Quick Answer

Yes. If you run services through a company in one country while you work from another, create a functional analysis transfer pricing file before relying on your compensation setup. Document Functions, Assets, and Risks, and connect that record to your agreement, invoices, and real conduct. For U.S.-linked filings, keep the packet ready when the return is filed because the IRS can request it within 30 days.

As a global professional running your own business, you already know how to deliver valuable work across borders. The harder part is often quieter: figuring out whether your international tax position will hold up if anyone ever asks questions.

That is where a functional analysis comes in. For a business of one, it is not a dense corporate exercise. It is the documented story of the value you create, who creates it, what assets are used, and who really bears the risks. In practical terms, it is the file that helps show why the way your company pays you is fair, supportable, and consistent with transfer pricing rules.

This is not compliance for its own sake. It is about being able to explain your structure clearly, with facts that line up from agreement to invoice to actual conduct.

First, Does This Even Apply to You?#

Use this screen first. For this guide, it likely applies when all three are true for your setup: you and your company are related parties, there is a transaction between you, and the arrangement is cross-border.

Confirm there are actually two parties#

Start here: are there actually two parties? If you operate through a separate legal entity, the answer is often yes. The practical question is whether you act both as an individual and through a distinct company or business. This guide starts from situations with "two or more organizations, trades, or businesses," not one person billing directly.

Plain-English definition: related parties are parties under common ownership or control by the same interests. In a business-of-one setup, that can mean you control the company.

Verification check: gather incorporation documents, shareholder register or cap table, director records, and anything else that shows ownership or control. If control is unclear, treat that as an early professional-review flag.

Confirm there is a real transaction#

Next, confirm there is a real transaction between you and the company. A controlled transaction is any transaction or transfer between members of the same controlled group. In practice, this often includes services you perform for your own company where the company pays or compensates you.

| Verification record | Example from the section |

|---|---|

| Service agreement | service agreement between you and the company |

| Payment or compensation record | payroll records, management fees, contractor invoices, or director compensation records |

| Client contract | client contracts held by the company while you personally deliver the work |

Do not write this off as "internal" just because it is your company. If the company is legally separate, service payments can still be controlled transactions.

Verification check: look for one or more of the records above.

Related-party status alone does not prove your pricing is non-arm's-length. It means the pricing needs support.

Check the cross-border element#

Then check the cross-border element. This guide is focused on related-party cross-border transactions. Ask whether you and the company are in different countries for the arrangement. A common pattern is a company formed in one country while you live or are tax resident in another and perform services there.

If both sides are in the same country, or your facts change during the year, you may still need advice, but this specific cross-border screen may be less relevant.

| Likely applies | Likely does not apply |

|---|---|

| You own or control a company in one country, and it pays you for services you personally perform from another country. | You freelance directly in your own name with no separate company. |

| Your company signs client contracts, and you personally deliver the work across borders. | You have a separate company, but no payment, service arrangement, or other transaction between you and it. |

| You and the company are related parties, and there is a service fee, salary, contractor payment, or management charge between you. | You cannot clearly confirm common control, the contracting party, or where services are performed; treat this as a professional review checkpoint. |

If you are mostly in the left column, move to FAR documentation next: functions performed, assets used, and risks borne. If your facts are mixed or unclear, treat that as a professional review checkpoint before relying on a pricing position.

For a step-by-step walkthrough, see Section 351 Transfer Planning for a Clean Incorporation.

The "Why": Understanding the Core Principle#

When your own company pays you, the core rule is simple: the amount should match what unrelated parties would agree to for the same work. That is the arm's length principle. In your setup, you as the individual service provider and your company as the legal entity sit on opposite sides of a controlled transaction. Your pricing needs evidence, not just preference.

Define the two parties clearly#

Before you price anything, state the parties in plain language. One party is you personally performing the services. The other is your company paying for those services. Because the payment is between related parties, it is a controlled transaction.

Verification point: if you cannot clearly state who performs the key functions, which assets are used, and who assumes the material risks, your pricing position is not ready.

