Quick Answer

3D Secure is a pre-authorization identity check for card-not-present payments across merchant/acquirer, issuer, and interoperability domains. If you are asking what is 3D Secure in practical terms, it is a checkout control that can run frictionless for some transactions and challenge others. The article’s core guidance is to deploy 3DS as an operational system: use 3DS2 by default when available, design explicit handling for incomplete challenges, and verify liability assumptions with payment partners before scaling.

How 3D Secure works#

If you're asking what 3D Secure is, the short answer is simple: it adds a cardholder-authentication layer to online card payments, designed to verify identity before authorization. For platform teams, the real question is not whether 3DS exists, but whether your implementation protects revenue and customer data without adding avoidable checkout friction.

Treat 3DS as an end-to-end checkout decision, not a box to tick in gateway settings. It is meant to verify cardholders and reduce unauthorized use, but the outcome depends on how your stack handles authentication in real customer flows.

The stakes are operational, not theoretical. With global digital commerce projected to surpass $8 trillion by 2028, cardholder authentication is a core payments decision for teams balancing risk control with a smooth buying experience.

In practice, deployment decisions often involve EMV 3-D Secure, including modern 3DS2 implementations. Customer experience can vary: some transactions move through with little visible friction, while others require a step such as a One-Time Passcode (OTP) challenge, so your checkout needs to handle both paths cleanly.

This guide is for platform builders making deployment choices across checkout, operations, and risk. It gives you practical decision rules, launch checkpoints, and failure plans you can use in production.

For related platform-control context, see What Is KYB? Know Your Business Verification for Marketplace Onboarding.

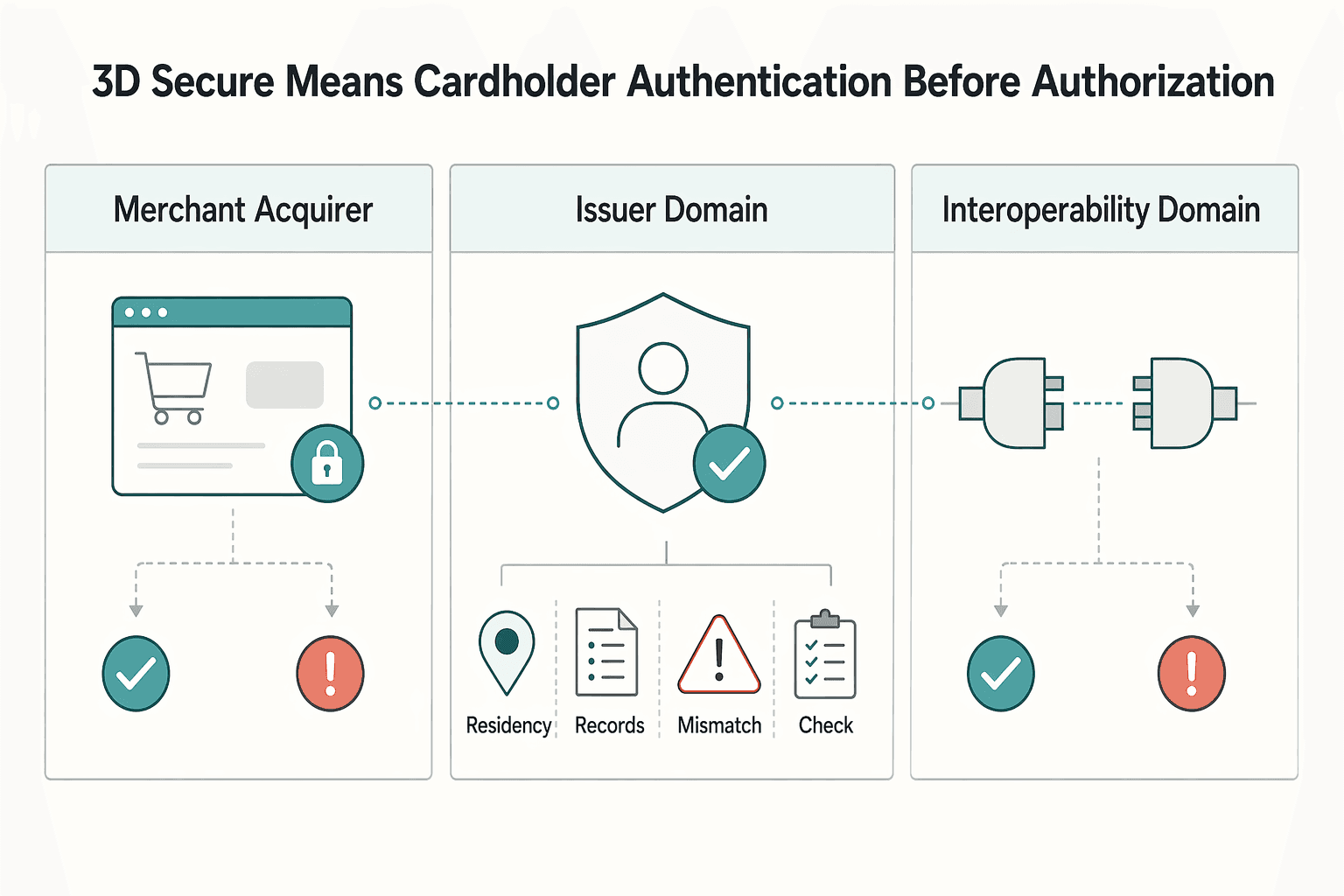

3D Secure means cardholder authentication before authorization#

3D Secure is a cardholder authentication step used in card-not-present payments. In programs like Visa Secure, this verification happens before the transaction is sent for authorization.

| Domain | Description |

|---|---|

| Merchant/acquirer domain | the bank or merchant receiving the payment |

| Issuer domain | the cardholder's issuing bank |

| Interoperability domain | the underlying systems that support 3DS |

It is not the authorization decision itself. Keep those outcomes separate in your data model and reporting. A payment can stop if authentication is not completed, or it can be declined later during authorization.

The "3D" refers to the three domains above, and it helps to keep them separate in your logging and support views.

Operationally, treat 3DS as a multi-party flow, not just a checkout UI element. Customers may be redirected to their issuer or asked to complete a challenge step such as an OTP, so your logs should capture authentication status separately from authorization outcome.

Branded names can blur this distinction. Visa Secure is Visa's program for Visa transactions that use the 3-D Secure standard, not a separate protocol.

In practical terms, 3D Secure is a payer-authentication protocol for card-not-present payments designed to reduce fraud risk.

How the 3DS checkout flow actually works#

3DS is an authentication step inside online card payments. Some transactions continue with little visible friction, while others require the cardholder to verify identity before payment is approved.

The flow starts with transaction data#

The flow typically starts on the merchant or acquirer side, where transaction data is collected and sent for cardholder authentication. From there, the three 3DS domains exchange information to authenticate the transaction.

Providers describe that middle layer differently, and a payment platform or a scheme may use different labels. In practice, it serves as the bridge between the merchant/acquirer side and the issuer side.

Why some customers see no extra step#

With 3DS2, richer data sharing supports better risk assessment and can reduce how often extra authentication steps appear. That lower-friction path matters because additional prompts can hurt conversion.

For higher-risk transactions, configured risk rules can trigger stricter authentication. When that happens, the customer may need to enter a password, an SMS code, or a temporary PIN.

Design for both real UX paths#

Design checkout for both outcomes: a lower-friction path and a stricter-authentication path. If you only design for the lower-friction path, stricter checks can feel like an unexpected interruption.

During stricter authentication, make state explicit: in progress, failed, or retry needed. Customers can pause or fail a code step, so unclear status handling adds avoidable friction.

The tradeoff teams often underestimate#

The tradeoff is straightforward: stronger authentication can add friction. 3DS1 was often associated with clunky steps like device switching or waiting for OTP delivery, and extra steps can still reduce completion rates even with 3DS2 improvements.

If you operate in the EU, this is also a compliance reality: 3DS is mandatory in the PSD2 context. Treat authentication as a normal part of checkout, and optimize both the lower-friction and stricter-authentication paths with equal care.

