (not universal) | Option | Best for | Fee transparency | FX control for foreign currency transactions | Proof pack quality (invoice + confirmation + payout record) | Cross-border reliability notes | One-off or recurring vendor payments | Approval flow needs | Month-end matching effort | Avoid when |

|---|---|---|---|---|---|---|---|---|---|---|

| 1 | Specialist transfer provider such as Wise | Recurring agency invoices and milestones | Can be clearer when pricing and conversion details are shown before release; still check for hidden markups | Can be stronger when quoted amounts are visible up front | Can be strong when you consistently store invoice, transfer confirmation, and payout record | Cross-border exceptions can still happen, including technical and interoperability issues | Both, especially recurring | Light to medium | Low to medium | Policy requires bank-native initiation and controls |

| 2 | Traditional bank wire | Higher-value payments where bank controls are required | Can be less transparent because total cost can depend on fee layers and markup treatment | Can be less flexible unless your bank provides clear quote options | Bank traceability can help, but you still need to retain invoice and beneficiary-side confirmation | Cross-border exceptions may involve multiple institutions and handoffs | Both, usually planned recurring | Medium to high | Medium | You need lightweight self-serve tracking for frequent small payments |

| 3 | Platform-mediated payouts | Multi-vendor or multi-country payout operations | Varies by platform and program | Varies; confirm conversion visibility in exports | Can be strong when approval history and records are centralized; verify export fields first | Reliability depends on platform support scope and onboarding state | Best for recurring, multi-vendor flows | Medium to high | Low once configured | You have one India agency and low volume, so setup overhead dominates |

| 4 | Card checkout or merchant rails | Urgent, smaller invoices when transfer rails are not ready | Processor fee is often visible, but landed cost can still be high | Can be limited for invoice-style cross-border settlement workflows | Payment confirmation is usually available; confirm export fields meet your audit needs | Exceptions and disputes can require additional handling | Mostly one-off or occasional | Low | Medium to high | Work is recurring or invoice size makes card cost hard to justify |

How to read this table#

- Specialist transfer provider such as Wise

A practical starting point when you want repeatability and clear pre-send visibility. Validate it with one live payment and confirm you can quickly retrieve the invoice, payment confirmation, payout record, and close evidence.

- Traditional bank wire

A fit when internal banking controls matter most. A common downside is cost opacity, so log the sent amount, quoted FX terms if provided, and the amount the agency confirms it received.

- Platform-mediated payouts

Strongest when India payouts are part of a broader vendor-payment program. Confirm support scope, approval flow, and export fields before rollout.

- Card checkout or merchant rails

A practical exception path for urgent small invoices, not a default for recurring vendor bills. Public processor table examples such as 2.9% + $0.30 for online and 2.6% + $0.15 for swipe are a reminder that visible pricing can still be expensive in practice.

Do not confuse domestic scale with cross-border fit. India's digital-payments market reached about USD 2.52 trillion in February 2024, and UPI exceeded 15 billion transactions per month in November 2024. Cross-border flows can still run into technical glitches, interoperability gaps, and scaling limits. For this decision, choose the method you can document, approve, and tie back reliably every cycle.

Option 1 Wise Transfer for Invoice-Driven Agency Work#

For U.S. teams paying an India agency against clear invoices and milestones, Wise can be a strong first option when approval and tracking consistency matter. The main advantage is visibility before release: fee, exchange-rate basis, send amount, and recipient amount are shown upfront. That makes approval cleaner and can reduce surprises.

- Best fit

Use this when payments follow a monthly retainer, milestone invoices, or both, and each invoice is specific enough to approve directly. If volume grows, Wise says discounts start at 25,000 USD in monthly sends, whether that is one transfer or multiple transfers.

- What you gain

The real benefit is the cleaner record each cycle, not just the transfer itself. Wise says fees vary by currency and can start from 0.57%, so check each live quote and save those quote details with the invoice for month-end review.

- Where tradeoffs show up

Upfront pricing is not the same as fixed pricing. Wise has said some currencies and payment methods may see small fee increases after pricing reviews, so do not copy last month's assumptions without checking the fee calculator and live quote again.

