Quick Answer

Start with one corridor and one rail, then expand only after pilot controls are proven. Use ACH, Wire transfer, SEPA, SEPA Instant, PIX, UPI, and SWIFT as options to screen for corridor support, beneficiary data requirements, and named exception ownership. Before go-live, require written provider confirmation for route behavior and production enablement, then verify daily reconciliation between payout records and ledger outputs.

How to Compare ACH, SEPA, PIX, and UPI for Platform Payouts#

Use this comparison as a decision aid, not a ranking. The point is to help you choose the right payout rail mix for marketplace payouts across ACH, Wire transfer, SEPA, SEPA Instant, PIX, UPI, and SWIFT based on operating fit, not headline speed alone. A strong choice usually balances speed, cost, geography, and payout experience.

| Team | Main concerns |

|---|---|

| Finance | Fee predictability, foreign exchange exposure, and whether payouts can be reconciled cleanly |

| Payments ops | Beneficiary data quality, exceptions, and compliance gates |

| Engineering | Whether the integration is reliable enough for real traffic, asynchronous status changes, and retries |

This is intentionally written for a cross functional audience. Finance cares about fee predictability, foreign exchange exposure, and whether payouts can be reconciled cleanly. Payments ops cares about beneficiary data quality, exceptions, and compliance gates. Engineering cares about whether the integration is reliable enough for real traffic, asynchronous status changes, and retries. If one of those teams cannot support a rail in production, the answer is usually no, even if the rail looks attractive on paper.

There is no universal winner. Local payment methods vary by country, while global wire options can help fill the gaps for cross-border transfers. In the source material, ACH and Fedwire are described as US local methods, while SWIFT is global. PIX and UPI are country specific rails, with UPI identified as India's real time payment system and PIX grouped with newer instant, low cost rails. That matters because you should verify country and corridor coverage before treating any rail as launch ready. A rail can be a strong fit in one market and irrelevant in the next.

It also helps to set expectations early on settlement and price. Terms like SEPA Instant, PIX, or UPI tell you something about the rail, but they do not guarantee the exact payout experience you will get from a specific provider route or configuration. The same caution applies to pricing. Provider fees, FX treatment, and rejection or return handling costs may stay unclear until commercial and provider confirmation. If you need a real go or no go decision, ask for corridor specific confirmation rather than relying on a generic product page.

One practical recommendation up front is simple. Do not choose your first rail mix only because it sounds fastest. Start with the rails your team can actually verify before launch. That means confirming supported markets and programs, checking the beneficiary data you must collect, and naming who in finance and ops owns final approval.

A common failure mode can be choosing a rail for speed, then discovering late that coverage is limited, pricing shifted during review, or no one owns exception handling when payouts start failing. The sections that follow are built to help you avoid that.

Need the full breakdown? Read ACH vs Wire Transfer for Contractor Payouts When Platform Teams Should Use Each.

At a glance comparison matrix for ACH wire SEPA PIX UPI and SWIFT#

Use this matrix to eliminate weak options early, not to approve go-live. If a cell says confirm with provider, treat it as unresolved.

Public comparison formats commonly start with fees, transfer speed, and supported countries. Keep that as your first pass, then require provider confirmation before you commit on settlement behavior, compliance workflow, or API/webhook operations.

| Rail | Settlement profile | Fee predictability | FX exposure | Compliance burden | Integration complexity | Best-fit use case | When to use / avoid | Operator checkpoint |

|---|---|---|---|---|---|---|---|---|

| ACH | Historically batch-based in one US example; exact timing varies by provider [known from public docs] | Confirm with your provider | Confirm with your provider | Confirm with your provider | Confirm with your provider | Use only after corridor/program fit is confirmed [confirm with provider] | Use when non-instant timing is acceptable; avoid when launch depends on unconfirmed speed [confirm with provider] | Internal launch pack: entity docs for KYB review, beneficiary data for KYC intake, named finance/ops approver [confirm with provider] |

