Quick Answer

To launch contractor payouts in the Philippines safely, define who owns BIR filing, payment, recordkeeping, and exceptions before choosing InstaPay or PESONet. Then validate the filing channel, keep traceable payout evidence for every transfer, and leave any unverified rail behavior, fallback handling, or classification issue in pilot until it is confirmed.

Why this guide matters for platform operators expanding into the Philippines#

Treat Philippines contractor payouts as a launch decision, not a checkout feature. The real go or no-go question is whether you can name the compliance owner, choose a payout path you can actually support, and prove what happened on every payment before volume hides mistakes.

Set the decision boundary#

This guide is for operators deciding whether they can launch contractor payouts in the Philippines with acceptable operational risk. It is not a general HR explainer, and it does not treat contractor payments as a simple bank-transfer problem. In this market, payment design and tax handling sit close together.

That framing matters because the public context cuts both ways. The Bangko Sentral ng Pilipinas January 2026 presentation includes a section called "Strong Foundation for Digital Payments." The same deck also says "Complete reforms strengthen the tax system." In practice, that means local payout options like InstaPay and PESONet cannot be evaluated in isolation from BIR-facing responsibilities.

Verification point: before you scope engineering, write down the exact question you are answering: "Can we launch contractor payouts in the Philippines with named tax ownership, traceable payment evidence, and documented exception handling?"

Connect BIR responsibility to payout design#

A common expansion mistake is treating contractor status as a reason to postpone tax design. Start from the opposite assumption: if you do not define who owns Bureau of Internal Revenue (BIR) obligations, your payout design will drift into unsupported manual work.

One freelancer-focused source is blunt that BIR registration is a legal requirement, and that people handling payments independently may be "fully responsible for tax compliance." That does not tell you every platform duty, but it is enough to rule out hand-waving. In practice, BIR questions shape what you collect at onboarding, what references you attach to payouts, what reconciliation output finance needs, and what support can explain when a contractor asks for proof.

If you cannot say who handles filing, payment, records, and exception review, do not launch the lane yet. Red flag: a product spec that names a rail but not the owner of tax filing, payment records, or fallback handling.

Define the outcome you need from this guide#

By the end, you should have three things: a practical sequencing path, a shortlist of validation items, and an operator-grade checklist. That includes explicit unknowns. If rail behavior, beneficiary coverage, or BIR process ownership is still unconfirmed, mark it as "must validate before production" instead of filling the gap with assumptions.

The useful outcome is not theoretical completeness. It is a decision you can act on: launch a pilot, pause until ownership is assigned, or limit scope to one controlled payout path while you verify missing pieces. That is the standard this guide is built for.

For a fuller walkthrough, see How Independent Contractors Should Use Deel for International Payments, Records, and Compliance.

What to prepare before you design payout flows#

Set your operating rules before anyone designs the payout UX. Align classification, compliance ownership, and payment evidence first so product decisions do not outrun operational reality.

- Define your contractor model and screening standard.

Document who qualifies for your contractor lane, what onboarding inputs you require, and who reviews exceptions. If local worker-classification tests apply to your model, capture how your team will apply them and how approval decisions are recorded.

- Name tax and compliance ownership up front.

Build a simple responsibility map for filing, recordkeeping, contractor support questions, and payout execution. If your platform only executes payouts, state that boundary clearly so product, finance, and support are not working from different assumptions.

- Inventory rails you can support now.

Keep a short matrix for InstaPay and PESONet with current provider support, required beneficiary data, and exception ownership. The World Bank Philippines retail-payments technical note treats PESONet, InstaPay, and the Legal and Regulatory Framework as distinct areas, so rail selection should be handled as an operating decision, not just a UI choice.

- Define payout evidence outputs before integration.

Agree on the minimum records each payout cycle must produce, such as status history, approval trail, provider reference, and reconciliation-ready output. This avoids mismatches where a payout appears complete in one system but cannot be verified across teams.

For a policy template, see How to Write a Payments and Compliance Policy for Your Gig Platform.

Set your compliance boundary before you pick rails#

Set the compliance boundary before rail selection: if ownership is unclear at any BIR step, you are not ready to launch that payout path.

Step 1. Use primary-source validation before assigning final ownership. Treat Revenue Memorandum Circular No. 087-2024 and Revenue Regulations No. 4-2024 as validation gates, not as shorthand for requirements. Keep ownership provisional until primary text or reviewed legal notes confirm what either one requires, allows, or exempts.

Step 2. Start with a provisional tax-responsibility split, then verify. A grounded starting point from Globalli is that Filipino contractors handle their own tax obligations, and foreign companies paying contractors do not need to withhold payroll taxes. Use that only as an initial operating boundary, not as definitive BIR legal guidance.

Step 3. Define channel scope without guessing channel rules. List eFPS, eBIRForms, and Tax Software Providers (TSPs) as channels your customers may need, then mark each one as "requires primary-source validation" for eligibility, mandatory use, and exceptions under EOPT-related processes.

Step 4. Add a hard launch stop and run a cross-functional test. If ownership is unclear for filing, payment, exception handling, or recordkeeping, do not launch. Test one sample case across product, finance, support, and legal; if answers differ on who owns what, the flow is still in policy discovery.

For a step-by-step walkthrough, see Gig Worker Tax Compliance at Scale: How Platforms Handle 1099s W-8s and DAC7 for 50000+ Contractors.

Choose the payout rail by use case, not by habit#

Once your BIR ownership map is fixed, rail choice becomes an operations decision. Treat InstaPay and PESONet as candidate lanes to validate against your payout shape, not as default choices carried over from another market.

Start with what you can verify now#

Use four operational attributes: speed expectation, batching behavior, reconciliation overhead, and exception visibility. Mark each one as must validate before production until provider evidence exists for how InstaPay or PESONet perform on each of them.

Use a simple scorecard status for each attribute:

- Confirmed by provider evidence

- Must validate before production

Only mark "confirmed" when it is tied to dated provider documentation, implementation guidance, or test output.

Use a certainty-based routing table#

| Scenario | Provisional routing choice | What you can decide now | Must validate before production |

|---|---|---|---|

| Single payouts | One local rail candidate plus one non-local fallback | Approval flow, payout reference capture, evidence storage | Speed expectation, coverage, failure visibility, return handling |

| Batch payouts | Batch-capable local routing as a hypothesis | Batch IDs, per-beneficiary status rows, reconciliation exports | Batch submission support, cutoffs, partial failures, status quality |

| Mixed routing | Rule-based split across local and non-local methods | Separate domestic-bank paths from cross-border/non-compatible beneficiaries | Eligibility rules, route-level costs, exception paths, support language |

Add non-local fallbacks for coverage gaps#

Use Wise, PayPal, and SWIFT as fallback candidates when local coverage or beneficiary compatibility is limited, but keep confidence levels explicit.

| Option | Grounded detail | Current status |

|---|---|---|

| Wise | Sending-money pricing starts from 0.57%; uses the live mid-market rate with an upfront fee; discounts start over 25,000 USD (or equivalent); Wise Business setup price is 31 USD | Concrete pricing signals available |

| PayPal | Consumer fees page shows Last Updated: February 19, 2026; this does not establish Philippines-specific contractor payout pricing or fit | Must validate before production |

| SWIFT | Confirm fee, timing, and eligibility with the provider | Must validate before production |

For Wise, that gives you usable pricing signals. For PayPal, the grounded signal is limited: the consumer fees page shows Last Updated: February 19, 2026. That does not establish Philippines-specific contractor payout pricing or fit. For SWIFT, confirm fee, timing, and eligibility with the provider before use. Keep both as must validate before production.

Keep a hard rollout rule#

If support cannot explain failed-transfer handling for a selected rail, keep that rail in pilot only. The team should be able to explain who sees failure first, what status record is stored, who contacts the contractor, and when finance retries versus escalates.

Related: How to Pay Contractors in Peru: Yape Plin and SBS Compliance for Platform Operators.

Build the operating sequence from onboarding to payout proof#

Choosing a rail is not the same as being ready to launch. Use a repeatable sequence: classify the contractor, assign tax and filing ownership, execute the payout with traceable controls, and keep proof that finance and support can review without engineering intervention.

| Stage | Minimum record or control | Escalation or limit |

|---|---|---|

| Onboard contractor | Classification note, signed services agreement, invoice or billing basis, reviewer identity with timestamp | If records repeatedly need overrides or resemble employee setup, route to legal or tax review |

| Complete tax profile | Visible ownership for each BIR-related filing or payment step; chosen channel such as eFPS or eBIRForms | Verify exact eFPS or eBIRForms steps, deadlines, and penalties with the BIR |

| Execute payout | Idempotency key or equivalent; one internal payout ID through approval, submission, provider response, and ledger posting; one provider reference and one ledger outcome per attempt | If provider status cannot be tied to the internal payout ID and beneficiary record, keep it unresolved and limit that lane |

| Produce cycle evidence pack | Approval log, payout result set, exception log, and reconciliation export with run date, approver, contractor identifiers used, internal payout IDs, provider references, status snapshots, and exception notes | Store rejects and reversals alongside successful payouts |

- Onboard the contractor and record the engagement classification.

Decide the engagement path, then store the rationale tied to your four-fold test review. Keep the evidence trail explicit: reviewer, review time, documents reviewed, and why the record was accepted or escalated. Practical minimum: classification note, signed services agreement, invoice or billing basis, and reviewer identity with timestamp. If records repeatedly need overrides or resemble employee setup, route to legal or tax review before more payouts.

- Complete the tax profile and assign filing-channel ownership.

Before you approve the first payout, make ownership visible for each BIR-related filing or payment step (platform, customer, or contractor). If your model uses electronic channels, record the chosen channel, such as eFPS or eBIRForms. Keep this conservative: verify exact eFPS/eBIRForms steps, deadlines, and penalties with the BIR before launch. One commercial guide says foreign companies paying Filipino contractors generally do not withhold payroll taxes because contractors handle their own obligations, but treat that as a model assumption to validate for your fact pattern, not a universal rule.

- Execute payout once with duplicate protection and traceable references.

Use an idempotency key (or equivalent) at payout request level and carry one internal payout ID through approval, submission, provider response, and ledger posting. Whether the lane is InstaPay, PESONet, or a non-local fallback, each attempt should map to one provider reference and one ledger outcome. Reconcile ledger events against payout status at a fixed post-submission checkpoint, not only at month end. If provider status cannot be tied to the internal payout ID and beneficiary record, keep it unresolved and limit that lane.

- Produce a cycle evidence pack and review before scaling.

For each cycle, compile an approval log, payout result set, exception log, and reconciliation export. This is an operating control set, not a legal schema claim. Keep it complete and consistent: run date, approver, contractor identifiers used, internal payout IDs, provider references, status snapshots, and exception notes. Store rejects and reversals alongside successful payouts to avoid support and reconciliation blind spots.

After the first live cohort, run a hard checkpoint before scaling volume: verify end-to-end status traceability, and test support handoff on a real exception. The World Bank retail-payments note treats operational risk and business continuity as part of payment operations, so if support cannot explain a failure from the evidence pack alone, the sequence is not ready to scale.

Need the full breakdown? Read How to Pay Contractors in Nigeria Using Local Rails for Compliance-Safe Operations.

Design fallback handling for downtime and payment exceptions#

Fallback design is a launch gate, not a cleanup task. If a lane has no verified rule text, no approved exception route, or no tested handling path, keep that lane out of full launch.

- Keep BIR downtime handling blocked until primary rules are verified.

The outline references Revenue Memorandum Circular No. 087-2024, but its downtime contingencies require separate verification. Do not encode production logic for manual filing or payment conditions yet. Mark these paths as unverified and require named tax/legal approval before launch.

- Treat manual routing as an approved exception record, not operator memory.

The section scope includes RCO and AAB, but routing conditions between them require separate confirmation. Require an exception record with trigger, proposed route, approver, and supporting evidence before proceeding. If that record is incomplete, the case is not launch-ready.

- Define payment exception branches with clear ownership and closure evidence.

Build explicit branches for returned transfer, unmatched beneficiary, and delayed credit, then assign one owner per branch. Avoid hardcoded external timing claims unless verified with the rail or provider. Require closure proof, such as provider reference, ledger impact, and communication status, before marking a case resolved.

- Enforce an operator stop rule and test it before scaling.

If fallback handling is undocumented for a lane, pause launches on that lane. Run simulation cases for downtime and transfer exceptions and confirm teams can resolve them from the documented records alone. If resolution depends on undocumented tribal knowledge, keep the lane in pilot.

If you want a deeper dive, read How to Pay Contractors in Ethiopia: Telebirr and NBE FX Rules for Platform Operators.

Prevent contractor misclassification from becoming a payout risk#

The main payout risk is not transfer failure; it is continuing contractor payouts after the engagement starts to operate like employment. Treat this as an operations control issue early, because drift usually appears first in onboarding, invoicing, and payout patterns.

Keep the contractor lane separate from employee setup#

Keep contractor setup limited to what the contractor lane needs: contract terms, tax profile, payout method, and invoice controls. Do not let contractor records inherit employee-style setup unless legal and tax owners explicitly approve it for that engagement.

This matters for fields tied to payroll-tax withholding or employee programs such as SSS, PhilHealth, Pag-IBIG Fund, or Home Development Mutual Fund. One source states foreign companies do not need to withhold payroll taxes for Filipino contractors because contractors handle their own tax obligations, but that should be treated as an operating guardrail, not legal advice.

Verification point: if a contractor can be activated while employee-only fields are enabled, your controls are mixed.

Watch the payout signals that reveal drift first#

Misclassification risk often shows up in payment behavior before anyone names it. Monitor these three areas:

| Signal | What to watch | Review trigger |

|---|---|---|

| Onboarding changes | Post-launch changes in role setup, reporting context, and payment terms | These are escalation signals, not automatic conclusions |

| Invoice controls | Whether invoice submission and approval stay active in the contractor flow | If invoices are routinely waived to speed repeat payouts, treat that as a review trigger |

| Recurring payout patterns | Repeated same-amount, same-cycle payouts with low invoice variation | These cases need more scrutiny, not less |

- Onboarding changes

Track post-launch changes in role setup, reporting context, and payment terms. These are escalation signals, not automatic conclusions.

- Invoice controls

Keep invoice submission and approval active in the contractor flow. If invoices are routinely waived to speed repeat payouts, treat that as a review trigger.

- Recurring payout patterns

Review repeated same-amount, same-cycle payouts with low invoice variation. Operationally, those cases need more scrutiny, not less.

Escalate on four-fold-test drift before the next payout#

Set a hard rule: when engagement behavior starts to indicate employment signals under your four-fold test framework, pause further automated payouts and require legal or tax review first. For counsel review context, you can include the labor reference material your team uses, including Department Order No. 174.

Keep escalation evidence operational: original contract, latest scope changes, invoice history, payout cadence, approver notes, and any request to shift into fixed recurring payouts. Each escalation record should show who reviewed, what changed, and whether payouts are blocked, limited, or cleared.

You might also find this useful: How to Pay Contractors in Mexico: SPEI CoDi and SAT Compliance for Foreign Platforms.

Phase your market entry with explicit go/no-go gates#

Expand only when your evidence stays clearer than your volume curve. If compliance clarity drops as payouts rise, pause expansion and fix that first.

Run a one-rail pilot and prove ownership#

Start with one payout rail and a small contractor cohort. The go signal is operational control, not volume: your tax/compliance owner, finance reviewer, and support team should each be able to explain and execute their part without fuzzy handoffs.

Make verification concrete. For each live payout, confirm you can retrieve the approval record, payout result, exception note, and reconciliation export in one review. If a pilot looks clean only because someone is patching gaps in chat or spreadsheets, you are not ready for Phase 2.

Add a second rail only after exceptions become boring#

Add InstaPay or PESONet only after exception handling is predictable on your first lane. Treat unknowns on rejection behavior, support escalation, and reconciliation workload as launch blockers until you validate them in production.

Use one rule: if support cannot classify and route transfer exceptions without specialist help, keep the new rail in pilot. Do not expand just because customers request more options.

Introduce Wise, PayPal, or SWIFT only where the numbers justify the extra ops load#

Broader provider mix can improve coverage, but it also adds pricing review, policy review, and support surface area. Wise provides clear inputs in the available evidence: a usage-based model with no subscriptions or plans, sending fees that can start from 0.57%, a 31 USD one-time Wise Business setup fee, automatic volume discounts after 25,000 USD in monthly transfers, and use of the live mid-market rate.

For PayPal, verify the current fee-policy version before rollout; the referenced consumer fees page shows Last Updated: February 19, 2026. For any provider, including SWIFT, scale only when coverage, cost, and support burden are all acceptable in your own operating model.

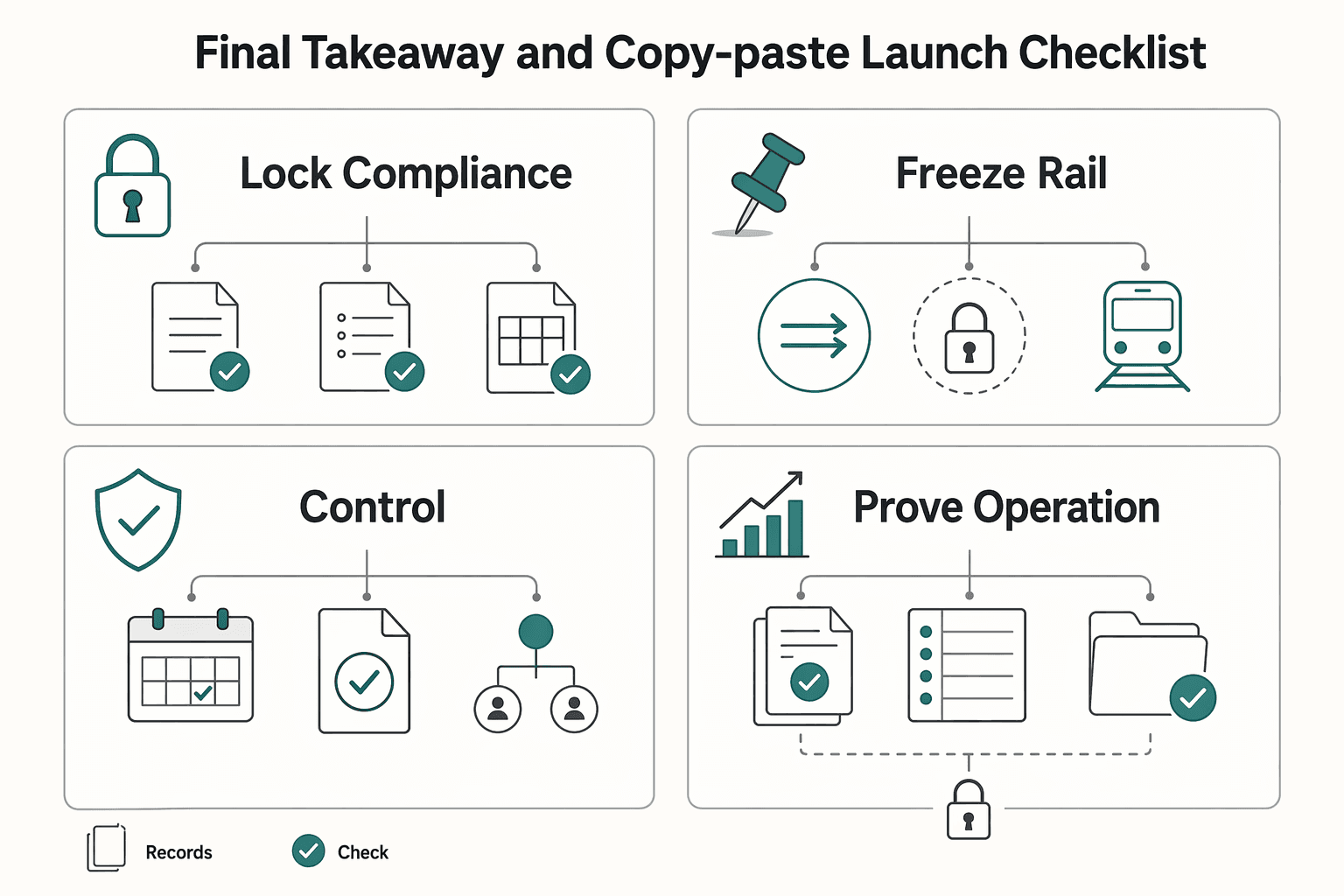

Final takeaway and copy-paste launch checklist#

If any item is still undocumented, keep the rollout in pilot.

- Step 1: Lock the compliance boundary.

Assign a clear tax owner and document the exact filing/payment path your team will use, including fallback ownership. This section does not validate BIR channel specifics (such as eFPS, eBIRForms, TSPs, RCO, or AAB), so confirm those separately before scale.

- Step 2: Freeze the rail decision and define non-local fallback.

Choose one primary local rail and keep unresolved behaviors in a validation queue until tested in production-like conditions. For non-local fallback, document why each option exists and keep dated pricing evidence: Wise says pricing is pay-as-you-use with no subscriptions/plans, fees vary by currency and can start from 0.57%, discounts begin above 25,000 USD equivalent monthly volume, and transfers use the live mid-market rate; PayPal's consumer fees page shows Last Updated: February 19, 2026.

- Step 3: Put classification controls in front of recurring payouts.

Use your approved contractor-classification process at onboarding and store the rationale with each record. If engagement facts drift, pause recurring payouts and escalate to legal/tax review before continuing.

- Step 4: Prove the operation before widening it.

Run one full cycle and confirm a retrievable trace from approval to payout result to reconciliation output, including exception notes. If teams must reconstruct events from chat or memory, treat that as a launch blocker.

This pairs well with our guide on How to Launch a Legal Compliance Platform for Freelancers and Handle Their Payments.

Frequently Asked Questions

What does BIR require for electronic filing and payment under the EOPT rules?

Under Revenue Regulations No. 4-2024 and the FAQ alert citing Revenue Memorandum Circular No. 87-2024 dated August 7, 2024, the default direction is electronic filing and payment. Taxpayers already enrolled in eFPS should keep using eFPS. Those required to use eFPS but not yet enrolled should use eBIRForms for e-filing and pay electronically, with attachments submitted through eAFS or the eSubmission Facility as applicable.

When can taxpayers use manual filing or payment if electronic systems are unavailable?

The cited BIR guidance allows manual filing when BIR electronic platforms such as eFPS, eBIRForms, and Tax Software Providers are unavailable. If the issue is specifically an eFPS outage and there is an advisory of unavailability, the taxpayer may use eBIRForms instead. Manual fallback is an availability exception, not a convenience path.

How should a platform decide between InstaPay and PESONet when details are incomplete?

Do not guess between InstaPay and PESONet when operational details are incomplete. Treat rail selection as pending validation until provider data is confirmed. Use a controlled rollout and confirm exception handling and reconciliation before scaling.

Which payment method categories are commonly used to pay contractors in the Philippines?

One cited source groups common options into international wire transfers, digital platforms, and specialized contractor payment services that handle currency conversion. That framework helps with coverage planning when local-rail support is limited. The final choice should be treated as an operations decision first, not just a checkout feature choice.

How does contractor misclassification risk affect payout program design?

Misclassification risk matters because the payout model assumes the worker is correctly treated as a contractor. If classification is uncertain or the engagement starts to look like employment, pause and escalate for legal and tax review. The article points to Department Order No. 174 as one labor-guideline reference for review context.

What minimum evidence should a platform keep for payout audit readiness?

Keep a complete record for each cycle, including filing proof, payment confirmation, attachment submission record, and reconciliation output. The practical test is whether finance or support can retrieve the full record without rebuilding it from chat, email, or spreadsheets. Rejects and reversals should be stored alongside successful payouts.

What should founders validate before scaling from pilot to full launch?

Before scaling, confirm the filing path is clear and documented, the fallback path is defined for BIR platform downtime, and reconciliation works at the cycle level. Document the exact channel choice, whether that is eFPS, eBIRForms, or a TSP-linked route. If clarity drops as volume rises, pause rollout and fix controls first.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bsp.gov.ph/Pages/IRG/irg-files/2026/Republic%20of%20the...trusted

- bsp.gov.ph/Media_And_Research/Annual%20Report/AnnRep_20...trusted

- documents1.worldbank.org/curated/en/368161629268352616/pdf/Philippine...trusted

- documents1.worldbank.org/curated/en/796871601650398190/pdf/Philippine...trusted

- paypal.com/us/digital-wallet/paypal-consumer-feestrusted

- pdp.depdev.gov.ph/wp-content/uploads/2023/01/PDP-2023-2028.pdftrusted

- wise.com/us/pricing/send-moneytrusted

- wise.com/us/pricingtrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Pay Contractors in Ethiopia with Telebirr and NBE FX Checks

This brief is for platform founders and operators who need a go/no-go answer on Ethiopia before they spend engineering, compliance, or go-to-market budget. The real question is not whether contractors exist in Ethiopia or whether digital payments exist. It is whether your exact payout model looks feasible enough, based on actual evidence, to justify real work now.

Pay Contractors in Peru with Yape, PLIN, and SBS Checks

Treat Peru as a posture decision, not just a rail decision. If you choose a local wallet-style method first, then sort out contractor status, tax data, and evidence later, you may get a smoother payout experience. You also raise launch risk in areas that are much harder to fix once money starts moving.

Pay Contractors in Mexico: SPEI, CoDi, SAT, and CFDI Decisions for Platforms

Mexico contractor payouts usually break for a simple reason: teams launch from a generic Latin America plan, then discover that payout rail choices, tax steps, and operating structure cannot be separated in practice. If you are evaluating multiple rails and operating models at the same time, you need Mexico-specific decisions before you send the first live payout.