Related: What is a 'Permanent Home' in the Context of a Tax Treaty?.

3D Secure 1 and 3D Secure 2 are not equivalent for product outcomes#

For product outcomes, 3D Secure 2 should be your default where supported. Treat 3D Secure 1 as legacy fallback. The two are not interchangeable in practice. They differ in checkout friction, mobile fit, and how much context issuers get for risk decisions.

3DS1 is redirect-first, while 3DS2 is risk-based and can keep many payments frictionless or handle challenges in-app or in an embedded overlay. That design difference is why the user experience and completion rates can diverge in live checkout flows.

| Protocol version | UX pattern | Mobile behavior | Data richness for issuer decisions | Operational implications (support + fraud ops) |

|---|---|---|---|---|

| 3D Secure 1 | Full-page redirect to issuer/bank page | Poor fit for modern app and small-screen checkout | Limited context versus newer protocol | Higher redirect-related abandonment risk; less context for fraud review |

| 3D Secure 2 | Embedded challenge (in-app/overlay) or frictionless flow | Better fit for native/mobile checkout (SDK support) | Materially richer inputs (cited as about 10x more data fields) | Better chance of frictionless outcomes; clearer segmentation of challenge vs non-challenge cohorts |

| 3DS1 fallback in modern stack | Compatibility path when legacy routing appears | Redirect-dependent flow with poorer mobile fit than 3DS2 | Typically loses fuller 3DS2 context | Track separately as fallback traffic, not as your primary optimized path |

The conversion gap is mostly a friction story. The cited comparison reports 3DS1 redirect-style flows can reduce checkout conversion by about 3-15%, while 3DS2 is reported at under 5% impact and often neutral or positive. Reported frictionless routing for 3DS2 is 85-95%, with one cited Mastercard estimate around 90% requiring no customer interaction. Treat these as directional, not universal, because outcomes vary by issuer, processor, and market.

EMVCo's protocol evolution matters because newer 3DS versions move beyond browser-era redirects and fit embedded and mobile checkout more cleanly. EMVCo maintains the specification, cited at version 2.3.1, and newer versions support richer data exchange plus modern authentication patterns.

The operating detail that matters most is verification. Do not stop at "3DS2 is enabled." Check by cohort that transactions are actually on 3DS2. Review frictionless versus challenged outcomes, and confirm issuer-bound context such as device fingerprint, transaction history, and shipping address is present. If fallback traffic is blended into overall metrics, you can misread both conversion and support load.

Card-network timelines reinforce the point: Visa and Mastercard ended 3DS1 support in late 2021 and 2022 respectively. You may still encounter legacy paths, but they should be contained as compatibility handling, not treated as a preferred checkout path. Keep policy segmented as well. One cited example shows universal 3DS application produced +30% conversion in India and -55% in Brazil, so challenge policy should be tuned by segment rather than applied uniformly.

Program names can confuse teams so map them once#

Program labels cause avoidable confusion unless you standardize them early. Map every 3DS label to a single internal glossary, and store the protocol version next to the label. The version helps explain checkout behavior and reporting differences, because 3DS1 and 3DS2 do not behave the same way.

| Field | What to include | Example |

|---|---|---|

| Label exactly as shown | label exactly as shown by the PSP or network | Visa Secure |

| Protocol version | protocol version when available | 1, 2.1, 2.2, 2.3 |

| Where the label appears | where the label appears | API field, dashboard column, or customer message |

| Observed authentication outcome | observed authentication outcome | observed authentication outcome |

| Internal owner | internal owner for the mapping | payments or product ops |

In processor docs, legacy tickets, or fraud reviews, you may see labels like Visa Secure, Visa Secure 3DS1, Verified by Visa, and MasterCard Secure Code. Treat these as program labels around 3D Secure, not proof that transactions followed the same protocol path.

Keep the glossary simple and exact. Include:

- label exactly as shown by the PSP or network

- protocol version when available, for example 1, 2.1, 2.2, 2.3

- where the label appears, such as an API field, dashboard column, or customer message

- observed authentication outcome

- internal owner for the mapping, for example payments or product ops

For validation, compare the dashboard label with raw authentication fields in logs or provider exports. If a cohort is labeled "Visa Secure," verify in those fields whether it is running as 3DS1 or 3DS2.

Failures here are often organizational as well as technical. Product, finance, and support can all draw the wrong conclusions when naming is inconsistent. Keep one approved glossary in payments documentation and reference it in support macros and KPI definitions.

Choose challenge policy with explicit tradeoffs not gut feel#

A single global default can be the wrong policy. Set your 3DS posture by segment, with named owners and review points, because authentication in card-not-present flows can involve tradeoffs between checkout friction and risk control.

A first-time payer and a repeat payer may not need the same starting posture. Use segment defaults, then require documented exceptions.

| Transaction context | Candidate 3DS posture to test | Potential conversion impact (hypothesis) | Potential risk-control impact (hypothesis) | Owner for override decisions |

|---|---|---|---|---|

| First purchase with limited internal history | Consider a challenge-preferred default, with named exceptions | Friction may increase; validate with internal data | More identity checks in flow; validate outcomes | Risk |

| Repeat payer with stable internal history | Consider a frictionless-preferred default, with monitoring | Friction may decrease; validate with internal data | Challenge steps may be fewer by default; monitor outcomes | Product, with risk veto |

| Account-change window (for example recovery or profile/security change near payment) | Consider a temporarily stricter posture | Completion may dip while active; validate with internal data | More identity confirmation in a sensitive window; monitor outcomes | Risk and trust/safety |

| Segment under active fraud review | Consider temporarily tightening posture, then re-review on schedule | Completion may drop while active | Short-term containment while investigating | Risk, with payments ops informed |

Treat the table as a policy baseline, not a guaranteed outcome model. Fixed challenge-rate targets, fraud thresholds, conversion deltas, or monetary cutoffs are not established here, and several details are not usable for detailed 3DS policy extraction, so keep those as internal test hypotheses rather than hardcoded rules.

Hard rules to prevent policy drift#

Once you choose a segmented policy, lock down how changes happen with rules like these:

- If a segment moves to stricter authentication, log the reason, owner, start date, and review date before launch.

- If product requests a more frictionless path for a sensitive segment, scope it to a named cohort and track it separately.

- If a merchant tier gets a custom rule, store it in one shared payments policy record, not in chat or tickets.

- If support reports confusing challenge steps, including conflicting OTP instructions, treat that as a policy review trigger, not only a support script issue.

- If teams disagree on posture, no change goes live without a single accountable approver recorded.

The goal is consistent judgment you can explain and repeat across markets and merchant tiers, even when pressure shifts between conversion and fraud.

Failure modes to design for before launch day#

Before launch, assume some 3DS sessions will end in an incomplete state, not a clean success or failure. Your job is to make those cases recoverable, visible, and clearly separate from completed authorization.

That matters because issuers control whether a payment goes through a challenge or frictionless flow, and issuers return the authentication result that you include at authorization time. Treat that result handoff as a hard checkpoint. Otherwise, you can end up with one system showing "paid" while another shows "failed."

Test for issuer variability, not one happy path#

Issuer behavior varies, so pre-launch testing should cover at least these outcomes:

- issuer-selected flow does not complete

- customer abandons the challenge

- challenge does not complete in session

- authentication result is missing when authorization is attempted

- authentication result does not match the expected order or payment attempt

Use one strict rule. If a challenge is incomplete, or you do not have a usable authentication result tied to the correct attempt, do not move the order to paid or authorized. Move it to a distinct internal state such as "authentication incomplete" or "authentication review needed."

Make handoff and retry behavior idempotent and visible#

If your integration retries after a failed or incomplete handoff, retries need to be both idempotent and visible. Bind them to the same order or payment attempt, and make sure ops tooling shows what happened.

Enforce one reconciliation checkpoint per authentication attempt: keep a stable internal payment reference plus provider references for each 3DS step. Without that, support and ops end up doing manual forensics across logs, provider dashboards, and tickets.

If a retry path can create a second authentication attempt or re-send authorization, that is not a minor reliability bug. It is a money-movement risk.

Define fallback for incomplete 3DS responses#

Set a deterministic fallback rule before launch: incomplete 3DS responses should land in a known terminal or recoverable state, never an ambiguous one.

Decide ownership in advance. Either the customer can safely resume, or the flow must be explicitly failed and restarted. Do not leave orders between "authorized" and "failed" while teams guess whether to fulfill, retry, or refund.

Give support a root-cause map, not a generic script#

Support usually hears "authentication got stuck" first, so give them a map that ties customer language to technical buckets and evidence collection.

| Customer report | Likely root-cause bucket | What support should collect | Immediate handling rule |

|---|---|---|---|

| "My bank screen never loaded" | Issuer-selected flow did not load or complete | order ID, payment attempt time, screenshot if available | Do not confirm payment success; route to payments ops check |

| "I approved it, then nothing happened" | Authentication result handoff issue | order ID, last visible screen, bank app confirmation if shown | Check for missing authentication result before retry |

| "I closed the window and came back" | Abandoned challenge | order ID, whether a second attempt was made | Treat as incomplete authentication, not completed payment |

| "I got two different outcomes" | Authentication result mismatch or duplicate continuation | order ID, email receipt status, card hold details if available | Escalate for reconciliation before fulfillment |

If you enforce one pre-launch gate, make it this: pass tests for abandoned or incomplete challenge paths, missing result handling, and duplicate-retry handling before scaling traffic.

For a step-by-step walkthrough, see What Is Churn Rate? Measuring Subscriber Loss for Subscription Platforms.

Liability and chargeback outcomes need precise caveats#

Successful authentication is not the same thing as a guaranteed chargeback outcome. If Visa Secure or Mastercard Identity Check is presented internally as "fraud liability solved," finance and ops can make avoidable mistakes.

Keep three outcomes separate in reporting and stakeholder updates: did authentication complete, did authorization succeed, and what dispute exposure remains after both steps.

Treat liability shift as conditional#

You will see claims that 3-D Secure can shift residual fraud liability to the issuer. A vendor case study published on 30 July 2025 makes that claim for its own implementation. Treat that as a vendor-stated outcome, not a blanket rule across Visa and Mastercard rails.

Use a strict messaging rule: do not approve statements like "no chargebacks after authentication" unless your acquirer or processor confirms the applicable program terms in writing. If that confirmation is missing, treat the liability claim as unverified.

Explain protocol success and dispute outcomes as different layers#

Teams may hear "authenticated" and infer "protected." That compresses too much into one label. Authentication success does not automatically determine dispute outcomes. Use this model in dashboards and case notes:

- Authentication outcome: completed, challenged, incomplete, or failed

- Authorization outcome: approved or declined

- Dispute outcome: subject to network, issuer, acquirer, and program conditions

Keeping these fields separate helps avoid a reporting failure where strong authentication completion is reported while chargeback exposure is assumed to be zero.

Verify the terms before you scale the claim#

The key checkpoint here is documentary, not technical. Before launch or expansion, get written confirmation from your acquirer or processor on the liability statements you can rely on for your 3DS traffic. At minimum, keep:

- written program-term confirmation from your acquirer, processor, or network-facing partner

- end-to-end test results across purchase paths, including renewals or special-event flows where relevant

- support escalation contacts for major launches, since real-time vendor collaboration may be needed if fraud controls degrade at volume

Keep the risk story conservative#

The safest way to describe 3DS is as one control in a broader defence-in-depth approach. The underlying guidance is consistent: teams must balance customer experience with fraud prevention, and no single strong customer authentication approach fits every scenario.

Use cautious language in internal and external materials. 3DS adds an authentication step and may affect fraud liability under specific program terms. It does not mean "chargebacks are gone." A practical rule is simple: no blanket liability statement goes live until it is verified against your acquirer and documented for your exact program setup.

This pairs well with our guide on What Is Strong Customer Authentication? EU Mandate Explained.

Assign ownership before you assign engineering tickets#

Clear ownership matters before the first ticket is filed. If ownership is vague, 3DS incidents around challenge flow and authentication-result handoff can stall quickly.

Use this split as an operating model, not a network-mandated rule. Product can own challenge policy and UX thresholds. Engineering can own enrollment lookup and authentication-result handoff reliability. Payments ops can own exception handling and partner escalations. Finance or risk can own fraud and dispute monitoring for card-not-present transactions.

| Function | Owns | Practical checkpoint |

|---|---|---|

| Product | Challenge policy, UX thresholds, customer messaging | Is it clear when you expect a frictionless flow versus a challenge step, knowing challenge behavior can vary by issuer and risk signals? |

| Engineering | Enrollment lookup and authentication-result handoff reliability | Do you reliably capture enrollment lookup and the authentication result before sending transaction information to the acquiring bank? |

| Payments ops | Exception queues, reconciliation, processor/network escalations | Can ops trace authentication outcomes, including customer trust confusion and device-compatibility issues, quickly enough to escalate with partners? |

| Finance/risk | Fraud and dispute monitoring for card-not-present transactions | Are authentication outcomes reviewed with fraud and dispute trends before policy changes are made? |

This ownership model keeps rollout and incident response practical: product sets friction tolerance, engineering protects handoffs, ops handles exceptions, and finance or risk sets risk limits.

Use this production rollout checklist#

Before you launch live volume, make sure you can trace each payment attempt from issuer authentication to authorization with the authentication result attached. That is the baseline that keeps checkout, support, and reporting aligned once real traffic starts.

| Area | What to confirm | Note |

|---|---|---|

| Core handoff | your 3DS provider sends the authentication request to the issuer, the issuer returns an authentication result, and your authorization request includes that result | Confirm end to end |

| Issuer-dependent pathing | authentication can be frictionless or challenge-based, for example password or OTP | Validate in the support flow |

| Production paths | get written provider confirmation on which authentication paths can appear in production | Written confirmation |

| Pre-launch tests | test both challenge and frictionless outcomes, and verify your authorization step includes the issuer authentication result | Issuer-boundary scenarios |

| Operational views | prepare internal operational views so teams can trace authentication outcomes to authorization decisions | Before go-live |

| Liability language | liability shift can apply when issuer authentication succeeds; it is not universal across all cases | Keep operations docs precise |

| Market caveat | Clover describes 3DS as optional in North America and priced at 4¢ per transaction (USD or CAD), while Europe is tied more closely to PSD2 strong customer authentication expectations | Confirm with your processor or acquirer before scaling |

Monitor performance after go-live with one decision cadence#

After go-live, set one weekly decision cycle and stick to it. A fixed cadence helps keep policy changes grounded in evidence instead of support noise or one-off incidents. In that review, look at these operational metrics together:

- challenge rate

- challenge completion rate

- authentication success rate

- conversion delta

- fraud and dispute trend

Keep the definitions consistent week to week, and treat incomplete evidence as unresolved until it can be classified. If key event links are missing, hold policy changes until the trail is complete.

If you run both 3D Secure 2 and fallback paths, review those cohorts separately when data is available. Blended totals may mask path-level changes, so treat missing or mixed data as unknown rather than assuming both paths are performing the same.

End each weekly checkpoint with one action against pre-agreed internal thresholds and incident volume:

- Keep policy when performance and risk stay within your agreed range.

- Tighten policy when risk is rising and current authentication controls are not containing it.

- Relax policy when conversion or completion drops and internal evidence points to avoidable friction or technical failure.

Tie this cadence to economics as well as risk, because payment processing fees can materially affect profitability at scale and the cost stack includes both fixed and negotiable components. Use your own baselines for 3DS decisions; no universal 3DS benchmark thresholds are established here. For a practical framework, see 3D Secure Conversion Data: What the Numbers Say About Authentication and Drop-Off.

Related reading: What Procurement Means for Platform Operators Managing Strategic Sourcing and Vendors.

What to do next#

The next step is not a broad rollout. Start narrow, prove that policy and handoffs work, and expand only when the results are stable. The objective is to protect revenue and customer data without adding unnecessary friction.

