Quick Answer

For payments teams, SCA means Strong Customer Authentication in the European Union context, and it should be treated as a launch dependency for money-moving flows. Start by mapping where authentication can interrupt checkout or collection, then verify fallback behavior through API states, webhooks, and final ledger records before scaling to new EU markets.

SCA is a launch constraint for EU payment flows#

Strong Customer Authentication (SCA) matters in the European Union payments context because a failed auth step can interrupt money movement. The goal here is practical: decide where it applies in your stack and what to verify before you expand into EU markets.

This is written for teams that own Platform Payments & Infrastructure, not for casual card users. That usually means founders, product leads, engineers, and finance or ops owners responsible for collection, conversion, settlement, and Payouts across contractor, creator, marketplace, or embedded payments flows. In that setting, payment compliance work is not just a legal issue. It can change checkout and operations, and it can affect how quickly you can enter a new market.

A useful starting point is to treat EU payments work the way you already treat other EU cross-border obligations: as a mix of shared regional rules and local implementation detail. The official European Commission sites referenced in the broader research sit on the europa.eu domain, and they show that marketplace and platform obligations can reach actors both inside and outside the EU.

For example, EU VAT guidance notes that, from 1 July 2021, cross-border B2C e-commerce rules changed, and schemes like One Stop Shop let eligible businesses register in one Member State for VAT declaration and payment duties. Those sources are not SCA rules. They are a useful reminder that "EU-wide" does not always mean identical in every country.

That caveat matters from the start. For example, cross-border VAT rulings must be requested under the national VAT ruling conditions of the relevant EU country. Confirm exact applicability before go-live rather than assuming one pattern will hold everywhere.

Keep the scope tight. Focus on payment operations and product decisions around collection and payout-adjacent flows, not every other EU control. Adjacent topics like VAT still matter for launch readiness, but they do different jobs. If your team is about to expand into the EU, build an explicit applicability note by market before engineering starts.

Define Strong Customer Authentication in platform terms#

For this article, treat Strong Customer Authentication as a launch dependency for EU payment flows: if authentication does not complete, the money-moving action may not complete either. The operational question is not just compliance; it is whether your product handles success, failure, and recovery clearly enough to protect conversion and support outcomes.

| Area | What to document |

|---|---|

| Merchant of Record | Who owns commercial and payment-program setup decisions |

| API integration | Who owns initiation, status handling, retries, and customer messaging in your product |

| Provider controls | Which authentication behavior is actually supported in each target market |

Set the boundary early in one ownership note:

- Merchant of Record: who owns commercial and payment-program setup decisions.

- API integration: who owns initiation, status handling, retries, and customer messaging in your product.

- Provider controls: which authentication behavior is actually supported in each target market.

Keep a regional-vs-local mindset. EU Commission VAT programs show this pattern clearly: OSS expanded on 1 July 2021, while country-level conditions still matter in related processes. Use the same discipline here by documenting your target market, expected provider behavior, and what evidence you retain for success, failure, and abandonment.

Map where SCA appears across your money movement stack#

If your team cannot identify SCA touchpoints for each money-moving flow, pause launch and complete the flow inventory first.

Map each flow end to end: invoice or checkout, transaction intake, routing/authorization, settlement, and final ledger posting. In a payment orchestration model, the orchestration layer sits between checkout and downstream steps, so treat that middle layer as a core control point. At intake, you may generate an internal transaction ID and log the request in the ledger; use that as your first durable audit artifact.

Separate user-visible flows from background flows. Cover checkout, retries, saved payment methods, subscription renewals, and payout-adjacent actions on the same map so fallback ownership is explicit.

| Flow | Who initiates | SCA likelihood | Fallback path | User impact | Audit artifact |

|---|---|---|---|---|---|

| Checkout / invoice payment | Customer | Possible step | Return to completion path and retry with clear state | Can block completion | Internal transaction ID, provider reference, status events, ledger log |

| Retry flow | Customer or system | Possible touchpoint | Controlled retry or clean restart | Confusion/abandonment risk if unclear | Retry linkage, idempotency key, status history, ledger updates |

| Saved payment method charge | Customer or system | Possible touchpoint | Re-route customer to complete payment | Interrupted purchase or delayed collection | Token/payment method reference, provider events, final ledger posting |

| Subscription renewal | Background scheduler | Possible touchpoint | Recovery message + completion path | Silent failure risk if unmanaged | Renewal job ID, provider response, customer notice, journal entry |

| Virtual Accounts inbound payment | External payer | Different pattern from card collection | Reconciliation hold/manual review | Delay in crediting funds | Virtual Account identifier, payer reference, bank match, ledger posting |

| Payouts / international wire release | Platform or ops process | Different pattern from collection flows | Hold, correct beneficiary details, re-approve | Recipient delay and support load | Approval log, beneficiary details, SWIFT code, account number or IBAN |

For international wires, keep initiation and settlement as separate states in your map: operational records use SWIFT plus account number or IBAN, and transfer timing can be 1-5 business days. Keep one owner per fallback path and one traceable audit trail from initiation to ledger.

