Quick Answer

Use two-factor authentication by requiring a password plus a different proof, then enable it first on primary email, banking, payout, and domain accounts. Start with an authenticator app or physical security key when available, keep SMS as backup where stronger options are missing, and run a real sign-in check before calling setup done. Save backup codes and recovery steps so device loss does not block urgent access.

How 2FA adds a second layer of protection#

Two-Factor Authentication (2FA) is a practical way to reduce avoidable account risk. It adds a second identity check, so a stolen password is less likely to lead to unauthorized access to billing, payouts, or client delivery.

If you have asked what is two factor authentication, the practical answer is simple: sign-in requires two distinct forms of verification. That matters because passwords are vulnerable to attack, and many business accounts store personal and financial information. Keep the terms straight from the start. 2FA is a subset of MFA, and MFA can use two or more factors.

For independent professionals, a practical starting point is three account groups:

- Personal identity anchors, especially primary email.

- Business-critical tools used to deliver client work.

- Financial surfaces, including banking, invoicing, payout platforms, and domain access.

By the end of this article, success should be concrete:

- A strong primary method is active on each high-impact account.

- A backup access path is configured and tested.

- A recovery checklist is documented so you know what to do first after lockout.

Treat this as a baseline, not total protection. 2FA can reduce the impact of phishing, credential theft, and brute-force attempts, and it can still block unauthorized access when a password is compromised. Setup quality and regular checks are what keep that protection real.

A practical way to use this guide is to read once, then execute section by section with your account list open. The value is not in knowing terms. The value is finishing setup on real accounts, testing recovery before you need it, and scheduling review before the details fade.

Build the Mental Model Before You Touch Settings#

Start with factor separation, not button clicking. A second prompt only helps when it comes from a different factor category.

| Factor type | Examples |

|---|---|

| Something you know | password, PIN, or passphrase |

| Something you have | smartphone authenticator app, physical security key, or hardware token |

| Something you are | biometrics such as fingerprint or facial recognition |

Two-Factor Authentication means exactly two distinct factors. Multi-Factor Authentication is broader and can require two or more, so 2FA is one type of MFA. When a platform shows multiple prompts, ask one question first: are these prompts from different categories?

Use these categories when you review settings:

- Something you know: password, PIN, or passphrase.

- Something you have: smartphone authenticator app, physical security key, or hardware token.

- Something you are: biometrics such as fingerprint or facial recognition.

Do not trust labels alone. Two-step verification can describe strong two-factor sign-in, but the label does not guarantee separation. Confirm that the second factor is truly different from the first.

This distinction protects continuity. A separate second factor can still block unauthorized access when a password is exposed. Keep a simple access record with each account factor pair, backup method, and last sign-in test date.

Use one checkpoint before moving on: sign out, sign back in, and confirm both factors are required. If a provider limits available methods by account type, note that in your record so future reviews are faster.

When settings are unclear, run a quick separation test before you trust the setup:

- Identify the first factor and where it lives.

- Identify the second factor and where it lives.

- Confirm that losing one does not automatically give you the other.

This prevents a common setup mistake: assuming two steps always means two factors. In practice, lockout recovery can take longer when nobody documented which factor pair was actually active. Write down what was enabled, what fallback exists, and who owns the account. That simple record can turn a confusing outage into a shorter recovery task. For related credential hygiene, see The Best Password Managers for Freelancers and Teams.

What 2FA Protects You From and What It Does Not#

2FA lowers unauthorized-access risk, but it does not remove risk. Use it as a strong control, then back it with disciplined account habits.

Password-only sign-in is exposed to common attacks. Adding a second verification step can block unauthorized access even when a password is stolen or compromised. In day-to-day terms, that lowers the impact of phishing, credential theft, and brute-force attempts.

2FA is important, but it is only part of the solution. To keep it effective, pair the control with user education and awareness.

Carry one rule into operations: after major account changes, confirm both factors still work. Keep your access and recovery steps documented so weak points are easier to spot before an incident.

Use a simple if-then rule to avoid confusion during incidents:

- If the prompt is unexpected, deny it and verify account activity before trying again.

- If sign-in fails on a critical account, follow the documented recovery steps before changing more settings.

- If recovery also fails, move to the provider recovery path and log what blocked access.

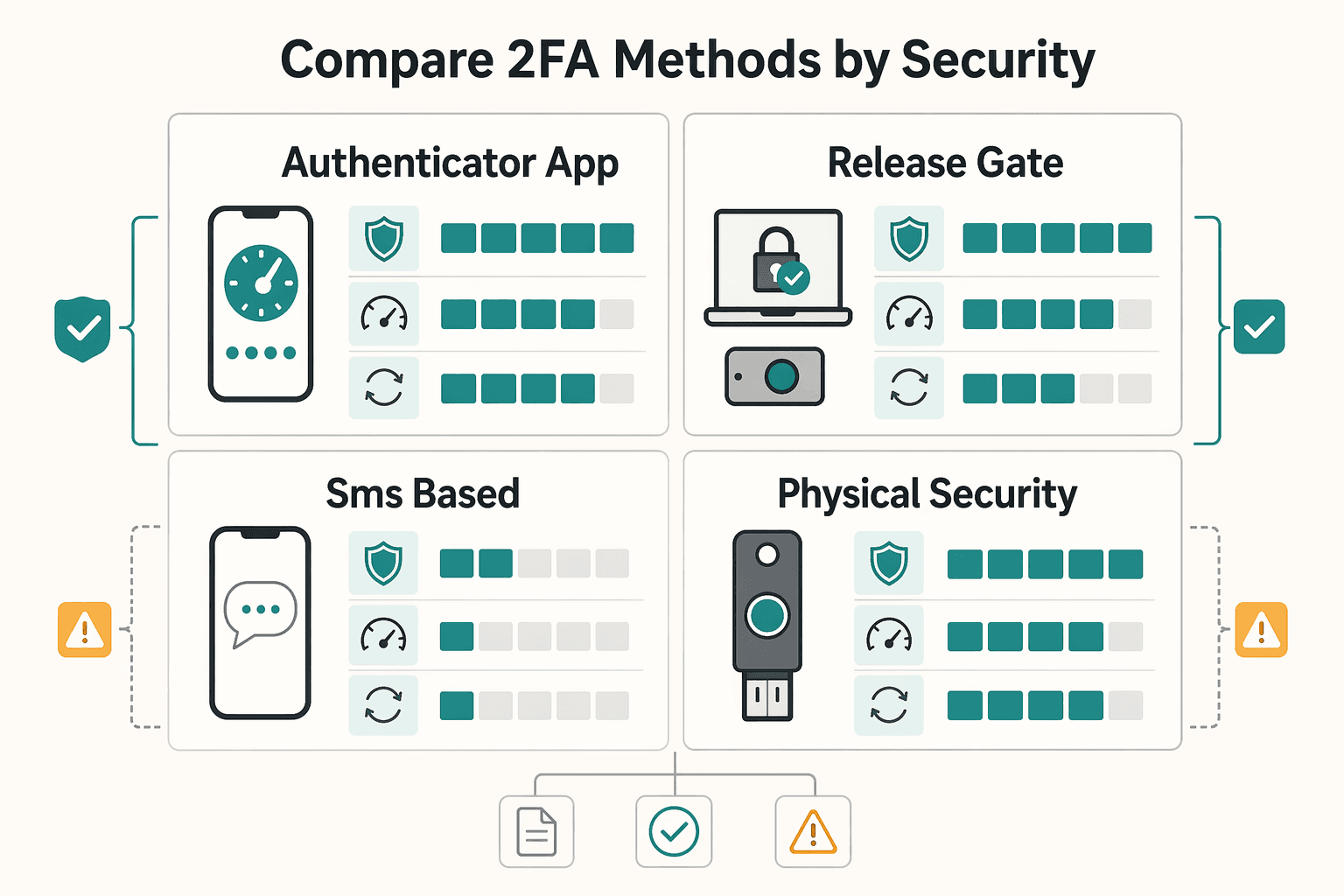

Compare 2FA Methods by Security, Friction, and Recovery Risk#

For business-critical accounts, choose an authenticator app or physical security key when available. Keep SMS as fallback coverage when stronger options are missing.

The method choice drives most of the real-world protection because the strength of 2FA depends on the quality of the second factor. These options can all be used as second factors, but they differ under phishing pressure, device loss, and recovery stress.

| Method | Security tradeoff | Daily friction | Recovery consideration | Practical note |

|---|---|---|---|---|

| Authenticator app | Strong baseline and not exposed to SIM-swapping risk in the same way as SMS | Can be moderate | Plan for device loss before lockout | Common across business tools; Microsoft Authenticator is one example |

| Push notification approval | Common 2FA method; outcomes depend on careful approval behavior | Can be low to moderate | Test fallback access before you need it | Approve only sign-ins you initiated |

| SMS-based authentication | Better than no second factor, but more exposed to SIM swapping and social engineering | Can be low | Tied to phone-number control and delivery channel | Useful as temporary coverage where app or key options are missing |

| Physical security key or hardware security token | One of the strongest common options against phishing | Setup can be moderate, then lower day to day | Keep backup access ready | Best fit for high-impact accounts |

Before standardizing on one method for important accounts:

- Test a fresh sign-in to confirm the second factor is enforced.

- Test the recovery path on purpose, such as a backup method or a second enrolled device.

- Record method, fallback path, and last test date in your access record.

If SMS is your only option today, enable it now. Then move that account to an app or key as soon as support appears.

Use this tradeoff lens when comparing methods on a real account:

- Security strength under phishing pressure.

- Friction for everyday sign-in.

- Recovery speed when a phone is lost.

- Dependence on one provider channel, such as SMS delivery.

That lens keeps decisions practical. A method that looks strong but has no tested recovery path can fail at the worst moment. A method with low friction but poor prompt discipline can also fail. The best choice is the strongest option your provider supports that your team can run consistently with verified fallback.

If your account estate is mixed, do not wait for perfect consistency. Secure high-impact accounts first with stronger factors, then phase the rest toward the same baseline as options appear.

Which 2FA Method Should You Choose First#

Choose by account impact first, then by available method. For high-impact accounts, start with a physical security key or push notification approval and add a tested fallback path on day one.

Your first method does not have to be final. Treat the first setup as the best available choice now, with a clear review path.

| Account criticality | Preferred first method | Strength against password compromise | Recovery difficulty | Practical decision |

|---|---|---|---|---|

| High: admin email, banking, domain registrar | Physical security key or push notification approval | Stronger than password-only access | Varies by backup setup | Enroll primary and backup access early |

| Medium: invoicing, cloud docs, client tools | Push notification approval or biometrics | Strong improvement over password-only access | Varies by backup setup | Use an available method first, then refine setup |

| Lower: low-impact accounts | Push notification approval or SMS-based authentication | Better than password-only access | Varies | Enable now, then review other options later |

If you use push approvals, enforce prompt discipline:

- Approve only sign-ins you initiated.

- Reject unexpected prompts.

- If prompts repeat unexpectedly, pause approvals and secure the account before continuing.

If a platform offers only SMS, turn it on now rather than waiting. Add a dated reminder to review other available 2FA methods later, then verify recovery still works with a fresh sign-out and sign-in test.

A practical sequence for first-time rollout looks like this:

- Rank accounts by impact if compromised.

- Apply an available 2FA method to the top tier first.

- Configure fallback before closing each account.

- Run a live sign-in test while details are still fresh.

- Record ownership and next review date.

This approach helps avoid spending time perfecting low-impact accounts while high-impact ones stay weak. In access control, order matters as much as method.

The First 30 Minutes Setup Checklist for Solo Operators#

Use this first session to finish accounts end to end. Partial setup can create false confidence and leave weak gaps in critical logins.

Pick a starting order based on which accounts are most critical to your work.

For each account, setup is complete only when these checkpoints are done:

2FA enabled: confirm the setting is actually on.Method active: verify at least one second factor is enabled so 2FA can run.Backup access configured: if backup codes are offered, store them in your chosen secure location.

Keep short notes as you go so recovery does not rely on memory:

- Account name

- Active method and fallback method

- Storage location for backup codes

Before moving to the next account, run a real sign-out and sign-in check. The common flow is simple: choose a verification channel, receive a code, enter it, and confirm access.

Method options can vary by implementation. Document what is available today, enable the strongest practical option, and set a dated reminder to upgrade when stronger options are added.

If you get stuck mid-setup, do not skip forward. Resolve the current account first or log a clear blocker with the next action. A half-configured critical account is riskier than an untouched low-impact account.

Use this simple completion test before you mark any account done:

- You can sign in with the primary factor path.

- You can still sign in with the fallback path.

- You know exactly where recovery data is stored.

That test keeps the session outcome measurable. At the end of 30 minutes, you should have fewer unknowns, not just more toggles switched on.

If you need to pause, end with an explicit handoff note to yourself: which account is next, what method is active, and what still needs testing. Related: The Best Gear for a Portable Home Office.

Build a Recovery Kit So 2FA Does Not Lock You Out#

Build recovery at the same time you enable 2FA. Two-factor authentication adds a second, independent check and uses two different types of proof to verify identity, which helps protect company accounts against account takeovers and data theft. It can also create a dependency, so plan how you will recover access if your primary method fails.

| Recovery evidence item | What to store | Why it matters during lockout |

|---|---|---|

| Recovery phrases or backup credentials | Current values and the date generated | Can provide a fallback when primary verification is unavailable |

| Device inventory | Primary and backup devices that can approve sign-in | Can reduce guesswork about which device still has access |

| Support escalation path | Provider help path, account identifiers, and contact route | Can save time when self-service recovery fails |

| Identity proof requirements | The ownership checks a provider may request | Can help reduce failed recovery attempts and delays |

One practical option is two storage locations: an encrypted digital vault for routine access and an offline copy for disaster scenarios. Use the storage pattern that fits your risk level and internal controls.

Define break-glass rules before an incident:

- State when backup factors are allowed, such as lost device, failed primary sign-in, or urgent access needs.

- If another person can assist, name who can approve emergency recovery actions and where that approval is logged.

- After any break-glass use, consider rotating exposed factors and refreshing backup credentials.

Set a recurring recovery drill cadence (for example, quarterly) on at least one non-primary device. Sign out fully, run the real recovery path, and record what worked, what failed, and what changed.

Recovery quality is easiest to judge with one question: could you regain access today without your primary phone? If the answer is uncertain, your recovery kit is incomplete.

Keep provider variation in mind. Recovery and device replacement steps can differ across platforms, and common business platforms may use methods such as authenticator apps or passkeys, so store account-specific notes instead of one generic process. The key is speed and clarity during stress: where to go, what to submit, and which fallback path to try first.

A practical drill script can be short:

- Pick one critical account.

- Simulate no access to your usual device.

- Use documented fallback to sign in.

- Confirm account access is restored.

- Update notes immediately if anything failed.

This turns recovery from theory into evidence. You do not need complex documentation. You need current details that work when you are under time pressure.

Stop Common 2FA Failure Modes in Daily Operations#

Daily behavior decides whether 2FA works when it matters. Treat each login prompt as a verification step, not routine noise.

For any second-factor approval, check context before you continue. If a request is unexpected or does not match the app or site you just opened, do not approve it.

Do not normalize unexpected prompts. If sign-in requests appear that you did not initiate, pause and verify account activity before continuing.

Use SMS intentionally. It is a common 2FA method, and 2FA is still better than password-only access because a stolen or guessed password is not enough on its own. Recheck available factor methods during regular reviews and keep recovery details current.

Add one daily checkpoint for high-impact accounts: if anything about a sign-in request feels off, pause and verify before proceeding.

Common failure pattern to avoid:

- A password is stolen or guessed.

- A second-factor request is approved without verification.

- An attacker gains access.

Common prevention pattern:

- Treat every second-factor prompt as a verification step.

- Do not approve requests you did not initiate.

- Keep factor and recovery settings current.

- Include phishing training in routine security practice.

These habits require discipline, not new tools. They are small actions that preserve the value of your 2FA setup.

Handle Travel, New Devices, and Number Changes Without Panic#

Lockouts can happen during transitions, not just routine days. Travel, phone replacement, and number changes can expose weak fallback paths.

| Transition | Primary action | Verification step |

|---|---|---|

| Before travel | Sign in to primary email with a non-SMS factor; confirm recovery access works without the primary SIM | Test one high-priority account while SMS is unavailable |

| New phone | Migrate authenticator app entries first | Validate high-priority accounts before wiping the old phone; keep both phones available until critical accounts pass a live sign-in test |

| Number change | Update the number immediately if any account still depends on SMS-based authentication | Run a live sign-in test; confirm the update is complete across your critical account list |

Continuity depends on one principle: keep at least one verified sign-in path that does not rely on your primary SIM. That principle can reduce stress during travel days and hardware changes.

Before travel, verify access without your primary SIM#

Travel can interrupt calls and texts, and a SIM-swap incident can do the same, which can block verification codes on short notice. Run a short pre-travel check while you still have time to fix gaps.

- Sign in to primary email with a non-SMS factor.

- Confirm recovery access works without the primary SIM.

- Test one high-priority account while SMS is unavailable.

- Record what passed and what needs follow-up.

If a test fails, fix that account before departure or document a fallback order you can execute under pressure. The goal is not perfection. The goal is no surprises when you are away from your normal setup.

Move to a new phone in two passes#

Migrate authenticator app entries first, then validate high-priority accounts before wiping the old phone. Start with accounts that unlock others, such as primary email and core financial logins.

If a phone is lost or stolen, switch to containment steps immediately. Revoke active sessions, rotate factors, remove the missing device from trusted lists, and re-issue physical security key access if used. Confirm the missing phone can no longer approve sign-ins.

During migration, keep both phones available until critical accounts pass a live sign-in test. Deleting old device data too early can trigger lockouts.

Treat number changes as access events#

If any account still depends on SMS-based authentication, update the number immediately and run a live sign-in test. This can reduce lockout risk during urgent access.

Keep provider caveats in mind: factor options and SMS support can vary by provider, region, plan, or service and can change over time. An eSIM is still a SIM, so resilience comes from tested backup factors and verified recovery access.

After a number change, run through your critical account list and confirm the update is complete. Partial updates create hidden risk because some accounts still point to the old number while others do not.

Apply 2FA to Finance-Critical Workflows and Shared Access#

Start where a single account compromise can move money. Priority goes to banking, payout approvals, invoicing controls, and the accounts that can reset those logins.

| Rollout step | Priority target | Action |

|---|---|---|

| 1 | Reset authority accounts, especially primary email and admin access | Secure these first |

| 2 | Direct money movement accounts | Secure these next |

| 3 | Invoicing and payout support tools | Secure these after that |

| 4 | Shared actions | Enforce individual sign-in and approval separation |

Use stronger factors first where available, such as authenticator apps, push approvals, or hardware keys. SMS-based OTP flows can still be useful fallback coverage, but basic OTP methods are more vulnerable to phishing and SIM-swap attacks, so they should not be the default for high-impact money paths when stronger choices exist.

For shared work, avoid credential sharing so each person signs in with individual access. Pair that with an extra approval step for payout or banking changes to reduce the chance that one compromised login triggers an irreversible action.

Keep an audit-ready change log for access and factor updates. Record what changed, who requested it, who approved it, and when it was reviewed. Before standardizing policy across tools, confirm your required factors are supported.

A practical rollout sequence for finance-critical access:

- Secure reset authority accounts first, especially primary email and admin access.

- Secure direct money movement accounts next.

- Secure invoicing and payout support tools after that.

- Enforce individual sign-in and approval separation on shared actions.

This sequence prioritizes high-value access first, then broadens coverage.

Also define escalation ownership before incidents happen. When a factor change request appears on a finance-critical account, someone should validate request legitimacy before approval. That pause step adds a risk-based check before approval.

Set a Quarterly 2FA Maintenance Cadence#

Use a regular review rhythm that fits your environment to keep two-step access reliable as accounts, devices, and settings change. This is a policy choice, not a universal requirement.

Treat each review as a health check, not a documentation task. Start with critical accounts, then verify authentication setup, then clean up follow-up items.

Checklist for critical access#

- Confirm each critical account still has a working authenticator app sign-in path.

- Verify user-level 2FA activation is still enabled where the platform requires it.

- Confirm device or local server time is accurate and an NTP source is reachable.

- When an account is re-enrolled, validate the QR code or key enrollment flow and authenticator passcode step.

- Record what changed, who reviewed it, and when the next check is due.

Trigger reviews between scheduled checks#

Keep your scheduled review as the baseline. If you run trigger-based checks internally, use access or device changes as prompts. If a user reports code failures, recheck in order: activation state, enrollment state, then time sync.

Track status and control temporary exceptions#

Track a small set of status signals you can maintain consistently:

- Critical accounts with a confirmed working authenticator app path.

- Critical accounts reviewed for activation and time-sync prerequisites.

Document temporary exceptions so fallback methods do not become permanent. For each exception, record account, owner, reason, compensating control, and planned revalidation date.

A cadence only works when ownership is explicit. Assign one person to prepare the list, one person to verify high-impact accounts, and one person to confirm exception follow-up is completed.

Use short review outputs that make next actions obvious:

- Accounts fixed during review.

- Accounts needing follow-up.

- Exceptions still open or closed.

- Date of the next check.

This keeps maintenance practical and helps reduce drift between policy and account settings.

Conclusion#

Treat 2FA as an ongoing habit, not a one-time setting. It adds a second layer beyond passwords and can materially reduce account risk, but it is still risk reduction, not a guarantee.

That matters for business continuity. A compromised account can create privacy loss and direct financial harm, so pick the strongest second factor each account supports. For mobile verification, use an authenticator app when available, and use SMS when stronger options are not offered.

Use this same-day closeout plan:

- Start with your highest-impact accounts.

- Enable 2FA with the strongest available method for each one.

- Run a real sign-in test, and if a one-time code expires, request a new code and continue.

- Schedule a regular 2FA review so this stays repeatable.

Then keep one final rule: every major account change gets a live sign-out and sign-in check. That habit helps keep your access controls current as tools, devices, and account settings change.

Frequently Asked Questions

What is two-factor authentication in one sentence?

It is a sign-in method that verifies identity with two distinct factors. A common example is a password plus an app approval, SMS code, biometric check, or security key. The practical goal is to make one compromised password insufficient for account access.

Is 2FA the same as MFA?

No. 2FA uses exactly two factors, while MFA can use two or more. That makes 2FA one subset of MFA. In practice, the important point is not the label but whether your factors are truly separate.

What are the three authentication factor types?

A practical baseline is three factor types: something you know, something you have, and something you are. Some frameworks also include factors like location, so treat these three as the core model rather than the only possible design. If you are unsure, map each sign-in step to a factor type and check for separation.

Which is better for business accounts, authenticator app, SMS, or security key?

There is no universal winner for every account. Common options include app approvals, SMS codes, biometrics, and physical security keys. Choose a method your provider supports and make sure your recovery steps are clear for that provider.

Can 2FA still be hacked through phishing or MFA fatigue?

Yes. 2FA reduces the impact of phishing, credential theft, and brute-force attacks, but it does not guarantee zero account takeovers. Treat it as risk reduction, not a guarantee.

What accounts should a solo professional secure first with 2FA?

Start with the highest-impact accounts first, especially accounts that store personal or financial information. Then expand across the rest of your business accounts.

What should I do if I lose my phone and cannot get my 2FA codes?

If you have a backup sign-in option, use it first. Then follow your provider recovery or security-device replacement process, because requirements differ by platform. After access is restored, review your factors and recovery options.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 4 external sources outside the trusted-domain allowlist.

- consumer.ftc.gov/articles/use-two-factor-authentication-prote...trusted

- accountablehq.com/post/what-is-two-factor-authentication-2fa-a...external

- accountablehq.com/post/what-is-two-factor-authentication-2fa-b...external

- microsoft.com/en-us/security/business/security-101/what-is...external

- microsoft.com/en-ie/security/business/security-101/what-is...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Best Password Managers for Freelancers and Teams

A client asks for an urgent file, you open their portal, and the login fails. Ten minutes later your invoicing app wants a reset too. That is why your password setup is a business risk, not just a nuisance. Weak credential habits can turn one mistake into wider account access problems, then into delivery delays and cleanup work.

The Best Gear for a Portable Home Office

The evidence here does not directly test portable-office gear decisions, so use this as a practical framework rather than a proven standard.

How to Make Friends as a Digital Nomad

Trying to make friends as a digital nomad can feel harder when every week starts from zero. One practical option is a 30-day onboarding experiment with a small target you can track: for example, three people you would like to see again, plus one recurring social slot that stays on your calendar.