Quick Answer

The safest sequence is to classify the worker before payout setup, verify PAN, define TDS treatment before the first payout, and use only payout rails your team can monitor, reconcile, and pause. If classification facts, PAN, or withholding treatment are unresolved, block or escalate the case instead of paying first and fixing it later.

What to set up before paying contractors in India#

If you are hiring contractors in India, your first compliance decision is classification, not payment speed. Before payout design, you need a defensible sequence for contractor status, tax handling, and rail selection, with clear stop points when key facts are incomplete.

This guide is for teams that own that chain end to end: compliance, legal, finance, tax, risk, and payments operations. In marketplace, creator, and services models, the same questions come up at onboarding, first payout, audit, and exception review:

- capture the working-relationship facts needed for classification

- align tax handling with the documented classification

- use payout controls your team can monitor, reconcile, and pause

- block or escalate when classification or tax facts are unresolved

That sequence matters because India treats employees and independent contractors differently for legal and tax purposes, and contract labels alone are not decisive. Classification turns on the real working relationship, with courts applying two primary tests: control and integration. If your team controls how, when, or where work is performed, or if the worker operates as part of your internal organization, your risk can look employee-like even when the agreement says "contractor."

A practical checkpoint is fixed working hours or shift timings. If your program design depends on that level of control, pause payout setup and review classification first.

The downside is not theoretical. Misclassification has been described as creating backdated PF and ESI liabilities, tax penalties, and possible permanent establishment exposure. In severe cases, that exposure is described as potentially pulling global profits into Indian corporate tax at 40%.

Treat payout design as a compliance control, not just an operations choice. A faster rail is not automatically better if it weakens traceability, return handling, or approval evidence. Later sections compare payout flows through that lens.

This is an operational explainer, not legal advice. India's Labour Codes and related legal and tax treatment can require interpretation. When classification or tax treatment is unclear, escalate to India-qualified counsel or tax advisers and document the decision trail.

Build the legal and payment mental model first#

Treat classification and payout as one control system from day one. Contract labels and day-to-day working models can diverge; when they do, you create worker misclassification risk that can spill across legal, tax, and payment operations.

Keep the legal anchors in the right place#

Use the Labour Codes as reference anchors, not quick-answer shortcuts. They help define what your team should confirm and document before money moves.

The Labour Codes changed the compliance architecture around wages, flexibility, digital compliance, gig work, and industrial relations, but outcomes can still vary by state implementation. Keep a short classification note in each file that explains why the worker is treated as a contractor, who approved that view, and what facts would trigger a recheck.

Treat payout design as a compliance control#

Payout design is a compliance decision, not just treasury plumbing. For contractor payouts, your process should support withholding review and records you can reconcile later.

| Before first payout | If missing |

|---|---|

| What service was purchased | Pause payment |

| Which contract version governs it | Pause payment |

| How TDS treatment was reviewed | Pause payment |

Before the first payout, make sure the file answers three questions: what service was purchased, which contract version governs it, and how TDS treatment was reviewed. If any answer is missing, pause payment.

Also document why you approved any advance. In practice, contractor requests can include upfront or milestone payments in the 10-30% range. Pricing is not standardized, and halted projects can leave upfront spend hard to recover.

Related: The Agency Scaling Blueprint: From Solo Freelancer to Hiring Your First 5 Global Contractors.

Decide contractor status before you design payouts#

Decide status before payout setup. If you see multiple employee-like signals, pause onboarding and send the case for legal review before first payment. In India, status is assessed on substance across multiple criteria, not contract labels alone.

Use a pre-onboarding decision table#

| Signal area | Lower-risk contractor signs | Employee-like red flags | Verify before approval |

|---|---|---|---|

| Control | Worker controls how work is performed; engagement is output or milestone based | Managerial control over tasks, methods, or day-to-day performance | Scope, instruction flow, required working pattern, supervision pattern |

| Contract substance | Written contract clearly states services and fee basis | Weak or unclear contract substance | Signed contract version and a short note on why the substance fits contractor treatment |

| Payment method | Payment is tied to deliverables, milestones, or agreed service fees | Salary-like or time-wage style payment that looks like employee treatment | Invoicing/payment basis and approval note on classification fit |

| Other criteria | Facts across criteria align with contractor treatment | Facts across criteria point toward employee-like substance | Escalation note that captures unresolved risk and any state/industry context |

Control, contract substance, and payment method are core checks. A written contract helps, but it does not cure a working model that operates like employment. Treat payment design as a status signal, not an admin detail.

Watch for employee-like substance#

Focus on substance, not labels. The pattern to watch is strong employer control and other facts that point toward employee-like treatment across criteria.

Different legal and tax treatment applies to employees and independent contractors in India, and misclassification risk is high. If challenged, outcomes can include regularisation, back wages, statutory benefits exposure, fines, legal liability, and reputational damage.

Escalate before money moves#

Apply one internal escalation rule consistently: if multiple employee-like signals appear, stop onboarding and route the case to legal review before activation or payout setup.

Keep the review pack short and concrete: signed agreement, brief classification note, payment method, and the facts behind each red flag. This gate matters because labor-law outcomes can vary by state and industry.

For a closer look at UPI as a payout rail, see How to Pay Contractors in India Using UPI: Compliance and Speed Explained.

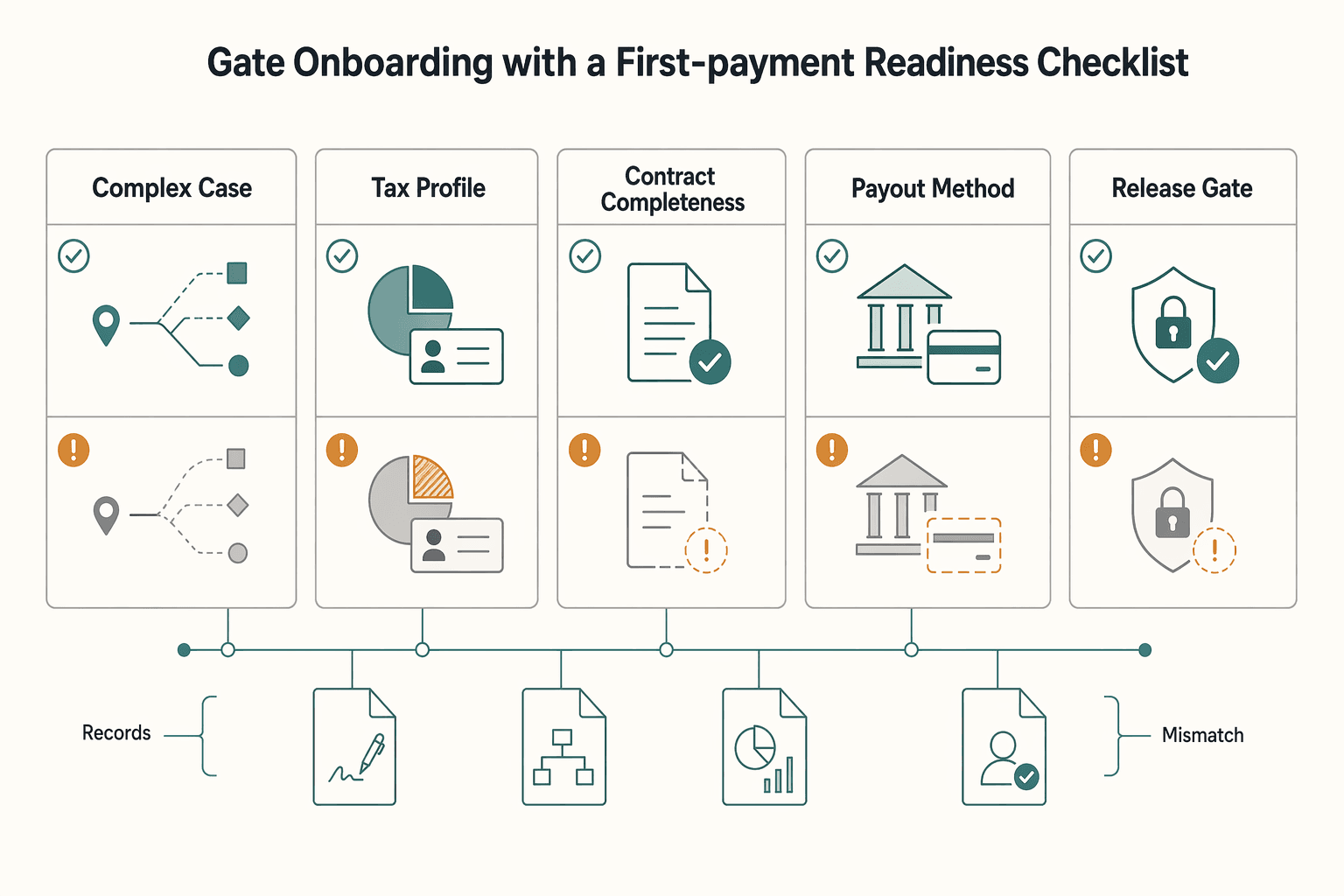

Gate onboarding with a first-payment readiness checklist#

After status review, use a hard gate: no activation and no first payment until readiness checks are complete in order. This is a practical first line of defense against compliance and operational risk.

| Step | Verify before activation | Why it should block first payment |

|---|---|---|

| Identity and KYC completion | Required onboarding fields are complete and tied to the correct payee profile | Incomplete core data weakens every downstream check |

| Tax profile data quality | Tax-related fields are captured cleanly in the same profile path your payment workflow reads | Data gaps here create avoidable processing and support risk later |

| Contract completeness | Signed agreement is on file, scope is clear, and fee basis matches the planned payment model | Paying before contract completion weakens decision support and auditability |

| Payout method readiness | Intended rail, beneficiary details, and operating ownership are confirmed in the systems actually used | "Approved" does not mean "payable" if setup is incomplete |

| Approval sign-off | Approver identity and approval date are recorded before activation | You need a visible decision trail, not implied approval |

Before go-live, add one explicit checkpoint: confirm compliance, payments, and approvers are looking at the same records. When teams work from different systems or unsynced profiles, risk visibility drops and delays increase. Keep the evidence pack minimal but durable: signed agreement, statutory mapping snapshot at activation, tax profile snapshot at activation, and approver identity.

Also confirm program-level reality, not assumptions: what your current stack enables for this India flow, and what still needs manual handling. Assign ownership for manual gaps before activation.

If your model includes agency-supplied workers, apply this gate even more strictly. Principal-employer exposure can arise when statutory dues are missed. Verify immediate statutory mapping checks, for example UAN and ESIC IP number, as part of onboarding records.

For the licensing side of payout flow design, see How Foreign Platforms Should Scope RBI Payment Aggregator Licensing in India.

If you are turning this checklist into a controlled workflow, map each approval, hold, and release state to your payout process in Gruv docs.

Collect PAN with controls that survive audit#

PAN collection is a payout control, not profile hygiene. If PAN is missing or wrong, your TDS handling under Section 206AA and the contractor's year-end tax records can both be disrupted.

Store PAN in a dedicated tax field, not free text. Verify it with the same identity inputs used in the Income Tax portal's Verify PAN Status flow: full name, date of birth, and mobile number. PAN is a ten-digit alphanumeric number, so your intake check should confirm the value is captured cleanly and tied to the same payee profile your finance team will actually pay.

Set a clear intake rule#

Use a strict consistency rule: the submitted full name must align across PAN verification, contractor profile, and payout record. If there is a material mismatch, or PAN appears to belong to someone else, treat PAN as unresolved and block payout until review is complete. Keep a compact evidence pack:

- PAN value in the tax profile

- name and date of birth used for verification

- verification date and result

- operator or approver identity for any cleared mismatch

Plan for retries. The verification OTP window is 15 minutes, so handoff delays can leave checks incomplete.

Tie PAN directly to TDS and tax usability#

Section 206AA requires PAN to be furnished to the tax deductor. If PAN is not furnished, tax is deducted at higher fallback rates under that section, including 20% as one comparison point. If PAN is invalid or belongs to the wrong person, it is treated as non-furnishing for this purpose.

The downstream effect is practical. TRACES states Form 16 is generated only for valid PAN and correct PAN reporting in TDS statements. TDS and TCS information is reflected in Form 26AS and AIS, so incorrect PAN reporting can make year-end tax records harder for the contractor to use.

Define failure behavior before payout day#

| PAN status at payout time | Operational action | Why |

|---|---|---|

| Verified and consistent | Release for normal TDS processing | Tax profile is usable and auditable |

| Missing PAN | Temporary hold or approved route under Section 206AA logic | Standard withholding path may be wrong |

| PAN inconsistent with identity details | Hold and rerun verification with corrected data | Wrong PAN is treated as non-furnishing |

| Verification incomplete | Keep onboarding incomplete until verification finishes | Unverified tax identity weakens reporting |

If an override is unavoidable, require a reason code, approver identity, and a dated remediation target.

Protect PAN as personal data#

Keep PAN data inside controlled systems, not in email or screenshots. Apply reasonable security safeguards, restrict unmasked access to need-to-know roles, mask PAN in routine views, and log access and exports. Retain PAN only as long as needed for legal and compliance purposes, then erase it unless retention is required by law.

The control objective is simple: verified PAN before activation, restricted visibility after activation, and no first payout while tax identity is unresolved.

For the full breakdown, read How to Get a PAN Card as a Foreign National in India.

Run TDS withholding as an operations process, not a one-time setting#

Run Tax Deducted at Source (TDS) as an ongoing control, not a one-time onboarding field. At minimum, resolve compliance and contract issues before the first payment, then re-check the facts you rely on before approved payouts: payee classification, service description, and any prior-period corrections.

Complete payee records help, but they do not replace an auditable process. The goal is a decision trail that another reviewer can follow later if withholding decisions are questioned.

Use a fixed sequence before every approved payment#

Start with classification. If the working reality no longer supports contractor treatment, escalate before processing payment. The point is straightforward: courts are described as looking at how work actually runs, not contract wording alone, using multiple factors rather than a single test.

| Step | Required action |

|---|---|

| 1 | Confirm payee classification and current service description |

| 2 | Confirm payee profile details and resolve any identity or profile conflicts |

| 3 | Determine withholding treatment under your approved internal rule for that payment |

| 4 | Approve payment only after withholding treatment is finalized |

| 5 | Post ledger evidence for gross amount, withheld amount, and net payout |

| 6 | Reconcile withholding records, payout records, and contractor-facing tax records |

Keep decision branches auditable#

| TDS decision branch | When this branch applies | Required operator evidence |

|---|---|---|

| Standard contractor payout | Classification remains contractor and profile is stable | Payee ID, service description used, profile status at approval, treatment selected, gross, withheld, and net amounts, approver and timestamp |

| Profile conflict | Payee profile data is missing, inconsistent, or recently changed without completed review | What conflicted, fields reviewed, who decided, whether payout was held, temporary handling if any |

| Service type uncertainty | Invoice, SOW, or contract descriptions do not align clearly enough for confident treatment | Documents reviewed, why treatment is uncertain, escalation owner, final decision and approver |

| Retroactive correction | A prior payout needs correction due to earlier record or treatment error | Original payout reference, corrected entry, approver, correction date, ledger adjustment, contractor communication record if used |

| Repeated exceptions | The same payee, team, or queue repeatedly needs manual overrides | Exception count or pattern, root-cause note, manager review, remediation owner, escalation record |

Escalate early when facts are unclear#

Use these triggers before exceptions become routine:

- service type is unclear across invoice, SOW, and business-owner description

- payee profile and payment request conflict

- a retroactive correction is needed after payout

- repeated manual exceptions appear for the same payee or workflow

Repeated exceptions are a control risk, not just an ops inconvenience. If a contractor-status issue is present, treat the exposure as potentially running back to day one.

Reconcile for tax-reporting readiness, not just close#

Month-end close is not enough. Your records should prove three links for each payout: what was withheld, what was paid, and what the contractor can use for tax reporting support. Keep one-to-one references where possible so finance can trace a withheld amount to a specific payout and any later correction.

A practical test is simple: can someone outside the original team explain, from retained records alone, why a specific amount was withheld on a specific payout date? If not, tighten the process before scaling it.

For a detailed walkthrough, see Enhanced Due Diligence for High-Risk Contractors: What Triggers EDD and How to Conduct It.

Choose payout rails by compliance fit and failure behavior#

Choose the rail you can prove, reconcile, and investigate in your own environment, not the one that only looks faster in a demo. If auditability and structured reconciliation matter most, prefer the option that gives your team usable reference data and clear failure events.

Treat rail selection as a control decision after withholding setup, not a checkout preference. A convenient flow can still fail operationally if finance cannot match payout status to ledger records or support cannot trace a missing credit.

| Payout path | When it may fit | What to verify before relying on it | Failure behavior to define up front |

|---|---|---|---|

| Domestic rail in your current stack | Domestic contractor payouts in your current stack | Whether records are detailed enough for finance reconciliation and case investigation | How you classify delayed credit, returns, and beneficiary-detail issues, and who owns each workflow |

| Alternative domestic rail in your stack | Domestic use cases you already operate and support | Whether your setup exposes outcomes and references your teams can actually reconcile | How you handle failed attempts, ambiguous status states, and retry approvals |

| Cross-border movement involving India | Any flow that is not purely domestic | Whether legal, tax, and payments owners confirm the route and required documentation | What triggers a compliance hold, provider rejection handling, and escalation ownership |

Treat legal and policy review as a design gate for cross-border flows#

For cross-border movement touching India, include legal and tax review before finalizing the rail. The point here is not a specific threshold or filing rule. Operating conditions can be restrictive and can change, so validate controls before rollout, not after an incident.

An official report describes India as a challenging place to do business and notes restrictive conditions such as data-localization enforcement and increased tariffs. It also documents a tax-law change passed on August 6, 2021. That is a practical reminder to date-stamp assumptions and re-check them over time.

Use source-quality checks before you lock policy assumptions#

When government guidance is part of your decision, verify source quality before you rely on it. Confirm the official domain and secure connection indicators, for example .gov and HTTPS lock signals where applicable. Record what guidance you relied on, who approved it, and when.

Define failure ownership before the first exception#

Set investigation ownership and evidence requirements before go-live. At minimum, define what counts as delayed credit, what confirms a return or reversal, what proof is retained for beneficiary mismatches, and who can approve retries.

Do not scale a rail until finance can reconcile real cases and support can investigate from retained records alone. If that bar is not met, use the path with clearer evidence and fewer ambiguous exceptions until controls are mature.

For a broader operating model, see Gig Worker Tax Compliance at Scale: How Platforms Handle 1099s W-8s and DAC7 for 50000+ Contractors.

Block, release, or escalate with explicit decision rules#

Blocked cases should be decided by written rules, not by whoever is online. Set a default action, assign an owner, and require retained evidence for any release or override.

Use an exception matrix as an internal control tool. Set explicit release and override checkpoints:

| Exception category | Default action | Release owner | Mandatory evidence before release or override | Escalate when |

|---|---|---|---|---|

| Missing required contractor data | Keep blocked under internal policy until reviewed | Compliance or policy owner | Outreach record, contractor response, profile snapshot, approval note | Repeated missing data, conflicting details, or pressure to bypass policy |

| Unresolved legal interpretation risk | Pause payout pending decision | Legal owner with business sponsor | Signed agreement or other traceable communications, decision memo, business justification | Disagreement on interpretation or indicators of higher legal exposure |

| Payout setup mismatch | Hold and correct setup before retry | Payments operations owner | Failed-attempt record, corrected payout details, retry approval | Repeated failures or unclear status outcomes |

| Compliance-review hold | Keep blocked until specialist review closes | Compliance owner | Case notes, review outcome, required records, approval record | Any bypass attempt or incomplete review evidence |

The key control is override quality. Require evidence you can reconstruct later from retained records, not informal approvals. A practical minimum is documented proof of agreement, such as signed documents or traceable communications.

Set severity by downstream exposure#

Use severity tiers so escalation stays consistent:

- Low: contained operational issue, reversible before funds move

- Medium: material delay or repeated data defects with no clear policy breach

- High: plausible legal, compliance, or policy exposure that needs formal review before release

Treat policy uncertainty as an escalation signal. A proposal can be far from enacted and still justify a pause-and-review decision.

No silent retries#

If you use a no-silent-retries internal rule for blocked cases, require every replay to include a reason code, the prior failure reference, approver identity, and the exact change made before retry. That helps keep the audit trail intact and reduces the risk of reprocessing unresolved blocked cases without accountable approval.

Keep an evidence pack that can answer regulator and auditor questions fast#

Release and override decisions are only defensible if the file is complete and traceable. For each third-party relationship, keep one evidence pack that can quickly show the classification basis, risk assessment records, monitoring and remediation history, compliance mapping, and how key decisions moved from approval to ledger posting.

Start with a minimum retained record set#

Do not rely on a generic "supporting docs" folder. Define the minimum before go-live, then append lifecycle evidence each time. At a minimum, retain:

| Record type | Retain |

|---|---|

| vendor identification | vendor identification and service-scope records |

| executed contract version | executed contract version in force when services were delivered |

| risk assessment | risk assessment records and ongoing monitoring evidence |

| remediation tracking | remediation tracking records, including exception handling |

| compliance mapping | compliance mapping artifacts used for internal and regulatory checks |

| approval evidence | approval evidence for onboarding, release, overrides, and retry actions |

Store this pack in a central repository with a clear owner. Documentation gaps often surface during audits, and response slows down when proof is scattered across emails, spreadsheets, drives, and tickets.

Make traceability work from request to ledger#

A usable pack needs an unbroken chain from payment request to the accounting result used in close:

| Evidence point | What it should show | Why it matters |

|---|---|---|

| Payment request or payable event | Who was paid, for what service, and under which contract | Anchors business purpose |

| Procurement record | Contract terms, vendor contact information, and service scope documentation | Confirms business context and ownership |

| IT/security evidence | Logs, monitoring outputs, and remediation evidence | Supports control effectiveness |

| Internal ledger event | Posting for expense, payable, and cash movement as applicable | Ties operations to books |

| Reconciliation export | File or report used in close to match provider activity to internal records | Supports close testing and exceptions |

If any link is missing, basic regulator or internal-control questions require manual reconstruction. A useful checkpoint is to verify completeness before auditors arrive and confirm end-to-end traceability while there is still time to close gaps.

Separate immutable proof from working notes#

Treat signed contracts, approval logs, risk snapshots, remediation records, payout references, and reconciliation exports as immutable or version-locked records. Keep investigation comments and outreach notes editable, but never let them replace original evidence.

If a record is corrected, preserve the original evidence, the correction date, and the newly approved record. If an assessment changes, retain the original and store the adjusted version separately with its own approver.

Set retrieval standards before you need them#

An evidence pack is not audit-ready until retrieval is tested. Set an internal retention schedule, assign repository ownership, and define how to pull a complete file for regulator inquiry, finance close review, or internal audit sampling.

Run retrieval checks before auditors arrive so gaps can be fixed in time. Organizations that maintain audit-ready documentation report 40% lower audit preparation effort compared with compiling evidence reactively.

Related reading: India Equalisation Levy: What Foreign Platforms Must Pay on Digital Advertising Services.

Assign ownership across legal tax finance and payments ops#

Assign a named owner to each high-risk decision so classification, withholding, and payout controls stay traceable. For each contractor file, define who is accountable for classification, who is accountable for Tax Deducted at Source (TDS), and who can approve payout release. Make everyone else explicitly consulted or informed.

Use a compact RACI template that covers only exposure-creating decisions:

| Decision | R | A | C | I |

|---|---|---|---|---|

| Contractor classification using control and integration tests | Legal | Legal lead | Tax, Finance, Payments Ops | Finance close owner |

| TDS determination and supporting record | Tax | Tax lead | Legal, Finance | Payments Ops |

| Payout approval after contract and tax checks | Finance or Payments Ops | Designated approver | Tax | Legal |

| Exception handling for blocked or failed payouts | Payments Ops | Payments Ops lead | Tax, Finance | Legal |

| Regulatory response | Legal and Tax | Named case owner | Finance, Payments Ops | Executive sponsor |

Treat this as an operating model and keep it consistent across approval workflows, exception handling, and retained evidence. A practical check is to sample recent payouts and confirm the classification memo, TDS record, and payout approval point to the same accountable roles.

Define legal-tax escalation before edge cases appear. If a case depends on interpretation of control, integration, or outcome-based terms, legal should log the risk view. Tax should record the withholding position against that view. If cross-border regulatory ambiguity appears, open a joint legal-tax review before release and keep the issue statement, owner, and decision trail in the file.

Run a regular control review (for example, monthly) to catch repeat overrides, unresolved data-quality gaps, and exceptions that remain open through month-end. Escalate patterns that suggest ongoing classification risk, since misclassification can later trigger back wages and statutory exposure.

For cross-border withholding decision points, see US-India Contractor Payment Withholding Decisions for Platforms.

Conclusion#

The control sequence should stay conservative: classify the relationship before money moves, define your PAN and TDS treatment before first payout, and use only payout rails your controls can govern. If any step is weak, the payment record can outrun the compliance record and make cleanup harder. Before volume grows, put three artifacts in place:

- a first-payment readiness checklist

- an exception matrix that defines block versus escalate

- an evidence pack that explains each payout end to end

A practical audit test is simple: take one recent payout and confirm a reviewer can trace it without side chats or memory. Keep the signed agreement, classification rationale, PAN/TDS decision support (where applicable), invoice, payout reference, and approval trail together.

Treat uncertainty as a stop signal, not an ops inconvenience. The source materials behind this article do not provide authoritative India-specific PAN, TDS, FEMA, or payout-rail rules, and one candidate source was inaccessible. Some accessible material is scoped to U.S. government-contractor equal-employment enforcement, not India contractor tax operations. If an India legal or tax point is interpretive, escalate early, document the reasoning, and avoid irreversible payout actions until you have a defensible decision.

Before scaling contractor volume in India, validate your exact market and program setup with Gruv so your controls match real capabilities Talk to Gruv.

Frequently Asked Questions

What is the minimum compliance sequence to hire and pay an independent contractor in India without avoidable gaps?

Start with classification before payment setup, then confirm the person is engaged as a self-employed individual or registered entity. Apply control and integration tests, complete PAN verification, sign a written outcome-based agreement, confirm GST-compliant invoicing, and set the TDS withholding approach before the first payout. Keep the records in one centralized file with clear approval ownership.

When should we block a contractor payout in India instead of paying and fixing later?

Block the payout when core compliance, payment, or audit-readiness elements are missing. Common triggers include unresolved PAN verification, unresolved TDS treatment, no signed outcome-based agreement, or unclear classification facts under the control and integration tests. Paying first can make later cleanup and audit defense harder.

How do we decide between INR bank transfer and UPI for contractor payouts?

Choose the rail your team can operate with reliable approval traceability and reconciliation to the contractor record. If a rail cannot support your required controls consistently, use the alternative path or pause for manual handling until controls are stable. This guide does not provide evidence-based performance differences between INR bank transfer and UPI.

What records should we retain to defend PAN and TDS decisions during audit?

Retain the records that show what you knew at payment time and who approved the decision. Keep the signed outcome-based agreement, classification record, PAN verification evidence, GST-compliant invoice, TDS support, payout reference, and approval trail in one centralized system. A reviewer should be able to follow one payout end to end from retained records alone.

When does contractor classification risk become serious enough to escalate to legal counsel?

Escalate when the working pattern no longer looks like independent, project-based work under the control and integration tests. The article describes the exposure as potentially including back wages and social-security-related liabilities such as PF, gratuity, ESI, and licensing issues. If the agreement and classification record do not clearly support independence, escalate before further payouts.

How should we handle cases where PAN data is missing or does not match contractor details?

Treat missing or mismatched PAN data as a high-risk exception and generally hold payment until it is corrected and reverified. Request corrected details, rerun verification, and preserve both the original and corrected records to maintain a clear audit trail. Do not use silent overrides that release payment without a defensible PAN basis for the TDS withholding position.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- cbp.gov/sites/default/files/documents/icp069_3.pdftrusted

- dol.gov/sites/dolgov/files/OALJ/PUBLIC/OFCCP/REFEREN...trusted

- ecfr.gov/current/title-25/chapter-V/part-900trusted

- ecfr.gov/current/title-45/subtitle-A/subchapter-B/par...trusted

- eeoc.gov/federal-sector/digest/digest-equal-employmen...trusted

- federalregister.gov/documents/2016/03/24/2016-06296/interpretati...trusted

- govinfo.gov/content/pkg/CHRG-115shrg24428/html/CHRG-115s...trusted

- gsa.gov/system/files/Alliant%203%20Master%20Contract...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: