Quick Answer

Define one benchmark cohort, then separate first attempts, failed retries, and pre-authorization blocks before comparing rates. Track Authorization Rate and Checkout Completion Rate side by side, and segment by processor path, issuing country, and payment method so owners can act on the right failure class. Keep any improvement only after it still reconciles through settlement files and payout records.

How to Benchmark Payment Decline Rates#

A useful decline-rate benchmark is not a headline percentage. It is a repeatable view of your own traffic that clearly defines the cohort, the processor path, and what happened after authorization through settlement and payout reconciliation.

Payment decline rate is easy to quote and hard to compare over time. If your denominator mixes raw attempts with repeated retries, the number can look better or worse without any real operating change. The first check is simple: are you measuring unique outcomes, or retry noise?

Why headline rates fail in operations#

Headline rates fall apart fast when processor traffic is blended together. If your stack runs across more than one processor path, one aggregate decline number can hide route-specific issues. The transaction path matters, and acquirer-to-processor connectivity is not unlimited. Processor-scoped analysis is usually a baseline requirement for meaningful comparisons.

Who this article is for#

This article is for finance, ops, and product owners who need metrics that hold up beyond the checkout result. If you own ledgers, reconciliation, settlement reporting, or payout execution, you need to confirm that front-end outcomes reconcile to transaction history, settled records, and funding or payout records.

That validation matters because acceptance movement alone is not an operations win. Where payout timing is manually controlled, payout reconciliation still has to match transaction history. Settlement confidence also depends on transaction-level records that confirm payments were settled and paid out, not just authorized.

What a benchmark needs before you trust it#

A benchmark becomes decision-ready when you can answer:

- Is the cohort raw or deduplicated, and were failed retries excluded?

- Is the view scoped to one processor path?

- What geography, payment-method mix, and time window are included?

- Can the result be validated against settlement and payout records?

If those answers are missing, treat the number as context, not a target. Methodology notes can change over time, and cross-region comparisons can break under country-specific network rules. Timing matters too. Analytics windows and reconciliation files can run on different daily schedules, so mismatched windows can create apparent incidents.

The rest of this article focuses on building a benchmark process you can run weekly, audit at month end, and improve without losing the link between authorization, settlement, and cash movement.

Start with clean definitions before you compare anything#

If your definitions move, your benchmark is noise. Before you compare trends or external references, lock one shared metric dictionary with each metric's stage, numerator, denominator, included payment methods, and retry treatment.

| Metric | How it's framed | Operational note |

|---|---|---|

| Payment Success Rate | Pair it with your decline view | Shows where failures happen, not just whether one percentage moved |

| Authorization Rate | Share of submitted authorization requests that were approved | Keep it separate from checkout funnel events |

| Checkout Completion Rate | checkout_started and checkout_completed are funnel events | If completion drops before authorization submissions, the issue is more likely checkout friction or abandonment |

Pair Payment Success Rate with your decline view so you can see where failures happen, not just whether one percentage moved. A decline metric can move while overall outcomes stay flat when retries or pre-authorization blocks are handled differently, and checkout abandonment is tracked as a separate funnel outcome.

Keep Authorization Rate and Checkout Completion Rate separate. checkout_started and checkout_completed are funnel events, while authorization success rate is the share of submitted authorization requests that were approved. If completion drops before authorization submissions, the issue is more likely checkout friction or abandonment than issuer behavior.

Split out failures that never reached issuer authorization. Some payments are blocked before an issuer is asked, so labeling every failed payment as an issuer decline misstates root cause and pushes teams toward the wrong fix.

Keep card decline metrics separate from all-method performance. Card acceptance maps to successful authorization, while some non-card methods are judged at capture after authorization. Mixing both under one decline label conflates network performance with non-card rail behavior.

Check whether a benchmark claim is trustworthy before you use it#

Use a benchmark as an operating target only after you can match its scope to your own traffic. If sample scope or transaction mix is missing, treat it as directional context, not a target.

Headline rates are not enough for decisions because they can hide differences in processor path, market mix, and checkout inputs. In practice, a headline number alone will not tell you enough.

Before you copy a benchmark into planning docs, use this comparison table and start with two checks:

- Timeframe alignment. If your internal rollup window differs from the source's processing window, the comparison can drift before performance differences are even evaluated.

- Transaction context alignment. Payment context and fields like MCC can change what a reported authorization or decline rate actually represents across categories, countries, and acquiring setups.

| Source | Cohort definition | Payment Gateway or processor scope | Geography | Payment method mix | Timeframe | Public methodology gaps |

|---|---|---|---|---|---|---|

| Stripe Acceptance analytics | Your own processed payments, including payment success rate and network authorization rate | Supports viewing multiple processors | Supports country-level cuts | Supports card-brand and input-method cuts; no cross-merchant benchmark mix is stated on this page | Data processed daily from 12:00 PM UTC to 11:59 PM UTC | Optimization calculations are estimates, not guaranteed outcomes; estimated-impact methodology can change |

| Cybersource analytics | Historical payment transaction data across authentications, authorizations, captures, and settlements | Includes processor dimension in decline analysis | Supports country-level decline analysis | Includes currency and other decline factors; benchmark transaction mix is not specified on this page | Previous six months | Public page describes analysis dimensions, not a published external benchmark cohort |

| PYMNTS 2025 Global Digital Shopping Index | Survey of 18,468 consumers and 3,464 merchants across eight countries | Gateway or processor scope is not specified in the cited sample disclosure | Eight countries | Transaction or payment-method mix is not specified in the cited sample disclosure | Fielded Oct. 17, 2024 to Dec. 9, 2024 | Commissioned by Visa Acceptance Solutions; confirm methodology details before using as an operating target |

| PYMNTS 2023 platform business survey | N = 196 PayFacs, ISVs, or marketplaces providing payment acceptance features | Gateway or processor scope is not specified in the cited sample disclosure | Geography is not stated in the cited sample disclosure | Transaction mix is not specified in the cited sample disclosure | Fielded July 10, 2023 to Aug. 25, 2023 | Small, specific sample; confirm transaction-path and method-mix details before target-setting |

Keep a short evidence pack for each external benchmark: source link, sample disclosure excerpt, field dates, sponsorship note, and a one-line judgment. If scope is not disclosed well enough to match your traffic, use the benchmark to guide questions, not targets. For related context, see How to Handle Payment Disputes as a Platform Operator.

Segment benchmarks by the paths that actually fail#

Use segmented benchmarks, not one blended decline rate. For decisions, split by the payment path components that can fail independently: Payment Method, region, Issuing Bank country, Acquirer or processor path, and first-attempt vs retry routing.

A blended Payment Decline Rate can hide opposite realities, such as healthy domestic authorization and weak cross-border corridors, or flat first-attempt performance masked by retry recovery. If you want a benchmark you can act on, segment by failure-path ownership.

Start broad, then cut toward the failure path#

Start with a wide view, then go deeper only when the upper layer shows concentration. Stripe acceptance analytics supports cuts like card brand, country, and input method, and Adyen troubleshooting highlights acquirer-supplied payment context, including payment instrument and shopper interaction.

| Segment level | What to split by | What it helps you answer | When to stop here |

|---|---|---|---|

| Global view | Payment Method, overall region, processor scope | Is Payment Success Rate or Authorization Rate actually moving? | Executive rollups or very low-volume programs |

| Corridor view | Merchant region to Issuing Bank country, domestic vs cross-border path | Is decline concentration corridor-specific? | When issuer/acquirer detail is too sparse to stay stable |

| Issuer/acquirer view | BIN, Issuing Bank country, Acquirer or processor, transaction type (ecommerce/POS) | Is one bank, BIN cluster, or acquiring path driving change? | Main operating layer when volume supports it |

| Checkout step view | Input method, shopper interaction, first attempt vs retry path | Is loss pattern tied to interaction type or retry behavior? | After upper layers isolate a clear problem |

This is an investigation order, not a universal industry standard.

Split first attempts from retries every time#

Keep first attempts and retries as separate populations. Stripe recommends analyzing unique declines and excluding failed retries for clearer authorization performance, and Braintree notes repeated attempts can skew decline rates.

If your setup uses different routing for initial attempts and retries, report those paths separately. Stripe Orchestration docs define a main processor for the initial attempt and a retry processor after failure, so merged reporting can hide where lift actually came from.

Use low-volume caution, not false precision#

Low-volume micro-segments can swing sharply from week to week, so false precision is a real risk. If a segment is thin, roll up one level and watch trend stability before you assign hard targets.

If declines are concentrated in one bank family or BIN range, investigate that path directly instead of treating it as a portfolio-wide problem. Braintree's 40% one-bank BIN example is directional concentration guidance, not a universal threshold.

Keep SaaS Subscription Billing renewals separate#

For SaaS Subscription Billing, separate first-time checkout from recurring collections. Stripe distinguishes first on-session customer-initiated transactions (CIT) from later recurring merchant-initiated transactions (MIT). It also notes the first subscription payment is typically on-session with about a 23-hour completion window.

Recurring collections are a different population and can include automated recovery logic. Stripe Billing supports Smart Retries, with a recommended default of 8 tries within 2 weeks. Mixing renewals into first-checkout benchmarks blurs customer-entry performance with recurring retry behavior, which makes both views less reliable.

Map decline causes to technical owners across the payment stack#

After you segment declines by corridor, attempt type, and payment path, assign ownership by failure class so the right team acts first. Do not route one blended decline bucket to every team.

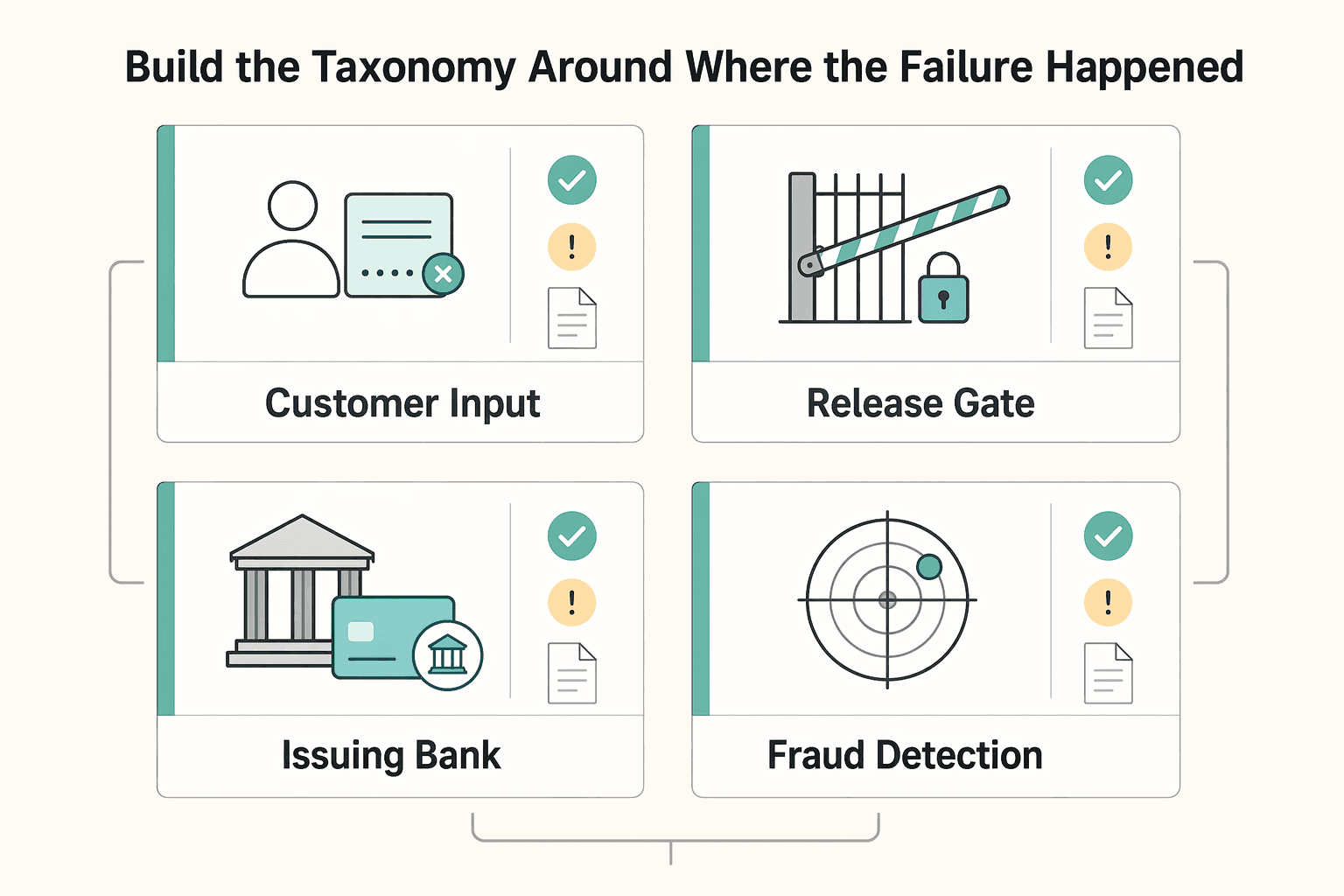

Build the taxonomy around where the failure happened#

Build the taxonomy around the point of failure, not the headline symptom. Use four owner lanes.

| Decline class | What it usually looks like | Primary owner | First action |

|---|---|---|---|

| Customer input or checkout abandonment | Shopper drops before completion, cancels, or fails a checkout step | Product / checkout team | Check Checkout Completion Rate, step-level drop-off, and whether the event happened before authorization |

| Payment Gateway, acquirer, or integration issue | API errors, acquirer-side errors, issuer not reachable, malformed requests | Payments engineering | Review provider request logs and refusal fields, then isolate by processor or acquiring path |

| Issuing Bank response | Authorization reached the issuer, but the issuer declined | Payments ops / issuer-acquirer owner | Split hard vs potentially recoverable responses, then test retry timing or routing only where retry is appropriate |

| Fraud Detection Systems decision | Merchant-side block or risk refusal before issuer approval | Risk / fraud team | Review risk rules, score thresholds, and false-positive candidates before changing routing |

This lines up with provider behavior: Stripe separates issuer declines, blocked payments, and invalid API calls, and Adyen exposes resultCode, refusalReason, and refusalReasonCode for classification. So 16 Shopper Cancelled is not an issuer issue, 4 Acquirer Error is not a fraud issue, and 20 FRAUD should go to risk review before routing changes.

For each decline cluster, first confirm whether authorization reached the issuer. If it did not, do not record it as issuer performance.

Use response families to decide if retry is eligible#

Retry only where responses indicate recoverability. Treating all declines as retryable adds noise and can distort performance. Checkout.com response families are practical for triage:

| Response signal | Meaning | Retry note |

|---|---|---|

| 20xxx | Soft decline | A later attempt may succeed |

| 30xxx | Hard decline | Usually requires issuer or cardholder remediation before retry |

| 4xxxx | Risk response | Belongs to fraud strategy rather than issuer retry logic |

| Visa recommendation code 03 | Decline that should not be retried | Suppress retries when the issuer returns a Do Not Try Again instruction |

Visa response categories also help with retry timing and eligibility. Recommendation code 03 indicates a decline that should not be retried, and retries should be suppressed when the issuer returns a Do Not Try Again instruction.

For subscription renewals, keep retry policy disciplined. The same Billing docs recommend the default Smart Retries pattern of 8 tries within 2 weeks; apply it only to declines that are retry-eligible.

Spend effort where evidence points#

Once a cluster is confirmed issuer-side, test issuer-path variables such as retry timing and, where relevant, routing path on eligible decline families. When a cluster is risk-side, review and tune Fraud Detection Systems first.

Provider docs note that blocked payments can come from Radar risk decisions, and legitimate blocked payments can be remediated through rule changes or allow-list adjustments. That is why risk-originated declines should be worked in the risk lane before routing experiments.

Also keep acquirer and issuer-availability incidents separate. Adyen distinguishes 4 Acquirer Error from 9 Issuer Unavailable; they require different owners and different actions. Predefined escalation lanes can make spike response faster and cleaner early in an incident.

Define escalation lanes before incidents#

- Finance or payments ops opens the incident, confirms cohort scope, and attaches Request ID or RID, transaction logs, processor, country, and response-family counts.

- Product owns shopper-cancelled and pre-authorization checkout failures tied to Checkout Completion Rate and step instrumentation.

- Payments engineering owns invalid API calls, gateway errors, acquirer errors, and issuer-reachability issues.

- Risk owns blocked payments and fraud-coded refusals first, including rule and allow-list review.

For Visa Acceptance card-decline triage, start with Request ID and transaction logs in the Enterprise Business Center. This creates a shared evidence baseline before escalation broadens.

The objective is simple: get the right owner the right evidence fast enough to improve Payment Success Rate without adding unnecessary retry traffic or extra risk. Related: SaaS Subscription Billing Benchmarks: Churn MRR Expansion and Payment Decline Rates.

Decide when to optimize routing and when to tighten controls#

Use a clear split: if issuer-linked declines rise while fraud loss is stable, test Transaction Routing before you add checkout friction or tighten fraud thresholds.

That split matters because these failures come from different decision systems. Issuer declines are decided on the issuer or payment-provider authorization side, while blocked payments are risk-side and may never reach issuer authorization. If blocked-payment share is flat but issuer declines are climbing, extra checkout friction alone is unlikely to fix the root cause.

Use a hard split before you change anything#

Before you change anything, confirm whether authorization reached the issuer. If it did not, start with fraud controls or checkout behavior before attributing the issue to issuer performance. If it did, review the decline response family, processor/acquirer logs, and any Merchant Advice Code (MAC) or equivalent guidance before you test retries or routing changes.

Do not create noise with retries. Hard declines are generally poor retry candidates, and network rules can prohibit reattempts in some cases. Even when retries are allowed, limits still apply. The Visa Category 2 reference of 15 times in 30 days is a ceiling, not a target.

Apply the counter-rule too. If approvals improve but abuse signals or false-positive complaints worsen, pause routing expansion and recalibrate Fraud Detection Systems.

Compare the interventions before you spend effort#

| Intervention | Best fit signal | How to validate | Main tradeoff |

|---|---|---|---|

| Transaction Routing across processor, Acquiring Bank, or network path | Issuer-linked declines up, blocked-payment share stable | Hold cohorts steady by issuer country, acquirer, and route. Checkout.com notes confidence can take a week to a month. | Can improve approvals, but adds payment-path reporting and reconciliation complexity. |

| Fraud Detection Systems recalibration | Blocked payments rising, false positives visible, abuse signals changing | Compare blocked-payment rate, approval rate, and abuse outcomes on the same cohort before and after rule changes. | Looser rules can raise abuse exposure; tighter rules can suppress legitimate payments before issuer contact. |

| Checkout UX or extra friction | Checkout Completion Rate falling before authorization, or customer input failures dominate | Verify step-level drop-off and confirm auth was never attempted. | Can cut conversion without changing issuer-side declines. |

Change one lever at a time. Routing, fraud controls, and checkout friction can all move conversion through different mechanisms, so changing them together makes attribution and rollback harder.

Write the tradeoff in language leadership can act on#

Treat vendor-reported uplifts as directional, not guaranteed outcomes, until your own traffic validates them. Use a plain-English decision note:

- Expected gain: higher authorization or payment success on issuer-side traffic.

- Risk cost: more abuse exposure or more false positives if controls are mis-set.

- Operational cost: more route-level monitoring, exception handling, and reconciliation overhead when adding processor or acquirer paths.

Carry this rule forward: when evidence is issuer-side, test routing on controlled cohorts; when evidence is risk-side, tighten or recalibrate controls first.

Before changing routing or risk thresholds, align your runbook with idempotent retries, status tracking, and webhook handling in the Gruv docs.

Run a seven-day incident sequence for sudden decline spikes#

Treat the first week as a structured incident template: confirm the spike is real, isolate where it sits, then change one thing at a time.

Day 1 and 2 triage#

Start by validating the metric before you diagnose causes. Rebuild the view from raw events, remove duplicate-attempt noise, and use consistent cohort definitions during triage. If available in your data model, use card fingerprints instead of charge IDs to reduce retry distortion.

Then separate failures into issuer declines, blocked payments, and invalid API calls so the right owners work the right problem. After that split, segment the spike by processor, issuing country, issuing bank, and BIN to find concentration. Also note the reporting window for the dataset you are using, since delayed processing can mislead same-day decisions.

Day 3 and 4 diagnosis#

Once the metric is stable, test concentration directly. Is the spike tied to one transaction-routing path, one payment method, or one checkout step?

Review processor-level and decline-code-level cuts together. If one route or acquirer path is the issue, decline codes and issuer or scheme response detail should cluster there. If you use Adyen, inspect resultCode, refusalReason, and refusalReasonCode, and review raw acquirer response detail where available.

Day 5 action#

Ship one controlled fix only, then evaluate before a wider rollout. Good candidates are a narrowly scoped routing adjustment, one checkout-step fix, or a targeted invalid API-call correction.

Define proceed or stop gates before release, for example:

- no clear recovery in the affected cohort after the next stable reporting cycle

- a worse mix of decline families after the change

- downstream capture or settlement issues even if authorization improves

Authorization recovery alone is not enough if funds do not capture cleanly.

Day 6 and 7 validation#

Validate recovery in the same segments where the spike appeared, not only in blended totals. Recheck authorization outcomes by processor, route, payment method, issuer segment, and checkout step.

Finish with lifecycle checks across authentications, authorizations, captures, and settlements. If authorization improves but capture or settlement quality degrades, treat the incident as unresolved. Related reading: State of Subscriptions 2026 Benchmarks for Platform Operators.

Tie benchmark improvements to ledger, reconciliation, and payout reliability#

A benchmark improvement is only real if it also holds up in accounting and cash movement. If Authorization Rate or Payment Success Rate improves but ledger traceability, settlement consistency, or payout reconciliation gets worse, treat the change as incomplete.

Use this section after incident triage to confirm downstream reliability, not just front-end acceptance. Acceptance analytics and back-office controls are different checks on the same payment flow.

Check the ledger before you celebrate#

Before you call a change a win, review Payment Success Rate and network Authorization Rate separately, then validate ledger linkage for the changed cohort. For Stripe, balance transactions are ledger-style records, and each includes a source field that links the balance entry to the related Stripe object.

Checkpoint: confirm you can trace each sampled payment from your internal record to the provider reference and the related ledger event in balance transactions. If that chain is inconsistent, month-end close risk can increase even when approval metrics improve.

Control for settlement timing before comparing periods#

Keep settlement timing and reporting windows stable before and after any routing or provider-path change. With Adyen, settlement occurs when a batch closes, and timing also depends on payout-frequency setup. Adyen batch reports provide credits, debits, and transaction counts. Transaction-level settlement detail supports per-transaction reconciliation and cost review.

| Check | What to compare | Why it matters |

|---|---|---|

| Batch consistency | Credits, debits, and transaction counts by settlement batch | Detects timing-window drift |

| Transaction traceability | Payment records to transaction-level settlement detail | Confirms settled records align with approved payments |

| Cost visibility | Transaction-level costs before and after the change | Highlights cost shifts alongside approval changes |

Watch payout friction as a downstream signal#

After benchmark changes, review payout exceptions, holds, and bank-deposit matching for the same cohort. Provider docs note that automatic payouts can include funds from multiple transactions, so payment-level improvement alone does not guarantee clean payout-to-bank reconciliation. Adyen reserve mechanics can deduct from pending and next payout balances, and in Stripe, paused payouts block transfers to bank accounts.

If approvals improve but payout reconciliation degrades, pause expansion and fix the cash path first. If you use Stripe bank reconciliation, note it is currently limited to direct US-based accounts on an automated payout schedule.

Keep the audit trail provider-specific but complete: internal payment record, provider reference, ledger or settlement event, payout identifier, and bank-deposit match. That chain helps finance defend month-end close.

Build the evidence pack your team can audit and reuse#

Standardize one monthly evidence pack and use it every month. That is how benchmark gains stay auditable, reusable, and defensible instead of turning into one-off wins.

At minimum, the pack should answer the same four questions in the same order each cycle: what was measured, which segments moved, what changed in production, and what happened before versus after. Keep definitions explicit. Track Payment Decline Rate, Payment Success Rate, and network Authorization Rate separately, and state whether authorization uses unique declines with failed retries excluded.

What belongs in the monthly pack#

Use one fixed structure so finance, ops, and product review the same evidence every time.

| Pack element | What to include |

|---|---|

| Metric definitions | Numerator, denominator, retry treatment, and reporting window |

| Segment tables | Global total plus the cuts most likely to explain movement, including region or country, payment type, decline code, issuer BIN, retry strategy, and any gateway or acquirer dimensions your data can reliably attribute |

| Intervention log | Date, owner, change ticket, hypothesis, affected traffic share, and rollback trigger for each gateway, routing, fraud, or checkout change |

| Before/after outcomes | Same cohort rules, same reporting window, and exact delta for declines and authorization |

For trend stability, include a trailing view alongside the current month. Cybersource describes the previous six months as a useful window across authentication, authorization, capture, and settlement stages.

Score outside sources before they become targets#

Use external benchmarks only after you record credibility notes.

| Source | What it can support | What to record before using it |

|---|---|---|

| Stripe | Analysis method and metric framing | Use for how to analyze Payment Success Rate and network Authorization Rate, not as a universal target |

| Cybersource | Segmentation dimensions and comparison windows | Record dimensions (country, payment type, decline code, BIN, retry strategy) and window assumptions |

| PYMNTS | Directional context when methodology is disclosed | Log sponsor, research producer, sample, geography, and fieldwork dates |

| Omnispay | Operational monitoring guidance | Treat as educational guidance, not audited benchmark standards |

| MidMetrics | Decline-rate fundamentals | Treat as educational guidance, not cross-industry proof |

| Sona | None from this research set | Do not use benchmark figures from this set |

| LinkedIn posts | Weak signal | Do not use as primary evidence without clear methodology and sample design |

If sample scope, payment-method mix, geography, or timeframe is missing, keep the source as directional context only.

Add checkpoints and keep a decision register#

Require three controls before sign-off: data freshness, cohort lock, and named owner approval. Record extract timestamp and provider report date, lock cohort rules before review, especially retry treatment, and attach sign-off for each gateway or acquirer change.

Keep a decision register next to the pack with one row per pattern: segment, suspected cause, action taken, result, owner, and next review date. That register is what lets the team resolve repeat decline patterns faster in later quarters.

For a step-by-step walkthrough, see How to Build a Deterministic Ledger for a Payment Platform.

Avoid the benchmarking mistakes that waste quarters#

The evidence pack matters only if it prevents bad decisions, not just bad math. The biggest misses are usually the same four.

- Using one global target without segment context

A single target across all payment networks and payment methods can hide the real issue. Review results by card brand, country, input method, and other payment dimensions before setting or reporting targets, and normalize scheme-specific refusal text because raw acquirer responses differ across schemes and can change.

- Treating every decline as fraud

Not every decline is a fraud problem. Payment failures include issuer declines, blocked payments, and invalid API calls, so classify the failure type first, then tune the right lever. Otherwise you can add friction while the real issue remains in issuer behavior or integration.

- Claiming success-rate lift without downstream validation

Payment success rate or network authorization rate improvement is not enough on its own. Authorized payments may not be captured, and settlement timing varies by location and payment method, so validate gains with transaction-level reconciliation against settled and paid-out records before calling it a clean win.

- Copying external benchmarks into internal targets

External benchmarks are directional until methodology and sample scope are clear. Use them as targets only when field period, sample, geography, cohort definition, and payment-method mix are disclosed.

Account for country and program variation before setting targets#

Set quarterly targets by market and program state, or do not set them. One Payment Decline Rate target across the US, eligible European countries, and cross-border traffic can hide real differences in Strong Customer Authentication (SCA), issuer behavior, and acquiring setup.

SCA is often a major adjustment. In eligible European countries, SCA is fully enforced, and authentication handling can directly affect Authorization Rate because banks may decline payments that are not properly authenticated. Qualify Europe targets by SCA scope, exemption usage, and payment-method mix. If those controls changed mid-quarter, treat that period as a program change, not clean operating performance.

Do not assume Europe authentication patterns will carry into the US or other non-SCA markets. One provider's US 3DS analysis found issuers often treated 3DS requests as higher risk and declined them more aggressively. A single cross-region benchmark can punish teams for market behavior they do not control.

Before you publish targets, lock a country-level matrix with:

- issuing country

- merchant or acquirer country

- SCA enabled state

- exemption usage

- payment gateway or processor route

- active risk-policy version

Use "Europe" carefully in target decks. In the PSD2 context, one-leg scope does not automatically cover non-EEA issued cards used at merchants acquired by EEA acquirers, so "SCA applicable" is not a universal label.

For cross-border programs, review payment networks and acquiring configuration before you attribute movement to team performance. Merchant and cardholder country mismatch can change network treatment, and local acquiring can improve issuer familiarity. If Payment Success Rate moved after an acquirer-country or routing change, call it out directly so setup effects are not misread as team execution changes.

For more on authentication-related declines, see Strong Customer Authentication (SCA) for Subscription Platforms: Reducing Decline Rates.

Conclusion#

A useful benchmark is not a headline percentage. It is a segmented, auditable operating view that separates authorization rate from conversion and payment success, then helps trace movement to likely failure points: gateway path, issuer response, or downstream settlement and payout.

Start with definition control. Authorization rate is the share of attempted payments that are approved, and authorization is not the same as conversion. If first attempts and retries are blended, teams can fix the wrong layer, so lock cohort rules and period comparisons before you set targets.

Then apply clear action logic. Use issuer and network detail, including raw acquirer responses, to diagnose why a transaction failed before deciding on retries or other changes. Visa response handling is category-based and includes explicit non-retry cases, and Visa Acceptance guidance says that when no category code is returned, the default is no retry.

Treat improvements as provisional until finance can reconcile them. One provider's acceptance analytics supports segmented analysis, including payment success plus network authorization with pivots, but impact methodology can change. Validate with your own before-and-after evidence. Confirm operational quality through payout and settlement reconciliation, including payout-to-batch matching, line-level payment, refund, and chargeback visibility, and provider-to-internal record mapping.

If you do one thing next, publish the same monthly evidence pack every cycle:

- Metric definitions and cohort lock rules

- Segment tables by auditable dimensions such as gateway path, issuer country or bank, payment method, currency, and first-attempt vs retry

- Intervention log with date, owner, and expected impact

- Reconciliation proof, including payout-batch matching, settlement lines, and provider or merchant reference mapping

If a number does not hold up under segmentation, retry scrutiny, and reconciliation, it is not a benchmark yet. If your benchmark program now needs tighter payout controls and audit trails, review how Gruv Payouts fits your operating model.

Frequently Asked Questions

What is Payment Decline Rate in one line, and how is it different from Payment Success Rate?

Payment Decline Rate is the share of payments declined during authorization. Payment Success Rate is a complementary metric, and Stripe recommends analyzing it alongside network authorization rate to understand where payments are failing. Use both so you do not treat every failed payment as the same failure type.

What benchmark range is reasonable to reference, and what caveats make that range unreliable?

There is no universal "good" decline-rate range you can apply across all platforms. External benchmarks are directional unless definitions align on acceptance rate, authorization rate, or capture outcomes, and on whether retries are excluded. For PSP-to-PSP comparisons, Checkout.com specifically recommends comparing acceptance rate rather than authorization rate.

Are high declines usually a fraud problem or a data and infrastructure problem?

High declines can come from either fraud-related pressure or operational issues, so treat both as active hypotheses. Provider docs note declines can indicate fraud or integration issues, and Checkout.com also includes temporary issuer, acquirer, and network outages as causes. Diagnose before you add friction.

Which segmentation dimensions should we prioritize first for platform operations?

Start with issuing country, issuing bank, and issuing BIN, since those are primary filters for investigating authorization failures. Then segment by decline code, processor, and currency to isolate likely root causes. Also separate unique first-attempt declines from retry noise when measuring performance.

What should a team do in the first seven days after a decline-rate spike?

There is no strict industry-standard seven-day runbook in the retrieved sources. In that first week, validate metric definitions and remove retry noise, then segment quickly by country, bank, BIN, processor, currency, and decline code to localize the issue. As you test fixes, monitor not just authorization movement but also downstream capture, settlement, and chargeback quality.

What minimum methodology details must exist before we trust an external benchmark?

At minimum, you need clear metric definitions and comparability rules: what is being measured, whether that means acceptance, authorization, or capture, and how retries are handled. You also need sample context and timing, not just a headline number. A disclosed survey sample can be useful context, but it still does not make rates automatically comparable to your program.

How do we confirm that decline-rate improvements did not break reconciliation or settlement quality?

Do not treat authorization lift alone as proof of success. Provider docs note authorized payments may still fail to capture, and Checkout.com separates capture rate from authorization performance. Confirm improvements with downstream checks, including settlement and chargeback monitoring, before calling the change operationally clean.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

- docs.stripe.com/payments/analytics/acceptancetrusted

- docs.stripe.com/declinestrusted

- eba.europa.eu/single-rule-book-qa/qna/view/publicId/2018_4233trusted

- eur-lex.europa.eu/eli/reg_del/2018/389/2023-09-12/engtrusted

- eur-lex.europa.eu/eli/reg_del/2018/389/oj/engtrusted

- itl.nist.gov/div898/handbook/ppc/section3/ppc333.htmtrusted

- checkout.com/docs/payments/optimize-payments/boost-accept...external

- checkout.com/docs/business-operations/monitor-payment-per...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Churn Rate Benchmarks by Industry for Payment Platforms

If you run a payment platform, start with this assumption: there is no single churn benchmark you can safely copy from search results. Published benchmarks come from different market cuts, including broad industry datasets, B2B SaaS reports, subscription-app reports, and payment-method segments. These are not directly comparable without normalization.

How to Compare SaaS Billing Benchmarks Before Expansion

For expansion decisions, treat payment decline rate, churn, and expansion as one system, not three separate metrics. That gives product, finance, and GTM a view they can defend before rollout resources are committed. If you own the budget call, you need that view before your team starts treating one good month as a trend.

Strong Customer Authentication (SCA) for Subscription Platforms: Reducing Decline Rates

If you want fewer surprises, treat SCA as a scope and sequencing decision, not a feature hunt. This ranked list is for teams running recurring collections across markets that want to reduce avoidable decline risk under PSD2 without adding unnecessary checkout friction.