Quick Answer

Choose by corridor, then urgency: PIX for Brazil-local payouts, SEPA Instant for urgent euro disbursements when that path is live, ACH or Same Day ACH for U.S.-domestic cycles, and SWIFT when no local route fits. The practical decision is not just speed; it is whether statuses, rejects, and fallback behavior can be reconciled without manual cleanup. Confirm beneficiary data requirements and provider status reporting before your first production batch.

How to Choose the Right Payout Rail by Market#

If you own payouts, you do not need another glossary. You need a fast way to choose the rail that fits the job, then avoid the failures that show up after launch. This payout rail comparison is for finance, ops, and engineering teams that care less about labels and more about whether money lands on time, statuses reconcile cleanly, and exceptions stay out of inboxes.

At the routing level, the question is simple: which network carries this payment from origin to destination? In practice, that choice is where teams lose hours. ACH is a domestic U.S. rail. SEPA covers euro payments across 41 countries. SEPA Instant targets funds in under ten seconds when the instant path is actually available. SWIFT is a global messaging layer used by 11,500+ institutions in 200+ countries, which is why it still matters when local options do not fit the corridor.

The hard part is not naming the rail. The hard part is choosing one that survives production reality. Cross-border payments can involve multiple financial institutions and regulatory jurisdictions. That creates more places for timing, status, and data quality to drift. That is why this article focuses on the decisions that break in live operations: corridor fit, cutoff sensitivity, beneficiary data quality, exception handling, and who owns reconciliation when provider status and your internal ledger disagree.

A few rules matter from the start. If money never leaves the U.S., ACH is generally cheaper and easier than SWIFT, so do not default to a cross-border route out of habit. If you are sending euros inside the SEPA area, separate standard SEPA Credit Transfer from the instant option because urgency changes both customer expectations and operational handling. If the destination market has a strong local rail, check that option before you accept the overhead that comes with cross-border routing.

One verification step will save you pain later: confirm corridor support, cutoff behavior, and status reporting with your bank or payout provider before launch, not after your first failed batch. One common failure mode is assuming "available" means "operationally reliable." It does not. A rail may be technically supported but still create manual work through rejected beneficiary details, missed cutoffs, delayed confirmations, or reconciliation gaps.

The goal here is practical: help you choose by market, urgency, and operational risk in minutes, then execute with fewer failed payouts, fewer manual investigations, and fewer surprises between finance and engineering.

At a glance comparison of PIX SEPA ACH and SWIFT#

Start with the rail that matches the destination market and payout shape: local instant rails can outperform correspondent routing on speed and fee drag, while SWIFT remains necessary for reach in long-tail or complex cross-border corridors.

| Rail | Market scope | Settlement pattern | Cutoff sensitivity | Fee pattern | Return risk | Best-fit payout use case | Best used when | Avoid when |

|---|---|---|---|---|---|---|---|---|

| PIX | Brazil | Can settle in seconds on local instant paths | Depends on bank/provider/program | Often lower fee drag than correspondent routing on supported routes | Implementation-dependent; beneficiary/program errors still create exceptions | Brazil-local contractor, seller, or wallet-to-bank payouts where speed matters | You are paying out in Brazil and your provider supports PIX for that program | You need corridors outside Brazil, only have correspondent routing, or have not validated live support/status handling |

| SEPA Instant / SEPA Credit Transfer | Eurozone / SEPA area | SEPA Instant can settle in seconds; standard SCT is usually same-day or next-day in most schemes | SEPA Instant is less cutoff-driven when available; SCT is more cutoff-sensitive | Often lower and cleaner than correspondent routing for in-footprint euro payouts | Mostly tied to data quality and whether instant support is actually available | Euro payouts inside the SEPA area, including recurring and urgent disbursements | You are sending euros within SEPA and routing urgent vs standard payouts deliberately | You assume all SEPA corridors are instant-capable, or need a country/currency outside SEPA |

| ACH / Same Day ACH | United States | Same-day or next-day in most schemes | Cutoff-sensitive, especially around processing windows | Usually cost-efficient for domestic U.S. volume | Scheme returns and data errors can add ops work | Predictable domestic U.S. batch payouts (contractors, creators, marketplace sellers) | Your payout is U.S.-domestic and low unit cost matters more than real-time delivery | You need international reach or strict real-time expectations |

| SWIFT | Global cross-border bank corridors | Commonly 1-5 business days, depending on corridor conditions | High; timing depends on corridor, banks, and intermediaries | Fee-accretive, with possible correspondent deductions | Higher exception/reconciliation risk across multiple institutions/jurisdictions | Long-tail cross-border payouts, one-off high-value transfers, and corridors without usable local rails | No local rail fits, or payment complexity/value makes correspondent routing the practical option | A local instant or domestic rail already fits and simpler timing/cost/reconciliation is the priority |

| Coverage caveat | All markets | Coverage and timelines vary by bank, provider, and program | Confirm real cutoff behavior before launch | Pricing behavior varies by path/provider | Reject/return patterns vary by implementation | Use corridor-level verification, not country-count marketing | You have validated the actual settlement path, statuses, and fallback rail | You are assuming "supported" means production-ready |

Local instant rails can beat SWIFT when the market and program support them. SWIFT still matters when reach is the constraint.

Before launch, verify what rail is actually used under the hood for each corridor, then confirm cutoff behavior, status reporting, and reject/return handling. That check is what prevents "supported" from turning into manual ops work after go-live.

Related: A Guide to SEPA Transfers for European Freelancers.

What each rail is good at in real payout operations#

Pick rails by operational role, then verify corridor reliability before launch. SWIFT is the cross-border reach layer, ACH is the U.S. domestic rail, SEPA covers euro payouts in its footprint, and PIX is the Brazil-local instant path to check first for Brazil disbursements.

Operator view of the four main rails#

| Rail | Best for | Cited detail | Caveat |

|---|---|---|---|

| SWIFT | Cross-border bank reach when no local rail fits | 2-5 days; bank fees can run US$30-US$75 | Correspondent-fee drag possible |

| ACH | U.S.-only payouts where cost and predictable domestic operations matter | $0.26-$0.50 per transaction; one to three business days | Same Day ACH can clear up to US$1 million but is not an instant rail |

| SEPA / SEPA Instant | Euro payouts | SEPA Instant can settle in seconds when supported; standard SCT remains the planned-cycle path | Treat standard SEPA Credit Transfer and SEPA Instant as different operating paths |

| PIX | Brazil-local payouts when speed matters | Use only after confirming the provider is actually using PIX for the program | Test status handling and rejects before scaling |

- SWIFT: Best when no local rail fits and you need cross-border bank reach. In cited ranges, transfers can take 2-5 days and bank fees can run US$30-US$75, with correspondent-fee drag possible.

- ACH: Best for U.S.-only payouts where cost and predictable domestic operations matter. Cited ACH ranges are $0.26-$0.50 per transaction with settlement in one to three business days; Same Day ACH can clear up to US$1 million, but it is still not an instant rail.

- SEPA / SEPA Instant: Best for euro payouts, but treat standard SEPA Credit Transfer and SEPA Instant as different operating paths. SEPA Instant can settle in seconds when supported; standard SCT remains the planned-cycle path.

- PIX: Best for Brazil-local payouts when speed matters to recipient experience. Confirm your provider is actually using PIX for your program, then test status handling and rejects before scaling.

SEPA Instant is not just faster SEPA#

The key difference is operational certainty, not just speed. If you promise near-immediate euro payouts, confirm corridor by corridor that the instant path is enabled for your provider, program, and beneficiary bank. "SEPA supported" alone does not confirm that your production flow is running on SEPA Instant.

Do not generalize one instant rail to another#

FedNow, Faster Payments, UPI, SPEI, PIX, and SEPA Instant are all local instant networks that can settle in seconds, but they do not share identical coverage, participation rules, fallback behavior, or exception patterns. Some rails are domestic by design, while SWIFT is a global overlay. Availability claims are not enough; stress-test performance and exception handling in production conditions.

If you want a deeper dive, read What Are Payment Rails? ACH Wire SEPA and Real-Time Networks Compared.

Decision rules by corridor urgency and payout amount#

Route by corridor first, then use urgency and payout amount to break ties. If destination is Brazil and speed matters, route to PIX first. If payout is in euros within the SEPA footprint, use SEPA Instant only when that path is live for the bank and corridor. For U.S. domestic planned cycles, use ACH or Same Day ACH. If no local route fits, use SWIFT for reach.

Default routing rules#

Use these as first-choice rules, not settlement guarantees. Transfer speed varies by provider and payment method, and quoted windows can miss compliance checks, correspondent hops, and weekend gaps.

| Scenario | First choice | Grounded note |

|---|---|---|

| Brazil payout, speed matters | PIX | Confirm your provider is routing over PIX for your program and how rejected statuses feed back into your ledger |

| Euro payout, urgent | SEPA Instant | SEPA covers euro payments across 41 countries; the instant route targets funds in under ten seconds when the participating path is enabled |

| U.S. domestic payout, predictable cycle | ACH / Same Day ACH | Use ACH for routine batches and Same Day ACH when same-day is required; the cited Same Day ACH limit is US$1 million |

| No local route or cross-border reach is required | SWIFT | Connects 11,500+ institutions in 200+ countries, with higher operational complexity across institutions and jurisdictions |

The key operational check is corridor-level path verification, status events, and fallback behavior. "SEPA supported" or "bank transfer supported" is not enough when urgent payouts depend on an instant variant.

Scenario contrasts#

| Payout job | Best first choice | Why it usually fits | Red flag that changes the choice |

|---|---|---|---|

| Recurring contractor payouts | ACH for U.S. domestic, standard SEPA or SEPA Instant for euro payouts, PIX for Brazil | Predictable schedules usually fit local rails and simpler reconciliation | Missing beneficiary data, cutoff sensitivity, or a payout promise that requires immediate receipt |

| Marketplace seller payouts | PIX in Brazil, SEPA Instant where supported, Same Day ACH for faster U.S. funding | Seller experience is often sensitive to payout timing and visibility | Instant path is unavailable, or exception rates are high enough to erase the speed benefit |

| Treasury-like large transfers | Same Day ACH only when domestic U.S., same-day is sufficient, and amount is within the 1 million dollar limit; otherwise SWIFT is often the fallback for cross-border reach | Amount, bank support, and jurisdiction often matter more than consumer-style speed | Choosing the fastest rail without checking amount limits, bank acceptance, and internal controls |

A practical rule: contractor and seller flows usually start with local rails; treasury-like transfers often prioritize reach, amount handling, and control over raw speed.

When the first-choice rail is unavailable#

Set fallback policy before launch instead of deciding at payment time. Define your retry approach, allowed alternate rail by corridor, and the internal override path for exceptions.

If PIX or SEPA Instant is unavailable, choose based on payout promise. If later arrival is acceptable, downgrade to a non-instant local route where available. If delay changes the commercial outcome, hold for review instead of auto-routing to a higher-cost or harder-to-reconcile path.

Fastest is not always lowest risk. Instant rails reduce waiting time but also reduce time to catch bad beneficiary data before submission. SWIFT solves reach, but cross-border payments can involve multiple institutions and jurisdictions, which increases exception and reconciliation workload. A clear routing plan improves speed, reduces returns, and keeps reconciliation cleaner only when fallback and status handling are part of the rail decision.

Want a quick next step for "pix sepa ach swift payout rail comparison"? Try the free invoice generator.

Hidden costs and failure modes competitors gloss over#

The headline fee is rarely your true payout cost. In practice, costs rise in exception handling: intermediary deductions, returns and holds, status drift, and retries that are not tightly controlled.

| Rail | Hidden cost driver | What to verify before launch | What breaks when controls are weak |

|---|---|---|---|

| SWIFT | Correspondent-bank intermediary chains can add fees and delays | Confirm whether the recipient must receive an exact amount, and whether reporting shows deductions and final credited amount | Contractors receive less than expected, finance must explain short payments, and gross-to-net reconciliation fails |

| ACH / Same Day ACH | Exception handling overhead can outweigh base rail savings | Define how returns, holds, and status changes flow into your ledger, who owns review, and when resubmission is allowed | Manual queue work grows, payouts are delayed, and teams repeatedly investigate "sent but not received" |

| SEPA / PIX | Bad beneficiary data can cause rejection and rerouting work | Validate beneficiary fields before submission and confirm whether failures are immediate or asynchronous | Support sees one status, finance sees another, and unresolved items trigger avoidable retries |

SWIFT makes hidden cost visible fastest. Traditional cross-border payouts use correspondent banking (bilateral nostro/vostro accounts), with SWIFT as the messaging layer, and intermediary chains can introduce significant fees and delays. If the recipient must receive a precise amount, check net credited amount, not only "payment sent."

ACH, SEPA, and PIX usually hurt most when exception ownership is unclear. Bad beneficiary data, cutoff misses, holiday mismatch, asynchronous status drift, and return/hold handling can all push work into manual investigation and rerouting.

Across all rails, weak controls produce the same outcome: delayed contractor payouts, reconciliation backlog, and duplicate-attempt risk. Use idempotent retries with idempotency keys, and do not send a fresh attempt until you verify the prior reference and latest provider status.

We covered related bank-identifier mechanics in What is an IBAN and How is it Different from a SWIFT Code?.

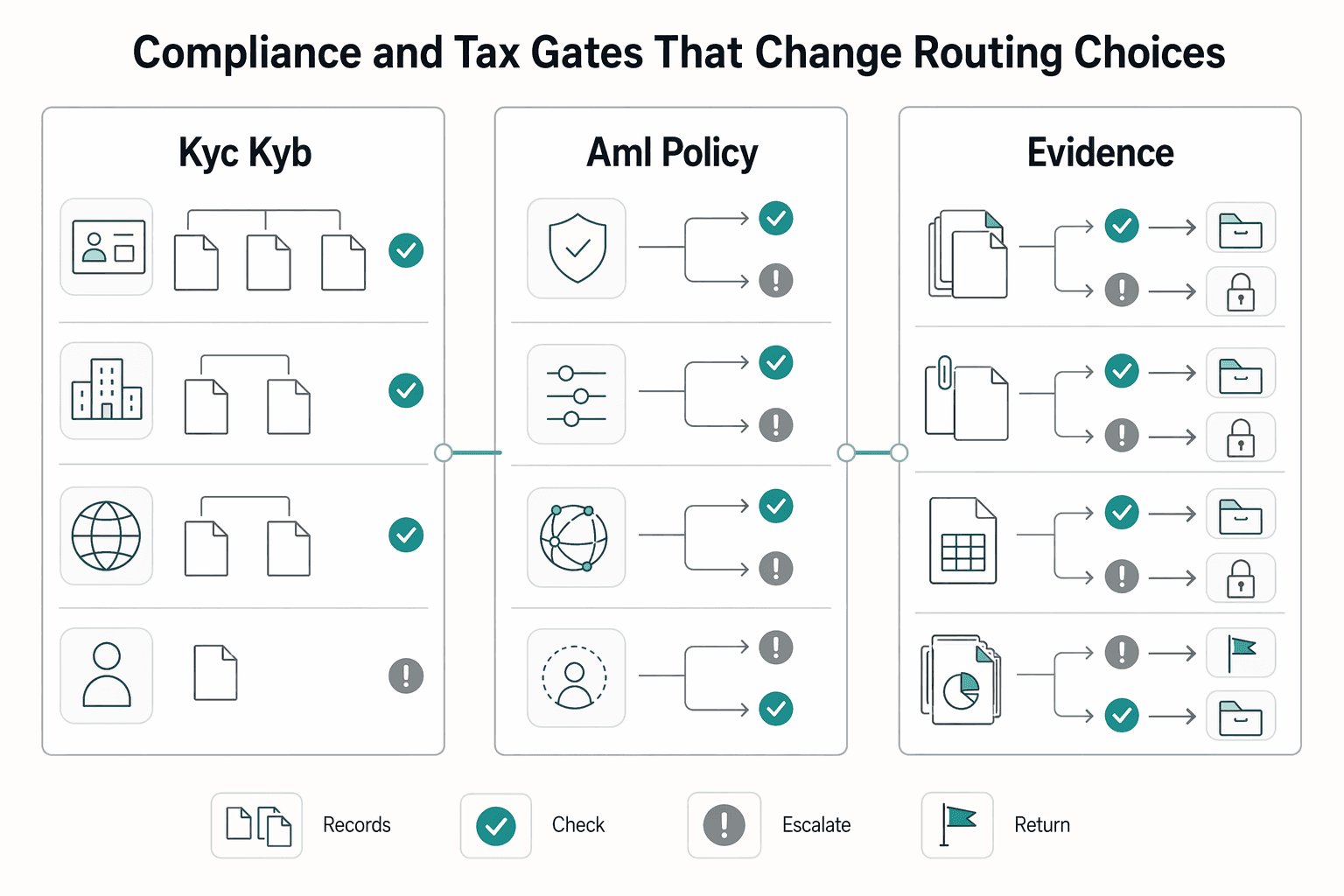

Compliance and tax gates that change routing choices#

Routing only matters after approval eligibility is clear. If KYC, KYB, AML, or a market-level policy check has not cleared, PIX, SEPA, ACH, or SWIFT should not be released.

Use a pre-payout decision first: is this payee, entity, corridor, and payout purpose approved for your program right now? Providers may expose multiple rails, but releasability depends on your onboarding state and policy result.

| Gate | What it blocks | Verify before release | Common failure mode |

|---|---|---|---|

| KYC / KYB | Payee or business not fully approved | Current approval status tied to the beneficiary record | Bank details exist, so ops assumes payout-ready while identity review is still pending |

| AML / policy screening | Payout held for review or not approved under program rules | Latest policy result and whether the hold is temporary or final | Team reroutes to another rail instead of resolving the compliance hold |

| Tax documentation readiness | Program-required tax artifacts are missing or outdated | Required artifact on file and linked to paying entity and payee type | Manual release happens first, reporting cleanup happens later |

| Audit evidence | Inability to defend why a payout was sent | Approval trail, policy result, payout reference, and reconciliation export retained together | You can prove money moved, but not why it was allowed |

Tax artifacts are usually readiness gates, not rail features. If your program requires forms such as W-8 or W-9 before release, or depends on 1099 workflow readiness, that requirement can block payout even when beneficiary bank data is valid.

For cross-border context, recipient tax obligations can still apply regardless of rail choice. IRS guidance says the foreign earned income exclusion applies only to a qualifying individual with foreign earned income, and that person still files a tax return reporting the income. Under the physical presence test, this includes 330 full days in a 12-month period, and the days do not have to be consecutive. FBAR is separate reporting context for foreign bank and financial accounts.

Keep the evidence pack simple and complete: approval trail, exact policy result at release time, provider payout reference, and reconciliation export with final status. If a payout is escalated or manually approved, attach that reason before release.

For a step-by-step walkthrough, see The S-Corp Election vs. C-Corp: A Tax Comparison for US-Based Agencies.

How to implement routing without breaking reconciliation#

Implement routing as one ordered chain with one payout identity from normalization to final reconciliation; that is what keeps execution fast without losing auditability.

Start by normalizing beneficiary data before rail selection. Run eligibility and compliance checks against that normalized record, then choose the rail only when the payout is both data-complete and approval-complete. Execute idempotently, ingest webhook or file updates, and reconcile your ledger to the provider's final status and export.

Before a payout moves from submitted to paid, require a match across three fields: internal payout ID, provider payout reference, and latest provider status. If any one is missing, treat it as an active reconciliation gap now, not a cleanup task for later.

Map standards to the execution path#

Payment formats shape both execution and auditability. Standardized formats support clearer audit trails and lower error risk, so they should be mapped directly to your payout state model.

| Execution path | Common format or message family | What to persist with the payout record | Common failure mode |

|---|---|---|---|

| U.S. ACH | NACHA | Internal payout ID, file or batch identifier, provider reference, latest status | File accepted upstream, but ledger marked paid before downstream confirmation |

| Euro payouts including SEPA Credit Transfer | ISO 20022 / PAIN patterns | Internal payout ID, message identifier, provider reference, returned status or rejection detail | Rejection arrives later and cannot be matched cleanly to the original instruction |

| API-led local or cross-border path | Provider API payload plus webhook events | Internal payout ID, request identity, webhook event IDs, final reconciliation export | Timeout or replay triggers a second send because first acceptance is unclear |

For format-level context, see Batch Payout File Formats: NACHA ACH ISO 20022 PAIN and SEPA Credit Transfer Explained.

Even when a cross-border payments API abstracts routing, FX, and compliance, your internal record model still has to handle asynchronous state updates.

Retry and replay rules that prevent duplicates#

Treat retries as verification first, not blind resend. If an API call times out or a file response is unclear, check provider acceptance, webhook events, or reconciliation export before sending again.

Handle webhook replays as updates to an existing payout record, never as new payouts. Keep compliance status codes and reason details on the same payout record so ops can resolve exceptions and finance can see whether a hold is tied to sanctions, PEP, AML, or destination-country screening.

Recommended ownership split#

One workable split is: finance owns policy and approvals, ops owns exception queues and manual review, and engineering owns event integrity, state mapping, and idempotent execution. The point is clear accountability for whether a payout was blocked by policy, failed in transit, or duplicated on retry.

| Team | Owns |

|---|---|

| Finance | Policy and approvals |

| Ops | Exception queues and manual review |

| Engineering | Event integrity, state mapping, and idempotent execution |

Use one rule across corridors: rail choice can vary, but payout identity, evidence, and reconciliation controls should stay consistent.

Related reading: How to Use a SWIFT MT103 to Trace a Delayed Wire Transfer.

Prelaunch checks for finance ops and engineering#

Launch only when each corridor has a documented primary rail and fallback, because there is usually more than one way to move money from payer to payee and the fallback can materially change outcomes.

| Check area | What to verify before first production batch | Red flag |

|---|---|---|

| Corridor fit and fallback | For each payer-to-payee corridor, record the intended rail path (for example PIX, SEPA, ACH, or SWIFT) and the fallback path. Account for the fact that cross-border execution can involve several rails in sequence. If fallback uses SWIFT, note that timing can be 1-5 business days (corridor-dependent) and costs can be higher due to bank fees and FX spreads. | Treating rail availability as a single yes/no decision with no corridor-specific fallback impact |

| Tradeoff clarity | Confirm the launch decision explicitly weighs cost, speed, working capital, and customer experience. Include risk tradeoffs such as disputes and fraud risk in the same decision record. | Choosing a path on speed alone, then discovering unacceptable cost or risk in live traffic |

| Test readiness | Run prelaunch tests that cover both standard and exception outcomes so teams know how to handle non-happy-path payouts before go-live. | First production issues become the first time finance, ops, and engineering align on exception handling |

| Shared traceability | Ensure finance, ops, and engineering can trace each payout decision and outcome through one consistent internal record. | Teams can confirm money movement happened, but cannot clearly explain path choice or handling decisions |

The practical launch rule is simple: if a fallback rail changes timing, cost, risk, or customer experience, treat it as part of the product decision, not an edge case.

Conclusion#

The practical answer is simple: choose by corridor fit first, urgency second, and operational risk third. Headline coverage is not a routing strategy. A rail that looks broad on paper can still create slower settlement, higher fees, or harder reconciliation once you are in production.

That is the real takeaway from this comparison. Use local rails where the corridor and your program genuinely support them, then escalate only when the payout job requires it. For euro payouts, SEPA gives you a defined regional path across 41 countries, and the instant variant is built for a very different promise than standard credit transfer, with a target of under ten seconds. SWIFT still matters for cross-border reach because it is used by 11,500+ institutions in 200+ countries. But that reach comes from a messaging layer tied to correspondent banking, not from a guarantee of a simple or cheap funds path.

That distinction matters more than most teams expect. Cross-border payments are still widely described as slow and expensive, and long intermediary chains can add both delay and fees. Many markets now have fast domestic electronic rails, but that does not remove cross-border constraints. So when a viable domestic route exists for your actual corridor and provider setup, treat that as your starting point rather than your fallback. If no local route exists for the actual origin, destination, and provider setup, then SWIFT becomes the necessary choice, not the default choice.

The operator move is to keep your routing logic neutral and checkable. Build a corridor matrix that names the primary rail, the approved fallback, the beneficiary data you must collect, and the status evidence you need back from your provider to reconcile the payout cleanly. One useful checkpoint is verifying that the provider reference and your internal payout ID stay linked through the final payout state and into your reconciliation export. If that link breaks, finance may need to investigate exceptions by hand, even when the payment itself eventually lands.

Rollout should be phased, not all at once. Confirm coverage and controls per program. Test a small set of real corridors first. Assign clear ownership for fallback decisions and reconciliation quality. The common failure mode is not choosing the wrong rail in theory. It is assuming rail availability means rail reliability, then discovering too late that returns, delays, and reconciliation outcomes can differ by path.

If you want a quick second pass on corridor options, use a neutral comparison tool and keep the decision rules tighter than the marketing copy. Start with the Payout Method Comparison Tool: ACH Wire SEPA PIX UPI and More for Platform Operators.

Frequently Asked Questions

Which rail should I choose first for contractor payouts in Brazil?

Start by checking whether your provider offers a viable local rail path for that Brazil corridor, then design your fallback. For contractor payouts, the practical rule is local rail first, fallback second. Confirm the exact beneficiary data you need on each path, then document what happens if the primary rail is unavailable for that payer, provider, or payee bank. The red flag is treating a cross-border fallback like a minor routing change when it can change timing, fees, and reconciliation evidence.

When should I use SWIFT instead of local rails like PIX or SEPA Instant?

Use SWIFT when the payout is cross-border and you do not have a viable local rail path for that origin-to-destination pair. SWIFT has broad reach across 11,500+ institutions in 200+ countries, but it is a messaging network, not the mechanism that directly moves funds. Intermediary banks can add both time and deductions. If you choose it, make sure ops can capture the provider reference and explain why the received amount may differ from the sent amount.

What changes operationally between SEPA Instant and SEPA Credit Transfer?

The big change is your payout promise and exception handling, not just speed. SEPA covers euro payments across 41 countries, and the instant path targets funds in under ten seconds. Instant schemes are typically designed for 24/7/365 processing, while standard SEPA Credit Transfer can be more exposed to cutoffs and batch timing. Before launch, test how your provider reports accepted, completed, and failed states on each path so finance is not reconciling one rail as if it behaved like the other.

How do I decide between ACH and SWIFT for U.S.-origin payouts?

If the payout starts in the United States and stays domestic, start with ACH because it is a domestic rail built for that job. Move to SWIFT when the destination is outside the U.S. or when the corridor requires cross-border bank messaging rather than domestic account-to-account transfer. The failure mode to watch is assuming a U.S. sender automatically means ACH, even when the payee account and settlement path make it a cross-border payment.

Is Same Day ACH enough for urgent payouts, or should I use an instant rail?

Same Day ACH can be enough when "urgent" really means same business day and your payout fits the cited 1 million dollar limit. If you need funds movement in seconds rather than later that day, evaluate an instant domestic option such as FedNow where your provider and program support it. Check this before promising timing to contractors, because domestic rail availability is not uniform across every bank and provider.

What minimum checks should I run before enabling a new payout corridor?

At minimum, lock a corridor-level decision record with a primary rail and named fallback, then verify the required beneficiary fields for both. Run one happy path test, one rejection or return, and one delayed or held case. Confirm each can be matched back to your internal payout ID and provider reference. If you cannot trace final status through to reconciliation, the corridor is not ready for production.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- congress.gov/119/crec/2025/12/17/171/213/CREC-2025-12-17-...trusted

- fincen.gov/report-foreign-bank-and-financial-accountstrusted

- govinfo.gov/content/pkg/GPO-CRECB-1967-pt15/pdf/GPO-CREC...trusted

- hbs.edu/ris/download.aspxtrusted

- hbs.edu/ris/Publication%20Files/Du_Huang_Scharfstein...trusted

- irs.gov/individuals/international-taxpayers/figuring...trusted

- irs.gov/individuals/international-taxpayers/foreign-...trusted

- jud.ct.gov/LegalResources/Docs/LJDocs/CTReports/FullVol...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Payout Method Comparison Tool for Platform Operators Across ACH, SEPA, PIX, and UPI

Use this comparison as a decision aid, not a ranking. The point is to help you choose the right payout rail mix for marketplace payouts across ACH, Wire transfer, SEPA, SEPA Instant, PIX, UPI, and SWIFT based on operating fit, not headline speed alone. A strong choice usually balances speed, cost, geography, and payout experience.

Batch Payout File Formats for NACHA ACH, ISO 20022 PAIN, and SEPA Credit Transfer

A workable batch payout strategy starts with one blunt fact. Saying a provider "supports ISO 20022" is often not enough to build against. You need to separate the message standard from the payment scheme, then confirm exactly what your bank or processor will accept in production.

What Are Payment Rails? ACH Wire SEPA and Real-Time Networks Compared

For platform operators, rail choice is an operating decision, not just a glossary term. It affects payout speed, exception handling, and how much cleanup your support and finance teams inherit.