Quick Answer

Choose one operating model, lock deduction order, and define the exact event that makes a payout final before scaling. In this topic, success means every line from Gross Pay to Net Pay can be replayed from stored records, not spreadsheet memory. Use Form W-4 or Form W-4P status as a release gate, route nonresident cases to Notice 1392 review, and stop auto-release when ownership or jurisdiction inputs are unclear.

How Gross-to-Net Payout Models Work#

Payroll tax references matter, but they are not a payout architecture. Teams often collect withholding rules, filing-status details, and tax-form requirements before they have defined who owns each deduction line. That guidance still matters for withholding logic. IRS guidance on the Additional Medicare Tax can be useful context for tax review, but it does not define deduction sequencing, ledger mapping, release gates, or recipient-facing payout explanations.

Platform teams still need ownership, booking, and release logic. Answer four questions clearly: who owns each deduction, who is responsible for withholding, when each amount becomes final, and what record explains every move from Gross Pay to Net Pay. Finance, ops, and engineering should be able to reconcile the same transaction from that record.

Before you turn any tax reference into product logic, confirm that the source is authority and not just background. Publication 963 is explicitly informational and cannot be cited as authority for a technical tax position. If a source cannot support the rule, do not let that rule auto-release funds.

This guide focuses on choosing a gross-to-net model you can defend in production. We compare practical payout models against policy gates, explainable deductions, and clean reconciliation. The 2025 Form 1040/1040-SR instructions also note that more complex situations may require numbered schedules. Your payout design should expect branching while still keeping one consistent ledger path from gross to net.

How to choose the right gross-to-net model for your platform#

Choose a model your team can explain end to end, not one that only estimates withholding in isolation. Start with four checks.

| Check | What to define | Grounded detail |

|---|---|---|

| Deduction ownership | Ownership for every line between Gross Pay and Net Pay | Each deduction should have one accountable owner and one traceable ledger path |

| Withholding responsibility | Whether the flow is doing withholding or simply passing amounts through to the recipient | The IRS Tax Withholding Estimator helps complete Form W-4 or Form W-4P, but it cannot be used if there is no job or pension, it cannot estimate withholding on future income, and it is not for nonresident U.S. tax-status cases |

| Timing tolerance | Estimated and final values as different states in the payout flow | Pay-period federal withholding and year-to-date withholding should not be merged or treated as interchangeable |

| Audit burden | The simplest model the records can defend under jurisdiction-specific rules | Hawaii requires Form G-75 to be attached to Form G-45 and Form G-49 when business activity spans more than one island |

- Deduction ownership

Map ownership for every line between Gross Pay and Net Pay before you scale volume. In practice, each deduction should have one accountable owner and one traceable ledger path.

- Withholding responsibility

Decide whether your flow is actually performing withholding or simply passing amounts through to the recipient. The IRS Tax Withholding Estimator helps complete Form W-4 or Form W-4P. It cannot be used if there is no job or pension, it cannot estimate withholding on future income, and it is not for nonresident U.S. tax-status cases, where the IRS directs users to Notice 1392.

- Timing tolerance

Treat estimated and final values as separate states in your payout flow. IRS guidance also separates pay-period federal withholding from year-to-date withholding, so those fields should not be merged or treated as interchangeable.

- Audit burden

Pick the simplest model your records can defend under jurisdiction-specific rules. For example, Hawaii requires Form G-75 to be attached to Form G-45 and Form G-49 when business activity spans more than one island. Your payout records should preserve that level of filing detail.

For the margin side of the decision, see Platform Economics 101.

The deduction waterfall every credible implementation must define#

Define one fixed deduction sequence and keep it stable across calculation logic, ledger mapping, and support workflows. A workable internal pattern is gross amount, platform or processing fees, statutory withholding, reserves or holds, disbursement cost, then final Net Pay. The point is not to claim one universally mandated order. It is to make every payout consistent and traceable.

- Sequence before math

Name each stage before you calculate anything. ACF separates operational processing from withholding calculation, so do not bury fees and withholding in one opaque formula. If an input changes after a step runs, your flow should clearly say whether to recalculate, absorb the difference, or pause for review.

- Separate statutory lines from commercial lines

Keep statutory withholding and garnishment lines separate from platform fees. IRS Publication 15 separates federal income tax withholding from nonpayroll federal income tax withholding. ACF separately calls out pre-tax deductions and other garnishments or child support. If your team cannot classify a line quickly, payout explanations and disputes break down.

- Assign ownership and remittance responsibility per line

For each deduction, define who owns the line operationally and who must book and remit it. Treat recordkeeping as part of the design, not cleanup after launch. Each line should be traceable to its calculation basis, owner, booking path, and remittance or release action.

- Pin jurisdiction inputs to exact checkpoints

If you use fields such as Filing Status, State Income Tax, or Local Income Tax, document exactly when those fields affect calculation and when they are stored only for reporting or review. Branch logic should also handle worker type differences and insufficient-funds scenarios. If key tax-profile data changes before disbursement, either recalculate or route to manual review.

Your control test is simple: for any payout, you can trace one path from gross to Net Pay and reproduce the input snapshot used at calculation time. A common failure mode is allowing reserves, fee updates, or profile edits after withholding without triggering a recalculation.

Three payout ownership models for fees and withholding#

After you define the deduction waterfall, decide who owns each deduction line. Keep that ownership explicit as an internal policy choice. IRS Publication 15 (2026) treats Federal Income Tax Withholding, Nonpayroll Federal Income Tax Withholding, and Recordkeeping as separate topics. It does not, by itself, select a single platform ownership model.

These are internal operating models, not IRS-defined categories. Use one model intentionally so payout math, ledger entries, and payout explanations stay traceable.

| Model | What the platform owns | Main upside | Main risk | Release checkpoint |

|---|---|---|---|---|

| Platform-withholds-first | Fee calculation, withholding calculation, booking, and release logic (if you choose to centralize those steps) | One controlled calculation point | More compliance and documentation load | Freeze the calculation input snapshot before release |

| Payee-self-remits | Commercial fees and disbursement, but not centralized withholding or remittance logic (in this internal model) | Lower operational handling inside the platform | More confusion around Gross Pay vs Net Pay | Make payout statements explicit about what was and was not withheld |

| Hybrid split | Ownership varies by entity, product, or payee class | Flexibility where one rule does not fit all | More branching and inconsistent treatment risk | Require a branch reason code and rule version on every payout |

Platform-withholds-first model#

Choose this model when control and traceability matter more than simplicity. If adopted, you calculate fees, run the withholding logic you support, and release the remainder only after those steps complete. The upside is one controlled calculation point, not a guarantee that every outcome is correct.

Keep statutory lines separate from commercial lines throughout. Publication 15 (2026) distinguishes Federal Income Tax Withholding from Nonpayroll Federal Income Tax Withholding and separately names Recordkeeping. Each payout should show which line came from a fee rule, which came from a withholding rule, and which owner your internal workflow assigned for remittance.

Before release, confirm that the payee profile, amount basis, and rule version used for calculation are still current. If inputs changed after withholding ran, recalculate or hold for review so booked values and payout explanations do not drift apart.

Payee-self-remits model#

This model reduces what the platform owns, but it raises the bar for clear disclosure. In this internal model, you can still deduct your own fees and disbursement costs while withholding and remittance are not centralized in the same way.

The main risk is explanation ambiguity. If you show Gross Pay and Net Pay without saying whether withholding was applied, recipients can easily misread what the platform handled. The 2025 Form 1040 instructions also note that some situations require "one or more of the numbered schedules." That reinforces that tax handling can branch in more complex cases.

Your key control is disclosure clarity. In payout statements, APIs, or reports, label each commercial deduction and state plainly when withholding was not performed by the platform. Keep the exact statement or template version and the accepted terms version as part of the record.

Hybrid split model#

Hybrid ownership gives you flexibility only if you control the branching discipline. Some payouts are handled centrally and others pass responsibility through under internal rules. That can work, but it also creates a higher risk of inconsistent treatment.

Documentation is the control point. Publication 15 (2026) separates withholding topics and names Recordkeeping, and the 2025 Form 1040 instructions indicate additional schedules in more complex cases. In practice, each payout in a hybrid model needs a stored branch reason, rule version, and owner for each deduction line.

Do not let a payout move branches mid-flow without recalculation or manual review. Correct ownership exceptions early and explicitly, because they get much harder to unwind later.

Related: Affiliate Network Payout Structures: Performance-Based Commission Models for Publisher Partners.

Three payout ownership models for timing and rails#

Once deduction ownership is set, the next decision is timing. You need to define what makes a payout final and what event counts as disbursed. Use one timing model per product line, define it explicitly, and keep the same rule in your ledger, support tooling, and recipient messaging. Treat these as internal operating patterns rather than universal standards.

Real-time quote then disburse#

Use this model when the pre-release quote or pricing event is your control point for the payout amount. Record the calculation snapshot, quote identifier if applicable, selected rail, and release timestamp together so the locking moment is traceable.

If key inputs change after the quote but before release, follow a documented exception process before disbursement.

Batch-close model#

Here, batch approval is the control boundary, so freeze the payout set at close and release only from that frozen set. Keep the freeze artifact complete: batch ID, approver, approval timestamp, and rule version for each payout line.

If a payee or calculation input changes after close, route it through exception handling or a later batch instead of silently editing the approved batch.

Asynchronous provider-confirmed model#

This model separates initiation from final provider outcome. Keep requested and completed as distinct states, and map disbursed only to the provider-confirmed event your team has designated as final.

Store a compact evidence trail for each payout: provider reference, status history, timestamps, and payload version sent. Publication 15 (2026) lists both Electronic Filing and Payment and Recordkeeping, so keep payment timing fields and recordkeeping artifacts distinct. If records include sensitive information, share them only on official, secure websites.

For payout timing tradeoffs, see NET-30 vs Instant Payout for Influencer Marketing Platforms.

Compare the six models before committing engineering time#

Before you build, put the ownership model and timing model in one view. That gives product, finance, ops, and engineering a shared decision record instead of six different assumptions.

| Model | Best-for team | Deduction owner | Withholding owner | Timing behavior | Reconciliation complexity | Failure blast radius |

|---|---|---|---|---|---|---|

| Platform-withholds-first | Define for your context | Assign explicitly | Assign explicitly | Define finality event | Estimate before build | Define affected scope |

| Payee-self-remits | Define for your context | Assign explicitly | Assign explicitly | Define finality event | Estimate before build | Define affected scope |

| Hybrid split | Define for your context | Assign explicitly | Assign explicitly | Define finality event | Estimate before build | Define affected scope |

| Real-time quote then disburse | Define for your context | Inherit chosen ownership model | Inherit chosen ownership model | Define quote-lock point and release point | Estimate before build | Define affected scope |

| Batch-close | Define for your context | Inherit chosen ownership model | Inherit chosen ownership model | Define batch freeze and release rules | Estimate before build | Define affected scope |

| Asynchronous provider-confirmed | Define for your context | Inherit chosen ownership model | Inherit chosen ownership model | Define requested vs provider-confirmed final state | Estimate before build | Define affected scope |

| Escalation trigger (governance row) | Define owning team | Define who can change policy | Define who can change policy | Define when pass-through is no longer acceptable | Track recurring exceptions and unresolved payout deltas | Define containment and rollback path |

Treat payroll references as comparators, not policy defaults#

Use payroll-oriented references as comparators during design reviews. Keep them in a separate "reference used" column so your team can see what came from payroll-oriented guidance and what came from your own ownership, timing, and evidence decisions.

When teams lean on a single payroll-oriented source, scope drift is a real risk. The Internal Revenue Service language, "What is not covered in this publication," is a practical reminder to capture what your model still needs beyond that source.

Verify rule sources before encoding decisions#

For any row tied to regulation or statutory text, log the source view and date markers used at decision time. If you use eCFR, note that it is authoritative for reference but unofficial, and capture both "up to date as of 4/02/2026" and "last amended 2/26/2026" when those markers appear.

Apply the same traceability to version history and filings. A version comparison record with dates like 01/08/25 (introduced) and 06/24/25 (amended), and a filed-date artifact such as "As filed ... on February 10, 2026," can provide a defensible timeline for why a rule was implemented when it was.

For wire cost controls, see Wire Transfer Fees for Platforms and How to Minimize Outbound Costs.

Before locking architecture, map your decision table to concrete status events, idempotency behavior, and reconciliation exports so engineering and finance are designing the same system. Read the docs

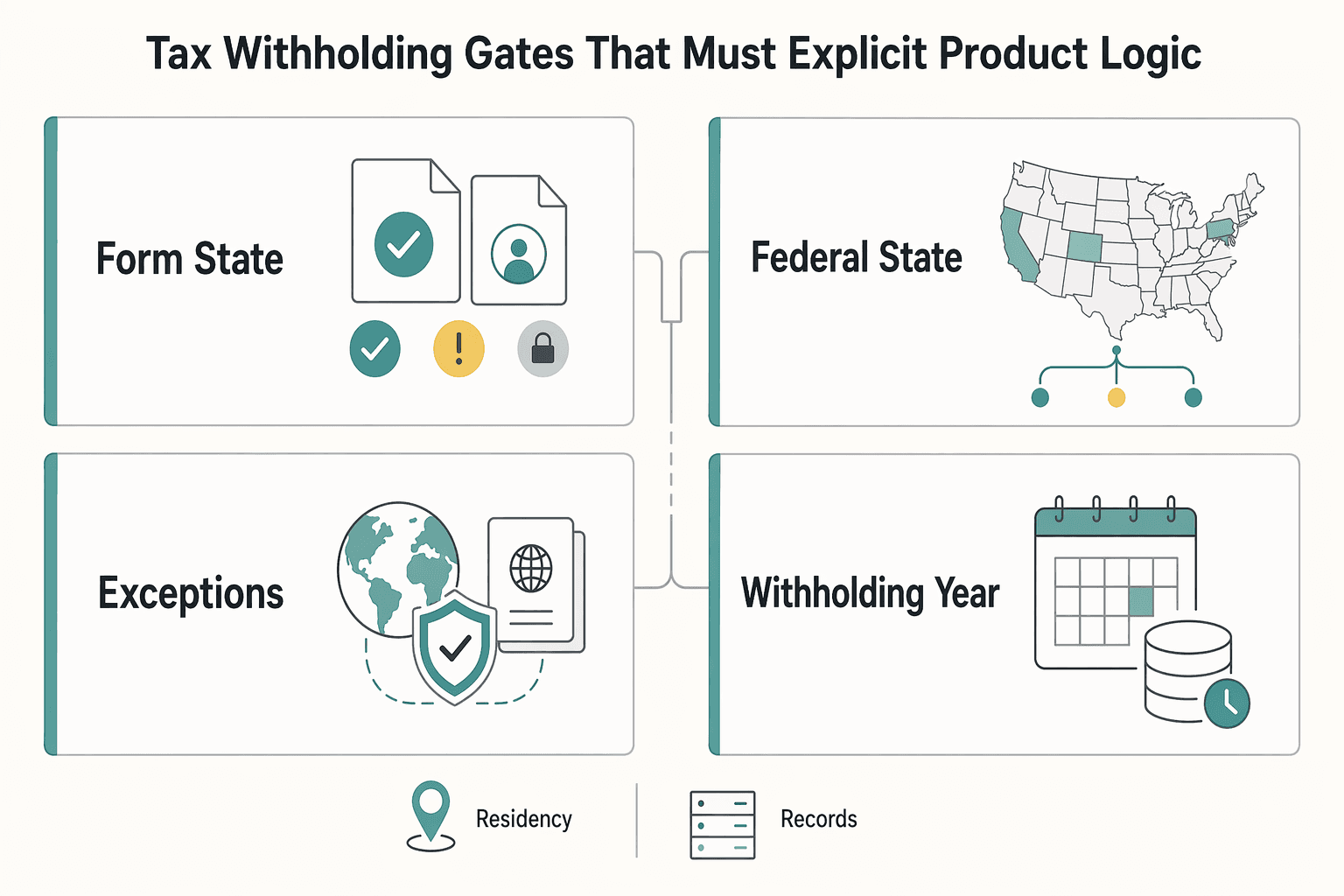

Tax and withholding gates that must be explicit in product logic#

Once you pick ownership and timing, encode the release conditions that stop unsupported payouts. Do not auto-release funds unless your system can show the withholding owner, the jurisdiction branch used, and the form state that made the decision valid.

| Gate | Required record | Release handling |

|---|---|---|

| Form state before release | Form W-4 or Form W-4P type, status, effective date, and who received it | Block release when the state is partial, stale, or unclear |

| Federal, state, and local branching | A distinct branch for Federal Income Tax Withholding and each jurisdiction-specific withholding path | Separate withholding from reporting and remitting behavior in the schema |

| Nonresident exception path | Residency flag, source of that flag, and last-confirmed date | Route to a Notice 1392 path and require review before disbursement |

| Withholding vs year-end reporting | Payout math documents focused on why a payment was released now and reporting documents focused on what must be filed later | Label non-authoritative material clearly |

| Manual review escalation | Resolve the exact missing item: W-4 or W-4P state, residency confirmation, branch ownership, or withholding-vs-reporting classification | Stop the payout and send it to review |

- Gate on form state before release

Treat Form W-4 and Form W-4P as active dependencies, not passive attachments. Store form type, status, effective date, and who received it, and block release when that state is partial, stale, or unclear.

If you use the IRS estimator as a comparison input, keep its limits explicit. It is not for users without a job, pension, or annuity with Federal Income Tax Withholding, and it does not estimate withholding on future income before a job or paycheck starts. Input mistakes can materially skew results, so keep pay-period withheld tax distinct from year-to-date withheld tax in your capture flow.

- Branch federal, state, and local logic separately

Keep distinct branches for Federal Income Tax Withholding and each jurisdiction-specific withholding path, each with its own eligibility evidence and release condition.

Also separate withholding from reporting and remitting behavior in your schema. State materials can split these duties. For example, Missouri lists employer withholding and a separate 12 CSR 10-2.016 Quarter-Monthly Period Reporting and Remitting Withholding Tax entry.

- Force a nonresident exception path

For nonresident U.S. tax status, do not rely on estimator-based assumptions. Route to a Notice 1392 path, require review before disbursement, and keep explicit evidence for that branch: residency flag, source of that flag, and last-confirmed date.

- Separate withholding decisions from year-end reporting

Keep payout math documents focused on why a payment was released now, and keep reporting documents focused on what must be filed later.

Label non-authoritative material clearly. The IRS Entertainment Audit Technique Guide states it is not an official pronouncement of law or IRS position. The MTC guaranteed-payments white paper is marked draft for discussion only.

- Escalate uncertainty to manual review

If withholding responsibility, form validity, or jurisdiction control is ambiguous, stop the payout and send it to review.

Make reviewers resolve the exact missing item, W-4 or W-4P state, residency confirmation, branch ownership, or withholding-vs-reporting classification, so exceptions do not become permanent defaults.

Related reading: Account Takeover in Payout Platforms and How to Stop Payee Hijacks.

Timing logic that explains why calculated net differs from disbursed net#

When amounts across records drift, treat it as a reconciliation-control issue first, then test the arithmetic. Define explicit internal checkpoints and bind each checkpoint to one auditable event.

Do not let one generic status carry multiple meanings. For each checkpoint, store one immutable record with:

- event ID

- effective timestamp

- actor or service

- version reference

Use one designated checkpoint to update reported totals, and reconcile books and records to that single point. This aligns with IRM 4.10.4's reconciliation checkpoint between books/records and reported income. If a later event changes the outcome, record it as a separate adjustment instead of overwriting prior history.

Keep resolution artifacts separate from settlement artifacts. IRM 4.70.14 distinguishes resolution from settlement and includes a Revenue Agent Report in the agreed-resolution path. When versions conflict, reconcile the differences and document technical corrections instead of masking prior entries.

The audit evidence pack every payout needs#

Keep one evidence pack per payout that is complete, minimal, and reproducible from source data.

| Evidence item | What to keep | Grounded note |

|---|---|---|

| Calculation record | Core calculation details from Gross Pay to Net Pay, including deductions and withholding basis used at run time | An operator should be able to verify the booked net from the stored record |

| Settlement proof | Internal and provider-side settlement details | Reconciliation should check for internal and external mismatches before they become backlog |

| Compliance attachments when relevant | Form 8938 attachment and filing timing when it applies | Filing Form 8938 does not remove a separate FinCEN Form 114 (FBAR) obligation, and if no income tax return is required for the year, Form 8938 is not required |

| Masked operational view | Taxpayer name, TIN, and whether foreign deposit or custodial accounts were closed during the tax year | Some accounts maintained by a U.S. payer are excluded from Form 8938 reporting |

| One-click export | An export from the platform record that reconciles Gross Pay to Net Pay without spreadsheet-only logic | This makes reviews easier to repeat under pressure |

- Calculation record

Keep the core calculation details needed to explain every dollar from Gross Pay to Net Pay, including deductions and withholding basis used at run time. An operator should be able to verify the booked net from the stored record, not only from a rebuilt spreadsheet.

- Settlement proof

Include internal and provider-side settlement details so initiation, completion, or failure can be reconciled. Reconciliation should check for internal and external mismatches before they become backlog.

- Compliance attachments when relevant

Not every payout needs foreign-asset reporting artifacts. If Form 8938 applies, attach it to the annual return and file it by that return's due date, including extensions. Filing Form 8938 does not remove a separate FinCEN Form 114 (FBAR) obligation. If no income tax return is required for the year, Form 8938 is not required.

- Masked operational view

For Form 8938 cases, align support data to actual form elements such as taxpayer name, TIN, and whether foreign deposit or custodial accounts were closed during the tax year. Also confirm reportability, because some accounts maintained by a U.S. payer are excluded from Form 8938 reporting.

- One-click export

If feasible, provide an export from the platform record that reconciles Gross Pay to Net Pay without spreadsheet-only logic. This makes reviews easier to repeat under pressure.

For country-level rail selection, see Reduce Payout Fees by Matching Disbursement Rail to Destination Country.

Failure modes that cause payout incidents and how to prevent them#

Frame payout incidents first as evidence and change-control failures, not as proven payout-rail mechanics. Treat root cause as unconfirmed until records show a clear, end-to-end link between gross and net outcomes.

- Calling a duplicate payout a retry race before the record proves it

A double disbursement can be a symptom, but retry races, idempotency keys, or replay-safe writes are not proven as the cause or fix until records confirm it. Confirm the duplicate event in both internal and external records before assigning a mechanism. If that chain is missing, keep it classified as unresolved.

- Using stale or secondary rule references for withholding branches

The supported risk is weak rule-source control, not a proven profile-data branch error. IRS Publication 525 is explicit that severance payments are subject to income tax withholding, so inconsistent withholding outcomes should trigger a source-and-date check first. Use eCFR as a working reference, but remember it is labeled authoritative and unofficial.

- Missing corrections and updates in legal reference change control

FederalRegister.gov states it is not the official legal edition, advises verification against an official edition, and includes links to the official PDF on govinfo.gov. The referenced rule was corrected on 04/16/2024, which is a concrete failure mode if you do not monitor corrections. Record the rule source and review date used for each rule-sensitive calculation.

- Treating reconciliation gaps as known ledger-provider drift too early

Do not treat specific prevention mechanics like daily exception queues or hard close criteria as settled without verifying them against your own records. Apply a stricter standard: do not assign root cause until internal and external records are reconciled. If they do not align, escalate as an unresolved mismatch rather than labeling it as settled drift.

For a step-by-step walkthrough, see How Intermediary and Correspondent Banks Change Payout Outcomes.

Conclusion#

The model that holds up is not the prettiest estimator. It is one operating model with named owners, dated withholding gates, and an evidence trail from Gross Pay to final disbursement so you can show which rule applied and when.

- Pick one deduction model and lock the order in writing.

You do not need a universal payout waterfall. You need one sequence that finance, ops, product, and engineering apply the same way every time, with clear ownership and timing for when each amount becomes final. That clarity is especially important where withholding is involved. Under Canada Income Tax Act section 227(4), deducted or withheld amounts can be deemed separate from payer property and held in trust for remittance.

- Set withholding gates before release, and treat shortfalls as a required branch.

A payout is not complete just because the commercial math is complete. You also need enough information to apply the correct withholding path and enough available funds to satisfy it. ACF guidance for processing an Income Withholding Order or Notice, current as of April 30, 2024, explicitly includes "Not Enough Money to Withhold Full Ordered Amount." If your flow has no branch for that case, pause, review, and document before disbursing.

- Keep reporting evidence and payout evidence in one audit path.

The final net number is not enough on its own. Keep classification, deduction lines, withholding basis, and reporting artifact together in the same transaction record. CRA's fee-for-service guidance shows why: these payments generally require a T4A slip, but some cases require T4A-NR, T5018, or T1204 instead. If those branches live outside the payout record, audit reconstruction can become manual.

A final caution: do not copy payroll logic into platform disbursing without defining scope. Oracle payroll guidance notes that some pre-tax deduction categories have different tax and withholding treatment. It also notes that tax-related data may need to be maintained by PRE (Provincial Reporting Establishment). Use that as a design reminder to keep jurisdiction and payment type explicit, not as a blanket rule for every platform flow.

If your process cannot show one auditable path from Gross Pay to disbursed net, fix the model before adding volume. The goal is proof, transaction by transaction, of what was deducted, why, who owned it, and what was sent.

If you are moving from model selection into rollout, use this as the next checkpoint for compliance-gated disbursements, provider status tracking, and batch operations where enabled. Explore Gruv Payouts

Frequently Asked Questions

What is a gross-to-net payout calculation for a platform, and how is it different from payroll take-home calculations?

A platform gross-to-net view can separate commercial deductions from tax-withholding rules. Payroll-oriented withholding tools are built around wage or pension and annuity contexts, including Form W-4 or Form W-4P. The IRS also says its Tax Withholding Estimator is not for estimating withholding on future income before a paycheck and is out of scope if there is no job, pension, or annuity with federal income tax withholding.

What should be deducted first in a platform payout waterfall?

The provided sources do not establish one universal deduction order for platform payouts. Treat the sequence as a policy decision you define and document, not a default you can safely copy. If teams describe different orders for the same payout, resolve that before you scale.

Who is responsible for withholding and remittance in multi-party payout flows?

The provided sources do not give a single platform-wide responsibility rule for multi-party payout flows. What they do support is that liability can extend to third parties paying or providing for wages under 26 CFR 31.3505-1. In practice, assign responsibility explicitly in your legal and finance operating model before launch.

Why can calculated net and disbursed net differ on the same transaction?

From this evidence set, you can ground withholding treatment and payment classification, but not payout-rail timing causes for net differences. Classification matters: periodic payments are treated differently from nonperiodic distributions for withholding purposes. For nonperiodic distributions, the default withholding rate is 10% unless another rate is elected, and Form W-4R allows elections from 0% to 100%.

What data fields are required to make gross-to-net calculations audit-ready?

These sources do not provide a universal platform field checklist. For withholding-sensitive cases, keep the governing form or election context clear, including whether Form W-4P or Form W-4R applies. Also preserve residency-related decisions, since nonresident taxpayers cannot use the IRS Tax Withholding Estimator and are directed to Notice 1392.

How do we reduce duplicate payouts and retry-related errors?

This evidence pack does not support a specific technical control pattern for duplicates or retries. This question should be handled by internal engineering policy rather than inferred from these sources.

When should we move from a simple payout model to a managed withholding model?

There is no fixed threshold in these sources for when to switch models. A source-grounded indicator is when outcomes depend on form state and payment classification, including W-4P for periodic treatment and W-4R for nonperiodic withholding elections. Nonresident handling under Notice 1392, plus payer notification obligations for pension or annuity withholding elections, can also indicate added operational complexity.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Platform Economics 101 for Commission Fees, Payout Costs, and Gross Margin

**Use gross margin, not top-line fee percentage alone, to make pricing decisions.** If your fee model stops at commission revenue, it is not ready for a pricing decision.

Affiliate Network Payout Structures for Publisher Commissions

Commission design is an operating decision, not a pricing footnote. The structure you choose affects what behavior you reward and the economics of the program. It is easy to announce rates. It is much harder to define a model that still holds up once reversals, edge cases, and partner questions start showing up.

Calculate NRR for a Subscription Platform Without Reconciliation Gaps

The formula is the easy part. In practice, the hard part is producing a single Net Revenue Retention number that finance, ops, and product can all trace to the same recurring revenue base and the same set of in-period movements.