- What to verify on your first recurring payment

Run the first transfer as a controlled test. Save the pre-send quote, transfer confirmation, and payout record with the invoice, then confirm with the agency what amount was credited and which reference they received.

- Common failure modes

Process gaps can still cause delays, so verify beneficiary details and invoice references before sending. If the agency may request FIRC, align early on what documentation is needed and who obtains any bank-side document instead of assuming issuance is guaranteed.

Choose this route when your priority is a repeatable, low-friction paper trail for recurring vendor payments. Recheck the live quote each cycle, confirm recipient amount before release, and match payment references to invoices before close.

For a step-by-step walkthrough, see The Best Way for a German Agency to Pay a US-Based Freelancer.

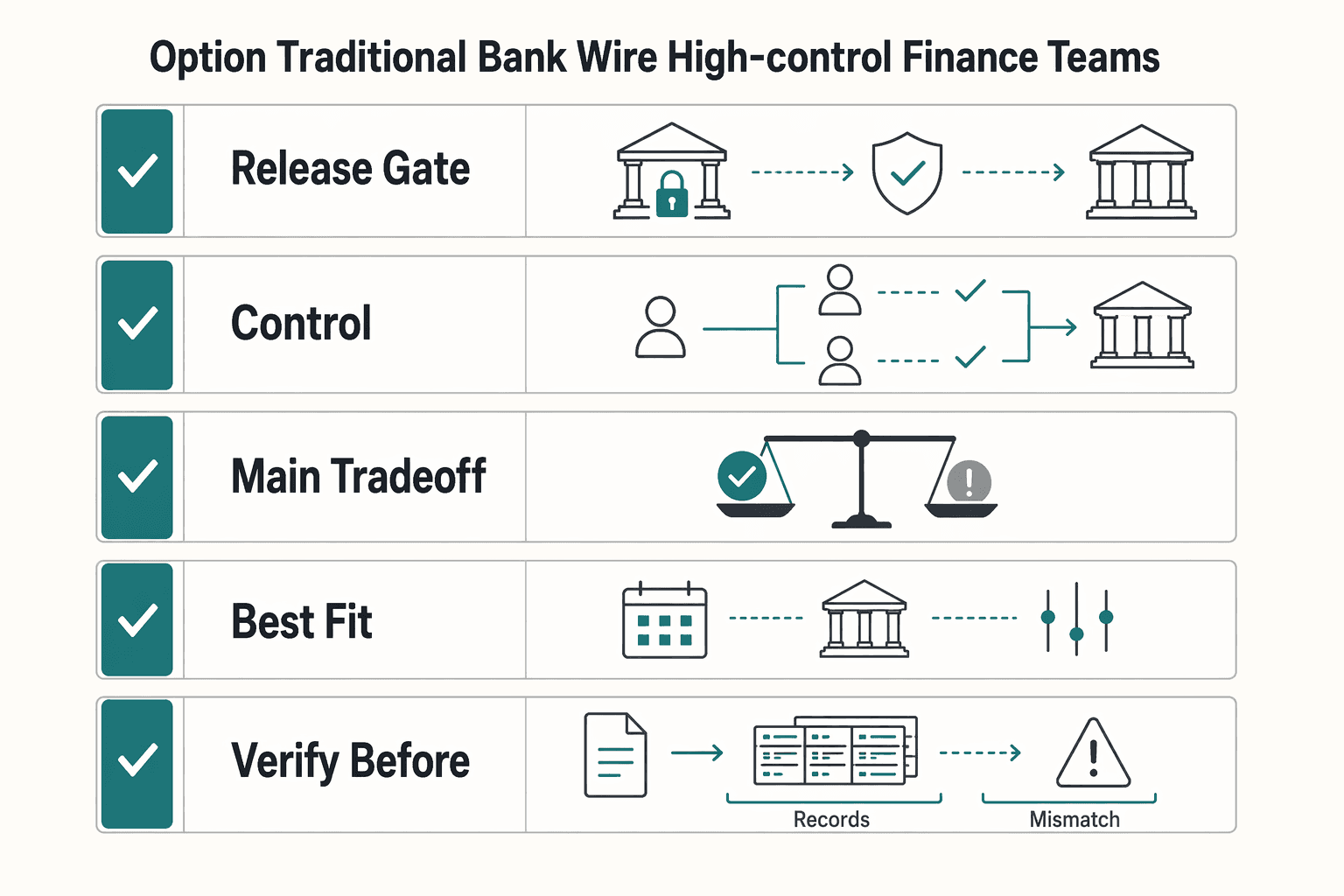

Option 2 Traditional Bank Wire for High-Control Finance Teams#

Use a traditional bank wire when your priority is control inside the banking channel, not maximum convenience. This can fit when release has to follow bank-native approvals and your finance process prioritizes that control.

- Best for: vendor payments where release must follow bank-native approvals.

- Main advantage: can provide clear internal control over the payment order and authorization flow.

- Main tradeoff: wire outcomes depend heavily on instruction quality, and missing fields can cause delays or returns.

- Best fit

Choose this route when your team needs payment release, approval, and confirmation to happen inside your bank workflow.

- What to verify before release

Treat each wire as a data-quality check. For cross-currency wires, routing may include an intermediary bank, and when it does, the intermediary SWIFT BIC must be included.

- beneficiary legal name exactly as held by the receiving bank - beneficiary account and required bank-routing details - country code in required 2 character format where requested - intermediary-bank details and SWIFT BIC if applicable - invoice or remittance reference the recipient can match

- Form-level checks for US-to-India flows

If the receiving side provides a wire or remittance form, use that form as your source of truth. In HDFC's USA-to-India instructions, the sender is asked to provide specific remittance-form details and enter the purpose code in fields 70 and 72.

- Common failure mode

Common avoidable issues come from instruction errors: name mismatches, missing purpose details, or incomplete intermediary routing data. If the receiving bank gives purpose-specific rules, follow them exactly. For example, HDFC says not to include NRE or NRO savings account numbers for FCNR deposit remittances.

Choose bank wire when your process values controlled release and evidence inside bank records. Then store the final instructions, confirmation, and invoice together for a reliable audit trail.

Option 3 Card Checkout and Merchant Rails for Speed#

Use card checkout as an exception path for urgent or smaller invoices when payer-side completion speed matters more than finance-close simplicity. It can solve a timing problem, but it may not fit every workflow as the default.

- Best for: one-off, time-sensitive vendor payments when the agency can accept a checkout link, card invoice, or merchant payment page.

- Main advantage: card and wallet methods can make the front-end payment step easier to complete for some international payments.

- Main tradeoff: recurring or higher-value invoices may need tighter finance-close and documentation workflows than a simple checkout flow.

Before first use, confirm the setup behind the checkout, not just that cards are accepted:

- whether settlement runs on local rails or global rails (for example, ACH/SEPA versus SWIFT)

- whether the agency legal name on the checkout or invoice matches your contract

- whether your invoice or remittance reference appears in the confirmation

- whether separate remittance proof is still needed for agency documentation workflows, including provider-specific paths for items such as FIRC

If checkout options are too narrow, payment completion can drop. In checkout contexts, missing preferred payment options is linked to abandonment or cancellations above 50%, so verify accepted methods before the due date. For repeat invoices, consider transfer rails and evaluate local versus global routes, since local rails are often faster and more cost-effective.

Option 4 Platform-Mediated Payouts for Multi-Vendor Ops#

Platform-mediated payouts make the most sense when your real problem is control across many vendors, not speed on one invoice. If you are paying multiple agencies or contractors in India and other markets, a shared approval layer and centralized payout record can be more useful than a faster one-off transfer.

Why teams move here#

The main benefit can be centralized control: one place for approvals, payout status, and records across international payments. This works best when permissions are enforced at execution time, with clear role-based access for who can prepare, approve, and release payments. Used well, payment tools can simplify work and reduce errors.

What to verify for India before you commit#

Start with payout fit, not the demo. Contractor payments in India are generally made in INR, so confirm INR support for your vendor type and program, and confirm what payment references are preserved in records and exports.

Before onboarding, lock contract basics in writing: payment terms, IP rights, and confidentiality policies. Then run a small pilot and review which records you can actually extract after payout, such as:

- Approval history

- Payout confirmation and status history

- Invoice or remittance reference

- Beneficiary name matching contract records

- Currency shown as INR where applicable

The tradeoff most teams underestimate#

Do not assume a platform automatically fixes close work. Payment reconciliation can still remain manual, especially if exported records are incomplete for your accounting workflow.

Also expect availability and documentation flows to vary by market and program. Confirm availability and post-payment documentation for your exact U.S.-to-India setup before committing. For occasional single-vendor payments, this can be extra overhead. For multi-vendor operations with approval controls, it is often a practical upgrade.

Related: What to Do If You've Been Misclassified as an Independent Contractor.

Set Payment Terms Before the First Dollar Moves#

Set payment terms and payout-evidence requirements before you collect bank details. That order prevents a lot of month-two friction because the hard questions get answered while everyone is still aligned.

| Term area | What to set | Record note |

|---|---|---|

| Invoice and acceptance rules | Agree the invoice format and milestone acceptance process before kickoff, including who approves completion, what delivery evidence is acceptable, and how approval or rejection is handled | Set this before you collect bank details |

| Currency and payout-proof handling | State the invoicing and settlement currency approach, who carries conversion or transfer shortfalls, and which payment references must be preserved for matching later | If remittance proof may be requested, agree the documentation path in advance and what happens if a document is unavailable |

| Dispute boundaries | Put clear language around late-fee handling, rework boundaries, and dispute steps | Use a predictable process instead of ad hoc escalation |

| Clause/version trail | Keep a dated snapshot of the version you relied on when you reuse public clause references | Version metadata and retained downloads help preserve that record |

- Lock invoice and acceptance rules in writing

Agree the invoice format and milestone acceptance process before kickoff, including who approves completion, what delivery evidence is acceptable, and how approval or rejection is handled.

- Define currency and payout-proof handling

State the invoicing and settlement currency approach, who carries conversion or transfer shortfalls, and which payment references must be preserved for matching later. If remittance proof may be requested in your payment corridor, agree the documentation path in advance and spell out what happens if a document is unavailable.

- Set dispute boundaries early

Put clear language around late-fee handling, rework boundaries, and dispute steps so invoice holds and scope disagreements follow a predictable process instead of ad hoc escalation.

- Keep a version trail for clause language

When you reuse public clause references, keep a dated snapshot of the version you relied on. FAR Part 52 includes a clause-editing checkpoint at 52.104, and the Part 52 page can be downloaded and retained with your draft. Version metadata such as FAC 2026-01, effective 03/13/2026, plus eCFR recency markers like up to date as of 3/19/2026 and last amended 2/26/2026, help preserve that record.

Final recommendation: finalize payment terms and evidence requirements first, then onboard payout details.

First Payment Execution Checklist#

For a first transfer from the United States to India, treat execution as a document-control exercise. Align identity and scope, decide which record controls if something conflicts, and save what you relied on.

| Control point | What to do | Grounding note |

|---|---|---|

| Legal identity, scope, and contacts | Keep separate records for project scope and contact details, then verify they point to the same counterparty you are paying | This mirrors separating an Authorized Scope of Work (Attachment 1) from Project Contact Information (Attachment 2) |

| Document precedence | Write a simple precedence rule into your payment file before release | Where documents conflict, Specific Award Conditions shall control |

| First-transfer evidence file | Save the records you relied on for this transfer and the approvals used to release it | No mandatory U.S.-to-India evidence pack is established here |

| Record updates | Update the record promptly if contact details change | This follows the same control discipline used in EDA conditions |

| Public references | If you use U.S. government material, confirm it is on an official .gov domain and loaded over HTTPS | Some manual chapters may be unavailable or under review, so note what you used at the time of review |

- Align legal identity, scope, and contacts before payout setup

Keep separate records for project scope and contact details, then verify they point to the same counterparty you are paying. This mirrors the EDA pattern of separating an Authorized Scope of Work (Attachment 1) from Project Contact Information (Attachment 2).

- Decide which document controls if records conflict

Write a simple precedence rule into your payment file before release. The operating model is the same as the source principle that where documents conflict, Specific Award Conditions shall control. Make it explicit which record governs identity and scope.

- Save a first-transfer evidence file based on what you actually used

There is no mandatory U.S.-to-India evidence pack established here, so do not treat any checklist as universal. Save the records you relied on for this transfer and the approvals used to release it.

- Refresh records immediately if details change

If contact details change at any point, update the record promptly. That follows the same control discipline used in EDA conditions.

- Validate public references before relying on them

If you use U.S. government material during verification, confirm it is on an official .gov domain and loaded over HTTPS. Some manual chapters may be unavailable or under review, so note what you used at the time of review.

Related reading: The Best Way to Pay Freelance Collaborators in Europe from the US.

Before your next transfer, run a quick side-by-side cost and settlement check: Use the payment fee comparison tool.

Recurring Payment Cadence That Prevents Month-End Chaos#

Once the first payout works, process drift can become a bigger risk than setup. The fix is a repeatable monthly cadence, consistent records, and a clear status on every unresolved item before close.

- Run one monthly payment calendar as a control

Set a stable approval cutoff, payout day, and close-review day, and keep that rhythm consistent. This supports timing discipline alongside authorization, accuracy, completeness, and compliance in your internal controls. When payouts and close work collide, uncertainty rises fast.

- Use the same record structure each month so reconciliation stays traceable

You do not need a mandated format, but you do need consistency. Keep invoices, disputes, payments, and communications together in one system of record, along with open exceptions and owners. For each invoice, you should be able to trace either a completed payment record or an open exception.

- Label unresolved items before making close decisions

Use plain internal labels such as in-flight, held, or returned to make review easier. These are workflow labels, not mandated accounting classifications. Tie each label to evidence, such as a transfer confirmation, provider status, or return notice, so close decisions stay defensible and do not turn into late-signal manual chaos.

- Handle exceptions as they appear instead of batching avoidable cleanup

Earlier triage can reduce month-end cleanup. Duplicate bills and unreconciled bank spends can quietly erode margins over time, so each exception should get a clear next action. More frequent matching also helps reduce cash opacity before close week.

Common Failure Points and What to Do Next#

When a payment issue appears, start by verifying records before you assume anything else. Confirm what you can document, note what is still unknown, and work from that shared record.

- Delay after send

Build a shared record from available documents, and label any gaps as unconfirmed before escalation.

- Support-doc dispute, including FIRC

Treat any FIRC request as case-specific and confirm in writing what can be provided now, who owns the next step, and when it is due.

- Unexpected cost drift on foreign currency transactions

Record the instructed amount and the reported settled amount, and escalate repeated unexplained differences for formal review.

If a dispute shifts into legal or policy interpretation, verify the source record before relying on it. FederalRegister pages include a link to the corresponding official PDF on govinfo.gov, and FederalRegister XML content is unofficial and does not provide legal notice. eCFR content is authoritative but unofficial, so use it as a recency check and verify against an official edition when needed.

The Practical Default for Most Small Teams#

For most small teams, the practical default is an invoice-first transfer method with documentation built into every payment, and cards used only when speed truly matters. Do not chase the fastest rail. Make each payment easy to approve, easy to prove, and easy to match later.

- Use an invoice-first transfer rail as your default

Start with a method you can match cleanly: one invoice, one approved payment, one transfer confirmation, and one receipt confirmation. Wise is one option because it says you see the fee and exchange-rate breakdown before confirming. It says it uses the live mid-market rate with a separate upfront fee and works on a pay-for-use basis without plans. It also says fees vary by currency, so do not assume last month's cost pattern will repeat.

Keep the core records together each time: invoice, pre-send pricing details, final transfer confirmation, and recipient confirmation. That set is your minimum audit trail when settled amounts are questioned later.