| Wire transfer | Cutoff-sensitive in one US example [known from public docs] | Confirm with your provider | Confirm with your provider | Confirm with your provider | Confirm with your provider | Use only after provider confirms operational fit [confirm with provider] | Use when urgency justifies cutoff management; avoid without clear exception ownership [confirm with provider] | Internal launch pack plus written cutoff/exception ownership [confirm with provider] |

| SEPA | Confirm with your provider | Confirm with your provider | Confirm with your provider | Confirm with your provider | Confirm with your provider | Use only after coverage and program fit are confirmed [confirm with provider] | Use when corridor and beneficiary-field rules are confirmed; avoid assumptions from rail name alone [confirm with provider] | Internal launch pack plus provider-confirmed beneficiary fields and corridor approval [confirm with provider] |

| SEPA Instant | Name suggests speed, but actual route behavior is not established here [confirm with provider] | Confirm with your provider | Confirm with your provider | Confirm with your provider | Confirm with your provider | Use only after explicit production enablement confirmation [confirm with provider] | Use when instant routing is confirmed in writing; avoid marketing-page assumptions [confirm with provider] | Internal launch pack plus explicit enablement and failure-owner assignment [confirm with provider] |

| PIX | Confirm with your provider | Confirm with your provider | Confirm with your provider | Confirm with your provider | Confirm with your provider | Use only after local corridor and data-rule confirmation [confirm with provider] | Use when local support is confirmed; avoid if onboarding data requirements are unclear [confirm with provider] | Internal launch pack plus local beneficiary data checklist and exception owner [confirm with provider] |

| UPI | Confirm with your provider | Confirm with your provider | Confirm with your provider | Confirm with your provider | Confirm with your provider | Use only after eligibility and data-rule confirmation [confirm with provider] | Use when program approval is confirmed; avoid if compliance ownership is open [confirm with provider] | Internal launch pack plus verified beneficiary data capture and escalation owner [confirm with provider] |

| SWIFT | Confirm with your provider | Confirm with your provider | Confirm with your provider | Confirm with your provider | Confirm with your provider | Use only after corridor-level route confirmation [confirm with provider] | Use when fee/FX/status handling are documented; avoid if these remain vague [confirm with provider] | Internal launch pack plus written fee, FX, and status-handling confirmation [confirm with provider] |

Two checks prevent most bad rail decisions:

- Confirm whether the provider is describing internal movement or an external bank transfer. Public comparison material explicitly distinguishes "internal, instant" vs "external, varies."

- Pressure-test speed claims against operating constraints. One cited US example describes wire cutoffs and ACH batch behavior, which is a reminder that timing can break on banking-hour and routing realities.

Practical first-pass rule: mark a rail red until you have written confirmation of corridor support, required beneficiary data, and a named finance/ops approver.

If you want a deeper dive, read PIX vs. SEPA vs. ACH vs. SWIFT: Choosing the Right Payout Rail for Each Market.

Which payout rail should you launch first for your platform#

Launch the first rail your team can operate and reconcile daily, not the one with the strongest speed claim. Start with one corridor and one rail, prove control in production, then expand.

Start with payout shape, then verify corridor reality#

| Starting condition | Rail to evaluate first | Why this is a practical first choice | Verify before go live |

|---|---|---|---|

| Domestic, recurring bank payouts with no instant promise | ACH | Often aligns with scheduled, repeat payout flows | Coverage map, beneficiary data requirements, return handling, and daily reconciliation ownership |

| Time-sensitive payouts where local instant routing is confirmed for your program | PIX, SEPA Instant, or UPI | These are named local instant rails and can fit urgency-driven payouts when enabled for your corridor | Corridor approval, production enablement, webhook/status model, and exception ownership |

| Cross-border payouts or corridors without confirmed local rail coverage | Wire transfer or SWIFT | Practical fallback when local instant options are not available for your approved scope | Written fee/FX handling, status visibility, cutoff handling, and escalation path |

This is a launch rule of thumb, not a universal law. Public material can indicate broad global coverage or local instant capabilities, but you still need corridor-level confirmation before committing a rail to finance, ops, or product.

Choose the rail you can close operationally every day#

Your first rail should let engineering and finance close the loop daily across Payouts API records, webhook events, and ledger exports. During pilot, use provider docs plus the status page as operating inputs, not procurement artifacts, so delays and degraded states are handled predictably.

Roll out in a narrow sequence#

| Step | Requirement |

|---|---|

| 1 | Pilot one corridor on one rail |

| 2 | Review failed, delayed, and rejected payouts until the exception queue has a clear owner and response path |

| 3 | Add a second rail only after retry handling and duplicate-event protection are stable |

Related: Procurement Technology Stack for Platform Operators: What Tools to Use at Each Growth Stage.

Hidden costs and tradeoffs that change total payout cost#

Total payout cost is rarely the number on the fee card. The reliable way to model it is: published fees + conversion behavior + failure handling + internal ops time.

Visible fees are still the starting point, but they are not the full picture. In PayPal's public documentation, consumer and merchant fee menus are separate, Currency Conversions is its own fee area, and merchant fees include categories like Chargeback Fees. Even when a page shows a clear number like Starting at 2.89% + $0.29 per transaction, it is not all-in by itself, because exchange rates or issuer/bank fees may still apply.

| Cost driver | What looks visible first | What usually changes real cost | What to verify before margin modeling |

|---|---|---|---|

| Provider fee schedule | A percent-plus-fixed number | Market-specific pages, product-specific pricing, and exception-based treatment in some cases | Exact market page, product scope, and page date |

| Currency conversion | One quoted rate | Spread behavior and additional bank/issuer charges outside provider line items | Quote source, timestamp, and whether external bank/issuer fees can apply |

| Failed payouts | Headline transfer fee | Rework, correction cycles, and support effort | Rejection reasons and manual touches per failed payout |

| Internal operations | Often omitted | Reconciliation workload and exception queue handling | Who owns exceptions and time-to-close per case |

Consumer-first versus operator-grade payout flows#

Consumer-friendly payout flows can be strong for recipient simplicity. For operators, the key constraint is that public consumer and merchant pages do not automatically produce a complete business payout-cost model across corridors and products.

Even basic classification can shift costs: PayPal defines domestic as sender and receiver in the same market, and international as sender and receiver in different markets. If your payout population crosses that market boundary, your modeled cost logic must change with it.

Also treat fee pages as moving inputs, not fixed constants. The cited pages show different update dates (February 19, 2026, February 9, 2026, and 21, April 2025), so your model should record which market page and date you used.

Speed changes cost, not only wait time#

If you prioritize faster methods (including local instant options such as PIX, SEPA Instant, or UPI where available), include the operating burden in the same cost model. Faster payout expectations usually mean stricter monitoring, faster exception ownership, and tighter status handling to avoid support and finance cleanup.

Cost of failure checklist#

Before labeling any rail "lower cost," price failure paths explicitly:

- Duplicate payout risk: retries without replay-safe controls (for example, idempotency handling) can turn one incident into outsized loss.

- Delayed cash visibility: submitted payouts that do not reconcile cleanly to ledger movement create treasury and close-process overhead.

- Unresolved exception queues: rejected payouts and missing status resolution convert directly into labor cost.

If headline pricing is close, choose the option your team can verify, reconcile, and close without manual backlog drift.

For a step-by-step walkthrough, see Platform Payout Cost Estimator for Wire, ACH, and Local Rails.

