Quick Answer

Start with a cost bridge, not a headline fee. Model GMV and take rate by segment, then add direct payout-path costs, FX and settlement friction, compliance handling, and return/reversal effects before deciding on pricing. Use webhook logs, idempotency trails, and reconciliation exports as evidence gates so each assumption can be traced to a recent month. Approve a fee change only after baseline, upside, and constrained pass-through cases still hold once collection-to-disbursement costs are fully applied.

How to model platform economics on gross margin, not just top-line fee percentage#

Use gross margin, not top-line fee percentage alone, to make pricing decisions. If your fee model stops at commission revenue, it is not ready for a pricing decision.

The core mistake is simple. Teams model fee percentage as if it were margin. It is not. Gross profit margin is the share of net revenue left after cost of goods sold (COGS), often treated here as cost of revenue. For a platform, that means you cannot stop at "we charge X% of transaction volume" and assume the rest is upside. You still have to account for cost of revenue.

That distinction matters because growth can hide weak economics for a long time. You can be growing fast and still have weak economics if margins are off. A fee change can look strong in a dashboard built around top-line volume, then disappoint once cost-of-revenue items are included.

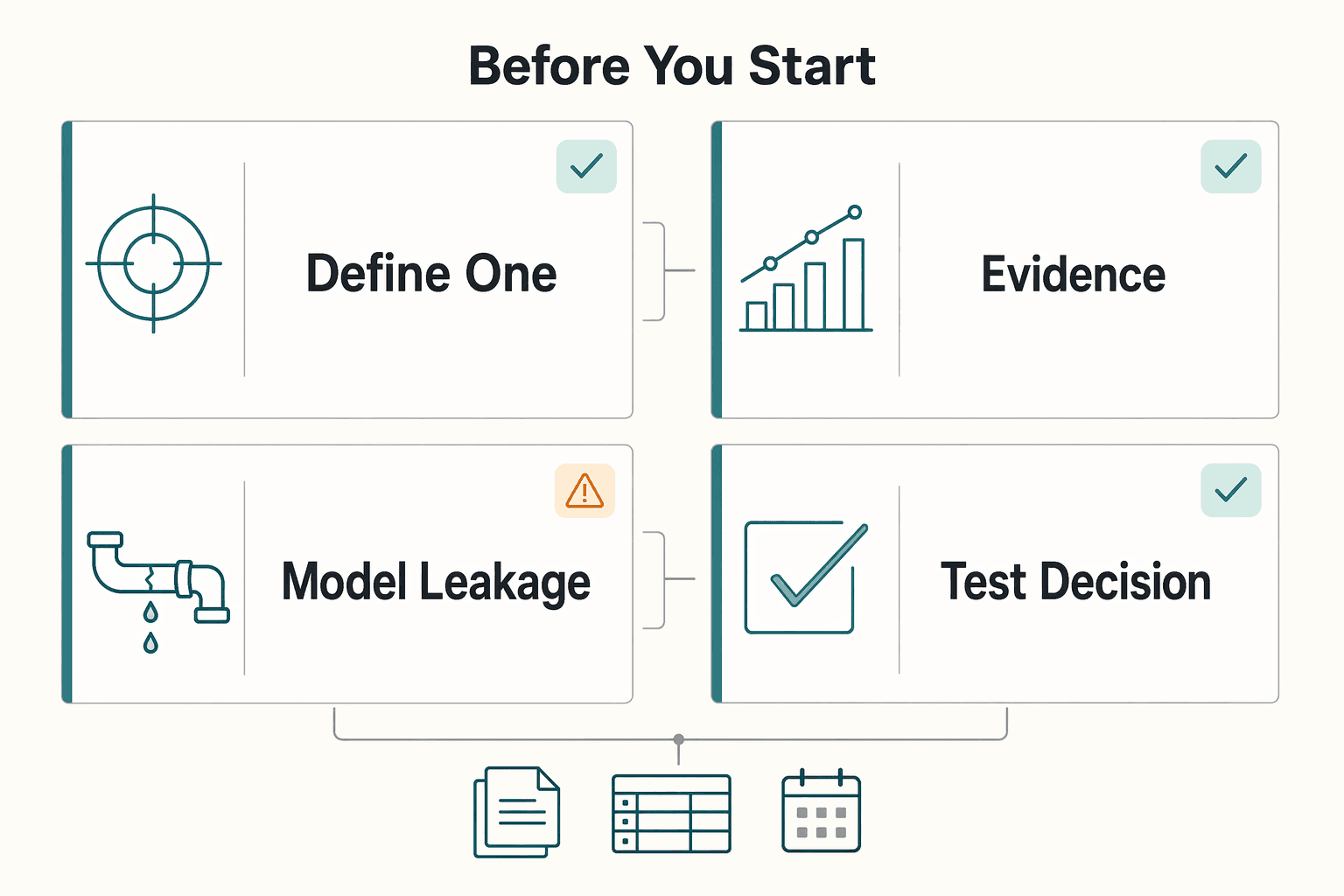

Before you start#

Use this guide as a shared working model for finance, ops, product, and engineering, not as a finance-only spreadsheet. The goal is decision-ready unit economics: can each transaction, seller segment, or payout flow create more value than it costs? If you cannot answer that at the unit level, you are not ready to change fees with confidence.

| Step | Action | Check |

|---|---|---|

| Define one margin view | Pick a single formula for revenue, COGS, and gross margin before anyone debates pricing | Leadership sees one set of numbers, not a finance version and a product version |

| Tie assumptions to records | Build your first pass from actual records for at least one recent month | If a scenario assumption cannot be traced back to a system of record, treat it as a hypothesis, not an input |

| Model the leakage paths early | Include cost-of-revenue items that sit between collection and disbursement, even if they look small at first | If a proposed fee increase only works under perfect operating assumptions, the model is too fragile for launch |

| Test the decision, not just the math | Run a baseline case, an upside case, and a failure case where costs rise or conversion drops | You know whether margin improves only on paper or under normal operating conditions too |

Use gross margin as your decision gate and take rate as a tuning input. That gives the whole team a model they can run, challenge, and update without arguing over definitions first. It also sets up the rest of this guide: clean terms, minimum inputs, a full cost bridge, scenario tests, and a launch checklist that catches downstream surprises before your fee change goes live.

For a step-by-step walkthrough, see Choosing Between Subscription and Transaction Fees for Your Revenue Model.

Separate platform commission economics from sales comp terms#

Keep your platform pricing metrics and sales compensation metrics separate from the start. A platform fee percentage on GMV is not the same thing as a sales gross margin commission plan.

- Define the two terms once, in writing.

A platform take rate is tied to Gross Merchandise Value (GMV), the total value of goods sold over a period. A gross margin commission plan is a sales comp model where commission is based on gross margin, meaning revenue minus COGS.

- Set one canonical formula and one revenue base.

Use one-line definitions in your model and leadership deck so finance and product do not report different versions of performance. Keep the formula language fixed wherever these metrics appear.

- Add a "do not confuse" line when both appear.

Use a plain note such as: "Platform take rate on GMV is not a sales gross margin commission plan metric."

- Use a traceability gate for fee decisions.

If a metric cannot be traced to ledger events and payout records, treat it as directional rather than decision-grade.

Gather the minimum inputs before you run any fee scenario#

Run fee scenarios only from traceable inputs, not blended averages. If the inputs are not reproducible, treat the output as directional.

Build the input pack first#

Before you model scenarios, assemble a minimum input pack:

- Gross Merchandise Value (GMV) mix by segment

- Current take rate by that same segment

- Payout rail costs

- Direct processing costs by corridor

Keep segmentation consistent across files. If GMV, payout cost, and processing cost use different segment logic, your model will mix unlike inputs and create false precision. For each segment, you should be able to name the source report and the owner who can reproduce it.

Treat compliance and tax gates as conversion assumptions#

Model compliance and tax gates as part of conversion, not as footnotes. Include Know Your Customer (KYC), Anti-Money Laundering (AML), Form W-8, and Form W-9 handling in corridor assumptions for hold, release, or rejection.

| Gate or form | Model as | Possible outcome |

|---|---|---|

| Know Your Customer (KYC) | Part of conversion | Hold, release, or rejection |

| Anti-Money Laundering (AML) | Part of conversion | Hold, release, or rejection |

| Form W-8 | Part of conversion | Hold, release, or rejection |

| Form W-9 | Part of conversion | Hold, release, or rejection |

Do not assume all eligible volume converts to payable volume on the same path. Define what your model does when required documentation is missing, stale, or pending.

Prove the money-movement path with systems evidence#

Support each lane with systems evidence: webhook event logs, retry behavior under idempotency, and reconciliation exports from initiation through completion, return, or reversal.

If provider status and reconciliation records do not match, keep that lane unresolved until you can trace it end to end for a recent sample cohort.

Reject stale or unsupported assumptions#

Reject a scenario when assumptions cannot be tied to system-of-record data for at least one recent month. Unit economics is useful only when you can provide the related supporting data points.

For legal or policy assumptions pulled from public registries, verify against an official edition or counsel before you use them to change the model.

Related: Currency Risk for Platforms: How to Protect Gross Margin When Collecting in USD and Paying in INR.

Map margin from collection to disbursement with a full cost bridge#

Use one cost bridge from collection to disbursement, with fixed row order and fixed segment logic across scenarios. If a fee change only improves margin before payout, FX, settlement, or compliance handling is included, treat it as unproven.

Build one bridge from collection to disbursement#

Build one table and keep assumptions explicit in every column.

| Bridge line | Baseline | Fee increase | Mixed pricing with partial unit fee scheme |

|---|---|---|---|

| GMV | Current GMV mix by segment and payable-conversion assumptions | Same mix unless you explicitly model a change | Same mix, with unit fee applied only to selected segments |

| Commission revenue | Current take rate by segment | Higher take rate only where the change applies | Base take rate plus unit fee on selected lanes |

| Non-commission revenue | Current non-commission charges, if any | Unchanged unless packaging changes | Changes only where packaging or unit fee changes revenue |

| Direct payout costs | Current payout-path costs by segment | Hold constant unless behavior or mix changes | Test recovery on higher-cost lanes |

| FX and settlement friction | Current conversion and timing treatment | Same unless corridor mix or timing assumptions change | Isolate impact on targeted corridors |

| Compliance handling costs | Current review, document, and exception-handling treatment | Include any added handling load from the pricing change | Recover cost only from cohorts that create it |

| Gross margin | Output after all rows | Net change after all rows | Net change after all rows |

If any row cannot be tied to a reproducible system source for at least one recent month, mark it unresolved and exclude it from decision-making.

Break out module-level economics only where they change the path#

Break out Virtual Accounts, Merchant of Record (MoR), and payout batches only when they change how revenue is recognized, how payouts move, or how exceptions are handled. Do not blend these paths into one generic direct-cost line if they follow different collection or disbursement mechanics.

Make FX and settlement friction explicit#

Keep quoted, settled, and paid-out amounts separate when currency conversion is involved, and separate completed volume from pending or held volume when timing affects period margin. Then compare baseline, fee increase, and mixed pricing side by side without changing hidden assumptions between cases.

Use this as a launch gate: if the fee increase only works under idealized assumptions, test the mixed model before shipping a blanket change.

Related reading: How to Invoice for Billable Hours vs Project Fees in QuickBooks.

Choose a commission structure that matches segment behavior#

Choose the structure that matches your segment economics, not the one that is easiest to present. Keep commission changes separate from sales-team compensation design: sales compensation is built to motivate sales agents, while platform fee design should follow your transaction economics and margin path.

Compare structures side by side#

| Structure | Best fit | Main risk | Rule for use |

|---|---|---|---|

| Flat take rate | Segments are similar enough in cost and pricing behavior | Expensive cohorts get cross-subsidized | Use when segment spread is limited and exceptions are rare |

| Category grid | Segments differ enough to justify distinct pricing | Too many categories and override requests | Keep categories limited and tied to observable cohort differences |

| Hybrid fee model | One base rate works for most volume, with a defined high-cost subset | Exception logic becomes opaque | Define exception eligibility up front and keep it cohort-based |

Test pass-through assumptions before changing headline fees#

Model no pass-through, partial pass-through, and full pass-through by segment, then treat uncertain pass-through as uncertain in the decision. If retention risk is already high, hold commission and optimize payout and failure-cost drivers first. If retention is stable, test commission changes with pre-set guardrails and a clear rollback path.

Keep fee logic distinct by GMV cohort when flows differ#

Set separate GMV cohorts where flow mechanics differ, including contractor payouts and marketplace catalog sales. Apply different fee logic only where a repeatable cost pattern is visible in the cohort, and document exceptions explicitly so finance and ops can reconcile them consistently.

Model payout operations before you change take rate#

If retry or return rates are rising, pause commission changes and stabilize payout quality first. Otherwise, you can mistake operational variance for pricing impact and misread gross margin.

Trace the payout lifecycle and assign margin effects#

Map each payout state in your flow and assign a margin impact to each one: initiation, compliance hold, provider acceptance, completion, and return or reversal. This keeps realized fee collection separate from payout-driven cost. Because fintech teams do not all measure gross profit the same way, define your treatment up front and keep it consistent across baseline and test cases.

Use webhook and idempotency records to estimate failure cost#

Use webhooks plus idempotency history to measure retries and failures without double-counting reversals. Link each disbursement to one instruction ID, one idempotency-key trail, and one final disposition so retries that were suppressed are not priced like completed attempts.

Add compliance holds and exception paths#

Include KYC and AML hold paths in the model, even when payouts later complete. Track straight-through payouts, compliance-held payouts, and returned payouts separately so timing effects do not blur month-level margin signals. Decision rule: if retry and return pressure is climbing, fix payout quality first, then retest take-rate changes.

Stress test policy and regulatory scenarios without overfitting to app stores#

After payout noise is stable, treat policy risk as a stress-test input, not your base case. Build explicit downside and adaptation scenarios, then approve pricing only if the model still works under constrained pass-through.

Build the policy cases first#

Model at least three cases before changing take rate:

| Case | What changes | Key assumption |

|---|---|---|

| Commission fee cap downside case | Percentage revenue is capped | Current percentage fee and assumed capped fee |

| Unit fee scheme adaptation case | A unit fee may be used | Whether a unit fee is available |

| Constrained pass-through case | Price changes are limited or delayed | Realistic pass-through share |

Keep assumptions explicit by segment: current percentage fee, assumed capped fee, whether a unit fee is available, and realistic pass-through share. If a case only works with near-full pass-through, treat it as fragile.

Use app store debates as context, not instructions#

Use Apple App Store, European Commission, U.S. Supreme Court, and Competition Commission of India debates as scenario inputs, not universal rules for your platform. They are useful only when you can map them to your own control points, such as billing path, bundling choices, seller dependence, distribution constraints, and multi-homing behavior.

Maintain an assumptions log: each external analogy should map to one internal product trait. If it does not map, remove it from the scenario pack.

Stress-testing practice in Europe was refined over a four-year period, which is a useful operating lesson: scenario design should be iterative. Also treat that source as analytical context, not official ECB policy.

Add quality and innovation effects, then label uncertainty#

Include quality and innovation effects, and label uncertainty directly. Platform-control research shows tradeoffs around openness and bundling: opening can increase participation while reducing direct sales, and bundling choices can change partner behavior.

Model these as ranges, not precise point estimates. If lower fees may increase participation but reduce resources for quality, trust, or support, represent both effects separately and keep unknowns explicit.

Common margin model failures and how to recover fast#

Basic model hygiene usually breaks pricing decisions before policy shocks do. If you cannot show which GMV cohorts are cheap or expensive to serve, do not ship a fee recommendation.

Segment profit by how money actually moves#

The fastest failure is treating all GMV as equally profitable. A domestic payout on a clean path is not operationally equivalent to a cross-border payout that creates more review, exceptions, or support load.

Segment at minimum by payout rail, geography, and compliance path, then tie each segment back to ledger events and payout records from a recent period. This makes it clear whether margin compression comes from the corridor itself or from operational friction. Red flag: one blended take rate masking a loss-making corridor.

Add tax-document handling as an operating cost, not a footnote#

If your product supports foreign-asset reporting workflows, model that handling path explicitly. Include Form 8938 and FBAR (FinCEN Form 114) operations where those steps show up in product flows or support queues.

Keep the trigger logic accurate: Form 8938 is threshold-based, not universal. IRS guidance says reportability is generally above $50,000, notes some cases use higher thresholds, and for specified domestic entities cites $50,000 at year-end or $75,000 at any time during the year. Filers may need Form 8938, FBAR, or both depending on circumstances. Track document-related tickets, exports, and exceptions as separate cost drivers.

Lock accounting treatment before you compare scenarios#

Do not compare scenarios that mix accounting boundaries. Align commission treatment with your ASC 340-40 policy, document what is in or out of gross margin, and hold that boundary constant across versions.

Before publishing a recommendation, backtest prior periods and explain forecast error by driver: mix shift, payout costs, tax-document volume, or accounting reclassification. If you cannot explain the miss, the next forecast is not decision-grade.

Conclusion and copy-paste execution checklist#

If you keep only one rule from this guide, keep this one: a higher commission alone is not enough evidence of durable margin. Durable margin usually depends on one shared definition set, segmented evidence, and a fee decision you can verify after launch. Use this as a copy-and-paste checklist for your next pricing review or a two- to four-week diligence sprint.

- Lock the glossary before touching the model.

Write a one-page glossary and circulate it across finance, ops, product, and engineering. Confirm the canonical formulas for Gross Merchandise Value (GMV), commission revenue, and gross margin, and make sure everyone is using the same analysis unit. If a number cannot be traced to a clear system-of-record source, it should not drive a fee change.

- Validate the input pack by segment, not by average.

Your model inputs should work by segment and route to market, because averages can hide important differences. Check that you have current pricing logic, conversion evidence, and direct cost assumptions for each meaningful slice such as customer size, vertical, product family, channel, or geography. A simple checkpoint: pick one recent month and confirm every major assumption has a source of record, not just a spreadsheet owner.

- Run three scenarios and test funnel constraints explicitly.

At minimum, model a baseline case, an upside case, and a constrained or mixed-pricing case. State your pass-through assumptions clearly, then test where growth or margin pressure actually sits: capacity, conversion, velocity, or mix. This keeps scenario work tied to operating reality instead of headline fee changes alone.

- Treat regulation as material and jurisdiction-specific.

Before approving any price move, label policy-sensitive assumptions by country or market instead of treating one framework as universal. Digital platform regulation is an active issue across jurisdictions, so scenario conclusions should reflect where rules differ and where uncertainty is still high.

- Approve one decision with an owner, timeline, and verification plan.

Name the exact fee change, the decision owner, launch date, and first post-launch review date. Your verification set should track realized commission revenue, direct costs, conversion behavior, and unit economics against the pre-launch baseline, reviewed by segment rather than only in aggregate.

That is the standard worth holding: shared terms, segmented evidence, and one decision you can defend after the month closes.

Frequently Asked Questions

What commission range is common for platforms, and when does it stop being a useful benchmark?

A commonly cited marketplace range is 10% to 20% of Gross Merchandise Value (GMV), and that same source notes commissions can sit outside the range. Use it as a rough benchmark, not a pricing rule. It becomes less useful when category economics, seller margins, or marketplace goals differ from the businesses behind the benchmark.

Does increasing `take rate` usually improve gross margin, or can it reduce margin after payout and churn effects?

Not necessarily. A higher commission can help or hurt gross margin depending on what happens to net sales and direct delivery costs. Gross margin is what remains after delivery, so pressure-test any fee change with the core math (net sales - COGS) and trend checks over time.

Which costs are most often missed when modeling platform gross margin?

A common miss is treating commission as the whole story. Marketplace margins are affected by more than commission, so include the direct costs required to deliver the service in COGS and review margin trends to catch gaps early.

How should we model a potential `commission fee cap` without overreacting to `Apple App Store` dynamics?

Do not assume one platform’s fee debates map directly to your business. Use scenario modeling instead: current fee, a capped-fee case, and an alternative fee structure, then compare how each case changes gross margin.

What is the practical difference between platform commission economics and a `gross margin commission plan`?

Platform commission economics usually starts with transaction value and commission revenue. Gross margin is a broader profitability metric based on net sales minus COGS. Keep those definitions explicit so teams do not compare unlike numbers.

How often should finance, ops, and engineering recalibrate margin assumptions and pass-through rates?

There is no single required cadence in this grounding, but a regular review cycle is important. Re-check assumptions whenever fee logic or delivery costs change, and monitor gross-margin trends because they can flag operational issues.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- clame.nyu.edu/uploaded-files/E0A957/312658/Profitability%2...trusted

- documents1.worldbank.org/curated/en/272911522179505834/pdf/124656-WP-...trusted

- faculty.wharton.upenn.edu/wp-content/uploads/2016/11/SSRN-id3957209.pdftrusted

- federalregister.gov/documents/2024/10/08/2024-21867/regulation-n...trusted

- fincen.gov/report-foreign-bank-and-financial-accountstrusted

- funginstitute.berkeley.edu/wp-content/uploads/2013/12/PlatformControl20...trusted

- hbs.edu/ris/Publication%2520Files/ReviewPaper_2020_0...trusted

- home.treasury.gov/system/files/261/FSOC2024AnnualReport.pdftrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Choosing a Gross-to-Net Payout Model for Platform Disbursements

Payroll tax references matter, but they are not a payout architecture. Teams often collect withholding rules, filing-status details, and tax-form requirements before they have defined who owns each deduction line. That guidance still matters for withholding logic. [IRS guidance on the Additional Medicare Tax](https://www.irs.gov/businesses/small-businesses-self-employed/questions-and-answers-for-the-additional-medicare-tax) can be useful context for tax review, but it does not define deduction sequencing, ledger mapping, release gates, or recipient-facing payout explanations.

Currency Risk for Platforms Collecting USD and Paying INR

USD collection with INR payout creates a real gross-margin risk as soon as money movement happens across time instead of in one instant. The issue is simple: if the USD amount is known now but the INR conversion or payout happens later, your margin is exposed to the USD-INR move during that gap.

ASC 340-40 for Platforms: How to Account for Contract Acquisition Costs and Commissions

If you handle commissions or similar deal costs, start with two GAAP tests: is the cost incremental to obtaining a customer contract, and do you expect to recover it? If either answer is no, expense treatment is usually the right starting point.