Quick Answer

Choose the operating model by failure cost: centralized treasury is usually the first move when close reliability and exception handling matter most. Run one strict sequence for each transfer: approve request, lock FX quote, execute, post both-entity journals, then release payout batches. Keep replay safety with idempotency keys and block stale quote conversions. If payout timing in a stable corridor is the top risk, local pre-funding can be better, but only with explicit true-up documentation and entity-level balance controls.

Intercompany transfers break when finance and engineering optimize different things#

Intercompany transfers fail even when the money can move, because finance and engineering may be optimizing for different outcomes. If you run a multi-entity platform, you usually feel that split before a transfer fails in production or your close team sees it in reconciliation. Finance needs controlled, arm's length treatment that stands up in tax and consolidation. Engineering needs a transfer flow that stays reliable across cross-border rails, and we need both views aligned before you release funds.

- Scope that matters

This piece is about platform teams moving funds between legal entities under common control, where each transfer has to work as both money movement and an intercompany transaction. In U.S. rules, Section 482 applies when entities are "owned or controlled directly or indirectly by the same interests," and related regulations require an arm's length amount of compensation for value provided between controlled taxpayers. Key checkpoint: before you send a payment, confirm the source entity, destination entity, jurisdiction pair, currency, business purpose, and pricing basis.

- The constraint stack is real

Cross-border internal transfers sit inside transfer-pricing rules, tax regimes, and payment-rail behavior at the same time. OECD transfer pricing guidance is the international reference point for related-party cross-border pricing, and it was updated on 19 February 2024. On the payments side, BIS notes cross-border payments are generally slower, more expensive, and more opaque than domestic payments, and a single transaction can pass through several intermediary correspondent banks. Key checkpoint: do not design as if one instruction always produces one final settlement event. Expect multiple states over time, and preserve provider references through the ledger and reconciliation process.

- Success is approval-to-close, not send-to-settle

A transfer is only complete when it can be approved, executed, posted, matched, and eliminated correctly in consolidation. In multi-entity accounting, intragroup balances, transactions, income, expenses, and cash flows are eliminated in full. Key checkpoint: keep an evidence trail with approval, transfer intent, entity pair, amount and currency, provider reference, and journal entries before elimination. One common breakdown is that cash moves, but the intercompany position, pricing rationale, or elimination entries do not reconcile.

That is the lens for the rest of this piece. If you are mapping this for your team, we recommend treating your tax evidence, your rail behavior, and your close controls as one shared design problem. For intercompany payments across multi-entity platforms and cross-border internal transfers, you need an operating model that can withstand Section 482 scrutiny and jurisdiction differences highlighted by regulators. It also has to handle cross-border rails that do not always resolve in a neat, synchronous sequence.

Selection criteria that actually predict success#

Use a scorecard, not a demo impression. For cross-border intercompany transfers, these five criteria usually tell you more about production readiness than headline pricing or a smooth sandbox.

| Criterion | Risk signal | Key check |

|---|---|---|

| Compliance burden | The model repeatedly depends on manual tax or transfer-pricing explanation at close | Ask for the evidence pack up front: entity pair, business purpose, pricing basis, and jurisdiction mapping |

| Operational control | Traceability should be visible before launch, with production-grade KYC/AML controls and user-level auditability | Confirm audit history is retained and exportable; QuickBooks Online audit-log events are available for two years |

| Speed to launch | Sandbox wins are early signals, not launch proof | Require one end-to-end pilot from approval through posted journal and close review |

| Reconciliation complexity | Data is inconsistent even if payment execution succeeds | Require a stable request ID, provider reference, entity pair, currency, and ledger posting link on every transfer |

| Failure recovery time | Measure how quickly you can prove state and correct the books | Weight auditability and evidence packs heavily; evaluate FX as total cost, including both fees and the FX component |

- Compliance burden

Score this early. Related-party transfers still matter even when no explicit price is charged, and cross-border related-party pricing sits in an arm's-length framework. If a model repeatedly depends on manual tax or transfer-pricing explanation at close, treat that as ongoing operating risk. Key differentiator: ask for the evidence pack up front: entity pair, business purpose, pricing basis, and jurisdiction mapping.

- Operational control

Traceability should be visible before launch, not patched in later. AML/CFT expectations are set at an international standard level, so production-grade KYC/AML controls and user-level auditability should be clear before you go live. Key differentiator: confirm that audit history is retained and exportable. QuickBooks Online audit-log events are available for two years, which is a useful traceability benchmark.

- Speed to launch

A smooth sandbox is an early signal, not launch proof. Test environments simulate flows; they do not move real money, so readiness still depends on live-state handling, compliance checkpoints, and close outputs into your accounting system. Key differentiator: require one end-to-end pilot from approval through posted journal and close review.

- Reconciliation complexity

Cross-border flows create reconciliation friction when data is inconsistent, even if payment execution succeeds. ISO 20022 harmonization work points to concrete data requirements, so clean reference data is a core control, not admin overhead. Key differentiator: require a stable request ID, provider reference, entity pair, currency, and ledger posting link on every transfer.

- Failure recovery time

Measure recovery by how quickly you can prove state and correct the books, not just by whether funds moved. Fragmented systems and manual entries make close more cumbersome, so recovery design should be part of model selection. Key differentiator: when close reliability is the main pain, weight auditability and evidence packs heavily. FX should still be evaluated as total cost, including both fees and the FX component.

For teams tightening compliance controls around cross-border transfers, our guide to PEP screening for cross-border platforms and monitoring obligations covers the monitoring side in more detail.

The best operating models for multi-entity platforms#

There is no universal best model. The right choice depends on which failure hurts most: close breaks, local settlement misses, legal-entity confusion, or rollout risk.

| Model | Best when | Key consideration |

|---|---|---|

| Centralized treasury hub | You need unified control and clear policy ownership | Accounting load rises because intragroup balances and transactions must be eliminated in full at consolidation |

| Local entity pre-funding | Local payout certainty matters more than peak capital efficiency | Trapped liquidity and heavier transfer-pricing support; documentation should cover transaction-level local-file support |

| Hybrid corridor routing | Corridor behavior is mixed | Keep suitable euro routes on SEPA Credit Transfer and route selected other corridors through centralized SWIFT controls |

| MoR-led collection with entity redistribution | A marketplace model needs clear legal responsibility at collection | Collection, contracts, tax treatment, and redistribution journals should map to the same legal reality |

| Provider-partitioned model | One provider is not a clean fit across all corridors | Operations fragment unless outputs are normalized into one ledger view |

- Centralized treasury hub

Best when you need unified control and clear policy ownership. This usually follows an in-house-bank structure, with one entity managing group treasury and funding regional activity. The tradeoff is accounting load. Intragroup balances and transactions must be eliminated in full at consolidation, so intercompany journal pressure rises. Before you go live, require a complete transfer evidence pack, including entity pair, business purpose, provider reference, and ledger posting link, so cash movement and eliminations stay aligned at close.

- Local entity pre-funding

Best when local payout certainty matters more than peak capital efficiency. Local entities hold balances and run local disbursements, then rebalance with periodic intercompany transfers. The tradeoff is trapped liquidity and heavier transfer-pricing support. Cross-border related-party funding still needs an arm's-length basis, and your documentation should cover transaction-level local-file support, not just policy-level intent.

- Hybrid corridor routing

Best when corridor behavior is mixed. Keep suitable euro routes on SEPA Credit Transfer and consider routing selected other corridors through centralized SWIFT controls. This works because SEPA euro-transfer rules are harmonized across participating countries, with 41 countries per ECB status dated 22 May 2025. SWIFT timing can vary by route even when median speed is strong, with median under 2 hours, fastest under 5 minutes, and slowest over 2 days. Make routing decisions reproducible by storing corridor, entity, currency, amount class, reason code, and idempotency token.

- MoR-led collection with entity redistribution

Best when a marketplace model needs clear legal responsibility at collection. The Merchant of Record is the entity legally responsible for processing customer payments, so this is a legal-entity design choice first. This model can improve revenue-to-payout traceability if collection, contracts, tax treatment, and redistribution journals all map to the same legal reality. If those mappings diverge, legal, tax, and card-network risk all rise.

- Provider-partitioned model

Best for staged rollout when one provider is not a clean fit across all corridors. Teams often split by region or corridor type, for example, SEPA-focused flows versus longer-tail SWIFT corridors. The tradeoff is fragmented operations unless outputs are normalized into one ledger view. SWIFT's broad network coverage helps with reach, but it does not solve internal visibility by itself, so require the same minimum evidence fields from every provider before you expand.

If you need a more operational walkthrough of sending funds across borders, see International EFT payments for platforms.

Centralized treasury wins when control and traceability matter most#

If reconciliation delays and exception investigations are your highest-cost failures, start with a centralized treasury model. It is often the stronger first move when you need one control point across approvals, transfer status, FX handling, and intercompany ledger outcomes.

- Choose centralized when investigation time is the real cost

Centralizing treasury and cash functions can improve control and efficiency, especially when approvals and settlement would otherwise pass through multiple local teams. If you choose this model, we recommend giving one team authority to trace the transfer from approval through posting before your payout release moves forward and before your month-end close depends on manual reconstruction. Manual communication is a known source of intercompany settlement delay. The practical advantage is shared visibility: one team can trace approval, provider reference, FX state, and journal outcome without rebuilding the timeline across entities.

- Use one operating sequence for every funded transfer

Consistency matters more than elegance here. Run the same order every time: approve the intercompany request, lock the FX quote, execute the transfer, post journals, then release downstream payout batches. This is an operating control, not a legal requirement. Keep the release gate strict. Do not move payout batches from ready to sent until the provider reference is recorded and both-entity journals are posted.

- Design for stale FX quotes and safe replay before go-live

A common break point is quote expiry before conversion. If you use an Extended Rate Quote, store its expiry and block conversion attempts after that time. Then replay with idempotency keys so retries return the original result instead of creating duplicate transfers, especially after connection errors.

- Separate duplicate controls for funding vs payouts

Do not assume retry behavior is identical across providers. Some transfer APIs support idempotent replay, while some payout APIs enforce duplicate guards with batch identifiers. For example, some payout flows reject a reused sender_batch_id if it was used in the last 30 days. If funding and payout release are connected, implement both controls explicitly.

- Build an evidence pack finance can close from

Your centralized model only pays off if finance can close from the same record engineering uses to run it. For each transfer, keep transfer intent, policy approval, provider reference, journal entries, and an export used in your close workflow (for example, a QuickBooks Desktop report exported to Excel). In practice, capture request ID, entity pair, business purpose, currency pair, quote timestamp, settlement confirmation, and posting IDs for each side of the intercompany entry. If available, store payout tracking references like payout_batch_id or a Payout Trace ID to speed exception handling.

QuickBooks audit history should confirm your controls, not reconstruct missing steps. It records who changed what and when, and QuickBooks Desktop reports can be exported to Excel for close workflows. If month-end still requires forensic work - for example, to verify approval timing, FX lock timing, or post-payout journal edits - your evidence chain is still too thin for centralized operations to deliver full value.

Local entity funding wins when corridor predictability is high#

Local pre-funding can be a strong fit when payout timing is strict and corridor behavior is stable. Ask a simple question: is the cost of a missed local payout likely to outweigh the cost of holding extra liquidity? If it is, fund the local entity first and rebalance later through cross-border intercompany transfers.

- Pre-fund when payout timing is non-negotiable

Cross-border payments still face persistent frictions around cost, speed, access, and transparency. A pre-funding model is an established cross-border mechanism, and its advantage is simple: funds are already local before payout execution. If your corridor is predictable, this reduces dependence on urgent cross-border movement on payout day.

- Run local funding with explicit balance controls

Set entity- and currency-level minimum and target balances, and require approvals for top-ups and true-ups. These are operating controls, not universal legal requirements, but they help reduce both payout misses and unnecessary trapped cash. That matters because funding liquidity in cross-border structures can be materially costly, especially in tighter conditions.

- Document true-ups as intercompany transactions, not treasury housekeeping

Rebalancing between entities still needs a defensible transfer-pricing rationale. OECD transfer pricing guidance is the global standard for related-party cross-border pricing, and U.S. Section 482 allows IRS adjustments for commonly controlled taxpayers. Your records should clearly capture business purpose, entity pair, pricing rationale, approvals, settlement reference, and accounting support for both sides.

- Treat tax-document consistency as a funding gate

Inconsistent W-8/W-9 and VAT validation processes create avoidable compliance drift across entities. Form W-8 BEN is provided when requested by the withholding agent or payer, and Form W-9 provides the correct TIN to a requester or payer. For EU entities, validate VAT numbers through VIES and retain dated evidence of the result, since VIES returns live national-database responses. Also account for the 01/01/2021 change where the prior VIES UK (GB) validation path ceased.

For a step-by-step walkthrough, see When Platforms Should Use Wires vs Local Rails for Cross-Border Payouts.

Hybrid routing is the practical middle path for scaling platforms#

When corridor behavior differs, a hybrid model keeps you from forcing one rail and one control pattern everywhere. Keep stable euro corridors local on SEPA, and route volatile corridors through centralized SWIFT controls.

- SEPA for stable euro corridors

Use SEPA Credit Transfer for repeatable euro movements where the entity pair, amount range, and payout timing are predictable. SCT uses the same euro transfer rules for domestic and cross-border use across 41 SEPA scheme countries and supports more than 29 billion transfers every year. The advantage here is consistency, not a blanket claim that SEPA is always faster or cheaper.

If France-to-Germany rebalancing looks the same each week, keep it local instead of pushing it into a centralized queue. Do not assume a stable SEPA corridor predicts behavior in non-euro routes or bank pairs outside SEPA.

- SWIFT for volatile or higher-touch corridors

Use centralized SWIFT handling for corridors that need tighter oversight, and treat SWIFT correctly as messaging infrastructure, not settlement infrastructure. A message being accepted is not the same as final customer credit. Reported timing data shows the gap: 90% of cross-border payments over SWIFT reached the destination bank within an hour, while 43% reached the end customer account within an hour.

If payout release depends on an intercompany transfer arriving first, do not release on a simple "sent" status. Release only after your provider confirms the transfer has moved beyond message dispatch.

- Code routing rules so decisions are repeatable

Hybrid routing works best when the rules are explicit and deterministic. In rule-based orchestration setups, evaluate rules in order, with the first match winning, and define them with clear transaction conditions. If you route by amount, include currency. That turns routing from tribal knowledge into auditable system behavior.

In the ops UI, show the matched rule, selected rail, rule version, entity pair, amount class, currency, and any override. Watch for overlapping rules and silent manual overrides.

- Make every transfer replay-safe and explainable

Attach two controls at creation time: a deterministic reason code and a replay-safe idempotency key. Use your internal reason code to explain route choice, and use rail-specific codes for rail exceptions. For SCT exceptions, apply the scheme's specific R-transaction or inquiry reason codes under the 2025 rulebook in force from 5 October 2025.

Verification checkpoint: from one request ID, you should be able to retrieve the route decision, reason code, provider reference, and resulting ledger post. For a true retry, reuse the same idempotency key so the same prior result is returned, including server-error outcomes, instead of creating duplicate movement.

Related: Adaptive Payments for Platforms: How to Split a Single Transaction Across Multiple Payees.

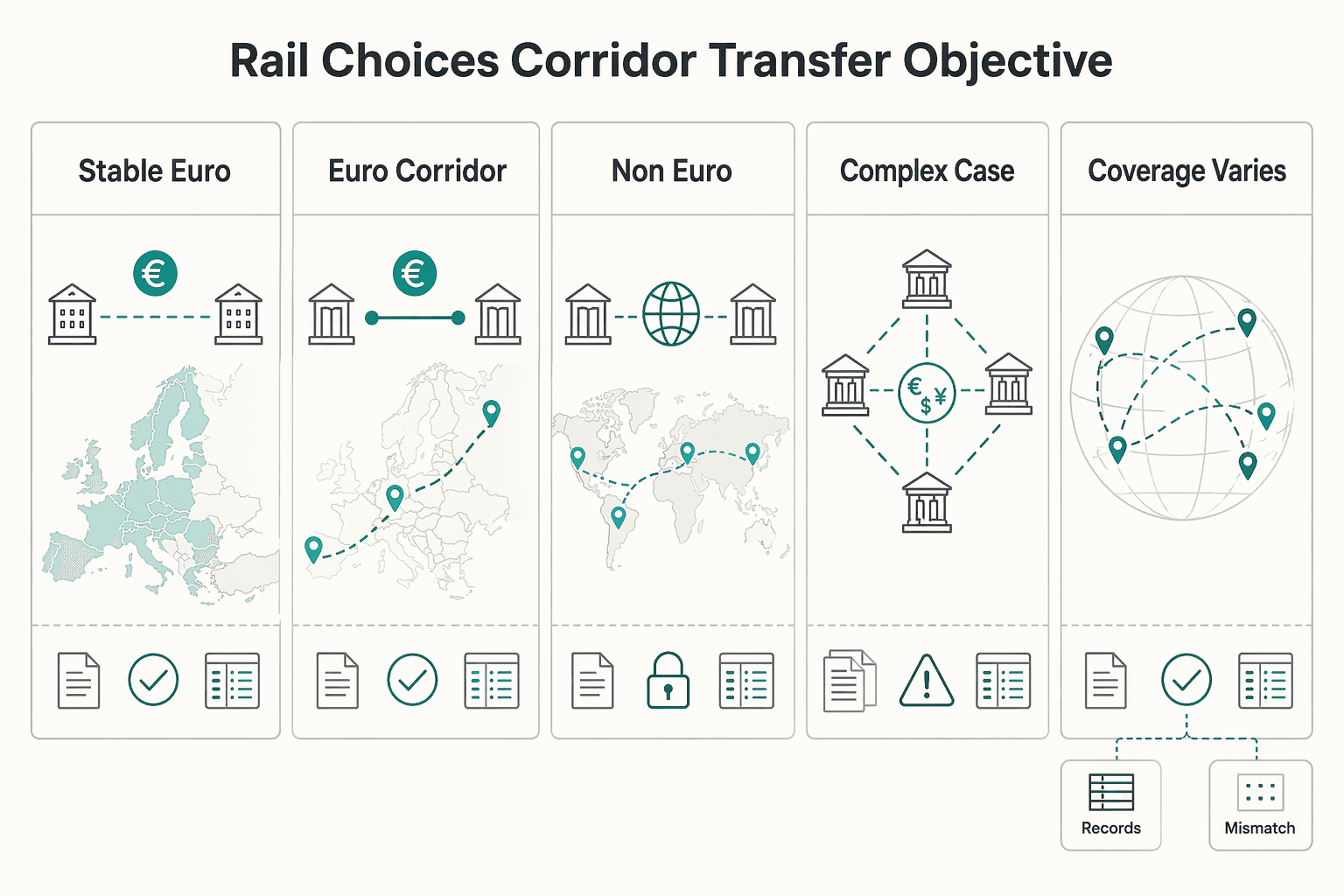

Rail and FX choices by corridor and transfer objective#

Choose rail and FX by transfer objective, not headline fee. For repeatable euro movements inside the 41 SEPA scheme countries, SEPA is usually the cleaner path. For broader geography or mixed-currency corridors, SWIFT-linked correspondent routes are often the operational default.

The tradeoff is not just price. Keep cost, speed, access, and transparency in view together. Correspondent banking remains central to cross-border coverage, but those frictions still show up in practice.

| Corridor type | Preferred rail | FX approach | Expected failure modes | Reconciliation burden |

|---|---|---|---|---|

| Stable euro corridor, liquidity balancing between entities | SEPA | No FX if both sides hold EUR; if conversion is needed, convert before transfer and send EUR end to end | PSP not formally participating in SCT, payment details issues, non-euro payment routed into a euro-only rail | Low when entity pair and amount band are consistent |

| Euro corridor, urgent payout funding where time to funds matters | SEPA (SCT Inst where enabled) | Keep funding in EUR where possible so release is not waiting on conversion | Assuming instant availability when SCT Inst is not enabled, treating "sent" as usable balance too early, institution or program support mismatch | Low to medium, depending on payout-release logic |

| Non-euro or non-SEPA corridor, urgent funding to keep payouts moving | SWIFT | Lock FX decision close to execution and store quote or rate reference with the transfer record | Slower funds availability, intermediary handling, and weak transparency if you only track dispatch | Medium to high |

| Mixed-currency month-end entity rebalancing with close-cycle deadlines | SWIFT | Prioritize auditable FX over lowest spread; store approval, rate source, value date, and resulting journals together | Timing mismatches across entities and incomplete FX audit trails | High |

| Coverage varies by market or program, even with broad provider reach | SWIFT | Treat FX setup as provider- and market-specific until confirmed for receiving institution and region | Assuming availability from generic coverage claims, then finding the receiving institution or program is not enabled | Medium to high |

| Corridor where a stablecoin-like option may exist only if separately enabled and approved | SWIFT as baseline | Use standard bank-rail FX unless the alternative path is explicitly enabled, legally cleared, and documented | Compliance gating not met, jurisdiction restrictions, missing authorization checks, added review from illicit-finance risk controls | High until fully approved and documented |

Before go-live, run these checks. For a neighboring cash-flow angle, see How Graphic Designers Protect Cross-Border Payments and Cash Flow.

- For euro liquidity balancing, verify the payment is in EUR and both PSPs formally participate in SCT.

- For urgent euro funding, verify SCT Inst is actually enabled for the relevant institutions and program if you are relying on near-immediate availability.

- For non-euro or mixed-currency corridors, optimize for a clean audit trail, not just the lowest conversion fee.

- For coverage, confirm receiving-institution and program availability before launch. If unconfirmed, keep fallback routing on SWIFT.

- For stablecoin-like alternatives, treat them as conditional rails requiring explicit enablement and compliance sign-off.

The minimum compliance and documentation pack before go-live#

Do not go live until your documentation can withstand tax and AML review. This is the minimum control pack that keeps routine internal transfers from turning into close-cycle exceptions.

| Control pack | Before launch, confirm | Key detail |

|---|---|---|

| Intercompany agreement and pricing rationale | A retrievable agreement reference, a retrievable pricing-method reference, and clear internal terms for transfer purpose, settlement currency, pricing logic, and true-up handling | Documentation must exist when the return is filed and should be produced within 30 days of request |

| Jurisdiction map for tax regimes | For each entity pair, record which country rules apply and which tax operations are triggered only in that lane | OECD Action 13 is organized around a master file, local file, and country-by-country reporting template |

| KYC, KYB, and AML release gates | KYB/CDD status for each legal entity, beneficial-owner identification and verification status, and a named owner for manual escalation | Identification happens at new account opening, subject to exclusions and exemptions |

| Tax forms and downstream reporting dependencies | VIES where relevant, plus W-8BEN or W-9 where they apply | GB VAT validation in VIES ceased on 01/01/2021; Form 1099-MISC examples include at least $10 in royalties and at least $600 in certain other categories; FBAR applies over $10,000 and is due April 15 with an automatic extension to October 15; Form 2555 lists a 2025 maximum exclusion of $130,000 |

1. Intercompany agreement and pricing rationale#

Start with an intercompany agreement that matches the transfer flow you are automating, then attach a transfer-pricing method note. The tax anchor is the arm's length principle for pricing between associated enterprises.

Before launch, confirm each live entity pair has:

- A retrievable agreement reference

- A retrievable pricing-method reference

- Clear internal terms for transfer purpose, settlement currency, pricing logic, and true-up handling

Timing matters. IRS guidance says transfer-pricing documentation must exist when the return is filed and should be produced within 30 days of request. Treat this as a pre-go-live control, not post-launch cleanup.

2. Jurisdiction map for tax regimes#

Build a corridor-by-corridor jurisdiction map before release. For each entity pair, record which country rules apply and which tax operations are triggered only in that lane. For larger multinational structures, OECD Action 13 documentation is organized around a master file, local file, and country-by-country reporting template.

Do not assume one tax treatment applies across all internal transfers just because product behavior looks similar. Some cross-border advisers describe documentation fragmentation, where groups lack one coherent framework that explains how the full model works.

3. KYC, KYB, and AML release gates#

If your operating workflow includes internal funding and downstream payout release, set operational gates so release does not happen before legal-entity checks are complete and escalation ownership is clear.

For covered U.S. institutions, CDD rules require written procedures to identify and verify beneficial owners of legal-entity customers. Those procedures must be included in the AML program, and identification happens at new account opening, subject to exclusions and exemptions.

Your control record should show:

- KYB/CDD status for each legal entity

- Beneficial-owner identification and verification status

- Named owner for manual escalation when review is pending

4. Tax forms and downstream reporting dependencies#

Document form and reporting dependencies only where they apply, and record them before the first transfer rather than during close.

- EU VAT checks: use VIES where relevant, noting the European Commission states GB VAT validation in that service ceased on

01/01/2021. - U.S. withholding/info forms: Form W-8BEN is provided by a foreign beneficial owner to a withholding agent or payer when requested; Form W-9 provides a correct TIN to a requester filing an information return.

- Form 1099-MISC: applies to specified payment categories, including examples of at least

$10in royalties and at least$600in certain other categories. - FBAR (FinCEN Form 114): annual filing when aggregate foreign account value exceeds

$10,000during the calendar year; dueApril 15with an automatic extension toOctober 15. - FEIE workflow: Form 2555 is used when a qualifying person computes the exclusion; IRS instructions list a

2025maximum exclusion of$130,000.

Build controls so retries are safe and audits are easy#

Operational failures often show up as duplicate execution and weak evidence trails. That makes retry safety and traceability practical release blockers for payment transfers.

1. Idempotency first#

Duplicate requests should resolve to the same transfer state, not new money movement. Require an idempotency key on transfer initiation calls. For the same business intent, retries should reuse that exact key so a repeated request can return the same prior result, including errors.

Do not stop at "header present." Store the key with the transfer intent and validate core fields, for example, entity pair, amount, currency, and purpose, on retry. Also document provider-specific behavior, because key limits and retention windows vary; for example, one common API supports keys up to 255 characters and may prune them after 24 hours.

2. One traceability chain across the full payment journey#

You need one continuous chain from request to reconciliation export: request ID -> provider reference -> ledger posting -> payout or settlement report. Without that chain, close can turn into manual matching across systems.

Persist the core links together in one record: internal request ID, provider transfer reference, webhook event ID, journal or posting ID, and reconciliation export row key. This makes "what happened?" answerable quickly during audits and month-end reviews.

3. Let the ledger win over balance views#

Use the General Ledger as the accounting source of truth, and treat wallet or balance views as derived operational projections. Projection reads can lag recent writes, so balance screens can be stale right after execution.

Apply a clear sequence for finance finality: authorize by policy, execute with the provider, then post and reconcile to the ledger. This is especially important with Virtual Accounts, which are linked representations to a master account rather than direct fund-holding accounts.

4. Webhooks need duplicate handling and late-outcome rules#

Assume asynchronous outcomes and build for delay, retries, and reordering. Final status may arrive long after the initial request response.

Webhook consumers should record receipt, detect already-processed events, and ignore duplicates while still returning success to stop further retries. Keep an explicit replay procedure for undelivered events and late arrivals, and if an event conflicts with a more advanced ledger state, route it for review instead of overwriting posted records.

Failure scenarios and what to do in the first hour#

In the first hour, contain downstream impact, investigate from the provider reference outward, and avoid workarounds that assume an uncertain transfer is settled.

1. Transfer delayed in transit#

Treat delay as a status problem first, not an automatic retry signal. Consider pausing dependent payouts or internal releases, publish an internal status update, and escalate by corridor and rail.

Use the external status artifact first. On ISO 20022 flows, check pacs.002 (Payment Status Report) before relying only on balance views. In SEPA corridors, use SCT R-transaction reason-code handling to triage exceptions consistently. If you cannot confirm rejection or return, avoid re-initiating and continue with the original request ID and provider reference.

2. Transfer returned or unmatched#

Treat returned or unmatched funds as an accounting exception immediately. Flag the amount as pending resolution operationally, investigate with the provider reference and transaction-identifying details, and post correcting entries in multi-entity accounting.

On ISO 20022-supported rails, pacs.004 (Payment Return) is direct evidence that funds were returned from a prior credit transfer. In SEPA, use defined SCT R-transaction reason codes to identify why an item rejected, returned, or was recalled. Also account for rail behavior: some transfers are not reversible after processing, and Fedwire is final and irrevocable once processed.

3. Compliance hold triggered#

If a compliance hold is triggered, treat it as a stop condition under your AML/KYC process until review clears it. Do not bypass the hold with manual overrides.

Start with the customer or counterparty file used for CIP (risk-based identity verification). Preserve a complete audit trail: transfer intent, approvals, screening outputs, provider notifications, timestamps, and references. In a U.S. banking context, SAR rules include a $5,000 threshold for certain suspicious transactions. They also include a 30 calendar day baseline filing deadline after detection, and a 60 calendar day outer limit when suspect identification is delayed.

4. Reconciliation mismatch at close#

When provider outcome and journals do not match, consider pausing close sign-off until parity is restored. This is an operating control that helps prevent fragmented-system and manual-entry errors from carrying into close.

Run a three-way check: internal request ID, provider transfer reference, and posted journal entry. If one leg is missing, close evidence is incomplete. The close pack should include provider status or return evidence, any ledger correction, and the reconciliation export row tying both together. Where U.S. sanctions recordkeeping applies, covered records may need to remain available for 10 years.

A 30-day implementation sequence finance and engineering can actually execute#

A four-week sequence can be enough to expose the real issues. Decide the model and corridor scope first, harden policy and retry behavior second, run narrow live pilots third, and expand only after close and compliance sign-off in week four.

Week 1 decide the model and corridor inventory#

Week 1 is for decisions, not code. Pick the first live model, centralized, local pre-funding, or hybrid, and approve one shared scorecard across finance and engineering.

Build a concrete corridor inventory for every in-scope flow: origin entity, destination entity, funding purpose, currency pair, expected rail, approval owner, and accounting destination. If a route is eligible for SEPA Credit Transfer, keep the boundary explicit: SCT is for euro payments between accounts in SEPA and spans 41 SEPA scheme countries. Routes outside that footprint should be marked for non-SEPA routing, with SWIFT as a common candidate in correspondent-banking flows.

Define measurable service indicators per corridor, with safety and efficiency both covered, for example, approval time, execution handoff time, exception response time, and reconciliation completion.

Week 2 harden policy gates, retries, and accounting outputs#

Week 2 is where you remove duplicate-payment and invisible-hold risk. Configure policy gates for AML/KYC review, approval thresholds, release ownership, and evidence retention before any live pilot.

On the API layer, make transfer creation replay-safe with Idempotency-Key handling for retryable POST behavior. Validate by replaying the same request with the same key and confirming one transfer state and reference, not two movements of funds.

Implement webhooks in the same week so asynchronous outcomes update correctly, including events that can arrive late or out of sequence. Validate that request ID, provider reference, and journal outcome still reconcile under event reordering.

Map accounting outputs now, including QuickBooks dependencies. Confirm your exact QuickBooks edition before committing to journal-entry import, because published QuickBooks guidance is inconsistent across contexts and regions.

Week 3 pilot real corridors and force the ugly edge cases#

Week 3 should be live but narrow. Pilot one or two corridors with enough activity to expose real behavior while limiting close-period blast radius.

Keep rail logic explicit: use SEPA only where euro and SEPA-account requirements are met; use SWIFT where correspondent-banking coverage is needed. Treat FX quote-expiry handling as a control, not just a pricing detail. Provider examples include 1-hour or 24-hour quote extensions, and expired quotes can fail with a 400 status code.

Force stale-quote retry tests on purpose, verify failure behavior, then confirm recovery does not create duplicate transfers. For each pilot transfer, retain the rail-selection reason, original request ID, approval record, provider reference, and resulting journal entry.

Week 4 simulate close, sign compliance artifacts, then expand#

Week 4 determines production readiness. Run a close simulation using the same month-end evidence pack: transfer intent, approvals, screening outputs, provider status or return evidence, journal entries, and reconciliation rows that tie them together.

Complete compliance sign-off in the same week. Align transfer-pricing documentation to OECD BEPS Action 13's three-tiered approach. Also verify tax-form handling by purpose, for example, Form W-9 provides a correct TIN for payer information-return workflows.

Expand corridor coverage only after the close simulation passes and the document pack is complete. If you cannot quickly produce request ID, provider reference, ledger posting, and transfer-pricing or tax support for pilot corridors, keep scope fixed until you can.

If you are turning this 30-day plan into build tickets, use the Gruv docs to map APIs, webhooks, and payout status handling to your rollout.

Choose the model that reduces failures you can measure#

Once your minimum controls are in place, evaluate failure recovery and close reliability alongside headline fees. A lower-cost route can still become expensive if it creates unreconciled balances, legal-entity cash-flow delays, or quarterly tax-provision timing issues.

- Score the model on recoverability, not just price

In cross-border payments, performance is multi-objective: cost, speed, transparency, and access. Judge each model by whether you can trace transfers end to end, retry safely, and close without manual reconstruction. If your team cannot explain a transfer from request through settlement output, any fee advantage may be a false economy.

- Prove corridor behavior end to end before expanding

Corridor behavior is not uniform: the World Bank tracks 367 country corridors across 48 sending countries and 105 receiving countries. Validate one meaningful corridor first, then prove compliance gating, settlement evidence, and accounting outputs before widening scope. Include retry controls in that proof: with idempotent requests, the same key should return the same result on retry, including prior errors. Then confirm finance can use payout reconciliation exports, including CSV outputs, to reconcile payout transactions in close workflows.

- Validate exact corridor, entity, and reporting fit before rollout

Coverage pages are a starting point, not a launch decision. Support changes over time, and capabilities can be region- or configuration-dependent, including cases where multicurrency setups support up to 18 currencies. For each entity and corridor, confirm destination-pair support, policy handling for incomplete payment data (execute, reject, or suspend), and close-ready reporting outputs. If any answer is vague, pause expansion and run a corridor-specific walkthrough for your actual entity setup.

Frequently Asked Questions

What counts as an intercompany cross-border internal transfer in a multi-entity platform?

It is an intercompany transfer when funds move between legal entities owned or controlled directly or indirectly by the same interests, rather than to an external party. In U.S. tax terms, Section 482 and Treasury Regulation 1.1502-13 frame these as controlled or intercompany transactions within a group, including related income, gain, deduction, and loss items. If the payment is to a supplier, contractor, or customer, it is typically treated as an external flow instead.

How is an intercompany transfer different from a vendor payout or a customer refund?

The core difference is internal versus external counterparty. In consolidated reporting, intra-entity balances and transactions are eliminated, while transactions with outside parties are what remain presented. Customer refunds and chargebacks follow a separate path, beginning with a customer contacting their bank and potentially involving a temporary refund during investigation.

Should we centralize treasury first or pre-fund local entities first?

The cited sources do not establish a universal winner between centralization and local pre-funding. Choose based on your operating risk and control requirements, and document routing and approval rules before expanding either model.

What is the minimum control set before sending internal cross-border transfers?

There is no single global checklist that fits every jurisdiction, but you should document core controls and traceability fields for each movement before launch. Where customer due diligence rules apply, 31 CFR 1010.230 requires identifying and verifying beneficial owners of legal entity customers. For SWIFT corridors, keep the UETR in your reconciliation trail so investigations and matching are traceable.

How should we handle delayed, returned, or unmatched internal transfers operationally?

When a transfer is delayed, returned, or unmatched, investigate using the full reference chain rather than amount-only matching. For SWIFT, trace with UETR. For SEPA Credit Transfer exceptions, retain provider reason codes because some SCT transactions require exception handling. A conservative control is to hold final disposition until provider references, bank evidence, and intercompany journal lines align.

Which documents should finance prepare for transfer-pricing and tax reviews before go-live?

Align transfer-pricing documentation to the arm’s-length standard under Section 1.482-1. Where relevant, maintain Master File and Local File records, which HMRC identifies as specified transfer-pricing records, with UK scope references tied to groups at €750 million or more in global consolidated revenue for periods beginning on or after 1 April 2023. Add tax forms only where they apply, such as Form W-9 for correct TIN collection, Form W-8BEN-E for foreign entity status, and VIES checks for EU VAT numbers.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- ecb.europa.eu/paym/retail/instant_payments/html/index.en.htmltrusted

- ecfr.gov/current/title-26/chapter-I/subchapter-A/part...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- federalreserve.gov/paymentsystems/over_pssystems.htmtrusted

- federalreserve.gov/paymentsystems/fedfunds_about.htmtrusted

- irs.gov/businesses/international-businesses/transfer...trusted

- irs.gov/businesses/international-businesses/transfer...trusted

- gov.uk/hmrc-internal-manuals/international-manual/i...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

How Platforms Choose International EFT Payments Across Borders

---

Adaptive Payments for Platforms: How to Split a Single Transaction Across Multiple Payees

The first decision is easy to state and easy to get wrong. Does one buyer checkout need to fund multiple recipients under explicit rules for platform fees, partner payouts, and failed or blocked money movement? If you cannot explain that money path on one page, pause before you code.

Tariff Pressure and Cross-Border Payment Choices for Platforms

If you are making expansion calls under tariff pressure, treat this as an operations decision first, not a market-opportunity story. Tariffs and cross-border payments can shift margin assumptions, support load, and launch risk on short timelines, so core planning should happen before onboarding, payouts, and reconciliation go live.