Quick Answer

Build one internal decline taxonomy and run retries from that layer, not from raw provider labels. Keep PDRC, refusalCode, and issuer indicators like merchant_advice_code on every failed attempt, then store origin_layer, mapping version, and action taken. Use idempotency keys plus webhook event IDs so duplicates replay safely and stale events cannot overwrite a newer payment state.

How platform engineers should use decline reason codes#

Payment decline handling is a control problem, not a single lookup table. If you treat every failure as one generic "declined" state, you collapse different failure types into one bucket and can end up applying the wrong retry, message, or escalation path.

Declines can come from different layers, including the processor, gateway, or issuing bank. Stripe also separates failures into issuer declines, blocked payments, and invalid API calls. Those need different handling. For platform engineers, the practical shift is to classify failures by likely origin and context, not by one surface code.

The next constraint is fragmentation. There is no universal decline-code set across gateway ecosystems, and provider docs make that clear. Global Payments can replace generic responses such as 101 - Decline with PDRC categories. Verifone publishes its own reason-code table. Stripe uses provider-specific decline codes. Worldpay can expose unmodified scheme or acquirer responses in refusalCode when enabled.

The workable pattern is to normalize provider responses into one internal decision model while keeping raw evidence. Primer documents unified mapping where possible, and one provider explicitly notes that raw response codes can inform retry logic. In practice, you need both:

- stable normalized classes for product and operations decisions

- original provider fields for investigation and retry-policy tuning

A useful build-time checkpoint for each failed attempt is simple: can you trace the provider, raw code or reason text, and normalized class, plus an inferred decline layer when available? Mastercard's split fields show why this matters. network_decision_code indicates a network-level decline, while merchant_advice_code appears for issuer declines.

This guide focuses on building that auditable model early, so adding new providers usually requires less core-logic rework. We covered the underlying reconciliation side in Understanding Payment Platform Float Between Collection and Payout.

Build the right mental model before touching code#

Treat provider reason codes as evidence, not policy. Your internal decline taxonomy should stay separate, because provider labels describe what that provider exposes, while your system still has to decide what happens next.

Global Payments describes PDRC as action-oriented decline detail, but limits it to Visa and Mastercard and only certain acquirers. Worldpay can return an unmodified upstream value in refusalCode if enabled, and says raw response codes can inform retry logic. It also notes that third-party acquirers may not return the code returned by the card scheme. Verifone's reason-code table spans failed, declined, and successful outcomes. So a provider "reason code" is not the same thing as your decline class.

Separate the three objects#

Before you implement retries, define three separate objects:

| Object | Definition | Why separate it |

|---|---|---|

| Raw provider response | Exact provider fields and source-specific values such as refusalCode | Preserves the original evidence from the provider |

| Normalized class | Your internal interpretation, such as retryable, non-retryable, validation-related, or unknown | Keeps internal decisioning separate from provider labels |

| Action policy | The operational decision your product and ops teams apply next | Prevents retry timing, customer messaging, and integration handling from collapsing into one field |

If those collapse into one field, incident response quickly turns into a debate about semantics. A code like 101 - Decline can raise questions about retry timing, customer messaging, or integration handling. Those are different decisions.

Use docs as inputs, not source of truth#

Use provider docs as mapping inputs, not your long-term control layer. PDRC, Verifone API reason codes, and response codes from Worldpay should feed your model, not define it.

A practical check on any failed attempt is whether you can show the original provider payload, the normalized class, and the action policy that was applied. If not, you are still mixing layers. Raw response behavior can vary by acquirer path, and refusalCode is a string field up to 20 characters, so keep storage and parsing assumptions explicit.

For broader trend data on churn, trials, payment declines, and LTV, see Subscription Benchmark Report for Platform Operators: Churn Trials Payment Declines and LTV.

Map where the decline actually originated#

Make origin a first-class field so remediation can target the right layer. For each failed payment, separate whether the signal points to the issuing bank, payment gateway, payment processor path, or remains unattributed.

Shift4's framing is a useful baseline: the same customer-facing "declined" can come from the processor, gateway, or issuing bank. Stripe makes a similar architectural point from a different angle. It separates failures into three top-level categories, issuer declines, blocked payments, and invalid API calls, with different handling paths for each.

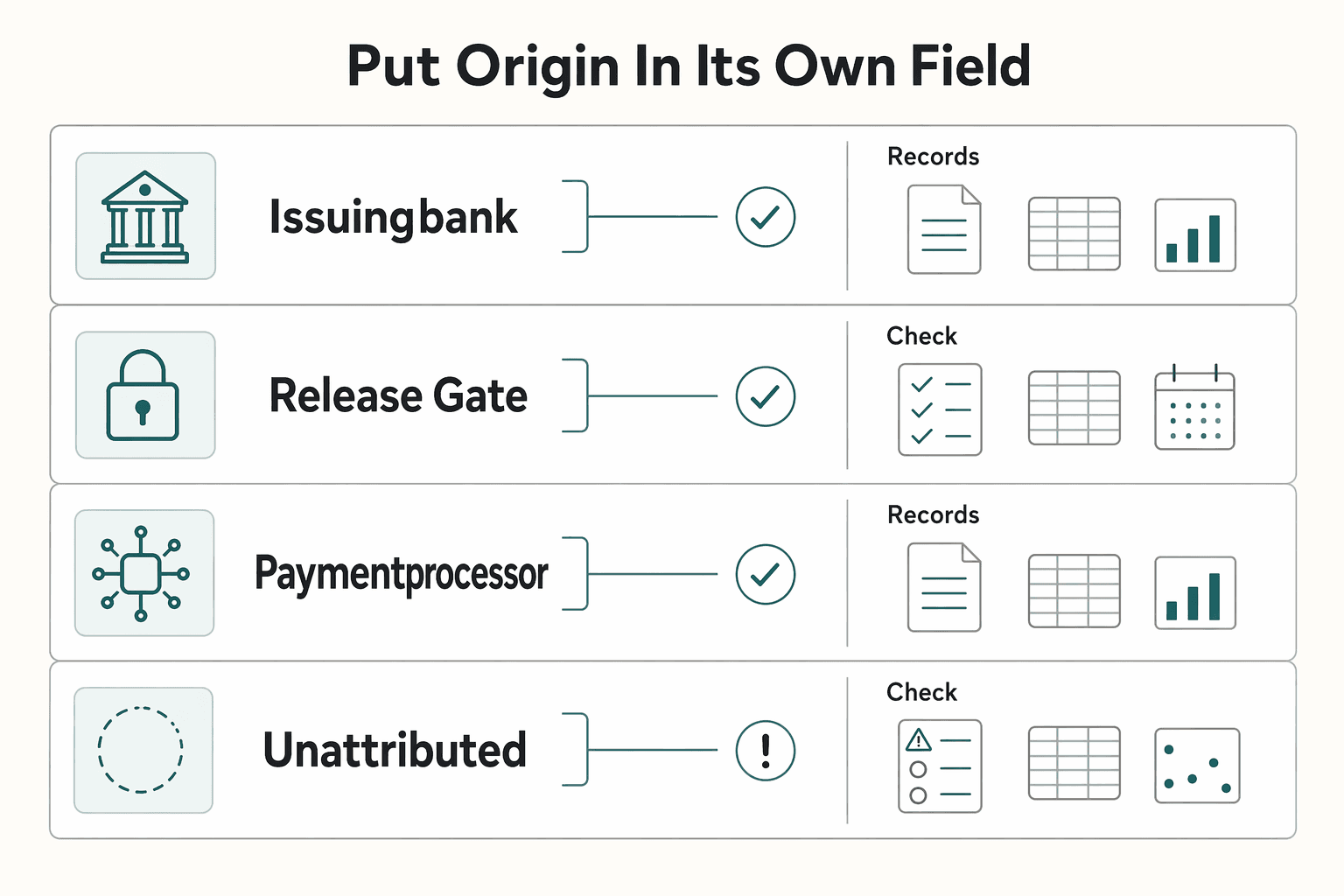

Put origin in its own field#

Do not bury origin in free text or try to reconstruct it later. Add origin_layer to your response model and make it explicit in the stored record.

| Field | Meaning | Typical next action |

|---|---|---|

issuing_bank | Authorization decision came from the bank or card issuer | Tune retry timing, customer prompt, and card-update flow |

payment_gateway | Blocked by gateway settings or gateway-side controls | Review gateway rules, filters, config, and request shape |

payment_processor | Failure surfaced on processor path | Check processor status, routing path, settlement state, and acquirer behavior |

unattributed | Evidence is insufficient to assign origin | Consider pausing automated remediation and escalating for operator review |

Braintree's distinction is useful here: gateway rejections are blocked by gateway settings, while declines are blocked by the customer's bank. If you merge those, integration defects and issuer pressure can end up in the same queue.

Add confidence, not fake certainty#

Origin is not equally explicit across providers, and raw responses can vary by processor configuration and by scheme over time. Model that uncertainty directly with origin_confidence, for example high, medium, or low, and tie it to evidence you can explain.

When a provider exposes source directly, preserve it. Shopify added a rejection-reason source field on March 16, 2026, which is exactly the kind of origin signal you should carry through instead of flattening away.

Treat unknown origin as operational risk#

When origin is unclear, consider unattributed as the default and require manual review before automated retries. That is an operational guardrail, not a universal industry rule.

Keep the checkpoint simple: for any failed attempt, one record should show the raw provider evidence, assigned origin_layer, and the rationale for origin_confidence. If any of those are missing, issuer decline reporting may be overstated and integration defects can stay hidden.

For benchmark ranges and peer comparisons, see Payment Decline Rate Benchmarks: How Your Platform Compares to Industry Standards.

Normalize provider codes into one internal taxonomy#

Once you have origin_layer, keep provider wording separate from product decisions. Do not let PDRC, Verifone, Payments.ai, or Worldpay codes drive behavior directly. Map them into a small internal taxonomy, and store the original provider value next to the normalized result.

Normalize to actions, not provider labels#

Provider semantics differ, even for similar outcomes. Global Payments' PDRC replaces generic 101, 102, and 103 decline responses with four categorized values. Verifone publishes one reason-code table across failed, declined, and successful transactions, so not every provider code belongs in a decline taxonomy. Payments.ai groups 200 series as Rejects and 300+ as Issuer Declines. Worldpay can expose an unmodified refusalCode from the scheme or acquirer when enabled.

Keep internal classes stable even when provider formats change. A practical set is retry_later, do_not_retry, validation_failed, and unknown. Those classes represent your decisions, not provider truth. Map directly when the provider signal is explicit. When it is broad or ambiguous, keep unknown until you have enough evidence.

| Provider artifact | Grounded meaning | Example normalized handling |

|---|---|---|

PDRC category 4 / code 133 | Explicitly "Declined. Do not retry." | do_not_retry |

Payments.ai 200 series | Rejects | Do not treat as issuer retry candidates. Map to validation_failed only when your own evidence confirms a non-issuer reject, else unknown |

Payments.ai 300+ | Issuer Declines | Requires code-level mapping before deciding retry_later vs do_not_retry |

refusalCode | Unmodified raw scheme or acquirer response code, if enabled | Preserve raw string, then map through your internal table |

| Verifone reason codes | One table spans failed, declined, and successful outcomes | Filter non-decline outcomes before normalization |

Avoid over-mapping whole provider families. A Payments.ai 300+ value tells you that it is an issuer decline, but not whether you should retry later or stop.

Keep raw and normalized side by side#

Use both. Raw codes support investigations and provider support. Normalized classes make retry behavior and reporting consistent.

One provider says raw response codes can inform retry logic. It also says those codes may change over time. Adyen warns that brittle logic tied directly to raw acquirer responses can break when issuers or acquirers change responses without notice. Keep raw values immutable, and anchor decisioning to normalized classes.

For each attempt, store:

provider_nameraw_coderaw_messagenormalized_classmapping_versionmapping_source, for exampleraw_scheme_codeorprocessor_response_code

mapping_source matters. Primer's model is to prefer raw issuer or network response codes, and fall back to processor response codes when raw values are unavailable. Without source tracking, later investigations become guesswork.

Also keep refusalCode as a string. Do not coerce it to an integer, or you can lose important formatting in variable-length raw codes.

Version the mapping like production config#

Treat taxonomy edits as controlled config. Worldpay notes that codes may be updated over time, and Verifone's reason-codes page shows a visible freshness marker, 09-Sep-2025. Provider semantics move, so ownership, versioning, and changelog discipline should be part of your internal mapping process.

For any normalized decline, you should be able to answer quickly:

- Which provider value came in?

- Which internal class did it map to?

- Which mapping version produced the result?

- When did that version become active?

Normalize provider codes into a small internal set, preserve raw response codes, and attach mapping_version to each decision. That gives you consistent product behavior without losing forensic detail.

Store the minimum decline event schema that survives audits#

If you cannot replay a failed attempt from stored data, your decline handling is hard to defend in an audit. A practical minimum is to keep each attempt immutable and reconstructable, then merge API and webhook signals into one timeline.

| Stored element | What to keep | Why |

|---|---|---|

| Per-attempt fields | provider_name, raw_code, raw_message, normalized_class, origin_layer when known, and decision_outcome | Keeps each attempt immutable and reconstructable |

| Idempotency linkage | An idempotency key or provider request ID for every create and retry path | Distinguishes a replay from a new request |

| Webhook delivery metadata | Delivery metadata for each webhook attempt | Duplicate deliveries can happen and redelivery can continue for up to three days |

| API and webhook linkage | Link webhook events to the originating API request when available and keep sync responses plus async events in one replayable timeline | Lets you reconstruct one timeline across both channels |

| Internal policy context | Operator notes or system rationale, if internal controls require them | Keeps extra context separate from provider-mandated fields |

Do not assume every API supports idempotency the same way. Where provider tooling supports created-order recovery, process events in that order. If your internal controls require extra context, capture operator notes or system rationale, but treat those as internal policy fields rather than provider-mandated ones.

Related reading: The Gig Economy in 2026: Payment Volume Trends Contractor Growth and Platform Consolidation.

Set retry and suppression rules that product and ops can enforce#

Start with one enforceable rule: retries run only when the mapped class explicitly allows them, not when a raw decline merely looks temporary.

Make the matrix explicit#

For each normalized class, define retry window, max attempts, user message template, and escalation owner. If any of those are missing, people will improvise under pressure. Keep the raw provider evidence visible behind each normalized class so the decision stays reviewable.

| Normalized class | Directional provider evidence | Enforced action | Customer message direction | Owner |

|---|---|---|---|---|

retry_later | Mastercard MAC 02 = "Cannot approve at this time, try again later"; PDRC 131 = "Could not approve. Further attempts permitted."; Worldpay Visa category 2 = reattempt up to 15 times over 30 days | Allow bounded retries with provider-specific caps where documented; add jitter if retries are automated | Temporary issue, try again shortly or we will retry automatically if applicable | Engineering owns automation; Ops reviews exceptions |

do_not_retry | Mastercard MAC 03 = "Do not try again"; PDRC 133 = "Declined. Do not retry."; Visa category 1 = "Reattempt not permitted" | Suppress automatic retries immediately | Use another card, update payment details, or contact issuer | Product owns wording; Ops handles escalations |

attempts_not_allowed | Global Payments PDRC 132 = "Further attempts NOT allowed." | Treat as hard suppression | Explain next step and do not promise background retry | Ops or Risk, based on org design |

unknown | No validated mapping or missing category guidance | No blind retry. Default to suppression and route for review until classified | We could not process this payment, try another method or contact support if urgent | On-call or payments operations |

Use Payments.ai as a starting pattern, not an automation rule#

Use Payments.ai, with 300+ issuer declines and 200-series rejects, for triage, not as final retry logic. Before you automate, validate provider meaning from Mastercard advice codes, Global Payments PDRC, or raw-response mappings from Worldpay.

A practical pre-launch check for any new mapping is to:

- confirm the docs explicitly say retry is allowed, delayed, or prohibited

- verify at least one real raw payload with code, message, and origin layer

- record the mapping version and owner for future updates

Treat mappings as versioned config, not one-time reference data, because provider code sets can change.

Bound retries hard, and suppress harder#

If class = do_not_retry, suppress immediately and show the next step. If class = retry_later, schedule bounded retries with explicit caps, and add jitter if they are automated.

The key control is the bound, not a universal jitter formula. Worldpay gives one concrete ceiling for certain Visa declines: category 2 can be retried up to 15 times over 30 days.

Over-retrying has a cost. PayPal warns that excessive retries can drastically impact network bandwidth. CardPointe notes that as of April 2022 Visa assesses fees on some decline reattempts under its Excessive Reattempts Rule.

Add a hard stop for unknowns#

Treat unknown as a governed state. When repeated unknown classes breach your own internal threshold, pause automation for that slice and alert on-call with raw payload context.

Include enough context for fast decisions: provider name, raw response code, raw message, normalized class, attempt count, mapping version, and linked API or webhook identifiers. Keep full raw code values intact. Make the default explicit too. If a decline has no category code, default to no retry until classification is validated.

If you're translating these classes into API/webhook behavior, use the Gruv docs to align retry, status, and audit-trail implementation details.

Make retries idempotent across APIs and webhooks#

Treat API calls and webhook events as separate arrival channels. Reconcile both against your own idempotency key and internal payment attempt ID before you make state changes.

Duplicates are expected. Stripe documents safe POST retries with the same idempotency key and notes that fulfillment logic can run multiple times, including concurrently, for the same Checkout Session. PayPal supports a similar pattern with PayPal-Request-Id, but support is API-specific, so confirm header support per endpoint before you rely on it.

Reconcile intent before you process outcome#

Decide first whether an incoming record is a new attempt, a replay, or a later update to an existing attempt. As a guardrail, avoid side effects until the message maps to exactly one internal attempt record keyed by business intent and request identity.

Keep raw provider decline fields as evidence on that attempt record. Use your internal identifiers for dedupe first, then run classification and retry policy.

Block stale updates from winning#

Late asynchronous events can overwrite newer retry outcomes unless you block them. Stripe explicitly warns that snapshot event data can be stale and recommends fetching the latest resource state before acting.

Add application-level transition guards, not just transport dedupe. If a newer attempt already reached a terminal internal status, record a delayed older event for audit but prevent it from changing customer-visible state.

Make the order of operations explicit#

Provider docs do not define one universal processing sequence, so define your own and enforce it. One workable order is:

- Classify the raw decline.

- Apply the action policy.

- Write the immutable ledger or event record.

- Emit customer status.

- Enqueue retry only if policy allows.

That order helps keep audit history intact and reduces the chance that retry jobs are queued before the underlying decline decision is durably recorded.

Verify what "final" means before ops sees it#

Do not show "final" outcomes until downstream status surfaces are proven consistent under replay. A single API action can emit multiple events, and Stripe can retry undelivered webhooks for up to three days, including after manual processing.

Before launch, test repeated POSTs with the same idempotency key, delayed webhooks after a later retry succeeds, and replay of already handled events. If any operator view can still flip a resolved payment back to declined, the flow is not final-safe yet.

Handle unknown and changing codes without breaking production#

Unknown decline codes can be normal, not just edge cases. If a code does not map, place it in an unknown/uncategorized bucket in your internal decline taxonomy, and keep handling non-destructive until triage is complete.

For new or unmapped codes, default to no blind retries and no permanent suppression. Global Payments notes that a bank decline does not always make retry eligibility clear, and its PDRC can include explicit outcomes like "Declined. Do not retry." Use that as provider-specific input, not as a universal policy.

Do not assume provider code tables are exhaustive or static across providers. Verifone states that some lists are not exhaustive and that result text can vary by processor or error. Worldpay notes that refusalCode can carry raw values not present in published tables. It also notes that those tables may change over time, and that raw codes can be strings up to 20 characters.

| Provider | Watchlist focus | Why it matters |

|---|---|---|

| Verifone APIs | Reason-code and platform-code pages, including update dates | Published guidance changes and text can drift |

| Global Payments | PDRC category behavior and no-retry outcomes | Retry decisions are not always clear from the bank decline alone |

| Worldpay | refusalCode first-seen values and table updates | Raw codes can be unseen, non-standard, and longer than expected |

Operationally, alert on first-seen raw codes by provider, and only move a code out of unknown after triage sets both its class and action policy.

Assign clear ownership across engineering, payments ops, and product#

Set ownership before rollout, or local fixes can slowly change your risk posture. A practical split is Engineering owning classification logic and the API response schema, Payments Ops owning exception handling and queue actions, and Product owning customer messaging policy. This is a working model, not an industry mandate. It lines up with how failures differ in practice: Stripe separates failures into issuer declines, blocked payments, and invalid API calls, and says each type needs different handling.

Put retry policy changes behind approval#

Treat retry policy edits as risk changes. Global Payments PDRC adds action-level detail for declines, including outcomes like "Declined. Do not retry," and Visa Acceptance reason-code guidance includes follow-up actions. So if you change a mapping from do_not_retry to retry_later, or expand auto-retry to a new class, require a formal approval path and documented approval by authorized parties before release.

Use a simple release gate: if a change affects automatic retry, suppression, or operator release behavior, it needs approval. Each deployed mapping version should be traceable to a change request ID, approval record, and test evidence for affected classes. To prevent silent policy drift, require a diff that shows the old class, new class, prior action policy, new action policy, and impacted provider codes.

Review misclassifications together#

Run a shared review for high-impact misclassifications. Incident responsibility should be explicit, and lessons learned should flow back into procedures, training, and testing. Closing the queue is not enough. Close the incident only after the taxonomy, tests, and operator guidance are updated.

Use one evidence pack for the review: raw provider payload, normalized class, action taken, customer message shown, mapping version, and whether the event came from an API response or webhook. Tie actions directly to taxonomy updates so ambiguous codes do not repeat.

Add module notes for MoR and Virtual Accounts#

Document module-level ownership notes for Merchant of Record (MoR) and Virtual Accounts flows. Stripe defines the MoR as the entity legally responsible for processing payments and liable for financial, legal, and compliance aspects, including refunds and chargebacks. If you use an MoR model, state whether decline escalations, customer follow-up, and evidence retention sit with the MoR owner even when normalized classes are shared elsewhere.

Do the same for Virtual Accounts. J.P. Morgan describes virtual accounts as unique identifiers for tracking and reconciliation, and notes they do not hold funds directly. In modules where exceptions are handled through reconciliation workflows, document that route explicitly and confirm coverage notes before rollout.

Related: Soft vs. Hard Payment Declines: How Your Platform Should Respond to Each.

Validate rollout with a concrete evidence pack#

Before you switch traffic, prove that the mapping and action rules work with stored evidence. A rollout is not ready unless you can show which raw code mapped to which normalized class, which action fired, and that retries did not create duplicate side effects. This validation is broader than code translation. It covers classification, retry behavior, routing, and compliance-sensitive escalation in one release.

Use a short pre-launch gate#

A practical pre-launch gate should answer four questions:

| Check | What to confirm | Failure to avoid |

|---|---|---|

| Mapping coverage | Observed provider values map to a defined class, and unlisted values route to unknown or manual escalation | Silent automation on unlisted values |

| Unknown-code handling | Uncategorized values do not trigger blind retry or silent suppression | Unsafe retry or suppression for new codes |

| Duplicate safety | The same request with the same idempotency key returns the same result instead of a second payment-side effect | Duplicate payment-side effects |

| Operator routing | High-impact classes land in the intended queue with raw payload, normalized class, and recommended action | Misrouted cases during review |

If you rely on provider-specific fields like Global Payments PDRC or Worldpay refusalCode, keep those raw values in test coverage because they can affect retry policy.

Compare outcomes by class, not only by total decline rate#

Check before-versus-after results grouped by normalized class. That is where false retries and false suppressions become visible, and it aligns with provider category models, for example success, decline, error, and fraud, and explicit states such as SUCCESS, DENIED, and ERROR.

You do not need a universal threshold. You do need a release stop condition: if a class shifts from do_not_retry to more retries, or from manual review to suppression, pause and inspect the mapping diff.

Keep the evidence pack reviewable#

Keep the pack compact but defensible:

- representative API and webhook payloads

- mapping version ID and approval or change reference

- old class or action versus new class or action for changed mappings

- retry test outcomes, including duplicate-request and webhook dedup tests

- audit trail exports that preserve sequence and ownership

For webhook validation, include duplicate-delivery handling in the test evidence: log processed event IDs, replay them, and show that no second operational action occurs.

Mark program variance before it surprises ops#

Do not treat one rollout result as universally valid. KYC, KYB, and broader AML or customer due diligence obligations can change routing by location, business type, requested capabilities, and enabled financial products.

Document that variance in the evidence pack up front. The main risk is silent divergence: the mapping looks correct, but program-specific or market-specific verification rules change escalation ownership and resolution flow.

Scope provider and program constraints before you promise behavior#

Promise only what the provider docs and your program setup actually support. The risk is not just a bad mapping table. It is promising deterministic retry or routing when coverage is partial, fields are optional, or outcomes depend on account or program configuration.

| Area | What is known | What is unknown or conditional |

|---|---|---|

Global Payments Payment Decline Reason Code (PDRC) | PDRC provides more detail on what action can be taken on a declined transaction. It is currently limited to Visa and Mastercard, and only certain acquirers. | Global Payments also says it is not always clear why a transaction was declined or whether it can be resubmitted, so retry certainty should not be promised. |

| Worldpay declines | refusalCode can return the unmodified raw response code if enabled, and refusal advice can add retry guidance. | Do not assume refusalCode is always present, scheme-identical, or static. Third-party acquirers can differ, codes may change over time, and raw code length can be up to 20 characters. |

| Adyen and Stripe program controls | Adyen requires verification before payments, payouts, and financial products. Stripe states KYC requirements change over time and vary by country, and field requirements can be checked via Country Specs API. | Do not present one fixed compliance or eligibility model across markets, account types, or product setups. |

In your external docs and support macros, use qualifier language such as "where supported," "if enabled," and "when available for this account and market." Mark program gates in the mapping record, not only in a wiki. Include provider limits, market scope, network or acquirer constraints, optional raw fields, enabled products, verification dependencies, and last-checked date. If MoR setup, connected-account eligibility, Financial Accounts program scope, or verification state can block execution for a given flow, route to an eligibility or manual class instead of forcing standard decline handling.

Set a recurring review cadence and treat provider docs as moving inputs. Worldpay notes that codes may be updated over time. Adyen warns that raw text can change without notice. References like Verifone reason codes carry explicit update dates, for example 09-Sep-2025. At each review, re-check field presence, semantics and coverage changes, compliance-by-country changes, and whether your docs still use "where supported" and "when enabled" where needed.

For a step-by-step walkthrough, see How to Build a Deterministic Ledger for a Payment Platform.

Conclusion#

A decline architecture stays reliable when you do three things consistently: preserve raw evidence, normalize once, and make product decisions from an internal class instead of whichever provider field arrived first. That keeps retries, messaging, reporting, and operator workflows aligned as you add processors, gateways, and issuer signals.

Provider semantics matter, but they are not a stable decision surface. Global Payments PDRC adds practical detail. Worldpay can return the unmodified upstream value in refusalCode when enabled. Mastercard decline details can include merchant_advice_code when an issuer declines a transaction, and those details can guide retry decisions. Keep these fields for investigation and escalation, but route automation through a stable internal layer.

This separation does not guarantee faster releases or cleaner operations on its own, but it can remove a common source of change friction. One retry matrix and one message policy can let you update behavior without rewriting provider-specific branches every time a code table shifts. That matters because semantics do change, and cross-gateway equivalence is not dependable.

Use one practical checkpoint before calling the system production-ready: from stored data, reconstruct a single attempt end to end without guesswork. You should be able to trace the API response plus webhook timeline, raw code and message, normalized class, origin layer, decision, attempt ID, and idempotency key. If an operator cannot answer what happened, which layer declined it, and why you retried or suppressed, the design is incomplete.

Keep one implementation risk front and center: duplicate and delayed events outlive clean retry diagrams. Stripe notes that idempotency keys can be removed after they are at least 24 hours old. Adyen can retry webhooks three times immediately and then from a queue for up to 30 days. If dedupe retention is shorter than the longest provider redelivery path, late events can reopen work or overwrite final state unless state-transition guards are enforced.

A practical first increment can be smaller than full code coverage across every provider. Consider three versioned artifacts:

- A mapping table from raw provider values to internal decline classes, including an explicit

unknownbucket and clear ownership for updates. - An immutable decline event schema storing provider name, raw fields such as

PDRCandrefusalCode, normalized class, origin, decision, attempt identifiers, webhook identifiers, and idempotency data. - A retry matrix keyed by normalized class with bounded retry behavior, suppression rules, customer messaging, and escalation ownership.

Then expand provider by provider using evidence, not assumptions. Keep sample payloads, mapping versions, and before-and-after retry outcomes so a new code or semantic change becomes a controlled mapping update, not a system-wide policy debate.

When you need to validate provider routing, policy gates, and market coverage before rollout, talk with the Gruv team.

Frequently Asked Questions

Who actually declines a payment, the issuing bank, payment gateway, or payment processor?

Any of them can decline it. Provider guidance notes that declines can come from the processor, the gateway, or, most commonly, the issuing bank. If origin is not explicit in your payload, keep it as unknown and investigate from raw response data instead of guessing in customer messaging or retry logic.

Can one global retry policy work across Global Payments, Verifone, and Worldpay?

Not as one unchanged rule table. Global Payments PDRC has scope limits, and Worldpay refusalCode is conditional (if enabled) and can reflect third-party acquirer behavior. Use one internal decision framework, but keep provider-specific mappings and guardrails underneath it.

What is the minimum decline data model a platform engineer should store?

There is no provider-agnostic mandated minimum in these sources, so treat this as an operational baseline, not a universal standard. Store provider identifiers, raw decline fields, your internal classification and decision, and stable attempt or transaction identifiers. Keep idempotency and webhook event identifiers for duplicate control. Also enforce a unique Order ID per transaction, since Global Payments states that each transaction must have a unique Order ID.

What should we do when a new decline code appears with unclear meaning?

Classify it as unknown, retain the full raw payload, and avoid blind automated retries until triage is complete. Visa Acceptance guidance says to contact Client Services when a received reason code is not listed. You can also log the mapping version used at processing time to support later root-cause analysis.

Should we prioritize raw provider reason codes or an internal decline taxonomy?

Use both. Raw provider values can preserve forensic detail, while your internal taxonomy gives you a stable layer for product behavior, retries, suppression, and messaging. For automation, drive decisions from the internal taxonomy and retain the raw fields for traceability.

How do idempotency key handling and webhook events reduce duplicate retries?

They help only when you persist and check them on every retry path. Stripe documents idempotency keys for safe retries and also warns that webhook endpoints can receive duplicate events, so dedupe must be explicit in processing. Keep processed-event state and idempotency records long enough for provider retry windows, including delayed webhook redelivery.

Which decline handling decisions should be controlled by engineering vs payments ops?

No provider-standard split is defined in these sources, so make ownership explicit in your operating model. Engineering should own durable controls such as schema, mapping logic, idempotency enforcement, and state-transition safety. Payments ops should own queue triage and provider escalation, with production rule changes moved back into versioned config or code.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

- csrc.nist.gov/pubs/sp/800/61/r3/finaltrusted

- developer.paypal.com/api/rest/reference/idempotencytrusted

- docs.stripe.com/declinestrusted

- docs.stripe.com/api/idempotent_requeststrusted

- finance.ec.europa.eu/regulation-and-supervision/financial-service...trusted

- finance.ec.europa.eu/financial-crime/anti-money-laundering-and-co...trusted

- developer.globalpayments.com/ecommerce/PDRCexternal

- developer.mastercard.com/mastercard-send-disbursements/documentation/...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: