Quick Answer

Use a country-by-country routing sequence: block ineligible rails, then price only the remaining options, then execute with auditable controls. For each payout, validate corridor fields and compliance blockers before comparing SWIFT, ACH, and real-time payments (RTP). Log fee and FX inputs with timestamps, apply explicit if/then fallback order, and store selected rail, rejected rails, and provider reference. Keep retries tied to one idempotency key and reconcile webhook state changes into the ledger journal.

How Country-Level Rail Routing Controls Payout Costs#

Use country-level routing decisions to control payout costs, rather than forcing every payout through one default rail. A single default can trade simplicity for higher cost. A practical approach is to decide at the country level: rule out rails that cannot work, compare full landed cost, then review results against live operations instead of provider defaults.

One scope note: the source material available for this section does not provide payout-rail benchmarks or routing-outcome evidence. It covers railway freight and public-budget documents, not payout operations. So treat this section as a method framework, not as a claim about measured payout-fee performance.

- Remove ineligible rails first.

Treat a rail as ineligible when destination-country, currency, beneficiary setup, or compliance requirements rule it out. Before you compare options, make sure each payout record includes the minimum routing envelope: destination country, corridor, currency, amount, urgency, beneficiary type, and required compliance or tax fields. If required data is missing, handle it as a stop condition rather than a soft warning.

- Compare total landed cost, not only the visible fee line.

Use one consistent pricing method per corridor, and keep assumptions current and traceable. As a checkpoint, make sure fee inputs and any conversion assumptions are timestamped and linked to the payout record. If the quoted cost cannot be explained from recorded inputs, avoid automating routing on top of it.

- Apply routing rules, then tune them with live results.

Once eligibility and landed cost are defined, write explicit if/then rules so Finance, Ops, and Engineering can explain why a payout took a given path. For each payout, store the selected route, rejected routes, decision reason, provider reference, and final outcome. That record helps when a payout is late, duplicated, or questioned, and it highlights tradeoffs over time. A slightly more expensive route may still be preferable if it protects service levels and reduces repeated failures in a country.

That sequence is simple on purpose. If you skip to fee comparison first, you can end up optimizing a number that does not hold up in real operations. Start with a narrow country set, validate the routing logic on live traffic, and use observed outcomes to guide the next round of savings. For a step-by-step walkthrough, see How to Reduce Stripe Processing Fees.

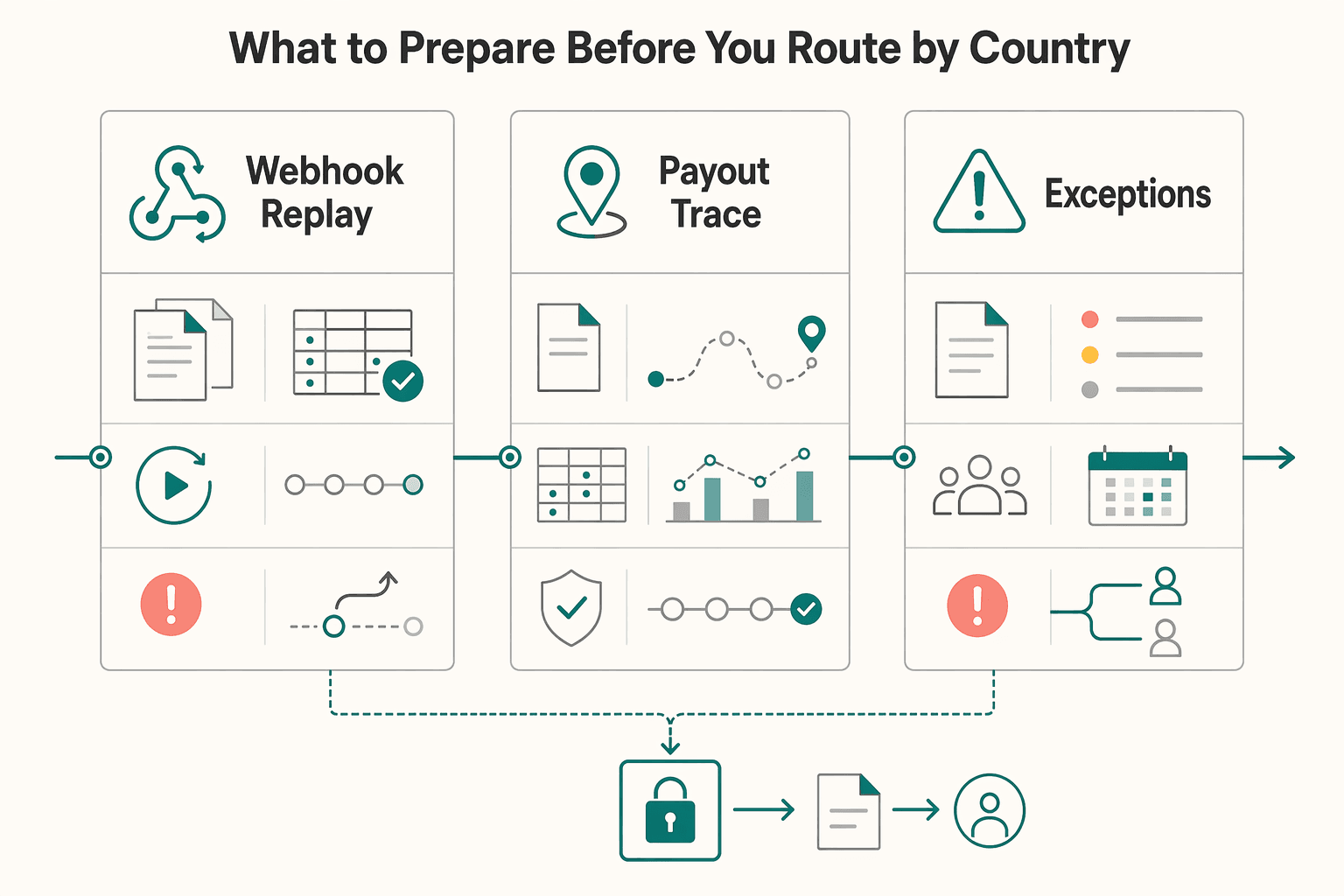

What to prepare before you route by country#

Get your operating inputs and controls in place before you compare rails; otherwise fee comparisons are hard to trust or audit.

- Set clear owners first.

Define who owns cost policy (Finance), exception handling and SLA operations (Payments Ops), and routing/idempotency behavior (Engineering). Also set one explicit override path so route changes are controlled and traceable.

- Require a complete payout envelope before routing.

Validate destination country, corridor, currency, amount, urgency, beneficiary type, and your required KYC/AML blocker fields before submission. If any blocker field is missing, treat the payout record as incomplete. If your flow includes EU online consumer payments, note the cited rule that payments above €30 require two authentication elements.

- Document landed-cost inputs with source and timestamp.

For each corridor, record the source and capture time for FX spread versus mid-market rate, plus expected wire transfer fee, currency conversion fee, and intermediary bank fee treatment. Keep pricing assumptions tied to the payout record; even commonly cited ranges, for example 1-3% conversion fees in travel guidance, vary by bank.

- Create an auditable trail before launch.

Prepare a route decision log, provider response log from webhook events, and accounting trace in your ledger journal so each payout can be followed from decision to final booked entry.

If you want a deeper dive, read Local Bank Transfer Networks by Country: A Platform Operator's Global Payout Rail Map.

Build your country rail eligibility map first#

Start by removing rails that are not usable for the destination, currency, beneficiary bank, or compliance state. Comparing fees before eligibility creates false choices and avoidable exception work.

| Rail | Shared fields | Rail-specific notes |

|---|---|---|

SWIFT | Country/currency support, beneficiary-bank reachability, supported payout types, fallback rank | Bank/account-data constraints, cutoff behavior |

ACH | Country/currency support, beneficiary-bank reachability, supported payout types, fallback rank | Program-specific bank constraints, settlement window notes |

real-time payments (RTP) | Country/currency support, beneficiary-bank reachability, supported payout types, fallback rank | Instant-scheme constraints, cutoff or availability notes |

- Build one country matrix that answers eligibility before cost.

Create a row per destination country, and split by corridor or payout currency where behavior differs. For each row, mark whether SWIFT, ACH, and real-time payments (RTP) are eligible based on currency support, beneficiary reachability, and beneficiary-bank constraints. Use the matrix to capture the fields in the table above.

Verification checkpoint: test your top payout countries against real beneficiary-bank examples. If your team cannot answer reachability from one place, the map is not ready.

- Add compliance gates as hard blockers, not scoring inputs.

Missing KYC, missing Know Your Business (KYB), or unresolved AML flags should remove a rail before any fee comparison. If compliance is treated as a soft penalty, late failures and stuck payments become more likely.

Keep compliance status in the same matrix row used for rail eligibility. Use a binary rule: eligible only when compliance status is pass; incomplete records do not proceed to rail selection.

- Capture operational constraints in the same row so routing works in production.

A rail can be technically available and still fail your operating needs. Add columns for supported payout types, settlement window labels your team uses, cutoff behavior, and provider/program notes where coverage varies by market.

Keep this in one place, not split across provider docs, tickets, and tribal knowledge. That is how you avoid low headline fees turning into high workflow cost.

- Define fallback order for every country before automation.

End each row with a clear fallback order across eligible rails. If the preferred rail is unavailable for that beneficiary bank, currency, or compliance state, routing should move to the next pre-approved option.

Validate this with dry runs: force first-choice ineligibility and confirm clean fallback with the reason logged. That is what makes the map reliable in live operations.

Calculate total landed payout cost not just fees#

Once eligibility is set, compare rails on total landed payout cost, not the lowest headline fee. Use the full end-to-end view for each corridor so obvious and hidden costs are both counted and you avoid cost blind spots.

Build one corridor formula and apply it consistently#

Use one cost model per corridor across SWIFT, ACH, and real-time payments (RTP), with the same component structure for every rail. If one option includes extra charges and another does not, the comparison is not decision-grade. Your checkpoint is reproducibility: Finance or Ops should be able to rebuild a past routing decision from the logged inputs and get the same result.

Price conversion inputs on a consistent basis#

When FX is involved, log inputs the same way every time - source, timestamp, and reference basis - so conversion impact is comparable across options. If an input is stale or cannot be verified, do not use it in the decision model. This keeps "cheap on paper" routes from winning because of inconsistent quote handling.

Separate fixed and variable cost drivers before batching#

Split fixed charges from variable charges in the model so batching is a deliberate choice, not a default. Batching often helps when fixed costs dominate, but the effect is smaller when variable costs are the main driver. Keep both single-payout and batched views in the same corridor model so tradeoffs are explicit.

Stress-test by urgency and transfer size#

For each country corridor, run at least these scenario pairs: urgent vs standard, and low-value vs high-value. Use recent exception history where available so expected rework is reflected instead of assumed away. Document assumptions and inputs in a versioned decision sheet per corridor. Related: Payout Failure Benchmark Report: Success Rates by Rail, Country, and Error Code.

Set routing decision rules that balance cost speed and risk#

Make routing deterministic: evaluate the transaction, weigh cost and performance together, execute the best eligible route, then feed outcomes back into the next decision cycle. That keeps cost control from turning into inconsistent, person-by-person choices.

| Rule input | Routing use | Note |

|---|---|---|

| Policy/compliance pass | First tie-breaker when two eligible routes are close | Keep the order stable |

| Landed cost | Second tie-breaker when multiple routes are eligible | Use the same inputs every time |

| Predicted settlement time | Third tie-breaker | Keep inputs explicit, including payout urgency and payout window |

| Recent failure risk | Fourth tie-breaker | Use your own error trends |

| Urgency override | Route to the faster eligible option when the lower-cost route is likely to miss the promised window | Record why |

| No-go states | Stop execution when required checks or required payout documentation are unresolved | Log the blocker and wait for correction instead of auto-retrying |

Write each country/corridor rule in plain if/then form so the same inputs produce the same route every time. Keep the inputs explicit, for example corridor eligibility, payout urgency, and payout window, and define which route is preferred when multiple options are eligible.

When two eligible routes are close, lock tie-breakers in one order and keep that order stable. A practical sequence is policy/compliance pass, landed cost, predicted settlement time, then recent failure risk from your own error trends.

Add an urgency override so low direct fees do not silently break delivery expectations. If the lower-cost eligible route is likely to miss the promised window, route to the faster eligible option and record why.

Define no-go states as explicit blocks, not silent queues. If required checks or required payout documentation are unresolved under your own policy, stop execution, log the blocker, and wait for correction instead of auto-retrying.

Finally, make outcomes operational, not archival: feed settlement performance and failure patterns back into rule updates on a fixed cadence. Related: Contractor Payout Speed Calculator by Rail and Country.

Implement payouts with controls engineers and ops can trust#

After you set routing rules, execution should be predictable: one payout intent creates one payout, state changes reconcile cleanly, and the record explains why ACH, SWIFT, or real-time payments (RTP) was used.

Require an idempotency key on every payout create call#

Make duplicate prevention non-negotiable: the same payout intent should always reuse the same key. Generate the key from your platform's payout intent, not a temporary request ID, and if transport fails after submit, replay the same create request with the same key before anything else.

Treat changed amount, currency, or beneficiary details as a new intent with a new key. A practical staging check is to send the same create request twice and confirm you get one payout record and one provider reference.

Process every provider state change through a webhook and reconcile it into the ledger journal#

Make the webhook stream your source for payout state transitions, then post each transition into your journal in a clean, auditable sequence. For each event, store the provider reference, event ID, prior status, new status, and timestamp.

This control matters because reconciliation across disconnected systems gets messy quickly. Build handlers to tolerate replayed or late events so the same journal movement is not posted twice.

Store the routing evidence, not just the final rail#

Keep the full decision trail per payout: selected rail, rejected rails, decision reason, and provider reference at execution. If urgency forced SWIFT over ACH, that should be visible directly in the payout record, not buried in logs.

Your audit checkpoint is simple: Ops or Finance should be able to reconstruct the routing decision from one record.

Use Virtual Accounts and Merchant of Record (MoR) flows where they reduce operational splits#

Use consolidation flows only where they reduce fragmentation between collection, conversion, and disbursement. In practice, fewer split systems can mean fewer engineering handoffs and fewer reconciliation mismatches for Ops, especially as each added rail or provider link adds implementation and maintenance overhead.

Keep this recommendation narrow and corridor-specific. Do not assume a Merchant of Record (MoR) model removes every local-entity or compliance obligation in every jurisdiction.

Handle exceptions and recover failed payouts quickly#

Recovery should run as a standard operating flow, not one-off firefighting, so failed payouts do not erase your routing gains.

Classify the failure before you retry anything#

Start by classifying each exception into a small set of buckets your team uses consistently: compliance hold, reachability failure, beneficiary data error, provider timeout, and settlement delay beyond SLA. Record the bucket with the provider error code, rail attempted, corridor, and the time the SLA clock started.

Your quality check is consistency: two operators reviewing the same payout should choose the same bucket from the stored evidence alone. Keep one nuance explicit in playbooks: an ACH payout can still be in normal processing, since ACH typically settles over several business days.

Match the recovery action to the bucket#

Apply the smallest corrective action that fits the bucket. For beneficiary data errors, fix the data first, then retry the same eligible rail. For reachability issues or delays that now put timing at risk, reroute using your preapproved fallback order, for example ACH to SWIFT.

Use extra caution with real-time payments (RTP): once confirmed, they are final and irrevocable. After a timeout, confirm outcome before you retry so you do not create a duplicate payout.

Escalate repeated patterns and notify recipients with status-based templates#

Escalate patterns, not single tickets. If the same bucket repeats in one corridor, have Payments Ops and Engineering review routing logic, fallback order, and provider behavior together.

In parallel, tie recipient communication to payout status: received, delayed for review, data correction needed, resent, settled. That keeps support responses consistent while recovery is in progress.

Track performance and continuously tune routing#

To keep payout fees down, treat routing as a continuous control loop: monitor corridor-level outcomes, review on a fixed cadence, and update DecisionRules only when the data shows drift.

Instrument the metrics that expose routing drift#

In Datadog, track four corridor-and-rail metrics: total landed cost per successful payout, success rate, median settlement time, and manual touch rate. Count outcomes consistently so a payout can be marked successful while still surfacing rework in manual touch rate.

| Metric | Scope | Note |

|---|---|---|

| Total landed cost per successful payout | Corridor and rail | Validate against ledger journal exports on a recurring sample |

| Success rate | Corridor and rail | Count outcomes consistently |

| Median settlement time | Corridor and rail | Validate against ledger journal exports on a recurring sample |

| Manual touch rate | Corridor and rail | A payout can be marked successful while still surfacing rework |

Validate those metrics against ledger journal exports on a recurring sample. If a payout cannot be traced from observed outcome to ledgered rail, state, and cost components, your routing data is not reliable enough for rule changes.

Review outcomes on a fixed cadence and update DecisionRules deliberately#

Run the review on a fixed schedule and focus on drift in FX behavior, fee behavior, and repeated failure patterns. When drift appears, update and version DecisionRules with a clear before/after metric slice, affected corridor, and effective date.

Run a monthly finance-ops-engineering checkpoint from ledger journal exports#

Use one shared monthly checkpoint across Finance, Ops, and Engineering. Confirm cost deltas, SLA adherence, and reconciliation completeness from ledger journal exports.

If reconciliation breaks for a corridor, pause additional routing changes there until traceability is restored.

Keep tax and compliance edge cases visible in reporting#

Keep Form 1099, FBAR, and Foreign Earned Income Exclusion (FEIE) workflow dependencies visible in reporting where enabled, alongside payout outcomes.