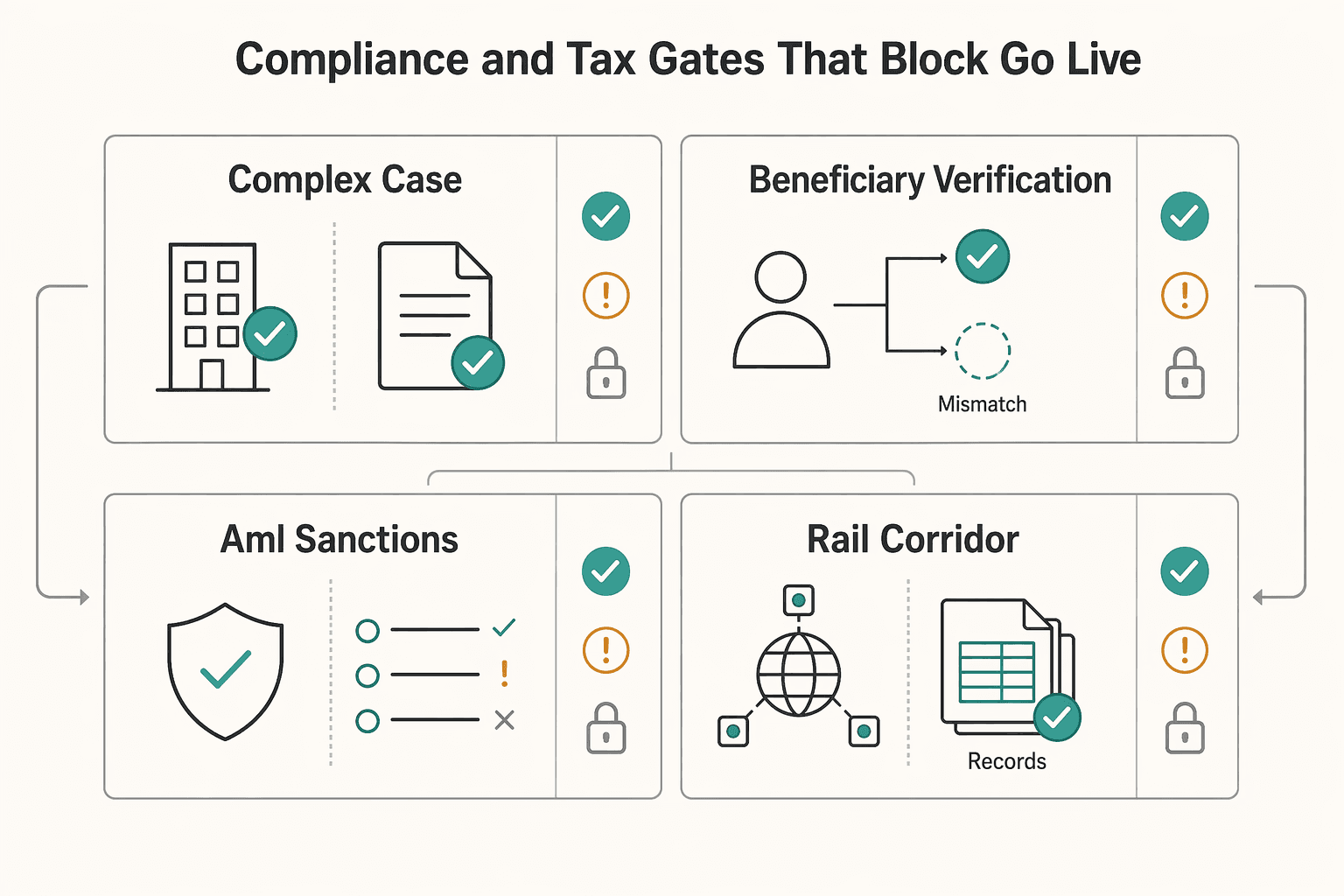

Compliance and tax gates that block go live#

A payout rail is not launch-ready when pricing is done; it is launch-ready when compliance, eligibility, and tax operations are fully cleared and documented.

Use this as an operational gating sequence, not a universal legal rule: entity approval, beneficiary verification readiness, AML/sanctions policy handling, then rail-and-corridor enablement checks. If you configure rails first, you can still fail at go live when earlier approvals or controls are incomplete.

| Gate | What must be true before launch | Common blocker | Evidence to keep |

|---|---|---|---|

| Entity approval | Your payout program can operate under the approved business profile | Document mismatches or incomplete ownership/business data | Approval status, owner, and final submitted entity records |

| Beneficiary verification readiness | Recipient records meet required checks for the intended payout flow | Missing fields or identity/profile mismatches | Required field list by route and exception handling notes |

| AML/sanctions policy handling | Review and escalation paths are defined and owned | Holds with no clear escalation owner | Policy decision log, queue owner, and exception records |

| Rail and corridor enablement | The selected method is actually enabled for your use case | Assuming a method is available for every recipient/corridor | Provider confirmation for production route coverage |

Delays usually come from control gaps, not from pricing models: unclear ownership, unresolved holds, and missing evidence. This is especially important when you plan to use SEPA, PIX, or UPI, where availability and eligibility can vary by provider setup and route.

Tax operations should be treated as a launch gate too. If payouts may trigger 1099 reporting duties, define upfront who captures tax-relevant payee data, who retains evidence, and where finance, ops, and compliance can retrieve it.

Build one pre-launch evidence pack#

Before go live, keep one shared pack that finance and ops can review quickly:

| Evidence item | What to keep |

|---|---|

| Compliance approvals | Final decision records |

| Approved policy exceptions | Scope and owner |

| Beneficiary data requirements | By payout route |

| AML/sanctions escalation | Ownership and queue location |

| 1099-related data capture | Ownership and storage location |

| Audit trail | Ownership for post-launch changes |

Do not mark ACH, wire, SEPA, PIX, or UPI as ready until each gate has a clear owner, an approval record, and retrievable evidence. For related U.S. routing context, see FedNow vs RTP vs ACH for U.S. Platform Payout Routing.

Integration and reliability checks for engineering and operations#

After compliance clears, the next go/no-go decision is technical: do not launch a rail until your team can submit payouts, track status changes, prevent duplicate execution, and reconcile movement without manual guesswork.

Set a minimum internal baseline before launch:

- a working

Payouts APIpath for create and status lookup - asynchronous update handling (for example, API webhooks) with replay-safe processing

- an idempotency-key policy your team controls end to end

- a reconciliation process engineering and finance can run consistently

That baseline keeps automation useful. Stripe's payments guidance frames automation as a way to make payments faster and reduce human error, which is the right standard for this stage.

| Failure mode | What it looks like in production | What to verify before launch |

|---|---|---|

| Duplicate request submission | A timeout or retry path triggers a second payout attempt | Where idempotency keys are created, how replays are handled, and how duplicate attempts are detected |

| Asynchronous update gap | Provider-side status changes but your platform record does not update | How status is re-fetched, how inbound events are replayed safely, and how missing updates are surfaced |

| Stale FX quote usage | Approved economics and submitted payout details drift | Who owns quote refresh decisions, and which quote reference is stored with the request |

| Payout state mismatch | Provider state and internal ledger/dashboard disagree | State mapping rules, terminal-state handling, and a repeatable reconciliation check |

What to test before production#

Use a sandbox-to-production parity checklist for the exact live path: beneficiary creation, payout submission, asynchronous status handling, reject/return handling, and payout lookup after timeout scenarios. The goal is operational predictability, not perfect sandbox fidelity.

Also test timeout behavior intentionally. If a request times out, your flow should continue through the same idempotency key path and then confirm final state through your normal status channels before manual intervention.

Use a shared launch sign-off#

Require one reconciliation sign-off shared by engineering and finance before go live. Include sample API payloads, saved asynchronous event payloads, timeout test evidence, state-mapping rules, and one completed ledger-vs-provider reconciliation run. If that pack is not ready, the rail is not operationally ready.

You might also find this useful: International ACH Transfers: Complete Guide for Platform Cross-Border Payouts.

Scenario recommendations by platform model and market#

Launch the narrowest payout scope your team can operate reliably today, then expand only when demand and controls are proven.

| Platform scenario | Recommended launch scope | What to verify before go live | Red flag |

|---|---|---|---|

| Creator or contractor marketplace in one domestic market | Keep your domestic rail mix plus one documented fallback route | Named owner for payout exceptions, beneficiary data requirements, and daily reconciliation between provider records and your ledger | Expanding to additional cross-border rails before recipient demand and exception handling are proven |

| EU-heavy payout volume | Treat tax setup as a prerequisite to rail expansion decisions | Finance has a written OSS position, including whether cross-border B2C activity is in scope, whether the EUR 10 000 threshold applies, and which Member State of identification applies under the Union scheme | Treating EU expansion as only a routing project |

| Brazil or India growth bet | Enable local routes only where provider/entity/corridor support and fallback handling are explicit | Provider support by country, entity, and recipient type; AML review owner; manual escalation path when a payout cannot be released automatically | Launching a local route without a fallback and owner for exceptions |

| Cross-border multi-currency program | Keep volume gated until FX controls are explicit and approved | Quote validity rule, approval threshold, stored quote reference, and what happens when the quote expires before submission | Submitting against stale or missing FX quote context |

For EU operations, keep one point clear in your launch memo: OSS is a VAT process, not a payout rail. From 1 July 2021, EU cross-border B2C VAT rules changed, including replacement of prior distance-sales thresholds with an EU-wide EUR 10 000 threshold.

