Quick Answer

Separate classification, payout, and evidence controls first, then hold payment release when role design or operating reality is unclear. For hiring contractors in the Philippines, the practical path is to decide the engagement model early, lock a complete agreement pack (scope, acceptance, invoicing, termination), and pay only when invoices, approvals, and transfer records align. Keep open tax and BIR issues on a tracked register and escalate low-confidence cases to local counsel before scaling.

What compliant contractor payouts require in the Philippines#

If you are hiring contractors in the Philippines, set your compliance controls before onboarding starts. One common breakdown is not finding talent, but proving during an audit, dispute, or internal review that the working relationship, contract terms, payout trail, and tax handling still line up.

This guide takes a control-first view for compliance, legal, finance, and payments teams. The aim is practical: make a few early decisions well enough that you avoid preventable tax and compliance problems later.

In the Philippines, hiring guidance treats labor regulation and tax compliance as core requirements alongside recruiting. For employer routes, that includes Philippine Labor Code compliance, Bureau of Internal Revenue (BIR) registration, and mandatory contributions. Even if you plan to engage contractors, that is still a useful signal. The structure you choose changes cost, compliance burden, and timeline. Read the rest of this article through three separate risk lanes:

- classification risk: the real working relationship does not match contractor treatment

- payout execution risk: payment operations create avoidable exceptions

- documentation and audit risk: you cannot clearly prove what was agreed, approved, and paid

Keep those lanes separate. It is easy to optimize payout speed first and leave classification unresolved, but unclear classification can increase compliance exposure quickly.

Before the first payout, pressure-test your evidence pack. As a practical checkpoint, include a signed agreement and clear terms on compensation, work hours, leave, and termination conditions. If the paperwork and day-to-day operating reality do not match, your position is harder to defend in review.

Working recommendation: decide the engagement model before you scale, keep documentation defensible from day one, and escalate unclear legal boundaries to local counsel before volume grows. This is an operational explainer, not jurisdiction-specific legal advice.

Related reading: How to Pay Contractors in India: FEMA Compliance TDS Deduction and Bank Transfer Mechanics.

Start with the risk model your team will operate#

Use one shared risk model before onboarding. Keep classification, payout execution, and documentation/audit as separate control lanes from the start.

Start by setting definitions so legal, finance, and operations are working from the same frame. For internal risk review, treat contractor misclassification as a mismatch between contract terms and day-to-day working conditions. An independent contractor agreement is important evidence, but this section does not assume that agreement alone is sufficient under Philippine law.

For Philippines engagements, assign clear ownership to each lane early:

- Classification risk: does the actual working relationship still align with contractor treatment?

- Payout execution risk: can payments run accurately, traceably, and without repeated exceptions?

- Documentation and audit risk: can you show what was agreed, approved, invoiced, and paid?

Keep those lanes separate in practice. A payout failure is not automatically a classification issue, and a worker-status concern is not just a finance exception. When teams collapse these checks into one onboarding step, problems become harder to isolate and may surface later as disputes or urgent cleanup.

Your practical objective is simple: reduce surprise exposure and exception work without turning onboarding into a legal bottleneck. This conservative approach fits a known gig-work tradeoff: these models can improve productivity while also increasing worker vulnerability in some arrangements. Before first payout, confirm that the role summary, contract scope, approval path, and invoicing method all tell the same story. If the classification facts are unclear, escalate early with local counsel before volume scales.

If you want a deeper dive, read How to Pay Contractors in the Philippines: InstaPay PESONet and BIR Compliance for Platforms.

Use market demand signals carefully#

Treat Jobstreet and LinkedIn as hiring context, not compliance evidence. They can help you gauge hiring activity, but they do not prove that a Philippines engagement is correctly structured as contractor work.

| Signal | Period | Change |

|---|---|---|

| Employment | December 2025 to January 2026 | Fell by 1.489 million |

| Unemployment | Year over year | Rose to 5.8% from 4.3% |

| Wage and salary employment | Year over year | Increased by 2.408 million to 32.96 million |

Do not force headline posting volume into a single proof point. If platform snapshots appear to disagree, record that inconsistency directly and keep it out of classification, tax, and worker-status decisions.

Before you use any platform signal operationally, anchor it to an official checkpoint. That checkpoint is the Philippine Statistics Authority January 2026 Labor Force Survey, which DOLE framed in a post-holiday seasonal slowdown context. One-period readings can mislead. Employment fell by 1.489 million from December 2025 to January 2026. Unemployment rose to 5.8% from 4.3% year over year. Wage and salary employment still increased by 2.408 million year over year to 32.96 million. Labor signals can move in different directions at the same time.

For each hiring push, keep a small evidence pack:

- platform name, pull date, and geography filter

- matching PSA or DOLE reference period

- label: planning context only, not classification support

Use location signals the same way. Location-level listing concentration can inform sourcing plans, interview coverage, onboarding support hours, and payout operations capacity. It should not be used to justify contractor treatment. If that argument starts to creep in, move the discussion back to role design and actual working conditions.

Make the contractor classification decision before onboarding#

Make the classification call before onboarding, because an Independent contractor agreement does not by itself repair a role that is operated like an employee position.

The core distinction is straightforward. An employee works for an employer for wages or other remuneration, while a contractor provides services without being treated as that business's employee. Misclassification can create back-tax and fine exposure. It can also deprive workers of protections and statutory benefits.

Build the decision at the role level first#

Start with role design, not candidate-by-candidate judgment. Use one pre-hire decision record per Philippines role so Legal, Compliance, Finance, and hiring managers review the same facts.

| Decision area | Contractor-side indicator | Employee-like indicator | What to verify before approval |

|---|---|---|---|

| How work gets done | Worker has autonomy over how to complete the work | Manager directs day-to-day methods and steps | Role summary is outcome-based, not supervision-based |

| When work gets done | Worker has meaningful control over timing | Company-set timing controls are built into the role | Hiring manager documents expected timing and flexibility |

| Team control | Relationship is centered on services and deliverables | Role is embedded in ongoing internal team control | Review cadence and approver are documented |

| Payment basis | Payment terms are tied to the Independent contractor agreement | Payment setup is not aligned to agreed service terms | Agreement and payment terms match |

This is a control framework, not a legal test. Confirm any official weighting formula or government threshold with the relevant authority. One current comparator is the U.S. Department of Labor's proposed independent-contractor analysis, but it is not a Philippines rule.

Treat control-heavy design as a pause point#

If role design depends on ongoing supervision, fixed schedules, or embedded team control, pause and escalate for legal review before issuing an Independent contractor agreement.

Keep the escalation note specific: role summary, reporting line, expected hours, if any, review cadence, tool access, and why contractor treatment is still being proposed. Low-confidence cases should go to qualified counsel, especially since the external materials used here explicitly state they are not legal, tax, or compliance advice.

Hold payouts until the file supports the classification path#

Use a clear internal checkpoint: if classification confidence is low, pause first payout until the review is completed and documented.

Before payout, confirm that payment terms are tied to the independent contractor agreement. If scope, deliverables, acceptance, and invoicing terms are not settled, the engagement is not ready for payout. A short delay on an unclear case may be lower risk than correcting a misclassified setup after payments and operating patterns are already in motion.

This pairs well with our guide on Enhanced Due Diligence for High-Risk Contractors: What Triggers EDD and How to Conduct It.

Draft agreements and evidence so they hold up under review#

Once you classify the role as a contractor, build the file so it can stand up to review in both contract language and operating records. Do not rely on the Independent contractor agreement by itself.

Build an internal minimum pack#

Use an internal agreement pack that documents the service relationship: signed Independent contractor agreement, written scope, deliverables, acceptance criteria, invoicing rules, and termination terms. Treat this as an operational control, not a claim that every item is legally required in all cases.

For Philippines engagements, keep the file consistent with a service-provider model. Payment terms should align to project-based results or accepted work, and the supporting records should reflect that setup.

| Document | What it should define | What evidence should align |

|---|---|---|

| Independent contractor agreement | Service relationship and core payment/commercial terms | Scope, invoices, payout setup |

| Scope/SOW | Deliverables and timing | Change requests, approvals, accepted output |

| Acceptance criteria | How completion is approved | Sign-off and invoice approval trail |

| Invoicing rules | Submission requirements | Compliant invoice and payout reference |

| Termination terms | Exit and unfinished-work handling | Final invoice and closure record |

If scope changes materially, document it before you approve the next invoice.

Match contract language to operating evidence#

In review scenarios, signed documents and operating records are often checked together. Keep approval logs, change requests, invoice approvals, and payout references with the agreement file so the story stays consistent.

One practical checkpoint from the source material is contractor BIR registration plus compliant invoicing. Before first payout, confirm that the invoice can be issued compliantly and maps back to the agreement and approval trail.

Control the result, not the person#

Use controls on outputs, acceptance, and invoicing, but avoid direct day-to-day management. When working arrangements shift from project-based results to direct management, contractor misclassification risk rises and may trigger what the source describes as Control Test exposure.

If the working model starts to look like direct management, pause and escalate classification review instead of trying to fix the issue with tighter contract wording.

Put one owner on retention and retrieval#

Assign one Finance or Compliance owner to document retention and retrieval. This is an operational recommendation, not a legal requirement claim.

Centralized records can help reduce misclassification risk and keep contractor documentation audit-ready. If contracts, approvals, invoices, and payout references are scattered across tools, retrieval gets harder during review.

Choose payout rails based on control, not convenience#

Choose the rail you can document end to end before you optimize for speed. Only Wise has verified pricing evidence on record. Treat other options as validation items until you collect equivalent proof.

| Payout option | What is verified from the sources | What you still need to validate |

|---|---|---|

| Bank transfer via International money transfer service | No provider-specific facts are verified in the provided material | Corridor pricing, exchange-rate treatment, reference fields, return handling, export quality |

| Wise Business | Wise states usage-based pricing with no subscription plans, says it uses the mid-market rate, shows fees from 0.57%, notes fees vary by currency, and provides a regulator's standardized format view; the page also shows Switch to Wise Business | Business setup details, payout batch behavior, reconciliation fields, corridor-specific costs for your currencies |

| BatchTransfer | No verified facts in the provided material | Pricing model, controls, limits, references, return handling, export format |

Set currency policy by cohort, then keep the contract, invoice, and payout records aligned to that policy. If you use PHP for a cohort, validate that flow in a pilot. If you use USD, validate the same controls for USD. The sources provided do not establish that PHP is inherently more predictable than USD in the Philippines.

Define failure handling before first batch volume. For returned payments, beneficiary mismatch, and delayed settlement, set internal ownership and SLA targets as policy choices. The sources do not establish specific SLA values or ownership models.

Pick the rail that makes reconciliation repeatable. Run a test payout and confirm that you can retain one linked record set: approved invoice, payout instruction, provider confirmation, and ledger reference. For Wise, keep a pricing capture from the business path plus the regulator-format fee view as part of your control file.

Related: How to Pay Contractors in Southeast Asia: Philippines Indonesia Thailand Vietnam.

Sequence compliance gates from intake to first payout#

Sequence is the control. Set the gates before the first disbursement so missing documents show up before money moves.

Lock the order before payment requests#

Use one fixed order and require evidence at each step.

| Step | What is recorded | Note |

|---|---|---|

| Contract | Signed and returned before performance | 1 copy is returned to the issuing office |

| Invoice routing | Invoices go to a specified address | An addendum can change the address |

| Acceptance | Recorded as conforming except as noted | Exceptions should be noted in the acceptance record |

| Payment status | Tracked by status | Use complete, partial, or final |

A grounded model is the staged form pattern used in FAR Part 52. The contract is signed and returned before performance, with 1 copy returned to the issuing office. Invoices go to a specified address unless an addendum changes it. Acceptance is recorded as conforming except as noted, and payment is tracked by status (complete, partial, final). The source is not Philippines contractor law, but the sequencing discipline is still useful.

Before release, confirm that the signed agreement, invoice path (including any addendum changes), acceptance record, and payment status are aligned.

Put policy gates before payout release#

KYC, KYB, AML, sanctions, and fraud checks are not established by the provided excerpts. If your internal policy includes them, define and run those gates before payment approval.

Keep exceptions explicit. Route them to a named approver, record the reason, and require re-approval if the exception remains open in the next cycle.

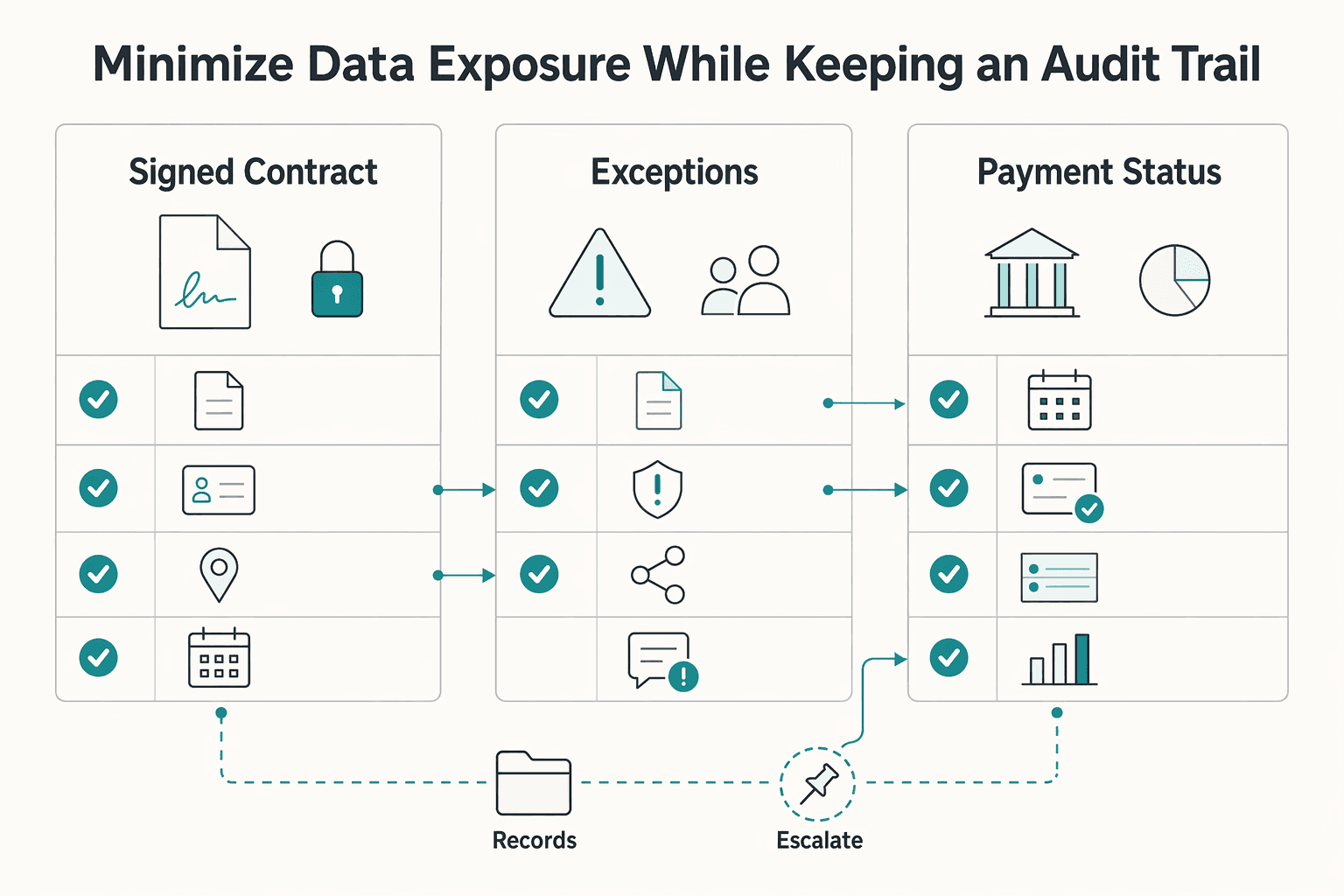

Minimize data exposure while keeping an audit trail#

Data minimization and role-based access controls are not specified in the provided excerpts, so treat them as internal control choices rather than source-backed requirements.

A practical first-payout pack, grounded in the provided form pattern, is:

- signed contract (returned copy)

- invoice routing details, including any addendum exception

- acceptance record, including exceptions noted

- payment status (

complete,partial,final)

If a required link is missing, resolve it before you scale volume.

For a step-by-step walkthrough, see Gig Worker Tax Compliance at Scale: How Platforms Handle 1099s W-8s and DAC7 for 50000+ Contractors.

Build a reporting checklist finance and legal can actually run#

Use one recurring Philippines report as a release control. If exceptions stay open, do not launch new hiring volume. Finance and legal should be able to answer four questions from one pack each period: onboarding status, contract completeness, payout exceptions, and unresolved compliance or tax flags.

| Report line | What complete means | Verification evidence |

|---|---|---|

| Onboarding status | Pre-payment checklist is complete before first payment | Intake and compliance records, payout-method record, required documents |

| Contract completeness | Written contract is signed and specific (scope, payment terms, IP, termination), and tax classification is documented | Executed agreement, tax classification file, and W-8BEN if relevant for a U.S. company |

| Payout exceptions | Exceptions are recorded and tied to the original payment record | Payment record, payout confirmation, invoice, and remittance evidence where applicable |

| Unresolved compliance flags | Red flags and tax questions are assigned to named owners and tracked to decision | Exception/risk log with owner, status, and decision note |

Keep the tax-risk register beside this checklist, not in a separate thread. Track potential tax liabilities, open advisory questions, owner, and escalation path.

Log BIR uncertainty explicitly as an open item. The provided materials are not fully aligned. One statement says you probably do not need BIR registration, while another says contractors working for foreign clients are supposed to register with the Bureau of Internal Revenue. Treat that as an issue to resolve with qualified legal or tax advice, not as settled policy.

Track misclassification risk the same way. If real working conditions drift from contractor treatment, keep it open as a compliance risk because the sources flag potential back-pay liabilities and penalties.

For reconciliation, keep payment records identifiable by source and route. Then tie each payment to the contract, invoice, payout record, and exception log.

Final gate: no new hiring wave launches until prior-period exceptions are closed or formally risk-accepted.

If you are turning this checklist into an operating runbook, compare your control points with Gruv Payouts to ensure statuses, exceptions, and payout references stay traceable.

Define escalation triggers before issues happen#

Escalate on patterns, material changes, and unresolved uncertainty, not one-off noise. Most contract risk appears during execution, and missed obligations can stay hidden until an audit or regulatory review.

Escalate when work reality drifts from the agreement#

Treat repeated gaps between contract terms and day-to-day practice as an escalation trigger. A signed agreement helps, but it does not resolve a mismatch between written terms and operating behavior.

If your records show ongoing practice patterns that conflict with deliverables-based terms, route the case to Legal and document why current practice does or does not still match the agreement.

Before expanding that role cohort, run a contract-first check. Contract terms, scope, change history, and operating evidence should align in writing.

Escalate when payout behavior changes materially#

Repeated payment exceptions or unresolved payout disputes should move out of routine operations. Repetition usually means your payout setup, contract terms, or reconciliation controls are out of sync with actual execution.

When issues repeat, Operations should verify the payment chain end to end: invoice, contract payment terms, payout records, and ledger entry.

If a payout dispute becomes a pricing-adjustment request, treat it as a contract interpretation issue first. The first checkpoint is what the contract says about price adjustments. If terms are fixed-price and allocate cost risk to the contractor, do not approve ad hoc adjustments without review.

Escalate unknown legal or tax points as risks, not questions#

Handle unresolved legal or tax points as active risks. Ambiguity in reporting or tax treatment may become visible only during audit, so delay is a control failure, not a neutral state.

Assign each issue to a named owner with a decision date, then track it to closure. Unclear ownership is how issues get passed around without resolution.

Keep the evidence pack small but complete:

- exact unresolved question

- affected contractors and related payments

- contract version and payout method used

- open deadlines, owner, and interim action

One practical way to route by issue type is:

- Operations: execution fixes (payment exceptions, reconciliation breaks)

- Legal: contract-practice conflicts, disputed terms

- Tax: reporting exposure, remittance questions, year-end treatment concerns

If an issue spans multiple lanes, assign one primary owner anyway. Ownership clarity is a core control, not admin overhead.

Avoid the common mistakes seen in generic hiring guides#

Use generic hiring content as context, not as your compliance decision. A common failure is treating marketing-style guidance and cost framing as if they were a complete Philippines-specific legal position.

One published guide captures the tension directly: it promotes EOR as the smart way to hire remotely while also stating that the legal market is layered and specific. Read material like that as commercial input, then validate your actual classification and documentation controls separately.

Another mistake is letting reduced Federal payroll taxes drive the whole decision. That cost framing may matter, but it does not replace paperwork controls. The risk to keep in view is misclassification, which can create exposure to back pay, benefits, penalties, and employee entitlements such as 13th month pay.

Treat your Independent contractor agreement as a starting control, not a complete defense. Written terms help reduce confusion on responsibilities, compensation, and benefits, but contracts and paperwork still need to stay in order.

Do not wait for a dispute to rebuild records. Keep a live evidence pack from day one:

- final signed agreement and current scope

- compensation terms, invoices, and payout records

- documented updates when duties or pricing change

If your records cannot show what was agreed, what changed, and what was paid, you are already in retroactive defense mode.

Execute a practical first 30-day rollout#

In the first 30 days, prioritize traceable controls over scale. Your role design, contract records, and payout records should match how work is actually managed day to day.

| Week | Focus | Checkpoint |

|---|---|---|

| Week 1 | Define role cohorts and escalation ownership | Review real manager instructions; if managers are directing day-to-day work, rostering, or team integration, escalate before onboarding |

| Week 2 | Standardize the evidence pack and set currency policy by cohort | Keep agreements, scope, compensation terms, and payout records aligned; there is no stated rule that mandates PHP or USD |

| Week 3 | Run a controlled pilot cohort | Track exception rates and test end-to-end traceability on completed payouts |

| Week 4 | Publish the standing checklist and finalize review cadence | Include unresolved classification questions and open statutory review items; route employee-like cases for review of payroll taxes, SSS, PhilHealth, Pag-IBIG, and 13th-month pay |

Week 1#

Start by defining small role cohorts in the Philippines based on real operating patterns, not job titles alone. If work is ongoing, controlled, and integrated into team routines, treat that as a higher-risk classification pattern and escalate before onboarding.

Set escalation ownership up front. When a case is unclear, pause and route it to Legal or Compliance rather than forcing it through as a standard contractor setup.

Use a practical checkpoint this week: review real manager instructions in early cases. If managers are directing day-to-day work, rostering, or team integration, contract wording alone is unlikely to support the classification decision.

Week 2#

Standardize the evidence pack before volume grows. At minimum, keep agreements, scope, compensation terms, and payout records aligned with how work is actually being performed.

Set any currency policy by cohort as a finance control, not a legal shortcut. Confirm whether any rule mandates PHP or USD with the relevant authority, and choose the option your team can reconcile and document exceptions.

Watch for mismatch risk. If written terms and payment behavior diverge from operational reality, treat it as an escalation trigger because misclassification risk increases.

Week 3#

Run a controlled pilot cohort and track exception rates closely. Focus reviews on record gaps and payout activity that cannot be tied cleanly to authorized work.

Test end-to-end traceability on completed payouts. Also test classification reality, not just paperwork. If day-to-day direction and integration look employee-like, escalate immediately.

Week 4#

Publish a standing checklist that Finance and Legal can run each cycle. Include unresolved classification questions, open statutory review items, and real-time compliance monitoring for active cases.

Finalize escalation ownership and review cadence while volume is still manageable. If a case starts to look employee-like, route it for review of statutory obligations such as payroll taxes, SSS, PhilHealth, Pag-IBIG, and 13th-month pay.

Expand only when prior exceptions are closed or formally accepted. In this first month, prioritize traceability and control before speed.

Conclusion#

The durable approach is to hire with controls, not speed: make the classification call early, keep documentation consistent, and release payouts only when the record is traceable.

Misclassification risk usually comes from how the engagement is run, not from contract wording alone. If work shifts from project-based results to direct management, you are moving toward Control Test risk. If a manager asks for strict hours, employee-style performance standards, or long-term commitments, pause and escalate before first payout.

Before you scale volume, enforce one minimum evidence standard across every contractor file. At minimum, keep a complete contract record, documentary proof, and audit-ready reporting so another reviewer can reconstruct the case without relying on memory.

The bar should be audit-ready, not just operationally convenient. In practice, that means keeping documentary proof and reporting discipline while avoiding assumptions that employee obligations automatically apply to contractor arrangements.

The tradeoff is straightforward: the contractor model stays lean only when compliance ownership is explicit. As volume grows, weak ownership and inconsistent controls become expensive, and adjacent employment operations often show the same pattern through remittance and year-end processing failures.

Implement the checklist and escalation map first, then run a limited Philippines pilot. Expand only after the pilot shows clean documentation, traceable payout records, and no unmanaged Control Test signals. If you can show clear decision rules, a complete evidence pack, and defined escalation triggers, you reduce regulatory surprise without making operations heavy.

Before scaling beyond your pilot cohort, run a final controls gap review using Gruv Docs so legal, finance, and ops are aligned on implementation details.

Frequently Asked Questions

What is the biggest compliance risk when hiring contractors in the Philippines?

The biggest risk is misclassification. If an independent contractor arrangement is found invalid, the worker can be treated as an employee of the client or principal. In validity disputes, regular employment is presumed unless disproven, and the employer carries that proof burden.

Is hiring contractors in the Philippines always cheaper than hiring employees?

No. Cost outcomes are case-specific, and a contractor setup is not automatically cheaper. If the arrangement is later treated as employment, the financial impact can outweigh expected savings.

What should be in an independent contractor agreement for Philippines engagements?

Do not treat a signed agreement as a complete risk shield. If the arrangement is questioned, the employer must be able to prove the contractor setup is valid. Keep the agreement and supporting records clear enough to substantiate that position.

Which payout method is better for contractor batches: bank transfer rails or tools like Wise Business BatchTransfer?

Neither is automatically better. Validate costs against current provider documents, not assumptions. Wise states that pricing is usage-based, and fees vary by product, currency, and payment type, so confirm the actual economics against your payout pattern before you scale.

Do public hiring pages provide enough detail for legal and tax decisions?

No. Public hiring pages can be useful market context, but they are not legal or tax authority. Do not use them as the basis for classification or tax decisions.

What should we do when classification or tax rules are unclear for a specific contractor case?

Pause and escalate. Route unclear cases to Legal or Tax before treating them as standard contractor onboarding. Document the open issue and wait for a clear decision and risk owner before first payout.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- acquisition.gov/far/part-52trusted

- board.oc.gov/sites/bos.egovoc.com/files/2020-03/rev-sup03...trusted

- dnr.maryland.gov/fisheries/documents/fao%202006%20mpa.pdftrusted

- federalregister.gov/documents/2026/02/27/2026-03962/employee-or-...trusted

- file.lacounty.gov/SDSInter/bos/bc/1033102_TempServicesBoardLet...trusted

- file.lacounty.gov/SDSInter/bos/supdocs/213493.pdftrusted

- govinfo.gov/content/pkg/CHRG-106shrg62810/html/CHRG-106s...trusted

- hr.uw.edu/labor/staff-unions/seiu-925/contracttrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Pay Contractors in the Philippines with InstaPay PESONet and BIR Clarity

Treat Philippines contractor payouts as a launch decision, not a checkout feature. The real go or no-go question is whether you can name the compliance owner, choose a payout path you can actually support, and prove what happened on every payment before volume hides mistakes.

Southeast Asia Contractor Payouts Across Philippines, Indonesia, Thailand, and Vietnam

Treat Southeast Asia as four separate launch decisions, not one regional rollout. If you approach the Philippines, Indonesia, Thailand, and Vietnam with a single APAC payout template, you can create avoidable rework in compliance, rail selection, and reconciliation.

Agency Scaling Blueprint for Hiring Your First Global Contractors

Scale after you harden what already works. Before you write a job description, lock down the parts of the business that usually break first under growth: contracts, cash, worker status, delivery documentation, and how work gets reviewed. This blueprint is about adding capacity without adding avoidable risk.