Quick Answer

Start with a two-part decision: use pain.001 for outbound initiation and require a proven return path such as camt.053 before launch. For batch payout file formats nacha ach iso 20022 pain sepa credit transfer, the practical win is confirming bank-specific acceptance rules, message version, and sample outputs instead of trusting broad ISO claims. Then choose SEC handling deliberately across CCD, CTX, PPD, or Outbound IAT and lock ownership for Return Reason Codes and Change Codes.

Where These Batch Payout Formats Differ#

A workable batch payout strategy starts with one blunt fact. Saying a provider "supports ISO 20022" is often not enough to build against. You need to separate the message standard from the payment scheme, then confirm exactly what your bank or processor will accept in production.

The practical recommendation is simple: choose your initiation format and your exception path together, or you risk reconciliation debt that is expensive to unwind later.

That matters most when you are mapping U.S. ACH into ISO-based messages. On the U.S. side, NACHA has served as trustee of the ACH Network since 1974. Its white paper describes the network as moving money and information directly from one bank account to another. The same paper says the network universally connects all 12,000 U.S. financial institutions and supports more than 90 percent of the total value of U.S. electronic payments. ISO, meanwhile, is the International Organization for Standardization. Those are different layers, and mixing them up early can lead to bad file assumptions later.

This guide is built for the production questions that show up after the slideware ends. You will get concrete checkpoints around pain.001 and related status or statement data handling. We will also call out where SEPA Credit Transfer and ACH may look similar at a distance, but where scheme rules and bank requirements still need implementation-specific confirmation. Before you commit engineering time, ask for the exact implementation guide your bank or provider uses, the message version it expects, and a sample of the status or statement data you will receive back.

If those items are vague, treat that as a delivery risk, not a documentation gap you can clean up later.

We will also be explicit about what is known versus what still needs confirmation. There is no universal one-to-one mapping between Nacha guidance and every SEPA implementation, and this article will not pretend there is. Where Nacha guidance is clear, we will say so. Where acceptance behavior depends on a sponsor bank, a processor, or a corridor-specific setup, we will label it as bank- or program-specific so you know what still needs signoff.

That scope note matters for trust. The Nacha ISO 20022 white paper itself states that the opinions expressed are those of Q Insights, so it is useful guidance, not a blanket statement of every participating organization's view. The aim here is to help you make sound choices on file family, exception design, and reconciliation readiness, while keeping a short, honest list of items that still require provider confirmation before launch.

This pairs well with our guide on FedNow vs RTP vs ACH for U.S. Platform Payout Routing.

Start with the terms that drive architecture#

Start by separating layers: ISO 20022 is a messaging standard, while ACH and SEPA are payment schemes.

If a provider says it "supports ISO 20022," that still does not confirm what it accepts in production.

In this U.S. mapping context, anchor on Nacha's ISO 20022 Credit Transaction Guide to Mapping U.S. ACH File Formats (August 2023, Version 4.01). The scope is explicit: mapping U.S. ACH formats such as CCD, CTX, PPD, and Outbound IAT. It also explicitly covers "Payment Initiation (pain.001) Credit Transfer File Structure and Content." Treat that as your starting point for outbound batch payout initiation.

Before field mapping, get three concrete artifacts from your bank or processor:

- The exact implementation guide they use

- The message version they expect

- A sample file they accept in production

Keep nearby message families separate in your plan. Teams often discuss pain.008 and camt.053 in the same program, but confirm their role from your bank documentation rather than inferring it from the U.S. ACH mapping guide alone. For Return Reason Codes and Change Codes, confirm where those events appear in provider output and request sample statement or status data early; if that evidence is missing, reconciliation scope is still open.

For a step-by-step walkthrough, see ACH vs Wire Transfer for Contractor Payouts When Platform Teams Should Use Each.

Choose the right file family before you build your payout pipeline#

If your immediate scope is outbound batch payouts, start with pain.001 for initiation and a camt.053 reconciliation plan on day one.

