Hiring in Germany exposes global companies to "Permanent Establishment" risk, where a single employee’s activities can subject your global profits to a ~30% local corporate tax. The core advice is to use an Employer of Record (EOR), which legally hires employees on your behalf to insulate your business from German tax and labor laws. This strategic path allows you to securely engage top talent and test the market without the immense cost and liability of forming a local entity or the legal dangers of misclassifying contractors.

Before You Hire: The Hidden Landmine Every Global Founder Must Know#

Moving from a tactical hiring checklist to a strategic market-entry playbook requires scanning the terrain for traps. Before you hire your first employee in Germany, you must understand a concept that poses a significant financial and legal risk to your global business: Permanent Establishment.

Defining the Threat: What is "Permanent Establishment" (PE) Risk?#

In the plainest terms, Permanent Establishment (PE) is a concept in international tax law where a certain level of business activity in another country can make your entire company liable for corporate taxes there. For a practical frame, use the OECD's permanent establishment guidance when you pressure-test the role. German tax authorities can determine that a single employee's activities create a "fixed place of business," effectively treating a part of your foreign company as a permanent German entity for tax purposes.

This isn't just about a physical office. A PE can be triggered by a variety of factors, and the bar is lower than many founders assume. The most common mistake is underestimating the scope of activities that create a taxable presence.

The Consequence: Your Global Profits on a German Tax Bill#

The consequences of unintentionally creating a PE are severe. If German authorities deem you have a PE, the profits attributable to your German operations become subject to local corporate taxes. This includes a 15% corporate tax plus a 5.5% solidarity surcharge, bringing the rate to 15.825%. On top of that, a municipal trade tax, which varies by city, is also levied. This results in a combined corporate tax burden that typically averages around 30%.

This means a portion of your company's global profits—not just revenue generated in Germany—could be allocated to the PE and land on a German tax bill, creating a massive, unforeseen liability and complex compliance requirements like VAT registration.

The Triggers: How One Employee Becomes a Tax Nexus#

So, what specific actions by your employee can create this tax nexus? The risk escalates when your employee moves beyond purely administrative or "preparatory" tasks and into core business functions. While every situation is unique, German tax law and double taxation agreements outline clear red flags.

Here are the most common triggers you must control:

- Concluding Contracts: If your employee has, and habitually uses, the authority to negotiate and sign contracts on behalf of your company, this is one of the strongest indicators of a PE. This is often referred to as a "dependent agent" and is a primary focus for tax authorities.

- Generating Revenue: An employee in a direct sales or business development role who actively generates revenue in Germany is performing a core business function that points toward a PE. Their work goes far beyond the "preparatory or auxiliary" activities that are generally exempt.

- A Fixed Place of Business: This is the classic trigger. While it can be an office or workshop, German tax law can also interpret a dedicated, long-term home office as a fixed place of business over which your company has a degree of control. Even having exclusive access to a lockable container in a shared office for business documents has been sufficient for German courts to rule that a PE exists.

- Duration and Permanence: The activities must have a degree of permanence. While a short, temporary project is less risky, an ongoing presence—generally considered to be six months or more—solidifies the connection to the German market and significantly increases your compliance risk.

Your Strategic Map: The 3 Paths to Engaging German Talent#

Understanding the risk of Permanent Establishment naturally leads to a critical question: how do you engage German talent without exposing your global business to local tax liability? This isn't about avoiding the market; it's about choosing your entry strategy with intention. You have three distinct paths, each with a fundamentally different risk profile, cost structure, and level of administrative burden. Your task is to consciously select the path that aligns with your immediate goals and long-term vision.

Path 1: The Contractor (The Agility Path)#

This path offers maximum speed and flexibility, bypassing the complexities of German employment law. It is best suited for short-term, specialized projects where the contractor's independence is clear and defensible. However, this agility comes with a significant and often underestimated compliance risk: "false self-employment."

Path 2: The Employer of Record (The Peace of Mind Path)#

For the risk-averse leader, the Employer of Record (EOR) model is the intelligent default. An EOR is a German company that legally hires an employee on your behalf, insulating your business from local tax and labor laws. If you need the operating model first, review A Guide to Employer of Record (EOR) Services and then compare vendors against your own control requirements. This is the most direct way to mitigate PE risk and administrative overhead while securing full-time, dedicated talent.

