Quick Answer

Yes. A pegged exchange rate can still create sudden operating risk, so platform teams should decide in advance how pricing, FX conversion, and payout approvals behave under stress. For currency pegging risk platforms currency devalues overnight scenarios, the practical defense is enforceable firm-quote expiry, corridor-level controls, and payout batches that trace back to one confirmed conversion decision in the ledger.

What a Broken Peg Changes for Platform Payments#

For a platform that collects, converts, and pays across borders, a currency peg is more than background macro context. It is a policy regime that can affect assumptions in your pricing, treasury, and payout logic. The core risk is not predicting markets. It is avoiding product and finance decisions that only work while a pegged rate stays stable.

- A peg is a policy choice, not a constant.

Currency pegging means a country links its exchange rate to another currency, a basket of currencies, or another value measure. You will also see it called a fixed exchange rate. The practical point is that the rate is held to a reference, often at a predetermined ratio, to provide stability. If your marketplace platform or embedded payments product depends on that stability to price fees, book balances, or time conversions, treat the peg as a live operating input.

- Stable does not mean risk-free.

Pegs are often used to support a more predictable trading environment, and the U.S. dollar is the main anchor for many of them. More than 66 countries have currencies pegged to the U.S. dollar. That scale is one reason teams get comfortable. The mistake is assuming a peg removes exchange-rate risk. It does not. A peg is a policy choice that can be maintained or adjusted, and your product may feel that before your customers understand what changed.

- Platform exposure shows up in operations before it shows up in theory.

Depending on your flow, if you collect in USD, convert later, and disburse in another currency, you can create timing exposure whether you call it that or not. The same is true if you promise a user-facing price before conversion actually happens, or if your payout engine batches transfers on a fixed schedule.

Use a simple checkpoint: confirm where your business is actually exposed today. Look at quote timing, settlement timing, payout timing, and the ledger event that locks each one. A failure mode to watch for is finding out too late that your product shows one price, your treasury converts at another moment, and your ledger has no clean link between the two.

- This article is for operators choosing response models, not traders guessing direction.

The focus here is finance, product, ops, and engineering teams responsible for payout continuity and ledger integrity under stress. The job is not to outsmart the foreign exchange market. It is to choose an operating model that still works if a pegged exchange rate stops being the quiet assumption beneath your flow.

Before you analyze macro scenarios, decide how your platform will respond if the peg stops behaving the way your product expects.

Choose the right response model before a peg event#

Choose your response model by where your product fails first, not by trying to call the market. If a USD-to-INR flow cannot absorb intraday margin movement, use controls that lock conversion timing, even if payout speed slows.

| Factor | What to assess | Implication |

|---|---|---|

| Gross-margin sensitivity | How much unplanned FX movement you can absorb between collection, conversion, and payout before payouts become uneconomic | Keep conversion execution timing tight when margin protection is the priority |

| Payout SLA rigidity | Whether payout timing is truly rigid or fast payout is mostly a growth habit rather than a hard commitment | Define conversion windows and exception handling before stress events when timing is rigid |

| Customer pricing flexibility | Whether your pricing model implies certainty or users can accept execution-time variation | If pricing implies certainty, use stronger internal FX controls; pass-through pricing can reduce exposure only if UX and support can handle it |

| Ability to enforce firm quote expiry | Whether you can reliably enforce quote expiry and reject stale execution | If you cannot, timing risk stays open; quote ID, expiry, execution, ledger entry, and payout event must stay linked |

This is a finance, product, ops, and engineering decision for teams that own ledger integrity, payout batches, quote handling, and escalation. It is not a speculative FX trading exercise.

- Gross-margin sensitivity

If margin protection is your priority, keep conversion execution timing tight. The key question is how much unplanned FX movement you can absorb between collection, conversion, and payout before payouts become uneconomic.

- Payout SLA rigidity

If your payout timing is truly rigid, define conversion windows and exception handling before stress events. If fast payout is mostly a growth habit rather than a hard commitment, you usually have more room to protect margin.

- Customer pricing flexibility

If your pricing model implies certainty, you need stronger internal FX controls. If users can accept execution-time variation, pass-through pricing can reduce your exposure, but only if your UX and support model can handle it.

- Ability to enforce firm quote expiry

If you cannot reliably enforce quote expiry and reject stale execution, timing risk stays open. The practical standard is technical enforceability: quote ID, expiry, execution, ledger entry, and payout event must stay linked.

Treat this as governance, not guesswork. Foreign exchange risk is a defined control area in examination guidance, and stress in pegged regimes does not behave like routine confidence swings in floating regimes, so your operating model should reflect that.

Final checkpoint: confirm that every payout batch can be traced to the exact conversion decision that funded it. If you cannot do that today, move to the tighter model now.

If you want a deeper dive, read Intacct vs. NetSuite for Payment Platforms: Which ERP Handles Multi-Currency and High-Volume AP Better.

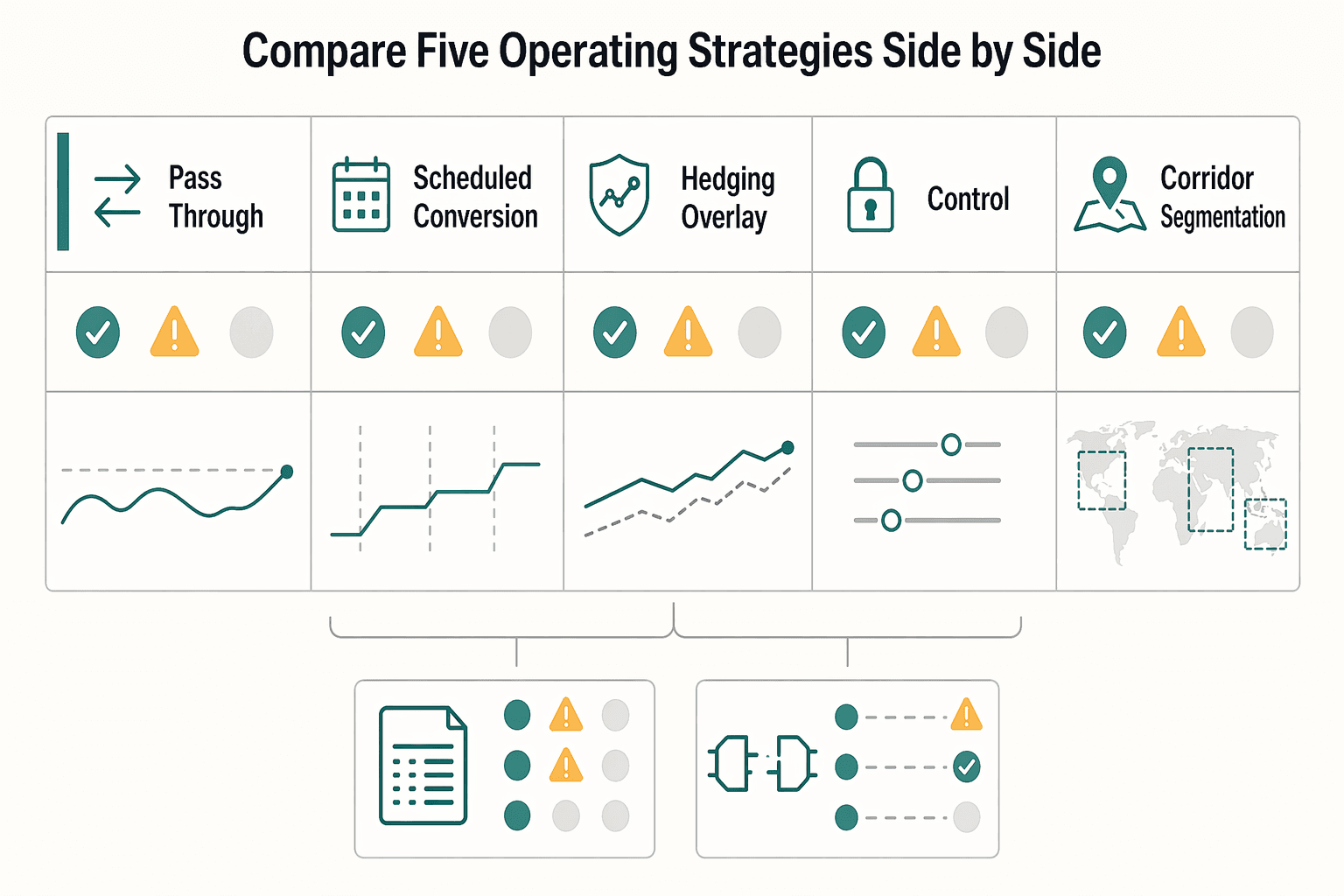

Compare five operating strategies side by side#

These options are not interchangeable. Pick the model that controls loss where your workflow is most likely to fail first: pricing, conversion timing, or payout execution.

| Strategy | Best for | Key pros | Key cons | Failure mode |

|---|---|---|---|---|

| Pass-through pricing | Flows where users can accept execution-time FX movement | Moves FX movement to execution, helps protect margin during volatility | Higher UX and support burden if price certainty is expected | Stale or unclear quote handling creates disputes about which rate applied |

| Scheduled conversion windows | Teams with predictable payout cycles | Clear operating cadence for conversion and payouts | Less flexibility if conditions move between windows | A windowed cadence locks in timing when you need flexibility |

| Hedging overlay | Recurring net exposure that remains after pricing/timing controls | Can reduce residual economic exposure | Added treasury process and cost | Hedge structure and real flow timing drift apart |

| Temporary payout controls | Incident periods when normal assumptions are unreliable | Buys time to contain operational and pricing risk | Slower payouts and heavier exception handling | Controls are activated or lifted at the wrong time |

| Corridor segmentation | Multi-corridor platforms with uneven risk by route | Contains corridor-specific stress instead of applying one policy everywhere | More policy/routing complexity | Weak isolation lets stressed corridors affect others |

Use the next grid as an internal scoring sheet, not a universal ranking.

| Evaluation row | Pass-through pricing | Scheduled conversion windows | Hedging overlay | Temporary payout controls | Corridor segmentation |

|---|---|---|---|---|---|

currency peg break risk | Shifts risk to execution-time pricing | Concentrates timing decisions at window cutoffs | Offsets some economic exposure, not execution risk | Pauses activity while conditions are unclear | Limits where break risk can spread |

firm quote dependency | High | Medium | Medium | Low to medium | Medium |

ledger reconciliation complexity | Medium | Lower to medium | Higher | Medium to high during incidents | Higher with route-specific rules |

Impact on payout batches | More variable outcomes if quotes are stale | More predictable cadence, less intraday flexibility | Depends on hedge-to-flow alignment | Potential delays and backlog risk | Batch behavior differs by corridor policy |

In practice, implementation effort usually lands in different teams:

- Finance ops: scheduled windows and hedging controls, plus explainable conversion and funding records.

- Product UX: pass-through messaging and expectation-setting around execution-time rates.

- Engineering: segmentation and incident controls, especially webhook reliability and strict

idempotency keyhandling so retries do not create duplicate funding or payout actions.

Context check: the foreign exchange market averaged US $5.3 trillion per day in April 2013, and large international banks are the main participants. Market depth does not remove platform-side control risk.

If you are running high-growth embedded payments, start with corridor segmentation and add scheduled windows only where payout timing is stable. For compliance-heavy Merchant of Record operations, default to scheduled windows with pre-approved temporary payout controls; add hedging as a second-layer decision when residual exposure remains.

Related: A guide to currency options for 'hedging' against forex risk.

Use pass-through pricing when margins are thin and users can absorb FX movement#

Use pass-through pricing when the conversion rate is a live transaction input, not a rate your product implies is locked. If the user sees one rate but execution can happen later at another, disputes are likely.

Choose it when the rate is part of the transaction#

Choose this model when the user accepts that conversion is finalized at execution. In that setup, pass-through shifts more timing risk to the conversion moment instead of leaving it inside your treasury window.

That aligns with the IMF's July 2004 point on exchange-rate transitions: flexibility depends on a deep, liquid FX market and on participants being able to manage exchange-rate risk. Pass-through is not a shield by itself; it is a risk-allocation choice.

Treat control design as the deciding factor#

Pass-through pricing is only as strong as the controls behind it:

| Control | Requirement |

|---|---|

| Explicit acceptance | Make it clear the quote is time-bound and conversion is final only at execution |

| Quote-expiry enforcement | Expired quotes should fail cleanly, not drift into silent repricing |

| Retry discipline | Retries should respect quote state and require fresh acceptance when needed |

Verify the evidence trail before rollout#

Before rollout, confirm each payout can be traced end to end in your records: accepted quote state, execution timing, provider response, and payout event. FDIC examination material includes dedicated foreign-exchange risk sections, and weak traceability becomes a control issue quickly when rates move.

If you cannot reject stale quotes cleanly and prove which quote governed which payout, do not use pass-through for high-volume cross-border flows yet.

Use scheduled conversion windows when payout timing is predictable#

Scheduled conversion windows are a strong fit when your payout cadence is predictable and you can batch by corridor, because they improve control without promising better FX pricing. If pass-through pricing creates too much user-facing rate movement, this model shifts more of the timing decision into treasury operations.

Why this model works#

Use it when your payouts already run on a recurring schedule. You can automate payouts daily, weekly, or monthly, and providers can automate timing through configured sweeps instead of one-off manual sends. That gives you a defined operating rhythm for conversion, payout, and reconciliation.

Batching also simplifies finance operations. A payment batch groups payable items for processing together, so you can run one corridor-level conversion decision at each window instead of many separate ad hoc decisions. In practice, that often means fewer spread surprises than fully ad hoc conversion, but it is still not a price guarantee.

Where it breaks#

The main tradeoff is exposure between windows. If a peg breaks before your cutoff, the unconverted balance can reprice in one move.

The Swiss National Bank example is the reminder: on 15 January 2015, it discontinued the CHF 1.20 per euro minimum exchange rate. Scheduled windows can reduce day-to-day noise, but they do not prevent gap moves or remove settlement risk.

Operator rules that matter#

For USD collections and INR contractor payouts, with preset windows and an exception queue, execution quality depends more on controls than labels:

| Rule | What to enforce | Operational detail |

|---|---|---|

| Lock cutoff times | Use a hard cutoff and enforce it | Submissions or approvals after cutoff move processing to 5 am the next business day in documented ACH/check batch flows |

| Define override authority | Unapproved batches should not process | Set who can approve exceptions and what evidence is required |

| Post webhook status changes into the ledger | Record conversion and payout status changes in ledger state | Providers send payout events after scheduled or on-demand triggers, often as JSON payloads for your app. Do not treat raw webhook receipt as finished reconciliation |

Add a hedge overlay when exposures exceed your tolerance#

Use a hedge overlay when scheduled conversion windows still leave more FX risk than your platform can absorb. It fits recurring net exposure, including forecast net U.S. dollar obligations, when pricing and payout timing controls cannot neutralize the risk on their own.

When it earns its keep#

A treasury hedge sits behind the product, so you can keep the standard payout UX while finance offsets part of the exposure outside the user flow. The practical gain is lower shock concentration in one operating period and better planning confidence for cash, margin, and payout funding. A hedge reduces risk; it does not eliminate FX risk.

What to verify before you trade#

Do not hedge gross flow because top-line volume is large. Hedge the approved net forecast, with date buckets, corridor assumptions, and settlement timing documented. Before execution, confirm the exposure forecast, treasury approval, and trade confirmation match on currency, amount, and maturity, and reconcile to the ledger.

Where teams get hurt#

Weak estimation is the common failure mode. If the hedge profile and actual cash-flow pattern diverge, basis mismatch can erase much of the benefit. Plan for liquidity pressure as well: in stress periods, derivatives exposure can face margin calls when cash is already tight. Treat risk measurement as one input, not the whole risk decision, and avoid treating historical model outputs as predictions; if forecast quality is weak, keep the overlay smaller or stay with conversion controls.

For a step-by-step walkthrough, see Choosing Functional Currency for Your Business.

Apply temporary payout controls when peg stress turns into an incident#

When peg stress becomes an active incident, temporary payout controls are the safest way to contain loss while you keep compliance checks and auditability intact. The goal is not a full freeze. The goal is to slow or pause only the flows you cannot safely verify, then restore service in controlled steps.

Order of operations#

Use a tight sequence during the incident:

- Pause high-risk corridors first.

Limit action to corridors where pricing or execution confidence has broken, rather than stopping all payouts.

- Tighten firm-quote expiry.

Shorten quote validity so stale pricing cannot move through funding and release.

- Route exceptions to manual approval.

Pull non-standard payouts out of straight-through processing until quote, approval, and status are clear.

- Resume in staged payout batches.

Bring back lower-risk flows first, then widen once controls and reconciliation are stable.

If payouts slow, communicate that directly: what is affected, why, and what must be true for release.

Evidence pack to require before wider resume#

| Evidence item | What to verify | Why it matters |

|---|---|---|

| Incident timeline | Declaration time, control changes, and resume milestones | Creates a defensible incident record |

| Affected ledger entries | Pending, held, released, reversed items during incident window | Confirms financial state matches operating decisions |

| Provider references from webhooks | Event IDs, timestamps, status transitions per payout | Distinguishes true execution from delayed/replayed updates |

| Customer-impact log | Delays, notices, escalations, refunds | Keeps support, finance, and compliance aligned |

Before scaling back to normal flow, your payout status, provider webhook state, and ledger state should agree for each released item.

Control discipline on alternative rails#

Do not treat alternative rails as a reason to weaken controls. Stablecoins are digital assets designed to maintain stable value relative to fiat or another reference asset, and current policy framing includes AML/KYC compliance alignment. Keep the same compliance gates and the same evidence standard before funds move.

Segment corridors and products so one peg break does not hit everything#

Segmentation can help limit blast radius, but specific corridor or product-control rules vary by platform and operating model. Build segmentation logic based on your own corridor data and control ownership rather than assuming a single framework applies across all products.

Best fit#

Use this pattern only as an internal operating choice. Decide fit based on your own production data, control ownership, and incident history.

How to segment it#

If you proceed, keep the design auditable and explicit so teams can see which rule applied and why. Avoid hidden routing logic that you cannot trace during an incident.

What breaks#

More routing paths can increase policy complexity and make errors harder to detect. Before rollout, confirm rule ownership, change control, and test coverage in your own environment.

Related reading: How to Evaluate Multi-Currency Personal Finance Software for Tax Residency, FBAR, and Invoicing.

Conclusion#

The practical takeaway is not to predict when a currency peg might come under pressure. It is to decide in advance how your platform will price, convert, approve, and reconcile when stability stops being reliable.

-

Choose the operating model before stress chooses it for you. A peg is meant to stabilize FX behavior and reduce volatility, but that same design can limit a country's ability to respond independently to shocks. That matters because Brookings notes the U.S. dollar has strengthened considerably since mid-2021, and the dollar's nominal effective exchange rate closely tracks global financial conditions. The difference is simple: a platform with preagreed rules for quote expiry, payout approvals, and corridor exceptions can tighten controls cleanly, while a platform relying on judgment calls usually ends up honoring stale assumptions.

-

Operate in three states, not one. For most teams, the durable model is normal-state controls, incident-state payout governance, and post-incident reconciliation rooted in ledger evidence. If a corridor cannot obtain or honor a valid firm quote, do not keep it moving just to preserve payout speed. Slow or pause that corridor, keep lower-risk routes running, and make finance, ops, product, and engineering own explicit parts of the decision. The key checkpoint is an evidence pack that ties quote ID, execution timestamp, payout event, and provider references from webhooks into one incident record. A common failure mode is retries firing during market stress, duplicate payout attempts appearing, and teams being unable to prove which rate was actually committed.

-

Design cross-border products so one corridor problem stays local. Brookings also says dollar appreciation shocks predict downturns in EMDEs, which had reached 57.9% of world output by 2021. So even if your exposure feels like a single-country issue, the operating risk is often broader than one market or one payout partner. The differentiator here is segmentation: separate conversion rules, approval thresholds, and payout logic by corridor and product type so a stressed route does not freeze the rest of the platform.

-

Make the binding moment explicit in the product. If you are designing flows now, define exactly when the FX rate becomes binding, which compliance gate must clear before payout release, and who can override an exception. Do not leave that buried in ops habit or provider behavior. A useful red flag is any payout promise your ledger cannot trace back to a quote and final execution state.

-

Treat reconciliation quality as part of the customer promise. The U.S. share of world GDP at purchasing power parity was 15.7% in 2021, yet the dollar's nominal effective exchange rate still closely tracks global financial conditions. In practice, that means you should assume shocks can show up outside the corridor where you first notice them. If your records are clean, a peg break is a contained operating event. If they are not, it becomes a platform-wide trust problem.

We covered this in detail in How to Choose a Presentation Currency for Financial Reports.

Frequently Asked Questions

What is currency pegging risk for a platform business?

For a platform, pegging risk is the risk of depending on a currency relationship that is treated as fixed for pricing or payouts. A currency peg ties one currency’s exchange rate to another, often the U.S. dollar, and some countries use a currency basket instead of one currency. Pegging is commonly described as a fixed-rate setup intended to add stability.

Can a currency devalue overnight even under a currency peg?

The grounding material does not support a timing claim like whether a move can happen overnight. It supports that pegging is intended to bring stability through a fixed-rate setup, but that is not the same as an absolute guarantee.

How does a peg break hit marketplace margins first?

Pegs can promote trade and raise real incomes, but they can also lead to persistent trade deficits.

Should we pause payouts during peg stress or keep them running?

The source material does not provide platform-specific payout instructions for peg stress. A pause-or-continue decision should be handled by your own operating and risk policy, not assumed from the peg itself.

What early signals suggest a pegged exchange rate is becoming fragile?

There is no single early-warning signal or threshold in the source material here that indicates a peg is about to fail. The excerpts provide definitions and trade-offs of pegging, not predictive operational signals.

What should finance, ops, and engineering do in the first 24 hours after a devaluation?

Build a 24-hour devaluation response plan for finance, ops, and engineering based on your own incident-response protocols.

How do we reduce peg-break exposure without breaking user experience?

Based on the source, the defensible baseline is to treat a peg as a stability mechanism tied to fixed ratios, not as a certainty guarantee. Design user promises and risk controls accordingly. If margin sensitivity is the real issue, this companion guide on protecting gross margin in USD collection and INR payout is the next useful read.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bis.org/publ/bppdf/bispap96.pdftrusted

- bis.org/cpmi/pietf/fx_risk_mitigation.pdftrusted

- brookings.edu/wp-content/uploads/2022/09/BPEA-FA22_WEB_Obs...trusted

- businesslawreview.uchicago.edu/print-archive/event-contracts-are-step-too-f...trusted

- downloads.regulations.gov/ITA-2023-0010-0061/attachment_1.pdftrusted

- ecb.europa.eu/press/financial-stability-publications/fsr/s...trusted

- fdic.gov/risk-management-manual-examination-policies/...trusted

- federalreserve.gov/monetarypolicy/files/FOMC20140430meeting.pdftrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Currency Risk for Platforms Collecting USD and Paying INR

USD collection with INR payout creates a real gross-margin risk as soon as money movement happens across time instead of in one instant. The issue is simple: if the USD amount is known now but the INR conversion or payout happens later, your margin is exposed to the USD-INR move during that gap.

Intacct vs. NetSuite for Payment Platforms: Which ERP Handles Multi-Currency and High-Volume AP Better

Treat this as an integration-debt decision first, and an ERP comparison second. For payment platforms, multi-currency accounting and higher-volume AP risk usually shows up at the seams between product behavior, finance controls, and integrations, not in top-level feature lists.

Currency Options for Hedging Against Forex Risk

You can deliver the work and still receive less in your home currency by the time payment arrives. If your contract is in one currency but your home currency is another, the invoice value can change between signing and settlement.