Quick Answer

Start by treating account takeover payout platform payee hijack fraud as a release-control decision, not only an authentication issue. Put explicit hold/release rules around payout-destination changes, require secondary verification when session or device context looks abnormal, and log who approved each outcome. Build one evidence trail that links edit history, approval actions, and final payout status so compliance and legal teams can escalate quickly when signals conflict.

Why Account Takeover Is Different in Payout Platforms#

Treat account takeover payout platform payee hijack fraud as a money movement control problem first and an account security problem second. Once an attacker can change payout details, contact points, or credentials, the issue is no longer just login abuse. It becomes a question of who can stop funds, who can approve a release, what evidence exists, and how quickly finance, risk, compliance, and legal can reconstruct the timeline.

- Reframe the exposure around disbursement loss.

Public summaries already make the core risk plain. IC3 defines Account Takeover Fraud as unauthorized access to victim accounts for financial or information theft, and notes that attackers may "steal funds, redirect paychecks, or otherwise affect funds of the targeted victim." Federal Reserve Financial Services describes ATO as causing significant losses through unauthorized fund movement and warns that attackers may also change account information such as the user's email address or phone number. In a payout context, that detail matters because contact-point changes can cut off the real payee right when your team needs to verify a bank change or place a hold.

- Put the right owners in the room early.

This guide is for the people who own decisions after a suspicious payee edit appears, not just the people who tune login controls. That usually means compliance, legal, finance, risk, and payout operations, each with named authority for holds, verification, release, and evidence retention. A practical checkpoint is simple: if your platform cannot show who changed the payee-linked destination, what approval action followed, and when funds were released, you have a governance gap, not just a fraud problem. One failure mode to avoid is routing these events into a generic AP or customer support queue, where the issue gets treated as a profile update instead of a live disbursement redirection risk. If you own this queue, make sure your reviewer can see that chain without asking another team for screenshots.

- Use the rest of this guide to make those decisions explicit and document the limits.

What follows is a working structure for prevention, detection, response, and evidence handling, with clear tradeoffs between payout friction and loss prevention. The focus is on auditable controls: what to verify before release, what should trigger a hold, what artifacts to preserve, and how to build a defensible incident record while facts are still developing. Keep public threat data in proportion. IC3 reported more than 5,100 ATO complaints with losses exceeding $262 million since January 2025, while FRB Services cited more than $15.6 billion in reported U.S. losses in 2024 and over 36% growth in reports versus 2023. Those figures support urgency, but they do not give you a platform-specific ownership model or legal escalation threshold. Where jurisdiction-specific duties or filing choices matter, you will still need specialist counsel.

Define the exact payee hijack risk you are controlling#

Define this as an ATO-driven payout redirection risk, not just a bank-detail update. For account takeover payout platform payee hijack fraud, scope the event to unauthorized access, payout-detail swaps, credential abuse, and session hijacking when those actions can lead to a released disbursement.

Step 1#

Use one policy sentence for the threat: an unauthorized actor gains access to a payee account, changes the payee-linked payout destination or related contact credentials, and triggers or attempts a disbursement. This keeps your definition aligned with FRB Services' ATO framing: unauthorized access, potential fund transfer or withdrawal, and possible changes to email, phone, or credentials.

Run a quick intake check: do you capture all three elements together - access method, destination change, and payout status? If the record only says "bank details edited," your scope is too narrow.

Step 2#

Separate this event type from adjacent fraud queues before assigning owners. A payee hijack can look like a supplier-data change, support ticket, or Accounts Payable controls exception, but the risk changes when account access abuse is part of the same event.

LSEG's ATO patterns support that boundary: fraudulent payee additions and manipulated bank details used to divert payments. If you route these as routine master-data corrections, teams may review only the edit and miss the login, session, or contact-point changes that enabled it.

Step 3#

Keep external framing brief and defensible. IC3's November 25, 2025 alert describes ATO as unauthorized access to online financial, payroll, or health savings accounts and states that victims include individuals, businesses, and organizations across sectors. FRB Services' February 17, 2026 summary recognizes the same ATO category.

That is enough to support a dedicated internal definition without treating "payee hijack" as a universal legal label.

