Quick Answer

Choose billable hours when scope is uncertain, then move to project fees only after deliverables and approvals are clearly documented. For quickbooks billable hours vs project fees, the practical sequence is control first, optimization second, and outcome-based pricing last. Use hybrid pricing when a fixed base scope is stable but extra requests are likely. Keep cashflow steadier by pre-setting invoice timing and requiring written approval for any out-of-scope work.

Stage 1: The Foundation - Mastering Billable Hours for Bulletproof Control#

If scope is still fuzzy, do not force a project fee. Here, hourly billing is your risk-control model. It makes the work visible, catches scope drift early, and reduces the chance that effort slips into unpaid goodwill.

Read the signals before you price#

Before you choose a billing model, get clear on the signals that most directly affect dispute risk and billing capture:

| Factor | Stay hourly when | Consider a project fee when |

|---|---|---|

| Scope boundary | Scope is still fuzzy or boundaries are still moving | The scope boundary is clear enough to defend in the engagement agreement |

| Boundary test | You cannot describe the boundary of the work in one short paragraph and defend it in an engagement agreement | The engagement has a fixed deliverable |

| Predictability | Uncertainty is still high | Inputs are stable and historical patterns are reliable |

In practice, focus on whether the scope boundary is clear enough to defend in the engagement agreement, whether work descriptions are specific and understandable to the client, and whether your tracking process is consistent enough to avoid missed billable entries.

Hourly is usually the safer default when uncertainty is still high and boundaries are still moving. If the engagement has a fixed deliverable, stable inputs, and reliable historical patterns, that is usually when it makes sense to consider a project fee.

A simple rule: if you cannot describe the boundary of the work in one short paragraph and defend it in an engagement agreement, stay hourly for now.

Run a no surprises cadence#

Time tracking is not about surveillance. It is about dispute prevention and billing capture. A legal-industry source notes that technology-driven tracking systems can reduce billing leakage by up to 30%, but that is directional, not universal, and comes from a legal-services context. The broader point is the same: disciplined tracking improves your chances of capturing work you actually performed.

| Step | When | Detail |

|---|---|---|

| Log time | The same day | Time tracking is about dispute prevention and billing capture |

| Tie each entry to the right client and service description | When logging time | Use the right client and service description for each entry |

| Write descriptions a client can understand without translation | When logging time | Use descriptions a client can understand without translation |

| Send client-facing updates | Usually weekly or at each agreed checkpoint | So the invoice never lands as a surprise |

| Do one approval check | Before billing | Confirm the work matched the engagement agreement, out-of-scope requests were flagged in writing, and billing descriptions line up with updates |

Keep the operating standard plain: log time the same day, tie each entry to the right client and service description, and write descriptions a client can understand without translation. Then set a client-facing update cadence, usually weekly or at each agreed checkpoint, so the invoice never lands as a surprise.

Before billing, do one approval check. Did the work match the engagement agreement? Were out-of-scope requests flagged in writing? Do your billing descriptions line up with what the client already saw in updates?

That last step matters. Clear engagement agreements and transparent billing descriptions are strong protection against disputes. Common failure modes are predictable: undercharging, missed billable-time capture, and billing arrangements that create avoidable ethics risk.

Keep hourly profitable in QuickBooks#

If you use QuickBooks, treat setup as a control point. Verify current behavior in your specific product and subscription before you rely on any workflow assumption. This section does not establish QuickBooks-specific tagging, mapping, or invoice pull-through procedures.

Whatever tool you use, the control goal is simple: capture work promptly, align entries with the engagement agreement, and review billing descriptions for clarity before you send them.

Verdict: start hourly when scope risk is real, and treat tracking as a collection control, not just an admin task. This is operational guidance, not tax, legal, or accounting advice. For contract language, tax treatment, or compliance rules, verify with a licensed professional in your jurisdiction.

Related: A Guide to QuickBooks Self-Employed for Freelancers. Want a quick next step? Try the free invoice generator.

Stage 2: The Optimizer - Using Project Fees to Drive Profitability#

Use project fees only when you can still see profitability clearly as work moves. The goal is not just to quote a fixed number, but to keep your fee, costs, and profitability visible in your records so surprises show up early.

A practical readiness check before you quote: confirm the work is clear enough to track, review, and approve without constant re-interpretation. If it is not, keep using hourly billing until the engagement is more stable.

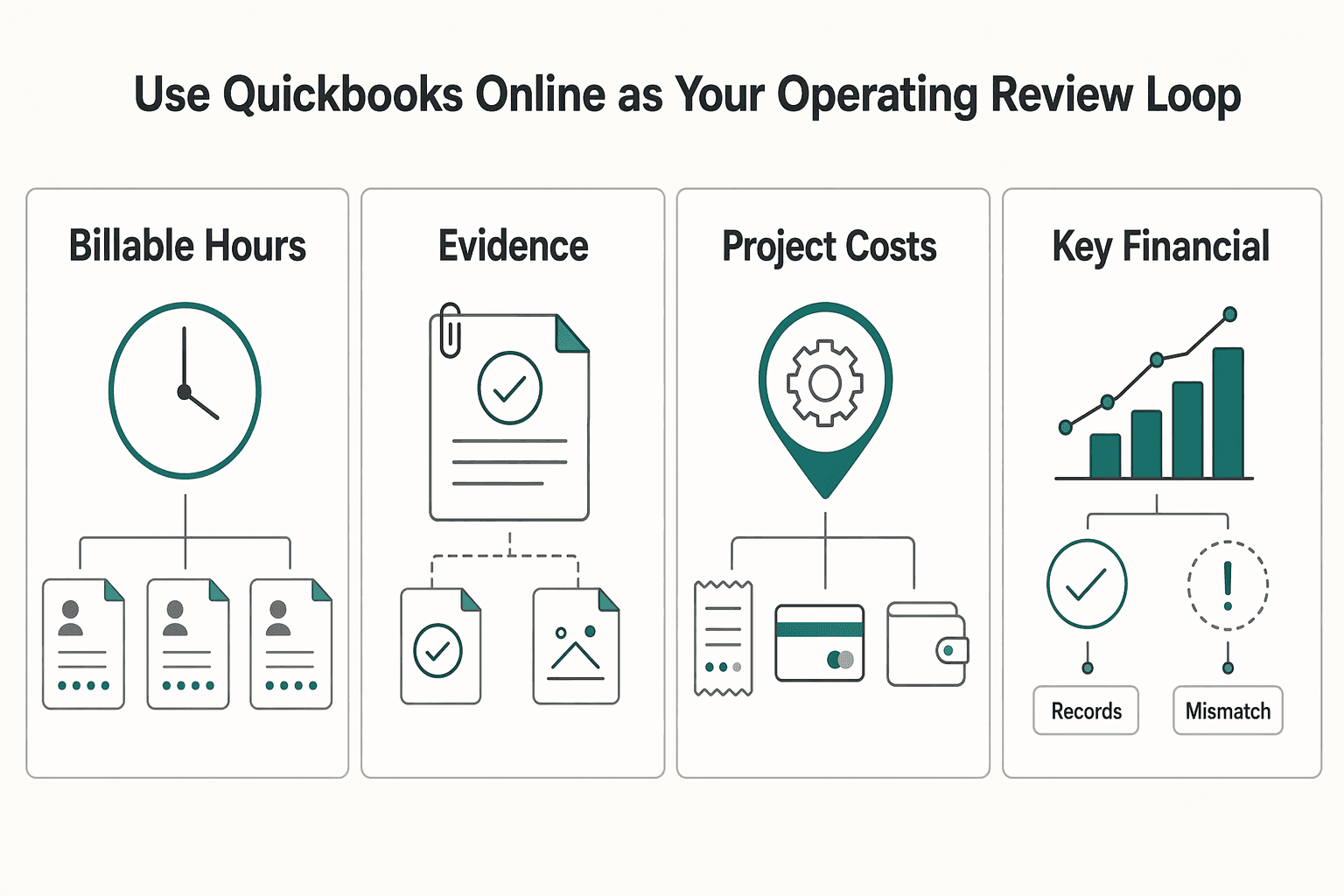

Use QuickBooks Online as your operating review loop#

QuickBooks Online is positioned for service businesses, and it is useful here because it supports tracking hours, expenses, and project costs in one system. Treat that as your operating review loop, not just an invoicing tool.

| What to review | Why it matters | Action if trend weakens |

|---|---|---|

| Billable hours | Shows whether delivery effort is being captured consistently | Review scope and delivery process before the next proposal |

| Expenses | Shows whether project spending is being recorded on time | Tighten coding and entry discipline, then recheck margin impact |

| Project costs | Helps you see whether total delivery cost is drifting | Revisit project assumptions and reset how you price similar work |

| Key financial metrics and reports | Surfaces trend changes for resource and pricing decisions | Make the next pricing or staffing adjustment from report data, not guesswork |

Run this review on a recurring cadence during active work. Data quality is the control point: if entries are late or inconsistent, profitability signals degrade. If others touch the books, train them and enforce clear entry rules so reporting stays decision-ready.

Project fees also need basic risk control in the workflow. Keep scope-change requests and approvals documented, and keep billing timing aligned with the agreement so collection delays do not erase profit gains.

Verdict: project fees can improve profitability when tracking and review discipline are strong; if visibility is weak, hourly remains the safer model.

For a step-by-step walkthrough, see How to Automate Pass-Through Expense Tracking from Clients in QuickBooks.

The Critical Missing Piece: Bulletproofing Your Project Fee Against Scope Creep#

The key point here is simple: do not rely on unverified scope-control or QuickBooks instructions. Confirm specific contract and invoicing mechanics directly in QuickBooks or with a qualified adviser before relying on them.

Use this section as a verification checkpoint before you bill fixed-fee changes:

| Item to lock down in your own documents | What to confirm before work starts |

|---|---|

scope and out-of-scope | Your contract language is explicit and signed |

change request and change order | Your approval path is written and date-stamped |

overage work terms | Your policy is current and documented |

| Invoicing enforcement in QuickBooks | Your estimate/invoice records preserve approvals and history |

Reference artifact captured from the blocked page: 5a14cc86-2c19-11f1-94bc-64b15e5f4cca. Because the source content was not accessible, verify product-specific steps directly in your own QuickBooks account and current contract templates before you apply them.

Verdict: keep fixed-fee protection operational, but treat unverified process details as "confirm first" items, not assumptions. For related workflow context, see How to Handle Billable Expenses in QuickBooks.

Stage 3: The Strategist - Unlocking Maximum Profit with Hybrid & Value-Based Models#

The strategic move is to shift from reactive rate-setting to evidence-based pricing, and to use the model your current evidence can support without exposing you to avoidable margin risk.

| Current condition | Recommended move | Reason |

|---|---|---|

| Scope is mostly stable but extras are common | Start with hybrid | Clear base deliverable, with likely extras or revisions |

| Client needs regular access or recurring outputs | Move to a retainer | Ongoing support, recurring production, or steady advisory work |

| Business impact is clear and both sides accept shared assumptions | Evaluate value-based | Work tied to a clearly measurable business outcome |

| Conditions are not clear yet | Do not force a jump | Unclear models can quietly kill margins |

Use this section's progression as a practical filter: start with hybrid when you need control, move to a retainer when work is ongoing, and use value-based only when outcomes can be clearly evidenced.

| Model | Best-fit use case | Cashflow predictability | Margin upside | Execution risk |

|---|---|---|---|---|

| Hybrid | Clear base deliverable, with likely extras or revisions | Medium | Medium to high | Medium |

| Retainer | Ongoing support, recurring production, or steady advisory work | High | Medium | Medium |

| Value-based | Work tied to a clearly measurable business outcome | Medium | High | High |

Hybrid implementation checklist:

- Keep base scope pricing and overage handling separate.

- State exactly what triggers overage work.

- Require written approval before extra work starts.

- Keep invoice visibility clean in QuickBooks by separating base fee lines from approved extra lines.

- Before sending, confirm each extra line maps to an approval date and approver name.

Retainer guardrails:

- Set service boundaries in writing.

- Set response expectations in writing.

- Set rollover policy in writing.

- Set a review cadence to confirm the retainer still matches real demand.

- Use recurring invoice or reminder options only after verifying what your QuickBooks setup currently supports.

Value-based workflow:

- Baseline the current state.

- Define the outcome metric.

- Agree on attribution logic.

- Set pricing bands tied to that shared logic.

- If a required figure is not verified yet, mark it as pending in your working notes and keep it out of the pricing logic until both sides agree on the source.

Verdict: hybrid is a controlled transition model, retainer is a stability model, and value-based is strongest when outcomes are measurable and agreed before pricing. For a deeper dive, read Value-Based Pricing: A Freelancer's Guide.

Beyond Billing: You're Not Choosing a Method, You're Designing Your Business#

You are not just picking an invoice format; you are choosing where delivery risk, margin risk, and cashflow risk will sit in your system.

Use these working definitions to make decisions quickly:

- Billable hours: you bill for recorded time, which lowers delivery-risk exposure when scope is moving, but depends on disciplined time capture and regular invoicing.

- Project fees: you bill one fixed price for a defined scope, which improves price predictability for the client but increases your exposure if scope drifts.

- Hybrid model: you set a fixed base scope and price, then bill approved extras separately to balance predictability with flexibility.

- Value-based pricing: you price around the business result, which can improve margins when scope is stable, trust is high, and outcomes are clearly tracked.

| Model | Main risk exposure | Admin burden | Cashflow pattern | Best-fit work |

|---|---|---|---|---|

| Billable hours | Time not captured or not defensible later | High | Variable unless billed on a tight cadence | Discovery work, shifting scope, clients needing detailed reporting |

| Project fees | Margin erosion from uncontained scope changes | Medium | More predictable when tied to agreed billing points | Clearly bounded deliverables |

| Hybrid | Extras handled informally instead of approved and separated | Medium to high | Usually steadier than pure hourly | Stable core scope with likely add-ons |

| Value-based pricing | Misalignment on what outcome is being priced | Medium | Deal-dependent | Trusted relationships with clear success criteria |

Before changing models, confirm your reporting can show profitability after shared costs are allocated, not just top-line revenue. QuickBooks class-based reporting is often used for that kind of checkpoint, and many teams underuse these features due to setup gaps. If you only review gross revenue, work can look healthy while true margins deteriorate.

Use this implementation checklist before rollout:

- Scope and revision limits are written in plain language.

- Change requests follow a documented approval path before billing.

- Invoice timing is pre-set (billing periods or milestones) and visible to the client.

- Retainer guardrails are explicit (what is included, what triggers refill, and what is out of scope).

- Reporting views separate revenue, direct delivery costs, and allocated overhead by class/project.

If any item is weak, stay with the lower-risk model until controls are in place. You might also find this useful: A Guide to Time Tracking Software for Billable Hours.

Frequently Asked Questions

Which is usually more profitable: billable hours or a project fee?

This grounding pack does not support a universal profitability winner between billable hours and project fees. What it does support is that timely, well-documented records reduce catch-up risk and make later performance reviews more reliable.

What is the practical difference between a fixed fee and a hybrid model?

If you use a fixed-fee or hybrid label, define in writing what is included, what is extra, and how extra approvals are documented. Confirm official QuickBooks definitions for these models in-app or with QuickBooks support. | Common scenario | Billing-model guardrail | Primary risk | Recordkeeping checkpoint before billing | |---|---|---|---| | Scope is unclear, exploratory, or likely to change fast | Do not lock in terms you cannot document yet | Unbilled or disputed work from weak notes or late entry | Confirm work is recorded when it happens, with clear dated notes | | One defined deliverable with tight boundaries | Use only if scope boundaries are written and approved | Scope creep hidden inside one price | Confirm approval records and deliverable boundaries are documented | | Clear base scope plus likely extras | Use only if extras require dated approval | Extras get buried and are hard to defend later | Confirm base work and extras are documented separately |

How do I reduce billing leakage when using QuickBooks for hourly or hybrid work?

Use documentation and timing checkpoints rather than software assumptions: record work when it happens instead of trying to catch up later, keep dated notes and approvals, and review records before invoicing. QuickBooks-specific setup and estimate-to-invoice behavior are not verified in this evidence pack, so test your exact workflow before relying on it.

What is the difference between an estimate and an invoice?

In many workflows, an estimate is used before billing and an invoice requests payment. Verify how your contract and product define each, and keep written approval records.

What documents should I keep for each billing model?

Regardless of model, keep dated documentation of what happened: scope and change records, work notes, approvals, and acceptance trail. The recurring failure mode in this evidence is weak documentation now, followed by rushed reconstruction later.

Can I trust the books to tell me whether a project fee worked?

Only if the records are classified correctly, because data entry is not the same as bookkeeping. Where income and costs are placed affects financial statements, business understanding, and taxes later. If you are using these numbers for year-end decisions, review them with a CPA or EA rather than assuming software entry is enough.

What should I watch if other people help deliver the work?

If you bring in help, worker classification matters because confusing employees and contractors can become costly later. That affects bookkeeping and taxes, not just invoicing. Verify current local rules before building those assumptions into pricing.

Is anything here legally or tax-enforceable by default?

This evidence pack does not establish legal or tax enforceability defaults for billing models, estimates, invoices, or scope documents. If you need a hard rule or threshold, treat it as unknown until verified for your jurisdiction and facts.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 4 external sources outside the trusted-domain allowlist.

- egrove.olemiss.edu/cgi/viewcontent.cgitrusted

- sandiegocounty.gov/hhsa/programs/bhs/documents/CIMHOperationsan...trusted

- slo.lafco.ca.gov/files/c0ef83009/February+2026+Full+Agenda+Pa...trusted

- snap.berkeley.edu/project/14165954trusted

- capforge.com/post/from-field-to-the-ledger-the-definitive...external

- finoptimal.com/resources/quickbooks-tips-service-businessesexternal

- getflexpoint.com/blog/msp-billing/project-based-pricingexternal

- leanlaw.co/blog/the-mid-sized-firms-guide-to-billing-co...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Value-Based Pricing for Freelancers Under Real Payment Risk

Value-based pricing works when you and the client can name the business result before kickoff and agree on how progress will be judged. If that link is weak, use a tighter model first. This is not about defending one pricing philosophy over another. It is about avoiding surprises by keeping pricing, scope, delivery, and payment aligned from day one.

A Guide to QuickBooks Self-Employed for Freelancers

**QuickBooks Self-Employed can support basic bookkeeping, but predictable cashflow comes from your payment controls, not invoicing alone.**

Choosing Time Tracking Software for Billable Hours in 2026

---