Quick Answer

You lose money on international wire transfers because fees can be deducted at several points: the sender's bank, intermediary banks on the SWIFT route, your receiving bank, and any currency conversion. Reduce losses by agreeing on currency and fee responsibility before invoicing, using exact routing details, collecting the sender's confirmation, and reconciling the landed amount on posting day.

Why international wire fees quietly drain your invoice#

Most money lost on cross-border payments does not disappear in one obvious charge. It leaks out in small deductions at different points along the route. The client may pay an outgoing fee at their bank. One or more correspondent banks may take a cut as the payment moves across SWIFT. Your own bank may charge to receive it. If a currency conversion happens anywhere along the way, that can add more drag. By the time the funds land, the amount credited can be lower than the amount invoiced even when the client is sure they paid in full.

A few terms are worth keeping straight. SWIFT is the banking network many institutions use to route cross-border wires. Intermediary bank fees are deductions taken by correspondent banks that relay funds between the sender and your bank. Currency conversion fees can apply when money is sent or received in a different currency. None of this is unusual on its own. The problem is treating those costs as someone else's issue until the short credit shows up on your statement.

The practical fix is to inspect the payment path before money moves, not after. Ask the client for the transfer confirmation and note any correspondent details shown there. Confirm your own bank's policy for incoming international wires and how any fee appears when the credit posts. Agree on currency before you issue the invoice, because once the sender chooses a different currency or route, you usually lose control over the final net amount. Then reconcile the landed amount the day it posts, while both sides still have the transfer details in front of them.

Treat this as a sequence with clear owners. Before the due date, you send final receiving details and payment terms. On send day, the client shares the transfer confirmation and reference. On posting day, you match what was sent to what landed and flag any shortfall immediately. It sounds basic, but it prevents the usual failure where everyone assumes someone else has the record.

Keep the evidence as you go. Save the sender's confirmation, the payment reference, and your bank's credit advice. Those are the documents that let you trace a shortfall instead of arguing from memory.

A common failure mode is assuming the sender's fee, or a "free wire" promotion, covers the whole trip. It usually does not. Deductions can still happen in transit, so your invoice terms should say plainly that fees may be taken before receipt and that a lower net credit does not settle the balance. If clients regularly pay you in another currency, compare the net result across channels and decide whether a multi-currency setup would reduce avoidable conversion costs. For background, see How to Get Paid in Multiple Currencies Without Losing Your Shirt.

Map the cost path from client to your account#

The fastest way to lose control of a wire is to treat it as one fee. Before the client sends anything, map the payment across four cost points: the outgoing fee at the sender's bank, route deductions taken in transit, the incoming fee at your bank, and any FX markup. That map does two useful things. It shows which costs are under someone's control, and it shows where you will need proof if the amount that lands comes in short.

Because a wire is generally hard to unwind once the receiving bank accepts it, the right time to ask questions is before the send and again on the day the payment posts.

| Component | Who controls it | What to check |

|---|---|---|

| Outgoing fee (sender bank) | Client and their bank | Ask the client to confirm the posted fee and whether cross-border pricing differs from domestic. |

| Route deductions (intermediaries) | Route dependent | Deductions may occur as funds move between banks. If the confirmation shows correspondents, note them. |

| Incoming fee (your bank) | You and your bank | Get your bank's written policy for receiving international credits and how any fee appears when the wire posts. |

| FX conversion or markup | Provider policy | Agree on currency before the transfer and compare the expected net to the invoice total. |

That is the planning view. In practice, the operating rule is simpler: collect proof, match it quickly, and escalate early if the numbers do not line up.

Use these checkpoints every time:

- Ask the client to share the confirmation details, including amount, currency, and any listed correspondents if shown.

- Confirm whether your bank charges to receive international wires and how that line item appears on your statement or credit advice.

- Align on currency before invoicing and confirm whether the sender will initiate in your account currency.

- Reconcile the landed amount the day it posts and raise any gap immediately while the transfer details are still easy to find.

A simple timeline keeps those checkpoints from drifting:

- Before send: confirm channel, currency, and who covers each fee category.

- Send day: collect the confirmation, payment reference, and any route details shown by the sender's bank.

- Posting day: compare sent versus received amounts and classify the gap as inbound fee, known deduction, or unexplained difference.

- If unresolved: ask the sender to open a trace with their bank right away and share the case details so both sides work from the same reference.

In practice, two problems show up over and over. The first is assuming the sender's wire fee covers the full route. It does not stop deductions later in the chain. The second is noticing the short credit only at month end. By then, the person who approved the payment may have moved on, the bank receipt is harder to retrieve, and tracing takes longer than it should.

A cleaner approach is to write down who pays which charges, state how short credits are handled, and save both sides of the record: the client's confirmation and your own credit advice. That gives you a before-and-after picture you can actually use.

Once you know where a payment can leak value, the next lever is the channel the client uses to send it.

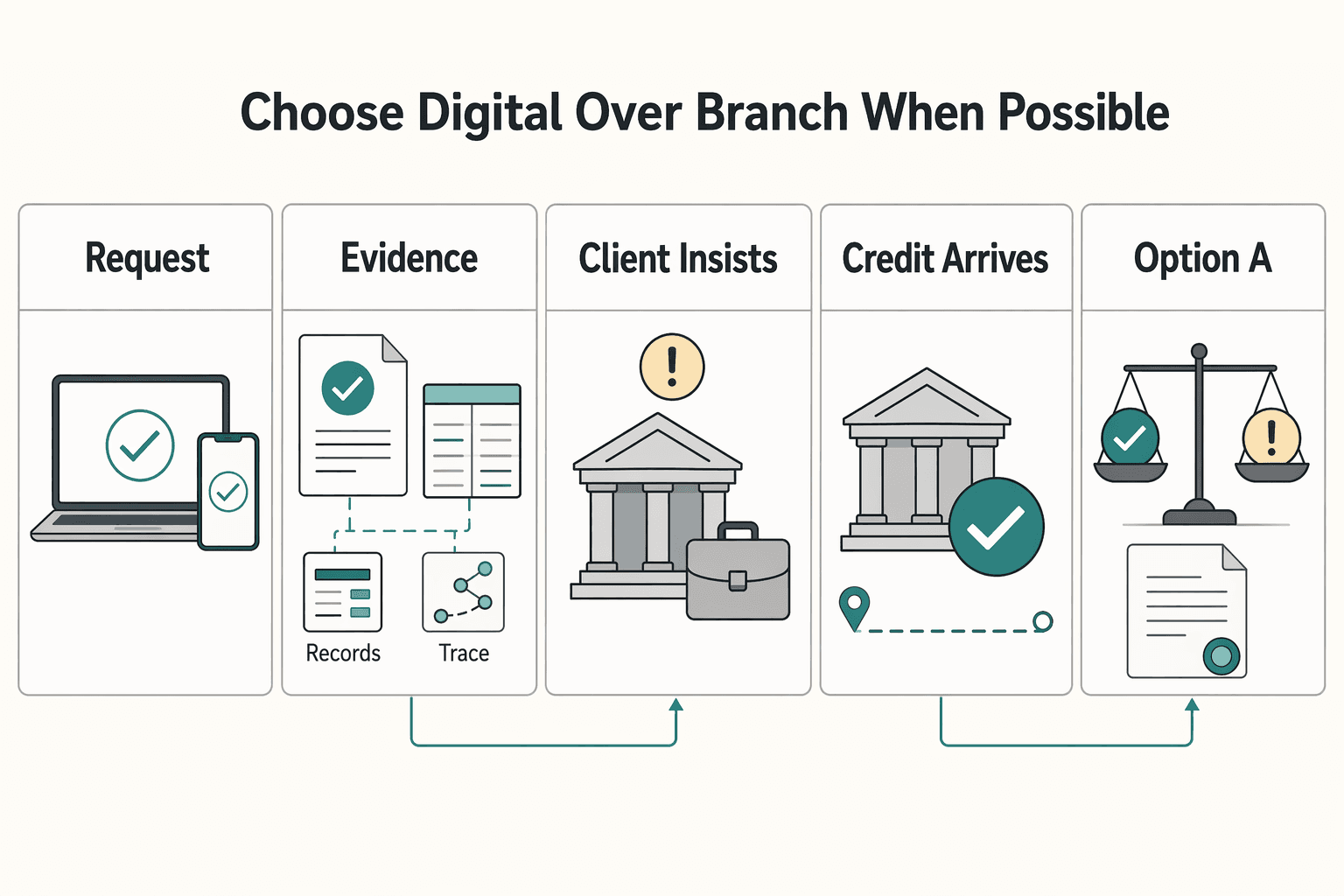

Choose digital over branch when possible#

If the client has a choice, ask them to use the bank's online channel instead of going to a branch. The digital path usually creates cleaner records and, at some banks, can cost less. Wells Fargo, for example, has listed lower pricing for some online wires than for branch-initiated wires. Even so, do not assume that pattern holds everywhere. Have the client confirm the current schedule for the specific account and channel they will actually use.

This is not just about convenience. It gives you better control. A digital confirmation is easier to save, easier to read, and easier to match against the payment that lands. If something goes wrong, you want a receipt that clearly shows the amount, currency, date, and reference, not a branch interaction that leaves you with little more than "we sent it."

Make that preference explicit in your process:

- Put the request on the invoice, for example: "Please initiate via your bank's online portal."

- Ask for the submission confirmation and keep it with the invoice record.

- If the client insists on branch initiation, decide in advance who covers any representative-assisted fee.

- When the credit arrives, compare it against the confirmation while the details are still easy to retrieve.

If branch initiation is unavoidable, keep the same evidence standard. Ask for a receipt or confirmation that still shows amount, currency, date, and transfer reference. If the client only sends a payment note without those fields, request the full confirmation before marking anything as in progress. You are not being difficult. You are preserving the minimum data needed to reconcile and trace.

