Quick Answer

Start with corridor-level modeling and optimize for what the recipient receives, not the posted wire fee. Separate domestic routes from SWIFT paths, then calculate a full stack that includes intermediary deductions, receiving-bank charges, and FX markup. Use one checkpoint before pricing decisions: compare instructed amount, debited amount, and received amount for recent payouts by currency pair. Then set routing rules so urgent cases can use wires while routine flows move to lower-variance rails such as ACH.

Why wire transfer fees add up for platforms#

If you want to reduce outbound wire costs, treat wires as a total-cost problem, not a line-item fee problem. The visible send charge is only part of what you pay. Real cost often includes intermediary bank charges, receiving-bank fees, and foreign exchange costs, including exchange-rate markup on cross-border transfers.

That distinction matters because wire transfers are still a major operating rail, not a niche edge case. Stripe notes that more than 200 million wire transfers were sent in the US in 2024, up 9% from the previous year. Wires can move money faster than ACH, but that speed often comes with higher fees, especially once a payment leaves a domestic route and moves through SWIFT or other third-party institutions.

For platform teams, the practical mistake is usually not that you picked an expensive provider. It is that you modeled only the send fee and missed the deductions. On international payouts, third-party costs are commonly applied on SWIFT transfers, and the recipient can receive less than expected even when your own platform fee table looks acceptable. On domestic wires, fees are generally lower and more predictable than international wires, which is why you should separate those routes in your analysis instead of blending them into one average.

A useful early checkpoint is simple: compare the amount you instructed, the amount debited, and the amount the recipient actually received for a sample of recent payouts by corridor and currency. If those three numbers do not reconcile cleanly, you do not yet have a real wire-cost baseline. That gap is often where hidden margin loss sits.

Recipient-side fees can also affect landed value. The Wise guide summary describes incoming domestic and incoming international wire fees as usually around USD 15 where charged. That is not a universal number, but it is a reminder that recipient-side costs can affect your payout experience and support burden.

So the goal of this guide is narrow and practical: help finance, ops, and engineering teams reduce total outbound wire cost without damaging payout reliability. Pricing and eligibility vary by provider and route. Use the next sections as an operating method: map routes, model landed cost, set routing rules, and verify what recipients actually get before you optimize for price.