That prevents a common launch gap: leaving returns and Notifications of Change too late.

| File family | Best fit job | What the grounded sources support | What you still need to verify |

|---|---|---|---|

pain.001 | Credit transfer initiation | Nacha's August 2023 Version 4.01 guide covers "Payment Initiation (pain.001) Credit Transfer File Structure and Content" and maps CCD, CTX, PPD, and Outbound IAT | Exact bank implementation guide, expected message version, corridor-specific required fields, and a sample accepted file |

pain.008 | Debit collection context | Confirm pain.008 implementation detail with your scheme documentation | Whether your provider supports it, which version they support, and which debit-specific validations they apply |

camt.053 | Post-settlement statements, returns, and change handling | Nacha's August 2023 Version 2.01 guide covers "Bank to Customer Statement (camt.053) File Structure and Content for Returns," including Return Reason Codes and Change Codes | How complete provider statement enrichment is, where return and NOC events appear, and whether references are enough for automated matching |

Sequence matters: pain.001 defines how you submit outbound instructions, while camt.053 defines how return and change events come back. If you build only submission, exceptions usually fall to manual reconciliation and missing identifiers show up too late.

Before you build transforms, lock down your provider document set. For U.S. ACH mapping, confirm whether they align to Nacha pain.001 Version 4.01 and camt.053 Version 2.01, and request one accepted example plus one returned example. For returns, confirm exactly where Return Reason Codes and Change Codes appear in provider output.

Treat pain.001.001.03 and SEPA Credit Transfer requirements as open version-and-corridor checks unless your bank documentation states them directly. Likewise, treat EPC alignment as something to confirm with your bank or sponsor, not something implied by broad ISO 20022 support or ACH mapping material.

If provider docs are thin, especially on pain.008 and camt.053 statement enrichment, mark that as open scope now. Otherwise you risk shipping a pipeline that can send funds but cannot reliably explain or recover post-submission outcomes. If you want a deeper dive, read SEPA Instant Credit Transfer for Euro Payouts.

Pick ACH SEC codes based on remittance and operational burden#

Pick your ACH Standard Entry Class (SEC) code only after bank/provider validation, not team memory.

Treat

CCD,CTX,PPD, andOutbound IATselection as an implementation decision that must be confirmed in writing.

| SEC code | Grounded note | Confirm before build |

|---|---|---|

| CCD | Named in Nacha's pain.001 mapping scope | Confirm provider production support, accepted remittance fields, release approvals, and failure/change output |

| CTX | Named in scope; may be used for richer remittance | Confirm operational burden, source data quality, field validation, and downstream reconciliation output |

| PPD | Named in Nacha's pain.001 mapping scope | Confirm provider production support, accepted remittance fields, release approvals, and failure/change output |

| Outbound IAT | Named in scope; escalate early for cross-border-sensitive flows | Confirm whether ISO Country Codes and additional review gates apply, and who owns those checks |

Use this short pre-build checklist:

- Which SEC options your provider supports in production for your payout use case

- What remittance fields they accept at submission and preserve downstream

- What approval and review steps they require before release

- What statement/export output you get when items fail or are changed

If you are leaning toward CTX for richer remittance, verify the operational burden before build. Confirm your source data quality, field validation, and downstream reconciliation output so added detail does not become added manual cleanup.

For cross-border-sensitive flows, escalate Outbound IAT design early. Explicitly confirm whether ISO Country Codes and additional review gates apply in your corridors, and who owns those checks.

Be selective with Same Day ACH. The provided ACH comparison source says standard ACH typically settles in one to three banking days, and says Same Day ACH is faster with a $1 million per-payment cap; use that speed only if your funding, approvals, and exception handling can meet tighter windows. Related: Payout Method Comparison Tool: ACH Wire SEPA PIX UPI and More for Platform Operators.

Implement in the right order so finance ops and engineering stay aligned#

Run outbound file creation, submission controls, and inbound statement handling as one track from day one.

Payment formats handle both payment instructions and the statement data you need for reporting and reconciliation, so an outbound-only build creates avoidable finance-ops risk.

| Checkpoint | What to lock down first | Verify before moving on |

|---|---|---|

| 1. Canonical payout model | One internal payout record and one bank/provider-approved pain.001 serialization path | Your team can generate accepted sample files from real scenarios |

| 2. Pre-submit controls | File-format checks, duplicate prevention, and approval gates tied to the exact batch payload | A retry does not create a second logical submission |

| 3. Status and statement ingestion | Asynchronous payment acknowledgments and statement-data mapping (including camt.053 where applicable) | Returned events can be matched back to the original payout record |

| 4. Evidence pack | Immutable batch artifacts for audit and reconciliation | You can reconstruct one batch from source payload to final outcome without manual stitching |

Start by agreeing on the canonical payout record before debating transport details. For pain.001, that means defining one authoritative field map for your implementation and validating against accepted bank/provider samples, rather than relying on memory or ad hoc exports across teams.

Before enabling live submission, prove controls under failure conditions. Your pre-submit layer should confirm format validity for the accepted file type, prevent duplicate logical batches during retries, and enforce approvals that finance ops and engineering can both trace to the exact payload that was sent.

Then finish the return loop and evidence generation before scaling volume. Treat statement/acknowledgment ingestion as core implementation work, not cleanup: if you cannot quickly map inbound events to original payouts, reconciliation slows and exceptions become manual.

Direct bank connectivity can take real build-and-test time, sometimes up to six months for one bank, so this order reduces rework and ownership gaps early. Need the full breakdown? Read Platform Payout Cost Estimator for Wire, ACH, and Local Rails.

Design returns and NOC handling as a first-class operating system#

Treat returns and Notification of Change (NOC) handling as a core operating workflow, with named owners and clear release authority for corrected re-submissions.

If ownership stays ambiguous, one ACH item can be triaged three different ways by finance, ops, and engineering, with no single decision path.

Assign owners before the first exception spike#

Set decision rights before exception volume rises.

| Exception type | First owner | Decision | Required attachment |

|---|---|---|---|

| Return Reason Codes | Payments ops or finance ops | Confirm true return vs duplicate vs posting issue | Original batch ID, entry ID, camt.053 reference, reason code, SEC code |

Change Codes from Notification of Change (NOC) | Ops with data stewardship support | Identify source-record corrections needed | Original value, corrected value, date received, affected future batches |

| Corrected re-submission after NOC or fixable reject | Finance or treasury release owner | Approve whether corrected entry can be sent again | Evidence of correction, prior return/change event, approval record |

Keep one evidence chain per item: original payout record, related camt.053 event, SEC code (CCD, CTX, PPD, or IAT), and re-submission approval. Without that chain, you cannot reliably show whether data was corrected or the same bad instruction was sent again.

Make camt.053 the shared state source for exceptions#

Use

camt.053as the shared exception-state source across finance, ops, and engineering.

In U.S. ACH, operators transmit Nacha file formats within U.S. borders, and financial institutions translate them into ISO 20022 account statements for corporate clients.

Define explicit transitions such as submitted, statement-confirmed settled, returned, NOC received, correction pending, and corrected re-submitted. Keep scope clear too: Nacha's mapping tool is for ACH return and NOC information, not a complete bank statement mapping, so use it for exception truth and verify each returned item can be traced from batch entry to translated statement event without spreadsheet stitching.

Pause rollout when the pattern is still unclear#

Set an internal threshold for unresolved returns, and pause new corridor rollout when that threshold is exceeded until open items are categorized by SEC code.

This prevents broad "ACH failure" labels and forces root-cause separation.

| Case | Action or impact |

|---|---|

| Unresolved returns exceed an internal threshold | Pause new corridor rollout until open items are categorized by SEC code |

| Transport failures | Replay idempotently |

| Semantic rejects tied to account data, format content, or field completeness | Do not auto-replay |

Mandatory (M) field omitted | Causes rejection at the ODFI |

Required (R) field omitted | May be rejected at the RDFI |

Apply the same rule discipline to retries: replay idempotently for transport failures, but do not auto-replay semantic rejects tied to account data, format content, or field completeness. Nacha's guidance distinguishes correction cases from retry cases: omitting a Mandatory (M) field causes rejection at the ODFI, while omitting a Required (R) field may be rejected at the RDFI. Related reading: ACH Payment Processing Platforms for U.S. Collections and Payouts.

Compare ACH mapping and SEPA expectations without false equivalence#

A shared ISO 20022 surface helps with interoperability, but it does not create shared acceptance rules.

Use

pain.001to reduce formatting drift, then validateACHandSEPA Credit Transferagainst their own scheme and bank requirements before release.

On the U.S. side, the grounded scope is specific: Nacha's August 2023, Version 4.01 credit transaction guide maps U.S. ACH formats, with dedicated sections for CCD, CTX, PPD, and Outbound IAT, plus mapping detail for file header, company/batch header, and entry detail records. Treat that as mapping guidance, not a cross-scheme rulebook.

| Area | ACH + Nacha mapping focus | SEPA Credit Transfer expectations under EPC guidance |

|---|---|---|

| Primary use | Map U.S. ACH structures into pain.001 credit transfer content | Use pain.001-based initiation, but confirm acceptance behavior with your bank/provider |

| Rule control | Nacha manages ACH Network development, administration, and rules in the U.S. | Local scheme and bank implementation rules control acceptance and rejects |

| Practical implementation | Strong record-level mapping coverage, including separate Outbound IAT treatment | Re-check local usage rules before reusing U.S.-centric assumptions |

| Interoperability | Shared message structure can reduce translation overhead | Shared structure does not guarantee corridor-level pass rates |

Where pain.001.001.03 helps and where it does not#

If your providers support pain.001.001.03, aligning on one initiation version can simplify serializers, test fixtures, and operational comparisons across corridors.

That is an interoperability benefit, not a rule-equivalence guarantee.

Acceptance still depends on local scheme and bank validation. A structurally valid XML file can still fail for content, enrichment, or mandatory-field reasons in a specific corridor.

Constraints teams miss in practice#

Remittance Information is explicitly a named subsection in the Nacha mapping structure, but this section does not establish SEPA-wide limits. Treat remittance length and format behavior as provider-confirmed, corridor-specific configuration.

Do the same for XML character handling. Validate edge-case names and remittance text in your target bank/provider flow, then confirm what is preserved, normalized, or rejected in downstream outputs.

Known - Nacha's guide is a U.S. ACH mapping guide for

pain.001credit transfer content. - It includes detailed mapping coverage and separateOutbound IAThandling.

Unknown until sponsor bank/provider confirmation - Required or preferred

pain.001version in each SEPA corridor. - Corridor-specificRemittance Informationconstraints. - Bank/providerXMLcharacter validation and reject behavior.

If you are moving from ACH flows into euro payouts, make provider confirmation a release gate. Related reading: PIX vs. SEPA vs. ACH vs. SWIFT: Choosing the Right Payout Rail for Each Market.

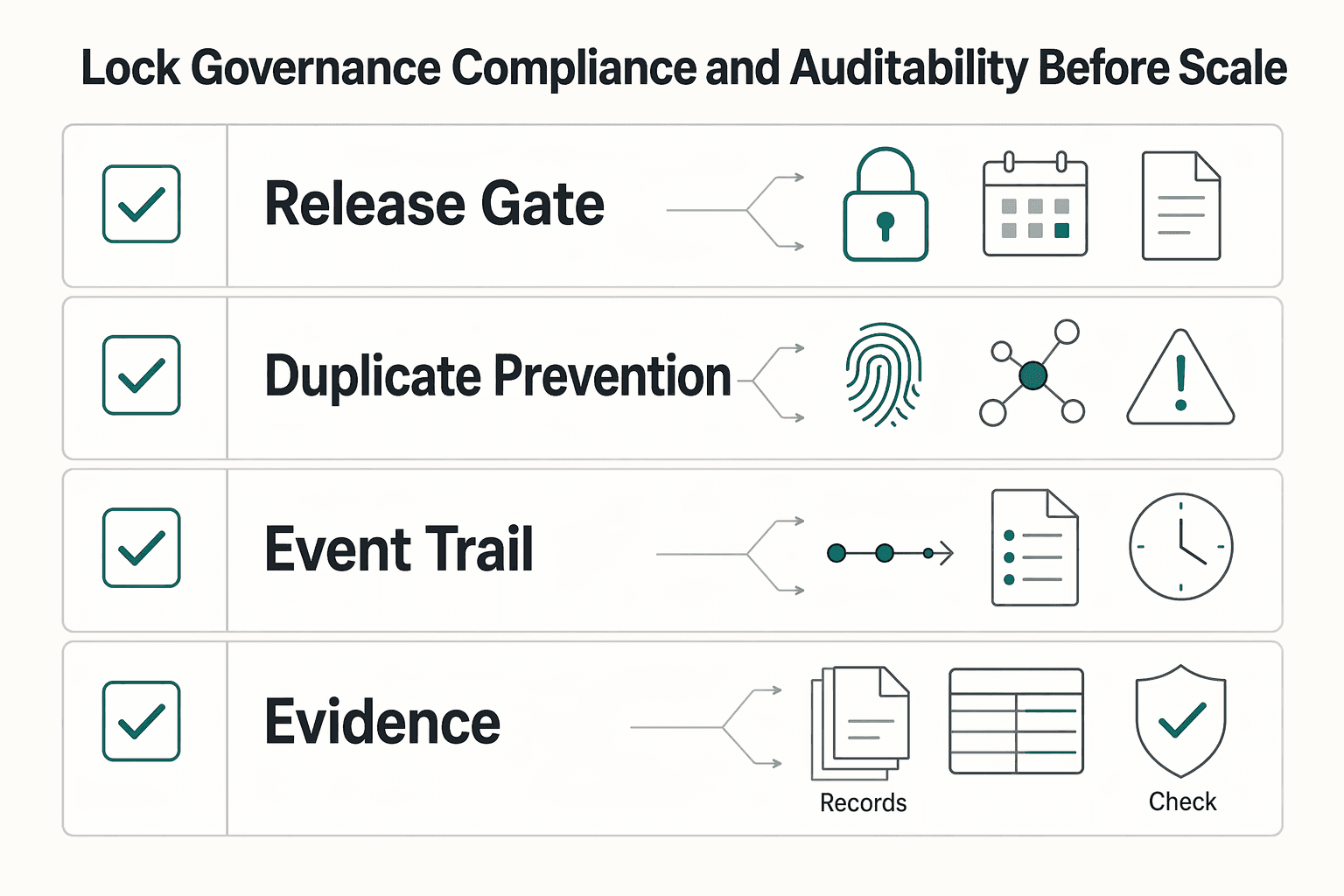

Lock governance, compliance, and auditability before scale#

Before you scale batch payouts, lock your internal control standard and validate it by market. Nacha has served as trustee of the ACH Network since 1974 and says it manages the network's development, administration, and rules, but that does not define your internal approval, duplicate-prevention, or audit model.

| Control area | What to define |

|---|---|

| Approval | Who approves each outbound pain.001, and when |

| Duplicate prevention | How you prevent duplicate submission, for example stable idempotency handling |

| Event trail | What event trail you retain from approval through downstream status artifacts, including camt.053 only if it is part of your reporting flow |

| Evidence export | How finance can export batch evidence without engineering intervention |

| Program-specific gates | Whether KYC, KYB, AML review, sanctions screening, or hold/release controls are pre-submit conditions |

Set your operating baseline in writing before higher volume:

- Define who approves each outbound

pain.001, and when. - Define how you prevent duplicate submission, for example stable idempotency handling.

- Define what event trail you retain from approval through downstream status artifacts, including

camt.053only if it is part of your reporting flow. - Define how finance can export batch evidence without engineering intervention.

Treat compliance gates the same way: make them explicit and program-specific. If your sponsor bank, program, or jurisdiction requires KYC, KYB, AML review, sanctions screening, or hold/release controls, make those pre-submit conditions, not post-submit cleanup.

Keep one market-level check before launch. Nacha's white paper states its views may not reflect every participating entity, so bank/provider confirmation should be a release gate for each corridor. We covered this in detail in Same-Day ACH for Platforms: How to Speed Up Contractor Payments Without Wire Transfer Fees.

Conclusion#

The practical path is not complicated: use pain.001 for credit payout initiation, pick CCD, CTX, PPD, or Outbound IAT on purpose, and treat scheme/version verification as part of launch scope, not later cleanup. Teams get into trouble when they build "generic ISO 20022 XML" first and assume the scheme details can be patched in afterward.

That is the main lesson from the Nacha material. Nacha describes its guides as guidance on applying ISO 20022 to U.S. ACH formats, not as legal advice, and it explicitly says knowledge of both XML and Nacha rules and formats is needed to interpret the mappings correctly. If you remember one operator rule from this article, make it this: bank acceptance and scheme rules should beat your internal assumptions.

A shared operating model across product, engineering, and finance ops matters because the handoff points are where most rework starts. Product decides what payout experiences and remittance data the business wants. Engineering turns that into pain.001 serialization and submission controls. Finance ops owns the day-two truth: whether the batch was accepted and whether beneficiary data needs correction. When those three groups use different labels for the same batch or do not agree on the relevant SEC code, you create reconciliation debt before volume even arrives.

Your next move should be a corridor-by-corridor readiness check. Keep it simple and evidence-based:

- Confirm the accepted

pain.001version with each sponsor bank or provider instead of assuming one version is universal. Nacha's older guide recommendspain.001.001.03, while the August 2023pain.001mapping PDF is labeledVersion 4.01, and Nacha also tells users to periodically make sure they have the most current version. - Decide the SEC code before file generation, not during exception triage.

CCD,CTX,PPD, andOutbound IATare explicitly named in Nacha's mapping guidance, so they should exist in your payout data model as first-class choices. - Record what you verified. A dated copy of the bank implementation guide, the accepted message version, and the corridor owner will save time when a file is rejected and nobody remembers which rule set was approved.

If you want a clean decision rule for launch, use this one: do not go live until you can prove which initiation format you are sending, which SEC code each batch uses, and which current bank requirement you validated for that corridor. That is what turns payout format selection from a documentation exercise into a predictable operating capability.

Frequently Asked Questions

What is the practical difference between `pain.001`, `pain.008`, and `camt.053` for a payout team?

For outbound payouts, pain.001 is usually the first file to care about because it is the credit payment initiation format. camt.053 is different because it is the bank-to-customer statement message structure used in the returns and Notifications of Change mapping context. pain.008 sits in the same Payment Initiation family, but its exact role for your flow should be confirmed against your bank or provider implementation specs.

Is `pain.001.001.03` mandatory for `ACH`, `SEPA Credit Transfer`, or only certain bank implementations?

Do not treat pain.001.001.03 as universally mandatory. Nacha says that version is the one it recommends, and says its approach is aligned with EPC SEPA implementation guidance, but that is still not the same as every bank or corridor requiring it. The practical rule is to use pain.001.001.03 as your starting assumption, then confirm the accepted version with your sponsor bank or provider for each market.

How do `CCD`, `CTX`, `PPD`, and `Outbound IAT` change payout file design and reconciliation effort?

They are not just labels for reporting. Nacha’s pain.001 credit mapping guide is explicitly about mapping U.S. ACH formats for CCD, CTX, PPD, and Outbound IAT, so your file generation and validation rules should branch by SEC code instead of assuming one generic ACH payout shape. A good checkpoint is to make the SEC code part of batch metadata before serialization, then test reconciliation outputs separately for each code.

Where do `Return Reason Codes` and `Change Codes` appear, and how should ops teams act on them?

In the Nacha mapping material, those appear in the camt.053 returns and NOC context. That is where your ops team should look for post-submission events that explain why an item came back or what account information needs correction. Treat them differently: a return reason usually means stop any blind replay and decide whether the payment is fixable, while a change code should open a controlled update to beneficiary master data with an audit note before the next batch.

Can we launch with `pain.001` first and add `camt.053` later without creating reconciliation risk?

The provided mapping guidance does not prescribe a rollout sequence. If you launch pain.001 first, you still need a reliable day-one feed for settlement outcomes, returns, and NOCs (whether camt.053 or an equivalent provider statement feed), or reconciliation risk increases. A practical minimum is an evidence pack per batch that links the original file, transmitted file fingerprint, provider reference, and each return or change event received.

When should we enable `Same Day ACH`, and what has to be true operationally before doing it?

The provided material does not define Same Day ACH cutoffs, fees, or readiness thresholds. Set go-live criteria with your bank or provider operating rules, and make sure return and NOC handling is already stable before you compress timelines.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 7 external sources outside the trusted-domain allowlist.

- websail-fe.cs.northwestern.edu/downloads/OTyper_data_aaai18/FIGER_data/word...trusted

- docs.oracle.com/cd/F52784_01/psft/pdf/fscm92fgat-b022022.pdfexternal

- docs.oracle.com/cd/E27605_01/fscm91pbr2/eng/psbooks/fgat/htm...external

- documentation.sepamail.org/images/e/ea/ISO20022_usage_guide_V3.pdfexternal

- instantpaymentguide.com/comparing-ach-rtp-and-fednowexternal

- iso20022.org/sites/default/files/2020-03/ISOInitiatives_J...external

- kansascityfed.org/Payments%20Conferences/documents/4068/2012-c...external

- kyriba.com/resource/what-are-bank-reporting-and-payment...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

SEPA Instant Credit Transfer for Euro Payouts

SEPA Instant Credit Transfer is real, fast, and operationally useful, but it is not an automatic yes for every euro payout program. The practical question is this: where does instant speed create enough product value to justify the extra validation work before launch?

Payout Method Comparison Tool for Platform Operators Across ACH, SEPA, PIX, and UPI

Use this comparison as a decision aid, not a ranking. The point is to help you choose the right payout rail mix for marketplace payouts across ACH, Wire transfer, SEPA, SEPA Instant, PIX, UPI, and SWIFT based on operating fit, not headline speed alone. A strong choice usually balances speed, cost, geography, and payout experience.

PIX vs. SEPA vs. ACH vs. SWIFT for Platform Payout Decisions by Market

If you own payouts, you do not need another glossary. You need a fast way to choose the rail that fits the job, then avoid the failures that show up after launch. This payout rail comparison is for finance, ops, and engineering teams that care less about labels and more about whether money lands on time, statuses reconcile cleanly, and exceptions stay out of inboxes.