If VAT treatment is complex, pause assumptions and route it through a VAT Cross-border Rulings (CBR) request under the applicable national ruling conditions and participating-country scope.

We covered this in detail in Batch Payout File Formats for NACHA ACH, ISO 20022 PAIN, and SEPA Credit Transfer.

30 day execution checklist from shortlist to production#

Use a 30 day plan only for a narrow launch with clear ownership. If corridor scope or exception ownership is still unsettled, treat this as a sequencing template, not a rollout promise.

| Week | Focus | What to lock by week end | Stop if |

|---|---|---|---|

| 1 | Shortlist and owners | Corridor-level rail shortlist (ACH, Wire transfer, SEPA, PIX, UPI) plus named owners for KYC, KYB, AML, finance approval, and payout exceptions | A rail is listed without a clear country, entity, or recipient-type decision |

| 2 | Technical design | Agreed payout request model, webhook handling approach, idempotency key policy, retry behavior, and failure-queue ownership | The team can submit payouts but cannot clearly explain duplicate prevention or replay handling |

| 3 | Controlled pilot | Small pilot batch, daily reconciliation between provider records and your ledger, and a written exception log | Exceptions are handled in inboxes or chat instead of a tracked queue |

| 4 | Production readiness | Finance, ops, and engineering sign-off, with explicit notes for where each rail is supported and when it is enabled | Any corridor is assumed live without documented enablement |

Week 2 is the highest-risk checkpoint: design ambiguity here becomes payout errors later. Keep one documented idempotency policy, one state map from webhook events to internal payout states, and one owner for stuck or ambiguous payouts.

Before go-live, run a rail-by-rail coverage check. "Supported" is not enough unless it is confirmed for your entity, corridor, and beneficiary type. This matches the implementation-first lens in the World Bank fast payments main report (September 2021): move only when reconciliation, exception ownership, and enablement are explicit.

Related reading: How Bahtnet Works: Thailand Central Bank Wire Transfer for Platform Operators.

Want a quick next step for "payout method comparison tool ach wire sepa pix upi platform operators"? Try the free invoice generator.

Conclusion#

Choose the rail mix your team can actually operate with confidence. Headline speed is not the deciding factor if finance cannot reconcile it, ops cannot handle exceptions, or compliance still has open questions.

The cleanest way to close this decision is to anchor it in business fit and scope. ACH and Fedwire are US-local methods, so they make sense when your payout motion is centered on US dollar transactions and your team already knows that operating path. SWIFT is a global network, so it stays relevant when you need broader reach before a local option is proven. Local payment methods should be treated as market-specific infrastructure choices, not automatic upgrades. They may improve recipient experience in the right corridor, but only if your provider, entity setup, and beneficiary types are actually supported.

That is why your next step should be practical, not theoretical. Use the comparison matrix, the scenario rules, and the 30 day checklist to make one cross functional decision this week: which rail you will pilot first, in which corridor, with which fallback. If you are split between a faster local rail and an older route, pick the option your team can verify every day. A slightly slower method with clean reconciliation is usually the lower-risk launch choice than a faster route that leaves you guessing when a payout is delayed, rejected, or duplicated.

The trust-first checkpoint is simple. Before full rollout, get written confirmation from the provider on corridor coverage, beneficiary and entity support, and any production conditions that change by market or route. For cross-border programs, pay extra attention to hidden fees, unpredictable exchange rates, and lengthy settlement times. Those are the costs that usually turn a good-looking comparison into a bad operating outcome. If those points are still vague after commercial review, you do not have a go live decision yet.

One final rule is worth keeping: do not approve a rail on a demo alone. Approve it when finance, ops, and engineering can review the same pilot evidence and reach the same conclusion about what happened to a payout, including failures.

Frequently Asked Questions

Which payout rail should a marketplace launch first if it has limited engineering bandwidth?

Start with the first rail your team can reconcile every day, not the one with the fastest headline speed. For a US-first launch, that can mean a domestic option like ACH, with a narrow pilot before you add anything else. If your exception queue, API webhook handling, and idempotency rules are still shaky, do not widen rail coverage yet.

When should operators choose ACH or Wire transfer instead of SEPA Instant, PIX, or UPI?

Choose ACH or wire transfer when your first market is US-local, your finance team already knows the operating path, or your target corridor does not have dependable local instant-rail coverage. The grounded distinction that matters is scope: ACH and Fedwire are US-local methods, while SWIFT is a global network, so wire or SWIFT becomes the fallback when local instant coverage is missing. If you need cross-border reach before you have local-rail certainty, older rails are often the lower-surprise choice.

What minimum criteria should a payout method comparison tool include for finance and engineering teams?

At minimum, compare each rail on corridor coverage, beneficiary support, fee predictability, FX exposure, regulatory complexity, and integration requirements. Your tool should also show whether the rail supports the technical basics you need: payouts API behavior, API webhooks, idempotent retries, and clear payout status mapping into your ledger. Include one more column as well: what must be confirmed with the provider before go live rather than assumed from marketing copy.

What usually breaks after launch in payout operations: compliance gating, settlement, or reconciliation?

This depends on the rail and implementation, so treat all three as launch risks to test. A rail can be technically “live” before your internal records are trustworthy, which makes reconciliation an early pressure point for many teams. A good checkpoint is simple: can engineering and finance explain one failed payout from API request to final ledger entry without guessing?

How should teams compare foreign exchange quote risk across payout methods?

Do not compare FX on a single quoted rate alone. Compare when the foreign exchange quote is created, whether it is indicative or committed, how long it remains usable, and what happens if the payout is retried, delayed, or rerouted. Cross-border business payments are exposed to currency fluctuations, so your approval rule should name who accepts quote risk and at what point a stale quote must be refreshed.

What evidence should be collected before approving go-live for a new payout rail?

Collect a small but complete evidence pack. It should include written confirmation of corridor and beneficiary support, your idempotency and retry policy, webhook-to-ledger state mapping, and pilot reconciliation sign-off from finance and operations. Keep one exception log from the pilot as well, showing how failed or ambiguous payouts were resolved.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bis.org/publ/work1295.pdftrusted

- ecb.europa.eu/pub/pdf/other/ecb.paymentsmarketinfrastructu...trusted

- fastpayments.worldbank.org/sites/default/files/2023-10/Future%20of%20Fa...trusted

- fastpayments.worldbank.org/sites/default/files/2021-11/Fast%20Payment%2...trusted

- niwaplibrary.wcl.american.edu/wp-content/uploads/Reduced-Crowell-Moring-sa...trusted

- paypal.com/us/business/feestrusted

- taxation-customs.ec.europa.eu/archives/taxable-persons/vat-cross-border-ru...trusted

- vat-one-stop-shop.ec.europa.eu/index_entrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

PIX vs. SEPA vs. ACH vs. SWIFT for Platform Payout Decisions by Market

If you own payouts, you do not need another glossary. You need a fast way to choose the rail that fits the job, then avoid the failures that show up after launch. This payout rail comparison is for finance, ops, and engineering teams that care less about labels and more about whether money lands on time, statuses reconcile cleanly, and exceptions stay out of inboxes.

Procurement Technology Stack for Platform Operators at Each Growth Stage

If you run a marketplace, contractor, or creator platform with cross-border money movement, your stage can matter more than feature count. Use what gives you control now, and defer added overhead until you need it. Then watch for upgrade triggers that show your current stack is no longer enough.

International ACH Transfers for Platform Operators

**International ACH can fit repeatable, non-urgent cross-border payouts when lower payout cost matters and you can still control approval, submission, recipient credit, and reconciliation.** For finance, ops, and product owners, this is less a payment-method debate than an ownership and control problem.