Path 3: The German GmbH (The Full-Commitment Path)#

Forming a Gesellschaft mit beschränkter Haftung (GmbH), or limited liability company, is the ultimate commitment to the German market. This path is for founders ready to build a substantial, long-term presence, hire a larger team, and own local intellectual property. It offers the most control but carries the highest cost and complexity.

To clarify your decision, here is a direct comparison:

| Factor | Path 1: Contractor | Path 2: Employer of Record (EOR) | Path 3: German GmbH |

|---|---|---|---|

| Speed to Hire | Very Fast (Days) | Fast (Days to 2 Weeks) | Slow (4-8+ Weeks) |

| Compliance Risk | Very High (Misclassification) | Very Low (Managed by EOR) | High (Managed by You) |

| Upfront Cost | Low | Low to None | Very High (€12,500+ share capital) |

| PE Risk | Moderate to High | None | Not Applicable (You have an entity) |

| Best For | Short-term, project-based work with clear autonomy. | Your first 1-10 hires; testing the market; risk mitigation. | Long-term commitment; building a large team; owning local IP. |

Path 1: The Contractor Model (The High-Agility, High-Risk Path)#

The allure of the contractor path—its sheer speed and apparent simplicity—can be powerful. You have a critical project, you've found the perfect person, and you want them to start now. This is the moment, however, where a savvy leader pauses. Before you sign that freelance agreement, you must understand the single greatest compliance trap in German employment law: "false self-employment" (Scheinselbstständigkeit).

This isn't a minor administrative issue; German authorities view it as a form of black market labor designed to circumvent the country's robust social welfare system. Consequently, the burden of proof is entirely on you, the hiring company, to demonstrate that your contractor is genuinely independent and not a "disguised employee." What's written in your contract is secondary to the day-to-day reality of the working relationship.

The Red Flag Checklist: How German Auditors Think#

To stay compliant, you need to think like an auditor from the German Pension Insurance Association (Deutsche Rentenversicherung). They will scrutinize the relationship for signs of dependency. If you answer "yes" to several of the following questions, you are in a high-risk situation:

- Integration: Is the contractor deeply integrated into your operational structure? Do they have a company email address, attend regular internal team meetings, or report to a direct manager?

- Instruction: Are you dictating how, when, and where the work gets done? True contractors control their own process and schedule; employees follow instructions.

- Exclusivity: Does the contractor derive the vast majority (typically over 80%) of their income from your company? A lack of other clients is a primary indicator of economic dependence.

- Entrepreneurial Risk: Does the individual bear any genuine business risk? Do they use their own equipment, have their own office space, and actively market their services to other clients?

The Financial Fallout of Misclassification#

Getting this wrong has severe and retroactive financial consequences. If authorities reclassify your contractor as an employee, your company can be held liable for up to four years of back-paid social security contributions. Critically, this includes both the employer's and the employee's share, plus late payment penalties. What began as a cost-effective arrangement can instantly transform into a staggering liability. In cases deemed intentional, the back-payment period can extend to 30 years, and company directors can even face criminal proceedings.

Path 2: The EOR Model (The Peace of Mind Path for Global Leaders)#

If the risks of the contractor path feel like a high-wire act without a net, the Employer of Record (EOR) model is the sturdy, compliant bridge to the other side. This path is engineered for the leader who prioritizes control, risk mitigation, and strategic focus over administrative entanglement. It allows you to engage top German talent as full-fledged employees without the immense overhead of creating your own German legal entity.

Your Shield Against PE Risk and Admin Overload#

An Employer of Record is a German-based entity that becomes the legal employer for your hire, on your behalf. This structure directly neutralizes the single greatest tax threat we discussed: Permanent Establishment risk. Since your employee is legally on the payroll of a German company (the EOR), your business has no direct employment nexus in the country. The EOR is the one registered with local tax and social security institutions, not you. This severs the link that tax authorities could use to claim your global profits are subject to German corporate tax.

All-in-One Compliance, Handled#

Beyond tax insulation, the EOR’s primary function is to absorb the entire administrative burden of German employment. A credible EOR partner manages every critical step of the employment lifecycle, ensuring full compliance with Germany’s notoriously complex regulations:

- Compliant Contracts: Drafting and executing a legally sound German employment contract that incorporates all mandatory clauses, from probation periods to termination notices.

- Social Welfare Registration: Handling the complete registration of your employee into Germany’s robust social welfare system, including pension, unemployment, and statutory health insurance.

- Payroll & Withholding: Processing monthly payroll, accurately calculating and withholding all required income taxes and social contributions, and remitting them to the correct German authorities.

- Labor Law Adherence: Ensuring you remain compliant with German labor law, including regulations on working hours, paid leave, and the stringent protections afforded to employees.

Transparent Costing: Budgeting for Your German Hire#

This model replaces financial uncertainty with predictable costs. On top of the employee's gross annual salary, you must budget for the mandatory employer-side social security contributions. As of 2025, this amounts to approximately 21% of the gross salary (up to certain income ceilings).

Here is a typical breakdown of those employer costs:

| Contribution | Employer's Share (Approx. %) |

|---|---|

| Pension Insurance (Rentenversicherung) | 9.3% |

| Health Insurance (Krankenversicherung) | 7.3% + a share of additional contributions |

| Unemployment Insurance (Arbeitslosenversicherung) | 1.3% |

| Long-Term Care Insurance (Pflegeversicherung) | ~1.7% |

| Total Employer Share | ~21% |

Additionally, employers are solely responsible for accident insurance contributions (Unfallversicherung), with rates varying by industry. The EOR’s management fee is then added to this subtotal, giving you a single, all-inclusive monthly invoice. This clarity allows you to budget with precision and confidence.

The Smart Default for Your First Hire#

The EOR path offers an unparalleled balance of speed, compliance, and strategic flexibility. It empowers you to secure world-class talent and test the German market without the multi-month bureaucratic process and significant capital investment required to establish a German GmbH. You get the operational benefits of a dedicated employee without the legal and financial liabilities of being a German employer.

Path 3: The GmbH Model (The Full-Commitment Path for Market Domination)#

While the EOR model offers an intelligent entry point, there comes a time when your ambitions for Germany demand a permanent foundation. This is the moment to plant your flag. The GmbH (Gesellschaft mit beschränkter Haftung), Germany's limited liability company, is the ultimate structure for founders who see the country not as an experiment, but as a core pillar of their long-term growth. This path is for when the drivers are undeniable: you need to hire a significant local team, anchor valuable intellectual property in Germany, or establish a physical office for sales and operations.

The Bureaucratic Gauntlet: A Realistic Look at the Process#

Forming a GmbH is a serious undertaking, requiring capital, patience, and professional guidance. It signals to the German market that you are here to stay. The setup process is rigorous and methodical. You are no longer outsourcing compliance; you are building it from the ground up.

Here are the essential steps you will navigate:

- Engage a German Notary (Notar): The entire process is overseen by a notary, who will draft and certify your articles of association (Gesellschaftsvertrag).

- Open a German Corporate Bank Account: With the notarized documents, you will open a corporate bank account in the name of your GmbH.

- Deposit Share Capital (Stammkapital): You must deposit the minimum share capital of €25,000. At least half of this amount, €12,500, must be in the account before the company can be registered.

- Register with the Commercial Register (Handelsregister): The notary will file your company for registration with the local commercial register. Only upon entry does the GmbH legally exist.

- Tax and Trade Office Registration: Finally, you must register with the local trade office (Gewerbeamt) and the tax office (Finanzamt) to receive your tax numbers.

Becoming a German Employer: Your New Responsibilities#

Once your GmbH is established, you are a full-fledged German employer, directly shouldering all associated legal and administrative duties. Your primary obligations now include:

- Obtaining an Employer Number (Betriebsnummer): You must apply for this number from the Federal Employment Agency before you can register employees for social security.

- Managing German Payroll: You are responsible for correctly calculating and withholding payroll taxes (Lohnsteuer) and social security contributions, typically by retaining a German tax advisor (Steuerberater).

- Navigating Labor Law Directly: You must adhere to all aspects of German labor law, from the Working Hours Act to robust protections against dismissal.

- Engaging with Works Councils (Betriebsrat): In companies with five or more employees, the workforce can elect a Works Council. This body holds significant co-determination rights on matters like working hours and dismissals, requiring you to inform and consult with them.

Choosing the GmbH path is a declaration of intent. It is the most complex and costly of the three paths, but it offers the highest degree of control and integration into the German economy.

Your Next Move: From Anxiety to Action#

Confronting the realities of German labor law can feel overwhelming. But successfully hiring your first employee in Germany isn’t about memorizing regulations; it’s about making one sound strategic decision. The complexity isn't a barrier; it's a signal to choose your path with intention. By reframing the challenge through the 3-Path Framework—Contractor, EOR, or GmbH—you move from reacting to compliance risks to proactively choosing a model that serves your goals.

Your decision hinges on a clear-eyed assessment of your company's risk tolerance, timeline, and long-term ambition in the German market.

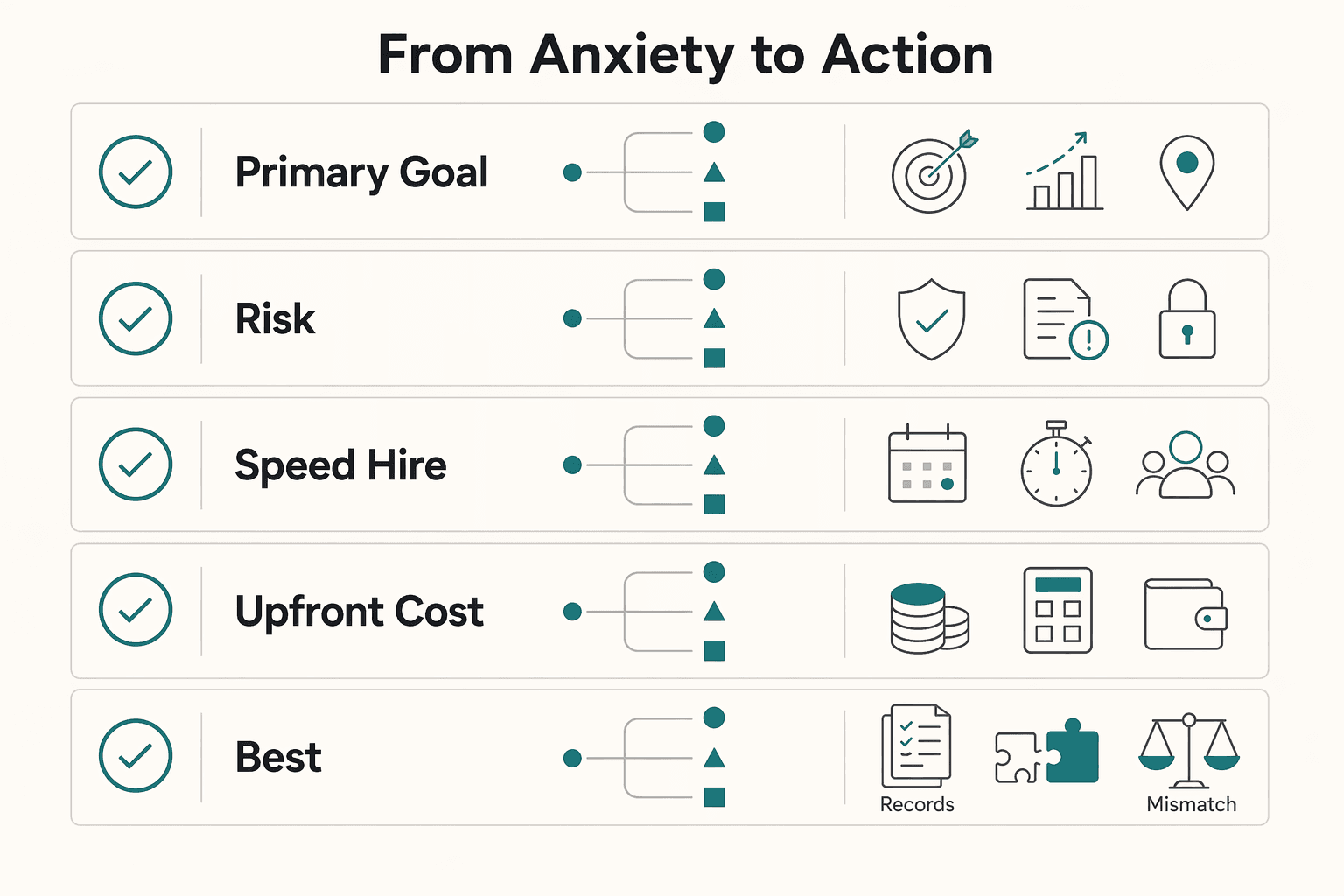

Here is a strategic breakdown to clarify your choice:

| Decision Factor | The Agility Path (Contractor) | The Peace of Mind Path (EOR) | The Full-Commitment Path (GmbH) |

|---|---|---|---|

| Primary Goal | Speed & Flexibility | Risk Mitigation & Compliance | Long-Term Market Control |

| Risk Profile | Very High. Constant risk of Scheinselbstständigkeit misclassification. | Very Low. The EOR assumes legal liability for employment, payroll, and tax compliance. | High Initial / Moderate Ongoing. You bear 100% of the legal and administrative liability. |

| Speed to Hire | Very Fast (Days) | Fast (Days to 2 weeks) | Very Slow (4-8+ weeks for entity formation) |

| Upfront Cost | Low | None. Pay a monthly service fee on top of salary and social costs. | Very High. Requires €25,000 in share capital, plus notary and legal fees. |

| Best For... | Short-term, specialized projects with a provably independent contractor. | Your first full-time hire, market testing, or securing key talent without PE risk. | A proven, long-term commitment, typically when hiring multiple employees (5+) or requiring a physical office. |

Ultimately, the path you choose is a direct reflection of your business strategy. Hiring a contractor is a short-term tactic with significant legal exposure. Establishing a GmbH is a long-term investment in infrastructure. For the global leader focused on securing talent and validating the market, the Employer of Record model presents the most intelligent default. It allows you to engage top talent with the operational control you need, while outsourcing the immense legal and administrative burden to a dedicated local expert.

You are the architect of a global enterprise. This is the strategic map to build your foundation in one of the world's most powerful markets with confidence and control.

Frequently Asked Questions

Do I need a German company to hire an employee in Germany?

No, you do not necessarily need to form your own German company. An Employer of Record (EOR) is a German entity that legally hires an employee on your behalf, managing all local payroll, taxes, and compliance. This allows you to secure full-time German talent without establishing a legal entity yourself, thereby avoiding the cost, complexity, and PE risk.

What are the total employer costs for an employee in Germany?

Beyond the gross salary, budget for mandatory employer social security contributions, which total approximately 21% of the employee's gross salary (up to certain income caps). This covers pension, health, unemployment, and long-term care insurance. Employers also pay for accident insurance, with rates varying by industry.

What is the risk of hiring a contractor instead of an employee?

The primary risk is "false self-employment" (Scheinselbstständigkeit). If German authorities reclassify your contractor as an employee, you can be held liable for up to four years of back-paid social security contributions for both the employer's and the employee's shares, plus significant fines.

What is Permanent Establishment (PE) risk?

PE is a tax concept where having an employee in Germany—particularly in a revenue-generating role—can be interpreted by tax authorities as creating a taxable presence for your foreign company. If this happens, a portion of your company's global profits could become subject to Germany's corporate taxes of around 30%.

What are the mandatory benefits for an employee in Germany?

Every employee is entitled to extensive mandatory benefits, including:

- Statutory health, pension, unemployment, and care insurance.

- Paid sick leave for up to six weeks at full pay from the employer.

- A minimum of 20 days of paid annual leave (25-30 days are standard).

- 14 weeks of fully paid maternity leave.

How long is a typical probation period in Germany?

A probationary period (Probezeit) can be set for a maximum of six months. During this time, the notice period for termination by either party is typically just two weeks. It is a standard and highly recommended practice.

What are Germany's rules on employee termination?

Germany has some of the strongest employee protection laws in the world. After the six-month probation period, an employee can only be terminated for specific, legally justifiable reasons (operational, personal, or performance-related) as defined by the Protection Against Unfair Dismissal Act. A dismissal without a valid, documented reason can be successfully challenged in labor court.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

- irs.gov/pub/irs-trty/germany.pdftrusted

- oecd.org/content/dam/oecd/en/publications/reports/201...trusted

- oecd.org/content/dam/oecd/en/publications/reports/200...trusted

- bamf.de/EN/Themen/MigrationAufenthalt/ZuwandererDrit...external

- make-it-in-germany.com/en/working-in-germany/working-environment/sa...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Can Digital Nomads Claim the Home Office Deduction?

Claim the deduction only when your facts and records can carry it. With the home office deduction for digital nomads, the real decision is usually a three-way call: claim it, do not claim it, or pause and get help because your file is not ready.

What to Do If You've Been Misclassified as an Independent Contractor

Treat this as a protection problem first, not a label debate. If your work was treated as an independent contractor arrangement even though the relationship functioned differently, your first goal is to protect pay, rights, and records while you choose the least risky escalation path. You can do that without making accusations on day one, which often keeps communication open while you document what happened.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.