- Treat cards as the exception, not the baseline

Use card rails when speed is worth the tradeoff, not as your recurring default. If you do use a card, plan for tighter documentation so payment context stays clear later.

If you do use a card, tighten the record set: invoice, approval note, payment receipt, and written confirmation of what the charge covered. Keep it as a one-off path unless you intentionally change policy.

- Recheck method fit before growth creates friction

Re-run your method choice on a regular cadence and test whether fees were clear before send, follow-up work stayed low, and the close file can be reviewed by someone else without guesswork. Wise says discounts begin above 25,000 USD monthly volume, or equivalent. It also lists sending and conversion fees starting from 0.57% with currency-based variation. Wise notes that fees can change as transfer costs change, so periodic rechecks are operationally necessary.

More broadly, cross-border corridors can still be slow and costly. The ECB called out this friction on 27 June 2025. If repeats, delays, or unexplained differences start appearing, tighten controls early instead of waiting for month-end issues.

If your vendor payment volume is growing and you need policy-gated payouts with clear status tracking and reconciliation-ready records, review Gruv Payouts.

Frequently Asked Questions

What is the best way to pay an Indian development agency from the US?

The approved sources for this section do not support a single "best" payment method, and they do not provide direct guidance on US-to-India agency payment operations. Use a method your team can document from invoice through receipt, and apply that process consistently.

How can I reduce FX leakage and transfer friction on recurring US-to-India payments?

Use a consistent process and compare what was invoiced, what was sent, and what was confirmed as received each cycle. If differences repeat, resolve them before the next payment.

What payment terms should I lock before the first transfer?

There are no standard U.S.-to-India agency terms to assume. Set terms in writing before the first payment and make sure both sides agree on how payment proof and follow-up requests will be handled.

When should I choose Wise versus a bank wire for agency invoices?

There is no reliable cost, speed, or reliability comparison between Wise and bank wires to lean on. Choose based on your internal approval and documentation requirements, and keep that approach consistent unless you have a documented reason to change.

What records should I store for audit trail and reconciliation?

Keep records that let your team trace the payment path and any exceptions or follow-up requests. When using U.S. government guidance, rely on official .gov pages and confirm HTTPS before sharing sensitive information.

How do I handle chargeback risk if I pay by card?

This section’s sources do not provide chargeback-rate or card-rail risk benchmarks for agency invoices. Use your internal risk and documentation policies for card payments, and keep dispute-related records organized. If recurring disputes create friction, review your internal payment policy.

What should I do if the agency asks for FIRC after payment?

The approved sources here do not define FIRC issuance rules, required documents, or timelines. Share the payment records you can verify, ask for the exact missing item, and confirm next steps in writing. If you consult U.S. government references during that process, use official secure .gov pages with HTTPS.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- acquisition.gov/far/part-52trusted

- bia.gov/frequently-asked-questionstrusted

- bia.gov/sites/default/files/dup/assets/bia/ots/ots/p...trusted

- bis.gov/news-updatestrusted

- bphc.hrsa.gov/sites/default/files/bphc/data-reporting/2024...trusted

- business.defense.gov/Programs/Indian-Incentive-Program/FAQstrusted

- congress.gov/committee-report/119th-congress/senate-repor...trusted

- dos.ny.gov/system/files/documents/2026/03/031126_0.pdftrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How LLC Owners Separate Business and Personal Finances

For an LLC, separating business and personal money is best treated as a weekly habit, not a one-time bank setup. It keeps records cleaner, cuts month-end cleanup, and creates clearer boundaries as the company grows.

What to Do If You've Been Misclassified as an Independent Contractor

Treat this as a protection problem first, not a label debate. If your work was treated as an independent contractor arrangement even though the relationship functioned differently, your first goal is to protect pay, rights, and records while you choose the least risky escalation path. You can do that without making accusations on day one, which often keeps communication open while you document what happened.

Indian Freelancer Payment Analysis That Protects Net INR

For freelancers in India, the number that protects cash flow is the net INR credited to your bank, not the USD amount on the invoice. Start from that outcome and work backward through every payment decision.