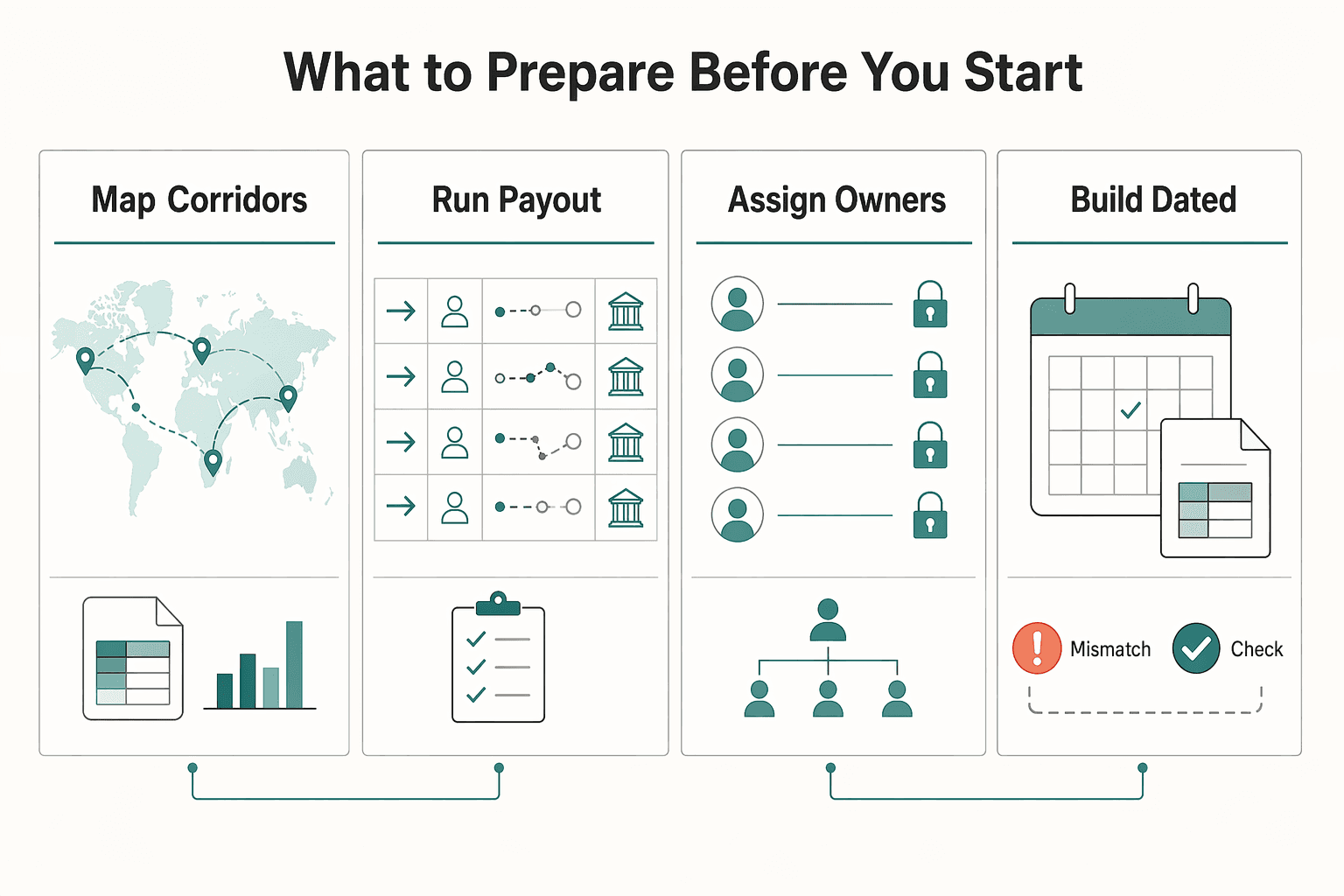

What to prepare before you start#

Before you compare providers, build a prep pack that separates routes, assigns control owners, and ties every pricing assumption to current terms.

| Prep item | Key details | Checkpoint |

|---|---|---|

| Map corridors and volumes by rail | Split domestic and international flows; track country pair, send currency, receive currency, and monthly volume; keep ACH and CHIPS separate from SWIFT corridors | For each top route, state payout count, value, currency path, and rail in use today |

| Run a payout-data quality pass | Collect the beneficiary and bank fields current routes and providers require; test a recent sample for missing or mismatched details | Data quality issues are visible before pricing comparisons |

| Assign owners by decision type | Finance owns pricing inputs and landed-cost assumptions; Ops owns routing policy and exception handling; Engineering owns integration controls, including Webhooks and Ledger journals | Payout events are traceable and reconcilable |

| Build a dated record of provider terms | Save the exact pricing and disclosure pages used in the model; Wise says pricing is usage-based, fees vary by currency, it uses the live mid-market rate, and discounts can apply above 25,000 USD monthly equivalent | Each model assumption maps to a current source |

- Map corridors and volumes by rail. Split domestic and international flows before you model costs, and track each route by country pair, send currency, receive currency, and monthly volume. Keep domestic rails (for example,

ACHandCHIPS) separate fromSWIFTcorridors so you are not averaging unlike paths.

Checkpoint: for each top route, you can state payout count, value, currency path, and rail in use today. Red flag: one blended "average wire cost" across domestic and cross-border routes.

- Run a payout-data quality pass. Collect the beneficiary and bank fields your current routes and providers require, then test a recent sample for missing or mismatched details.

Checkpoint: data quality issues are visible before you start pricing comparisons. Failure mode: avoidable exceptions can erase modeled fee gains.

-

Assign owners by decision type. Finance owns pricing inputs and landed-cost assumptions. Ops owns routing policy and exception handling. Engineering owns integration controls, including

WebhooksandLedger journals, so payout events are traceable and reconcilable. -

Build a dated record of provider terms. Save the exact pricing and disclosure pages for each provider you evaluate. For example, Wise states pricing is usage-based, fees vary by currency, it uses the live mid-market rate, and discounts can apply above 25,000 USD monthly equivalent.

Checkpoint: each model assumption maps to a current source, not memory.

Build a true landed-cost baseline for each payout corridor#

Do not approve a route change until each corridor has two views: the expected landed amount and the worst-case landed amount the recipient may receive. Headline send fees are only one part of total cost.

Step 1. Build the full cost stack#

Model each payout type separately, especially on SWIFT corridors where costs may be split across multiple institutions.

| Cost layer | What to capture | Why it matters |

|---|---|---|

| Wire send fee | The provider or bank's quoted outbound wire fee | This is the visible charge teams usually anchor on first |

| Intermediary bank fees | Deductions between sender and recipient | These can reduce delivered amount even when sender fees look acceptable |

| Receiving bank fee | Charges taken by the beneficiary bank on receipt | Recipient shortfalls still hit your support team |

| Exchange rate markup | The spread between the market FX rate and the provider's offered rate | FX margin often costs more than the visible transfer fee |

| Wire transfer reversal fee | Charges when a wire is recalled or reversed | Less frequent, but material enough to model |

Do not collapse this into one "international wire cost" line. For each corridor, capture send currency, receive currency, rail, and where conversion happens when you can verify it. Visible fees get attention, but bigger drivers can sit elsewhere: even a 1-3% FX markup can add hundreds of dollars on larger transfers. If a provider promotes low or zero fees, check the FX rate basis at the same timestamp before treating the route as cheaper.

Step 2. Separate fixed charges from route variance#

On SWIFT routes, separate fixed charges from variance created by correspondent hops and FX-conversion behavior. The correspondent banking network has long been the default architecture for cross-border movement, but route conditions are shifting: one cited view reports active correspondent relationships declined 22 to 29% (2011-2020) while cross-border payment volume grew 61% in the same period.

Treat correspondent deductions and FX behavior as a range, not a constant. If your corridor model assumes deductions repeat exactly every month, your baseline is too optimistic.

Step 3. Add exception costs before route comparison#

A corridor can look cheap on send fees and still be expensive in operations. Add explicit exception costs for investigation effort, delayed recipient support, and manual reconciliation when payout events do not match Ledger journals.

Use actual handling effort from your team where possible. The red flag is a route that lowers send fees while support, tracing, and reconciliation work rises.

If you want a deeper dive, read Same-Day ACH for Platforms: How to Speed Up Contractor Payments Without Wire Transfer Fees.

Set route rules for when to use wires and when not to#

Turn corridor analysis into a fixed policy: use wires when timing sensitivity or payment certainty justifies higher cost, and default to non-wire rails when it does not.

Step 1. Define routing buckets#

Set clear buckets for each corridor so teams are not re-deciding rail choice case by case.

| Bucket | Use when | Notes |

|---|---|---|

| Wire bucket | Time-sensitive or large transactions where same-day settlement and high certainty matter more than fee efficiency | Reserve for cases where a delay or miss would cost more than the wire itself |

| Default bucket | Routine non-wire rail for predictable payouts when urgency is lower and delivery pattern is stable | Use as the routine path when a wire is not justified |

| Corridor alternative bucket | Use a corridor-specific path only when payout evidence shows lower landed-amount variance or fewer avoidable exceptions | Use only when your own payout evidence supports it |

Wires are typically irrevocable once completed, so reserve this bucket for cases where a delay or miss would cost more than the wire itself.

Step 2. Require hard release checks#

Before any routing rule or override goes live, require the same checks every time:

- Destination country and complete receiving-bank details

- Whether FX conversion is required and where it occurs in the payment flow

- Expected intermediary-path uncertainty for wire payouts

- Recent return and repair patterns from

Payout batches

If you cannot replay recent payouts and explain why each would route the same way under the new rule, do not automate it yet.

Step 3. Keep a narrow treasury exception#

Allow explicit exceptions for treasury-style payments where timing risk is materially worse than higher wire cost. Require a short evidence pack: business reason, deadline, approver, beneficiary confirmation, and provider reference after send.

Review exception use monthly. If wire usage is rising because of weak payout data quality or process discipline, fix that root cause instead of broadening wire usage.

For a step-by-step walkthrough, see How to Send an FFC Wire Transfer With Fewer Errors.

Design payout operations that keep costs down at scale#

Once routing rules are set, cost control comes from operating discipline. If bad beneficiary data, ambiguous retries, or unreconciled provider events reach production, outbound costs usually rise with volume even when listed wire fees do not.

| Control area | What to do | Why it matters |

|---|---|---|

| Batch release validation | Check provider- and rail-required bank identifiers for each corridor, including IBAN, BIC, and ABA routing number where relevant, plus currency and destination-country fit; show pass/fail counts and row-level reason codes in the batch preview | Issues are fixed before money moves |

| Retry and state handling | Keep a stable internal payout ID, persist an idempotency key across retry attempts, and use Webhooks to update payout state over time | Retries stay controlled and payout state remains traceable |

| Event reconciliation | Map each payout event to both a ledger journal entry and the provider reference across status changes, returns, reversals, and provider-exposed fee or deduction events | Timing gaps and deductions stay explainable |

| Funding-path mapping | Record incoming funding currency, stored balance currency, payout currency, and the exact conversion point | Avoidable conversion loops become visible early |

Step 1. Validate bank details before each batch release#

Use Payout batches as a release gate. Before submission, check the bank identifiers your provider and rail require for each corridor, including IBAN, BIC, and ABA routing number where relevant, plus currency and destination-country fit.

Cross-border payment models can differ in cost, speed, accessibility, and compliance overhead, so data that passes on one route may still fail on another. Your batch preview should show pass/fail counts and row-level reason codes so issues are fixed before money moves. If urgent payouts bypass pre-flight checks, repair work usually shifts downstream where it is slower and more expensive.

Step 2. Make retries idempotent and drive state from Webhooks#

At scale, manual processes do not keep up. Treat retries as a controlled flow: keep a stable internal payout ID, persist an idempotency key across retry attempts, and use Webhooks to update payout state over time.

Keep the checkpoint simple: pick a payout that retried and confirm, from event history, whether one provider-side payout was created or not. Webhooks improve visibility, but they do not replace a clear state model.

Step 3. Reconcile each event to Ledger journals and provider references#

Reconciliation is what keeps timing gaps and deductions explainable. Map each payout event to both a ledger journal entry and the provider reference used by finance, ops, and support.

Do this for the full lifecycle, not only the initial send: status changes, returns, reversals, and any provider-exposed fee or deduction events. For validation, sample a recent payout and trace it from batch row to provider reference to final ledger journal without side spreadsheets.

Step 4. Map the funding path, not just the payout path#

Document where cash sits and where conversion happens before payout. For inbound funding and prefunding, map how Virtual Accounts and Multi-currency accounts affect FX hops by corridor rather than assuming one setup is always cheaper.

For each remittance corridor, record:

- incoming funding currency

- stored balance currency

- payout currency

- exact conversion point (if conversion occurs)

This makes avoidable conversion loops visible early. If funds are converted into a treasury currency and then converted back before payout, that extra hop can add cost before the wire is even sent.

Get these controls right and you reduce preventable exceptions, which are often the most expensive part of outbound wire operations. Related reading: How to Conduct a Functional Analysis for Transfer Pricing.

Add compliance and tax gates without breaking payout speed#

Run compliance and tax checks in the same release path as routing: hold payouts when status is incomplete, auto-release when status is complete, and use human review only for risk flags.

Step 1. Sequence identity and screening checks before route selection#

Check KYC/KYB first, confirm AML screening second, and evaluate rail or corridor eligibility last. This keeps you from pricing or routing payouts that are not actually release-ready.

Make the checkpoint visible in each payout record: identity status, latest screening result, and the approval or escalation timestamp/case reference. If a batch can be released without those fields, you are creating avoidable exceptions and manual retry risk.

Step 2. Tie tax document readiness to payout logic#

If your policy requires tax documentation or tax validation, make that a payout-release condition, not a cleanup step. Your logic should confirm the required document state for that payee and entity (for example W-8, W-9, Form 1099 support data, or VAT validation) before submission.

Store a usable evidence set: document type, version, collection date, validation result, and linked payee/legal entity. In Payout batches, operators should see tax-ready or tax-hold with a reason code before release.

Step 3. Track FEIE and FBAR artifacts when your program enables them#

For cross-border contractor programs, treat FEIE/FBAR items as policy artifacts, not ticket notes. FEIE may apply only if IRS requirements are met, including foreign earned income and a foreign tax home; for the physical presence test, the threshold is 330 full days in a 12-month period, and those days do not have to be consecutive. Even when income is excluded, it still must be reported on a U.S. tax return.

Track what the contractor submitted or acknowledged, when they did it, and which policy version they saw. For FBAR-related workflows, keep the FinCEN due-date or notice reference your program relied on, including event-specific extension notices when applicable. Keep release decisions tied to document completeness and risk status, not a self-checked claim.

Negotiate and configure provider pricing with proof, not assumptions#

Lead with corridor-level proof, not a blanket discount request. Take route evidence to Wise, Chase, or your bank, and negotiate send fee and FX treatment separately, then judge the offer by landed outcome after intermediary and receiving-bank deductions.

Step 1. Bring a corridor evidence pack#

Build your case by country and currency pair, then split by rail and operating pattern where cost behavior changes. For each route, include payout count, typical amount bands, single vs Payout batches, online vs ops-channel initiation, sending legal entity, and the actual landed amount observed. If a provider only sees gross volume, you are likely to get generic pricing instead of route-specific terms.

Step 2. Ask for terms that match your real operating mix#

Run the commercial discussion in three tracks: send-fee pricing, FX pricing, and eligibility conditions. Confirm whether online initiation, batch/file submission, and multi-entity sending all qualify for the quoted terms. A strong headline price is not useful if most of your actual traffic falls outside the eligibility rules.

Step 3. Validate the quote against your landed-cost baseline#

Re-run the provider quote through the same baseline model you already trust. The pass/fail test is whether total landed cost and delivered amount improve, not whether one visible fee line drops. Compare old vs new assumptions in one view: expected landed amount, worst-case landed amount, and corridor-specific exception or shortfall patterns.

Step 4. Re-run comparisons on a fixed cadence#

Reprice on a fixed rhythm (quarterly is practical) and treat terms as perishable. Cross-border payments have been a G20 priority since 2020, with multiple improvement paths under active development rather than one permanent best route. Keep the same evidence pack and re-check whether last quarter's cheapest route is still cheapest after real deductions and delivery outcomes.

Common failure modes and how to recover without cost blowups#

The lowest-cost recovery is usually to pause new Payout batches, verify instructions from the source, and only retry after you can explain what failed.

Step 1. Separate a payment discrepancy from a retry decision#

If the delivered result is different from what you expected, do not auto-resend. First confirm what was sent, what was received, and how the provider currently classifies the payment so you are not compounding an unresolved exception.

Step 2. Re-check instructions against the source document#

Use the provider's International wire instruction requirements page and validate the exact country entry, not a copied template. Reconfirm both Overall instructions and Purpose of payment codes before you attempt a fix, because partial edits can leave required fields out of sync.

Step 3. Treat missing evidence as a hold, not a guess#

If supporting sources are unavailable (for example, a gateway timeout), hold retries until you can re-validate the required instructions. A short pause is usually cheaper than a second failed attempt and additional exception handling.

For a deeper look at tracking delayed wires, read How to Use a SWIFT MT103 to Trace a Delayed Wire Transfer.

Your next 30 days checklist for lower outbound wire costs#

You can reduce outbound wire cost variance in 30 days without a major rebuild by tightening routing discipline, execution controls, and provider terms.

Step 1. Build corridor baselines from actual payout history#

Start with recent outbound payout history and group it by corridor, currency, and route type. For each group, track sent amount, delivered amount, visible provider fee, and landed shortfalls linked to exchange rate markup, intermediary deductions, or receiving-bank charges.

Do not rely on a single average. Define an expected landed amount plus a worst-case variance band per corridor, and validate it with payment traces and support evidence, since hidden FX markups can cut the amount received even when send fees look acceptable.

Step 2. Publish routing rules that people and code can follow#

Turn those baselines into clear route rules by scenario. Use wires when urgency or value justifies the cost; use lower-variance options when predictability matters more than speed.

Make the rule visible in payout orchestration so every payout shows route, reason code, approval state, and final provider reference. This prevents undocumented overrides that later make cost and outcome reviews hard to explain.

Step 3. Add pre-flight checks before money leaves#

Block release when required beneficiary details are incomplete or malformed. Wiring instructions require recipient bank account and routing information, so pre-flight validation should happen before execution, not during repair.

Then tie release and closure to control evidence: provider events via Webhooks and matching accounting outcomes in Ledger journals. Treat retries as exceptions until internal status, provider reference, webhook event, and ledger entry reconcile.

Step 4. Negotiate once using your own evidence, then re-test#

Run one negotiation cycle with your highest-volume providers using your corridor data, not generic discount requests. Separate send-fee treatment from FX treatment, then re-test landed outcomes after repricing.

Because faster options may carry higher charges, judge offers on total landed cost, not the visible fee line alone.

Step 5. Start a monthly review and keep adjusting#

Set a monthly review across finance, ops, and engineering to monitor fee drift, shortfall variance, return patterns, webhook gaps, and route-level manual effort. If a corridor keeps producing unexplained deductions, tighten the rule or re-price before the next payout cycle.

That recurring loop is what keeps outbound wire costs down over time. Related: Decoding International Wire Transfers: Why You're Losing Money.

Frequently Asked Questions

What fees actually make outbound wires expensive for platforms beyond the visible send fee?

The visible send fee is only one line in the stack. Total cost can also include intermediary bank fees, receiving bank fees, exchange rate markup, and other third-party costs that often appear on international transfers sent through SWIFT. If you want a real operating view of wire cost, model landed amount by corridor instead of comparing headline send fees.

Why does the recipient sometimes get less than the sender expected on international wires?

Shortfalls usually come from a mix of hidden fees and FX markups, not one single deduction. On a SWIFT route, intermediary or correspondent banks may take fees for routing or currency handling, and the receiving bank may also apply its own charge. Your check is simple: compare sent amount, delivered amount, and any fee notes on the payment trace before you assume the provider underpaid.

When should a platform still use wire transfers instead of ACH or regional rails?

Use a wire when payout timing matters more than fee minimization, especially for urgent payouts. Compared with ACH, wires can start moving faster, but the fees are usually higher, so they are a poor default for routine low-urgency payouts. If payout timing is flexible and predictability matters most, ACH is usually the better first route to test.

How do intermediary and correspondent banks change payout predictability?

Each extra bank in the path can add fees or currency-conversion charges you do not control. That is why two payouts that look identical at initiation can land with different net amounts across corridors. If a corridor is noisy, treat the payment trace as evidence, then update that corridor’s expected and worst-case landed amount before the next batch. For a deeper explanation, see Correspondent Banking Explained.

What is the speed-versus-cost tradeoff between SWIFT, Fedwire, CHIPS, and ACH?

Do not assume a fixed ranking that holds across every provider, cutoff, and corridor. The grounded rule is narrower: wires can start moving faster than ACH, but they often cost more, while international routes can also carry third-party deductions. In practice, your decision should turn on corridor history and whether a SWIFT payment is likely to pick up intermediary charges.

How can we reduce wire costs without increasing payout failures or compliance risk?

Start with corridor-level measurement, not headline fee comparisons. Track the full stack for each route: initiation, intermediary, receiving, and FX-related costs, then compare sent and delivered amounts to see where deductions recur. For international SWIFT routes, plan for possible third-party charges upfront and route volume toward options with more predictable landed amounts.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- docs.fcc.gov/public/attachments/DOC-418284A1.pdftrusted

- downloads.regulations.gov/BSC-FFM-2026-0001-0001/attachment_17.pdftrusted

- federalregister.gov/documents/2026/03/24/2026-05727/reforming-le...trusted

- fincen.gov/report-foreign-bank-and-financial-accountstrusted

- irs.gov/individuals/international-taxpayers/figuring...trusted

- irs.gov/individuals/international-taxpayers/foreign-...trusted

- miamidade.gov/resources/management/documents/redevelopment...trusted

- occ.gov/publications-and-resources/publications/comp...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Same-Day ACH for Platforms: How to Speed Up Contractor Payments Without Wire Transfer Fees

---

Why Your International Wire Arrives Late and Costs More

When a client says they paid but your money arrives late, lands short, or is hard to trace, that is a cash-flow risk, not a minor inconvenience. If the amount and timing are uncertain, planning your next moves gets harder.

Why International Wire Transfers Arrive Short and How to Reduce Fee Leakage

Most money lost on cross-border payments does not disappear in one obvious charge. It leaks out in small deductions at different points along the route. The client may pay an outgoing fee at their bank. One or more correspondent banks may take a cut as the payment moves across SWIFT. Your own bank may charge to receive it. If a currency conversion happens anywhere along the way, that can add more drag. By the time the funds land, the amount credited can be lower than the amount invoiced even when the client is sure they paid in full.