Quick Answer

Subscription platforms reduce avoidable SCA-related declines by classifying each payment event before changing 3DS behavior, authenticating the first charge or setup stage correctly, and reviewing renewal changes separately from routine renewals. Exemptions should be an optimization layer, not the core strategy, and weekly metrics should be segmented by CIT or MIT, region, and flow type so issues can be traced and fixed.

Strong Customer Authentication for Subscription Platforms That Need Fewer Surprises#

If you want fewer surprises, treat SCA as a scope and sequencing decision, not a feature hunt. This ranked list is for teams running recurring collections across markets that want to reduce avoidable decline risk under PSD2 without adding unnecessary checkout friction.

- Define scope before adding authentication.

In the material here, SCA under PSD2 is triggered when a customer initiates an online transaction and both banks are in the EU or the UK. Start by mapping which payment events can fall into scope, which do not, and where bank location changes the answer. Keep refunds on a separate decision path; the material here treats refunds as outside SCA scope. If finance, legal, and payments ops label the same flow differently, your decline analysis will break before you even assess authentication behavior.

- Apply the actual requirement and assign ownership clearly.

SCA requires at least two authentication elements. Even though banks perform authentication, your business is still responsible for implementing the required checks in the payment process. The tradeoff is operational: stronger authentication can improve security, but it can also add friction. Teams usually get into trouble not because PSD2 is unfamiliar, but because authentication decisions are applied too broadly, too late, or without a shared record of why.

- Prioritize controls that reduce avoidable risk first.

SCA has been established for years, so the priority is execution discipline, not novelty. Work in this order: confirm applicability, place authentication at the right point in the journey, and verify outcomes with records your teams can audit. Maintain a dated flow inventory, document bank-location assumptions, and retain provider response records for exceptions and edge cases. If you cannot explain why one charge path was handled differently from another, you have both a compliance gap and a debugging gap.

Selection Criteria for This List and Who It Is For#

Use this list as a practical prioritization tool for subscription payments under SCA, with one important caveat: the evidence behind this section is stronger on EU VAT and OSS compliance operations than on PSD2- and SCA-specific rules.

- Regulatory exposure is the first filter.

Start with controls that reduce cross-border inconsistency. EU VAT rules for cross-border B2C e-commerce changed on 1 July 2021, and official guidance says everyone in the supply chain is affected, including platforms.

- Auditability is the second filter.

Rank controls higher when your team can show a dated record of what was done and why. In OSS, that means concrete artifacts such as electronic VAT returns and required platform record-keeping, with filing cadence of quarterly for Union and non-Union schemes and monthly for the import scheme. As a working standard, rely on official europa.eu guidance and retain the version and date you used.

- This list is for teams with shared compliance ownership.

It fits best when risk, finance, and payments ops coordinate across markets and need repeatable decision records. The process bar is high. Under OSS, selecting the Member State of identification can bind you for the current calendar year plus the two following calendar years.

- Use this as a decision list, not a feature chase.

Adopt the higher-ranked controls first, then add lower-ranked controls only when your own records show a real gap. If you operate in a narrow, single-market setup, this may add more process overhead than value.

That framing matters because the first operational mistake usually happens before any 3DS setting is touched: teams do not classify payment events cleanly enough to make consistent decisions.

1 Classify Every Payment Event as CIT or MIT Before You Touch 3DS Logic#

Start with a clear event taxonomy before you change 3DS behavior. If your team cannot consistently label payment events internally as CIT or MIT, your 3DS decisions become much harder to apply and explain.

This matters most in mixed flows such as sign-up charges, scheduled renewals, invoice collections, and retries. Those flows can share billing code while reflecting different customer interaction patterns, so classification should be explicit at event level.

Best for#

Use this first if you run both on-session and off-session payments and have accumulated billing exceptions over time. You may label first checkout and later renewals differently in your Payment Intents API and billing logic, but treat that as an operational label, not a legal conclusion on its own.

Why classification comes first#

Not every 3DS flow requires an explicit challenge. Low-risk transactions can proceed through a frictionless flow, and 3DS is always a tradeoff between security, user experience, and authorization performance. That is why event classification comes first. You need a reliable event map before you can decide authentication behavior.

What to label and verify#

At minimum, keep the following for each payment event:

- your internal event label, such as checkout, renewal, plan change, invoice charge, or retry

- whether it was handled in-session or off-session

- the 3DS path requested and the provider response returned

Then validate your logs against provider artifacts. Where supported, session-retrieval endpoints such as Mastercard Retrieve Session can confirm the request fields stored in session, with authenticated access. Do not treat correlationId as durable evidence; it is transient and does not persist in the gateway.

Red flags and practical rule#

A common failure mode is one shared payment path reused across different event types with only the UI text changed. Reporting can look tidy while the underlying event labels are inconsistent.

Use a simple rule: if customer interaction changes, create a separate event class first, then set 3DS behavior for that class. Keep a compact evidence pack per class with the request summary, provider response, session or intent identifier, and a dated rationale for the label.

2 Authenticate the First Charge Correctly for Immediate and Trial Starts#

Get the first customer-facing payment event right. If you charge at signup, handle authentication there. If you charge later from stored credentials, set up authentication at signup while the customer is present.

Do not fold charge-now and charge-later starts into one reusable checkout path. Stripe separates recurring revenue into 5 key payment flows, and these two behave differently. That distinction matters because SCA is broadly enforced across eligible European countries, and missing authentication can lead to bank declines.

- Immediate start: authenticate on the first paid checkout

If a subscriber is charged at signup, that payment is the checkpoint to complete 3DS when required. Do not defer this to renewal or retry logic. Your records should clearly show the initial paid signup path, the provider's authentication result, and the intent or session ID tied to that checkout.

- Trial start: prepare authentication during signup for later stored-credential charging

If signup happens now and charging happens after a free trial, set up authentication while the customer is in session when your conversion flow relies on stored credentials. This reduces the risk of discovering authentication gaps only at the first post-trial charge. Mastercard's Europe authentication guide also treats delayed charge and free-trial scenarios as a separate use case, which supports handling this path explicitly.

- Validate both paths separately before rollout

A shared signup component can create duplicate customer prompts if setup and payment logic are layered poorly. A reported Stripe integration issue described users being asked for card details and 3DS twice. Treat that as a practical failure mode to test for. Confirm one card-entry and authentication experience per path, and keep provider responses plus intent or session identifiers together in your evidence pack.

Once first-charge handling is clean, the next risk is assuming every later charge is just a routine renewal. That is where misclassification starts to compound.

3 Treat Renewal Changes as a Separate Risk Class Not a Minor Variant#

Do not treat every post-signup charge as the same recurring event. Under Article 98 of Directive (EU) 2015/2366 (PSD2), the RTS covers both Strong Customer Authentication (SCA) requirements and exemptions, so renewal changes, invoice charges, and ad hoc charges should be reviewed as separate decisions, not inherited defaults. If you need the wider operator view, keep a separate reference to PSD2 and PSD3 compliance for platform operators instead of merging every charge type into one rule path.

This is where teams usually fail. The problem is rarely ignoring SCA outright. It is assuming a changed charge is close enough to a normal renewal. The EBA consultation record supports a cautious approach here: the 2016 Consultation Paper received 224 responses and surfaced around 300 issues or clarification requests, including on exemption scope and thresholds.

Use a comparison table that forces a fresh decision#

| Payment event | CIT/MIT posture to confirm, not assume | SCA or exemption review trigger |

|---|---|---|

| First charge now | Customer-facing classification is often used, but confirm your actual setup | Review at first paid checkout and do not carry this decision forward automatically |

| First charge later | Treat signup and later collection as separate events | Review the original agreement and the delayed collection event separately |

| Recurring renewal | Do not force a fixed renewal label | Reassess when amount, timing, frequency, or billing basis changes |

| Invoice charges | Classification depends on how invoice payment is initiated and collected | Review when invoice collection differs from your standard subscription route |

| Ad hoc charges | Highest risk of mislabeling as normal recurring | Review each exception before reusing prior exemption or classification logic |

What to verify in practice#

For each changed renewal or non-baseline charge, keep a decision record with:

- who initiated the payment event in practice

- what changed versus the baseline recurring agreement

- whether an exemption was used

- the provider response or payment artifact tied to that decision

- the internal owner who approved any exception path

The failure mode is false sameness#

The common risk is false sameness. Upgrades, overages, or manual collections get routed through baseline renewal logic because they are still subscription revenue. That may work operationally, but it weakens your ability to defend classifications when issuer behavior changes or a decision is challenged. The EBA itself describes this area as involving difficult tradeoffs between competing PSD2 objectives, so uniform treatment of all later charges is usually convenience, not control.

A practical team rule#

If a charge differs from the baseline subscription in amount, timing, frequency, or billing reason, route it through a separate review path before reusing the same CIT or MIT posture. Apply the same rule to invoice and ad hoc charges. This adds maintenance and testing overhead, but it is usually lower cost than defending a broad renewal label that covered multiple risk classes.

4 Use Exemptions as an Optimization Layer Not a Compliance Strategy#

Exemptions can help, but they are not the foundation of a sound SCA posture. Use them as an optimization layer only after your baseline flow can still complete when an exemption is not accepted.

Under Article 98 of Directive (EU) 2015/2366 (PSD2), the RTS covers both SCA requirements and exemptions. Build your operating model around that structure. Keep the compliant path primary, and treat exemption paths as conditional performance improvements.

Where exemptions help#

Exemptions, including transaction risk analysis (TRA) paths, can reduce friction when they are accepted. But exemption scope and thresholds were major consultation issues, and the RTS itself reflects tradeoffs between competing PSD2 objectives. Expect variable outcomes and review performance continuously rather than assuming steady gains.

What to verify before tuning exemptions#

- your 3DS stack supports 2.1, 2.2 or later when the optimization depends on newer 3DS features

- your provider logs show whether an exemption path was attempted, whether 3DS was triggered, and the final issuer outcome

- your reporting can segment outcomes by issuer and geography so you can isolate concentrated drops

Fallback rule when acceptance weakens#

If exemption acceptance drops in a specific issuer or geography segment, route that segment to stronger authentication defaults instead of repeating the same exemption retry pattern. When performance is unstable, prioritize the path that can complete with SCA and handle recovery in failed-payment operations.

What to keep in your evidence pack#

For each exemption-tested flow, keep a reviewable record of:

- payment classification

- exemption or low-risk path attempted

- provider response artifact

- whether 3DS was invoked

- issuer outcome by segment

If a use case remains unclear, escalate early to payments ops, PSP support, and legal. Published guidance acknowledges that some SCA requirements still need refinement for certain scenarios.

5 Build an SCA Control Set by Priority Not by Feature Availability#

Build your control set around decision quality and cost impact, not around whichever Stripe feature is easiest to switch on. In practice, define the control logic first, then use Stripe Billing and Stripe Radar to implement it.

Use the pricing facts below to pressure-test each new rule before you ship it:

| Stripe setup choice | Concrete pricing fact | What it means for control priority |

|---|---|---|

| Standard payments pricing | 2.9% + 30¢ per successful domestic card transaction, 3DS included at no additional charge, no setup, monthly, or hidden fees | Bundled 3DS can make extra rules feel harmless. You still need to prove the rule adds control value rather than complexity. |

| Custom pricing | $0.03 per 3DS attempt | More authentication attempts create direct incremental cost, so low-value branching is easier to spot. |

| Managed Payments | 3.5% fee on each successful transaction, in addition to standard Stripe processing fees, and additional charges apply for subscription payments | Control choices can affect unit economics quickly, so finance review should happen before rollout. |

Before you add a new Radar branch or Billing configuration, run one gate:

- confirm the account's actual Stripe pricing model

- confirm whether your country-specific pricing page supersedes the generic fee table

- confirm whether the change increases 3DS attempt volume, not only successful payments

The failure mode to avoid is feature-led complexity: a large rule stack with weak control rationale. Treat Managed Payments as additive, not a replacement for standard processing fees, and assign explicit approval ownership across risk, engineering, and finance.

After the control set is in place, the question becomes whether it is doing what you intended. That only shows up if you measure the right things and segment them correctly.

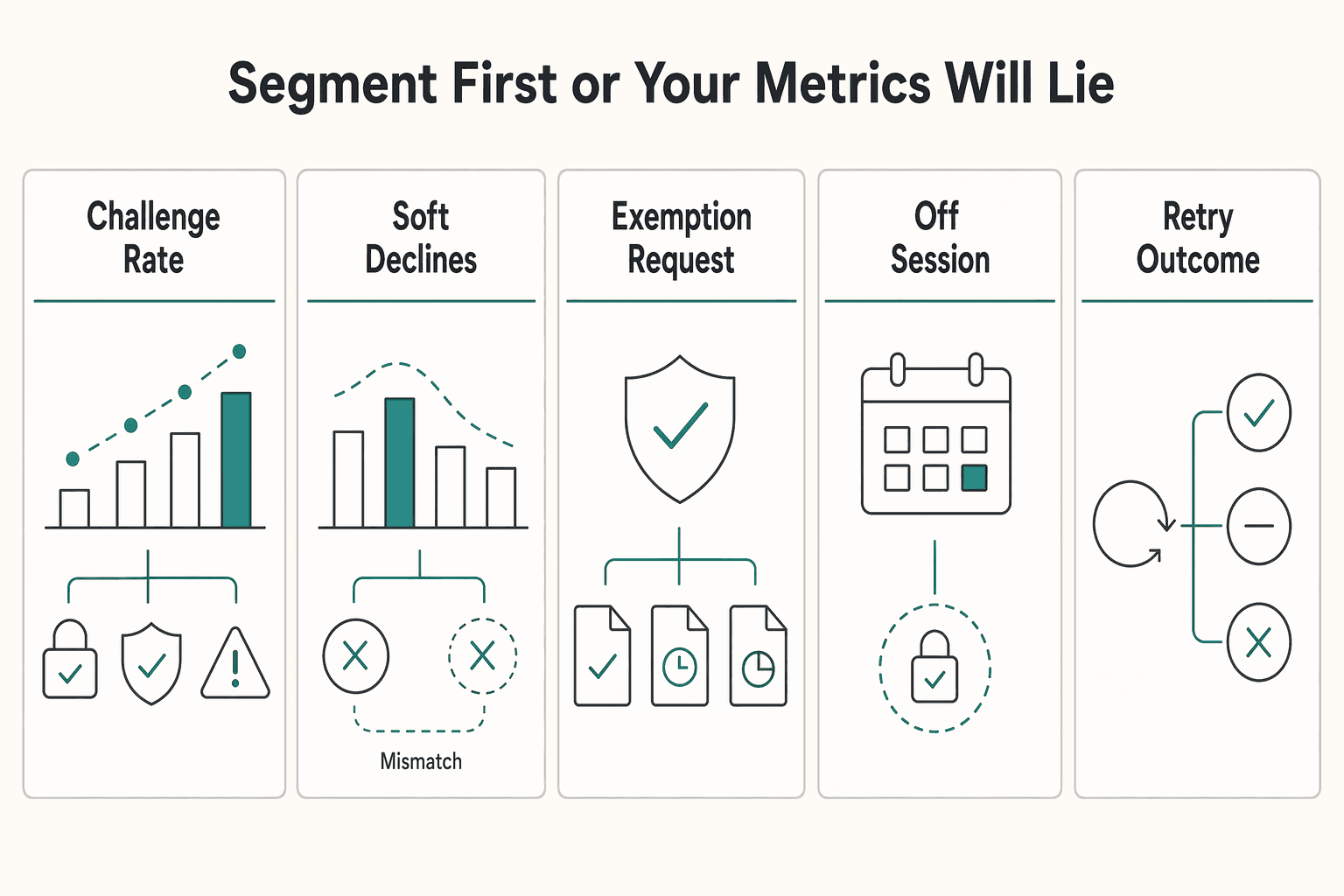

6 Track the Minimum Metrics That Actually Predict Decline and Compliance Risk#

A small weekly scorecard, segmented correctly, will tell you more than a broad monthly dashboard. For subscription payments subject to SCA, blended reporting often hides where authentication friction is actually happening.

Under PSD2, SCA has been in force since September 2019, and implementation complexity across European payment systems has been a recurring challenge. Treat region-level splits as required context, not optional reporting detail.

Segment first or your metrics will lie#

Start with three cuts: CIT vs MIT, region, and payment flow type such as first payment, trial conversion, scheduled renewal, invoice charge, or retry. If you skip one, you risk masking where 3DS friction rises or where exemption behavior shifts.

Before sharing metrics with finance or risk, verify the data mapping in your integration. A practical checkpoint is unit testing plus record-level review. Confirm the CIT or MIT label, 3DS outcome, and PSP response align with what your billing logic intended.

| Metric | Segment it by | What it tells you | Verification detail |

|---|---|---|---|

| Challenge rate | CIT vs MIT, region, first payment vs renewal | Where authentication friction is concentrated | Confirm PSP 3DS status matches your app event label |

| Soft declines tied to authentication | Region, flow type, retry attempt number | Whether failures are linked to authentication handling | Separate auth-related decline reasons from generic failures |

| Exemption request and acceptance rate | Issuer region, payment flow, acquiring bank | Whether exemption routing is still being accepted | Confirm the exemption flag was actually sent |

| Off-session payment recovery rate | MIT renewals, trial conversions, retry sequence | Whether off-session collection is recovering payments | Compare the first failed attempt with the next successful action |

| Retry outcome by acquiring bank | Acquiring bank, flow type, region | Whether issues are concentrated in one acquiring setup | Keep acquiring bank identifiers in failed-payment exports |

Read combinations, not single lines#

Single metrics can mislead. The better signal is how metrics move together inside the same segment, such as rising challenge rates with weaker completion or approval, or high exemption requests with falling acceptance.

Authentication-linked soft declines usually deserve priority over generic failed-payment totals because they point to fixable classification or authentication-path issues. When a cluster appears in one region or flow, inspect classification and 3DS behavior before changing retry logic.

Escalate with an evidence pack, not with a screenshot#

When performance worsens in a specific CIT or MIT segment, escalate with traceable evidence: payment IDs, timestamps, CIT or MIT labels, 3DS status, exemption flag status, acquiring bank, and retry sequence. That gives your PSP and internal teams a usable investigation set.

Use external benchmark reports as context only. Some widely cited payments findings come from surveys of more than 1,000 merchants conducted in November and December of 2022, and are explicitly described as informational rather than advice. They should not replace your own weekly evidence.

If off-session recovery weakness starts to affect collections, pair this scorecard with your dunning review in A Guide to Dunning Management for Failed Payments. The operating rule is simple: track fewer metrics, but make each one traceable to a flow, a region, and a decision you can change.

7 Define Escalation Triggers Before Incidents Happen#

Define escalation triggers before the incident, not during it. Focus them around three things: cross-border interpretation disputes, OSS decisions that can create multi-year lock-in, and auditability gaps. If legal, tax, finance, and payments are split across markets, this keeps the same issue from stalling in parallel queues.

| Escalation path | Trigger | Required detail |

|---|---|---|

| VAT Cross Border Rulings (CBR) | Teams cannot align on the VAT treatment of a complex cross-border transaction | Document the countries, entities, transaction pattern, and exact point of disagreement; if two or more companies are involved, one should submit on behalf of the others |

| Executive signoff on OSS choice | A proposed fix touches registration location, filing ownership, or invoicing treatment | Require written signoff before implementation; the Member State of identification can bind the calendar year of the decision plus the two following calendar years |

| Audit escalation | The evidence pack will not hold up under filing review | Use transaction records, affected countries, internal decision notes, provider correspondence, invoice or record references, and impacted periods; OSS returns are quarterly for Union and non-Union schemes and monthly for the import scheme |

1 Formal clarification when cross-border interpretation is the blocker#

Escalate when teams cannot align on the VAT treatment of a complex cross-border transaction. In the EU, VAT Cross Border Rulings (CBR) exist so taxable persons can obtain advance rulings on complex cross-border VAT transactions involving two or more participating countries.

Set a checkpoint before opening that path: document the countries, entities, transaction pattern, and exact point of disagreement. If two or more companies are involved, one should submit on behalf of the others, and the request must follow national VAT-ruling conditions in the participating country where it is introduced.

2 Executive signoff before OSS choices that can lock the business in#

Escalate before making incident-driven OSS registration changes. Under OSS, a taxable person registers in one Member State of identification, and that Union-scheme choice can bind the calendar year of the decision plus the two following calendar years.

In normal circumstances, that Member State cannot be changed unless the fixed establishment in the current Member State is dissolved or moved to another country. If a proposed fix touches registration location, filing ownership, or invoicing treatment, require written signoff before implementation.

3 Audit escalation when evidence is weaker than filing cadence#

Escalate when your evidence pack will not hold up under filing review. OSS guidance explicitly covers record keeping and audits, and return cadence is defined: quarterly for Union and non-Union schemes, monthly for the import scheme.

Use an evidence bundle that goes beyond a screenshot: transaction records, affected countries, internal decision notes, provider correspondence, invoice or record references, and impacted periods. If that bundle cannot be assembled within your response SLA, route immediately to the owner of records and filings.

8 Keep an Audit Evidence Pack That Proves Decision Quality#

Keep an evidence pack that makes each SCA decision traceable: what you decided, why you decided it, what tradeoff you accepted, and who approved it.

| Evidence item | Store | Why it matters |

|---|---|---|

| Decision memo | Date, owner, affected flow, options considered, final decision, and rationale | Shows which logic was live when a decline pattern, partner query, or audit question appeared |

| Flow map | Classification logic and labels such as CIT, MIT, or similar flow types | Links labels to expected behavior so reviewers can see why similar payments may take different paths |

| Provider artifacts | Response payload fields, status signals, exemption outcomes, retry decisions, and timestamps where available | Lets the team reconstruct what the PSP or issuer actually did for a given transaction |

| Exception approvals | Approver, reason, time window, and review trigger | Makes tradeoffs explicit rather than informal or open-ended |

This fits the way SCA rules were developed. Under PSD2 Article 98, the EBA developed the RTS on SCA and CSC in close cooperation with the ECB, with a documented process: a December 2015 discussion paper with 118 responses, an August to October 2016 consultation with 224 responses, and assessment work that identified around 300 clarification issues. Decisions are expected to be legible and reviewable, especially when objectives compete.

1 Decision memo tied to a specific rule version#

For each material rule change, store a short note with the date, owner, affected flow, options considered, final decision, and rationale. The key control is version clarity. You should be able to show which logic was live when a decline pattern, partner query, or audit question appeared.

2 Flow map that links classification to behavior#

Keep the classification logic, not only the final outcome. If your team uses labels such as CIT, MIT, or similar flow types, map those labels to expected behavior so reviewers can see why similar payments may take different paths.

3 Provider artifacts that corroborate internal decisions#

Store provider-side artifacts with internal records, including response payload fields, status signals, exemption outcomes, retry decisions, and timestamps where available. Your internal rule is incomplete if you cannot reconstruct what the PSP or issuer actually did for a given transaction.

4 Exception approvals with explicit tradeoffs#

When approving an exception, record the approver, reason, time window, and review trigger. The RTS history explicitly reflects tradeoff handling across competing PSD2 objectives, so your exception log should do the same rather than treating exceptions as informal, open-ended decisions.

If you do one thing, standardize this template. It reduces documentation overhead and makes later reviews materially faster and more defensible.

9 Common Failure Modes That Keep Decline Rates High#

If approval results are still unstable after rollout, check these breakpoints first before escalating to issuer or acquirer root-cause analysis.

- Wrong PSD2 scope from the start

Scope errors can make a healthy flow look broken. PSD2 does not apply if your acquirer is outside the EEA. If your acquirer is in the EEA, PSD2 applies when the payer's card was issued in the EEA. Validate this first, because one geography mistake can invalidate the rest of your SCA logic.

- Later MIT declines caused by weak setup-stage authentication

Renewal declines often start at setup. For MIT arrangements, SCA may be required when the arrangement is created, while later merchant-initiated charges may proceed without reapplying SCA. If soft declines cluster on later charges, trace back to setup and confirm authentication actually completed. This is a tradeoff. EMV 3-D Secure adds an extra checkout step and can increase abandonment, but skipping authentication on the wrong setup path often shifts the problem into renewals where recovery is harder.

- Exemptions treated as if they were approvals

Exemptions are requests, not guarantees. The issuer may accept or reject an acquirer-requested exemption, so verify where you requested it, during authentication or payment submission, and what issuer decision followed. If a segment repeatedly fails under one exemption path, stop replaying the same request and route that segment to stronger authentication handling.

- Retries that repeat the same failed context

Generic retries usually do not recover SCA-related soft declines when the context is unchanged. After rollout, transactions presented without SCA are likely to see more soft declines, so check the prior response and whether updated authentication handling is possible before retrying. If it is not, escalate by issuer, acquirer, and flow type instead of treating it as routine retry noise.

10 30 Day Execution Plan for Compliance and Payments Teams#

Use this 30-day plan as an internal control cadence, not as a regulator-mandated timeline. The goal is to bring high-risk flows under control, prove traceability, and stop uncontrolled rule changes.

| Week | Primary work | Checkpoint |

|---|---|---|

| Week 1 | Inventory every live payment path and assign one owner per path | Pull a small production sample for each path and confirm you can reconstruct the request payload, authentication step if present, processor response, retry action, and final state |

| Week 2 | Ship only the minimum control set and define rollback conditions before launch | Every rule should have a written rollback trigger before production |

| Week 3 | Freeze a baseline and rehearse escalation before you need it | If the team cannot assemble transaction IDs, response text, retry history, and affected volume within one business day, monitoring is not ready |

| Week 4 | Sign off the evidence pack and limit scope to flows you can defend | Sign off only flows where the team can explain why the chosen authentication or retry handling was appropriate |

- Week 1, inventory every live payment path and assign one owner per path.

Start with the flows that move money: signup, free trial conversion, scheduled renewal, invoice charge, payment method update, and any manual collection path. Keep labels simple and explicit, and make sure each path has one accountable owner.

Your checkpoint is traceability, which the ECB names as a control area. Pull a small production sample for each path and confirm you can reconstruct the request payload, authentication step if present, processor response, retry action, and final state. If a material flow cannot be reconstructed from logs the same day, pause rule changes.

- Week 2, ship only the minimum control set and define rollback conditions before launch.

Keep the first release narrow: setup-stage authentication handling, renewal-change rules, soft-decline handling tied to authentication, and suppression of blind retries when the context has not changed. Every rule should have a written rollback trigger before production.

Anchor signoff to named ECB control domains: governance, risk assessment, incident monitoring and reporting, risk control and mitigation measures, and traceability. If you run any attended or device-assisted path, verify session handling: start session at transaction start, finish session at transaction end, and keep a session open for payment and line-item transactions. Treat "No session" in RESPONSE_TEXT as a hard failure signal. If primary port 5015 is busy, use secondary port 5016 for status, cancel, or reboot actions. Stale sockets can make the POS appear connected when it is not.

- Week 3, freeze a baseline and rehearse escalation before you need it.

Set one clean weekly baseline before judging approval movement. Segment by flow type, issuer or acquirer corridor, and whether authentication was attempted.

Run one escalation drill using a real case. Define who contacts PSP support first, who decides on legal or compliance review, and what evidence must be attached. If your team cannot assemble transaction IDs, response text, retry history, and affected volume within one business day, monitoring is not ready.

- Week 4, sign off the evidence pack and limit scope to flows you can defend.

Your evidence pack should include approved rule logic, exception decisions, sample traces, incident notes, weekly metrics, and rollback decisions. Sign off only flows where the team can explain why the chosen authentication or retry handling was appropriate.

Keep documentation review-ready: records should support harmonized and efficient assessment rather than relying on memory. Record the exact implementation guidance version used at signoff, including integration docs current at that time, for example a page updated on 19-Jan-2026 if it informed your controls. If documentation cannot explain why a flow behaved a certain way, keep rollout scope narrow and review weekly.

The Main Takeaway for Risk and Finance Owners#

Treat subscription payments under SCA as a control sequence, not a one-time rules project. The highest-value move is to enforce a consistent order: label flows, verify first-charge authentication evidence, then escalate using outcome data.

- Classify payment paths first

Separate your live paths into consistent operating buckets, for example CIT, MIT, and off-session, before adding more rules. Even if legal treatment differs by provider or route, consistent labeling lets risk and finance review outcomes by flow instead of by anecdote. Your baseline check is practical: for each path, confirm you can reconstruct the event type, whether authentication was attempted, and the provider or issuer response.

- Make first-charge authentication evidence clear

One source frames SCA under PSD2 as additional customer validation, typically using at least 2 of 3 factors. For card payments, a common implementation method is 3DS (versions 1 and 2). The key question is not whether 3DS exists somewhere, but whether you can show which flow triggered authentication and what result it produced. Also avoid blanket friction: one industry source warns that applying SCA broadly above EUR30 can increase abandonment.

- Monitor outcomes weekly and escalate with evidence

Teams usually resolve avoidable decline issues faster when SCA is treated as a living control system. Track outcomes by flow label, geography, response text, retry history, and whether each case is reconstructible end to end. Keep escalation packs simple and complete: flow classification, authentication outcome, exemption attempt if any, provider response artifacts, and internal retry or exception decisions. This matters because implementation expectations have shifted over time, so static assumptions age quickly.

If you run cross-border subscriptions, start with these three controls, prove impact, and only then add narrower optimizations where unresolved risk remains.

Frequently Asked Questions

When does SCA apply to subscription payments in practice across EEA issuer and acquirer combinations?

This article does not support a reliable SCA rule matrix by issuer and acquirer combination. Treat each live payment path as flow specific until your PSP or acquirer gives written confirmation. If that confirmation is missing, record it as an open control gap instead of inferring the rule from geography alone.

Do recurring subscription renewals always require authentication?

No supported source here proves a universal always or never rule for renewals. Segment renewals by the actual payment path and document what provider responses show in production. Avoid a blanket internal policy statement unless you can evidence it.

What is the operational difference between first subscription payment and off-session renewal?

This article treats the first payment and the off-session renewal as separate control points. It does not provide SCA-specific legal or processor rules that settle the distinction on their own. Document them as separate events with separate logs and review trails so first-charge assumptions are not reused for renewal flows without proof.

Can transaction exemptions be trusted as a stable strategy for recurring payments?

The sources here do not support saying exemptions are consistently stable or unstable for recurring collections. Treat exemptions as implementation dependent behavior that you monitor in your own data. Ask PSP support for written scope, limits, and exception conditions tied to your flow types.

How do plan changes, variable recurring payments, and invoice charges change SCA handling?

This article does not provide detailed SCA handling rules for plan changes, variable recurring payments, and invoice charges. Keep each flow type separately labeled in your records instead of grouping all of them under renewal. If tax treatment questions also arise, route them separately from payment authentication questions.

Which metrics should we monitor each week to reduce SCA-related declines without increasing risk?

Do not invent target rates because the article does not provide validated SCA benchmark thresholds. Monitor challenge rate, authentication-linked soft declines, exemption request and acceptance, off-session recovery, retry outcomes by acquiring bank, and whether each case is reconstructible from logs. Keep OSS reporting separate from payment-authentication reporting.

What must be confirmed with PSP support or legal counsel because provider and bank behavior varies?

With PSP support, confirm only what is evidenced for your implementation, including supported flows, response handling, and written constraints. With legal or tax counsel, separate SCA handling from VAT registration and reporting decisions. For complex cross-border VAT treatment, CBR exists for advance rulings, and where multiple companies are involved, one company should submit on behalf of the others. OSS is optional, uses one Member State of identification, and exclusion by a Member State is possible.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- acquisition.gov/far/subpart-22.10trusted

- apps.dot.illinois.gov/eplan/desenv/061424/191-76K05/76K05-191.pdftrusted

- department.va.gov/procurement-acquisition-and-logistics/nation...trusted

- dol.gov/agencies/whd/government-contracts/service-co...trusted

- dol.gov/agencies/whd/government-contracts/prevailing...trusted

- eba.europa.eu/sites/default/files/documents/10180/1761863/...trusted

- federalregister.gov/documents/2024/11/15/2024-25534/negative-opt...trusted

- ftc.gov/system/files/ftc_gov/pdf/p064202_negative_op...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: