Quick Answer

To maximize NetSuite as a payment platform, start with core ERP finance and Accounts Payable, define ownership and posting rules, and add automation and integrations only after reconciliation is stable. Let NetSuite own accounting truth and AP controls, use an external orchestration layer when routing is the harder problem, and expand to OneWorld or analytics only when business scope and transaction definitions are ready.

Why most NetSuite payment projects stall before ROI#

NetSuite payment projects often stall when teams try to enable too much at once. The practical path is to sequence modules and automations so you reduce rework instead of creating it. NetSuite is built for incremental expansion, so it is usually safer to lock accounting controls first, then layer on payment automation and integrations.

Step 1. Start where accounting truth is created#

Start with the core finance objects and Accounts Payable. That is where key payment records are created. NetSuite's core ERP already includes finance and accounting, and you can add modules as needs evolve. For payment platforms, that usually means stabilizing AP before broader automation. NetSuite AP automates invoice review, approval, and payment, and it supports automated journal entries.

Use a simple checkpoint: trace one representative invoice or payout-related transaction in the General Ledger report. If engineering and finance cannot quickly agree on how it posts, your rollout order is still too aggressive.

Step 2. Align shipping speed with finance controls early#

Fast delivery still matters, but payment architecture has to work in operations and in the ledger. NetSuite supports control requirements with configurable financial reporting, GL-account-level report configuration, and transaction-level history through the Transaction Audit Trail.

Do not treat a payment flow as done unless the same event is clear in ledger outcomes and financial reporting without manual repair. Intelligent Payment Automation features such as approval routing, status tracking, and automated GL entries are most useful after you define which status changes affect accounting.

Step 3. Set architecture scope before buy/build decisions#

Start with scope and ownership before you compare products. Not every feature is available in every account. Oracle notes that some features require an extra purchase, and availability can vary by account and contract.

Treat product choice as a lifecycle decision, not just an implementation task. Oracle also states support is targeted to end for the Payment Automation SuiteApp on December 31, 2026, and notes a March 4, 2026 cutoff for certain HSBC-linked customers to continue using it until support ends. Before you proceed, assign clear owners for approval policy, payment status, and final General Ledger posting in NetSuite.

Related guide: Gateway Routing for Platforms: How to Use Multiple Payment Gateways to Maximize Approval Rates.

Choose what NetSuite owns and what your payment stack owns#

Get the boundary right before you build anything. Let NetSuite own accounting truth and AP controls, and let your payment layer own routing and execution when that is the harder problem. If you need deep payout orchestration, provider routing, or multi-rail decision logic, it is often cleaner to keep that outside the ERP and sync the outcomes back cleanly.

NetSuite is well positioned for AP automation, approvals, payment status visibility, and General Ledger outcomes. It also defines payment orchestration as managing and routing payments across gateways, processors, and payment services, which can be broader than what you want the ERP to own directly.

Step 1. Use a boundary table before you pick a vendor#

Use this as a boundary tool, not a ranking. The entries reflect public product and integration descriptions. Treat unknowns as pilot checks.

| Option | Control surface | Implementation speed | Reconciliation burden | Lock-in risk |

|---|---|---|---|---|

| NetSuite Intelligent Payment Automation | NetSuite owns AP-facing workflows for vendor details, bank info, and payment status; processing runs through the BILL vendor network | Can be faster when AP is the main issue and vendors are U.S.-based | Can be lower when finance wants status tracking in NetSuite, but still depends on BILL network processing and mappings | Coupling sits in the NetSuite + BILL model; Oracle docs also limit vendor-payment coverage to the U.S. |

| BILL with NetSuite integration | Operations can span BILL and NetSuite with sync for bills, payments, vendors, and accounts | Can move quickly if the team accepts a dual-system operating model | Depends on sync quality during close | Operational coupling shifts toward BILL even if NetSuite stays the ledger |

| Tipalti | Global payables execution sits outside NetSuite while extending NetSuite's ERP workflows | Depends on how much external payables scope you deploy | Requires disciplined reconciliation because execution and accounting are split | Coupling shifts toward the external payables engine |

| Stampli | AP workflows run through a Built for NetSuite verified integration with continuous sync claims | Often useful when invoice and approval friction is the main bottleneck | Depends on sync quality through posting and payment events | Dependency can shift toward the AP layer even with NetSuite central |

| Centime | Confirm with the vendor | Validate in a pilot | Validate with settlement and posting samples | Validate contract terms, data export, and exit path |

One detail matters more than it first appears: NetSuite Intelligent Payment Automation is embedded in NetSuite, powered by BILL, and Oracle says payment statuses are trackable in NetSuite. Oracle also states it supports payments to vendors operating in the United States and is not currently available in Canada, China, and Japan. If your AP problem is domestic U.S. vendor payments, that can be a clean place to start. Do not anchor new ownership decisions on the legacy Payment Automation SuiteApp, because Oracle targets support end on December 31, 2026.

Step 2. Consider external orchestration when routing is the hard problem#

When routing is the hard problem, consider keeping it outside NetSuite. If your core challenge is payout orchestration, provider routing, or custom multi-processor decisioning, an external orchestration layer may be the cleaner owner. NetSuite describes orchestration as connectivity and routing across payment providers, and Oracle describes its payment features as connected to third-party systems, processors, and financial institutions.

Integrate on narrow seams. Use SuiteCloud Platform Integration for system connectivity, and RESTlets only when you need custom server-side HTTP logic. For each payout, assign exactly one owner for route selection, one owner for execution state, and one owner for final GL posting. If two systems can both decide route or both mark a payout as paid, reconciliation risk is already rising.

Step 3. Start inside NetSuite when AP is the hard problem#

If your pain is invoice review, approvals, vendor payment handling, or payment recording, start inside NetSuite. NetSuite positions AP around invoice review, approval, and payment automation, and it claims automated journal entries reduce manual debit and credit work while improving payment recording accuracy.

This is where Intelligent Payment Automation can fit well. BILL's direct NetSuite integration can also fit if your team is comfortable operating across two systems. Stampli is a reasonable fit when approval and invoice workflow friction is the main bottleneck. Tipalti becomes more relevant when payables execution needs are broader and more global.

Step 4. Write the ownership contract before anyone codes#

Do not start coding until ownership is documented. Write down these three owners before implementation:

- Approval policy owner: which system defines approval, override, and escalation rules?

- Payout status owner: which system is authoritative for pending, paid, failed, or reversed states?

- Final General Ledger posting owner: which NetSuite posting event creates the accounting outcome finance closes on?

Then prove the boundary with one real payment evidence pack: approval record, payment status trail, synced vendor or bill record, and the resulting NetSuite posting outcome. If that pack does not tell one consistent story from approval to GL, the boundary is not ready.

If you want a deeper dive, read How to Maximize Your Xero Investment as a Payment Platform: Integrations and Automation Tips.

Prioritize modules in the order that prevents integration debt#

Module order affects how much integration rework you take on later. For this payment-platform scope, a practical starting point is ERP core and AP. Add OneWorld early when multi-entity scope is real, treat analytics as a reporting layer once transaction definitions are stable, and bring in other modules only when they change a live payment or posting outcome.

Step 1. Start with NetSuite ERP core and Accounts Payable#

Keep the first milestone tight: core finance objects and AP flows. NetSuite describes modules as components for specific business functions, and its ERP core as handling critical financials and accounting tasks. If your immediate problem is vendor payouts, approvals, and close accuracy, keep the first release there.

Oracle also positions AP processes as manageable within NetSuite, and NetSuite Intelligent Payment Automation as improving efficiency and reducing AP processing costs. Expand into CRM or commerce when those records directly affect approval, payment handling, or posting.

Checkpoint: prove one full bill-to-payment path in NetSuite, including the bill record, approval record, payment status trail, and final posting result, before widening scope.

Step 2. Add Global Business Management early when multi-entity scope is known#

If you already know you need multiple subsidiaries, business units, or legal entities, include Global Business Management, OneWorld, in your initial design. NetSuite positions OneWorld for multi-entity operations in one ERP, with support for 27 languages and 190 currencies.

Make this an early design choice because entity and currency context can shape core transaction records. Before go-live, validate with a two-entity AP scenario so the approval, payment, and posting path is coherent in each entity.

Step 3. Position Business Intelligence as an analytics layer#

NetSuite Analytics Warehouse is positioned as a cloud data warehouse and analytics layer that consolidates NetSuite and non-NetSuite data. For this scope, use it as a reporting consumer after you define core payment and posting states.

In practice, define transaction ownership in NetSuite first, then feed analytics once payment and posting states are consistent.

Step 4. Add CRM, commerce, SuitePeople, and PSA based on active dependencies#

Bring in adjacent modules when they directly change payment control or accounting outcomes. NetSuite CRM manages interactions, SuiteCommerce unifies ecommerce, POS, order, and related operations, SuitePeople covers HR, and PSA covers project-services operations.

Use a simple dependency test: if a module does not change an approval rule, allocation rule, payment handling path, or posting result in the current release, defer it.

Gather prerequisites before implementation starts#

Payment builds go better when you settle accounting assumptions before automation starts. Lock ownership and migration assumptions up front so AP and General Ledger outputs stay reliable from day one.

Step 1. Build the source-of-truth pack#

Build the source-of-truth pack before you touch automation. Create the core artifacts first: chart of accounts, posting rules, approval matrix, and exception ownership. In NetSuite, the chart of accounts is an early prerequisite because it defines where transactions post and how reporting is structured.

If invoice approvals are in scope, include the workflow prerequisites in the same pack: required features, roles and permissions, the NetSuite Approvals Workflow SuiteApp, and approver assignment for each invoice creator. NetSuite requires a supervisor approver per creator, so verify that mapping before workflow tests. Use one vendor bill as a checkpoint and confirm the target account, approver path, exception owner, and expected final posting.

Step 2. Validate migration assumptions from QuickBooks or other legacy tools#

Treat migration controls as implementation work, not cleanup for later. Build opening balances from a prior-system trial balance in debit and credit format, then reconcile open liabilities separately before automation baselines are set.

If QuickBooks is the source, use both the Accounts Payable Aging Summary and Accounts Payable Aging Detail during reconciliation. For AP imports, follow the sequence rules: if you import both vendor bills and vendor payments and want payments applied to bills, import the bills first. For large CSV loads, split batches when transaction size approaches Oracle's 5,000-line guidance limit.

Step 3. Define success checkpoints before build starts#

Define success measures before design or build begins. Track AP cycle time, manual status interventions, and close quality. Keep baseline and target definitions explicit so you can tell whether automation reduced manual effort and error risk instead of just changing dashboard output. For close outcomes, track both cycle-time movement and control integrity, not just reporting presentation.

Step 4. Mark vendor capabilities as unknown until you test them#

One of the simplest ways to avoid bad decisions is to mark unverified claims as unknown. For Zone & Co, Centime, and other AP vendors, treat unverified capability claims as unknown until they are confirmed in your own test matrix. Public pages can include strong positioning, but that is not evidence of posting ownership behavior, reconciliation burden, or operational fit in your environment.

When evidence is missing, record "unknown" and attach a test case. That keeps selection grounded in implementation results instead of marketing language.

For a walkthrough, see How to Build the Ultimate Finance Tech Stack for a Payment Platform: Tools for AP Billing Treasury and Reporting.

Define events and posting contracts before enabling automations#

Automation only works cleanly when the event contract is explicit. No event should affect General Ledger outcomes in NetSuite unless you have defined who owns the status, whether it should post, and how retries or reversals are handled.

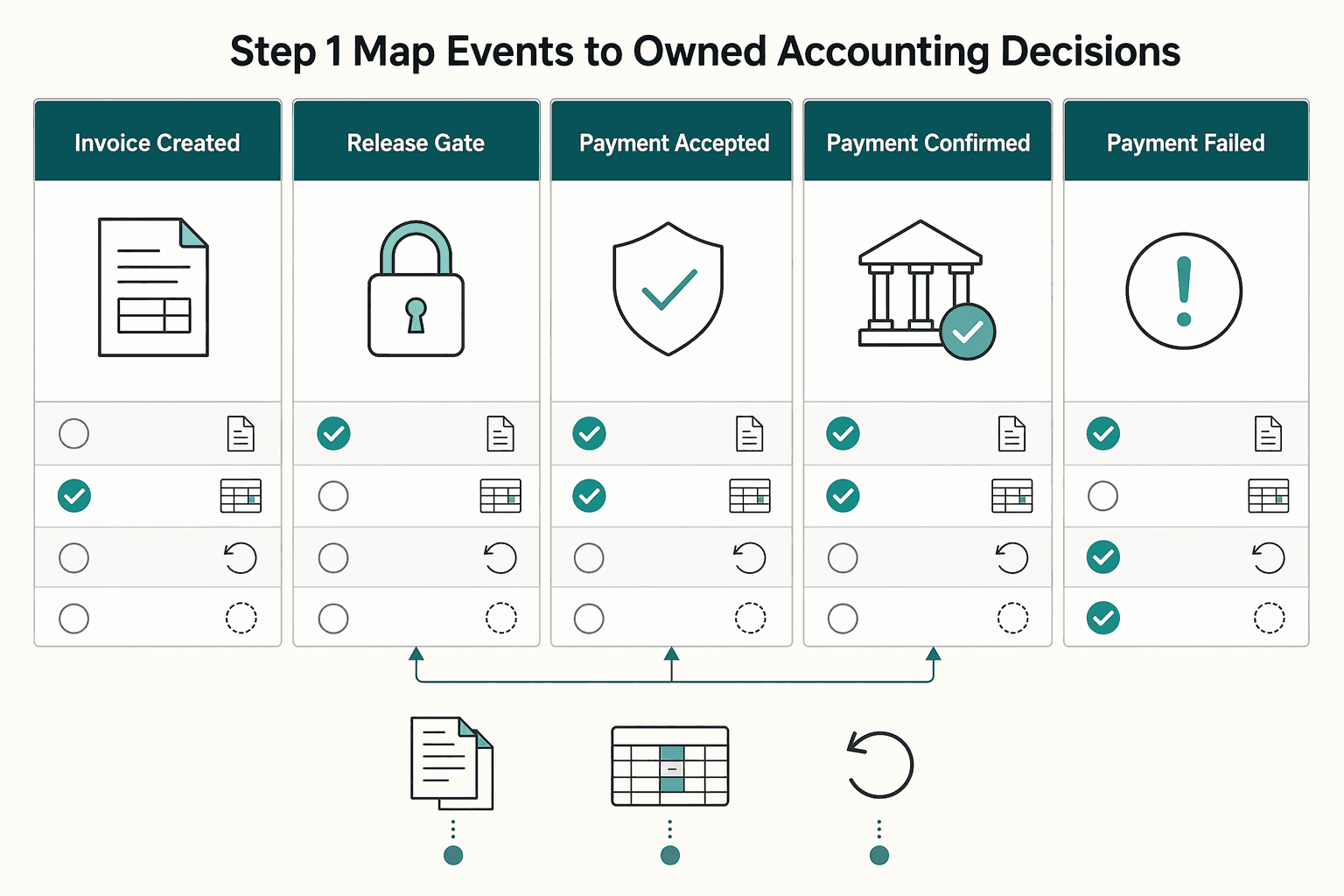

Step 1. Map events to owned accounting decisions#

Start by listing the events you actually process across invoice intake, approval, payment, failure, reversal, and retry. For each event, decide whether it is status-only, a posting trigger, a reversal trigger, or a non-accounting event.

NetSuite documentation highlights payment-stage visibility and approval routing. Use that visibility, but keep it separate from ledger action. Your contract should explicitly state which events can change accounting records and which only update status in NetSuite ERP.

| Event | Operator state (example) | Accounting decision to define |

|---|---|---|

| Invoice created or received | Pending | Status only, or post if your AP policy requires it |

| Approval completed | Pending or approved | Usually status only unless approval is your release trigger |

| Payment accepted by provider | Pending | Hold final post until your defined confirmation point |

| Payment confirmed | Posted | Post once according to your contract |

| Payment failed or returned | Investigation required or reversed | Define reverse vs hold vs wait-for-evidence |

| Retry or duplicate delivery | No state change or pending review | Never post again because the same event was delivered again |

If you use NetSuite Intelligent Payment Automation, include its scope in the boundary decisions. Oracle notes U.S.-based availability requirements, so do not assume one NetSuite-native lane covers every payment flow.

Step 2. Enforce idempotency on outbound requests and inbound webhooks#

Retry safety lives or dies on idempotency. Stripe documents idempotent requests for create and update calls and recommends idempotency keys. It also warns that webhook deliveries can be duplicated and recommends logging processed event IDs.

Use both controls to prevent duplicate postings and reconciliation drift between provider status and NetSuite ERP when retries happen:

- Send idempotency keys on supported create and update requests.

- Persist processed webhook event IDs before running posting logic.

Step 3. Define explicit async triage states for operators#

Asynchronous flows need operator states that reflect reality. Define internal triage states, for example pending, posted, exception review, or reversed, and treat them as your operating model rather than assumed default NetSuite statuses.

For each queued item, show the fields operators need to act: source event ID, provider object ID, last event timestamp, NetSuite transaction reference if available, current state, and owner.

Step 4. Replay event tests and validate reporting before release#

Run replay tests before release, not just unit tests. Stripe supports local webhook testing with the Stripe CLI. Stripe also retries undelivered events for up to three days, so your tests should include duplicate deliveries and delayed redelivery at minimum; add other scenarios based on your implementation.

Then validate Financial Reporting extracts against expected totals from your source-of-truth pack. If totals, counts, or reversal outcomes do not match expectations, fix the contract before you enable broader automation.

Related guide: Intacct vs. NetSuite for Payment Platforms: Which ERP Handles Multi-Currency and High-Volume AP Better.

Before rollout, map your event states and retry behavior against Gruv's API and webhook patterns in the developer docs.

Automate approvals and payouts with clear escalation paths#

Approval automation is worth it only if escalation is explicit. You want speed without creating a side door around control. Use threshold-based routing for Accounts Payable payment release, and keep override rights narrow, visible, and reviewable.

Step 1. Configure layered approval routing before automating release#

Set Payment Run Approval Routing in NetSuite Intelligent Payment Automation, powered by BILL, before broad rollout. You can define approval limits, levels, and workflow, and only approved payments move forward to processing when routing is enabled.

Keep invoice approval and payment release approval as separate decisions, even if the same approvers are involved. BILL supports threshold-based enforcement, so payments above your configured amount must be approved, for example, a $1500 payment against a $999 threshold.

Treat override power as an escalation path, not a default path. BILL documents that an Administrator can pay regardless of bill approval policy, so assign override ownership and require separate attestation in your internal records.

Step 2. Define an urgency rule that does not weaken controls#

Urgent payouts need a written rule, not a case-by-case bypass. Use a simple standard: if a payment stays inside a pre-approved path and within its threshold, route it through the defined workflow. If it falls outside, require manual signoff and record the reason in the case or approval note.

Document the lane criteria clearly. The lane design is your policy, not a built-in low-risk or high-risk label in NetSuite or BILL.

Step 3. Keep payment status visible in one operating view#

Teams cannot manage approvals well if status is scattered. NetSuite Intelligent Payment Automation supports real-time tracking, and dashboard reminders include payment runs awaiting approval and approved runs awaiting BILL submission.

Use that to keep a shared operating view with at least these internal states: awaiting approval, approved awaiting BILL submission, processing, failed, and canceled. If you still rely on the legacy Payment Automation SuiteApp, treat it as transitional given the stated support-end timeline of December 31, 2026.

Step 4. Route failed and stale states into an owned exception queue#

Failed and stale payments belong in a queue with an owner, not in an email thread. In NetSuite, operators can investigate through SuiteBanking > Payment Automation > Dashboard, then the canceled list, then the Payment Audit Trail, and use the Failed Reason field on the payment record.

Email alerts are useful signals, not your control surface. BILL may notify users when an ePayment fails, and Oracle references delayed-payment alerts sent at 2 PM ET daily. Your actual control is the owned exception queue with a required next action and daily aging review.

Related guide: White-Label Checkout: How to Give Your Platform a Branded Payment Experience.

Build reconciliation that survives scale and audits#

If you treat reconciliation as cleanup, scale will outrun control. Build it as a release gate instead. Each payment should be provable at three levels: transaction event, settlement batch, and posted General Ledger outcome in NetSuite.

Step 1. Capture transaction-level evidence when the event occurs#

Start with the smallest auditable unit: one payment or payout event. For each event, retain the provider reference, your internal reference, amount, currency, status change, and target accounting object, whether that is a bill, invoice, or payment record. When available, use transaction-level settlement reporting. Adyen's Settlement details report is intended for transaction-level settlement reconciliation and includes payments that were settled and paid out.

Checkpoint: sample events, including retries, and confirm that one business event leads to one expected accounting outcome. Duplicates can occur during retries. Stripe documents idempotency as protection against performing the same operation twice, but idempotency keys can be pruned after they are at least 24 hours old. Duplicate control cannot rely only on processor memory. Keep your own durable reference controls in NetSuite and your integration layer.

Step 2. Match settlement batches to bank payouts#

Once transaction evidence is in place, reconcile each settled batch to actual cash movement. Stripe's payout reconciliation report is built to match each bank payout to the batch of transactions it settles.

For each payout, keep the provider report, the related bank statement line, and the underlying transaction list. Check that each bank payout traces to its settlement batch, and that each transaction in that batch is explainable. One common break here is timing mismatch: settlement is recorded before cash lands. That may be valid, but it still has to be classified and cleared, not left as a generic pending item.

Step 3. Tie controls to Financial Reporting and posted General Ledger results#

Operational dashboards help, but they are not enough for control evidence. SEC ICFR framing focuses on the reliability of financial reporting and external financial statements, so dashboard status alone may be insufficient.

Use Financial Reporting outputs and posted General Ledger balances as the control surface. This aligns with NetSuite's reconciliation model of comparing bank statements, payment gateways, and internal ledgers, and with GL-focused matching workflows in a centralized workspace. Check that provider totals, bank evidence, and posted GL totals align for the close period. If an operational screen says paid but the posting lands in the wrong account or currency, the GL outcome is the source of truth.

Step 4. Use a daily break taxonomy and expansion gate#

Keep the break taxonomy short enough to use every day:

- Timing mismatch: date or settlement timing difference with a traceable reference.

- Mapping mismatch: amount, account, or currency mismatch; NetSuite reconciliation guidance explicitly surfaces unmatched and mismatched amount and currency conditions.

- Duplicate event: one business action appears twice from retry or posting duplication.

- Unknown reference: payout, settlement line, or GL entry cannot be tied to a known transaction.

Use this taxonomy as an internal expansion gate. Do not broaden automation coverage until daily break rate and time-to-resolution are stable for two close cycles. This is a house rule, not a vendor-mandated threshold, and it helps prove repeatable accounting outcomes before you add more volume, entities, or payment lanes.

Pair this with What Is a Payment Facilitator (PayFac)? And Should Your Platform Become One.

Add compliance and tax gates without freezing throughput#

Compliance and tax gates can sit on the payout-release path without freezing the whole case. The practical rule is simple: unresolved required gates block payout, while the rest of the work stays visible so operations, finance, and support can clear issues quickly.

Step 1. Place identity controls at onboarding and again before payout release#

Use two explicit checkpoints: onboarding and payout trigger. Jurisdictional obligations differ, but a second pre-release check can help catch stale, incomplete, or newly risky records before cash leaves.

In regulated U.S. contexts such as money services businesses, AML programs are required, and customer identification is part of that control framework. At account opening, collect the minimum required identity data for your regulated context. For legal entities, where applicable, include beneficial-owner identification and risk-based verification.

Model outcomes as explicit states, not pass or fail only: pending, needs review, blocked, and not applicable, each with a reason code. If a screening vendor times out or returns no result, do not treat that as approval.

Checkpoint: test records where onboarding passed but the payout-trigger check is incomplete, and confirm payout cannot move from ready to released. Retain timestamped evidence, reviewer identity, and the exact check result used.

Step 2. Tie tax documents and VAT validation to payout readiness#

Tax readiness belongs in payout readiness, not a year-end scramble. For U.S. payees, use Form W-9 data for information-return workflows. For foreign individuals or entities, route to W-8BEN or W-8BEN-E and store structured fields, not only file uploads.

For EU VAT numbers, treat validation as a formal gate when VAT status affects processing. VIES is a validation lookup, so store what was checked at that time: VAT number, check date, and result. A common failure mode is keeping the form file but skipping the searchable fields needed for reporting and exception handling.

Step 3. Scope 1099, FBAR, and FEIE support carefully#

Support reporting preparation without drifting into tax advice. Keep 1099 payment-type and payee-classification data separate, and do not hard-code a 2026 nonemployee-compensation threshold from secondary sources without current IRS primary confirmation.

Use grounded details where they are available. Form 1099-MISC includes a $10 royalties threshold and multiple $600 categories. FBAR is filed on FinCEN Form 114 when aggregate foreign-account value exceeds $10,000 during the calendar year, due April 15 with an automatic extension to October 15.

Keep FEIE and FBAR handling limited to reporting support and data capture. Questions about filing obligations, exclusions, or treaty positions should go to qualified tax specialists.

Step 4. Separate payout blocking from case visibility#

Block cash movement when required gates are unresolved, but keep the case moving where it can. Payout eligibility should be its own state, separate from broader operational or accounting progress.

Avoid both extremes: freezing everything or releasing funds with open compliance or tax issues. The practical middle path is visible workflow progression with a hard stop only at payout release.

Checkpoint: exception views should show the failed gate, owner, date opened, and next required action. A single generic status like "compliance failed" creates unclear ownership and avoidable close-period friction.

We covered this in detail in Revenue Leakage from Payment Failures: How Much Are Failed Transactions Really Costing Your Platform?.

Execute a 30 60 90 day rollout with exit criteria per phase#

Use 30 60 90 as a phased evidence plan, not a calendar promise. Expand only when the current layer posts cleanly in NetSuite ERP and holds up under reconciliation and close checks in your General Ledger.

| Phase | Primary scope | Exit evidence | Stop condition | Example owner split |

|---|---|---|---|---|

| Days 1 to 30 | Core finance in NetSuite ERP and General Ledger | Transaction matching and reconciliation reports support close, finance signs off posting controls | Reconciliation breaks exceed your pre-agreed tolerance | Engineering: event contracts; Finance: posting controls; Operations: exception handling |

| Days 31 to 60 | Accounts Payable and approval automation | Interventions trend down from baseline, approval/payment statuses stay traceable, GL output remains stable | New automation creates unresolved mapping or posting breaks above tolerance | Engineering: integration behavior; Finance: approval-to-posting rules; Operations: stale/failed queues |

| Days 61 to 90 | Expansion modules such as Global Business Management (OneWorld) and NetSuite Commerce where needed | New entities, currencies, or channels post correctly and reconcile to the ledger | Entity, currency, or channel mappings introduce unexplained breaks | Engineering: module event mapping; Finance: subsidiary/currency controls; Operations: cross-channel exceptions |

Step 1. Lock accounting correctness first#

The first phase should prove accounting behavior, not just process flow. NetSuite positions core ERP around critical financials and accounting tasks, so Phase 1 should confirm clear transaction-to-posting mappings and stable ledger outcomes.

Set exit criteria around evidence, not "it runs." Validate transaction matching and reconciliation outputs. Compare the results to finance-approved posting expectations in the General Ledger, then retain reconciliation and reconciled-statement reports as close evidence.

If reconciliation breaks exceed the pre-agreed tolerance, pause expansion and remediate mappings first. Do not move to AP automation until reconciliation and close checks pass again.

Step 2. Expand Accounts Payable and approval automation#

Move to Accounts Payable only after ledger behavior is stable. NetSuite AP is built to automate supplier-invoice review, approval, and payment, so it makes sense as the second phase.

Measure operational impact against a baseline, including manual reroutes, status corrections, and exception tickets, then exit only when interventions decline and posting quality stays stable. If you use NetSuite Intelligent Payment Automation, keep scope aligned to documented support, including current regional availability limits.

Do not treat clean workflow statuses as proof of accounting correctness. A practical split is engineering on event behavior, finance on approval-to-posting controls, and operations on exception queues.

Step 3. Add broader modules only when business scope requires them#

Add expansion modules when the business case is real, not because day 90 arrived. NetSuite modules are designed to expand over time as goals change, but each addition should pass the same reconciliation discipline as the earlier phases.

Use OneWorld for actual multi-subsidiary or multi-currency scope, and add NetSuite Commerce when payment flows depend on web store or POS operations. In both cases, verify that new transactions map and reconcile correctly back to the ledger. If new entity, currency, or channel mappings create unexplained breaks, stop and remediate before adding more automation.

Avoid the failure patterns most teams hit in quarter one#

Quarter-one failures are often process failures, not feature failures. A common pattern is teams trusting vendor claims too early, automating before posting rules are settled, customizing edge cases too soon, and leaving exceptions without named owners.

Step 1. Validate vendor claims in your own NetSuite test matrix#

Use your own NetSuite Sandbox and test matrix as the decision source, not vendor positioning. Claims do conflict in the market: Centime describes itself as the only fully embedded NetSuite AP automation option, while NetSuite describes BILL-powered NetSuite Intelligent Payment Automation as fully embedded.

Oracle guidance supports this approach: sandbox environments are for safe testing and third-party integration trials before production, and Release Preview materials include a testing matrix for workflow testing. Use that matrix across Tipalti, BILL, Stampli, and Centime. Verify what object is created in NetSuite ERP, which events create a posting transaction, what approvals are required before journal entries post, and which statuses remain visible while approvals or payments are pending. Treat claims like Tipalti's "up to 80%" reduction as marketing context, not architecture proof.

Step 2. Freeze automation if General Ledger rules are still fuzzy#

If accounting cannot explain the expected ledger impact of an approved transaction, pause the rollout. In NetSuite, posting transactions are the transactions that hit ledger accounts, and journal entries are not posted until approved.

The recovery path is simple: freeze new automation, finalize General Ledger mappings, and rerun historical test cases until replayed outcomes match finance-approved expectations. A practical scope check is NetSuite Intelligent Payment Automation: it is BILL-powered, but documented as supporting payments to vendors operating in the United States only and currently unavailable in Canada, China, and Japan.

Step 3. Revert early edge-case customization to standard NetSuite patterns#

Early edge-case customization can become a trap. When those cases show up, default back to standard NetSuite patterns first. Oracle's customization guidance explicitly says to plan ahead using existing standard features and to set up internal controls.

Keep approval routing in supported capabilities like SuiteFlow where possible, and isolate only the custom logic you actually need behind clear interfaces. If you cannot clearly state which standard object owns the record, who approves it, and when it becomes a posting transaction, you probably customized too early.

Step 4. Assign named owners for exceptions and rollback decisions#

Exception handling needs named ownership before expansion. CISA and NIST both emphasize clearly defined responsibilities in response planning, and the same control principle applies here.

Assign three owners up front: queue triage, accounting signoff, and release rollback decisions. Make the owner list explicit in queue and release process docs so stalled statuses or questionable posting outcomes have a clear investigator, decision owner, and stop or revert authority.

Also see: How to Build a Deterministic Ledger for a Payment Platform.

Final takeaway and copy paste launch checklist#

The safest launch rule is simple: do not go live until ownership, posting behavior, and test evidence are explicit. If you want to move fast without creating cleanup work, keep scope narrow, get finance approval on controls, and rely on replay proof rather than demo confidence.

Step 1. Confirm ownership boundaries#

Document what NetSuite owns, what the payment service owns, and who owns final General Ledger posting. If NetSuite Intelligent Payment Automation is in scope, treat it as the in-ERP vendor payment path with embedded automation using BILL, and align on which system is the payment system of record. Checkpoint: every state change has one owner and one source of truth.

Step 2. Approve module order before adding reach#

A practical low-risk sequence is to start with NetSuite ERP core finance and Accounts Payable, then expand only after reconciliation is stable. This is a practical sequencing choice based on core finance coverage plus AP controls, including approval routing, status tracking, and automated GL entries, not a universal vendor-mandated order. Checkpoint: close is stable under real traffic, not just "module enabled."

Step 3. Validate event contracts with replay tests#

Define expected accounting outcomes for create, approve, initiate, pending, success, failure, reversal, and retry states. Treat webhook processing as asynchronous, design for duplicate deliveries, and use idempotency keys for create and update retries in line with Stripe guidance. Checkpoint: replaying the same event set produces the same General Ledger result every time.

Step 4. Enforce approvals, exceptions, and reporting controls#

Use policy-based approvals, including threshold routing and defined limits for payment runs. Set named owners for exception queues and define daily break categories tied to financial reporting so issues are triaged consistently. Checkpoint: breaks are quickly categorized and assigned without ad hoc chat or email handling.

Step 5. Gate go-live by evidence and rollback readiness#

Require a compact evidence pack before release: posting matrix, UAT results, replay outputs, sample invoices with expected debits and credits, approval proof, and the compliance gates required by your model. Depending on scope and jurisdiction, this can include risk-based AML and customer-identification controls and tax-document readiness such as Form W-9 and Form W-8BEN-E. Checkpoint: rollback is documented, including the disable path, approver, and double-processing prevention. Also avoid anchoring new work to the legacy Payment Automation SuiteApp path, with support targeted to end on December 31, 2026.

If you want a second set of eyes on module sequencing, payout controls, and reconciliation ownership, talk with Gruv.

Frequently Asked Questions

Which NetSuite modules should a payment platform implement first for ROI?

Start with core NetSuite ERP finance capabilities and Accounts Payable. That is where key payment records are created, and where invoice review, approval, and payment automation already exist. Add other modules only when they solve a specific requirement such as entity structure, approval ownership, or reporting scope.

When should we use `NetSuite Intelligent Payment Automation` and `BILL` versus a third-party integration?

Use NetSuite Intelligent Payment Automation when you want vendor payment automation directly inside NetSuite and your scope fits its documented limits. Those limits include U.S.-based companies, payments to vendors operating in the United States, production-account use, and USD bill payments. If you need broader geography, non-USD execution, or non-production validation, evaluate third-party integrations for those flows.

What automations deliver the fastest impact without creating long-term platform debt?

Approval routing, invoice-status tracking, and automated General Ledger entries are often the fastest low-debt wins. They improve visibility and payment recording without forcing broad architectural change. Keep the first release narrow by automating standard supplier-invoice paths before expanding into edge-case payout logic.

What are the top integration risks in NetSuite payment implementations, and how do we mitigate them?

The main early risks are implementing outside documented scope and leaving ownership of accounting outcomes unclear across approvals and payments. Mitigate them by confirming scope limits up front, assigning one owner for approval policy, payout status, and final GL posting, and validating expected journal-entry outcomes with finance before expansion.

What should a practical 30/60/90 implementation sequence look like for engineering and finance teams?

Use 30 60 90 as a sequencing framework, not a mandated rule. In the first 30 days, align finance and engineering on scope limits, posting rules, approvals, and test cases. In days 31 to 60, run AP approvals and status handling in a narrow lane and verify automated entries. In days 61 to 90, expand payment execution and subsidiary rollout only after close checks and exception handling stay stable.

How do we keep `Accounts Payable` automation from breaking `General Ledger` accuracy?

Define the expected accounting outcome for each workflow state before you enable automation. Validate sample invoices against expected debits, credits, and approval checkpoints reviewed by finance. If the team cannot clearly explain posting behavior for key states, pause expansion.

Which compliance gates should block payouts by default: `KYC`, `KYB`, `AML`, or tax-document gaps?

There is no universal default gate set for every platform. Block payouts based on the requirements tied to your business model, license type, and regulatory perimeter. Depending on scope, that can include customer identification controls, legal-entity and beneficial-owner verification, AML program obligations, and tax-document readiness such as Form W-9 or Form W-8BEN.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- cisa.gov/sites/default/files/publications/Incident-Re...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- irs.gov/forms-pubs/about-form-w-9trusted

- irs.gov/businesses/small-businesses-self-employed/re...trusted

- nvlpubs.nist.gov/nistpubs/SpecialPublications/NIST.SP.800-61r...trusted

- sec.gov/files/rules/interp/2007/33-8810fr.pdftrusted

- docs.oracle.com/en/cloud/saas/netsuite/ns-online-help/articl...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: