Quick Answer

Use a five-model control framework and pick the lightest lane your facts can support. In hiring contractors Germany workflows, clear first release only after the classification memo, signed service agreement, and required tax/KYC records are complete and consistent with real working conditions. If files involve labor leasing, verify an AÜG licence and the separate leasing agreement before activation. Recheck renewals for supervision, schedule control, and dependency drift; when those signals persist, move the case to employee or EOR review.

Hiring contractors in Germany without guessing#

If you are hiring contractors in Germany, treat this as a control decision, not a paperwork exercise. The goal is to choose the right compliance control level for misclassification risk before first payout, then define when internal review should escalate.

- Use a risk-led, role-centric lens.

Start with the role and risk profile, not vendor convenience. Decide how much review sits between onboarding and activation, and keep your working model aligned with how the engagement actually operates.

- Apply it across shared owners, not in silos.

This guide is for compliance, legal, finance, and risk teams managing cross-border engagements. Keep ownership explicit at each checkpoint so classification decisions are reviewed, approved, and carried through to payout operations.

- Aim for an audit-ready decision record.

By the end of this process, you should be able to pick a control level, define escalation points, and document why a classification decision was made. Keep the record simple and complete: the fact pattern reviewed, decision owner, approval point, and any exceptions.

- Separate internal policy calls from counsel-required calls.

This content is informational only and does not replace legal, tax, or compliance advice. Your internal rules can set process gates, but edge cases and disputed facts should be escalated for specialist review early.

Use the rest of this guide with disciplined evidence handling. Gather the facts, involve the right stakeholders, and keep the basis for each decision. Facts can shift over time, so your controls should include re-checkpoints that trigger escalation when the working reality no longer matches the original classification decision. Related: Hiring Contractors in the Philippines: Compliance Payouts and Tax Obligations.

Selection criteria and who this list is for#

Choose your model with four filters, not gut feel. If facts are stable and low risk, start lean. If facts are mixed, changing, or hard to evidence, move to stronger controls early.

| Filter | Use this to assess | Escalate when |

|---|---|---|

| Scheinselbständigkeit exposure | Whether the engagement is clearly project-based and supports independent status | Facts are unclear or the setup starts to resemble dependent self-employment |

| Payout volume in EUR | Whether classification and required-document checks can stay consistent regardless of volume | Your process cannot maintain those checks reliably |

| Cross-functional maturity | Whether legal, compliance, finance, and operations hand off cleanly and can verify required records and documents before activation | Handoffs do not run cleanly or required records and documents cannot be verified before activation |

| Tolerance for manual review | Whether volume is low and fact patterns are clear enough for manual review | Exceptions pile up, documents are incomplete, or the operating reality changes after onboarding |

- Scheinselbständigkeit exposure

Start here. Borderline classification in Germany is not a one-click call, so treat unclear facts as an escalation signal. If the engagement is clearly project-based and supports independent status, a lighter model may work. If it starts to resemble dependent self-employment, escalate early.

- Payout volume in EUR

Payout volume does not determine legal status. Keep classification and required-document checks consistent regardless of volume, and escalate when your process cannot maintain those checks reliably.

- Cross-functional maturity

Use stronger controls when legal, compliance, finance, and operations do not hand off cleanly. Germany has mandatory requirements for engaging freelance or contract talent, and there is no single common payment approach. If your team cannot consistently verify required records and documents before activation, centralize review.

- Tolerance for manual review

Manual review can work when volume is low and fact patterns are clear. It can fail when exceptions pile up, documents are incomplete, or the operating reality changes after onboarding.

This list is for teams that need defensible service-agreement standards and repeatable document checks, not teams expecting an instant legal conclusion. If you use an employed-contractor or labor-leasing route, confirm the provider has the required AÜG licence and that a separate leasing agreement is in place between provider and client. If either is missing, stop and escalate.

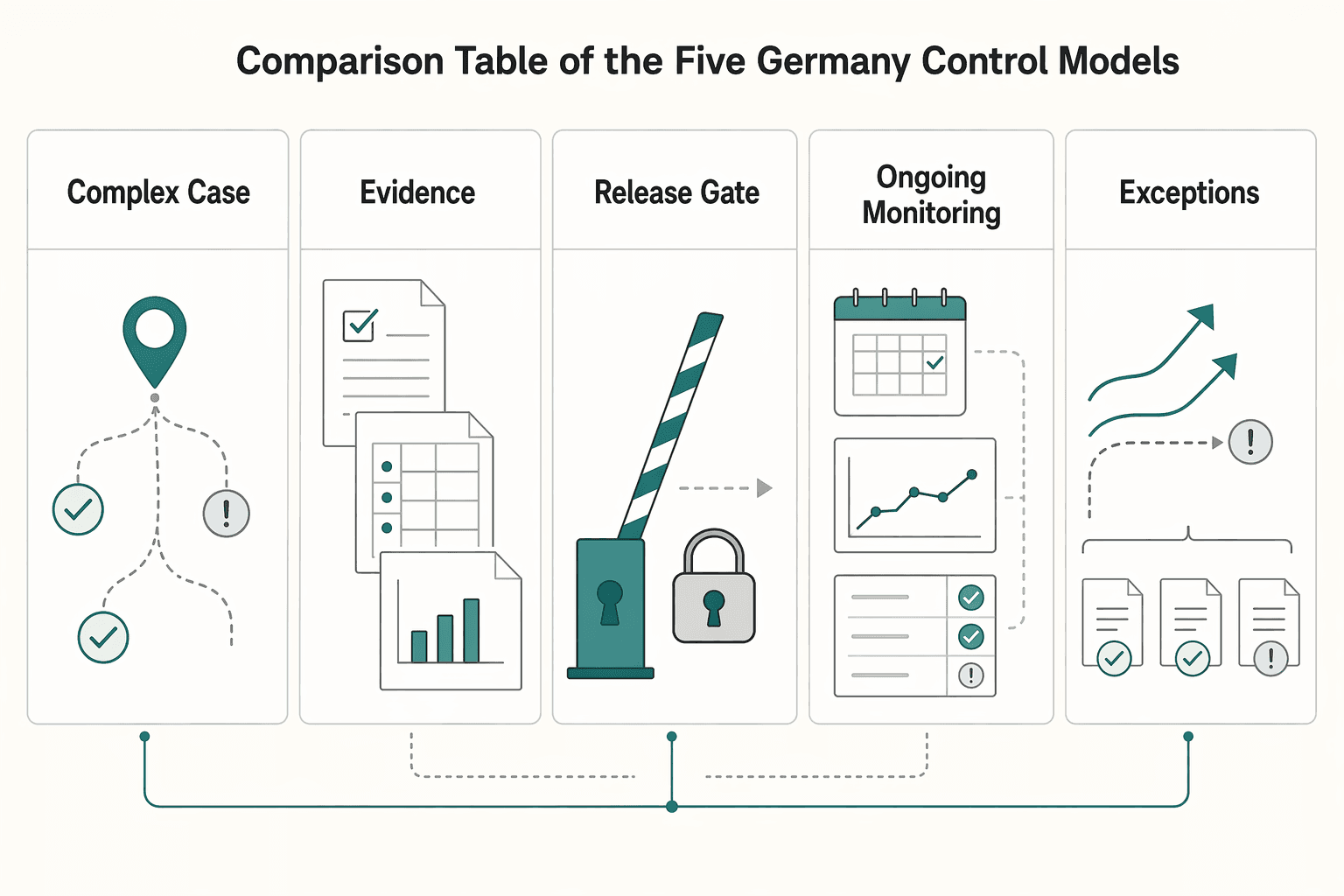

Comparison table of the five Germany control models#

Use the strongest model your current facts require before EUR payouts scale. Moving up early is usually easier than defending a weak record later.

There is no universal model here. The right choice depends on your actual exposure. That includes classification ambiguity, KYC and tax-form completeness, service-agreement quality, payout cadence, and whether you need a clean employee or EOR path if independent status no longer fits.

| Control model | Best for | Required artifacts | Escalation trigger | Tradeoff | Likely owner | Checkpoints |

|---|---|---|---|---|---|---|

| 1. Lean intake for low-volume, low-complexity cases | Clear project scope, low EUR payout frequency, and facts that support independent work | Basic classification screen, signed service agreement, identity/KYC completion, tax forms required for your payout flow, payout record setup | Missing contract, incomplete KYC, unclear business profile, or working pattern no longer matching the agreement | Fastest launch and lowest legal spend, but weakest defense if facts drift | Ops with compliance review | Before first payout: agreement signed, KYC complete, tax forms on file. Before repeated cycles: confirm payout pattern is still project-based, not payroll-like. Before conversion: document why contractor status no longer fits. |

| 2. Structured evidence-pack review | Mixed or changing facts, uneven documentation quality, or moderate misclassification concern | Classification memo, contract risk notes, role boundaries, approval log, retained onboarding records, KYC and tax-form checks | Contradictions between operating reality and contract terms, unclear independence, repeated documentation exceptions | Slower than lean intake, but stronger audit trail | Compliance with legal support | Before first payout: evidence pack approved and stored. Before repeated cycles: review whether scope, supervision, or dependency changed. Before conversion: use retained records to support counsel review and transition. |

| 3. Centralized pre-payout gate for high-volume EUR payouts | Frequent or recurring payouts where one weak decision can repeat quickly | Approved classification record, validated service agreement, KYC pass, tax forms verified, payout-release controls, exception-routing log | Any missing artifact at release, mismatch between work model and contract, repeated manual overrides | Strong prevention before money moves, but higher operational friction | Compliance and finance jointly | Before first payout: no release until required artifacts clear. Before repeated cycles: recheck exceptions, KYC changes, and payout cadence risk. Before conversion: freeze new cycles until the legal path is chosen. |

| 4. Ongoing monitoring and reclassification readiness | Programs with evolving scope, repeated renewals, or rising control over time | Initial classification file, periodic review notes, updated role description, service-agreement change log, payout history, exception history | Growing supervision, schedule control, role permanence, or economic dependency signals | Catches drift earlier, but needs disciplined recurring ownership | Compliance or legal, with ops input | Before first payout: baseline facts documented for later comparison. Before repeated cycles: periodic review completed on schedule. Before conversion: package original decision, current facts, agreement history, and payout records for final review. |

| 5. Conversion to employee or EOR escalation path | Cases where contractor status is hard to defend or no longer fits | Reclassification memo, transition approval, employee or EOR onboarding documents, contract termination or replacement documentation; where labor leasing may apply, confirm AÜG-related requirements with legal counsel | Persistent ambiguity, repeated exceptions, or employee-like control that cannot be corrected cleanly | Higher cost and longer onboarding, but often a clearer way to reduce long-tail misclassification exposure | Legal leads, HR/people or external EOR support, finance for changeover | Before first payout as employee/EOR worker: new employment basis is complete and documented. Before repeated payroll cycles: payroll, tax compliance, contracts, benefits, and labor-law responsibilities are assigned. Before conversion: set a decision date and stop treating the role as temporary ambiguity. |

Two practical calls matter most. First, once payouts become frequent in EUR, treat payout release as a real control gate, not a clerical step. Second, monitor for drift after onboarding, because weak evidence gets harder to defend over time.

When ambiguity does not resolve, model 5 is often the cleaner path. An EOR is a registered German legal entity that formally employs workers and can handle payroll, tax compliance, contracts, benefits, and labor-law requirements. A 2-4 week hiring timeline is a provider claim, not a guaranteed outcome. Employment decisions carry legal weight from day one.

Across all five models, a common failure mode is paperwork that no longer matches operations. That risk can be sharper in subcontracting-heavy setups. Fairwork notes the EU Platform Work Directive came into force at the end of 2024, with national transposition due by the end of 2026. If ownership is distributed and evidence is thin, the monitoring burden is likely to rise, not fall.

If you want a deeper dive, read The Agency Scaling Blueprint: From Solo Freelancer to Hiring Your First 5 Global Contractors.

If your team is locking down pre-payout controls and exception routing, review how a compliance-gated payout flow can support those checkpoints in practice: Explore Payouts.

Best for low-volume low-complexity onboarding#

Use this lean model only when the setup is genuinely simple and likely to stay that way. It fits a small contractor cohort with clearly defined deliverables and limited operational complexity. If day-to-day management starts to resemble standard employee oversight, this model is usually too weak.

When the lean model is a real fit#

A practical fit is a pilot with a small number of contractors engaged for defined project outcomes, not open-ended team capacity. Keep the scope and end conditions explicit from the start. Low volume alone is not protection if the operating reality drifts away from the original setup.

Minimum controls worth keeping even at low volume#

Even here, keep one minimum decision file before first payout:

- the decision date, owner, and indicators used for intake

- explicit thresholds for when the setup must be escalated

- a post-onboarding check to confirm the live arrangement still matches what was documented

Keep the gate simple: if the indicators or thresholds are unclear, do not activate payout until they are clarified.

Why teams start here, and where it breaks#

The appeal is obvious: speed and low admin overhead for narrow, early-stage use cases. The weakness is drift. Documents stay static while the working relationship changes.

Some vendor guidance makes the same point from another angle: self-service tools can leave teams exposed when follow-up checks are skipped. In this lean model, ongoing human review matters more than a longer intake form.

If facts stop looking simple, move quickly to a stronger evidence-pack review. If the role is clearly employment, shift to an employment path and decide between a local entity and EOR rather than piling on more contractor paperwork. In that employee-hiring context, source claims describe materially different effort and timing: an EOR is presented as a way to hire within days without entity setup, while GmbH setup is cited at 6+ months, €25,000 share capital, and roughly €10,000-€15,000 in legal and registration fees. On that same path, time recording and monthly minimum-wage checks are a baseline control, since variable hours plus weak tracking can pull realized hourly pay below the statutory floor.

This pairs well with our guide on Invoice Factoring for Contractors: How Platforms Offer Early Payment and Manage Risk.

Best for mixed contractor profiles with moderate risk#

When your contractor cohort is mixed and documentation quality is uneven, a documented review model is usually the right middle ground. If you are onboarding a mix of contractor profiles, treat that variance as a control signal and move beyond the lean approach early.

Worker classification depends on country-specific legal frameworks, and misclassification can lead to audits, back payments, and fines. In practice, that means one shortcut cannot be reused safely across files with different facts.

What changes at this level#

The main upgrade is a structured evidence pack that records why you are treating the person as an independent contractor and what controls support that decision. A workable internal pack can include:

- a classification memo with decision date, reviewer, known facts, and open questions

- contract risk notes on gaps, ambiguities, or terms that need revision

- role boundaries covering deliverables and operating expectations

- an approval log for onboarding clearance and exceptions

- retained onboarding records, for example tax forms, signed agreements, and key communications

These documents are not a guarantee on their own. Their value is the traceable record of how the decision was made.

The checkpoint that matters most#

For moderate-risk files, use one internal rule: if business structure or working pattern is unclear, pause activation and escalate before payouts begin. Also confirm that contracts, payroll, and tax handling are actively managed before the engagement scales.

Run one consistency check across intake details, contract terms, and planned operating reality. If they do not align, the file is not ready.

Why this model is worth the drag#

The downside is slower onboarding and more coordination across legal, compliance, finance, and operations. The upside is a stronger misclassification posture and a much cleaner audit trail.

That tradeoff is usually justified for mixed cohorts. If file quality is uneven but recoverable, this model is the practical middle ground. If facts are missing or contradictory, escalate early rather than approving on optimism.

For a fuller breakdown, read Vendor Approval Process for Platforms That Screen and Onboard Contractors.

Best for high-volume payouts where pre-payout controls matter#

For recurring, payroll-like contractor payouts in Germany, payout release can be a strong internal control. No payout until the file is complete, approved, and consistent with the actual working model. That is a practical guardrail for Scheinselbständigkeit risk, which depends on real working conditions, not contract wording alone.

This is a step up from documented review. You are not just creating a defensible file. You are making release depend on that file before first payout and before repeat EUR cycles scale a bad assumption.

The release order to use#

German law does not set one fixed internal sequence, but high-volume programs often define one. A workable order is: onboarding complete, worker classification approved, service agreement validated, internal policy checks and tax forms verified, then payout release.

| Gate | What should be true before release | Why it matters |

|---|---|---|

| Onboarding complete | Core identity, business details, payment method, and invoice path are captured | Incomplete intake creates avoidable exceptions later |

| Worker classification approved | A reviewer signs off on the facts and closes material questions | In Germany, real working conditions drive risk |

| Service agreement validated | The signed agreement matches scope, pay terms, independence, and termination logic | A clean contract does not help if day-to-day practice contradicts it |

| Internal checks and tax setup verified | Internal policy checks are complete and tax documentation is present; tax registration, VAT handling, and e-invoicing readiness are checked where relevant | Missing tax and invoicing artifacts become batch payout issues at scale |

| Payout release | All prior gates are green, or an exception is formally approved and logged | Prevents one weak file from becoming repeated payments |

For monthly cohorts, this keeps compliance from turning into post-payment cleanup. Give finance a bright-line rule: no first payout and no repeat payout on incomplete files unless an exception owner accepts it in writing.

The holds and exception routes that prevent drift#

Use automatic pre-payout holds for missing artifacts rather than relying on manual detection in chat or email. Hold release when classification approval is missing, the agreement is unsigned or outdated, internal policy checks are incomplete, or tax and invoicing records are not ready.

Also hold for inconsistency, not just absence. If the agreement says project-based work but the operations plan includes fixed weekly hours, manager approvals, or schedules that look employee-like, pause payout and reopen classification review before the next payment.

Route exceptions to a named compliance or legal owner with a short evidence pack: classification decision, current agreement version, key onboarding records, and the gate-failure reason. If that packet is hard to produce quickly, the control is not mature enough for high volume.

Operator details worth building in from day one#

At this level, keep exportable audit records for each release cycle: contractor ID, country, decision date, approver, agreement version, internal check status, tax form status, hold reason, and override reason when used. In a later review, you need to show what was checked before funds moved.

Tax and invoicing checks also need early attention. Contractors in Germany are expected to register with the tax office, handle VAT correctly, and meet mandatory e-invoicing requirements. If that setup is unclear, the same issue will repeat across invoices and payout cycles.

Add time recording and monthly checks where variable hours, day rates, or retainer structures start to behave like payroll. Weak tracking can pull realized hourly pay below the statutory floor, and Germany's statutory minimum wage is €13.90 per hour effective January 1, 2026.

Why the friction is usually worth it#

The benefit is straightforward: fewer preventable payout risk events, earlier detection of missing artifacts, and a cleaner audit trail if a relationship is challenged. That matters because misclassification exposure can include fines, retroactive social security liability for up to 30 years, and criminal exposure in intentional cases.

The tradeoff is tighter operational discipline. You need stronger SLAs, clear ownership across compliance, legal, finance, and operations, and much less tolerance for manual bypasses.

This model fits marketplaces paying recurring Germany contractors in EUR that run centralized compliance review and audit exports. If contract terms and operating reality diverge, freeze payout and re-review classification before money moves.

For a step-by-step walkthrough, see Enhanced Due Diligence for High-Risk Contractors: What Triggers EDD and How to Conduct It.

Best for ongoing monitoring and reclassification readiness#

Pre-payout gates handle the first decision. Ongoing review handles drift. For Germany engagements that renew, expand, or become embedded in daily operations, treat classification as a status you must keep validating against live facts, not a one-time approval.

This model fits programs where scope changes over time and the original classification can go stale. A practical internal standard is simple: if today's working reality no longer matches what was approved at onboarding, re-review is due.

What you should actually review#

Look at facts that show direction and control, not just whether a contract is still on file. The April 2025 European Labour Authority study highlights tools for assessing worker versus self-employed status and points to direction, control, and organisation as key concepts. That is a useful cue for internal review design. At minimum, reassess:

| Review area | Question to test |

|---|---|

| Supervision level | Is someone now directing how work is done, not only accepting outputs? |

| Schedule control | Has flexibility shifted to fixed hours, shifts, or required availability? |

| Dependency | Is the person now relying heavily on one platform or team for ongoing work? |

| Repeated renewals | Have short terms become a rolling arrangement without real re-scoping? |

| Role permanence | Does the role now look embedded rather than project-based? |

None of these items is a standalone legal trigger here. Use them to test whether the current operating model still matches the facts behind the original classification.

The review packet that makes this usable#

To make this work in practice, assign a recurring owner and standardize the evidence pack. Include the original classification record, current agreement version, renewal history, latest scope of work, recent invoices, and a short manager attestation on current supervision and scheduling.

That attestation can reveal drift early. If the agreement still describes independent project work but operations now run through standing meetings, approval chains, fixed coverage windows, or ongoing role expectations, the file is no longer internally consistent.

When to trigger reclassification review#

Trigger reclassification review as soon as operating reality no longer matches the original service agreement, and pause new renewals or scope expansion until the review closes.

The upside is early detection of status drift before outside scrutiny. The downside is the need for clear ownership and disciplined evidence retention. Misclassification risk carries financial and legal exposure, so stale decisions are expensive to leave untested.

We covered this in detail in How to Pay Contractors in Malaysia: DuitNow and Bank Negara FX Compliance for Platforms.

Best for conversion to employee or EOR escalation paths#

Use employee conversion or an EOR path when a contractor file stays in a gray area after review and the day-to-day setup keeps getting harder to defend as independent. This is an internal risk-control decision, not a fixed legal trigger under German law, and German misclassification thresholds should be confirmed with specialist counsel.

When this path makes sense#

This path fits recurring edge cases where ambiguity does not clear and exception requests keep pushing the role toward employee-like execution. Set internal triggers such as repeated exceptions and unresolved ambiguity after review, then escalate when the operating model keeps drifting away from clearly independent work.

If those signals keep showing up in the same file, pause renewal or scope expansion and open an employee or EOR review before the next pay cycle.

What the tradeoff really is#

The benefit can be lower long-tail exposure from keeping a borderline setup open too long. The cost is usually higher spend, longer onboarding, and more coordination across legal, payroll, finance, and HR. Treat conversion as a control outcome, not a failure case, when the role has materially changed.

A real escalation example#

A contractor starts with defined project deliverables and output-based invoicing, then shifts into a day-to-day model that is harder to defend as independent. At that point, focus on current operating facts, not just the original agreement.

Move the file into your employee or EOR decision track, document why the original model no longer fits, and route it to employee onboarding when that is the cleaner long-term option. If needed, hand off to How to Hire Your First Employee in Germany.

The cross-border checkpoint people miss#

If conversion creates a cross-border employment setup, run a social security coordination check immediately. Totalization agreements are designed to assign coverage to one country and exempt social security taxes in the other, and a common failure mode is dual social security taxation on the same earnings.

For U.S.-linked cases, include the appropriate proof artifacts for the chosen setup, such as a Certificate of Coverage where applicable. It can support an exemption from foreign social security taxes; treat worker-classification as a separate legal question.

Related reading: When Platforms File 1099 for Foreign Contractors and When W-8 Applies.

Contract terms to standardize in every Germany service agreement#

Standardize a short clause set in your Germany service agreements and treat it as a consistency control, not a cure for weak operating facts. Your day-to-day setup still has to match what the contract says.

| Clause area | What to standardize internally | What to verify before approval |

|---|---|---|

| Scope boundaries | Define the project, services, and what is out of scope. | Scope in the agreement matches intake, approvals, and requested work. |

| Deliverables | State what the contractor produces and how completion is identified. | Deliverables are specific enough for invoice review and not framed like an employee function. |

| Pay method and currency | Define payment mechanics, payment triggers, and payout currency, including Euro (EUR) when that is your chosen currency. | Finance setup, invoice rules, and contract terms use the same payment logic and currency. |

| Termination conditions | Set notice terms, offboarding steps, and handling of unfinished work, access, and final invoices. | Signed agreement contains executable termination language. |

| Dispute-handling language | Define how disputes are handled so escalation is not improvised later. | Legal has reviewed for consistency with your Germany contract standard. |

Match paper to practice#

The key control is alignment between the service agreement, classification review, and live working pattern. If those conflict, the contradiction matters more than polished wording.

That matters for worker-classification analysis and for the employee distinction referenced in public guidance as Arbeitnehmer. If scope or working patterns change, re-paper the relationship or reopen classification review before the next payout cycle.

What public guidance will not tell you#

Public vendor guidance is useful for themes, not definitive legal thresholds. In this source set, the accessible source (last updated January 31, 2025) frames Germany contractor hiring as requiring legal, tax, and compliance understanding. It does not provide a bright-line statutory Scheinselbständigkeit test or a definitive clause formula.

Use your standardized clause checklist for consistency. Escalate edge cases that need precise interpretation of German law to specialist review.

Make payout activation depend on complete documents#

Set one internal checkpoint: no payout activation until the signed agreement includes your required clauses and any tax documentation your process requires for that payee profile is present and approved. This is an internal control, not a claim that one universal German statutory document set applies to every contractor.

Before activation, run a three-way match across the signed agreement, onboarding record, and finance setup: legal name, service description, pay method, currency, and termination terms. Keep the signed version, approval record, and tax-document file together as the pre-payout evidence pack.

Red flags that require immediate legal or compliance escalation#

Escalate immediately when U.S.-Germany social security coverage cannot be shown clearly or when key coverage records conflict:

| Red flag | What the article says | Action |

|---|---|---|

| Cross-border coverage is unclear | Germany is listed by the U.S. Social Security Administration as a country with a Social Security agreement in force from December 1, 1979; these agreements are meant to assign coverage to one country | Escalate immediately |

| A coverage change is requested without current proof | If work facts that affect coverage change, pause approval until coverage evidence is updated; where U.S. coverage is being applied, require a Certificate of Coverage (COC) before proceeding | Pause approval until updated evidence is in place |

| COC submissions fail data checks | The online COC process includes checks for missing or mistyped information before transmission | Treat repeated data-check failures or incomplete submissions as an escalation trigger |

| A Germany classification call requires country-specific legal review | Confirm the bright-line Scheinselbständigkeit test and Germany-specific penalty thresholds with qualified legal counsel | Require legal or compliance review |

You might also find this useful: Gig Worker Tax Compliance at Scale: How Platforms Handle 1099s W-8s and DAC7 for 50000+ Contractors.

The practical next step for your team#

Your next move is to pick one control model for Germany now, assign clear owners, and define escalation triggers before onboarding the next contractor.

- Pick one control model and assign release authority

Choose the lightest model that fits your risk, payout volume, and team maturity, then apply it consistently for the next cohort. The key question is not the template set, but who can approve onboarding, who can block payout, and what facts force escalation. In Germany, status turns on the actual working relationship, not contract wording alone, so the named owner should confirm that the role still operates with genuine contractor autonomy.

- Set evidence checkpoints before optimizing speed

Build a defensible evidence pack first: classification record, service agreement quality, and pre-payment tax and invoicing checks. For Germany, confirm tax registration, VAT handling, and readiness for mandatory e-invoicing requirements before first payout. Keep one operating rule: no first payout until the evidence pack is complete and internally consistent, including work-authorization checks where relevant.

- Treat uncertainty as an escalation event, not a shortcut

If the working reality becomes unclear or drifts from the original setup, pause and escalate instead of trying to solve it in contract language. This is the practical control against Scheinselbstständigkeit risk. The downside can include fines, retroactive social-security exposure for up to 30 years, and possible criminal exposure in intentional cases. If these edge cases keep recurring, move the role into employee or EOR review, using How to Hire Your First Employee in Germany as the next path.

When your Germany contractor program is moving from ad hoc reviews to a formal control model, align on coverage and rollout constraints before implementation: Talk to Gruv.

Frequently Asked Questions

How do you hire an independent contractor in Germany compliantly without overbuilding process?

Use a lean process that still leaves clear evidence. Keep core checkpoints in place: a documented status assessment, a signed service agreement, and a pre-payout check that the live setup still preserves contractor autonomy. A template alone is not enough if the real working setup does not match the basics of an independent engagement.

What are the practical risks of misclassification and Scheinselbständigkeit for platforms?

The practical risk is financial and enforcement exposure, not just a labeling issue. Grounded consequences include social security back payments, fines, and possible criminal exposure. Risk rises when day-to-day working patterns no longer reflect contractor autonomy.

What must a Germany service agreement include at minimum?

At minimum, define scope clearly: specific tasks, deliverables, and deadlines. Also set pay rates or payment arrangements, project timeline, and termination conditions. In the Germany context, these arrangements are commonly documented as a Dienstvertrag or Werkvertrag.

When should a contractor in Germany be converted to employee status?

There is no universal conversion trigger, so this decision needs legal review when facts are mixed. Escalate when the role no longer shows real autonomy and starts operating like a permanent internal position. At that point, move to employee-hiring review, with How to Hire Your First Employee in Germany as a practical next step.

Which checks should happen before first payout versus during ongoing payroll cycles?

Before first payout, confirm the status assessment is documented, the service agreement is complete, and the engagement still reflects contractor autonomy. During ongoing payment cycles, rerun those checks when scope, timelines, or working-time expectations change. The goal is to catch drift early instead of assuming the initial setup stays compliant.

What key details are still unknown without country-specific legal advice?

Several high-impact points remain unresolved without Germany-specific counsel. Confirm the exact statutory test or weighting for Scheinselbständigkeit with a qualified adviser. Also confirm universal mandatory tax or KYC document lists, exact penalty amounts or interest percentages, and any one-size-fits-all conversion rule. Use internal controls for clear cases, and escalate edge cases rather than treating a template or simple process as a legal guarantee.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- acquisition.gov/sites/default/files/archives/loose_leaf/FAC_...trusted

- dau.edu/sites/default/files/Migrated/CopDocuments/Ac...trusted

- department.va.gov/procurement-acquisition-and-logistics/nation...trusted

- digitalcommons.law.uga.edu/cgi/viewcontent.cgitrusted

- dotd.la.gov/media/bognhjbv/contract-nos-4400032995-and-4...trusted

- eeoc.gov/best-practices-private-sector-employerstrusted

- eur-lex.europa.eu/legal-content/EN/TXT/HTMLtrusted

- federalregister.gov/documents/2025/01/15/2025-00636/framework-fo...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How to Hire Your First Employee in Germany

Moving from a tactical hiring checklist to a strategic market-entry playbook requires scanning the terrain for traps. Before you hire your first employee in Germany, you must understand a concept that poses a significant financial and legal risk to your global business: **Permanent Establishment**.

Agency Scaling Blueprint for Hiring Your First Global Contractors

Scale after you harden what already works. Before you write a job description, lock down the parts of the business that usually break first under growth: contracts, cash, worker status, delivery documentation, and how work gets reviewed. This blueprint is about adding capacity without adding avoidable risk.

Hiring Contractors in the Philippines with Compliance-First Payout Controls

If you are hiring contractors in the Philippines, set your compliance controls before onboarding starts. One common breakdown is not finding talent, but proving during an audit, dispute, or internal review that the working relationship, contract terms, payout trail, and tax handling still line up.