Quick Answer

Choose a Wyoming LLC when your near-term plan is owner-led operations without institutional fundraising, and choose a Delaware C-Corp when investor diligence and formal governance are likely soon. In delaware c corp vs wyoming llc, the practical decision turns on administrative discipline, record quality, and readiness for shareholder-board-officer structure. Before filing, confirm foreign qualification exposure if you will operate across states so early fee assumptions do not mislead your plan.

What Matters at the Next Growth Stage#

Choosing between a Delaware C-Corp and a Wyoming LLC is a stage-fit decision, not a state popularity contest. For delaware c corp vs wyoming llc, the real question is which structure you can run cleanly over the next 12-24 months while keeping room to scale.

A Wyoming LLC is often described as simpler to run, with flexible management and limited liability separation for members. A Delaware C-Corp uses a more formal governance model with shareholders, a board, and officers. That shape is often preferred when venture capital or IPO plans are realistic. Delaware is commonly tied to deeper business-law precedent, while Wyoming is often framed as a lower-cost, simpler operating base.

A useful decision rule is to match governance load to your actual calendar. If your next year is mostly delivery and cash management, simpler administration may be the better fit. If your calendar already includes investor meetings, data-room preparation, and term-sheet discussions, alignment with investor expectations may matter more than lower upfront costs.

| If your next 12-24 months look like... | Lean toward | Why |

|---|---|---|

| Client revenue, owner-led decisions, no institutional raise planned | Wyoming LLC | Operational simplicity and flexibility are often the priority |

| Active investor conversations or likely institutional diligence | Delaware C-Corp | Formal governance is often the expected shape |

| You are unsure now, but institutional funding is a realistic near-term path | Delaware C-Corp | It can align earlier with investor-facing governance expectations |

This guide stays focused on operating choices, governance burden, and timing tradeoffs. It is not legal or tax advice, and you should confirm your specific position with licensed professionals before filing.

At-a-Glance Comparison Table for Delaware C-Corp vs Wyoming LLC#

Use this as a pre-filing screen, not a final verdict. The goal is to test assumptions before you file, not after a deadline or diligence request.

| Criteria | Delaware C-Corp | Wyoming LLC |

|---|---|---|

| Setup steps | Out of scope in this source pack; verify the current state workflow before filing. | Out of scope in this source pack; verify the current state workflow before filing. |

| Filing primitives | Out of scope in this source pack; verify the exact filing document label in current Delaware forms before filing. | Out of scope in this source pack; verify the exact filing document label in current Wyoming forms before filing. |

| First-document stack after filing | Keep jurisdiction of organization and EIN consistent across core records; verify any additional packet items with current requirements. | Keep jurisdiction of organization and EIN consistent across core records; verify any additional packet items with current requirements. |

| Ongoing admin load | Evaluate filings, disclosures, and recordkeeping as one recurring workload. | Evaluate filings, disclosures, and recordkeeping as one recurring workload. |

| Investor fit | Out of scope in this source pack; assess against your own diligence expectations and timing. | Out of scope in this source pack; assess against your own diligence expectations and timing. |

| Privacy posture | Review disclosure and privacy requirements before filing. | Review disclosure and privacy requirements before filing. |

| Governance complexity | Out of scope in this source pack; confirm governance requirements with current state rules and counsel. | Out of scope in this source pack; confirm governance requirements with current state rules and counsel. |

| Dispute handling | Compare legal process expectations before choosing jurisdiction. | Compare legal process expectations before choosing jurisdiction. |

| Legal venue and predictability | Out of scope in this source pack; avoid venue-specific assumptions until counsel-level review. | Out of scope in this source pack; avoid venue-specific assumptions until counsel-level review. |

| Recurring state burden | Model recurring obligations, including tax and maintenance fee categories, before filing. | Model recurring obligations, including tax and maintenance fee categories, before filing. |

| Conversion complexity | Out of scope in this source pack; verify any conversion requirements directly with current state guidance and counsel. | Out of scope in this source pack; verify any conversion requirements directly with current state guidance and counsel. |

Practical checkpoint: before banking or diligence, make sure jurisdiction and EIN appear consistently across your records. Inconsistencies here create avoidable friction later.

Use the table in two passes. First, rule out any option you cannot support with monthly record discipline. Second, compare the remaining option against your most likely trigger in the next cycle, such as operating costs, compliance load, growth plans, privacy or disclosure requirements, or dispute profile. That keeps the choice tied to execution, not aspiration.

Choose by Business Stage Not Hype#

Start with your next stage and source quality, not internet certainty. The avoidable mistake is using nonbinding material as if it were filing instructions, so run a source-status check on the material in your decision file:

| Source type | Article guidance |

|---|---|

| official | Use it to verify current filing instructions and record the date you relied on |

| proposed | Treat it as not final and recheck it before using it to drive a filing choice |

| commentary | Use it for policy context, but still verify current filing instructions from official sources |

- Label each source as

official,proposed, orcommentary. - Record the date you relied on.

- Recheck anything marked proposed or informational before using it to drive a filing choice.

Why this matters: FederalRegister.gov says its display is informational and not the official legal edition, and a document labeled Proposed Rule is still not final. A CRS product can help with policy context, but you should still verify current filing instructions from official sources.

Then make a stage-based call you can execute cleanly. Choose the structure that fits your near-term plan, document responsibilities clearly, and keep records consistent from day one. Reputation may influence perception, but it should not override execution quality.

One practical habit helps here: keep a one-page decision log. Capture the entity choice, the source set you used, and the trigger that would cause you to revisit the decision. When conditions change, you update one file instead of re-arguing from memory. That can make later conversations with counsel and partners faster and less subjective.

Formation Sequence for a Clean Start#

A clean start usually comes down to sequence discipline. Pick the structure and state early, then document each step so your records stay aligned as you operate. Use this sequence:

| Step | What to do | Why it matters |

|---|---|---|

| 1 | Choose entity type and state of formation | State statutes will govern the entity |

| 2 | Appoint a registered agent in that state | Legal documents have an in-state recipient |

| 3 | File formation paperwork with the relevant state filing office | This is usually the Secretary of State |

| 4 | Organize filing confirmations and core entity records in one place | Keep records aligned as you operate |

| 5 | Plan foreign qualification early if you will operate outside the formation state | Track where registration is needed |

If you prefer the same sequence as a plain checklist:

- Choose entity type and state of formation, knowing that state statutes will govern the entity.

- Appoint a registered agent in that state so legal documents have an in-state recipient.

- File formation paperwork with the relevant state filing office, usually the Secretary of State.

- Organize filing confirmations and core entity records in one place.

- If you will operate outside the formation state, plan foreign qualification early and track where registration is needed.

After formation, keep a clear control file that matches the entity you formed and where you formed it. Focus on maintaining consistent legal-name and entity details across your records. This is risk control and execution clarity, not paperwork for its own sake.

Verification discipline matters. Keep dated filing proof, registered-agent details, and one canonical legal name string across records. Finishing the filing but letting post-filing records drift can create avoidable cleanup work later.

Add one extra consistency check before expanding operations: compare the legal name and entity details across formation records, registered-agent records, and any foreign qualification registrations. Small mismatches in punctuation or ordering can cause administrative rework, so fix them early.

Ongoing Governance and Admin Burden#

The key question is not which entity sounds more credible. It is whether you will keep governance records clean and current.

| Checklist item | Article detail |

|---|---|

| Material decisions | Record them with dates and clear approvers |

| Signer authority and role ownership | Keep them current |

| Ownership records and cap table entries | Update them when equity changes, where applicable |

| State maintenance tasks | Complete them and retain filing confirmations |

| Document archive | Keep it retrievable for diligence and audits |

Source quality limits this section. Three legal commentary links in the research packet returned access-denied pages, so they do not provide reliable detail on exact ongoing obligations. Treat specific claims about Board of Directors, Shareholders, Officers, or Operating Agreement duties as unverified here unless you confirm them in current primary Delaware and Wyoming materials.

You can still make a practical choice today. Pick the structure you can administer consistently, and do not add complexity for status signaling alone. Use a recurring checklist you can realistically keep up with:

- Record material decisions with dates and clear approvers.

- Keep signer authority and role ownership current.

- Update ownership records and cap table entries when equity changes, where applicable.

- Complete state maintenance tasks and retain filing confirmations.

- Keep a retrievable document archive for diligence and audits.

Record drift after formation can create delays when a bank, partner, or investor asks for proof. Repeatable admin habits help reduce that avoidable friction.

If you want this to hold up under pressure, assign owners and a regular review schedule now. Decide who updates authority records, who stores filing confirmations, and who reviews the archive. Governance discipline often fails when accountability is vague.

Cost Model That Actually Changes Decisions#

Use a two-year total-cost model, not a filing-fee snapshot. The path that looks cheapest at formation can get expensive if you later need restructuring and cleanup.

| Scenario | Delaware C-Corp Year 1 | Delaware C-Corp Year 2+ | Wyoming LLC Year 1 | Wyoming LLC Year 2+ | Practical call |

|---|---|---|---|---|---|

| Solo operator, no outside equity planned | Often higher setup and admin overhead | Recurring governance and admin work can continue | Often lower setup and simpler upkeep | Can remain simpler if ownership stays straightforward | Often favor LLC when you want lean operations and no investor track |

| Growing agency | More formal process and documentation effort can be required | Ongoing admin and support costs can stay material | Lower entry cost is common | Costs can rise as operations and state footprint expand | Start with the structure you can run cleanly and review yearly |

| Investor-track startup | Upfront legal and admin prep is often heavier | Ongoing governance work is expected | Lower initial spend can be attractive | Costs can shift if investor requirements later drive conversion or restructuring | Often favor C-Corp when investor readiness is a near-term priority |

Build your model in five buckets and force explicit assumptions for each:

- State filing and maintenance

- Registered agent

- Compliance labor, including internal time cost

- Professional support, including legal and accounting

- Conversion or restructuring work

Make hidden costs explicit. Treat headline fee comparisons as context-specific by profile and year. Include Franchise Tax where it applies, and treat State Corporate Income Tax exposure as operations-based, not formation-state-only. Profits may be apportioned to states where you operate, and some no-income-tax states still impose other business taxes.

Red flag: choosing only for the lowest formation cost can create the highest total cost if later changes require ownership, approvals, or tax-record cleanup.

Stress-test your model with at least two non-ideal scenarios. One is a delayed fundraise where you still carry legal and admin work for another year. Another is a faster-than-expected growth period that adds counterparties, contracts, and document requests. If the plan breaks under either scenario, revise your assumptions before you file.

If the structure decision is made and you are cleaning up day-to-day cash handling next, The 'Profit First' Method Part 2: Setting Up Your Bank Accounts covers the bank-account setup side.

Taxes and Compliance Boundaries You Must Clarify#

Formation state is only one part of the decision. Separate state-level charges, federal treatment, and multi-state obligations before you file.

| Boundary | What belongs here | Why it changes the decision |

|---|---|---|

| State entity charges | State filing, maintenance, and ongoing compliance items | These are recurring state costs, but they are not the full tax picture |

| State tax layer | State tax obligations where activity occurs | Exposure can follow where business activity happens, not only where formation documents were filed |

| Federal layer | Federal tax treatment and owner-level consequences | This should be evaluated separately with entity-specific assumptions |

| Multi-state operations | Foreign qualification, dual registrations, registered agents, and ongoing filings | Dual-state upkeep can outweigh initial filing-fee savings |

A practical boundary rule: once activity becomes material in a state, that operating state often matters more than the formation state. You can generally form an LLC without U.S. citizenship or residency, but that does not remove obligations where you actually operate. There is no single state that is universally best for every non-resident situation.

Take this question set to counsel and require written assumptions:

- Which states will have material activity, and what triggers obligations in each one?

- If operations are outside the formation state, what foreign qualification steps are required and when?

- What recurring filings, registered-agent requirements, and ongoing costs apply in both states?

- Which assumptions are still unknown for your exact entity structure and activity footprint?

| Known from this comparison | Unknown until entity-specific review |

|---|---|

| Forming in one state does not remove obligations in another state where you operate | Your exact all-in federal and state tax outcome |

| Foreign qualification can add recurring costs in both formation and operating states | Precise filing and annual totals for your timing, structure, and activity footprint |

| No single state is universally best for every non-resident case | The best formation or operating setup for your exact facts |

| State-level charges are only one layer of the decision | The final compliance calendar and responsibility split for your team |

Do not file until this boundary check is complete. If you form in one state and operate in another, plan for dual-state compliance early.

To keep this practical, ask counsel for outputs you can actually execute, not theory alone: required registrations, recurring filings, and who is responsible for each item. Then map those outputs to your internal calendar and document owners. The decision gets easier once responsibilities are visible.

If fundraising is close, The Anatomy of a FinTech Pitch Deck: What VCs Look For can help you prepare for investor conversations.

Legal System Tradeoffs in Real Disputes#

Legal venue tends to matter most when governance, investor-rights, or control conflicts are plausible. If those conflicts are unlikely and ownership will stay closely held, paying for higher legal complexity may be unnecessary overhead.

| Dispute posture | Practical implication |

|---|---|

| Likely board-control or investor-rights conflicts | Delaware-related disputes can hinge on standards of review in Chancery, including business-judgment-rule versus entire-fairness arguments in current commentary. |

| Mostly stable, closely held ownership | A simpler entity and governance setup can be the lower-overhead path when you do not need formal investor-governance machinery yet. |

Recent legal commentary shows this tradeoff is active, not theoretical. After a February 2024 Chancery opinion involving TripAdvisor, commentary described a clearer path for companies seeking business-judgment-rule protections when reincorporating out of Delaware. The same discussion argued that moves led by a controlling shareholder should face entire-fairness review. Treat this as an ongoing legal debate, not a universal rule.

Before filing, ask counsel for a short dispute memo focused on your likely conflict pattern, ownership concentration, and approval mechanics in your governing documents. Match the entity choice to your realistic dispute profile, not to abstract prestige.

A good memo should answer one operational question clearly: what type of conflict is most plausible for your ownership structure in the next two years. If the likely conflicts are internal and limited, simpler administration may be enough. If governance rights and control issues are likely to become formal disputes, legal predictability may deserve more weight.

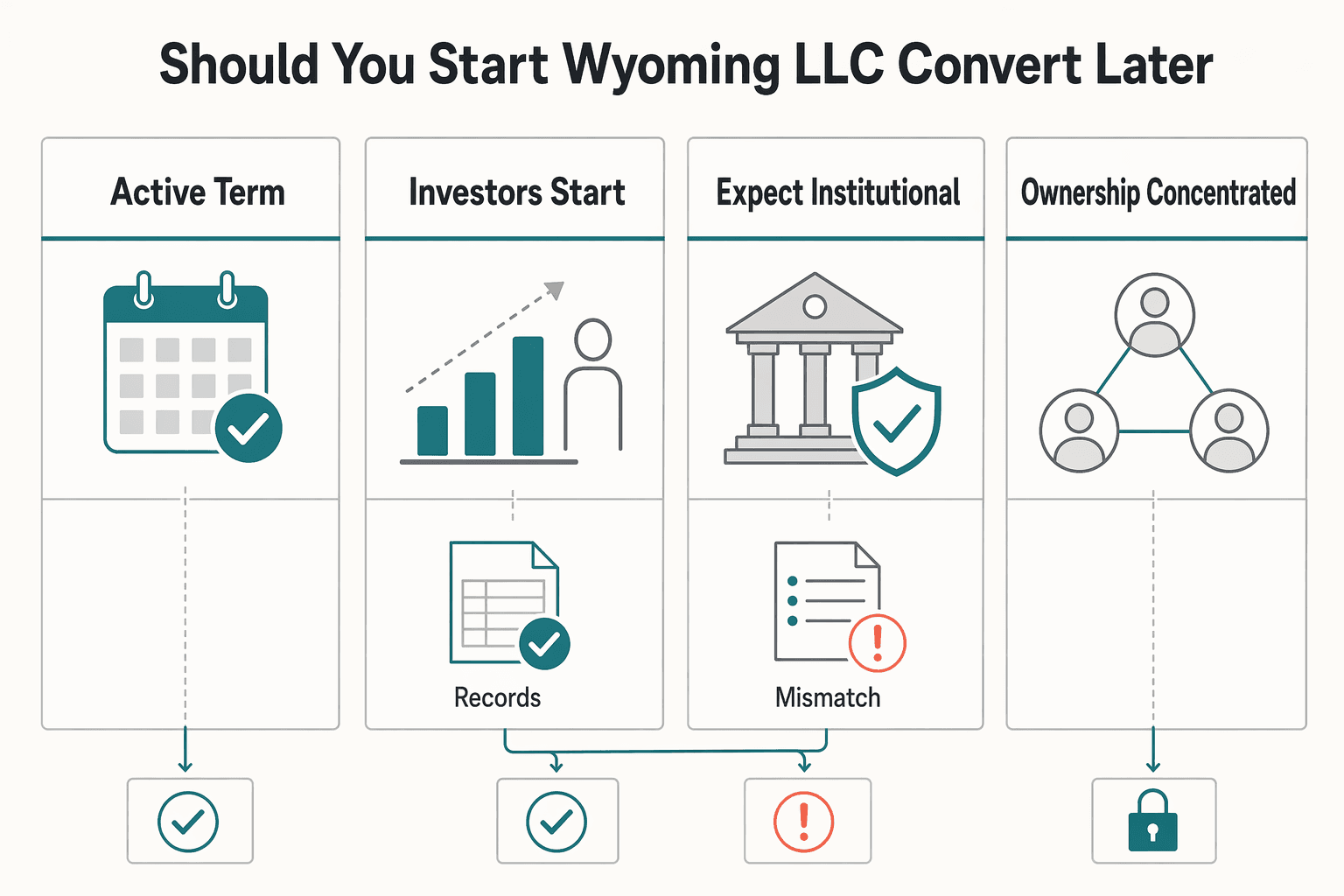

Should You Start as a Wyoming LLC and Convert Later?#

It can make sense when ownership is closely held and outside capital is not imminent. Start as a Wyoming LLC only if you define conversion triggers early and keep the records clean.

This path is not just extra paperwork. If approvals, ownership records, or compliance history are messy, conversion can become a timing and governance problem when financing pressure rises.

| Trigger | Action now | Why it matters |

|---|---|---|

| No active term sheet talks, no board-seat requests, closely held ownership | Stay as a Wyoming LLC and keep records current each month | You keep operations simpler while current needs stay simple |

| Investors start requesting preferred stock terms, governance rights, or a formal Board of Directors | Start Delaware C-Corp conversion planning with counsel | These requests can signal near-term diligence pressure |

| You expect institutional-style governance in the next funding cycle | Prepare conversion plans before diligence intensifies | Earlier preparation can reduce last-minute document cleanup |

| Ownership is concentrated and major governance changes are coming | Tighten approvals and consent records before restructuring | Control conflicts can be harder to unwind once financing timelines start |

Market reality still matters. One legal-academic source reports that 67.8 percent of Fortune 500 companies are incorporated in Delaware and describes Delaware's dominance as still strong. That does not mean every smaller firm should convert immediately, but it does mean a later switch should be treated as a significant legal and operational project.

Before choosing a convert-later path, confirm these prerequisites in writing:

- A signed Operating Agreement aligned with current ownership and decision rights

- Clean books with reconciled statements and no unresolved gaps

- Ownership clarity across member records, tax reporting, and bank ownership documents

- No open state compliance items, missed filings, or unresolved notices

- A dated approval record that clearly states who can authorize conversion steps

Red flag: if cleanup starts after fundraising begins, execution risk rises. Conversion, merger, and reorganization are recognized litigation topics, so weak records can turn a strategic move into a legal and timing problem.

Recommendation: if institutional financing is unlikely in your next cycle, start with a Wyoming LLC and document conversion triggers now. If term sheet conversations or governance-rights negotiations are already active, evaluate and plan the Delaware C-Corp move early rather than waiting for active diligence.

A practical handoff step helps: prepare a conversion-readiness folder before you need it. Keep ownership records, approvals, key filings, and financial statements in one place with clear dates. When investor requests arrive, you respond from an organized file set instead of rebuilding history under deadline.

Cross-Border Operations and Banking Friction Check#

Entity choice alone usually does not fix weak documentation. If you plan to scale across borders, banking readiness and record quality often determine how fast you can execute.

| Day-to-day task | What drives success | What entity choice changes |

|---|---|---|

| Bank onboarding | Complete KYC package and consistent entity records | Usually very little on its own. Documentation quality is the main factor |

| Access to banking and payment rails | Domestic entity setup plus matching Employer Identification Number (EIN) details | Entity form can help, but mismatched records can still slow reviews |

| Audit-ready finance operations | Separate business accounts, clean records, and no commingling | Discipline matters more than state label |

| Approval processes | Clear internal authority records and traceable approvals | Better governance can reduce avoidable back-and-forth |

Before scaling volume, keep a practical evidence pack current:

- Active entity records

- EIN confirmation aligned to legal name and tax profile

- Beneficial-owner records if a partner or bank requests them

- Signer-authority records for payout and contract approvals, if requested

- Governing documents aligned with actual ownership and control

- Reconciliation exports that connect invoices, payouts, and approvals

A common failure point is timing. One legal-practice example describes a founder getting a $50,000 purchase order but missing the window because a U.S. bank account could not be opened fast enough. The same source says low-cost DIY setups, including a $699 filing path, generic operating agreements, and weak KYC packages often lead to repeated banking friction.

Tax and filing hygiene can also create operational risk. Some non-resident LLC guidance lists severe late-filing exposure. Examples include a $25,000 late Form 5472 penalty and a $260-per-month, per-partner late Form 1065 penalty, with March 15 and April 15 deadlines shown for different structures. Treat these as caution indicators and confirm your exact obligations with licensed tax counsel.

For teams using Gruv, keep execution compliance-first: apply policy gates before release, maintain approval audit trails, and export reconciliations on a fixed cadence. Keep traceable payout records where supported.

Checkpoint before scaling: if your setup cannot support clean invoicing, payout approvals, and document retention on demand, fix that first. Pick the entity you can document consistently every month, then expand corridors after your evidence pack passes a mock audit check.

A useful test is a mock request drill. Ask someone not involved in daily finance to locate your core records as if a bank or partner requested them on short notice. If retrieval is slow or records conflict, treat that as a process issue to correct before you increase payment volume.

Decision Checklist Before You File#

After the banking-friction check, make one final call based on the next 24 months. If institutional fundraising is likely, Delaware has the strongest support in this evidence set.

| Decision check | What to confirm now |

|---|---|

| Growth intent | Are you planning to seek institutional capital soon, or building without that near-term goal? |

| Investor-familiarity signal | A law-review abstract reports 67.8% of Fortune 500 companies are incorporated in Delaware and says Delaware is hard to displace because of investor commitment and network effects. If fundraising is near-term, treat that familiarity as a practical advantage. |

| Evidence limits | This section grounding does not establish specific filing costs, tax amounts, EIN timelines, filing-office steps, or foreign-qualification thresholds. Do not treat those as assumed facts here. |

| Final call | Write one sentence: Given my next 24 months, I choose [Delaware C-Corp or Wyoming LLC] because [my fundraising plan and confidence in this evidence]. |

Delaware's dominance signal supports a fundraising-oriented path, but it is not a universal recommendation for every founder. If your decision depends on cost, tax, or filing mechanics, pause and verify those details before filing.

Before you sign, run one final consistency check. Your selected entity should match your growth intent, your governance capacity, and the evidence quality behind your assumptions. If any one of those three is weak, delay filing briefly and close the gap. A short pause here can be cheaper than unwinding a rushed decision.

Conclusion and Next Step#

Choose the entity that fits your next operating stage, not the one with the strongest brand signal.

If outside investment is a near-term goal, Delaware is often the cleaner fit because investors are widely familiar with Delaware law. Delaware's Court of Chancery focuses on business disputes and is often cited for legal predictability. If you are prioritizing affordability and operational simplicity right now, a Wyoming LLC is often the lower-friction starting point.

The practical tradeoff is governance burden versus investor readiness. A corporate structure requires formal roles across shareholders, directors, and officers, which increases paperwork from day one. Wyoming is commonly presented as simpler to run, while Delaware is commonly presented as carrying higher recurring state costs. Even where comparison tables list specific amounts, use them as directional and verify before filing because fee comparisons can conflict across sources.

Before you file, make one deliberate decision pass:

- Define your near-term objective: investor-backed growth or lower-friction operational simplicity

- Choose Delaware when investor expectations are likely to matter soon

- Choose Wyoming when you want a simpler structure and no immediate fundraising pressure

- Set a compliance calendar for your entity's recurring state obligations

- Confirm unresolved tax, multi-state, or conversion questions with licensed counsel before filing

Run that checklist, write your one-sentence decision, and file only when your records and responsibilities are clear. File once, then run the structure cleanly. Consider changing only when a concrete trigger appears, such as active investor requirements.

Frequently Asked Questions

Is a Delaware C-Corp better than a Wyoming LLC for raising venture capital?

In many cases, yes. One comparison says many venture capital and institutional investors specifically require Delaware entities, but not all do. If outside capital is likely soon, Delaware is often a cleaner fit with those investor expectations.

When should I start with a Wyoming LLC and convert to a Delaware C-Corp?

Start with a Wyoming LLC when outside fundraising is not a near-term priority and you want a more streamlined governance setup. Convert when investor requirements make Delaware necessary. Set that trigger before active fundraising creates time pressure.

What are the main ongoing admin differences between a Delaware C-Corp and a Wyoming LLC?

A corporation is generally more formal, with shareholders, a board of directors, and officers. An LLC is generally more flexible and streamlined. You may see comparison-site figures like $110 vs $120 formation fees, $60 minimum vs $300 annual fees, and 3-5 vs 5-7 business days, but treat these as examples, not universal statutory facts.

How much does Delaware legal predictability matter if I am not raising outside capital?

Delaware is often favored for its specialized Court of Chancery and familiarity among many investors. If you are not planning to raise outside capital, that advantage may matter less than keeping governance and administration simpler. The tradeoff is less about branding and more about your likely operating path.

Can foreign qualification wipe out the cost advantage of forming in Wyoming or Delaware?

This grounding pack does not provide the thresholds or full cost math needed to answer that confidently. Do not assume an early filing-cost advantage will hold across multiple states. Verify where you are actually doing business before relying on a cost comparison.

Which structure is usually cleaner for an independent professional who wants low surprise risk?

If outside funding is not in your near-term plan, a Wyoming LLC is often cleaner because governance is simpler and LLC liability separation is clear in principle. If fundraising is a real goal, a Delaware C-Corp is often cleaner because it aligns with many investor expectations from the start. One source also describes both states as offering essentially the same asset protection, so the practical decision is usually capital path plus governance burden.

Try a related tool

A former tech COO turned 'Business-of-One' consultant, Marcus is obsessed with efficiency. He writes about optimizing workflows, leveraging technology, and building resilient systems for solo entrepreneurs.

Sources

- courts.delaware.gov/Opinions/Download.aspxtrusted

- courts.delaware.gov/Opinions/Download.aspxtrusted

- epa.gov/sites/default/files/2020-07/documents/transp...trusted

- federalregister.gov/documents/2021/12/08/2021-26548/beneficial-o...trusted

- legis.delaware.gov/docs/default-source/publications/legislative...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Sole Proprietorship vs LLC for Global Freelancers in 2026

For most freelancers in 2026, the practical default is still simple: use the simplest structure you can run cleanly, then formalize when risk actually rises. If your work is still in validation mode and the downside is contained, a sole proprietorship is often the practical starting point. When contract exposure, delivery stakes, or dispute risk starts climbing, forming an LLC deserves earlier attention.

The 'Profit First' Method Part 2: Setting Up Your Bank Accounts

Most freelancers who try Profit First open a few extra bank accounts and call it done. That's the wrong move.

The FinTech Pitch Deck Anatomy VCs Actually Underwrite

A fintech pitch deck should help an investor make a fast, defensible decision under uncertainty, not admire slide design. Investors screen quickly, so if your core claim is unclear in the opening, you can lose confidence before your best evidence appears.