Quick Answer

Handle a single transaction across multiple recipients by locking the split model and fund flow before you build. Define split logic, fund custody, payout timing, and reconciliation ownership, then test one sample order from checkout through payout. Confirm your PSP supports the model, make payout event handling replay-safe, apply compliance gates before release, and launch with reconciliation controls from day one.

What Multi-Party Payments Actually Involve#

Teams can get split payments wrong long before they get the API calls wrong. The real work is deciding how one customer payment is allocated across recipients, who holds funds before release, when payouts happen, and who owns reconciliation when records conflict.

"Split payments" is a broad term. It can mean splitting across payment methods, or splitting one purchase across multiple recipients. This guide is about the platform and marketplace case: one transaction, multiple payees, often with a platform fee. If your actual problem is split tender at checkout, reset scope now. The operating model and provider evaluation can be different.

For founders, product, engineering, and finance ops, the better question is not "who has a split feature?" It is "which operating model can we run reliably?" Manual payout handling is where delays, reconciliation errors, compliance risk, and vendor frustration often surface. Complexity also rises as stakeholder count grows. It can rise further when multiple PSPs bring conflicting processes and more engineering overhead.

Start with one rule: lock the split model and fund flow before implementation. If allocation rules are stable at checkout, the first version can stay narrow. If amounts can change after fulfillment, milestones, or approvals, design for changing allocation rules, payout holds, and exception handling from day one. Pushing that work into event handling later can make payouts drift away from finance records.

Before you start#

Write down these four decisions in plain English and get product, engineering, and finance to sign off:

| Decision | What to write down |

|---|---|

| Split logic | What determines each recipient share, and when can that share change? |

| Fund custody | Where does money sit between collection and payout release? |

| Payout timing | Is money released immediately, on a schedule, or only after approval criteria are met? |

| Reconciliation ownership | Which team resolves mismatches between provider events, payout outcomes, and internal records? |

- Split logic

What determines each recipient share, and when can that share change?

- Fund custody

Where does money sit between collection and payout release?

- Payout timing

Is money released immediately, on a schedule, or only after approval criteria are met?

- Reconciliation ownership

Which team resolves mismatches between provider events, payout outcomes, and internal records?

This short document is more useful than a fast demo. For any sample order, your team should be able to explain expected recipient amounts, release conditions, and resulting internal records before opening integration tickets. Then work in sequence. Choose the allocation and release model, implement clear event handling, and launch with reconciliation controls so finance has a defensible record, not just an app status.

Keep recipient verification and release controls in view early. This guide does not define legal thresholds, but payout design still has to work with real verification and release conditions. Some providers support holding funds and releasing only when criteria are met, including beneficiary verification during onboarding. If your model includes conditional release, treat that as a core design choice, not an edge case.

By the end of this article, you should have a practical path to implement, reconcile, and support multi-party payment splits without improvising under pressure.

For a step-by-step walkthrough, see How to Handle Failed Payments Across Multiple Payment Methods and Regions.

Pick the split model before you touch APIs#

Choose one operating pattern before integration work starts, then test it from checkout through payout so product, engineering, and finance interpret each order the same way.

Step 1. Define the operating pattern in plain English#

| Decision area | What to define now | Failure mode to watch | Minimum checkpoint before build |

|---|---|---|---|

| Split scope | Whether a transaction is split across payment methods, multiple recipients, or both | Teams start integration without a shared definition of what is being split | One sample order documents the gross charge and every intended split amount |

| Pricing responsibility | Who is responsible for processing fees in your provider model | Fee ownership is unclear, so payout math and margin assumptions diverge | Fee responsibility is documented before build starts |

| Checkout-to-payout flow | How funds move from checkout through payout | Checkout works, but payout behavior is not validated | One sample order is mapped end-to-end from checkout through payout |

Step 2. Make the choice testable before integration starts#

Before you touch a provider dashboard, run one sample order and answer five questions clearly: the gross charge, recipient amounts, when amounts become final, what can still change before payout, and what event triggers payout.

Document how changes are recorded so the flow remains testable before integration begins.

Step 3. Verify that your PSP can support the model you chose#

Pressure-test your model against actual Payment Service Provider (PSP) behavior before you build. Stripe explicitly frames split-payment implementation as an end-to-end checkout-to-payout flow, which is the right checkpoint. Ask each provider the same questions early, using one real sample order:

| Pricing item | Price shown | Notes |

|---|---|---|

| Monthly active account | $2 per monthly active account | Counted in months where payouts are sent |

| Payout sent | 0.25% + 25¢ per payout sent | A payout occurs each time funds are sent |

| Instant Payouts | 1% of payout volume | Shown on Connect pricing |

| Domestic card transactions | 2.9% + 30¢ | Shown for domestic card transactions |

| ACH Direct Debit | 0.8% with a $5.00 cap | Shown for ACH Direct Debit |

- Can one purchase be allocated to multiple recipients in your flow?

- Who is responsible for processing fees: platform or recipient side?

- What counts as a payout for billing?

- What conditions must be true before funds are sent?

On Stripe Connect, fee responsibility is a core design input. Stripe offers one model where Stripe sets and collects users' processing fees, and another where the platform is responsible for Stripe processing fees. Connect pricing also shows $2 per monthly active account, 0.25% + 25¢ per payout sent, and 1% of payout volume for Instant Payouts. A monthly active account is counted in months where payouts are sent, and a payout occurs each time funds are sent.

Collection costs belong in the same decision. Stripe pricing shows 2.9% + 30¢ for domestic card transactions and 0.8% ACH Direct Debit with a $5.00 cap. Provider choice affects both product flow and cost structure, and pricing can change, so re-check current pricing before you lock the split model.

If you want a deeper dive, read Adaptive Payments for Platforms: How to Split a Single Transaction Across Multiple Payees.

Decide who holds funds and who actually processes them#

Once you choose a split model, name the trusted party for each money movement. If you skip this, teams can work from different assumptions when payouts are delayed or disputed.

The grounding supports two trust patterns: rely on a trusted party that ensures transfers, or design a decentralized flow without a trusted authority. For platform operations, role boundaries between policy, orchestration, and processing should be treated as explicit decisions, not defaults.

Step 1. Name authority per movement stage#

Define one owner and one observer for each stage: collection, holding period, release decision, disbursement initiation, and status reporting. If two teams believe they can release funds, the control model is not defined yet.

Use one sample order to confirm:

- Who accepts payer funds

- Who can authorize release

- Who can only observe or reconcile

- Which record wins when statuses conflict

If you cannot assign a single owner per stage, stop before deeper integration. Operational issues can appear as manual overrides, off-ledger adjustments, and dashboard conflicts.

Step 2. Treat Merchant of Record (MoR) as an explicit decision#

Do not use Merchant of Record (MoR) as a casual label. The grounding here does not support a universal rule for when MoR is legally required, so document the business and legal decision directly.

State one clear position in the architecture docs. Either MoR is an approved assumption for this flow, or it is not assumed and the platform is operating under another model. Record the decision owner, approval date, and open questions so the decision stays auditable.

Step 3. Document where money is between collection and payout#

Make "where money is believed to be" explicit at each state, without inventing custody mechanics. If inbound transfers or Virtual Accounts are in scope, mark each as validated, unknown, or not used until provider behavior is confirmed.

A compact funds-state table can be enough, and any pending state without a named authority or exit event is a control gap:

| Field | What to capture |

|---|---|

| State name | The internal name for the funds state |

| Authoritative record | Which record controls that state |

| Balance visibility | What balance view is available at that point |

| Next allowed action | What can happen next, and by whom |

Step 4. Define release authority for ACH and RTP#

For ACH and RTP, document release triggers and permissions as fields to validate, not assumptions. Keep rail-specific rules and timeline defaults provider-verified. Use a release-authority matrix with:

- Rail (

ACHorRTP) - Release trigger, meaning the exact internal event or approval record

- Who can initiate, if applicable

- Whether any override path exists, and if so, by whom and why

- Who can observe only, if applicable

- Evidence required, such as a linked order, review note, or support artifact

That evidence trail helps when release actions are blocked, duplicated, or disputed.

Need the full breakdown? Read How to Set Up a Multi-Entity Payment Structure for Global Platform Operations.

Prepare the implementation evidence pack before build starts#

Freeze the evidence pack before build starts so teams test one agreed version of tax inputs. Keep payment-ops assumptions (split behavior, event handling, and compliance gating) in a separate track.

Step 1. Publish the split rules and expected journals#

If you publish split rules, treat them as operational assumptions pending separate platform/provider validation. This IRS pack does not verify split behavior, payout outcomes, or ledger journals design.

Use one checkpoint: each team should produce the same result from the same example. If results differ, the rule is not ready for build.

Step 2. Define the integration contract without guessing provider behavior#

Document webhooks and idempotency assumptions in one contract, but keep them explicitly unverified until provider-confirmed. This IRS pack does not establish retry behavior, dedupe keys, or replay handling.

Keep ownership explicit. Name who approves contract updates, where example events live, and which replay scenarios must pass before implementation is accepted.

Step 3. Separate compliance and tax prerequisites by flow#

Track KYC, KYB, AML, and VAT validation in a separate compliance workstream. This IRS pack does not define market/program rules for those controls.

| Item | What the article says |

|---|---|

| W-8 | Out of scope here unless separately validated |

| W-9 | Out of scope here unless separately validated |

| 1099 | Out of scope here unless separately validated |

| FBAR | Out of scope here unless separately validated |

| Form 2555 or 2555-EZ | Document whether you need data to support FEIE claims |

| Year income was earned | Include the year income was earned even if payment arrives later |

| Physical presence test | 330 full days in a 12-month period |

| Full day | 24 consecutive hours |

| Missing the 330-day threshold | Fails the test even for illness, family problems, vacation, or employer orders |

| Limited waivers | May apply for war, civil unrest, or similar adverse conditions |

For tax inputs, keep FEIE checkpoints explicit and treat W-8, W-9, 1099, and FBAR requirements as out of scope here unless separately validated. FEIE applies only for qualifying individuals with foreign earned income who file a U.S. return reporting that income. For FEIE checkpoints, document whether you need data to support Form 2555 (or 2555-EZ) claims, include the year income was earned even if payment arrives later, and when relevant support the physical presence test standard of 330 full days in a 12-month period, with a full day counted as 24 consecutive hours and counted only while the tax home is in a foreign country. Missing the 330-day threshold fails that test even for illness, family problems, vacation, or employer orders; limited waivers may apply for war, civil unrest, or similar adverse conditions.

Step 4. Freeze go-live acceptance criteria#

Lock the go-live pass or fail list before build starts. At minimum for this IRS-grounded pack, include FEIE filing/reporting assumptions, the Form 2555 checkpoint, year-earned mapping, and physical-presence-test criteria. If a criterion is still being debated during launch week, treat it as not accepted.

Related reading: Intercompany Payments for Multi-Entity Platforms in Cross-Border Transfers. Use this evidence pack as a go-live gate, then align operational contracts and reconciliation surfaces in Gruv Docs.

Step 1 map the full transaction and split lifecycle#

Map the full flow from checkout to payout before you build. This is where the evidence pack turns into an actual operating sequence.

Start by fixing scope in plain terms. Split payments can involve multiple payment methods, multiple payers, or multiple recipients, and your lifecycle map should state which of those you are implementing. If that scope is ambiguous, teams can optimize for different assumptions. For marketplace-style flows, include how one transaction is routed to multiple recipients.

Use one shared lifecycle artifact that covers the full path:

| Lifecycle point | What to define now |

|---|---|

| Checkout | Transaction intent and total amount |

| Payment execution with the PSP | Provider reference and payment outcome |

| Split allocation | Which parties receive funds from the transaction |

| Recipient disbursement | Payout path and exception handling |

| Reconciliation check | How you verify checkout-through-payout outcomes |

Before orchestration changes, review the business model and existing payment flow with technical leads. Before build starts, walk key success and exception paths end to end, and flag where work is still manual. Manual payment splitting, accounting, and reconciliation can increase human-error risk, and adding payment service providers can increase implementation cost and complexity.

This pairs well with our guide on How to Reconcile Multi-Currency Payouts Across Multiple PSPs in One Ledger.

Step 2 implement eventing and replay-safe payout execution#

Build this step so one payout instruction produces one intended outcome, even when external events arrive late, duplicated, or out of order. If the lifecycle map is clear, event handling becomes easier to make safe.

Make payout handling replay-safe by default. Treat idempotency as an engineering guardrail across payout creation, status updates, and reversal handlers, not only at payment initiation. Use stable dedupe keys tied to stable references so retries, restarts, and replays are less likely to create duplicate money movement.

Keep two views of truth at the same time:

- An append-only event history for audit and replay

- A current-state record for fast operational decisions

Replay capability matters, but live payout decisions should not depend on replaying all events from 0 to n on every read.

Ingest external events as potentially unordered. Verify ordering behavior in your own PSP contract before relying on it. If ordering is uncertain, evaluate each event against allowed transitions before mutating payout state.

At ingestion, preserve enough raw event context for investigation and define clear failure handling paths. Treat webhook-signature, retry-window, and queue-design details as implementation choices. For secure payment flows, ensure KYC and origin-identification requirements are reflected in your process design.

- Isolate untrusted events

- Queue trusted but temporarily unprocessable events

- Support replay after code or mapping fixes

Persist references that make audit and reconciliation practical. Event-sourced patterns are often used when audit/compliance needs require reconstruction, so keep enough internal and external identifiers to trace execution without manual stitching.

| Example record field | Why it matters |

|---|---|

| Internal transaction intent ID | Connects the split to the original payment decision |

| Internal payout instruction ID | Identifies the specific disbursement attempt |

| Provider payout or transfer reference | Links external execution to internal records |

| Provider event ID or stored raw event | Supports dedupe, replay, and investigation |

| Reversal reference, when present | Connects corrections to the original payout trail |

Verify failure paths before cutover. Run pre-production checks that exercise replay-safe behavior:

- Duplicate-event simulation for create, update, and reversal paths

- Partial-failure simulation with retry to confirm no double effects

- Stale-event replay tests against terminal and near-terminal states

- Reference-trace checks from internal IDs to provider records to reconciliation records

Build replay tooling before launch, even if it is limited and operator-only. That keeps incident recovery and post-fix reprocessing controlled and fast, and supports catch-up when new consumers join later.

Step 3 apply compliance and tax gates at the right moments#

Treat compliance and tax as pre-release controls, not post-payout cleanup. Decide release eligibility before creating a disbursement attempt, and keep tax scope limited to what your system can collect and track.

Put release gates before payout creation#

If a provider program requires KYC, KYB, AML, or VAT validation, treat those checks as program-specific and verify current requirements before marking a payout releaseable.

At minimum, each payout instruction should store a compliance snapshot reference, a decision timestamp, and the ruleset version used for the approval decision.

If you cannot answer "which checks cleared this release?" from one record, holds and manual reviews become slow and error-prone. If a flow has partial gate coverage, document that gap explicitly.

Validate upstream data without over-claiming#

Run recipient profile validation upstream so payout release is not the first time bad data surfaces. If VAT validation is part of your program, validate early and persist the result with the recipient profile, rather than rechecking ad hoc during payout handling.

For blocked payouts, show operators exactly what failed, the latest validation status, and whether the next action is recipient remediation, internal review, or provider escalation.

Separate tax document handling from recipient tax outcomes#

Keep "documents your system tracks" separate from "tax positions a recipient may claim." This section does not establish when W-8 or W-9 is required, how 1099 must be generated, or any FBAR thresholds or triggers.

FEIE is the clearest boundary. The IRS states the exclusion applies only to a qualifying individual with foreign earned income, and the person still files a U.S. return reporting that income. A concrete filing artifact is Form 2555. Under the physical presence test, one route is 330 full days in a foreign country or countries during 12 consecutive months, and a full day is 24 consecutive hours from midnight to midnight. Missing that threshold fails the test regardless of illness, family problems, vacation, or employer orders, though the minimum time requirement can be waived in adverse conditions such as war or civil unrest.

Operationally, that means your payout logic should track required records and document status, while recipient FEIE or FBAR determinations stay in tax analysis unless counsel explicitly directs otherwise.

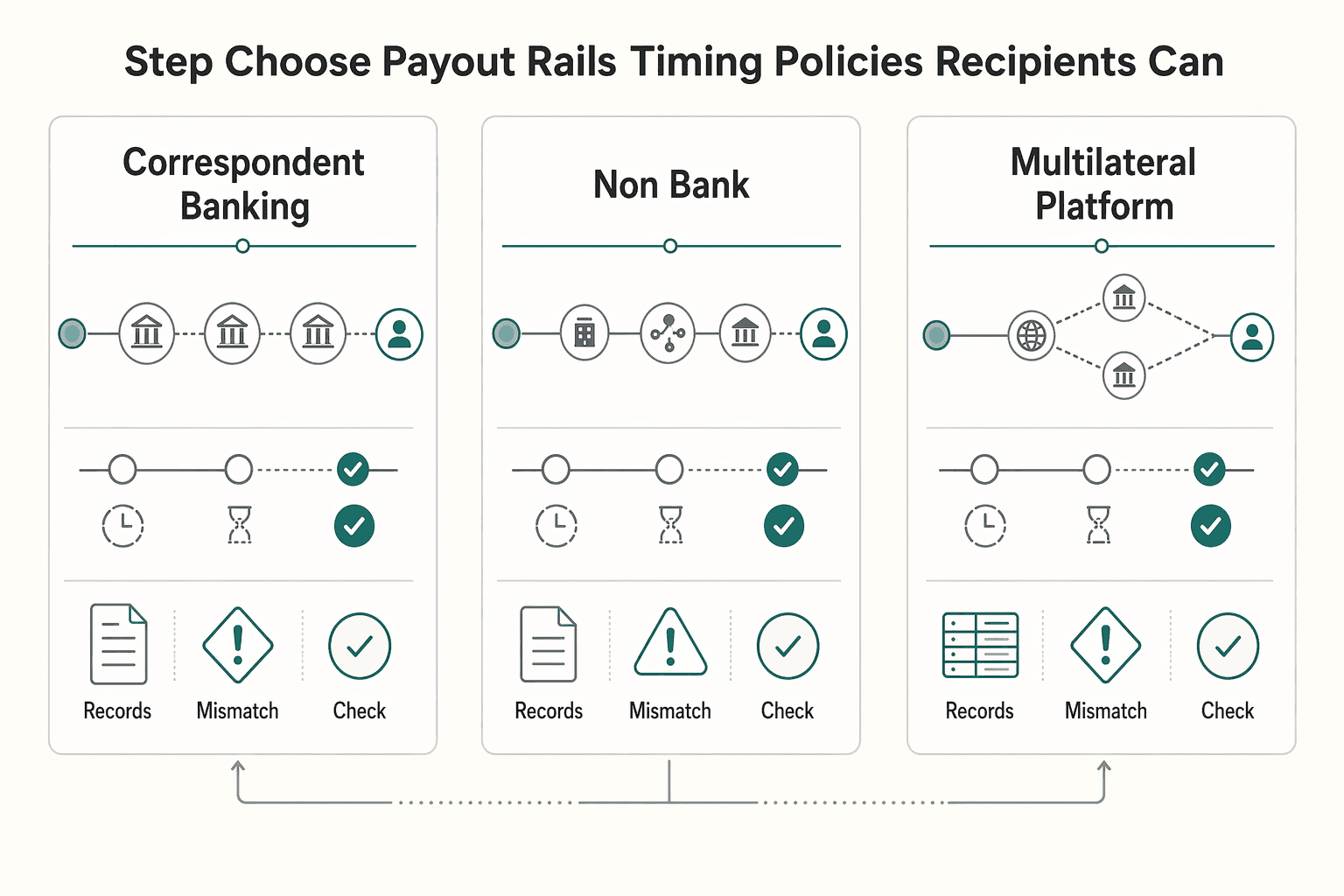

Step 4 choose payout rails and timing policies recipients can trust#

Once a payout is eligible for release, choose the rail based on reliable completion signals and explainable failure handling, not headline speed. Set recipient timing promises from your observed payout states, not processor marketing.

Rank rails by completion behavior first. Cross-border rail categories can look similar at the API layer but behave differently after submission. Prioritize what your team can observe and explain: initiated versus processing versus complete, pending-state behavior, and failure clarity.

| Rail or rail category | What to promise recipients | Main operator concern |

|---|---|---|

| Correspondent banking system | "Your international transfer is in progress; timing can vary by corridor and intermediary chain." | Delay and fee variability across corridors |

| Non-bank money transfer operators | "Your international payout is being routed through a specialist network; timing and outcomes depend on corridor conditions." | Corridor fit and flow conditions |

| Multilateral platform | "Your international payout is being routed through a multi-jurisdiction platform; timing depends on participant coverage and platform design." | Implementation risk, barriers, and operating-hour coverage |

For cross-border payouts, this tradeoff is structural. Traditional correspondent chains can add intermediaries, while non-bank operators may lower costs in some corridors, and multilateral platforms can shorten chains but still come with risk and implementation challenges.

Set timing promises from confirmed states. Use the slowest reliable confirmation point in your event model as the external promise. If completion is confirmed later, "submitted" is not "paid."

This matters even more in multi-step flows. When completion requires an initial request plus one or more update calls, recipient messaging should stay in processing language until completion is actually confirmed.

A practical status model is:

- Submitted

- Processing

- Completed

- Action needed

Map each status to a concrete provider event or internal decision point, and store provider reference, latest event timestamp, and accepted state per payout.

Define fallback logic before you need it. If you support multiple rails, decide fallback behavior in advance and make it explicit to recipients. Do not silently reroute. Use a simple policy sequence:

- Check whether the selected rail is available for that recipient and program.

- If unavailable, check whether an alternate rail is allowed under payout policy and current compliance state.

- Record original rail, replacement rail, reroute reason, and decision timestamp.

- Control automatic reroutes to reduce duplicate-send risk when late events arrive.

In split payouts, keep this trail per recipient so mixed outcomes stay visible to support and ops.

Treat Virtual Accounts as a measured choice, not a default. For bank-transfer-first flows, validate Virtual Accounts with a pilot before wider rollout, and base recipient promises on observed completion behavior in your own process.

Keep release policy above speed policy. Speed rules should never override a review hold. If controls place a payout in review, move recipient-facing status to an explicit review state and require a documented release decision before any rail instruction is sent. Rail selection should follow release approval, not replace it.

Related: What Is Payment Orchestration? How Platforms Route Transactions Across Multiple PSPs.

Step 5 build reconciliation and month-end controls from day one#

Build reconciliation controls at launch, not at month-end. Split payout flows can look fine in product and still fail in finance if you cannot reliably match intent, execution, and ledger outcomes across your records.

Create a complete audit chain for each payout. Treat reconciliation as a control that catches discrepancies before they reach financial statements. For each payout, make sure operations and finance can trace key records (for example intent, provider execution, payout status, and ledger posting) without manual stitching.

Do not rely on amount-and-date matching alone. That breaks quickly with PSP bundles, foreign currency, bank fees, and partial payments. Use configurable matching rules with stable references so edge cases are less likely to be missed.

Run exception handling on a consistent rhythm. Set a repeatable exception-review process for active payout operations. Prioritize buckets such as unmatched events, failed disbursements, and pending items that need review.

Route these by required action rather than into one generic queue. Unmatched events often point to mapping or reference gaps, while failed disbursements need a clear resolution path. Track aging, not just queue size, and keep cleared versus pending cash visibility explicit throughout the cycle.

Define finance handoff artifacts upfront. Define a small, consistent handoff set so finance can trace reported amounts back to source records. A practical set can include:

| Artifact | What it should show | Why it matters |

|---|---|---|

| Reconciliation register | Internal reference, provider reference, amount, currency, status, posting link | Supports traceability across systems |

| Exception log | Unmatched or failed items, owner, status, aging | Makes exception handling auditable |

| Cash status view | Cleared versus pending cash by account and period | Improves close visibility and bank-to-ledger checks |

Pause scaling if manual fixes become normal. If manual adjustments become routine during close, consider pausing further payout scaling until split logic or event mapping is fixed. Repeated manual journals usually indicate a control-path problem, not a sustainable operating model.

Track close-quality metrics alongside payout speed, including exception aging, manual journal volume, and cleared versus pending cash gaps. If control health degrades as volume grows, fix the evidence trail before expanding further.

Common mistakes and how to recover without a full rewrite#

Do not jump straight to a rebuild when launch quality drops. Many recoveries can come from tightening scope, adding missing controls, and validating edge behavior before reopening traffic.

Define approval boundaries clearly, test real provider behavior, and expect friction when controls are weak.

Step 1. Restate the scope around recipient allocation#

A practical first recovery move is to separate payer-method handling from recipient allocation. Freeze rule changes, rewrite scope as a recipient-allocation problem, and document one release-approval rule.

A grounded parallel is setting a threshold policy up front, such as 2 out of 3 or 3 out of 5. Your checkpoint is simple: one sample transaction should produce one unambiguous intended outcome. If two teams derive different recipient results from the same case, the rules are still unclear.

Step 2. Make duplicate protection a go-live gate#

Treat duplicate protection as mandatory before reopening traffic. The sources do not specify payout API idempotency requirements, but they do show the cost of single-point failure and the value of explicit safeguards in distributed signing operations.

Run deliberate resend and retry tests, and confirm one business outcome per intended action. If duplicate execution is still possible, the failure mode is still open.

Step 3. Validate provider behavior with live edge cases#

Provider due diligence should focus on edge behavior, not demos. Grounded evidence supports that protocol and implementation choices affect real operating performance.

For split payouts, reversal semantics, transfer statuses, and limits are unknown from these sources, so validate them directly with live test cases. Ask for proof, run small-volume scenarios, and retain logs or screenshots as evidence.

Step 4. Add manual release controls until compliance is real#

If compliance controls are incomplete, add temporary manual approvals before release. The sources do not define exact non-crypto KYC and AML gates, but they do support a control-versus-convenience tradeoff.

Extra steps are a valid recovery cost when release controls are not yet reliable. Reopening without a clear release gate is the higher-risk path.

Make your first launch boring and traceable#

Your first launch should prove the flow is traceable under stress, not just on the happy path. If your team cannot explain one test transaction from split decision to payout outcome and compliance gate, pause launch.

Step 1. Freeze the split choice and fallback. Document the split model, fallback model, and who can approve exceptions. Include a few sample orders with expected recipient shares and the owner who signs off on rule changes.

In on-chain payment splitting, the logic is an explicit artifact: a release or split function applies stored percentages or weighted rules. A fast check is to hand the spec to someone outside the build team and ask them to predict outcomes for the same samples. If results vary, the implementation will drift.

Step 2. Validate flow behavior with your own evidence. Treat docs and demos as a starting point, not acceptance proof. Run your own test flows for core allocation and state changes, then save request IDs, payloads, screenshots, and notes in a shared evidence pack.

Use observed behavior as the release standard. If a status appears final and later changes in testing, hold launch until product, ops, and finance align on what that state means in your process.

Step 3. Make risk tradeoffs explicit before launch. Document the tradeoffs you are accepting across throughput, privacy, and key-management responsibilities. For automated split logic, require a secure development lifecycle so release does not depend on assumptions about exploit resistance.

Your pass condition is one business outcome with a clean audit trail. Save event IDs, internal transaction IDs, and resulting state changes so engineering and finance can review the same evidence.

Step 4. Enforce compliance before payout release. Keep compliance in launch scope. If your MVP does not handle KYC and basic AML, you have not validated the hardest operational path. Even in an 8-12 week MVP window, scope should still cover the compliance pipeline end to end.

Set the gate at payout release. Verify that an ineligible recipient cannot move from payable to released, and that ops can see the hold reason. If your program also requires KYB or VAT checks, add them explicitly after confirming requirements.

Step 5. Reconcile end to end and publish the incident path. Before go-live, reconcile a small set of production-like transactions through your internal records: transaction intent, split rule applied, provider reference, payout result, and internal entries. If reconciliation needs spreadsheet stitching or tribal knowledge, fix that first.

Then publish a short incident path for payout failures: owner, escalation trigger, and customer messaging for sent, delayed, and failed states. Do not promise timing you have not observed in real tests.

When your split logic and controls are finalized, pressure-test execution against a compliance-gated payouts workflow. ---

Frequently Asked Questions

What is multi-party payment splitting in a platform context?

In a platform context, it usually means one customer payment being allocated across multiple recipients tied to the same purchase. The term can also mean splitting a transaction across multiple payment methods, so teams should define which meaning they are using before implementation starts.

How is splitting one transaction to multiple recipients different from splitting across payment methods?

They are different workflows and can have different failure points. Splitting across payment methods is about how the customer funds checkout, while splitting across recipients is about how one payment is allocated among multiple parties. Treating them as the same problem can create allocation and reconciliation confusion.

Can one payment be split automatically when recipient shares change after checkout?

Automated multi-party settlement exists, but the provided material does not support a universal rule for post-checkout share changes. Provider behavior differs, including real-time versus scheduled settlement. If shares may change after checkout, confirm exact behavior with live provider tests.

Who holds funds before payouts are released in a marketplace flow?

The provided material does not establish a universal legal or operational holder of funds before release. Your operating model should still define who collects funds, who holds them, and who triggers payouts. If that is unclear internally, resolve it before launch.

What happens if one recipient payout fails after others have already settled?

The provided material does not define a standard cross-provider outcome for partial payout failures. Treat this as provider-specific until tested. Ask for documented failure, retry, and reversal behavior, then validate it in sandbox or live test evidence.

How should marketplaces calculate commissions and fees when reversals happen?

There is no supported universal formula in the provided material. Keep fee and commission sequencing explicit across the full flow from checkout to payout, including reversal paths. Validate your logic with sample reversal scenarios and matching ledger outputs before scaling.

What should we ask a provider before committing to a split-payments integration?

Ask for proof on recipient onboarding requirements, payout timing, and partial-failure and reversal behavior. Also confirm whether settlement is real-time or scheduled, since both patterns exist. Your checkpoint is a traceable test flow from checkout through payout.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bis.org/cpmi/publ/d213.pdftrusted

- federalreserve.gov/boarddocs/supmanual/cch/cch.pdftrusted

- files.consumerfinance.gov/f/documents/cfpb_personal-financial-data-rig...trusted

- hbs.edu/ris/Publication%20Files/Du_Huang_Scharfstein...trusted

- irs.gov/individuals/international-taxpayers/foreign-...trusted

- irs.gov/individuals/international-taxpayers/figuring...trusted

- pmc.ncbi.nlm.nih.gov/articles/PMC9901816trusted

- pmc.ncbi.nlm.nih.gov/articles/PMC8189446trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: