Quick Answer

Yes. Rupee depreciation can improve your INR from USD invoices, but only after spread, payout charges, and bank deductions are reconciled. In January 2026, USD/INR reached ₹92.04, yet that headline move was only gross conversion upside. To judge real results, compare the benchmark rate at your timestamp, the customer rate actually applied, and the INR that hit your bank for the same invoice.

Rupee depreciation: an input you can systematize (and stop guessing)#

Rupee depreciation means the INR weakens against the USD, so the same USD invoice can convert into more INR before deductions. But if you do not control timing, fees, and proof, you are still guessing. Treat FX as part of operations. Define the terms, choose a repeatable collection rail, track what happened, and keep records you can defend later.

It helps to separate two ideas that often get mixed together.

| Concept | What it means (plain English) | Where it shows up in your work |

|---|---|---|

| Tax depreciation | An accounting or tax concept about recognizing asset value over time. | Your bookkeeping and tax filing, for example equipment. |

| Rupee depreciation | A decline in the value of the Indian Rupee (INR) relative to a foreign currency, often the United States Dollar (USD). | Your gross INR from USD to INR conversion, and your net after fees, timing, and tax handling. |

When people talk about freelancer income rising because the rupee weakened, they usually mean the second row: currency movement in USD/INR. That can increase gross INR from USD invoices, but what you actually keep still depends on fees, conversion timing, and tax handling.

The "paid, reconciled, repeatable" mindset#

Use one standard for FX decisions: paid, reconciled, repeatable. A favorable rate matters only if the money lands, the records match, and you can repeat the process next month without guessing.

| Lifecycle step | What to define |

|---|---|

| Contract terms | currency, due date, late fees, who pays transfer fees |

| Invoicing | what you invoice in, what reference rate you track (mid-market vs provider rate), and when you snapshot it |

| Collection rail | card, ACH, wire, platform, or invoice link; choose based on your cost, speed, and dispute profile |

| FX conversion | when you convert, what rate you actually received, and the fee structure |

| Payout | when funds land in your bank |

| Records | invoice, proof of delivery, payout confirmation, FX conversion details, reconciliation notes |

Where this varies and how to confirm safely#

Recent reporting looked favorable for USD earners. Coverage reported USD/INR breaching ₹91 in January 2026 and touching ₹92.04 on January 28. One example framed that move as a gross uplift without extra billed hours. Forecasts in the same coverage were split, with targets as weak as ₹93 and as strong as ₹87, so direction was not certain.

Treat that upside as a scenario, not a promise. What you finally keep can still be reduced by hidden fees, bad conversion timing, and tax mistakes.

For related tax context, see A Guide to the Qualified Business Income (QBI) Deduction for Freelancers.

The money-lifecycle mental model (and the 6 terms you must define before touching tactics)#

To control how FX affects your income, map your USD-to-INR path as a lifecycle and define six working terms before you optimize anything. Once each step has a name, you can see where money leaks, where timing risk sits, and what you can actually control.

The 6 terms you can reuse#

Use these as working labels in your process, not as official market standards.

1) Rupee depreciation: Rupee depreciation means a weaker Indian Rupee (INR) against the United States Dollar (USD). In practice, one USD can convert into more INR. That upside can still shrink after fees, conversion timing, and tax handling.

2) USD/INR: This is the currency pair you watch when you convert USD to INR. When USD/INR rises, one USD converts into more INR, before fees and margins.

3) foreign exchange (FX): FX is the conversion of one currency into another. For freelancers, FX shows up in platforms, payment processors, bank conversions, and sometimes client-side transfers.

4) mid-market exchange rate: In this model, the mid-market exchange rate is your benchmark rate. Providers may apply a different customer rate or bundle costs around it, so treat mid-market as a reference point, not a guaranteed payout rate.

5) Exchange rate margin and spread: In this model, an exchange rate margin is the gap between your benchmark rate and the customer rate you receive. A spread is the gap between a provider's buy and sell rates. Both can increase your real conversion cost.

6) Effective exchange rate: This is the rate you actually realize after provider pricing and all fees. This is the number to run the business on.

| What you look at | What it tells you | What it hides |

|---|---|---|

| Mid-market exchange rate | Market benchmark | Provider margin, fixed fees |

| Provider quoted rate | What they'll apply | Whether it includes a margin |

| Effective exchange rate | True cost and outcome | Missed fees you did not log |

Your "exposure windows" (where FX can move and costs appear)#

Most surprises happen in the gaps between events. Do not assume a universal sequence. Map your own timestamps across the contract, invoice, client payment, provider settlement, conversion, and final INR credit. Every gap is an exposure window.

Treat each window as risk, not guaranteed upside. INR weakness may improve INR receipts from USD invoices, but leakage from fees, conversion timing, and tax mistakes is common. Macro direction is uncertain and can change.

A practical step is to add three columns to every invoice record in your tracker: USD amount, INR received, all fees (itemized). If you cannot tie a number to a document or dashboard entry, you cannot defend it later.

If you use platform-based payouts, review the terms closely. For common pitfalls, see this breakdown of Upwork and Fiverr terms.

If you want a deeper dive, read The Best Ways to Diversify Your Income as a Freelancer.

Does rupee depreciation increase freelancer income in India?#

Yes, rupee depreciation can raise your INR from USD invoices, but only if that upside survives fees, conversion timing, and payout friction. The number that matters is net INR received for the same USD invoice, not just a favorable market move.

When the rupee weakens, each USD converts to more INR before costs. In January 2026, the rupee crossed ₹91 per USD and touched ₹92.04 on January 28, highlighting how quickly gross INR conversion can move for USD invoices. But that market move is only the starting point for your actual income.

For each invoice, track three numbers: the USD/INR benchmark, the Provider rate, and the Net INR received.

USD/INR benchmark: market reference at your comparison timestamp.Provider rate: the actual rate your bank, platform, or payout provider applied.Net INR received: what reached your bank after all charges.

Expected, quoted, received#

| Layer | What it shows | Record to keep |

|---|---|---|

| Benchmark rate | Market USD/INR reference | Logged rate source + timestamp |

| Provider rate | Customer rate actually applied | Quote screen, conversion receipt, or payout statement |

| Net INR received | Final INR outcome after charges | Bank credit entry + fee lines tied to that invoice |

Some freelancers invoice in USD but settle in INR, so conversion is a step to reconcile, not something to assume. For each invoice, match four records: the USD invoice, the provider quote or settlement record, the fee statement, and the final INR bank credit. If they do not align, you cannot tell whether gains came from FX or leaked through costs and timing.

If you use marketplace payouts, check whether conversion timing is controlled by the platform or whether costs are embedded in the payout path. That is often where headline FX gains get diluted. For clause-level traps, review this breakdown of platform terms.

Where gains leak#

Most leakage shows up in a few places, and each one is worth logging:

- Spread vs benchmark: compare your logged market reference with the applied provider rate.

- Embedded markup: if a payout says "no fee" but the rate is weaker, treat the quote itself as a cost record.

- Platform or payout costs: reconcile from statements, not memory.

- Bank deductions: verify the final credit against your bank ledger.

- Tax-related impact: poor handling or missing records can reduce apparent gains later, so keep the invoice, fee records, and bank credit together.

Do not plan cashflow around one forecast path. The same source material shows split outlooks, including ₹93 by December 2026 versus ₹87. The practical rule is simple: track net INR per invoice by payment rail and compare it with your benchmark. If one rail repeatedly widens the gap between expected and received INR, treat it as repeatable leakage and change the rail, terms, or conversion timing. For a related angle, see Digital Rupee Cross-Border Payments for Freelancers in 2026.

What FX rate actually "counts" for your invoice-and why timing windows create surprises?#

For reconciliation, the rate that matters most is the one used at actual conversion. The invoice-day USD/INR is a reference point, not your final outcome.

Exchange rates can move continuously in the forex market, and customer rates can differ from the mid-market rate when provider margin is applied. Reconcile against what was actually processed: the applied rate and the final INR amount received.

Track each exposure window with one artifact and one check#

Save one proof item per stage so you can trace where expected INR and received INR diverged.

| Exposure window | What can change | Artifact to save | Reconciliation check |

|---|---|---|---|

| Pricing agreed | Invoice currency can set where FX exposure sits | Signed SOW or client approval with payment terms | Confirm currency, amount basis, and due terms match the invoice |

| Invoice issued | Amount and due terms are documented | Invoice PDF | Match invoice currency and total to the SOW |

| Client payment initiated | A timing gap before conversion can create rate drift | Client remittance advice or payment confirmation | Match payer name and sent amount to the invoice |

| Funds received | Amount available for conversion | Provider receipt or dashboard status screenshot | Confirm the amount received before conversion |

| Conversion executed | Applied customer rate can differ from benchmark rate | Conversion receipt or settlement record | Match amount, applied rate, and net INR outcome |

| INR payout completed | Final take-home amount | Bank credit entry or payout statement | Match bank credit to provider settlement |

What you can decide and what you should buffer for#

Some parts of the outcome are in your control, and some are not. Focus on the decisions that shape the result:

- Invoice currency: decide where FX exposure sits.

- Payment rail: prefer rails with clear records for amount and applied rate.

- Conversion policy: use a repeatable rule instead of ad hoc timing.

- Payout settings: keep settings consistent across invoices.

Then build a buffer for what you cannot control: the time between quote and conversion and rate movement during that window. A common miss is budgeting from a benchmark quote while conversion happens later at a different customer rate.

If you use marketplace payouts, review platform rules before assuming how funds move. For rail-specific terms, see this breakdown of platform terms.

Pre-delivery cashflow check#

Before you commit to a delivery date tied to incoming funds, confirm these basics:

- Invoice currency and amount are final in writing.

- You know which record shows the applied conversion rate.

- You know which record shows the final amount received.

- You are planning from expected net INR received, not a benchmark quote alone.

You might also find this useful: The Best Budgeting Methods for People with Irregular Income.

The contract + invoicing playbook that turns FX volatility into a non-event#

A lot of FX pain starts at the contract stage. The goal is not to predict currency moves. It is to write avoidable risk out of the deal before the invoice is issued.

Your SOW should do five things clearly: set invoice currency, name the payment rail, assign payment fees, define acceptance, and set a late-payment path. If one of those is missing, you can spend time arguing process instead of reconciling a clean payment trail.

Build one control set into every SOW#

Treat these as operating controls, not optional wording. Your SOW is the source of payment logic, and the invoice should repeat it, not reinterpret it.

- Invoice currency

State billing currency in the SOW and keep the invoice aligned. That removes rate ambiguity when you and the client think in different currencies.

- Payment rail

Name the expected rail, for example bank transfer or a platform payout path. That cuts avoidable delay because both sides know what payment proof should exist.

- Fee bearer

State who covers transfer, intermediary, or platform-side costs. This reduces fee leakage and "paid in full" disputes when the net receipt is short.

- Acceptance trigger

Tie sign-off to a concrete deliverable and written response path. This reduces dispute delay from open-ended review language.

- Late-payment escalation path

Define next steps after the due date, for example reminder, pause, or escalation to a named contact. The point is predictability, not threats.

Use the right clause for the job#

Not every clause belongs in every deal. Match the clause to the payment pattern.

| Clause | Use for | Notes |

|---|---|---|

| Late-payment terms | Retainers and milestone work | Clear due dates and a documented basis for follow-up |

| Pause-work trigger | Retainers and multi-phase projects | Prevents one unpaid invoice from turning into several |

| Scope boundaries and change-request language | Milestone and fixed-fee work | Scope drift often turns into payment drift |

| Kill fee or termination mechanics | Long delivery cycles or reserved capacity | Clarifies what is owed if work stops midstream |

| FX review clause for long engagements | Long-running retainers with periodic pricing review | For shorter projects, shorter billing cycles are usually simpler |

In practice, late-payment terms fit retainers and milestone work; pause-work triggers fit retainers and multi-phase projects; scope boundaries fit milestone and fixed-fee work; kill-fee mechanics fit long delivery cycles or reserved capacity; and an FX review clause fits long-running retainers with periodic pricing review. For shorter projects, shorter billing cycles are usually simpler.

For platform-led work, some controls may be replaced by marketplace terms. Upwork says its platform provides tools for greater operational ease and transaction certainty, and highlights "Get paid on time" for talent. Treat that as context, not a blanket guarantee. Check the rules you actually use, especially approvals, holds, disputes, and payout handling, and compare them with this clause-level breakdown.

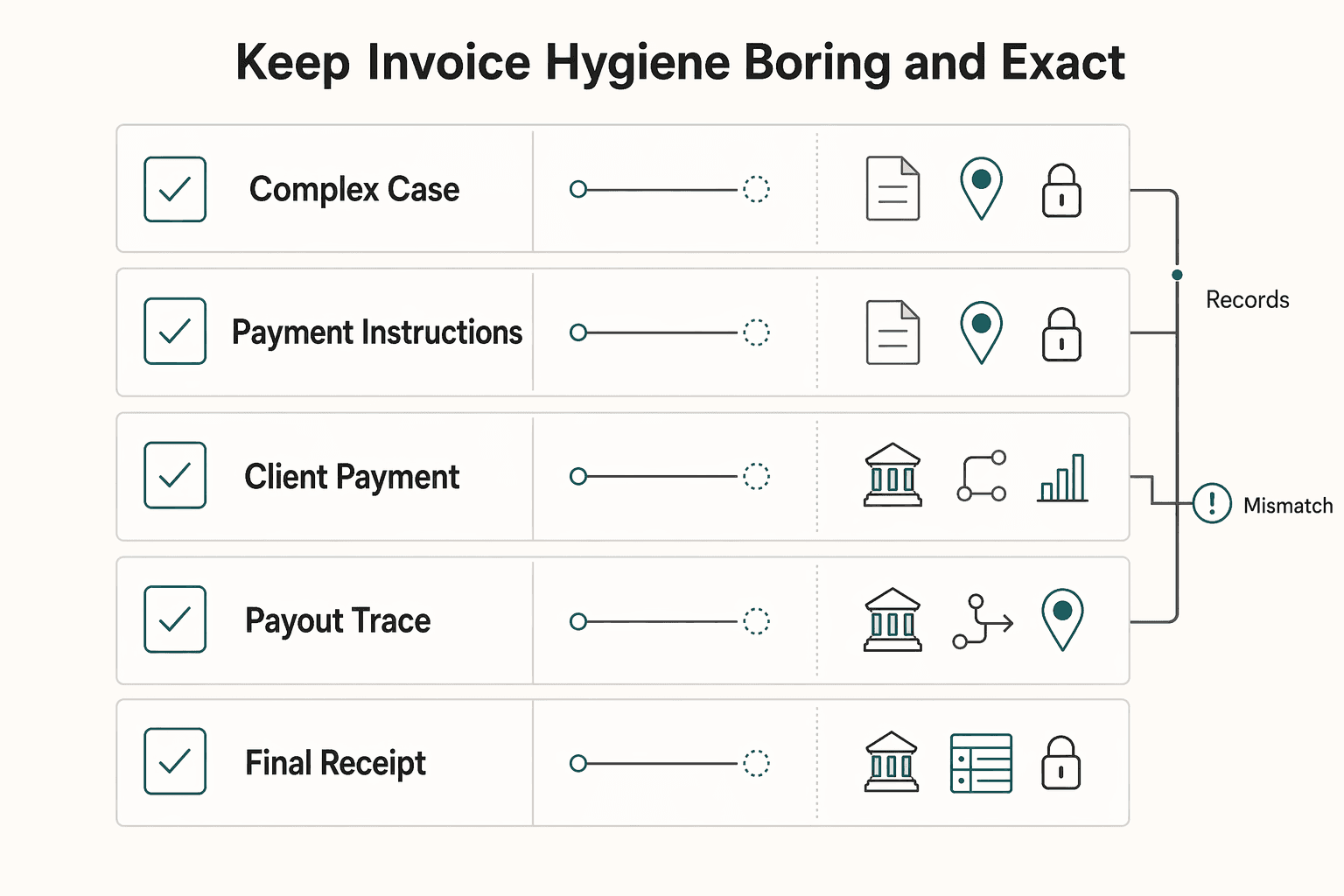

Keep invoice hygiene boring and exact#

Many payment delays come from mismatches, not drama. Keep a small evidence pack for every invoice and store it the same way every time.

| Item to control | What to store | What to match | What to reconcile |

|---|---|---|---|

| Invoice identity | Final invoice PDF | Invoice number, client entity name, currency, total | No duplicates and no version confusion |

| Payment instructions | Invoice payment section or client-approved payment details | Rail, beneficiary details, required payment reference | Client used the expected rail and reference |

| Client payment proof | Remittance advice, platform payment notice, or client confirmation | Payer name and sent amount against invoice | Claimed payment versus amount received |

| Conversion or settlement proof | Provider receipt, dashboard export, or settlement record | Amount converted, applied rate if shown, fees if shown | Net after fees versus expected net |

| Final receipt | Bank credit or payout confirmation | Date and amount credited | Settlement record equals bank credit |

Use a simple sequence: store at event time, match to the prior record, then reconcile to final bank credit. If you wait until month-end, shortfalls are often harder to trace.

Also separate business payment records from personal money movement early. It makes tracing, tax prep, and dispute follow-up cleaner when credits and provider statements are not mixed into personal transactions. If that is messy today, start with Separating Business and Personal Finances: An Important Step for LLCs.

Carry this rule forward: if a term affects amount, timing, or proof, put it in the SOW and repeat it on the invoice. If you cannot verify it later with stored records, tighten it before work starts.

For a step-by-step walkthrough, see The Best Way for a UK Freelancer to Get Paid by an Australian Client.

Before locking your payment rail, run your own numbers with the payment fee comparison tool to see where spread and transfer fees are reducing net INR.

If you earn in USD, should you convert to INR immediately or wait?#

Neither "convert everything now" nor "wait for a better USD/INR" is a durable policy for everyone. INR is in a floating-rate market, and rates can move during trading hours, so timing is uncertain. The practical approach is a simple treasury policy for a solo business: protect runway, match currency to expenses, and avoid forced conversions when rates move against you.

If you turn FX into a prediction game, you can still be forced to convert when obligations are due. Even when the rate looks favorable, the net benefit can shrink because of hidden fees, poor timing, and tax mistakes.

So the real goal is not the perfect rate. It is fewer fee leaks and fewer moments when you have to convert at a bad time because obligations are due.

The two-bucket policy (copy this and customize)#

A staggered policy can be easier to run than one all-at-once decision you may second-guess later. Build two buckets and define a rule you can follow even on busy weeks:

- INR Runway Bucket: Convert a defined portion on receipt to cover your INR obligations, such as rent, contractors paid in INR, EMIs, and operating buffer.

- USD Ops Bucket: Keep a defined portion in USD for USD expenses, such as software subscriptions, cloud, ads, and near-term liabilities you expect to pay in USD anyway.

Track the policy with two simple metrics:

- Net outcome per invoice: the INR you can actually reconcile back to a specific USD invoice, after conversions and fees.

- Monthly policy review: once per month, adjust your portions based on actual spend mix and upcoming cash needs, not one forecast.

| Decision driver | Convert more to INR | Keep more in USD |

|---|---|---|

| Expenses | Mostly INR (runway anxiety) | Meaningful USD bills |

| Cost control | Reduce forced conversions | Avoid repeated conversion fees |

| Risk tolerance | Prefer certainty | Can hold USD without stress |

Operational guardrails (don't skip these)#

The policy only works if the mechanics are clear. Before you rely on any setup, confirm the details in your provider's product settings and terms, where enabled:

- Rate visibility: Use providers that show real-time rates and transparent fees before you convert.

- Timing discipline: Because rates can move intraday, use pre-set checkpoints instead of ad hoc guessing.

- Forecast humility: Analyst views can diverge, so treat forecasts as scenarios, not certainty.

Prefer setups that leave a traceable quote, conversion, and payout trail. In systems like Gruv, where enabled, that can include firm quotes that expire and conversions that reject stale quotes, which keeps your realized-outcome math easier to audit.

Need the full breakdown? Read High-Earners vs. Low-Earners: A Breakdown of Platform Choices for Indian Freelancers.

How do you reduce fees, delays, and chargebacks when getting paid internationally?#

Start with total payout, not the headline fee. To reduce leakage, compare the provider's exchange-rate margin with the mid-market rate and calculate the final payout before you choose the provider. For delays and chargebacks, outcomes can vary by provider terms, so verify current rules before you rely on any one tactic.

Choose the rail based on how the payment actually moves#

Begin with how the client will pay, then compare total payout outcomes on that route before you lock in a provider.

| Rail | When it fits | Main checks before choosing | Practical move |

|---|---|---|---|

| Bank transfer / local receiving details | When this is the available route | Visible fee, offered rate vs mid-market, final payout after deductions | Run a like-for-like payout comparison before selecting the provider |

| Card payment | When this is the available route | Visible fee, offered rate vs mid-market, final payout after deductions | Compare total payout, not fee headlines alone |

| Marketplaces (Upwork, Fiverr) | When work and payout run through a platform | Visible fee, offered rate vs mid-market, final payout after deductions | Review current platform terms, then compare net payout. Use: this platform terms breakdown |

Build a payout workflow around verifiable numbers#

A common failure mode is comparing only the visible fee. In many cases, the exchange-rate margin costs more than that visible fee.

- FX spread check: Compare the provider's offered rate with the mid-market exchange rate, which you are using here as a real-market reference.

- Final payout check: Calculate what the recipient actually receives after deductions.

- Impact check: Even a 1-3% markup can materially change total cost on larger transfers. For example, a 2% difference on $10,000 is $200.

If you want a quick next step, Try the free invoice generator.

This pairs well with our guide on Foreign Exchange Risk for Freelancers Getting Paid Internationally.

Compliance friction is real: build a "no-surprises" documentation pack (and keep it tax-ready)#

Cross-border payments can be reviewed. The practical response is not panic. It is a clean document pack that makes the payment story easy to validate from contract to bank credit.

The cost here is not only tax paid. It is also the admin time, software, and accounting effort needed simply to determine what is owed and explain what happened. That is why this belongs in your core cashflow process, not in a pile of paperwork you postpone.

Common review checkpoints and how to keep them from becoming holds#

Exact provider rules vary, so treat these as practical checks, not provider-specific legal rules.

- Identity gaps

Expired ID, unclear uploads, or outdated address details can lead to extra verification. Keep a current ID pack and refresh profile details before large invoices or payout-method changes.

- Entity mismatches

Different name or address versions across contract, invoice, and beneficiary details can lead to follow-up questions. Standardize one legal name and address block across all documents and payout settings.

- Incomplete invoice context

Generic invoice descriptions without scope or delivery trail can be harder to verify. Store the SOW, milestone note, acceptance message, and delivery artifact with each invoice.

- Payout detail mismatches

Incorrect beneficiary details or changed destination settings can delay review or release. Re-check details before the first payout on any new route and save the confirmation receipt.

Quick check before you upload anything: compare five fields side by side across the invoice, payment confirmation, and bank credit: name, invoice number, amount, date, and payout destination.

Build the pack once and store it where you can still reach it later#

Use one master archive with client folders and invoice-level subfolders, plus an offline backup. Keep business records separate from personal transaction history where possible. That separation makes audits and tax prep easier, and it supports cleaner controls as your work grows. See separating business and personal finances.

| What to collect | Owner | Where to store it | Primary use |

|---|---|---|---|

| Government ID and current address proof | You | /Compliance/KYC/current/ | Identity/address consistency checks |

| Signed contract, SOW, change orders | You + client | /Clients/ClientName/01-Agreement/ | Commercial context for reviews |

| Invoice PDF, milestone note, acceptance message, delivery artifact | You + client | /Clients/ClientName/02-Invoices/Invoice-###/ | Reconciliation of billed work |

| Client remittance advice, payout receipt, FX/conversion receipt | Client + payment provider | /Payments/YYYY/Invoice-###/ | Reconciliation of amount, fees, rate, and timing |

| Bank credit evidence and tax working papers | Bank + you | /Bank/YYYY/ and /Tax/YYYY/ | Tax prep and filing support |

Do not rely on portal access later. Security checkpoints can block retrieval, and links that worked earlier may stop working. Download or capture records the same day each step is completed.

For India workflow, keep one subfolder per foreign receipt with the remittance evidence you actually receive or are asked to provide. That can include bank credit advice, payout confirmation, and any inward remittance support your bank, provider, or accountant asks for. Confirm the exact document list with them instead of assuming one fixed requirement.

What should you do the moment a payout is held?#

Freeze the facts first: hold notice, transaction ID, invoice, payout details, and the latest profile details submitted. Then send one consistent packet to support so the case is reviewed against a single version of events. Avoid piecemeal uploads that create conflicting records and longer back-and-forth.

What is the minimum document set to keep before you send an invoice?#

There is no universal minimum that fits every provider or every India scenario. A practical base set is identity documents, signed agreement or SOW, invoice, delivery proof, payout receipt, and matching bank credit evidence. Save client remittance advice when available because it makes reconciliation easier later.

How should you retain records if rules and portal access can change?#

Avoid deleting foreign-receipt records once funds arrive. Keep a documented retention routine with your accountant or CA and preserve payment and FX records beyond immediate filing needs. If a document exists only in a portal, download it immediately so access changes do not break your audit trail.

Related reading: How to Use QuickBooks Online to Manage Multiple Currencies as a Freelancer.

If you want a cleaner invoice-to-withdrawal workflow with clear status visibility and records, explore Gruv for freelancers.

Frequently Asked Questions

What should you do the moment a payout is held?

Freeze the facts first: hold notice, transaction ID, invoice, payout details, and the latest profile details submitted. Then send one consistent packet to support so the case is reviewed against a single version of events. Avoid piecemeal uploads that create conflicting records and longer back-and-forth.

What is the minimum document set to keep before you send an invoice?

There is no universal minimum that fits every provider or every India scenario. A practical base set is identity documents, signed agreement or SOW, invoice, delivery proof, payout receipt, and matching bank credit evidence. Save client remittance advice when available because it makes reconciliation easier later.

How should you retain records if rules and portal access can change?

Avoid deleting foreign-receipt records once funds arrive. Keep a documented retention routine with your accountant or CA and preserve payment and FX records beyond immediate filing needs. If a document exists only in a portal, download it immediately so access changes do not break your audit trail. Related reading: How to Use QuickBooks Online to Manage Multiple Currencies as a Freelancer. If you want a cleaner invoice-to-withdrawal workflow with clear status visibility and records, explore Gruv for freelancers.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- canton.edu/media/pdf/catalog15-16.pdftrusted

- digitalcommons.pepperdine.edu/cgi/viewcontent.cgitrusted

- hcpf.colorado.gov/sites/hcpf/files/ED%2025-03-28-A%20Final%20-...trusted

- icsi.edu/media/webmodules/Final_Book_Tax_Laws_&_Pract...trusted

- sec.gov/Archives/edgar/data/1829864/0001829864260000...trusted

- sec.gov/Archives/edgar/data/1829864/0001829864250000...trusted

- som.yale.edu/media/5046/downloadtrusted

- en.adgm.thomsonreuters.com/entiresection/22729external

Educational content only. Not legal, tax, or financial advice.

Related Posts

How LLC Owners Separate Business and Personal Finances

For an LLC, separating business and personal money is best treated as a weekly habit, not a one-time bank setup. It keeps records cleaner, cuts month-end cleanup, and creates clearer boundaries as the company grows.

What Freelancers Miss in Upwork and Fiverr Terms of Service

Use this manual when a client request touches platform rules and you need a clear call fast. It is built for **upwork fiverr terms of service** decisions where speed matters, but traceability matters more.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.