For a step-by-step walkthrough, see How to Hedge FX Risk on a Global Payout Platform.

Prepare owners systems and evidence before rollout#

Pre-rollout clarity on ownership and evidence is a control requirement, not admin overhead. If either is ambiguous, the first live incident turns into a delay over who can hold or release funds and which record is reliable. If you are launching this control, assign the hold owner and the record of truth before your first live exception.

| Evidence item | Keep for every payee-change event |

|---|---|

| Payout details | Before/after payout details |

| Actor | Actor ID |

| Time | Timestamp |

| Approval | Approval record |

| Verification | Payee Verification outcome |

| Overrides | Case notes for any override or release |

Step 1#

Assign named people, not shared teams, to payout-stopping decisions. At minimum, name owners for KYC exceptions, AML review and hold decisions, legal escalation, and payouts ops release authority, with a named backup for each decision type. We recommend naming the person your team calls when a payout must stop in minutes, not hours.

This follows a recognized compliance pattern: day-to-day BSA/AML coordination is assigned to a designated officer, not an unnamed group. Use that same accountability principle across your payout hijack controls.

Checkpoint: an analyst should be able to identify, immediately, who can place a hold, release a hold, require re-verification, and approve a legal exception.

Step 2#

Define which system records are authoritative for incident reconstruction before launch. In practice, this usually includes payout events, approval logs, account change history, and audit-trail records tied to payee profiles and payout destinations.

Also define your record-trust conditions upfront: whether logs are append-only or otherwise tamper-evident, who can modify entries, and how timelines are reconciled across systems. The goal is one agreed sequence for what changed, who approved it, and whether funds moved.

Step 3#

Set a minimum evidence pack for every payee-change event and retain it for investigation, dispute handling, and legal review. At minimum, keep before/after payout details, actor ID, timestamp, approval record, Payee Verification outcome, and case notes for any override or release.

Treat log design as investigation readiness, not just collection. If your team cannot retrieve a complete test evidence pack without ad hoc engineering exports, the control is not ready for rollout. If your analyst still needs engineering to pull the record set, your evidence design is incomplete.

Do not set one global retention period across all markets. Some U.S. records, for example, require retention for five years after account closure, and BSA retention duties can be additional to other legal requirements.

Step 4#

Document market and program differences for KYC/KYB depth so teams do not apply one global assumption everywhere. A risk-based approach means controls should vary by risk, jurisdiction, and use case.

Keep ownership-threshold rules jurisdiction-specific. In one U.S. CDD context, beneficial ownership includes individuals who own 25 percent or more of a legal entity customer, but that threshold should not be treated as universal. Your coverage note should state where each threshold applies, where it does not, and who approves differences.

Related: Source of Funds Checks for High-Risk Payout Accounts: When Platforms Need More Than KYC.

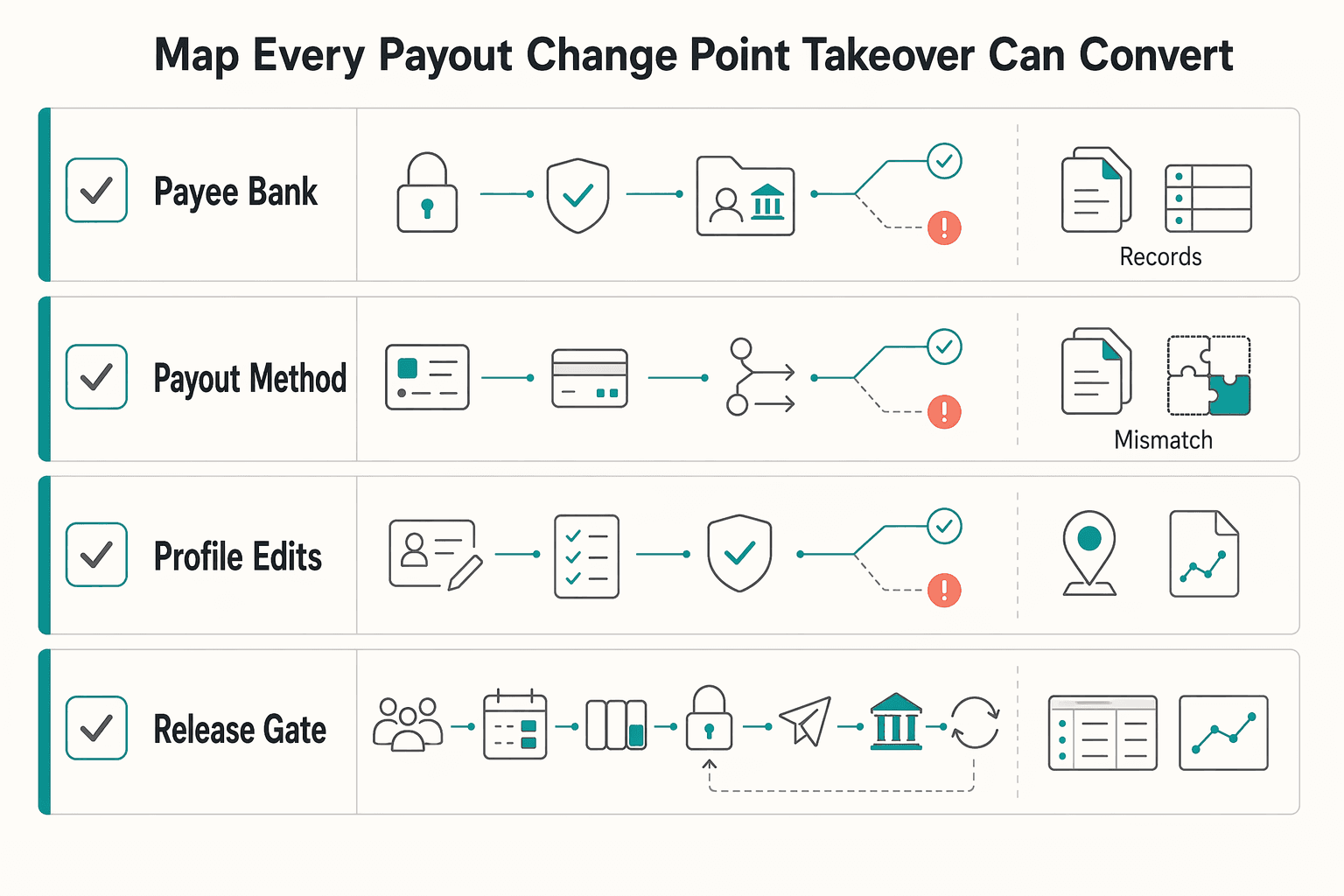

Map every payout change point where takeover can convert to loss#

Map every point where an authenticated session can still redirect money, not just the login event. If you cannot trace a payout change request from session creation to final release in one timeline, treat that as a control gap and pause automation expansion. If you cannot walk your team through that path on one screen, the mapping is not done.

Step 1. Draw the full path from sign-in to payout outcome. Start at first authentication and continue through payout execution confirmed or rejected. Include login, step-up challenge, payee profile access, payout detail edit, approval, queueing, release, retries, and settlement status updates. ATO loss often happens after access is established, not at the login screen.

Mark where Device-Based Risk Signals can block or trigger step-up verification before value leaves. Use signals such as IP address, geolocation, request timing patterns, and browser metadata as gating inputs for high-risk actions, not proof of fraud. Log both the gate decision and the protected action.

Use one quick test: pick a recent payee-detail change and ask an analyst to reconstruct, in order, the session ID, actor, device/browser context, change request, challenge result, approval record, and final payout status. If that requires multiple tools and ad hoc data work, your map is incomplete.

Step 2. Classify actions that can convert access into loss. Apply the most friction to edits that change payment instructions or reduce resistance to payout release.

| High-risk action | Why it matters | Minimum checkpoint before release |

|---|---|---|

| Payee bank change | Directly changes where funds go | Out-of-band confirmation of changed account information or payment instructions, plus logged risk review |

| Payout method change | Can reroute payment rail and destination behavior | Fresh session review and secondary confirmation before the next payout uses the new method |

| Profile edits (email/phone) | Can let attackers control later verification or notices | Step-up when edits follow unusual IP, geolocation, timing, or browser patterns |

| Payout release approval | Last chance to stop value leaving | Log approver, approval time, and exact change history reviewed before release |

For payment-instruction changes, keep confirmation outside the original communication method. If confirmation stays inside the same compromised session or mailbox, the control has not separated attacker access from approval.

Step 3. Add a checkpoint for tax-profile-linked edits. Treat tax-profile edits as control-relevant when they occur near payout-detail changes. Do not assume every W-9 or W-8 BEN update is fraudulent, but link the review because W-9 provides a correct TIN to payers and W-8 BEN is submitted when requested by the payer or withholding agent for foreign-status and withholding context.

When payout details and W-8/W-9 profile updates occur close in time, force linked review instead of separate queues. Preserve before/after tax profile state, who made the edit, and whether withholding or reporting treatment changed. IRS requester instructions also cite potential 30% or 24% withholding consequences when valid documentation is not obtained and obligations are not met.

Step 4. Keep delayed and retry paths in the same forensic timeline. Include queued payouts, delayed releases, retries, and manual reruns in the same forensic timeline. Stolen session cookies can allow authenticated access without credentials, and idle periods increase endpoint hijacking risk.

A common failure mode is a clean approval record followed by value leaving during a later retry or delayed execution. Build one timeline that links request, approvals, queue events, retries, and final release. If your logs cannot connect those states end to end, stop expanding straight-through payout automation until that gap is closed.

Set layered controls with explicit pass fail rules#

Set pass/fail rules by action type and session context so high-risk payout changes fail closed until verified. A valid login alone is not enough for high-risk payout actions, and layered controls should apply stronger authentication or equivalent controls to higher-risk transactions. We recommend writing the release rule so your reviewer can apply it under queue pressure without guessing.

Step 1#

Start with a simple control matrix, then tune it by product, market, and payee type.

| Action tier | Example action | Minimum gate | Fraud-loss prevention | Payout friction |

|---|---|---|---|---|

| Low | Non-sensitive profile edit with no payout impact | Log only, alert on pattern clustering | Low direct protection, useful for investigations | Minimal |

| Medium | Email or phone update, or profile edits that can affect later verification | Risk-based step-up using behavior and context signals | Helps stop follow-on takeover activity | Moderate |

| High | Bank account change, payout method change, or payout release after a recent payout-detail edit | Temporary hold, re-verification, and secondary named review before release | Highest protection against redirected funds | Highest |

The tier label matters less than the release rule: high-risk actions should not clear on an existing session alone.

Step 2#

Write the rules in plain, operational language. Example: if a payout-destination edit appears with anomalous session context, place the payout on hold and re-verify before release.

Re-verification should be outside the potentially compromised path. Preserve one auditable record with pre/post payout details, session identifier, risk signals, challenge result, re-verification result, reviewer identity, and final disposition. For implementation detail, see Payee Verification at Scale: How Platforms Validate Bank Accounts Before Sending Mass Payouts.

Step 3#

Connect fraud gates to existing compliance workflows so reviewers see the full risk picture at one decision point. Effective due-diligence processes are the framework that supports monitoring and reporting, so your review screens should surface current CDD/KYC state, active AML holds, and any source-of-funds requirements already defined in your policy.

Document the tradeoff and the override path explicitly.

| Decision path | Fraud-loss prevention | Payout friction | Minimum documentation |

|---|---|---|---|

| Standard high-risk gate (hold + re-verification + secondary review) | Higher | Higher | Rule trigger, verification performed, approver/rejector, timestamped disposition |

| Senior override for documented urgency | Lower than standard gate | Lower than standard gate | Senior sign-off, written reason, control bypassed, timestamp |

Single-point controls fail when the only meaningful check happens too late in the payment flow. Explicit layered rules close that gap and make exceptions reviewable later.

ATO pressure is high enough to justify this rigor: IC3 reported more than 5,100 ATO complaints since January 2025, with losses exceeding $262 million. If you want a deeper control framework, read Internal Controls for Accounts Payable on Platforms: How to Prevent Fraud and Ensure Accurate Disbursements.

Decide when to hold release or escalate#

After you set pass/fail rules, define outcomes in advance so reviewers do not improvise in the queue. Use written lanes for release, temporary hold, and escalation, with clear ownership and documentation for each. If you want consistent outcomes, your release lane needs the same level of detail as your escalation lane.

| Lane | Definition |

|---|---|

| Release | Trigger was explained and verified |

| Temporary hold | Payout is paused while missing proof or out-of-band re-verification is completed |

| Escalation | Normal fraud review cannot resolve the case; legal/compliance or senior review is required before funds move |

Step 1. Define the three lanes in writing. Make each lane specific enough that two reviewers would reach the same outcome from the same facts. Release means the trigger was explained and verified. Temporary hold means payout is paused while missing proof or out-of-band re-verification is completed. Escalation means normal fraud review cannot resolve the case and legal/compliance or senior review is required before funds move.

A practical rule: resolve in-lane when signals align, escalate when they conflict. A clean KYC profile should not, by itself, close a case with high-risk device signals and a recent payout-detail change.

Step 2. Escalate conflicting signals immediately. Do not let the hold lane become a parking lot for unresolved contradictions. If account documentation looks clean but session context looks wrong, escalate immediately and log why the fraud queue could not close it.

Your evidence pack should capture payout-edit timestamp, pre-change and post-change destination, session identifier, device-risk result, analyst notes, and the unresolved conflict. QA this path by sampling escalations and confirming each record shows who escalated, when, and why.

Step 3. Route cross-border and tax-sensitive cases to specialist review. Some payout edits are both fraud and reporting-risk decisions, so route them to legal/compliance when tax or cross-border flags are present. Relevant examples include potential FBAR exposure when aggregate foreign financial accounts exceed $10,000 during the year, Form 1099-NEC relevance at the $600 threshold (or when federal income tax is withheld), and FEIE questions where eligibility depends on meeting specific requirements.

Attach the account's tax/profile context, year-to-date payment context, withholding status, and country-linked account details so specialists can review without reconstructing the case from scratch.

Step 4. Set a maximum hold window with review checkpoints. Set an internal hold limit and checkpoint schedule so fraud controls do not become unmanaged payout backlog. Where bank-partner reporting is relevant, keep SAR timing discipline in view: 30 calendar days from initial detection, with delays capped at 60 calendar days in no-suspect cases.

At minimum, require an early checkpoint, assign a named owner for aged holds, and force senior escalation before the internal maximum expires. If uncertainty remains at the deadline, require an explicit decision rather than letting the case age silently.

Build the incident reporting pack regulators and auditors will ask for#

Use one standard incident packet for every serious case so reviewers can quickly see what happened, what controls ran, and why the final decision was made. We recommend using the same packet order every time so your legal, fraud, and finance reviewers do not rebuild the story from scratch.

| Packet part | What to include |

|---|---|

| Narrative | Affected account or payee; payout detail changed; login, edit, approval, and release timestamps; current explanation of how access was unauthorized |

| Action trail | Actor actions; system actions; controls triggered; approvals; final disposition; review notes; overrides; customer notification decision |

| Compliance and tax artifacts | W-9 on file or missing; W-8BEN on file or missing; withholding status; any VIES VAT validation result used in review |

| Chain of custody | Who handled each artifact; when; where it was stored; why it was added; detection time; escalation time; reviewer identities; material evidence references; final sign-off |

Step 1. Write the narrative in a fixed order. Lead with who, what, when, where, and why. For an ATO payout case, state the affected account or payee, what payout detail changed, key timestamps (login, edit, approval, release), and your current explanation of how access was unauthorized. Even outside formal SAR drafting, that order keeps the core story usable.

Practical check: a reviewer should be able to answer, from page one alone, what changed, what controls triggered, and whether funds moved.

Step 2. Record the full action trail, not just the outcome. Show actor actions, system actions, controls triggered, approvals, and final disposition in sequence. Include review notes, who approved or overrode, and whether the payout was released, held, blocked, reversed, or escalated. If customer notification was considered or sent, record that decision in the packet.

Step 3. Attach compliance and tax artifacts that affected the decision. Do not attach every document by default. Include the artifacts that were decision-relevant, and label their state clearly: W-9 on file or missing, W-8BEN on file or missing, withholding status, and any VIES VAT validation result used in review. Form W-9 is used to provide a correct TIN for information returns, and Form W-8BEN is provided by a foreign beneficial owner to a withholding agent or payer. For VIES checks, record valid/invalid and timestamp; VIES results are retrieved from national VAT databases, so urgent cases may need national follow-up.

Step 4. Preserve chain of custody from detection to closure. Maintain one evidence log that tracks who handled each artifact, when, where it was stored, and why it was added. Build counsel involvement into the plan early so evidence handling remains defensible. At close, the packet should show detection time, escalation time, reviewer identities, material evidence references, and final sign-off in one place.

Fix common failure modes before they become repeat incidents#

If you want fewer repeat incidents, treat each closed case as a control-design review, not just a one-off investigation. When you review a closed case, ask what your team would change before the next payout run.

Failure mode: relying on one clean signal to clear payout-destination edits. Recovery: require layered controls for bank account, payout method, or payee-detail changes. A successful login or a single low-risk signal should not release funds on its own. Require a secondary check before release (for example, step-up verification, out-of-band payee verification, or second-review approval), and record both the trigger and the secondary-check result.

Failure mode: tuning controls only for login abuse. Recovery: extend controls through payout execution and retry paths, where a hijacked session can still convert into loss. ATO risk does not stop at authentication; it can include account-detail changes and transfer activity. Trace suspicious edits from session start to final disbursement status so events do not disappear inside queueing, approval, or file-processing steps.

Failure mode: disconnected fraud ops and finance records. Recovery: maintain one reconciled timeline from detection to disbursement outcome. Include edit time, control outcomes, approvals or overrides, payout file creation, processor response, and final status (paid, blocked, returned, or reversed). This prevents "stopped" in one team's log and "released" in another.

Failure mode: copy-pasting one global KYC/KYB/AML policy everywhere. Recovery: annotate market and program differences using a risk-based approach. Legal and operational context varies, so your KYC/KYB depth, AML escalation ownership, and related tax/profile review triggers should be mapped by country or program, not assumed to be identical.

Conclusion#

Treat Payee Hijack Fraud as an operating control problem first. If ownership, hold logic, and evidence are vague, release decisions become inconsistent at a common loss point: after a risky account change but before money leaves the platform. If you cannot show your release logic to a new reviewer and get the same result, your control is still too loose.

Use this as a starter checklist, not a universal template. NIST CSF 2.0 is outcome-based, and FFIEC guidance says risk assessments should drive your authentication and control choices, so your final design should match your payout rails, markets, and fraud patterns.

- Confirm scope and name decision owners.

Define the exact account-takeover events you own, including credential abuse, session hijacking, payout destination edits, and release-approval abuse. Assign named people, not generic teams, for payout holds, payout release, legal review, and incident closure. Verification point: any analyst should be able to answer who can approve a held payout and who must review a compliance-sensitive case. Red flag: "fraud team decides" or "ops will review" with no explicit authority line.

- Map payout change points and signal checkpoints.

Trace the path from authenticated access to final payout execution, including delayed execution and retry paths. Mark every point where an attacker can convert access into loss, especially bank account changes, payout method changes, and profile changes that could lock out the real user. Verification point: for each high-risk action, you should be able to show the trigger, the secondary check result, the approver, and the final status/disposition. Failure mode: if ops logs and finance logs cannot produce one reconciled timeline, treat that as a real control gap.

- Implement pass-or-fail hold rules for high-risk actions.

Do not rely on a single login control. Guidance emphasizes layered security: when single-factor is inadequate, stronger authentication plus other controls are more effective. Practical rule: if a payout destination edit arrives with anomalous device or session behavior, hold the release and re-verify before funds move. If a business override is allowed, record who approved it and why.

- Standardize the incident evidence and escalation packet.

Your packet should include the event timeline, actor and system actions, controls triggered, approvals, reporting/notification actions, and final disposition. Auditable monitoring, logging, and reporting matter as much as the front-end control because they determine whether you can defend the decision later. Red flag: screenshots and chat messages standing in for auditable records.

