Quick Answer

Map the exposure window first, then hedge what is actually at risk. Track quote request, quote acceptance, settlement confirmation, conversion execution, and payout release for live USD-to-INR flows, and tie that trail to realized gross margin. Use forwards for predictable payout timing, add options when timing or amounts move, and keep swaps for short mismatch periods. Enforce stale-quote rejection, idempotency keys, and payout blocking until settlement and ledger records are complete.

USD Collection With INR Payout Creates Gross-Margin Risk Across Time#

USD collection with INR payout creates a real gross-margin risk as soon as money movement happens across time instead of in one instant. The issue is simple: if the USD amount is known now but the INR conversion or payout happens later, your margin is exposed to the USD-INR move during that gap.

That exposure is not theoretical. FX settlement-timing risk exists between payment initiation and settlement, and rate moves in that window can reduce expected cash flows in your functional currency. In practice, a platform can lose margin, slow settlement handling, and make reconciliation harder even when customer pricing looked fine at checkout. For marketplace, contractor, and embedded-payments teams, this often shows up as an operating problem before it is treated as a treasury problem.

Step 1: Quantify the timing window. Treat time as the first risk variable. You need to know when USD is collected, when settlement is confirmed, when conversion is executed, and when INR is released. A useful check is whether you can pull those timestamps for a live sample and tie them back to realized gross margin by corridor. If you cannot do that yet, any hedge decision is still based on assumptions rather than measured exposure.

Step 2: Frame the risk in the currency your business reports in. IAS 21 defines functional currency as the currency of the primary economic environment in which the entity operates. That matters because settlement-date FX moves change expected functional-currency cash flows. That is how a payout delay becomes a margin issue on your books. If finance and payments are looking at different base currencies, you can end up arguing about rate quality while missing the actual margin loss.

Step 3: Choose a hedge approach only after you know payout behavior. A currency forward fixes an exchange rate in advance for a future transaction, which can be useful when payout timing is predictable. But no single instrument is always right. If payout dates are uncertain or batch timing moves around, a hedge setup designed for fixed dates may fit poorly. The red flag is choosing hedging before you have measured how often payouts slip, split, or settle later than expected.

Step 4: Verify controls in production, not just in policy. USD/INR market infrastructure itself recognizes multi-day settlement risk. CCIL explicitly captures market risk for 3 settlement days, which is a useful reminder that exposure does not end at quote acceptance. The practical check is simple: after a live batch, compare the intended conversion timing, the executed rate, the final settlement state, and the ledger result. If those records do not line up cleanly, you likely have a gap between FX policy and execution.

That sequence drives the rest of this guide: measure the exposure window, choose a hedge mix that fits real payout timing, set clear approvals, and then verify the whole chain under live conditions.

What to prepare before you change FX policy#

Before you change FX policy, lock down scope, evidence, and control gates first. Then discuss instruments. If you cannot map exactly which USD collection paths end in INR payout, policy drift starts immediately.

| Area | What to prepare | Verification |

|---|---|---|

| Operating perimeter | List each USD-collection to INR-payout flow, and mark where Virtual Accounts or a Merchant of Record sit in the path | Trace every route from invoice or checkout to final payout batch, including which entity handled compliance controls |

| Evidence pack | Pull invoice timestamps, settlement or conversion timestamps, payout-batch history, and realized gross margin by corridor into one review set | Retain the reference code, amount, and date used in reconciliation |

| Compliance gates | Treat KYC, KYB, AML, and VAT validation as release criteria | Use VIES for EU cross-border VAT checks where relevant; India-regulated rails expect explicit customer identification and due-diligence requirements |

| Owners | Set clear ownership across finance, payments ops, and engineering for policy intent, payout execution, and data integrity | Each transaction change should include user, action, role, date, and time |

-

Define the operating perimeter. List each USD-collection to INR-payout flow, and mark where Virtual Accounts or a Merchant of Record sit in the path. MoR typically handles transaction-tax execution and KYC/AML adherence, and virtual bank account numbers can improve invoice-linked collection records. Verification check: you can trace every route from invoice or checkout to final payout batch, including which entity handled compliance controls.

-

Assemble the minimum evidence pack. Pull invoice timestamps, settlement or conversion timestamps, payout-batch history, and realized gross margin by corridor into one review set. If you use virtual-account collection, retain the reference code, amount, and date used in reconciliation, because those are used to match transfers to invoices. Red flag: dashboard FX views exist, but no ledger-backed record shows when conversion actually executed.

-

Confirm compliance gates before rollout. Treat KYC, KYB, AML, and VAT validation as release criteria. For EU cross-border VAT checks, use VIES where relevant. For India-regulated rails, expect explicit customer identification and due-diligence requirements; RBI's KYC Direction, 2016 (updated August 14, 2025), separates Customer Identification Procedure and Customer Due Diligence.

-

Assign accountable owners before instrument decisions. Set clear ownership across finance, payments ops, and engineering for policy intent, payout execution, and data integrity. The practical checkpoint is simple: each transaction change should include user, action, role, date, and time. Without that trail, rate and timing disputes become reconciliation noise instead of an operational fix.

Map the exposure window from collection to payout#

Treat this as a timing-control exercise: map every minute your USD-INR exposure stays open, and do not release payouts when rate or status is uncertain.

| Checkpoint | Record needed | Control note |

|---|---|---|

| Quote request | Provider reference, status, date, and time | Main failure point is the delay between quote request and conversion execution |

| Quote acceptance | Provider reference, status, date, and time | Quote acceptance is not execution |

| Settlement confirmation | Provider reference, status, date, and time | Exposure can stay open after quote acceptance and through settlement |

| Conversion execution | Provider reference, status, date, and time | If execution happens outside the valid window, margin math is already off |

| Payout batch release | Provider reference, status, date, and time | Payout release should be status-gated, not assumption-based |

- Break the path into five timestamped checkpoints.

For the same transaction sample, mark: quote request, quote acceptance, settlement confirmation, conversion execution, and payout batch release. Do not merge these into one "conversion time." Exposure can stay open after quote acceptance and through settlement, including cases where one side pays out before receiving the counter-currency. Verification point: each checkpoint has a system record with provider reference, status, date, and time.

- Mark stale-quote entry points and enforce a rejection or escalation rule.

The main failure point is the lag between quote request and conversion execution. If a quote expires (for example, after 30 minutes) or a lock window lapses (for example, 1-hour or 24-hour), your system should reject auto-conversion or escalate before INR payout is released. Quote acceptance is not execution. If execution happens outside the valid window, margin math is already off.

- Separate controllable delays from uncontrollable timing boundaries.

You can control execution lag, internal approval delays, and premature payout release before final status. You cannot remove weekend gaps or provider cutoff constraints, but you can model them and route exceptions. A concrete settlement boundary example is 06:30 CET for same-day submission in the referenced CLS timeline update. Also treat asynchronous status as a real control point: some fields arrive later, so payout release should be status-gated, not assumption-based.

- Set policy using a same-day vs delayed conversion contrast.

Same-day (or in-window) conversion reduces uncertainty. Delayed conversion outside the lock window increases exposure to stale quotes, cutoff misses, and status mismatches between dashboard views and ledger truth. If payouts are frequent and margin is thin, execute conversion as close as possible to confirmed settlement and release batches only after executed rate and settlement status are present. If you delay for cash reasons, record it as accepted exposure.

Choose your hedge mix based on payout timing and cash constraints#

Choose instruments by payout certainty first: lean on forwards when INR payouts are predictable and margin is thin, and use partial options coverage when timing or amounts are uncertain. Do not force all exposure into one instrument if dates and notionals are unstable.

Compare instruments on operating fit first#

Evaluate each tool on cost visibility, flexibility, operational overhead, and cash lock-up or line usage. Forwards usually give clearer upfront rate visibility, but they can reduce flexibility if payout timing or volume moves. Options preserve the right without obligation, which helps under uncertainty, but premium cost must be justified against expected margin protection.

FX swaps are a different tool: a spot exchange paired with a pre-agreed future reversal, typically for timing mismatches. Natural hedging is an operational offset, not a contract, where one FX exposure is balanced by another recurring exposure.

| Instrument | Best fit use case | Main failure mode | Finance approval needed | Ops approval needed |

|---|---|---|---|---|

| Forward contract | Predictable INR payout dates and thin margin | Locked rate/notional later looks unfavorable if timing or volume changes | Confirm tenor, line usage/liquidity impact, and mark-to-market tolerance | Confirm payout calendar is stable enough to match hedge dates |

| FX option | Uncertain payout timing or variable payout amount | Premium erodes margin if uncertainty is overstated | Approve premium budget and coverage share | Confirm uncertainty is real, not a forecasting gap |

| FX swap | Short-term timing mismatch between current exchange and future reversal | Misused as a directional hedge instead of a two-leg timing tool | Approve both cash dates and two-leg settlement tracking | Confirm both legs can be settled and reconciled operationally |

| Natural hedge | Recurring offsetting USD exposures already exist | Assumed offset fails in timing or amount | Validate offsetting flows are real and recurring | Confirm flows are mapped and not double-counted |

Set decision rules before volatility hits#

Set rules in advance so hedge choices are not made ad hoc during volatile periods. A practical baseline is partial forward coverage of forecast exposure rather than full coverage of every projected payout. One documented approach is 80% coverage over a three- to nine-month period.

- Use forwards first when payouts are regular, forecast error is low, and gross margin cannot absorb much USD-INR drift.

- Use partial options coverage when payout timing or volume is uncertain.

- Use swaps narrowly for short-term cash timing gaps.

- Use natural hedging only when treasury and ops can evidence offset in amount and timing.

For highly uncertain payouts, a forward-only rolling book can lock rates that later look unfavorable. If deferrals, batch shifts, or seasonal spikes are frequent, reduce pure forward concentration.

Segment hedge coverage by payout profile#

Avoid one global hedge percentage across unlike payout profiles. Set higher forward shares for steady monthly payouts and lower or options-based shares for seasonal or promotion-driven spikes.

If you need longer planning, use a layered horizon by forecast confidence. Documented practice supports planning windows from 18 months to three years, with more committed cover on higher-confidence near-term flows and less committed cover on variable distant flows.

Verification should be explicit by segment: finance can show approved coverage band, instrument mix, tenor, and exception rules; ops can show the payout pattern behind those decisions. If that evidence is missing, the policy is not yet operational.

For a step-by-step walkthrough, see Currency Options for Hedging Against Forex Risk.

Set ownership and approval rules that prevent policy drift#

Policy drift starts when urgent payouts bypass decision rights. Lock ownership and approvals before volatility hits. Assign named owners for quote acceptance, hedge execution, and payout release, and treat exceptions as formal approvals, not ad hoc messages.

Assign decision rights with a RACI chart#

Use one RACI chart across the full USD-collection-to-INR-payout flow, with one accountable owner per decision point. RACI means Responsible, Accountable, Consulted, and Informed.

| Decision point | Responsible | Accountable | Consulted | Informed |

|---|---|---|---|---|

| Quote acceptance | Payments ops or treasury | Finance lead | Product, engineering | Support |

| Hedge execution | Treasury or finance | CFO or controller | Ops | Product |

| Payout batch release | Payments ops | Ops lead | Finance, product | Engineering |

The exact split can vary by org, but the responsibility map must be explicit. Quick check: pick one recent payout batch and confirm you can identify the accountable owner for all three decisions immediately.

Set exception approvals before the exception happens#

Define exception approvals in writing before you need them. For stale-quote overrides, out-of-band conversions, and manual payout batches, document:

- what event triggers approval

- who can approve

- what evidence must be attached

Keep separation of duties: the person pushing release should not be the same person approving the override.

Require an auditable record from request to ledger posting#

Your record should let you trace rationale, justification, approvals, and transaction status end to end. At minimum, keep:

- request and accepted-quote timestamps

- provider reference and approved rate or hedge reference

- user or service identity

- payout batch ID and settlement confirmation

- ledger posting reference

- reconciliation export used to tie provider activity to the books

This record supports auditability and helps finance investigate margin variance with evidence for accuracy, completeness, and timeliness.

Define escalation when controls conflict with urgency#

Escalate when the proposed risk treatment exceeds the owner's authority or expertise. In practice, this is usually an urgent case where payout timing conflicts with control requirements.

Decide in advance who can choose between delaying payout, obtaining a fresh quote, or approving a manual path, and who must be informed after that decision. Test this with scenario drills: if teams cannot name the approver and required evidence without debate, the policy is still too soft.

Related reading: How to Handle Realized and Unrealized Gains/Losses on Foreign Currency.

Implement platform controls in the money movement stack#

Governance works only if the money movement stack enforces it. Build hard stops in code: reject expired FX quotes, make retries duplicate-safe, and block INR payout release until account state and required records are ready.

Reject stale FX quotes before conversion#

Make quote-validity checks part of the FX API flow, not a manual step. Quotes can expire for transfer creation, and one documented case is 30 minutes from quote creation. If a request arrives after expiry, fail closed and require a fresh quote.

Treat indicative and executed rates as separate controls. Indicative rates are informational and not guaranteed until conversion is confirmed, so alert on meaningful variance between indicative and executed rates and on delayed settlement states based on your own policy thresholds.

Verification point: for one recent USD to INR conversion, confirm you can trace quote creation time, quote acceptance time, execution time, and final executed rate in one record.

Make retries safe for both conversions and payouts#

Use idempotency keys for both conversion creation and payout creation so retries do not create duplicate economic events. This is required in real systems where webhooks can be delayed or retried, including automatic resend windows of up to three days and retry-queue behavior when acknowledgment is not returned within 10 seconds.

Store the idempotency key, provider reference, and final object ID together so reconciliation can prove one request produced one result.

Gate payout release on account state and evidence readiness#

Before you release a payout batch, check virtual-account lifecycle state and unresolved hold conditions in your own ledgering flow. One documented virtual-account model uses Active and Closed states, so map internal labels like credit, hold, and return to provider states and transaction outcomes instead of assuming label equivalence.

| Record | Condition in article | Threshold or retention |

|---|---|---|

| W-8BEN | When requested by payer/withholding agent | Keep masked and audit-ready |

| W-9 | Correct TIN | Retain W-9 records for four years |

| Form 2555 data | When FEIE handling is relevant | Keep masked and audit-ready |

| FBAR evidence | Where balances exceeded during the year | $10,000 |

| 1099-NEC support | For nonemployee compensation | $600 or more |

Store tax/compliance artifacts only where required for your product and jurisdiction, but keep them masked and audit-ready. Examples include W-8BEN (when requested by payer/withholding agent), W-9 (correct TIN), and Form 2555 data when FEIE handling is relevant. Keep FBAR evidence where balances exceeded $10,000 during the year, and 1099-NEC support for $600 or more in nonemployee compensation. IRS small-business guidance also says to retain W-9 records for four years.

Once these controls are live, test them under timeout, retry, and rate-volatility scenarios.

Stress test the policy and define automatic triggers#

Once your stack can reject stale quotes and block bad payouts, make sure the policy still protects margin when timing breaks. Treat stress testing as a decision tool, not a reporting exercise. If a scenario should change hedge coverage, payout timing, or approvals, pre-commit that action now instead of debating it during a live USD-INR move.

Run paired shocks on rate moves and settlement delay#

Stress USD-INR rate moves and settlement lag together, because losses usually come from both. A rate-only test misses real exposure windows that can run overnight or across weekends and holidays before settlement completes. That timing risk is material: BIS estimated $2.2 trillion of daily FX turnover was subject to settlement risk in April 2022, up from $1.9 trillion in April 2019.

For each scenario, capture two outputs:

- Expected gross margin impact before execution

- Realized gross margin impact after execution

Review the expected-versus-realized gap each cycle. That delta tells you whether assumptions are wrong, execution is drifting, or approvals are too slow.

Use two scenario families:

- Rate-only shocks around normal payout cadence

- Delayed-settlement cases where conversion or payout release slips one or more business days, especially around Friday cutoffs and holidays

If a provider or bank supports payment-versus-payment (PvP), separate those flows because PvP removes FX settlement risk. Apply stricter timing assumptions to non-PvP flows.

Verification point: in one completed test cycle, trace invoice timestamp, quote creation, quote acceptance, settlement confirmation, conversion execution, payout release, and final realized gross margin in one record.

Segment outputs by operating profile#

Use segmented thresholds, not one global rule. Evidence on currency shocks shows different firm profiles can react differently, so your platform cohorts should be tested as separate risk profiles.

Segment by traits that change exposure:

- Payout predictability

- Average hold time from USD receipt to INR release

- Margin buffer

- Natural offset between inflows and outflows

Cohorts with thin margins and unpredictable payout dates should trigger earlier than cohorts with faster conversion and stronger natural hedging. Blended portfolio averages can hide losses in fragile cohorts, so keep stress evidence at cohort level: scenario version, assumptions, executed conversions, delayed-settlement exceptions, approval logs, and ledger-backed realized margin.

Pre-commit trigger actions and rollback rules#

Define trigger condition, owner, action SLA, and rollback criteria in advance so stress results lead to decisions with clear governance.

| Condition | Owner | Action SLA | Rollback criteria |

|---|---|---|---|

| Expected gross margin deterioration in a cohort breaches your policy threshold under a USD-INR shock scenario | Finance owner | Same business day | Two consecutive test cycles back within threshold and no manual overrides for that cohort |

| Realized margin misses expected margin because settlement lag extends exposure beyond policy assumptions | Payments ops owner | Within 24 hours | Root cause closed, delayed-settlement rate returns to baseline, and latest cycle shows expected and realized results aligned |

| Non-PvP or delayed-settlement flows accumulate over a weekend or holiday window | Treasury or finance owner | Before next payout batch release | Exposure window reduced or temporary coverage added, with next batch settling inside policy timing |

| Manual exceptions for quote acceptance or payout release rise above your internal tolerance | Product plus engineering approver | Same business day | Exception volume normalizes and audit trail shows controls, not manual workarounds, carrying the flow |

Keep actions simple and automatic: tighten hedge coverage for the affected cohort, shorten payout windows, pause discretionary batch release, or require an additional approval. If rollback cannot be stated in one sentence, it is not a real trigger.

Even with solid triggers, losses still come from avoidable operating errors. For related context, see The Financial Impact of the Rupee's Depreciation for Indian Freelancers.

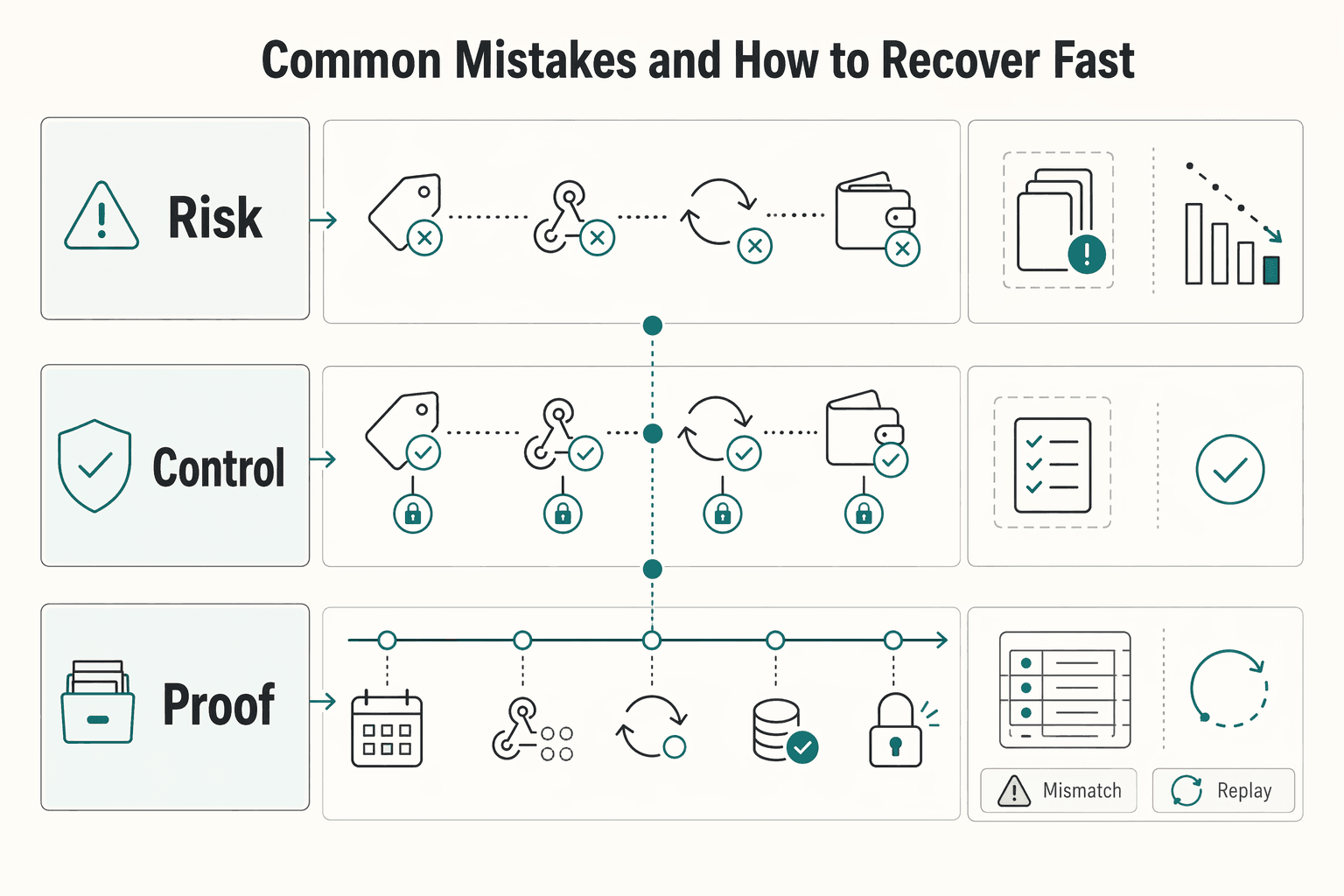

Common mistakes and how to recover fast#

Most USD-collection/INR-payout margin leakage comes from operating-control failures, not a single bad hedge decision. You recover fastest by tying each issue to traceable timestamps, approvals, and ledger outcomes.

1. Mistake: treating hedging as finance-only. Recovery: add product and engineering checkpoints directly into the flow: quote created vs accepted, webhook received vs applied, and conversion confirmed vs payout released. For at least one sampled payout, keep a full trace of quote timing, idempotency/retry handling, webhook receipts, settlement confirmation, and the event that unlocked release. This matters because webhook deliveries can be retried, and payloads can arrive stale, partial, duplicated, or out of order; without idempotent handling, retries can create duplicate side effects.

2. Mistake: over-hedging uncertain payout flows. Recovery: split predictable vs variable flows instead of forcing full forward coverage on both. Keep forwards where payout timing is reliable, and use options (including non-deliverable options where relevant) where timing is uncertain, since options provide a right, not an obligation, to transact. This avoids building hedge imbalance into the design and makes timing variance easier to absorb.

3. Mistake: running the book off one dashboard metric. Recovery: reconcile dashboard signals against ledger-backed realized gross margin on a fixed operating cadence. Compare indicative rate, executed rate, realized payout amount, and posted margin by cohort; if they diverge, trust the ledger first, then inspect event ordering and exception approvals. Single-view dashboard confidence is not enough when upstream events can be delayed or malformed.

4. Mistake: scaling volume before controls are ready. Recovery: gate expansion on control readiness, including KYC/KYB/AML, customer due diligence, and beneficial ownership records where required. Use a risk-based threshold for pauses and escalations, and keep evidence packs for CDD status, ownership data, AML alerts, and exception logs. Where FCA-style rules apply, payment delays can extend up to 4 business days when objective suspicion thresholds are met, so approval ownership and customer communications need to be explicit.

Conclusion and copy-paste launch checklist#

If you want this policy to survive first contact with production, make it a launch gate, not a slide. If one item below is unclear, unowned, or untestable, do not treat your USD collection and INR payout flow as ready.

-

Confirm scope. Write down every USD collection path, every INR payout path, and which product surfaces are in play: Virtual Accounts, Merchant of Record flows, and scheduled payout batches. The verification check is simple: your finance, ops, and engineering owners should all point to the same diagram and the same list of corridors. A common failure mode is fixing FX logic for one collection path while a second path still converts or releases payouts on older rules.

-

Confirm the data you will use to judge success. You need exposure-window timestamps from quote request through payout release, plus realized gross margin by corridor, not just dashboard FX averages. Pick one recent batch and reconstruct quote time, acceptance time, settlement confirmation, conversion execution, payout release, and final ledger posting. If you cannot do that for a sample batch, you will not know whether margin moved because of market timing, provider delay, or your own release logic.

-

Confirm the hedge policy and owner. State which exposures are covered with forward contracts, FX options, currency swaps, or natural hedging, and who can approve each. In India context, RBI materials explicitly list forwards, options, and swaps with Rupee as one of the currencies as hedging products. If you rely on natural hedging, treat it as a treasury choice that still needs review, not an automatic substitute for derivatives. The red flag here is a hedge mix that exists in treasury notes but is not tied to actual payout timing cohorts.

-

Confirm the controls before money moves. Stale-quote rejection, idempotent retries, exception approvals, and reconciliation exports should already be wired into the conversion and payout path. Your checkpoint is an exception drill: expire a quote on purpose, retry the request with the same idempotency key, and verify that payout stays blocked until a valid conversion is confirmed. Many margin incidents start with a small quote-TTL miss and turn into duplicate execution because retries were not controlled.

-

Confirm governance. Set a recurring stress-test cadence, maintain a trigger table, and name escalation owners for finance, ops, and engineering. You want pre-agreed actions for delayed settlement, sharp USD-INR moves, or out-of-band manual batches, including who can tighten hedge coverage or shorten payout windows. If the owner field is blank, the policy will drift the first time business urgency collides with controls.

-

Confirm compliance and tax readiness. Keep KYC evidence complete, with identity and address verification where required, and maintain any business-verification records required by your program. Validate VAT IDs through VIES when you are in an EU VAT context. For tax artifacts, collect Form W-9 for U.S. payees who need to provide a correct TIN, and Form W-8BEN where a foreign individual must establish foreign status for U.S. withholding or reporting. For U.S. persons with foreign accounts, know that FBAR reporting is tied to FinCEN Form 114 when aggregate foreign-account values exceeded $10,000 at any time during the calendar year. FEIE is not automatic and depends on meeting the bona fide residence test or the physical presence test. Store these records in masked, audit-ready form, including 1099-related outputs where enabled. Want to confirm what's supported for your specific country/program? Talk to Gruv.

Frequently Asked Questions

What causes gross margin leakage when collecting in USD and paying in INR?

The leak starts in the time gap between when you receive USD and when you convert or release INR payouts. When the exchange rate moves in that window, the value of your foreign currency position changes, and those gains or losses flow through income rather than staying theoretical. In practice, leakage can also be worsened by stale quotes, delayed settlement, duplicate retries, or payout release happening before conversion is confirmed.

When should a platform choose forward contracts instead of FX options?

Choose forward contracts when your payout dates and amounts are predictable enough to hedge exchange-risk exposure in advance. That is often a cleaner fit for recurring, steady INR obligations, and in India context the RBI allows a person resident in India to enter into a forward contract with an authorised dealer in India to hedge exchange risk exposure. Choose FX options when payout timing is uncertain, because an option gives you the right, not the obligation, to transact, which matters when batches may slip or shrink.

How much of USD-INR exposure should be hedged versus left open?

There is no universal hedge ratio that fits every platform, so do not copy another firm’s percentage. A better rule is to hedge the predictable slice and treat the uncertain slice separately based on actual payout timing variance and cash needs. If one cohort settles on a stable cadence, cover more of it. If another cohort slips often, use partial coverage or more flexible instruments instead of forcing a full hedge that may create its own mismatch.

Which controls are mandatory before scaling INR payout batches?

At minimum, your money movement path should include quote-expiry checks, idempotent conversion and payout requests, reliable webhook handling for asynchronous events, and payout-level reconciliation. If your team cannot trace one sample batch from quote acceptance to settlement confirmation to payout release, you are likely not ready to scale volume. Keep any jurisdiction-specific compliance approvals complete as well, but operationally these four controls help reduce avoidable margin and execution errors.

How should teams handle stale FX quotes without blocking all payouts?

Treat an expired quote as invalid and send the transaction to a refresh or re-quote path, because rates do expire and should be refreshed regularly. You do not need to freeze every payout, but you should block conversion on the stale quote and escalate only the affected items through an approved exception path. A key failure mode to avoid is retrying the conversion as if nothing changed, or retrying without the same idempotency key, which can turn a pricing issue into a duplicate execution issue.

What should be included in an audit-ready FX decision trail?

Store the quote creation time, quote acceptance time, expiry, quoted and executed rate, notional amount, provider reference, idempotency key, webhook receipt timestamps, settlement confirmation, payout release event, and the final ledger posting. Add the approval record for any manual override, plus a payout reconciliation export that ties transactions to the settlement batch. Your verification test is simple: for one payout, you should be able to reconstruct why the rate was used, when it was locked, and how it affected realized gross margin.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bis.org/publ/qtrpdf/r_qt2212i.htmtrusted

- cftc.gov/sites/default/files/filings/ptc/15/02/ptc022...trusted

- comptroller.war.gov/Portals/45/documents/fmr/Volume_06a.pdftrusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- fdic.gov/resources/supervision-and-examinations/exami...trusted

- investor.gov/introduction-investing/investing-basics/glos...trusted

- irs.gov/businesses/small-businesses-self-employed/re...trusted

- irs.gov/forms-pubs/about-form-w-9trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

When a Currency Peg Breaks and Your Platform Still Has to Pay

For a platform that collects, converts, and pays across borders, a currency peg is more than background macro context. It is a policy regime that can affect assumptions in your pricing, treasury, and payout logic. The core risk is not predicting markets. It is avoiding product and finance decisions that only work while a pegged rate stays stable.

How Rupee Depreciation Affects Real INR Income for Indian Freelancers

**Rupee depreciation means the INR weakens against the USD, so the same USD invoice can convert into more INR before deductions. But if you do not control timing, fees, and proof, you are still guessing.** Treat FX as part of operations. Define the terms, choose a repeatable collection rail, track what happened, and keep records you can defend later.

Local Currency Payouts vs USD Payouts for Contractor Platforms

USD versus local currency is not just a finance setting. For a platform, it changes compliance scope, recipient certainty, reconciliation effort, and how much engineering depth your payout layer needs. In practice, many teams avoid picking one currency forever. A common approach is to set corridor-level rules: use local currency where it is legally and operationally supported, and keep USD as a fallback where legal, coverage, or operational constraints are still real.