Use arm's-length logic, not owner logic#

The question is not whether payment happened. The question is whether the amount is defensible.

| Question | Owner-set logic | Arm's-length logic |

|---|---|---|

| Why this amount? | "I picked it" or "I needed this draw." | "It reflects what an independent party would pay for these services." |

| What supports it? | Internal preference, cash needs, tax outcome. | Functional analysis and transaction facts: roles, assets used, risks assumed, and pricing support. |

| What does your file show? | Mostly payment records. | A documented economic explanation for the compensation. |

Connect FAR to compensation and method choice#

Your Functions, Assets, and Risks (FAR) show where value is created. That analysis supports appropriate compensation and helps you choose a method that fits the facts, such as CUP, resale price, or cost-plus. No single method fits every case.

If you claim meaningful market, operational, or credit risk, your file should show real evidence of that risk. Keep detailed transfer pricing support, with the functional analysis as a core document. If your company is in the UAE, Article 34 specifically emphasizes using functional analysis to determine arm's-length price.

That is the logic layer. The next step is turning it into a file you can actually use. If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

The "How": Documenting Your Value in 3 Steps#

Start with a dated FAR memo before or as the transaction begins, then update it whenever functions, assets, or risks change. This is part of defining the controlled transaction, not optional narrative.

The strongest file shows how the business works in practice. Contracts matter, but your documentation also needs to show who performs the functions, whose assets are used, and who assumes and controls risks.

Before you start#

Open one document and record four facts: who you are, who the company is, what service you personally provide, and when the arrangement started. Add effective dates for any major change, for example client ownership, billing flow, country move, or key IP usage. If you are in the U.S., documentation should exist when the return is filed, and the IRS can request it within 30 days.

Write and rank your functions#

Start with the functions that matter most economically, then rank the ones that drive profit most.

Use two buckets:

- Strategic/core functions, the work clients are paying for

- Supportive/admin functions, important operations but generally not core profit drivers

Use these prompts in your memo:

- "I personally perform these core functions:"

- "The company performs or arranges these support functions:"

- "The functions that contribute most to profit are:"

Attach proof for each major function:

- Work outputs: deliverables, technical designs, presentations, final client work

- Decision ownership: scope, pricing, solution, hiring, client-strategy decisions

- Client-facing responsibility: proposals, meeting notes, SOWs, call summaries

Verification check: someone unfamiliar with your business should be able to identify quickly which functions drive revenue and who actually performed them.

Map the assets actually used#

Do not stop at legal ownership. Document the assets that create commercial value in the transaction, especially intangibles, and show how they are actually used by the company in winning and delivering work.

| Asset type | Owned by you | Used by company | Why it affects compensation |

|---|---|---|---|

| Personal brand and reputation | Can be | Can be, when the company sells on that reputation | May support client acquisition and pricing power |

| Specialized expertise | Can be | Can be, when services depend on that expertise | Can explain non-generic value |

| Methodology, templates, code, or content | Could be you or company | Yes, if used in delivery | Can affect margin, speed, and differentiation |

| Client relationships and network | Can begin as personal | Can be, if the company contracts and bills those clients | Can affect pipeline quality and revenue stability |

Checkpoint: add one evidence line for each asset, for example portfolio items, licensing terms, repeat methodology use, or client-introduction records.

Test risks against conduct and capacity#

This is where weak files often break down. For each claimed risk, document exposure and control, plus who has financial capacity to bear it.

| Risk | What to show | Records to include |

|---|---|---|

| Market risk | who drives pipeline and pricing decisions | proposal history, negotiation records, and pipeline notes |

| Credit risk | who bears late or non-payment outcomes | contracts, invoices, aging records, reminders, write-off records |

| Operational/professional liability risk | who controls delivery decisions and consequences | SOWs, change requests, acceptance criteria, issue logs |

| Financial risk | who chose invoice currency, who received funds, and who absorbed exchange movement | invoice terms, bank records, and decision records |

- Market risk: show who drives pipeline and pricing decisions. Include proposal history, negotiation records, and pipeline notes. Note mitigations like diversification, retainers, or tighter payment terms.

- Credit risk: show who bears late or non-payment outcomes. Include contracts, invoices, aging records, reminders, write-off records. Note mitigations like deposits or milestone billing.

- Operational/professional liability risk: show who controls delivery decisions and consequences. Include SOWs, change requests, acceptance criteria, issue logs. Note mitigations like scope controls and documented approvals.

- Financial risk (for example, currency exposure): show who chose invoice currency, who received funds, and who absorbed exchange movement. Include invoice terms, bank records, and decision records.

Red flag: a contract assigns risk to one party, but the conduct and cash impact show the other party actually controls or bears it.

Packet checklist before method selection#

Before choosing a pricing method, confirm your FAR packet includes (and add jurisdiction-specific requirements as needed):

| Packet item | Details |

|---|---|

| Dated transaction summary | parties, service, start date, key changes |

| Ranked functions memo | with evidence |

| Asset table | owned, used, and commercial relevance |

| Risk section | tying each risk to control, financial capacity, proof, and mitigation |

| Agreements, invoices, and charge calculations | match real operations |

If any item is missing, fix the file first. This FAR work is what makes comparable selection and pricing support more defensible later.

Related: How to Use a 'Cost-Plus' Model for Transfer Pricing.

Before you finalize your FAR file, sanity-check your country timeline so your transfer-pricing narrative and residency facts stay aligned with your records: Tax Residency Tracker.

The Stakes: Real-World Risks of Negligence#

When the file is weak, you usually lose control of the story first. That is the real operational risk here. Audits are expected to rise globally, and disputes are expensive and time consuming once they start.

Spot the operational risk early#

A thin FAR memo does not guarantee a bad outcome. It does make it harder to answer quickly, keep scope narrow, and defend why your structure and payments reflect how the business actually works.

| Risk area | Early warning signal you can recognize | What goes wrong without documentation | What improves with a defensible functional analysis |

|---|---|---|---|

| Your entity or payment structure gets challenged | Questions on how functions, assets, and risks are actually allocated across parties | You end up arguing from memory, and inconsistent records can widen the review. | You can show who performed key functions, which assets were used, and who controlled and could bear risk. That gives reviewers a coherent fact pattern early. |

| A limited inquiry turns into a disruptive audit | Information requests keep expanding across agreements, work records, and pricing support | You spend time rebuilding history and explaining inconsistencies. Even a reasonable position becomes harder to defend. | A dated FAR memo, aligned agreements, and supporting records let you answer in one structured packet instead of scattered replies. That aligns with pre-audit prevention. |

| Relief between countries gets harder | Signs that two jurisdictions may treat the same income differently | Relief can become longer and more complex. MAP requests are rising, and more than half are transfer pricing cases. | A clear factual record helps your advisor frame MAP if needed. Transfer pricing MAP cases average 35 months, versus 18.5 months for other cases. |

| Operational burden increases across the business | More management time is pulled into dispute response and record reconstruction | Time and focus get diverted from delivery to defense. The issue stops being "tax only." | Consistent documentation reduces avoidable friction and helps teams respond faster. |

Verification point: if a third party can review your FAR memo, intercompany agreement, and invoice support, and get the same story from all three, your position is stronger.

Escalate at the right moment#

Some issues are still document fixes. Others need specialist help.

Handle yourself now when the issue is still factual and document-driven:

- Update the FAR memo to reflect current functions, assets, and risks.

- Align agreement language with actual conduct and payment flow.

- Assemble evidence of who performs key functions and who controls risk.

- Date and log material changes (ownership, billing flow, service scope).

Engage a tax advisor now when any of these appear:

- The issue becomes cross-border and starts involving transfer pricing or competent-authority channels.

- Two jurisdictions appear to take different views of the same payment.

- The matter moves from document collection toward adjustment, settlement, or litigation.

- A jurisdiction-specific filing, penalty, or controversy trigger may apply and needs local-law verification.

Timing matters. Pre-audit prevention can be less burdensome than arguing during audit. As disputes mature, settlement opportunities during audit, MAP, and in some cases APA may become relevant. An APA may prevent litigation, but it is not a blanket fix. If a case reaches litigation, resolution may take over a decade.

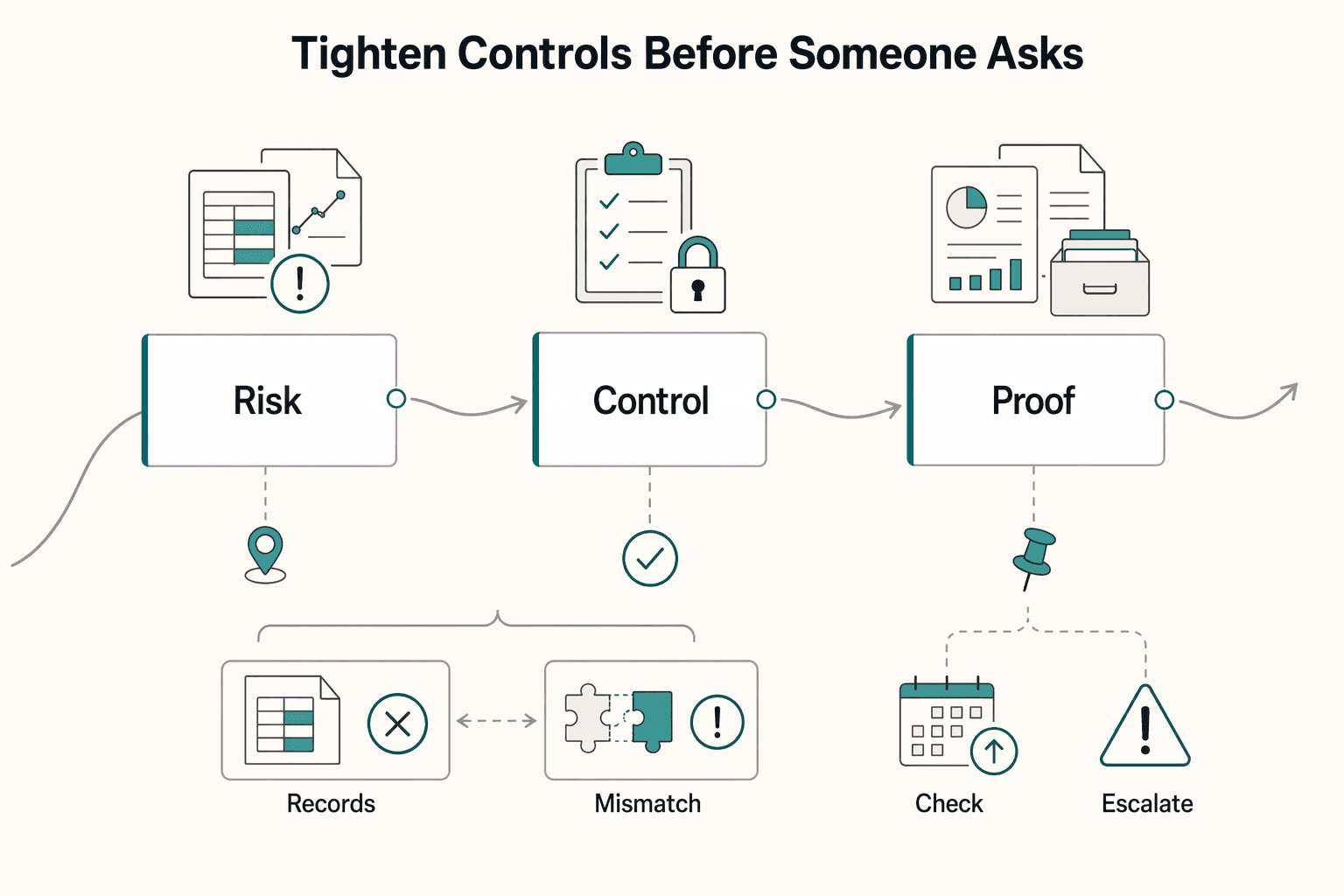

Tighten controls before someone asks#

Before an inquiry starts, get the internal record into shape:

- Confirm your FAR documentation is dated, current, and evidence-backed.

- Confirm the intercompany agreement matches real conduct, payment flow, and risk control.

- Reconcile invoices, charge calculations, and bank records to the agreement.

- Keep an audit-ready folder with agreements, work outputs, decision records, and change logs.

- Flag cross-border friction early so you can choose in-house handling or advisor escalation before scope expands.

If you do one thing after this section, make the file internally consistent. Problems get more expensive when the business facts are plausible but the records are not.

You might also find this useful: A Deep Dive into the 'Associated Enterprises' Article in Tax Treaties.

Conclusion: Your Analysis is Your Shield and Your Story#

A good file acts as both shield and explanation. It protects your position when your compensation story holds up against the arm's-length test: would independent parties reach similar results in similar circumstances.

Your analysis should explain why your agreement and actual conduct produce an arm's-length result, not just why the contract reads well on paper. Keep this closing checklist current so your agreement, evidence, and pay rationale stay aligned:

- Updated intercompany agreement that matches how the work is actually performed

- Evidence files for your assumptions (for example: contracts, invoices, deliverables, decision records, payment records)

- Current pay-method rationale that fits the facts and explains your method choice, since no single method is required

If those three items conflict, your position is easier to challenge and transfer pricing adjustments become more likely.

Escalate to a transfer pricing or cross-border tax advisor when facts change across entities or jurisdictions, or when a new service line or structure changes who earns income.

Use this analysis as a living document. Review and refresh it when your business model, services, or entity setup changes.

We covered this in detail in A Guide to 'Comparables Analysis' for Business Valuation.

If you want a cleaner operating setup for cross-border client work with clearer invoicing and payout visibility, review Gruv for Freelancers.

Frequently Asked Questions

Does transfer pricing apply to a one-person company?

Short answer: it can, when a related-party cross-border transaction exists between separate legal parties. What matters is not headcount but whether there is a related-party cross-border transaction. Next action: document the parties, jurisdictions, and transaction flow before deciding the issue is too small to matter.

What matters most for your setup?

Short answer: clear cross-border related-party facts matter most. OECD-style guidance applies the arm’s length principle to related-party cross-border pricing, while country rules can differ in thresholds and format. Next action: map your legal relationship and jurisdictions, then confirm local documentation expectations.

What is a simple functional analysis example for a consultant?

Short answer: describe your real Functions, Assets, and Risks, then tie them to reward. Arm’s-length reward is tested against who does the work, uses assets, and bears risk. Next action: write a dated FAR summary based on your actual delivery model, not job-title language.

What evidence should you retain for each FAR element?

Short answer: keep records that prove each FAR statement. Documentation supports audit risk assessment and helps your file hold up under review. Next action: retain contracts, work outputs, decision records, pricing support, and records showing who controlled risk and absorbed outcomes.

How do you pay yourself from your own foreign company compliantly?

Short answer: use a real agreement plus pricing support, not contract text alone. Arm’s-length support depends on agreement terms, method rationale, and supporting records. Next action: align your agreement, FAR, invoices, and payment records so they tell one consistent story.

What are the risks of getting transfer pricing wrong for a small business?

Short answer: the main risk is a weak file that makes adjustments and penalties easier to pursue. Article 9.1-style analysis tests whether related-party conditions differ from independent-party conditions. Next action: keep contemporaneous documentation and escalate early if an inquiry starts widening.

What is the arm’s length principle for a freelancer?

Short answer: your result should be consistent with what unrelated parties would achieve in comparable circumstances. That is the core standard used across transfer pricing frameworks. Next action: document why your fee reflects your FAR profile and method assumptions, rather than relying on a rough estimate.

Do I need complex software for this?

Short answer: usually no, a coherent, maintainable file is what matters. Authorities test documentation quality and usability, not whether it sits in a specific tool, and U.S. requests can require production within 30 days. Next action: keep one audit-ready packet and get help early for multi-jurisdiction or hard-to-benchmark pricing cases. If needed, review transfer pricing guidance for small international businesses.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- ecfr.gov/current/title-26/chapter-I/subchapter-A/part...trusted

- ecfr.gov/current/title-26/chapter-I/subchapter-A/part...trusted

- govinfo.gov/content/pkg/CHRG-113shrg89523/html/CHRG-113s...trusted

- irs.gov/businesses/international-businesses/transfer...trusted

- irs.gov/pub/fatca/int_practice_units/iso_c_01_02.pdftrusted

- law.cornell.edu/uscode/text/26/482trusted

- law.cornell.edu/definitions/index.phptrusted

- legalinstruments.oecd.org/en/instruments/87trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Transfer Pricing for Small International Businesses with Related Entities

For a business of one operating across related entities, transfer pricing is mostly about execution. Document each related-party charge when it happens, choose the most reliable method you can actually support, and have the file ready before you file your return. If you wait until year-end, the evidence can be harder to rebuild and your method support can be easier to challenge.

How to Use a 'Cost-Plus' Model for Transfer Pricing

Before you use this playbook, note the evidence limit for this section: the grounding available here does not establish technical rules for cost-base construction, arm’s-length legal tests, comparables screening, defensible markup ranges, or jurisdiction-specific thresholds. Treat the steps below as an internal execution checklist, and escalate technical transfer-pricing positions to a qualified advisor.