- Review market-specific legal and compliance constraints before expansion.

Legal, regulatory, and contractual requirements need explicit tracking as you add new payout programs or countries. Do not copy one global checklist unchanged and assume it survives local requirements.

Start small, but stay structured. Pilot these controls on one payout flow, test whether reviewers reach the same hold/release outcome from the same evidence, and only then expand automation. We recommend piloting with a real payout pattern your reviewers already know, then expanding only after you can replay the evidence trail cleanly.

Related reading: How Platforms Hold and Segregate Client Funds with Omnibus Accounts.

Frequently Asked Questions

What is Account Takeover in a payout platform context?

In this context, Account Takeover (ATO) means an unauthorized actor gets into a payee or operator account and uses that access to steal money or information. The payout-specific risk is not just login abuse. It is often the moment the attacker changes payout details or other account data so funds are redirected.

Is payee hijack fraud the same as ATO or only one subtype?

Treat payee hijack as a payout loss scenario inside the broader ATO category, not as a separate universe. IC3 describes ATO broadly across account types and sectors, while the payout version is the misdirection event where a compromised account sends funds to the wrong destination. That distinction matters because your controls must cover both account access and payout execution.

What minimum controls are table stakes before we scale payouts?

Start with layered controls on any payout destination edit: MFA or an equivalent-strength control combined with other layered security controls, selected through periodic risk assessments. FFIEC explicitly supports MFA or controls of equivalent strength combined with other layered security controls for higher-risk access. Your verification checkpoint should be simple. For every bank account, payout method, or payee detail change, you should be able to show the trigger, the secondary check result if one was required, who approved release, and the final paid, blocked, returned, or reversed status.

Why do single controls fail against session and device-aware attackers?

Because the attacker may not need to beat your login screen twice. CISA notes that stolen session cookies can authenticate to web applications and can bypass some MFA flows once the session is already authenticated. The common failure mode is a platform that treats one clean login as enough, even though session hijacking can happen later in the session.

What should trigger an immediate payout hold versus a monitored release?

An immediate hold is reasonable when payout destination changes coincide with anomalous session behavior, conflicting signals, or account-information changes that suggest the real user may be getting locked out. FRB Services Fed360 called out that ATO can include changes to a user’s email, phone number, or credentials. In payee redirection cases, that is a strong warning sign. A monitored release is more appropriate for lower-risk profile edits that do not change where money goes and that have a complete verification record.

What key details are still unknown from public ATO summaries and must be defined internally?

Public summaries rarely tell you the exact takeover path, and some legal commentary is blunt that the precise means are often shrouded in mystery. Define internally what evidence you require to close that gap: session history, cookie anomalies if available, payout edit timestamps, approval logs, retry path events, processor responses, and final settlement status. NIST SP 1299 is the right mindset here. Categorize, prioritize, and escalate as needed, but do not pretend public advisories give you full root-cause proof for every case.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bsaaml.ffiec.gov/manual/AssessingTheBSAAMLComplianceProgram/04trusted

- bsaaml.ffiec.gov/manual/Appendices/17trusted

- csrc.nist.gov/pubs/sp/800/92/r1/ipdtrusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- federalreserve.gov/supervisionreg/srletters/sr2114.htmtrusted

- ffiec.gov/sites/default/files/media/press-releases/202...trusted

- ic3.gov/CrimeInfo/AccountTakeovertrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How Platforms Validate Bank Accounts Before Mass Payouts

For mass payouts, the real question is not whether to verify payees. It is how much verification you require before release, who can override it, and what evidence you can produce later. If you cannot show that evidence on demand, your release rule is weaker than it looks.

Internal Controls for AP Platforms to Prevent Fraudulent Disbursements

Start here: your AP control design should reduce fraudulent disbursements and payment errors without turning every payout into a bureaucratic exercise. In practice, that means clear escalation points at the moments where money can move incorrectly, not extra approvals added just to look controlled.

When High-Risk Payout Accounts Need Source of Funds Checks Beyond KYC

A one-time KYC check may not be enough for higher-risk payout accounts. Risk can change after onboarding as transaction behavior shifts and customer risk profiles change.