For FEIE, keep the workflow logic tied to eligibility requirements rather than payout status alone: eligibility requires meeting conditions, including a tax home in a foreign country, and one qualifying path uses the physical presence test of 330 full days in a 12-month period. The physical presence test applies to both U.S. citizens and U.S. residents. U.S. citizens or resident aliens living abroad are taxed on worldwide income, and even when FEIE applies, they still file a tax return reporting that income.

For tax year 2026, the maximum FEIE is $132,900 per person, and the maximum is adjusted annually for inflation. Treat these as reporting and workflow dependencies, not assumptions inside payout routing logic. Need the full breakdown? Read How to Apply for a Withholding Certificate to Reduce FIRPTA.

Conclusion and copy paste launch checklist#

For launch, keep the plan conservative and explicit about uncertainty. Even the World Bank focus note includes an accuracy disclaimer, so the checklist should prioritize verification before scale.

- Define scope before decisions.

Document exactly which payment flows, markets, and constraints this launch covers, and keep anything out of scope clearly marked. The checkpoint is simple: a teammate should be able to read the scope and know what this plan does and does not decide.

- Separate confirmed inputs from assumptions.

For each major decision, label what is directly supported versus what is an internal assumption. If a decision depends on an assumption, record how you will validate it before expanding usage.

- Carry forward an explicit data-confidence note.

Add a plain-language caveat in your internal launch docs that source material may have limits and should be validated in your operating context. This prevents teams from treating external guidance as complete or final.

- Require traceable decision records.

Keep an audit-ready log of who approved each rule, what information they used, and when the decision was made. If you cannot explain a decision after the fact, treat that as a launch blocker.

- Time-box a mandatory recheck.

Set a review date and re-verify assumptions against the latest available guidance before broad rollout. As a baseline, note that the referenced World Bank focus note is dated February 2025.

This pairs well with our guide on How Interchange Fees Change the Price You Need to Charge.

Frequently Asked Questions

What is the fastest way to reduce payout fees by country rail without increasing payout failures?

Start with your highest-volume payout flow, not every route at once. Compare viable rails on total landed cost, change one routing preference at a time, and verify that settlement and reconciliation still look clean before you scale the change.

How do we choose between `SWIFT`, `ACH`, and `real-time payments (RTP)` for a specific destination country?

Start with rails that are available for the payer/payee path and use case, then compare cost and timing. ACH is a batch rail and is commonly cited at 1-3 business days, so it usually fits when that window is acceptable. For high-value international payouts, some businesses may still choose wires despite higher fees because of reliability.

Which matters more in practice for total cost, rail fee or `FX spread`?

There is no single winner in every case. The safer approach is to compare full landed payout cost across your viable rails and review outcomes over time, rather than optimizing only one visible fee line.

When should we group transfers into a `payout batch` instead of sending individual payouts?

Use batching when recipients can tolerate a slower settlement window. Batch rails such as ACH process in batches and are commonly cited at 1-3 business days, so they are typically a better fit for non-urgent payouts.

What should we do when the lowest-cost rail is not reachable for the beneficiary bank?

Do not force it. If the lowest-cost rail is unavailable for that payout path, route to the next viable option and record why the original rail was not used.

How should we route urgent payouts when the cheapest eligible rail may miss SLA?

Route to the faster viable rail and record that speed overrode direct cost. That is especially reasonable for high-value or time-sensitive payouts, where some businesses accept higher wire fees for reliability.

What minimum controls do we need for safe retries, auditability, and reconciliation?

At minimum, keep clear records of the selected rail, any fallback decision, and final settlement status, then reconcile those records to your ledger. If a payout cannot be traced from routing decision through settlement, fix that gap before expanding.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Choosing Local Bank Transfer Networks by Country for Platform Payouts

Treat this as a decision map for operators, not a glossary of payment acronyms. The goal is to help you choose a payout rail you can actually launch, support, reconcile, and defend when market or provider conditions shift.

Payout Failure Benchmark Report for Platform Teams

A useful **payout failure benchmark report** is not a prettier exception export. It is the operating document that tells your platform team which payout failures are real rail problems, which ones are recipient-data problems, which ones were held before release, and which ones were later recovered.

Contractor Payout Speed Calculator by Rail and Country

If you treat payout speed like a front-end widget, you can overpromise. The real job is narrower and more useful: set realistic timing expectations, then turn them into product rules, contractor messaging, and internal controls that support, finance, and engineering can actually use.