Set policy by segment first#

Do not apply one blanket rule to all card-not-present transactions. Segment traffic into a small set you can operate well, apply stronger authentication where risk is higher, and keep a frictionless path for lower-risk traffic.

Where supported, use 3D Secure 2 as the default path and treat 3D Secure 1 as legacy handling. Before launch, confirm three things with your payment partners:

- Which segments trigger or prefer 3DS, and which stay frictionless

- What your fallback is when issuer responses are slow, unavailable, or incomplete

- How the three domains, acquirer, scheme, and issuer, appear in logs and support tooling

Launch with explicit failure handling and KPIs#

Many rollout issues show up in challenge and exception paths, not just the happy path. Define in advance when to retry, when to fail cleanly, and when to ask the customer to try again.

Test challenge flows end to end on real devices, including issuer SMS one-time PIN flows where used. Also prepare support for customers who distrust authentication pop-ups or issuer pages because they can look like phishing. From day one, track:

- Challenge rate

- Challenge completion rate

- Authentication success rate

- Conversion change by segment

- Support contacts tagged to stuck authentication or suspicious pop-up

Expand market by market#

For multi-market stacks, validate each market and program before widening traffic. 3DS is available for CNP transactions across major card networks, but caveats still apply, and PSD2 is the key EU check.

Use a strict sequence: confirm coverage, confirm fallback behavior, confirm local caveats, then ramp traffic gradually. If your provider says 3DS is enabled, verify that the actual 3DS2 flow, challenge handling, and reporting are truly in place for that market.

If you are aligning 3DS policy with cross-border collections and payout operations, talk to Gruv to confirm market and program coverage.

Frequently Asked Questions

What is 3D Secure in one sentence?

3D Secure (3DS) is a cardholder authentication protocol for card-not-present online transactions. In checkout terms, it adds an authentication decision before the payment is finalized.

What do the three domains mean in practical checkout terms?

In practice, the acquirer domain is the merchant-side payment flow, the issuer domain is the cardholder bank making authentication decisions, and the interoperability domain connects the two. If authentication results are missing or mismatched, a practical first troubleshooting step is checking that handoff path.

How is 3D Secure 2 different from 3D Secure 1 for conversion and risk?

3D Secure 2 is the newer version and supports enriched data sharing plus dynamic methods such as biometrics and token-based authentication. That added context supports risk-based decisions, so some low-risk payments can complete frictionlessly instead of forcing every transaction into a challenge flow.

Does 3DS always add checkout friction?

No. Low-risk payments can go through a frictionless path with no OTP or biometric challenge. But when a challenge is triggered, it adds a step that can increase dropoff or failed payments, so track challenge rate and completion rate together.

Does 3DS eliminate fraud or chargebacks?

No. The source guidance is not universal: one provider states 3DS protection is limited to fraud-related chargebacks, while another source makes a stronger claim for one specific program. Treat liability and dispute outcomes as setup-specific, and confirm the exact terms with your payment partners before making internal promises.

Who should own 3DS decisions across product, engineering, ops, and finance?

This guide does not define a single mandatory ownership model for 3DS decisions. In practice, make ownership explicit across product, engineering, ops, and finance, and confirm that “enabled” in provider settings matches a fully completed API integration.

How should a platform decide when to force a challenge versus allow frictionless authentication?

Decide by transaction risk instead of defaulting every payment to the same path. Use stronger authentication on higher-risk transactions and allow frictionless authentication where risk is lower, then review conversion and risk outcomes together. If challenge failures cluster around OTP delivery, verify customer contact details.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- cisa.gov/news-events/bulletins/sb25-174trusted

- cms.gov/regulations-and-guidance/guidance/manuals/do...trusted

- congress.gov/crs-product/R47884trusted

- csrc.nist.gov/CSRC/media/Projects/risk-management/800-53%2...trusted

- dhs.gov/sites/default/files/publications/fps-pso-med...trusted

- eba.europa.eu/eba-response/245trusted

- en.wikipedia.org/wiki/3-D_Securetrusted

- federalreserve.gov/frrs/regulations/board-interpretations-of-re...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: