Quick Answer

Use a stage-based stack. At seed stage, move from Microsoft Excel to system requisition approvals, AP invoice control, and payout status visibility; at growth, add procurement intelligence and orchestration only when exception queues and retry failures climb; by Series C through IPO, require traceable records from request to reconciliation. Keep one hard checkpoint before any expansion: finance must be able to pull approval history, provider references, and final payment outcomes for one transaction without manual re-entry.

Procurement stack choices get expensive fast once payouts and compliance scale#

If you run a marketplace, contractor, or creator platform with cross-border money movement, your stage can matter more than feature count. Use what gives you control now, and defer added overhead until you need it. Then watch for upgrade triggers that show your current stack is no longer enough.

- Start with stage, not vendor shortlists

Early teams may prioritize tighter approvals, clearer payout visibility, and exportable records before they need a broad procurement suite. Growth teams may need faster exception handling and clearer ownership across finance, product, ops, and engineering. This is a stage-based decision guide for platform operators, not a generic software roundup.

- Deploy the minimum stack that proves control

Early on, that can mean a lightweight purchasing and approval layer, disciplined accounts payable checks, and a payout setup you can verify lane by lane. If feature demos are driving the decision instead of traceability, you may be overbuying. The first checkpoint is not "does it integrate?" but "can you tie a request, approval, payment instruction, provider status, and reconciliation artifact together without asking three teams for screenshots?" Deploy what gives you operational proof, not the widest feature map.

- Defer expansion layers until the trigger is real

You may be able to wait on deeper procurement intelligence, broad automation, or consolidation plays until volume, exception rates, or audit pressure justify them. One failure mode is adding point tools to fix approval delays when the real issue is missing payout status visibility or weak routing rules between AP and payments ops. If approval latency rises at the same time payment failures or manual retries rise, that can be an upgrade trigger. If teams are still re-keying data between purchasing, AP, and payouts, your stack may already be too thin for the risk you carry. Defer tools that optimize around a broken control layer.

- Validate market and rail constraints before you commit

Cross-border payouts are conditional, not automatic. Provider qualification can determine whether your platform can support them, and where connected accounts are available can depend on your business location and the features you enable. For marketplace models, payment methods also need explicit configuration before users can start processing. The detail that matters most is mundane but decisive. Confirm country availability, feature-dependent coverage, and payment-method setup in the implementation model you actually plan to launch, not in sales conversations. The right stack is constrained by market coverage, compliance programs, and rails, so the same design will not work uniformly across every country or program.

That is the lens for the rest of this guide: control first, then scale, with upgrade decisions tied to evidence rather than tool sprawl.

Related: Finance Automation and Accounts Payable Growth: How Platforms Scale AP Without Scaling Headcount.

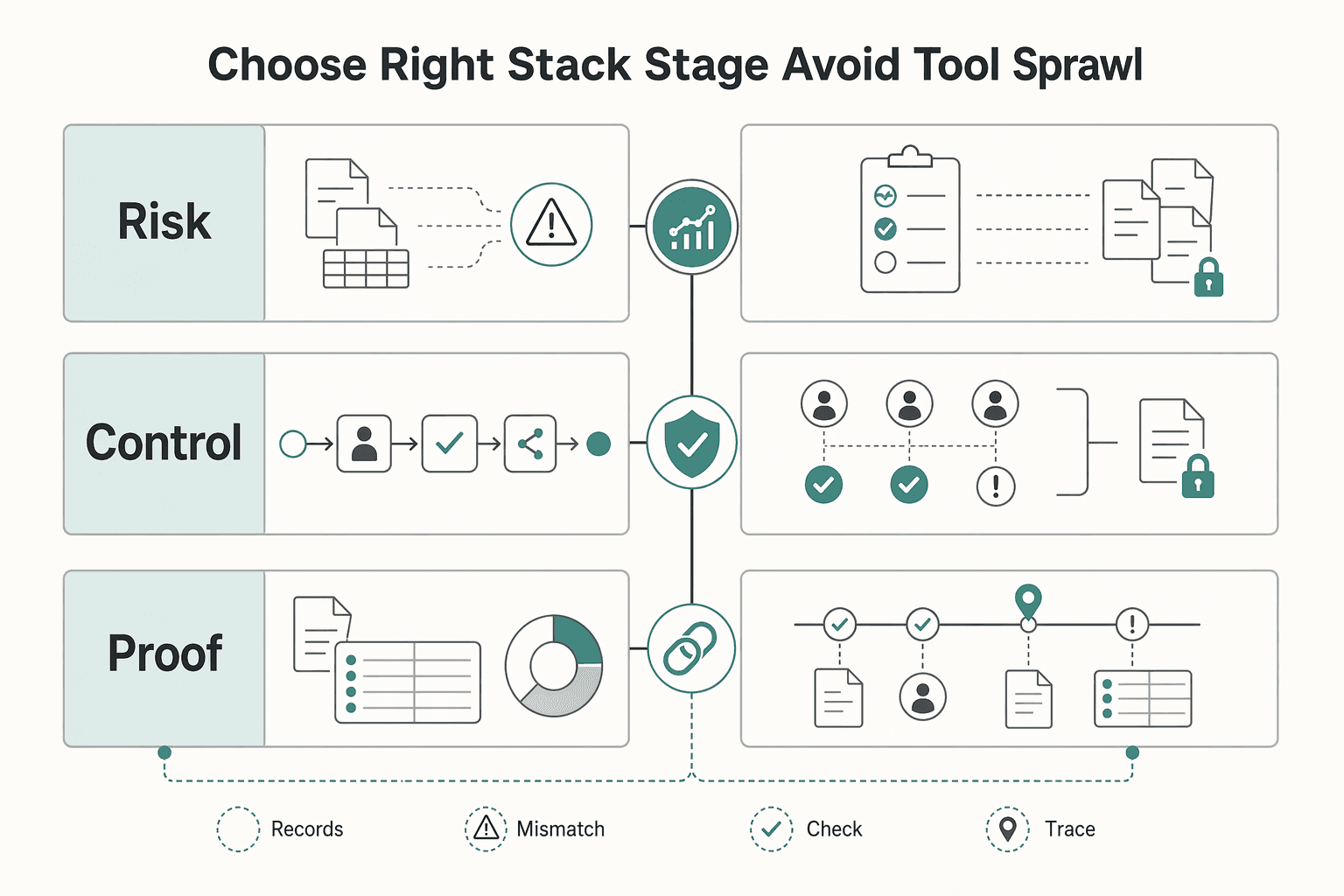

How to choose the right stack for your stage and avoid tool sprawl#

Choose the smallest stage-fit stack that gives you clear request-to-payment control, then add tools only when they close a specific gap. There is no one-size-fits-all architecture, so prioritize end-to-end operation over feature count.

- Control risk

Add the next layer only when it fixes a real visibility or approval gap. If requests still get stuck in email threads and spreadsheets, fix intake, approval, and routing first. Make missing approvals, unclear ownership, and off-book spend harder to hide.

- Integration effort

Sprawl usually breaks at integration points, not in product demos. Map how data moves across AP, engineering, and payments ops before you buy, and avoid tools that add new manual bridges. Favor software that reduces handoffs now, not after a future integration phase.

- Operator workload

More software does not automatically reduce work. If AP still re-keys details, asks engineering for payout status, or resolves exceptions in chat, you have shifted workload, not reduced it. Choose the option that removes manual touches on common exception paths.

- Audit evidence quality

If you cannot explain request-to-payment traceability in one flow, pause optimization buying and fix the audit trail. The flow should be clear across requisition, sourcing, purchase orders, receiving, invoicing, and payment, with exportable records. Evidence quality beats feature breadth while control is still maturing.

- Return on investment (ROI)

Evaluate ROI after control and integration checks. Stage-fit ROI is whether the tool reduces operator time, reconciliation friction, and visibility gaps enough to justify integration burden. Buy the next constraint, not the full suite.

This is not only a suite-selection problem. If no one owns the request-to-payment chain across AP, engineering, and payments ops, fix accountability before adding more tools.

If payments or card handling is part of your stack, read How Platform Operators Should Plan PCI DSS Level and Cost.

Best stack at seed stage when Excel still runs most procurement#

When Excel still runs most purchasing, the best seed-stage stack is three layers: system-based requisition approvals, explicit AP invoice approval, and payout controls for your first cross-border lanes.

| Layer | What to implement now | What to check before you buy |

|---|---|---|

| Lightweight e-procurement platform | A configurable requisition approval workflow so requests leave sheets, inboxes, and chat | You can export who requested, who approved, and when |

| Disciplined AP approval | A clear invoice intake -> review -> approval flow | Invoice approval is visible in-system, not re-approved informally in email |

| Payout controls for first global lanes | A provider that can send third-party payouts in local currency | You can verify required corridors, track payout status, and export transaction history |

The tradeoff is straightforward: this stack is fast to deploy and makes ownership clearer, but manual exception handling remains. Failed transfers, invoice mismatches, and out-of-band approvals still need operator intervention.

For a creator platform paying international contractors, the move is not Excel to a full suite. It is Excel approvals to requisition workflow + AP approval queue + payout tooling with searchable/exportable records. A good month-end test is whether you can pull requisition approval, invoice approval, and payout evidence for the same payment without rebuilding the trail by hand.

Best stack at growth stage when approval speed and exception handling break#

When approvals slow down and exceptions leave the system, keep your e-procurement platform as the control surface and add targeted layers for exception handling and payout orchestration.

| Layer | When it fits | What to verify |

|---|---|---|

| E-procurement platform as front door | Keep it as the control surface as volume grows | One approval path with a clear record; policy-driven routing, SLAs, and approvals run end to end |

| Procurement intelligence layer | Add it when AP is repeatedly fixing failed automated invoices and re-reviewing similar issues | AP can see failure reason, edit, and resubmission history in one place |

| Payout orchestration | Add it before more payout point tools when approval latency and payment failures rise together | Use idempotent retries; Stripe documents idempotency keys up to 255 characters and notes keys can be pruned once they are at least 24 hours old |

- Keep the e-procurement platform as the front door

This layer should continue to own requests, approval routing, and policy evidence as volume grows. The priority is one approval path with a clear record, not extra features for their own sake. Use a platform that can run policy-driven routing, SLAs, and approvals end to end. If approvals shift to chat or email, you have created a second lane with weaker controls.

- Add a procurement intelligence layer when AP exception work becomes repetitive

Add this when AP is repeatedly fixing failed automated invoices and re-reviewing similar issues. The goal is to reduce duplicate handling while preserving the audit trail. Require explicit human exception handling, not only straight-through automation. In the Dynamics 365 model, an AP clerk can edit a failed automated invoice and resubmit it to workflow, and teams can restart processing in bulk when multiple failures share one fix. Your checkpoint: AP can see failure reason, edit, and resubmission history in one place.

- Add orchestration before adding more payout point tools

If approval latency and payment failures rise together, centralize routing, policy gates, and retries before buying more point solutions. For global payouts, keep routing and compliance checks consistent before funds move. Enforce idempotent retries so a retried request is recognized as the same operation. Stripe documents idempotency keys up to 255 characters and notes keys can be pruned once they are at least 24 hours old. Validate this by forcing timeout/retry scenarios in test and confirming the same payout request resolves consistently.

For marketplace-scale operations, this stack is usually about consolidation, not dashboard sprawl. Connecting approval, exception, and payout visibility in fewer systems improves control and cash-flow visibility as finance work becomes more exception-driven.

For the metrics behind stage-by-stage planning, read KPIs for Each Stage of Platform Growth: From Seed to Series C to IPO.

Best stack from Series C to IPO when auditability matters more than feature count#

From Series C through IPO prep, the right stack is the one you can defend: every payment should be traceable from request through reconciliation without jumping across inboxes or side files.

| Control layer | What it must support | Verification |

|---|---|---|

| E-procurement policy record | Request, approver identity, policy decision, and entity context for each spend decision | Sample five payouts across two entities and confirm each has a linked request, approval record, policy rule, and owner |

| Reconciliation and payment-evidence layer | Payment instruction, processor or bank reference, status transitions, and the reconciliation artifact | Pull a month-end sample and confirm you can move from approved spend to settled payment to reconciled ledger support without re-keying data |

| Tax and reporting controls | Tax evidence and withholding support before expanding payout options by country; Form 1042-S is used to report certain income paid to addresses in foreign countries | For calendar years beginning in 2024, IRS electronic reporting rules generally require e-filing for filers of 10 or more returns |

- Keep the e-procurement platform as the policy record for every entity

At this stage, your e-procurement layer should hold the request, approver identity, policy decision, and entity context for each spend decision. Feature breadth matters less than whether you can show the same approval logic across entities and export a complete history for any payment path. Choose the product that preserves an auditable chain, not the one with the longest module list. For covered issuers, SEC rules require management ICFR reporting in annual reports, and management cannot conclude ICFR is effective if material weaknesses exist. A practical check: sample five payouts across two entities and confirm each has a linked request, approval record, policy rule, and owner. If any approval only exists in chat, email, or a spreadsheet, your control chain is already weak.

- Add a reconciliation and payment-evidence layer that ties instruction to provider outcome

Approval plus a "payment sent" status is not enough in late-stage operations. You need one chain that includes payment instruction, processor or bank reference, status transitions, and the reconciliation artifact showing what cleared and what was corrected. Require a single record connecting procurement request, approval, payment instruction, provider reference, and reconciliation output. This aligns with tighter audit expectations around financial statements and controls, including PCAOB AS 2201's integrated audit framing; approved amendments are effective December 15, 2026. Your verification step is simple: pull a month-end sample and confirm you can move from approved spend to settled payment to reconciled ledger support without re-keying data. A common failure mode is AP closing from an internal status while provider references remain isolated in another tool.

- Add specialized tax and reporting controls for foreign contractor payments before opening more corridors

For a global contractor platform, standardize tax evidence and withholding support before expanding payout options by country. For U.S. reporting, Form 1042-S is used to report certain income paid to addresses in foreign countries, so payout capability alone is not enough. Treat tax reporting as an operational workflow, not a year-end export task. For calendar years beginning in 2024, IRS electronic reporting rules generally require e-filing for filers of 10 or more returns. If you are near that volume, design structured outputs and entity-level review now. Your checkpoint: for a foreign contractor payment, can finance produce the payee record, payment amount, withholding treatment if applicable, and reporting file support without rebuilding by hand? If not, pause corridor expansion until that is fixed. For a deeper breakdown, see IRS Form 1042-S for Platform Operators: How to Report and Withhold on Foreign Contractor Payments.

At this stage, the question is not feature count. It is whether your controller, AP lead, and payments ops team can prove what happened, why it happened, and where the evidence lives by entity. If you cannot answer that now, standardize the evidence chain before adding more payout reach.

Compare stack options by stage before you commit budget#

Choose the stack for your next control gap, not your next demo. A stage-based view keeps budget tied to what you need to run safely now, while deferring modules that add integration work, admin overhead, or switching friction before they are necessary.

Overbuying early is common, and the later pain is usually weak evidence paths, uneven entity coverage, or market/program gaps, not missing feature checkboxes. Use each stage to define three things: what must be controlled now, what can wait, and what event forces an upgrade.

| Stage | Best-for profile | Must-have systems | Minimum compliance baseline | Defer list | Upgrade trigger | Practical caveat |

|---|---|---|---|---|---|---|

| seed stage | Lower spend, few approvers, first cross-border payouts, finance still close to spreadsheets | Lightweight e-procurement layer, centralized approval records, basic AP controls, payout status visibility | KYC/KYB intake before paying business counterparties where your provider/program requires it; tax document collection at onboarding; retention policy documented, with U.S. teams often planning around the IRS general 3 years context where relevant | Procurement intelligence, advanced orchestration, multi-provider routing, heavy customization | Approvals move into chat/email, AP re-keys payment data, first country/entity expansion creates recurring exceptions | Country and program support varies by provider and region, and some features are available only when specific programs are enabled |

| growth | More vendors, more exceptions, marketplace or embedded-payments complexity, month-end pressure | E-procurement as control surface, AP automation, stronger reconciliation layer, payout-status events synced back to finance | KYC/KYB gating becomes rules-based by counterparty type; where CDD obligations apply, beneficial-owner identification and verification require written procedures; tax document ownership and refresh points are defined; retention covers the request-to-payment chain | Broad suite expansion too early, duplicate point tools for the same approval step, nonessential sourcing modules | Approval latency and payment failures rise together, duplicate review work grows, exceptions cannot be cleared from one record | FATF standards are global, but implementation is local, so do not assume one KYB flow, one document set, or one threshold across jurisdictions |

| Series C | Multi-entity operations, controller oversight, tighter board scrutiny, audit sampling pressure | Entity-aware e-procurement, linked payment instruction and provider reference, reconciliation evidence, structured tax-reporting support where in scope | KYC/KYB ownership is clear by entity and product line; tax handling is tied to payee records and reporting outputs where applicable; retention expectations are written by record type | Niche tools that do not improve traceability, manual side files by subsidiary | You cannot pull a sample and show request, approval, payment result, and ledger support from one evidence path | Some features are technically available but not contractually or regionally enabled, so confirm what is live per entity before standardizing |

| IPO | Public-company-style control expectations, formal testing, repeatable cross-entity evidence | Auditable end-to-end chain, access controls, exception logging, tax/reporting support, retention schedule with owner and retrieval process | Treat retention as policy by record purpose: IRS recordkeeping depends on what proves the return, and employment-tax records may need to be kept at least four years after filing the 4th quarter for the year | New connectors without control owners, "temporary" spreadsheet approvals, corridor expansion without evidence design | Control testing finds gaps, consistent operation cannot be evidenced, or payment support must be rebuilt manually for reviews | Market coverage still varies; a country listed as supported does not guarantee every payout method, entity structure, or program type |

Single-vendor or best-of-breed#

| Option | Integration load | Failure isolation | Control depth | Operating cost pattern |

|---|---|---|---|---|

| Single-vendor consolidation | Usually lower early because there are fewer connectors and handoffs | Can reduce connector-related breakpoints, but one vendor incident can affect more of the chain | Often sufficient at seed/early growth when the goal is unified visibility | Often lower early; switching friction can rise later |

| Best-of-breed | Usually higher because you manage more seams across tools | Can isolate issues by domain when interfaces and monitoring are strong | Often stronger in specific layers like reconciliation, tax handling, or complex payout ops | Can avoid paying for broad unused modules; support and change-control overhead usually increases |

Before committing budget, trace one recent payment per entity. If you cannot show the approval record, KYC/KYB or payee setup step, tax document state, provider outcome, and retained support in one clear chain, fix that evidence path before adding more tools.

For a step-by-step walkthrough, see Delaware C-Corp vs Wyoming LLC for Your Next Growth Stage.

Execute in the first 90 days without breaking payouts or controls#

After you choose stage-fit tools, execution order is what protects payouts and controls. In the first 90 days, run changes in sequence: clean data, assign owners, define policy, configure systems, test integrations, then roll out with a documented rollback path.

| Step | Focus | Key detail |

|---|---|---|

| Data cleanup and owner map | Normalize vendor and payee records, remove duplicate counterparties, and assign clear ownership for each payment path | Keep approval evidence and change history in a tracked system so changes and approvals are retrievable |

| Policy before configuration | Document implementation steps, validation steps, and a rollback plan before launch | Do not enable a new approval route or payout lane until rollback triggers, approvers, and in-flight handling are defined |

| Evidence pack per payment path | Keep a standard pack with approval log, policy decision, provider status, reconciliation export, and exception-resolution notes | Test idempotent request behavior; verify paid, failed, or canceled outcomes; if ACH is in scope, keep the unauthorized return rate below Nacha's 0.5% threshold |

| Tax-reporting readiness | Collect and retain the records needed for later reporting | FBAR uses aggregate foreign account value above $10,000 at any point in the year; Form 8938 for an unmarried U.S.-resident filer starts above $50,000 at year end or $75,000 at any time during the year |

- Start with data cleanup and an owner map

Normalize vendor and payee records, remove duplicate counterparties, and assign clear ownership for each payment path before go-live. AP should not have to guess whether finance, payments ops, or engineering owns a failed transfer. Keep approval evidence and change history in a tracked system, for example ticketing or source control, so changes and approvals are retrievable.

- Write policy before configuration, with rollback rules

Set policy decisions before they become platform toggles. For each change, document implementation steps, validation steps, and a rollback plan before launch. Do not enable a new approval route or payout lane until rollback triggers, approvers, and in-flight handling are defined.

- Require one evidence pack per payment path

Keep a standard pack for every live path: approval log, policy decision, provider status, reconciliation export, and exception-resolution notes. For global payouts, test idempotent request behavior so retries do not duplicate the underlying operation. Also verify visibility into terminal outcomes such as paid, failed, or canceled, and assign failed-transfer triage ownership. If ACH is in scope, monitor unauthorized returns and keep the unauthorized return rate below Nacha's 0.5% threshold.

- Build tax-reporting readiness into onboarding and retention

Where cross-border tax obligations may apply, collect and retain the records needed for later reporting. FBAR is FinCEN Form 114, not filed with the IRS, and Form 8938 does not replace FBAR obligations. Thresholds differ: FBAR uses aggregate foreign account value above $10,000 at any point in the year, while Form 8938 for an unmarried U.S.-resident filer starts above $50,000 at year end or $75,000 at any time during the year. If U.S.-source payments to foreign persons are in scope, Form 1042-S may still be required even when no withholding applies.

Spot the red flags that mean your current stack is now a risk#

If you cannot explain and evidence each payment path quickly, your current stack is now a scaling risk.

- Re-keying between approval and payout

Manual re-entry between your e-procurement platform and payout system is a control gap, not just an efficiency issue. As volume grows, manual P2P work gets more complex and increases error and documentation risk. Test one live payment end to end: approval record, payee record, amount, and provider reference should flow without copy-paste steps.

- AP cannot trace approval to final outcome

If AP cannot move from approval to paid, failed, or canceled status quickly, traceability is weak. Approval evidence and later changes should be captured in systems that preserve the audit trail. If you cannot get from approval ID to provider status and reconciliation export in one path, treat that as a blocker before expanding to new geographies.

- Exceptions live in chat and spreadsheets

Exception handling spread across chat and sheets usually means poor control information quality. You need one owner, one tracked record, and one place for resolution notes and follow-up. If ACH is in scope, that owner should monitor unauthorized returns against the Nacha 0.5% threshold, with awareness of the 3.0% administrative and 15.0% overall return-rate levels.

- Tax handling for foreign contractor payments is ad hoc

Ad hoc cross-border tax workflows are a sign your stack is under-scoped. Not every foreign contractor payment is reportable, but U.S.-source amounts paid to foreign persons can trigger Form 1042-S duties for a withholding agent. Before adding optimization layers, require structured capture of payee tax status, payment source characterization, and retrievable records.

Choose the smallest stack that still gives you control, then upgrade on clear triggers#

Use the smallest stack that gives you control now, then add layers only when clear risk and maturity signals justify it. This keeps decisions grounded in limited budgets and avoids adding ownership and traceability burden before a new tool has real benefit.

- Start with the minimum stack you can control and evidence

The early goal is not maximum feature depth. It is a clean, auditable chain across approvals, payment execution, and reconciliation artifacts so controls are visible and retrievable.

- Set upgrade triggers before tool pressure turns reactive

Add the next layer when your current setup no longer supports the core process with acceptable speed and clarity, not because a category is popular. The 2024 Hype Cycle lens is useful here: judge additions by maturity, adoption, and expected benefit.

- Scale controls in response to risk

GAO Green Book Principle 10.02 is the operating rule: design control activities in response to identified risks. Expand your stack only where it closes a real control gap and improves traceability.

Your next step is practical and risk-based: map your current tools to current-stage requirements, then prioritize the highest-impact control gaps first. Use NIST RMF thinking for those choices by balancing effectiveness, efficiency, and legal constraints.

Related reading: Growth Mindset for Freelancers Who Want a More Stable Business.

Frequently Asked Questions

What tools should a platform operator use at seed, growth, and late scale?

At seed, keep it small: a lightweight e-procurement platform for approvals, a controlled AP process, and payout tooling that can return provider status and reconciliation data. At growth, consider adding a procurement intelligence platform when exception queues, duplicate review, and approval latency start consuming the team. By late scale, the priority often shifts from feature count to one auditable chain from request to approval, payment instruction, provider reference, and reconciliation artifact.

When does a procurement stack become too fragmented to manage safely?

The break point is not a tool count. It is the moment integration complexity makes you lose traceability or ownership. Pick one live payment and see if you can move from approval ID to final paid, failed, or canceled status and then to the reconciliation export without re-keying or hunting through chat. If not, fragmentation is already a control risk.

What are the minimum controls before scaling global vendor or contractor payouts?

You need clear separation of duties, because the 2025 GAO Green Book is explicit that dividing key duties reduces error, misuse, and fraud risk. You also need retained evidence for each payment path: approval log, policy decision, payee record, provider outcome, reconciliation output, and exception notes in one retrievable place. For foreign persons, confirm whether the payment is withholding-reportable before scale, because Form 1042-S applies to amounts paid to foreign persons that are subject to withholding. If you need the reporting detail, see IRS Form 1042-S for Platform Operators: How to Report and Withhold on Foreign Contractor Payments.

Should we choose one suite or combine best-of-breed procurement and payout systems?

Choose a suite when integrated consistency, a common data model, and a single interface matter more than functional depth. Choose best-of-breed when your payout, tax, or exception needs are materially more complex than your procurement needs, but go in knowing the tradeoff is higher integration and maintenance burden. Neither model wins by default. The right answer is the one you can control and evidence with the fewest brittle handoffs.

How do we decide when to add procurement intelligence instead of hiring more AP staff?

Do not make that call from team sentiment alone. APQC treats accounts payable as a high-volume process and benchmarks invoices processed per full-time equivalent, so start with your actual throughput, rework rate, and exception backlog. If headcount is growing but reviewers are still spending time on duplicate checks, status chasing, and manual routing, that is usually the point to evaluate adding intelligence. If the problem is unclear policy ownership or broken source data, another tool will just automate confusion.

What are the top mistakes when replacing Microsoft Excel in procurement operations?

The biggest mistake is moving forms into software without moving controls with them. Weak spreadsheet governance increases error frequency, and teams often recreate the same problem by keeping approvals in the new tool while exceptions, bank changes, and payout notes stay in spreadsheets or chat. Another common miss is skipping field cleanup before migration, which can leave duplicate vendors, inconsistent payment terms, and missing tax status in the new stack from day one.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- csrc.nist.gov/Projects/risk-management/about-rmftrusted

- ecfr.gov/current/title-17/chapter-II/part-229/subpart...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- gao.gov/assets/890/882014.pdftrusted

- guides.gaoinnovations.gov/greenbook/2025/principle-10-design-control-a...trusted

- guides.gaoinnovations.gov/greenbook/2025/principle-13-use-quality-info...trusted

- irs.gov/individuals/international-taxpayers/electron...trusted

- irs.gov/forms-pubs/about-form-1042-strusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

KPIs for Platform Growth from Seed to Series C and IPO

The useful way to read growth metrics is by stage, not as a fixed scorecard. **Key Performance Indicators (KPIs)** change with a company's lifecycle, and the decisions you make from them should change too.

How Platform Teams Scale AP Volume Without Adding Headcount

Use this as a decision list for operators scaling Accounts Payable, not a generic AP automation explainer. In these case-study examples, invoice volume can grow faster than AP headcount when the platform fit is right, but vendor claims still need hard validation.

IRS Form 1042-S for Platform Operators: How to Report and Withhold on Foreign Contractor Payments

If you own compliance, legal, finance, or risk for a platform paying foreign contractors, sellers, or creators, you may need to make **Form 1042-S** operational. That means clear decisions, reliable checks, and escalation points your team can apply and defend.