The common failure mode here is habit. A client walks into a branch because that is how they have always done wires, pays a higher fee, and assumes it is just part of the deal. Another is relying on a verbal update instead of a real confirmation. Neither gives you much to work with if the amount is short or the transfer stalls.

A one-line note on the invoice and a reminder when you send receiving details usually solve this. You are not trying to manage the client's banking routine. You are steering the payment toward the option that gives both sides a better paper trail and, sometimes, a lower total cost.

Channel choice helps, but it does not answer the next question: what will your own bank do when the funds arrive?

Control what you pay to receive#

Inbound fees are the easiest part of the route for you to verify directly, so confirm those first. Some banks charge to accept incoming international transfers, often up to 25 USD, and correspondent banks can still deduct fees before the money reaches you. If you do not plan for both, the first notice you get is a smaller credit than you expected.

Start with your own bank. Ask for the written policy on incoming international wires and confirm how any charge appears. Some banks deduct it from the credit itself. Others show it as a separate line item. That detail matters when you reconcile, because a short receipt can come from more than one source.

Once you know your bank's rule, decide who covers inbound costs and state that plainly on the invoice. Keep the policy on file. If the posted amount does not line up with what you were told, you need something firmer than "someone at the bank mentioned it."

A simple reconciliation note helps your team stay consistent. Log the sender-confirmed amount, the amount credited, and any inbound fee that your bank labels clearly. If a gap remains after those known items, treat it as a route deduction until traced. That keeps your follow-up precise and avoids mixing policy questions with transit deductions.

A few checks prevent most surprises:

- Call or message your bank to confirm whether it charges to receive international wires.

- Note the exact label that will appear on your statement or credit advice.

- Align with the client on currency before invoicing and confirm what they will actually select when they initiate the transfer.

- Request the incoming wire credit advice once the funds post and file it with the invoice and statement.

- Ask the sender for their transfer confirmation and compare the amount sent with the amount credited on the day it arrives.

Two failure patterns recur. First, people assume there is no inbound fee because they have never noticed one before. Then a deduction appears, the invoice gets marked paid, and nobody can tell whether the shortfall came from the sender, an intermediary, or the receiving bank. Second, route deductions get ignored because they are not always quoted upfront. That is why your invoice should say that fees may be deducted before receipt and that an underpayment does not clear the balance.

Currency choice matters more than it looks. Receiving in your account currency can make reconciliation simpler. Receiving in a different currency may shift conversion or handling costs to one side or the other. The right move is not always the same, but the process is consistent: choose the currency with the client, put it on the invoice, and compare the net you expected with the net you actually received. If multi-currency payments are becoming routine, see How to Get Paid in Multiple Currencies Without Losing Your Shirt for the setup tradeoffs.

Once your own receiving costs are clear, the hardest variable left is what happens in the middle of the route.

Cut intermediary charges on SWIFT routes#

You usually cannot remove intermediary banks from a SWIFT payment, but you can avoid creating extra friction for them. The strongest lever is not a special bank product. It is clean routing details, exact instructions, and a clear request for the most direct supported path.

| Instruction item | Include | Condition |

|---|---|---|

| Account details | Account name as on file; account number or IBAN | Exactly as your bank provides them |

| Bank identifiers | Receiving bank name; SWIFT or BIC | Exactly as listed by your bank |

| Correspondent details | Preferred correspondent details | If available for that corridor |

| Currency and reference | Currency to send; invoice number | For the payment reference |

| Route request | Most direct correspondent path | Use the shortest supported route for that currency |

That matters because route charges are often the least visible part of the wire. The client may only see what their own bank charged. You may only see the final short credit. Everything in between can feel opaque unless you tighten the instructions before the payment is sent.

Set expectations early. Add a line to your invoice terms stating that fees may be deducted in transit and that a lower net receipt does not settle the balance. That language will not prevent every deduction, but it will head off the predictable dispute that follows one.

Then send the client complete receiving instructions exactly as your bank provides them:

- Account name as on file and your account number or IBAN

- Receiving bank name and SWIFT or BIC exactly as listed by your bank

- Any preferred correspondent details your bank provides for that corridor, if available

- The currency to send and the invoice number for the payment reference

- A request that their bank use the most direct correspondent path it supports

Precision matters here more than style. Ask the client to enter the details into their bank portal exactly as provided and to request the shortest supported route for that currency. If an IBAN or SWIFT code is mistyped, the payment can be delayed, returned, or reprocessed. Every extra touch adds time and raises the chances of another deduction.

Use a copy-ready instruction block instead of retyping details in each email. Keep one approved version per receiving account, then paste it into invoices and payment reminders without editing core fields. Small typing changes are a common source of avoidable delays, and delays often create extra handling steps you did not need.

Once the payment is in motion, your job is verification. Collect the sender's confirmation, including the transfer reference, so you can investigate quickly if the credit is short or late. On posting day, compare the amount sent with the amount received and file your bank's credit advice with the invoice. If timing slips, remember that settlement depends on the corridor, currency, and intermediaries involved. Escalate early with both sides while the transfer trail is still easy to trace.

This is one of those areas where small administrative mistakes create expensive noise. Most of the time, the fix is not exotic. It is exact bank details, a direct route where possible, and fast follow-up when the landing amount does not match what was sent.

If a corridor keeps producing messy deductions or weak FX, that is the point where comparing the bank route with a specialist provider becomes worthwhile.

Decide when to use a money transfer provider#

A provider is worth comparing when fee and FX transparency matter more than raw speed, and when the agreement does not require a bank wire. That is the real tradeoff. If you need a more predictable landed amount and can live with the provider's delivery timeframe, test the option instead of defaulting to a traditional wire.

Wise is a clear example. It says it uses the live mid-market rate and charges an upfront fee that varies by currency, starting from 0.48%. That structure makes comparison easier because you can see the exchange-rate basis and the transfer fee without trying to back into a hidden spread from the final amount.

Still, this is not a blanket recommendation. Treat it as a corridor-by-corridor decision. For smaller or mid-sized invoices, where fixed bank charges and FX spread can take a noticeable bite, a provider may preserve more of the payment. For very large tickets, contract-driven payments, or situations where a bank route is required, the wire may still be the right tool.

Use a provider when these signals line up:

- You can accept the delivery timeframe and do not need same-day posting.

- The quote uses a mid-market rate and an upfront fee with no hidden FX markup, as Wise describes.

- The client is willing and able to use the provider and can include your invoice reference.

- A direct comparison shows the expected landed amount beats the bank route after fees and FX.

Watch for scale effects too. Wise lists volume discounts starting from 35,000 CAD, and its sending fee varies by currency. If you have repeat payments in the same corridor, that can lower unit costs over time. It does not mean the provider always wins. It means larger, repeat flows deserve a fresh comparison instead of a default assumption.

To keep the comparison honest, capture two live quotes within the same hour: the provider's all-in estimate and the bank's wire cost and rate. Check recipient name formatting and any required ID fields so a preventable delivery failure does not distort the result. Then save the provider receipt and your bank's credit advice and reconcile the final amount on posting day.

For repeat corridors, keep a simple comparison log with the same fields each time: transfer amount, fee structure, rate basis, expected net, and actual net received. Consistent fields matter more than fancy formatting. They help you see whether one route is reliably cleaner or whether results swing based on timing and channel.

If a provider wins on both net amount and acceptable timing, document the route and reuse it next time. If not, you still learned something useful about that corridor. For a broader comparison of non-wire options before you standardize, see Stripe vs. PayPal vs. Wise: The 2026 Battle for Best Freelancer Payments. The practical rule is simple: get two real quotes, compare what actually lands, and pick the channel that preserves more without creating timing or compliance problems for the payment.

Whichever channel wins, it only works cleanly if your paperwork tells the client what to use and how the payment will be judged.

Align contract and invoice terms to prevent losses#

Most fee disputes start as documentation problems, not bank problems. If the contract and invoice do not say who covers fees, what currency to use, which channel is acceptable, and what proof is required, you leave the most expensive parts of the payment to assumption.

| Term | Example language | What it sets |

|---|---|---|

| Fee responsibility | Sender covers outgoing fees and any intermediary deductions. Short credits do not settle the balance. | Who covers outgoing, intermediary, and receiving charges |

| Currency and channel | Pay in U.S. dollars via online wire or Pay via Wise if agreed. | The currency and, if relevant, the approved channel |

| Proof and reference | Include the invoice number and provide the transfer confirmation with the SWIFT reference. Recipient will file the bank credit advice with the invoice. | The evidence standard |

| Receipt standard | Payment considered received when the net amount credited equals the invoiced total. | When the net amount credited matches the amount due |

The fix is straightforward. Put the rules in writing before the invoice is due, and repeat the important ones on the invoice itself. At minimum, spell out who covers outgoing, intermediary, and receiving charges. Specify the currency and, if relevant, the approved channel. Make clear that a short-credited payment does not settle the balance.

Be specific enough that the client's finance team can act without a follow-up email. If both parties agree, write "Pay in U.S. dollars via online wire" or name a provider such as Wise when that channel is acceptable. That kind of instruction lowers the odds of a sender choosing the wrong currency, triggering an avoidable conversion, or paying through a channel that creates weaker records.

Useful language to place in the invoice footer or contract payment section includes:

- "Sender covers outgoing fees and any intermediary deductions. Short credits do not settle the balance."

- "Pay in U.S. dollars via online wire" or "Pay via Wise" if agreed.

- "Include the invoice number and provide the transfer confirmation with the SWIFT reference. Recipient will file the bank credit advice with the invoice."

- "Payment considered received when the net amount credited equals the invoiced total."

Those lines do more than make the document sound formal. They create an evidence standard. Ask the client for their confirmation and SWIFT reference, then save your receiving bank's credit advice on posting day. With those items in the file, you can match what was sent with what arrived and raise a shortfall immediately instead of chasing details weeks later.

It also helps to set an internal handoff rule: the person issuing invoices uses the same approved payment language every time, and the person reconciling receipts checks against that language before marking paid. The moment those two steps drift apart, fee disputes return. Keep one approved template and update it only when your bank details or accepted channels actually change.

Several failure modes are worth calling out because they are so common. Ambiguous fee language leads to back-and-forth the moment an intermediary takes a deduction. Missing currency direction can trigger a sender-side conversion with an avoidable markup. No SWIFT reference or invoice number slows reconciliation and can hide small shortfalls until month end. And naming a provider in your template without confirming the client's ability to use it can delay payment for reasons that have nothing to do with price.

Where supported, consider Virtual Accounts or Merchant of Record with Gruv if dedicated receiving details would simplify reconciliation across clients and corridors. The key is to confirm coverage and acceptance before you build those details into templates. Better tools help, but only if the counterparties can actually use them.

Contracts can also define when funds must arrive before work or shipment proceeds. Some businesses require full wire receipt before release. If cash-before-delivery matters in your model, state it clearly. The pattern does not change: assign fee responsibility, specify currency and channel, require proof, and only mark the invoice paid when the net amount credited matches the amount due.

Once those terms are settled, the day-to-day process should be simple and repeatable.

A short, repeatable checklist for every client payment#

At this point, the goal is boring, repeatable execution. SWIFT carries payment messages, not the funds themselves, so the control you actually have comes from precise instructions before the send and quick reconciliation right after the credit posts.

Use this checklist for every payment:

- Before sending an invoice: confirm the client's channel, whether online or branch, and ask what sender-side fee pattern they expect. Share your receiving bank's incoming wire policy. Agree on the payment currency so nobody triggers an unplanned conversion.

- On the invoice: state the currency, specify who pays which fees, and note that short credits do not settle the balance. Ask the sender to include the invoice number in the payment reference.

- After the transfer: collect the sender's confirmation with the SWIFT reference and reconcile the landed amount on the day it posts. If the net is short, including because of intermediary deductions, escalate promptly. File your bank's credit advice with the invoice.

- For future payments: document which corridor and channel produced the cleanest result and store the artifacts centrally, or with Gruv Payouts where enabled, so the next payment follows the better path.

Keep a minimum document pack for each payment file:

- Invoice with final payment terms and currency.

- Sender confirmation showing amount, date, currency, and transfer reference.

- Receiving-side credit advice and statement line item.

- Internal reconciliation note showing sent amount, credited amount, and disposition of any shortfall.

Two quick checks save the most time. First, compare the amount sent with the amount credited on posting day, not at month end. Second, keep the SWIFT reference with the invoice and the credit advice. That reference is your anchor if timing slips or the final amount is lower than expected.

The red flags are consistent: no net-of-fees language, vague currency instructions, and confirmations that do not include the SWIFT reference or invoice number. Catch those early and the rest of the process gets much easier.

If you want a deeper dive before you standardize your setup, read The Best Multi-Currency Accounts for Digital Nomads and Freelancers.

Keep more of each payment without surprises#

Most avoidable losses on cross-border payments come from weak setup, not bad luck. If you set expectations before the transfer and verify the result on posting day, surprises drop fast. That is the thread through every section above: choose a channel that creates clear records, state who covers which fees, lock the currency before the invoice goes out, and save proof on both sides.

You do not need a complicated control process to do this well. You need basic discipline: clear policies, simple internal checks, and a working understanding of how a wire moves over networks such as SWIFT and, when relevant, CHIPS. Ask the sender to include the invoice number and share the confirmation. Keep your own credit advice. Compare what was sent with what landed as soon as the payment posts, not weeks later.

That timing matters more than it seems. A short credit is easier to investigate when the sender still has the receipt handy, the bank can identify the route quickly, and nobody is reconstructing the payment from month-end records. Waiting turns a simple trace into a messy argument. If a payment stalls, use How to Use a SWIFT MT103 to Trace a Delayed Wire Transfer while the trail is still fresh.

If you do this consistently, the result is predictable: fewer payment disputes, faster reconciliation, and less revenue leakage from small deductions no one tracked. You get there by treating each wire as an auditable process, not a one-line bank event.

Make it repeatable#

Use a simple standing routine and stick to it:

- Terms: state who covers outgoing, intermediary, and receiving charges, and specify the currency and preferred channel.

- Invoice: include net-of-fees language, your bank details, and the invoice number for the payment reference.

- Posting-day check: reconcile the credited amount against the amount sent, attach the credit advice, and file the SWIFT reference.

- Exceptions: open a case the same day if a shortfall appears and ask the sender for route details.

- Review: record corridor outcomes and adjust your instructions if a path regularly produces deductions or delays.

If your volume is growing or you need cleaner records, dedicated receiving details and centralized storage can help. Where supported, explore Gruv Virtual Accounts and Payouts, and confirm coverage before you depend on them. The principle stays the same no matter what tools you use: map the route, collect proof at each step, and act quickly when the final credit does not match the invoice. For FX tradeoffs tied to currency choice, see How to Get Paid in Multiple Currencies Without Losing Your Shirt.

Frequently Asked Questions

How much do international wire transfers typically cost?

There is no single typical cost because different fees can be applied along the payment path. The sender may pay an outgoing fee, intermediary banks may deduct fees in transit, your bank may charge an incoming fee, and FX can add more cost. Estimate the full path, not just the sender's posted fee.

Do I pay for incoming international wires at my bank?

Yes, you may pay for incoming international wires, depending on your bank and account. Ask your bank for its written incoming wire policy and confirm whether the fee appears as a deduction from the credit or as a separate line item. Even if your bank does not charge one, the payment can still arrive short because of route deductions.

What are intermediary bank fees and why do they happen?

Intermediary bank fees are deductions taken by banks that relay the payment between the sender's bank and your bank. They happen because many cross-border wires move through correspondent banks instead of going directly from one bank to another. You may only notice them when the credited amount is lower than the amount sent.

Is it cheaper to initiate a wire online instead of in a branch?

Sometimes, but not always. Pricing depends on the bank and account, but online initiation usually creates cleaner confirmation records and may cost less than a branch visit. If the client has a choice, ask them to confirm the current fee schedule for the channel they will actually use.

What does Wells Fargo charge for international wires today?

The best answer is to verify the current fee schedule for the specific account and channel being used. Wells Fargo has listed lower pricing for some online wires than for branch-initiated wires, but the article notes not to assume that pattern holds everywhere. Ask the client to confirm the posted fee on their receipt and attach it to the invoice record.

When should I consider using a provider like Wise instead of a bank wire?

Consider a provider like Wise when FX transparency and total landed amount matter more than raw speed, and your agreement does not require a bank wire. Wise says it uses the mid-market rate and charges an upfront fee that varies by currency, starting from 0.48%, so it can be easier to compare with a traditional wire. The right test is a live comparison between the provider and the bank route in the same hour.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

- eur-lex.europa.eu/legal-content/NL/TXT/PDFtrusted

- occ.gov/publications-and-resources/publications/comp...trusted

- wise.com/us/blog/international-wire-transfer-feestrusted

- papayaglobal.com/blog/understanding-intermediary-bank-fees-fo...external

- papayaglobal.com/blog/how-to-avoid-the-hidden-fees-for-intern...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Stripe vs PayPal vs Wise for Freelancers in 2026

Cashflow reliability matters more than brand familiarity. If money arrives later than expected, gets reduced by fees, or loses value during conversion, margin disappears even when the client technically paid on time.

How to Get Paid in Multiple Currencies Without Forced FX

If you want to **get paid in multiple currencies** while protecting margin, separate collection from conversion. Receive the client's currency first, then decide if, when, and where to convert it.

The Best Multi-Currency Accounts for Digital Nomads and Freelancers

This shortlist is for cash flow decisions, not brand popularity. It is for freelancers, creators, and lean teams in the United States who need a cross-border payment setup that still works when real work hits: invoices go out, money lands, conversions happen on your timing, and urgent payouts do not depend on luck.