Handle exemptions and step-up paths without guessing#

Start conservative: in a new market, treat exemption attempts as optional until your own data shows reliable recovery. They can help conversion, but they can also create more incomplete-payment handling and support work.

Set your fallback order before launch:

- Run your initial authorization path.

- If the provider requires more authentication, move the payment into step-up immediately.

- Retry only after the provider returns a clear terminal or recoverable state.

Your API should expose those states clearly to product logic, and your webhooks should be your source of truth for asynchronous status changes.

A useful readiness check is continuity across one payment journey: exemption requested, step-up required, and final success or failure. If your internal transaction ID, provider reference, or ledger linkage breaks at any point, your team cannot reliably tell a customer whether to retry, wait, or stop.

| Exemption strategy | Expected conversion effect | Failure mode | Ops burden | When to prefer |

|---|---|---|---|---|

| No exemption attempt | Lower upside, more predictable authentication path | More users authenticate up front | Low | New market launch, limited payments-ops coverage |

| Selective exemption attempt | Moderate upside when recovery is reliable | Soft declines that need fast step-up recovery | Medium | You can track decline reasons and recovery by provider and route |

| Aggressive exemption attempt | Higher upside when issuer acceptance is strong | More soft declines and edge-case support handling | High | Mature market, strong observability, proven recovery path |

Do not treat the European Union as one operational rulebook. Even in adjacent compliance programs, mechanics differ: VAT e-commerce rules changed from 1 July 2021, One Stop Shop allows registration in one single Member State, and VAT Cross-border Rulings cover complex cases involving two or more participating Member States. Those are not SCA rules; they are a practical reminder to validate country and program behavior directly instead of generalizing from one launch.

For execution, keep an evidence pack: sample soft-decline responses, a support-readable decline taxonomy, webhook timelines, and customer message templates per recovery path. If a step-up is required, your customer message should state what happens next and whether the original attempt is still active.

For a step-by-step walkthrough, see What is Two-Factor Authentication (2FA) and Why You Need It.

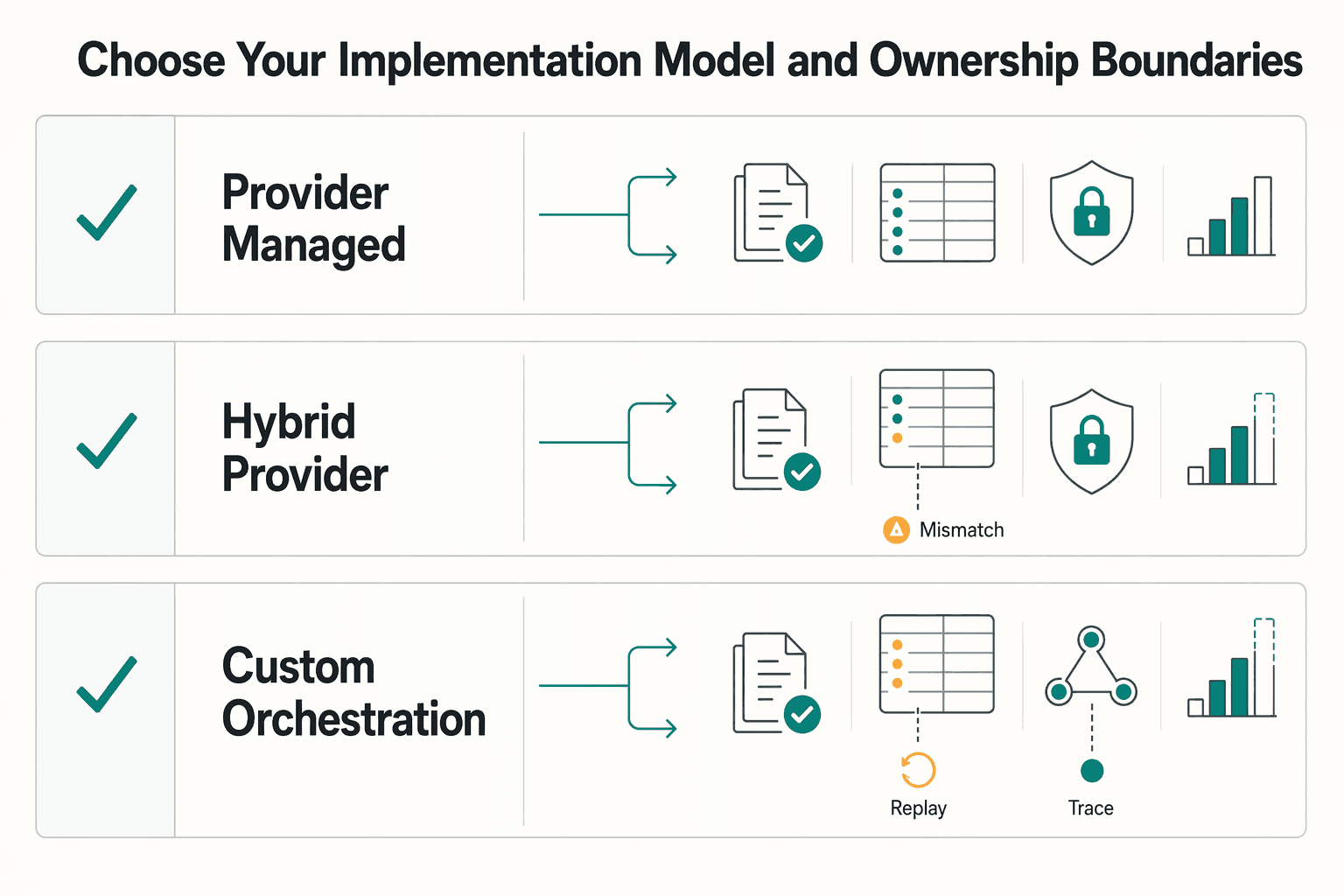

Choose your implementation model and ownership boundaries#

Choose the model you can operate reliably first, then add control only when measured gaps justify it. If payments engineering capacity is limited, provider-managed Strong Customer Authentication is usually the safer starting point, and custom orchestration should follow only when you can show a clear conversion, observability, or reporting gap.

Provider-managed flows reduce what your team has to own in the first launch. Custom orchestration increases control through your API, but it also increases failure recovery surface because your team must keep idempotency, webhooks, and ledger outcomes aligned under retries and late events.

| Model | Time to launch | Control | Conversion risk | Ops overhead | Best-fit platform stage |

|---|---|---|---|---|---|

| Provider-managed default | Faster | Lower | Lower implementation risk, less tuning room | Lower | Early launch, limited payments engineering capacity |

| Hybrid (provider challenge + your app state handling) | Medium | Medium | Medium if state mapping is inconsistent | Medium | Growing platform needing better support and reporting clarity |

| Custom orchestration | Slower | Higher | Higher if retries/timeouts/step-up recovery are immature | Higher | Later stage platform with proven volume and measured gaps |

Set ownership boundaries in writing before go-live. A practical operating split is: product owns UX decisions, engineering owns API contracts and idempotency behavior, and finance/ops own reconciliation from ledger outputs.

Treat Merchant of Record as a boundary-definition exercise, not an assumption. Document who handles dispute intake, who can retrieve authentication evidence, who exports reporting data, and which identifier is authoritative for reconciliation across systems.

One caution is non-negotiable: "SCA" is overloaded across domains. In public material, it can refer to security scan stages, Service Component Architecture, or Secure Cloud Architecture; for example, one F5 "SCA" repository is archived and read-only (Jul 26, 2023) with a latest visible commit of Jun 25, 2020. Confirm terminology and freshness before using any "SCA" source to guide payment-authentication ownership decisions.

Implement in production with API, webhooks, and ledger checkpoints#

In production, treat traceability and source freshness as release gates before you optimize anything else. If your flow uses API calls, async webhooks, and ledger posting, keep your operating language tied to what you can verify in logs and records, and label unverified behavior as an assumption.

Build order that reduces avoidable breakage#

Start by defining what is observable, then tighten execution details. Keep status names and handoffs explicit across product, support, and finance so teams are not relying on ambiguous dashboard labels. If you cannot prove an outcome path with consistent internal records, do not treat it as production-ready.

Release checks that are worth doing before traffic#

Date and label external security inputs you rely on during release review. For example, CISA bulletin SB26-020 is a vulnerability summary for the week of January 12, 2026, released Jan 20, 2026, and it states that vulnerabilities may not yet have CVSS scores. The same page also notes the site would not be actively managed during a funding lapse, so freshness and maintenance status should be part of your go-live check.

Also verify source accessibility before relying on it in runbooks. A referenced Medium piece is marked member-only, so treat it as non-universal operational input unless your team confirms access and review coverage.

Keep data handling boring and reviewable#

Keep operational data collection minimal and reviewable: retain what your team needs to explain state changes and reconciliation, and avoid spreading sensitive details into tickets or chat for convenience. Use role-appropriate views and clear audit trails so investigations do not depend on ad hoc data exposure.

Related reading: What Is a Legal Hold and When Should You Issue One?.

Build the compliance and evidence pack before EU rollout#

Before adding EU traffic, lock an evidence pack that lets legal, product, and ops independently verify how each authentication outcome was decided, recorded, and reconciled to the ledger. Keep it compact but reviewable:

| Artifact | Include |

|---|---|

| Policy decisions | Named owners and dates; authentication handling, exemption or step-up paths, retry rules, customer messaging, and when a payment can post to the ledger |

| Auth-flow diagrams | Who initiates payment, where customer action may be required, expected async events, and which internal status is final |

| Decline taxonomy | Customer-action-required, retryable failures, and non-retryable failures, each mapped to the next permitted action |

| Reconciliation outputs tied to ledger records | Sampled transactions showing internal payment ID, provider reference, auth result, and journal entry matched without manual interpretation |

A practical check: give this pack to someone outside engineering and ask them to explain the payment history from auth attempt to final ledger posting. If they still need screenshots, chat context, or a developer to decode statuses, the chain is not ready.

Keep adjacent controls in separate lanes#

KYC, KYB, AML, and VAT are related risk and compliance gates, but they are not substitutes for SCA readiness. Treat them as parallel workstreams, not proof that payment-auth design is launch-ready.

For VAT, keep scope precise. Official EU institutional sites are on the europa.eu domain. OSS covers registration, VAT declaration and payment, record-keeping, and audits. VAT Cross-border Rulings (CBR) let taxable persons seek advance VAT treatment rulings for envisaged complex cross-border transactions between participating EU countries. Important controls, but separate from SCA flow quality and decline handling.

Make go-live approval explicit#

Require named sign-off with explicit criteria:

| Role | Approval criteria |

|---|---|

| Legal/compliance | The documented approach matches target jurisdictions and programs, and VAT workstreams are tracked separately where needed |

| Product | Customer journeys and messaging cover auth-required, retryable, and terminal outcomes |

| Ops/finance | Reconciliation outputs tie cleanly to ledger records, and support can explain common decline paths without exposing sensitive data |

Set rollback triggers before launch. If ledger mismatches remain unresolved, auth-required states rise without recovery, or support cannot classify declines using the approved taxonomy, pause the route and revert to the narrower working path.

Prevent the failure patterns that damage conversion and trust#

The costliest mistake is treating Strong Customer Authentication as "done" once 3DS2 is live. In practice, trust and conversion hold only when you can see how authentication outcomes recover by route and explain the next safe action clearly.

3DS2 is a tradeoff, not a one-time switch: extra friction can increase abandonment, while weaker checks increase fraud exposure, and regional rules can shape requirements differently across markets. So one healthy checkout path is not enough evidence for all EU payment flows.

Watch for these red flags:

- SCA marked complete without route-level monitoring. Review outcomes separately by route so you can see where customers are challenged, where they recover, and where they drop.

- Retries that create conflicting states. If the same payment can end up with mismatched provider events, webhooks, or ledger outcomes, treat that as a blocker before scale.

- Support scripts that cannot guide the next step. Agents should be able to explain what failed, whether customer action is needed, and whether retry is safe without improvising.

Also keep language explicit in internal docs: spell out Strong Customer Authentication where possible. "SCA" is acronym-ambiguous across teams, and that ambiguity can cause avoidable handoff mistakes.

Conclusion#

If you remember one thing, let it be this: success here is not "we passed review." It is "we shipped an authentication design that behaves cleanly under real traffic, recovers safely, and leaves an audit trail your ops team can trust."

Part of the challenge is that the acronym itself is messy. When someone asks "what is SCA" in a payments launch, they usually do not mean Software Composition Analysis or Sustainable Competitive Advantage. Here, SCA means Strong Customer Authentication in the European payments context, described by one source as a requirement aimed at securing electronic payments within the EEA and tied to PSD2. If your team does not lock that definition early, scope drift starts fast and the wrong owners get pulled into the work.

The practical sequence is straightforward, and it is worth treating as a gate rather than a suggestion. First, disambiguate scope. Second, map the trigger points in each payment route. Third, decide whether provider-managed handling is enough or whether you truly need custom orchestration. Fourth, verify that your event handling and reconciliation hold up when requests are retried, delayed, or delivered out of order. Only then should you launch with monitoring that tells you where customers recover and where they stall.

The operator detail that matters most is boring in the right way. Before go-live, confirm that one provider reference can be traced to one internal payment record and one final ledger outcome. Replay webhook delivery, force retry paths through your API, and check that a payment cannot land in two internal "success" states. If that checkpoint fails, pause the rollout. A technically working authentication step is not enough if your books, support view, and customer-visible state can diverge.

The common bad tradeoff is chasing conversion while weakening control over retries and final state. A softer version of the same mistake is assuming compliance sign-off means the launch is production-ready. It does not. You still need clear customer messaging for recoverable failures, masked operational views instead of unnecessary sensitive data, and a decline taxonomy that support can actually use.

For teams expanding cross-border, keep the operating principle simple. Make compliance-first decisions, insist on traceable ledger outcomes, and route retries through your API and webhooks in a way that is observable and safe. If you do that, Strong Customer Authentication stays what it should be: a managed product and operations constraint, not a recurring source of avoidable declines, duplicate postings, and late-night incident reviews.

Frequently Asked Questions

What is SCA in payments, in one practical sentence for platform teams?

Use your payment provider and counsel to confirm the exact definition and implementation scope before launch.

When is SCA typically required, and when can it vary by country or program?

Treat applicability as payment-flow and jurisdiction-specific, then confirm it with your provider and counsel before launch. Do not use adjacent EU VAT programs as a shortcut here: OSS, the cross-border SME scheme, and thresholds like EUR 10 000 or EUR 100 000 relate to VAT treatment, not authentication scope. Country and scheme behavior can differ, so one working setup in one EU market is not proof for the next.

Who should own SCA implementation decisions across product, engineering, and finance/ops?

Set a shared process across product, engineering, and finance/ops, and document clear sign-off per market or program.

How does SCA affect checkout conversion, and which metric should teams watch first?

Use a primary launch metric and review it by route and market so country/program differences are visible.

Can we rely on provider-managed authentication, or should we build custom orchestration?

Choose the approach your team can operate reliably, and expand only when measured gaps are clear.

What should we verify before launching in a new EU market to avoid avoidable declines?

Verify country- and scheme-specific requirements instead of assuming one EU setup applies everywhere. For country or program uncertainty, use official EU pages on the europa.eu domain for adjacent rules. If tax treatment is part of the launch question, separate that workstream clearly: VAT Cross-border Rulings, OSS registration, and the cross-border SME scheme solve VAT questions, not SCA scope.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

- cisa.gov/news-events/bulletins/sb26-020trusted

- pa.gov/content/dam/copapwp-pagov/en/dhs/documents/h...trusted

- sme-vat-rules.ec.europa.eu/sme-scheme/cross-border-sme-scheme_entrusted

- taxation-customs.ec.europa.eu/archives/taxable-persons/vat-cross-border-ru...trusted

- vat-one-stop-shop.ec.europa.eu/index_entrusted

- vat-one-stop-shop.ec.europa.eu/one-stop-shop_entrusted

- 2accept.net/blog/challenge-vs-frictionless-3ds2external

- cloudaware.com/blog/aws-devsecopsexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

Microservices Architecture for SaaS Without Finance and Compliance Surprises

Choose your operating model before you choose your decomposition pattern. For most early products, that means a modular monolith with clear domain boundaries, not a full microservices setup on day one. The reason is practical. Every new service adds cognitive load, failure points, and maintenance cost, so the split pays off only when your team and controls are ready.

Permanent Home Test in a Tax Treaty: Meaning, Evidence, and Tie-Breaker Rules

For the elite global professional, "permanent home" is not a term of comfort; it is a high-stakes legal definition that can trigger crippling double taxation. While other guides offer academic theory, this is a strategic playbook. We will transform your compliance anxiety into agency with a clear, three-step framework to audit your footprint, build your evidence, and early control your tax residency.

What is the 'Center of Vital Interests' in a Tax Treaty?

Start by making one defensible tax residency call based on facts, not on a preferred country outcome. Use the treaty tie-breaker in order, document why each step does or does not resolve residence, and stop at the first clear result.