Quick Answer

Treat AI automation and instant settlement as workflow improvements, not blanket guarantees. Launch only the automation and faster-payment features you can support with current rail eligibility, exception handling, and verifiable performance evidence.

How AI Automation and Instant Settlement Change Contractor Payments#

Treat instant settlement as a market-by-market operating outcome, not a feature badge. This explainer is for founders and operators deciding where contractor payment automation can deliver immediate, final funds availability, and where it still means only faster initiation, approval, or messaging.

That distinction matters because mistakes create drag quickly. If you expand before you have payment compliance, payment visibility, and clear controls, you can increase failed or delayed payouts and investigation workload across finance, ops, and support.

Vendor language often compresses very different outcomes into one promise. Some rails define true finality with final and irrevocable settlement, and FedNow guidance requires participating institutions to make recipient funds available immediately on a 24x7x365 basis. That is not the same as a product that only speeds up internal processing. If you do not separate those clocks, you risk building product and GTM plans around a claim that does not hold once contractors expect cash to be available.

Cross-border conditions make this harder. The Financial Stability Board highlights persistent frictions in cross-border payments: high costs, low speed, limited access, and insufficient transparency. So the real question is not whether you can automate payments, but where your rails, compliance setup, and status visibility support a credible instant or near-instant promise.

This article keeps the terms precise: instant settlement, payment visibility, and payment compliance. It compares domestic and cross-border rollout options in practical terms and gives you launch checkpoints, including:

Keep forward-looking payment claims grounded in the Federal Reserve's FedNow overview and FedNow FAQ, and apply the FTC's advertising substantiation policy before you promise automation or settlement outcomes.

- whether rail-level finality terms are published

- whether you receive usable status events instead of generic in-progress states

- who owns exception handling when payouts stall or fail

One compliance point is non-negotiable for covered U.S. payment activity: AML controls are required. The rule at 31 CFR § 1022.210 requires an effective anti-money laundering program, and the operating principle is simple. Payment speed does not remove compliance duties.

The goal is practical. You should be able to choose first markets and an operating model that hold up under real payout conditions, so your launch promise matches what contractors actually experience. For a fuller breakdown, read Freelance Crypto Payments That Protect Cashflow and Reduce Disputes.

Start with precise definitions that teams often blur#

Set the definition early: instant settlement means immediate funds availability with near-real-time interbank settlement and clear finality, not just faster internal workflow steps. The Federal Reserve separates instant payments from broader faster payments, including Same Day ACH, so a “faster digital payment workflow” may only mean quicker initiation, invoice processing, or approvals.

Keep two clocks separate:

- Operations clock: invoice intake, approval chains, compliance review, payout creation.

- Settlement clock: starts at rail submission and ends at confirmed completion on that rail.

To verify claims, ask which rail is used and which document defines finality. FedNow states settlement through the service is final, and RTP states settlement is final and irrevocable. ACH remains scheduled. It processes for 23 1/4 hours every business day and settles four times daily, so it is not continuous real-time settlement. Also watch for funds shown as available before interbank settlement is complete. That is different from rail-level finality.

If your use case is cross-border and contractor trust is fragile, consider prioritizing transparent status alongside speed. Real-time tracking tied to a UETR or transaction ID gives teams and contractors a concrete in-flight view, while vague “processing” states can still drive support demand.

Be explicit about uncertainty. Vendor speed claims are often high-level and may not include rail-level SLAs for true finality. If a provider says “instant to same-day,” require corridor-level detail, rail mapping, funds-availability definitions, and exception-state evidence. Otherwise, treat the claim as faster initiation, not instant settlement.

Compare markets before you commit product and GTM resources#

Choose launch markets based on operational reliability, not headline speed claims. Start where rail access is clear, compliance ownership is clear, and exception handling is predictable. Those conditions are usually easier to verify for domestic payouts. For cross-border contractor payments, they are usually harder because multiple jurisdictions, providers, and supervision models are involved.

Compare programs on rollout risk, not market hype#

Use the table below for sequencing, not market-size ranking. The “expected exception volume” column is a directional operator estimate based on rail clarity, jurisdictional variation, and likely manual-review pressure, not a published country dataset.

| Market / program | Payout method availability | Compliance burden | Expected exception volume | Feasibility of near-instant settlement |

|---|---|---|---|---|

| U.S. domestic via FedNow Service | Near real-time interbank capability is available through participating institutions; FedNow went live on July 20, 2023 | Medium to high if your model involves transferring funds as a business, which can trigger MSB and money transmitter analysis; state-level treatment still needs review, including alignment with MTMA harmonization efforts | Low to medium when coverage and account controls are strong; higher when participation coverage or account checks are weak | High for supported domestic cases; not evidence of cross-border instant settlement |

| UK domestic via Faster Payment System | Real-time payments supported, with payments up to £1m; the rail processed 5.09 billion transactions and £4.2 trillion in 2024 | Medium; domestic setup is generally clearer than multi-jurisdiction payouts, but partner model and compliance allocation still need to be explicit | Low to medium for domestic contractor payouts when beneficiary details are clean | High for supported domestic payouts |

| SEPA Instant within Europe | Instant credit transfer capability exists, with funds available within seconds, but availability is not uniform across all SEPA jurisdictions | Medium; the EU Instant Payments Regulation entered into force on 8 April 2024, with a first compliance date of 9 January 2025, but country and institution readiness still must be checked | Medium because reach is uneven by jurisdiction and participant bank | Medium to high, but only where both institutions support the service |

| Cross-border corridors outside one domestic rail footprint | Availability varies by corridor, provider, receiving market, and local payout method | High; jurisdictions take varying approaches to supervising bank and non-bank PSPs | High, because cross-border payments involve two or more jurisdictions and global progress has not yet translated into tangible end-user improvements | Low to medium, and corridor-specific rather than globally consistent |

In practice, sequencing can be straightforward: a domestic rail with broad support is often easier to operate than a cross-border corridor with hidden review steps, uneven receiving coverage, or unclear compliance ownership.

Domestic vs cross-border operations#

Cross-border payments are more complex than domestic payments. In practice, that can mean more reconciliation work, more status ambiguity, and more manual intervention.

| Payment model | Operational complexity | Reconciliation load | Dependency on manual approvals |

|---|---|---|---|

| Domestic contractor payouts | Lower; rail behavior and compliance expectations are usually narrower and easier to document | Lower to medium; fewer entities and timing gaps can make reconciliation simpler | Lower in many setups, especially when onboarding and payout controls are completed before payout creation |

| Cross-border contractor payments | Higher; coordination across jurisdictions, institutions, and local payout methods | Higher; more timing breaks, status mismatches, fees, and corridor-specific exceptions can appear | Higher in many setups, because compliance reviews, beneficiary checks, and routing exceptions may need human intervention |

If you need one rule, use this one: launch where your exception path is boring. Fast happy-path payouts are not enough. Unsupported banks, compliance holds, or missing beneficiary data must also be easy to detect and resolve.

Verify these artifacts before you pick a market#

Before you commit a market, get the evidence that tells you how the flow actually behaves.

- Rail mapping by market and payout type. Get the specific rail used, not a broad “real-time” or “same-day” claim.

- Funds-availability definition and exception states. Confirm what completion means and which states exist between initiation and final credit.

- Compliance ownership by business model. In the U.S., transferring funds as a business can be MSB activity, so ownership between you and partners must be explicit.

Two failure modes to watch for. One is choosing a market for rail modernity while underestimating coverage and compliance fragmentation. SEPA Instant is a good example: regulatory requirements are evolving, but availability is still uneven across jurisdictions. The other is treating roadmap momentum as current capability. Most G20 cross-border targets are set for end-2027, and global progress has not yet produced consistent end-user improvements.

Recommendation: launch first where compliance requirements are clear and exception handling is mature, then expand into harder cross-border corridors after your status handling, reconciliation, and manual-approval flows prove reliable in production. This pairs well with our guide on The Pros and Cons of Accepting Cryptocurrency Payments.

Choose your operating model before choosing tools#

Choose the operating model first, because it determines who owns compliance checks, exceptions, and payment visibility when payouts stall. The core decision is who controls routing and who owns exception handling.

Three models and what changes operationally#

| Model | What it gives you | What you control | Payment visibility and risk |

|---|---|---|---|

| API-led orchestration | One layer across multiple providers, with routing by attributes like country, currency, or amount | High control over provider selection, retries, and how statuses are normalized | Visibility can be strong, but you own more exception handling when routes fail or constraints change |

| Provider-led managed flows | Provider-managed operations, with some programs absorbing parts of tax, fraud, disputes, and support | Less direct control and lower day-to-day operational ownership | Visibility is bounded by the provider’s events, reporting model, and program scope |

| Hybrid modular rollout | Start narrow, then add modules or control where pain appears | Medium control with a narrower initial scope | Visibility can fragment if modules expose different states, approval rules, or reconciliation outputs |

If you need policy control such as attribute-based routing and automatic retries to another processor, API-led orchestration has explicit support for that. The tradeoff is that you own more implementation and exception handling. Provider-led flows can reduce build burden and can include provider-led verification before payout in some platform models, but with less direct control over routing behavior.

Map Gruv modules to the job you actually need done#

Gruv’s public model is modular. Start with Virtual Accounts, Payouts, or MoR, then expand.

- Virtual Accounts: best when inbound attribution is the first bottleneck. They provide dedicated receiving details for bank transfers, and Gruv positions them for virtual IBANs and local account details in 30+ currencies where supported.

- Payouts: best when compliance-gated disbursement and release controls are the core need. Gruv Mass Payouts messaging includes smart validation and approval workflows.

- MoR: best when your commercial setup requires a Merchant of Record. That is a legal and finance decision, not only a tooling choice.

What to verify before you sign anything#

Before you sign, ask for operator-level artifacts rather than high-level product claims.

- Status taxonomy and event payloads: confirm all states between initiation and completion, and whether they are exposed consistently.

- Verification and hold evidence: confirm what you receive when payouts are held, rejected, or sent to review.

- Route constraints by bank or corridor: confirm transfer-priority and amount-limit constraints, since “supported” does not mean every payout size or urgency is feasible.

If you need fast multi-market pilots, start modular: inbound attribution first, compliance-gated payouts second, deeper orchestration only where routing variability creates real loss or support load. Plan contract and provider dependencies with change paths in mind as corridor or market conditions shift.

Put AI where it removes bottlenecks, not where it adds risk#

Once ownership of exceptions and release control is clear, put AI on payment-operations bottlenecks, not on final compliance judgments. The practical gain is less manual triage, cleaner inputs, faster correction paths, and clearer status visibility when payouts fail.

Where AI earns its place#

AI is most useful in the back-office work that still creates drag: exception handling, returns, reconciliation prep, and status-driven response workflows. Current evidence supports this. Teams still handle many exceptions manually, while AI can classify and route exceptions, read remittance data, and match it to payments.

That is different from deciding whether a payout should pass a compliance gate. Keep AI scoped to bounded tasks with observable outcomes, such as routing failed payout cases, capturing required fields during intake, flagging exceptions for review, and triggering correction steps after failed payments.

Good uses versus risky uses#

Use a simple rule: automate only steps with guardrails, visible outcomes, and a clear human handoff.

Good candidates:

- document intake with validation checks and configurable matching logic

- exception flagging that creates review tasks instead of auto-approving payouts

- reconciliation prep, including matching remittance details to payment records

- delayed or failed payout response orchestration, including prompt correction flows

Risky candidates:

- black-box approval or rejection of compliance-gated payouts

- release-logic changes operators cannot review

- autonomous handling where operators cannot explain why a case was routed, held, or cleared

Explainability limits and over-reliance risk still matter in financial operations. In the Bank of England and FCA survey published on 21 November 2024, only 2% of AI use cases were fully autonomous, while semi-autonomous patterns with human oversight were more common.

Use oversight as a design test#

For higher-risk decisions, design for effective human supervision during use. Operators should be able to understand what happened and intervene when needed.

Before rollout, verify:

- the policy boundaries the model can act within

- the operator view of case classification outcomes

- rollback behavior for misroutes and false flags

- logs for handoff, review, override, and final resolution

If automation bias appears, narrow the scope quickly. Let the model suggest, sort, and draft, but keep human confirmation for holds, releases, and compliance-sensitive exceptions.

Do not confuse vertical AI with payment infrastructure#

Audience fit matters. AI receptionists in home or field service can help with calls, intake, scheduling, and quoting, but that is adjacent to settlement infrastructure. It does not demonstrate instant settlement capability.

Be more cautious in cross-border payouts, where cost, speed, access, and transparency frictions still persist. Treat domestic service-workflow wins as evidence for intake and support efficiency, not proof that global payout operations will perform the same way.

Build compliance gates into the timeline from day one#

If you want faster contractor payouts, design for compliance before payout creation. KYC, KYB-style business verification, AML and sanctions controls, tax-profile collection, and jurisdiction-specific payout constraints can determine when a contractor is payout-ready.

Your operations clock and your settlement clock are different. Work can be approved internally, but payout can still be blocked if verification is incomplete, beneficial-owner data is missing for an entity, tax forms are missing, or a sanctions review requires investigation.

Where compliance changes the timeline#

Treat every payout as three stages: readiness gate, execution, and post-event confirmation. Delays often show up when those stages are blurred.

| Gate | What changes cycle time | Operator check before release |

|---|---|---|

| Identity and business verification | KYC checks and, for entities, beneficial-owner identification can be required before payout capability is enabled | Confirm required identity fields are collected and verification status is complete before creating the payout |

| AML and sanctions controls | Reviews can interrupt transaction flow, and blocked transfers can trigger reporting obligations | Confirm screening outcome, hold reason, and escalation owner are recorded |

| Tax profile readiness | Missing or invalid tax data can delay setup and create withholding obligations | Confirm the correct tax form is on file, such as Form W-9 for U.S. TIN collection or Form W-8 BEN for foreign-status documentation |

If a U.S. payee’s TIN is missing or incorrect, backup withholding can apply at 24 percent. That changes payout amounts, recordkeeping, and approval ownership.

A baseline artifact set to maintain#

Use this as an operational baseline and adapt it by jurisdiction, provider, and program requirements:

- required data fields: legal name, address, date of birth or entity details as applicable, TIN or foreign-status form, payout method details, country, and settlement currency

- evidence records: submitted documents, verification outcomes, screening result, tax-form receipt date, and any hold or restriction reason

- approval logs: who reviewed an exception, who overrode it, when, and under which policy

- escalation ownership: named owners in compliance, finance ops, support, and engineering for verification failures, sanctions hits, tax issues, and payout rejects

The failure mode to avoid is simple: creating the payout first and discovering later that the contractor was never payout-ready.

Sequence the steps in the right order#

Run policy checks before payout creation. Execute with idempotent requests so retries do not create duplicate payouts. Then reconcile asynchronously from status events and webhooks, while handling retries and duplicate event delivery.

That sequencing preserves a clean decision trail: readiness before money movement, retry-safe execution, and matched post-event confirmation instead of blind trust in event streams alone.

Say “where supported” and confirm it before launch#

Do not describe faster payout behavior as universal. Payout availability varies by country, industry, and provider configuration, and settlement currency support is country- or region-specific.

For each launch, state faster payout behavior as “where supported,” then confirm country coverage, payout-method availability, onboarding requirements, and program-specific restrictions before go-live. If those constraints are not confirmed in writing, treat the corridor as unproven. For a step-by-step walkthrough, see Short-Term Rental Industry in 2026: Compliance, Automation, and Niche Strategy.

Before rollout, pressure-test policy gates, idempotent retries, and exception ownership for your first corridor in the Gruv docs.

Design for failures you will definitely hit at scale#

Approved payouts can still fail in predictable ways, so the operational win is not avoiding exceptions. It is making each one visible, owned, and recoverable before it turns into repeat tickets and duplicate work. At scale, unresolved reconciliation gaps, stale quotes, payout rejects, duplicate retries, delayed webhooks, and stuck manual approvals can all look like “processing” unless you define them explicitly.

The failure table you actually need#

| Failure mode | Primary owner | Detection signal from real-time tracking | Customer-facing message | Recovery target |

|---|---|---|---|---|

| Unmatched deposits | Finance ops / reconciliation | Inbound funds posted but no automatic match to invoice or customer balance reference | “We received funds and are matching them to the correct payment record.” | Manually reconcile the transfer and attach it to the correct payout record before release |

| Stale quotes | Treasury / payments ops | FX quote validity window reached before execution, or quote no longer valid at submission time | “Your payout is pending a refreshed exchange rate before release.” | Refresh the quote, reprice if needed, and reapprove before sending |

| Payout rejects | Payments ops with support coordination | Payout status returns failed or returned, often with destination-data mismatch or bank-detail error | “Your payout was rejected by the receiving bank. We’re updating bank details before retrying.” | Correct destination data, validate against bank record, then reissue one clean payout |

| Duplicate retries | Engineering / payments platform | Repeated client or server retry against the same payout action after a network failure without an idempotency key or duplicate-object check | “We’re confirming your payout was created only once before any retry.” | Confirm there is a single payout object, suppress duplicates, and resolve any duplicate if created |

| Delayed webhooks | Engineering / platform reliability | Missing expected status event, webhook delivery failures, or undelivered events query shows delivery_success=false | “Your payout is still being tracked. Final confirmation is delayed, but we are checking directly.” | Backfill missed events, rebuild the status timeline, and reconcile against source-of-truth records |

Unresolved manual approvals | Finance ops / compliance approver | Approval request open beyond policy window, no decision owner, or queue growth without status progression | “Your payout is awaiting review. We’ll notify you as soon as approval is complete or more information is needed.” | Assign an approver, decide approve or reject, or request missing evidence with a dated status update |

Make status states concrete, not comforting#

Generic status labels create confusion. A contractor waiting on bank-detail correction needs a different next step than one waiting on approval, event confirmation, or a refreshed quote.

Use states that map to real decisions and evidence: received, under review, awaiting bank correction, sent, confirmation delayed, completed, rejected. This gives support and contractors a shared reference point and helps answer the common “where is my payment?” question with specifics instead of reassurance.

There is sequencing discipline here too. Show sent only after payout creation, and show completed only after confirmation evidence. That helps prevent overstating progress in flows where fast payout UX is not the same as final interbank settlement.

Operator details that prevent repeat incidents#

A small set of controls can reduce repeat failures. Validate destination details before release, because incorrect destination information is a common cause of returned payouts. Before retrying, verify idempotent handling so network failures do not create a second payout object.

Treat webhooks as asynchronous signals, not guaranteed real-time truth. If your endpoint times out, updates can be delayed. Acknowledge quickly, process heavy work asynchronously, and run backfill checks for unsuccessfully delivered events. Because retries can continue for up to three days, weak status messaging can create avoidable ticket volume.

Apply the same rigor to manual approval queues. If an item needs approval, track approver, request time, requested evidence, and escalation owner. Without those fields, work is waiting, not managed.

The deeper failure mode is fragmented records. Automation helps only when status history, approval trail, payout object, and reconciliation record are visible together.

A practical rule for rollout#

If real-time tracking shows execution is healthy but tickets keep rising, fix your state model before expanding corridors or making faster-payout promises.

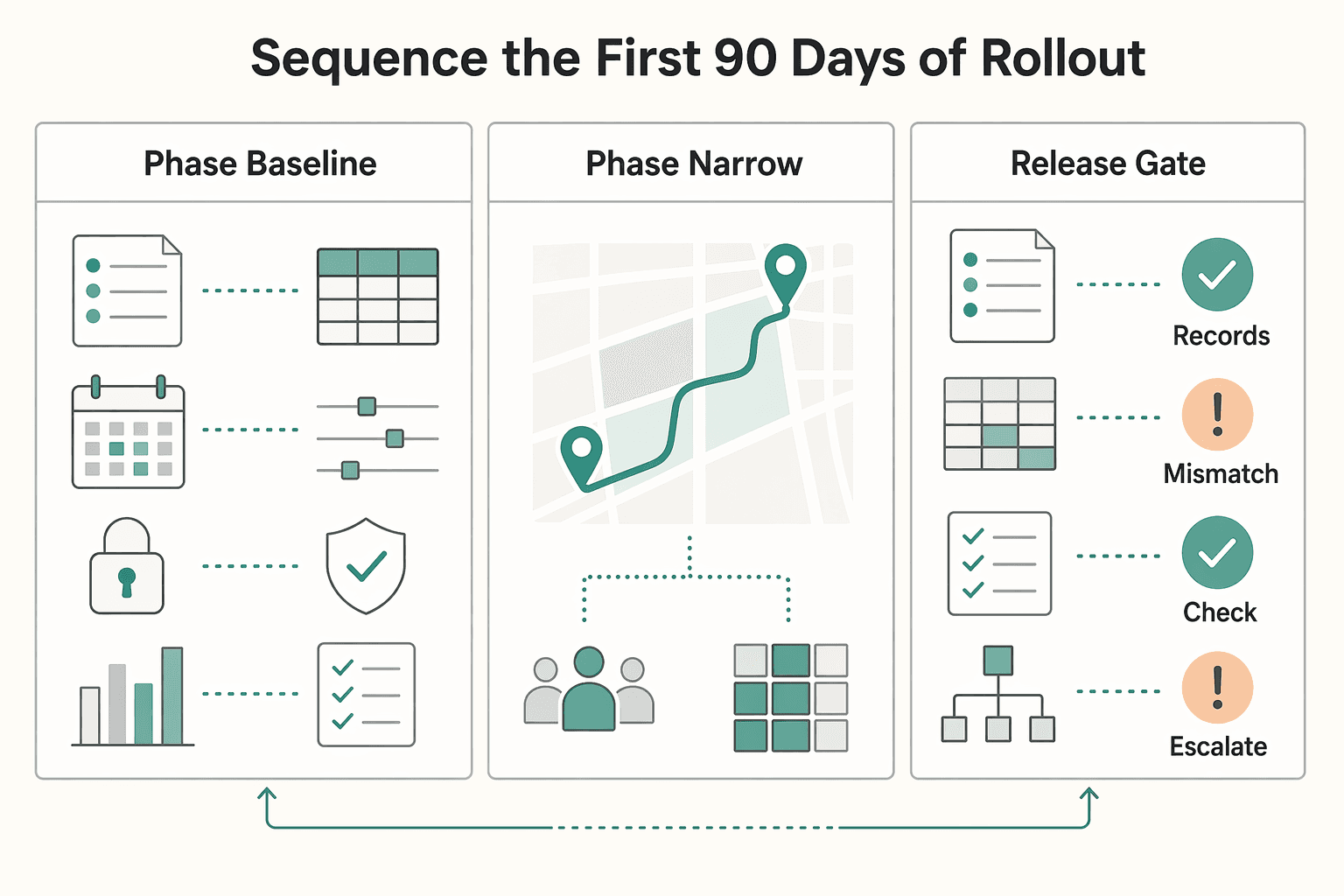

Sequence the first 90 days of rollout#

Treat the first 90 days as a gated rollout plan, not a broad launch: baseline first, pilot one corridor and one cohort second, then expand only if your controls hold.

This sequencing is consistent with phased payment implementation. The FedNow journey is split into 6 phases, with readiness assessment and cross-functional role definition before go-live. That matters because instant payments are irrevocable once sent, so weak data quality or unclear approvals become expensive quickly.

| Phase | What you are proving | What to measure | Minimum evidence before moving on |

|---|---|---|---|

| Phase 1 baseline | You understand current operations before automation changes them | invoice processing time, approval latency, exception categories, support contacts, reconciliation lag | Baseline report, owner list, exception taxonomy, current-state status map |

| Phase 2 narrow pilot | Automation works in one controlled payout path | Status-event coverage, payout completion consistency, reconciliation checkpoints, manual intervention rate | Event logs, query or report outputs, reconciled pilot transactions, approval records |

| Phase 3 gated expansion | Reliability holds as volume and market complexity increase | Stable completion rates, no material support-volume spike, complete audit trail across payouts and exceptions | Release review, sample audit pack, support trend review, unresolved-issue register |

Phase 1 baseline the current state before you switch anything on#

Start with operating reality, not corridor count. If you cannot measure invoice processing time, approval wait time, and top exception categories, you cannot tell whether automation improved outcomes or just moved delays.

Keep the baseline operator-focused. For each payout, capture request time, approval start and end, payout creation time, status changes, completion confirmation, and exception tags. The goal is a before-and-after record that finance ops, support, compliance, and engineering all trust.

Use this phase to lock ownership. FedNow readiness guidance calls for a cross-functional internal team with defined roles before launch. If approval policy, reconciliation, support messaging, or payout execution has no clear owner, pause and fix that first.

Phase 2 automate one corridor and one cohort, then instrument everything#

Pilot narrowly as a scoping choice, not a universal rule. Choose one corridor and one contractor cohort where requirements are already understood and exception handling is manageable.

Instrument status progression end to end: request received, approval decision, payout created, sent, delayed confirmation when relevant, completed. If your provider supports report pulls and queries, use them from day one instead of relying only on dashboard summaries.

Add a reconciliation checkpoint. The G20 cross-border program includes payment-status tracking and sets a target that credited payments should be reconciled by end of day by end-2027. Even outside full cross-border scope, that is a strong pilot standard.

Guard against false confidence from fast initiation. For any near-instant-settlement claim, require sample reviews where the payout object, confirmation evidence, and reconciliation record align.

Phase 3 expand only when the gates pass#

Expand only when three gates pass: completion consistency, support stability, and audit-trail completeness. Completion consistency means transactions reach the same end state through a repeatable sequence. Support stability means inquiry volume does not rise materially versus Phase 1 as pilot volume grows. Audit-trail completeness means you can reconstruct a payout without cross-team screenshot hunts.

Your release review evidence pack should include:

- status-event history for a representative transaction sample

- reconciliation outputs showing credited payments matched on time

- approval logs with timestamps and decision owner

- exception list with root-cause category and resolution outcome

If the pilot misses targets, stop adding surface area#

If early cohorts miss targets, pause expansion and diagnose before adding corridors. Start by checking policy gates and data quality, plus mismatched status definitions across systems.

Do not assume volume will smooth out execution risk. BIS notes many end-2027 cross-border targets are unlikely to be achieved on time. ECB rollout milestones are also phased by market type, including 9 January 2025 for receiving instant payments in euro area member states.

If stable, expand one variable at a time. If unstable, fix evidence trails, policy logic, or source data before adding countries.

Related: The Future of Contractor Payments: Embedded Finance Real-Time Rails and Programmable Money.

Measure outcomes with operator-grade checkpoints#

Measure each expansion release as an operations change: continue only when process, execution, and contractor-trust signals hold; hold or roll back when they weaken, even if vendor benchmarks look strong.

Track the three layers that show operating reality#

One completion metric is not enough. Use separate layers for internal friction, funds movement, and contractor confidence.

| Layer | What to track | What it tells you |

|---|---|---|

| Process health | manual approvals backlog, approval aging, exceptions waiting on missing data or documents | Whether automation reduced internal delay or shifted work into queues |

| Execution health | Status progression from request to approval to payout created to sent to completed, plus non-final or action-required states | Whether payments are reaching a final outcome reliably |

| Trust health | Contractor inquiry rate, top ticket reasons, repeat contacts on the same payout | Whether your status model and payout handling are credible to recipients |

Watch for faster initiation paired with a growing approvals backlog, and avoid treating sent as success. A payment status shows what is happening at that point in the lifecycle, and action-required states still need intervention until a final outcome.

For always-on rails, run continuous checkpoints. FedNow is designed for 24x7x365 processing, and its flow states that steps 2 through 6 complete within a few seconds and no more than 20 seconds. In a FedNow-supported corridor, use that as an execution-health check and investigate outliers.

Make every release carry its own evidence pack#

Do not approve from dashboard summaries alone. Require a release pack that lets finance ops, support, and engineering reconstruct outcomes without screenshot hunting.

At minimum, include:

- event logs showing resource state changes

- reconciliation outputs matching documentation to actual funds movement

- exception-resolution times by category

- payout status distributions, not only aggregate completion rate

The checkpoint is traceability: for a representative sample, payout record, event history, and reconciliation line should align on timestamps and end state. Stripe Event objects are one usable state-change artifact, and Adyen’s Payment accounting report is a useful model because it includes lifecycle status changes, events, and modifications.

A clean top-line completion rate with a growing tail of non-final statuses or slower exception resolution is a red flag.

Use continue, hold, and rollback rules from your own data#

Translate these measures into explicit SLO-based release decisions. An SLO is a defined reliability target for operating decisions.

Continue when recent performance stays within your target range and the evidence pack is complete. Hold when reliability degrades over your chosen recent window, even if all-time averages still look acceptable. Roll back when a release degrades status progression, increases reconciliation mismatches, or creates new approval or exception backlog.

Use vendor benchmarks as context, not as decision triggers. Papaya and Medius figures can help frame questions, but they are not proof that your contractor payout corridor is reliable.

Tie each external speed claim to an internal definition#

If a provider says instant, define the exact proving event. For true instant payment, the bar is recipient funds near real time with interbank settlement already completed. On RTP, submitted payments cannot be revoked or recalled, so finality matters more than a fast API response.

Map claims to the right layer:

Faster processing: process health, for example lower approval latencyInstant settlement: execution health, meaning rail-specific final confirmation plus reconciliation evidenceBetter payment experience: trust health, tracked through inquiry rates and repeat contacts

This translation keeps rollout decisions grounded in operator evidence instead of headline claims. Related reading: Freelance Finance Automation With Zapier and Stripe Controls.

Validate vendor claims before they shape strategy#

Treat vendor claims as hypotheses, not strategy inputs, until each one is mapped to a measured outcome, market scope, and an operational definition that matches your payout reality. These vendors are making different kinds of claims, so do not judge them with one yardstick.

| Vendor | What the claim is really about | What to verify before it affects strategy |

|---|---|---|

| EverPro | Productivity for home and field service operators: helping businesses win jobs, save time, and grow. | Confirm whether the benefit is internal efficiency only. Do not treat this as proof of payout rail capability or final settlement. |

| RelayFi | Control and approval governance, with automation tied to plan tier. Rules-based approvals are reserved for Grow and Scale plans. | Check plan gating first, then timing conditions. Same-day ACH depends on sending before 3pm EST on a business day. |

| Medius | Productivity plus control and fraud-risk reduction in AP automation; benchmark material uses data from thousands of AP teams. | Verify where those benchmarks were measured and whether they match contractor payout operations rather than general AP workflows. |

| Papaya Global | Compliance positioning with explicit KYC/AML language, plus marketplace copy stating 95% same-day payments. | Request corridor mix, sample basis, and exceptions, and confirm whether results apply broadly or only to selected routes. |

Decision rule: do not treat faster processing as final settlement. If a claim does not define what event counts as settled, classify it as process speed, not funds finality.

Use a claim-to-proof check for each major promise:

- what exactly was measured

- where it was measured

- which population or corridor mix was included

- which conditions or cutoff windows applied

- which evidence your team can inspect

Keep the answers in a shared assumptions register for product, finance ops, sales, and GTM. One row per claim is enough: vendor, exact wording, proof source, scope limits, open questions, and your approved internal interpretation.

Make the build versus partner call with explicit decision rules#

Use this rule first: build the control plane when your edge is orchestration, and partner for rail access when time-to-market is the constraint. In practice, this is an ownership-versus-speed decision, not a build-versus-buy ideology test.

A partner can reduce technical and administrative burden for an initial launch, but it does not transfer your compliance or operational accountability. Treat partner adoption as a connection strategy, not a risk-transfer strategy.

Build where your differentiation lives#

Build first if you expect to win on provider and corridor decisioning. That usually means routing logic, payout-state modeling, approval controls, reconciliation outputs, and operator visibility into what happened, what is pending, and what needs action.

Use this checkpoint: if the asset you are protecting is your payout method rules, approval model, reconciliation logic, and contractor-facing status states, build the control plane. If most upcoming work is bank connectivity, scheme access, and provider onboarding, you are probably building commodity rail access too early.

Partner when launch speed matters more than rail ownership#

Choose partner-first when you need one region live quickly or local rail access is the gating factor. FedNow went live on July 20, 2023, is designed for 24x7x365 processing, and allows institutions to participate through third parties. That can be a practical model for fast domestic rollout.

Apply more caution when the roadmap turns cross-border. Cross-border flows still face high costs, slower processing, frequent mistakes, and limited transparency, with added complexity from multiple intermediaries and interoperability limits. The FSB’s 11 global targets, including the end-2027 target that 75% of cross-border retail payments make funds available within one hour, indicate progress, not universally solved instant outcomes.

Score the choice before you commit#

Score each path from 1 to 5, where 5 is better for your business now, using evidence rather than deck language.

- Integration effort: Can you launch the first market without months of rail-specific build?

- Compliance ownership: Which obligations remain yours even when a partner executes part of the flow?

- Exception burden: How much reject, delay, and status-gap handling will require manual intervention?

- Market coverage: Does support exist for the exact country, currency, and payout path you need?

- Migration risk: If you add or replace partners later, how much ledger, status, and policy logic must change?

Always verify corridor support at country-and-currency level, not just headline footprint. Coverage varies by market and settlement currency, and local payout routes are often faster than cross-border paths.

| Founder situation | Best call now | Keep in house from day one | Why |

|---|---|---|---|

| One domestic region, speed matters most | Partner for rail access | Payment visibility, approval policy, reconciliation, contractor status messaging | Faster launch and lower connection burden while keeping rail portability in scope |

| One cross-border corridor, demand still uncertain | Hybrid | Corridor rules, compliance checks, real-time tracking, exception-handling logic | Cross-border variability makes portability and control logic more valuable |

| Multi-region expansion likely | Build control plane first, then add partners market by market | Routing logic, payout state model, audit trail, provider abstraction | Coverage is uneven and changes over time, so lock-in risk can rise across regions |

If you are launching one region now, partner-first can be the lower-execution-risk path when speed is the priority. If multi-region expansion is already part of your plan, build the layer that lets you change partners without rewriting core operating logic.

For a related perspective, see The Future of the Agency Model in the Age of AI.

Conclusion#

Near-instant contractor payouts are a market-by-market operational outcome, not a universal product feature. Treat automation and instant-settlement claims as corridor-specific assertions you need to validate, not language you can reuse across every launch.

Sequence markets by compliance clarity and operational readiness before headline speed. In the EU, the Instant Payments Regulation covers euro-denominated credit transfers within the European Union, with different receiving deadlines by market type: 9 January 2025 for euro area Member States and 9 January 2027 for non-euro area Member States. It also adds recurring compliance work, including at least daily checks for targeted financial restrictive measures. In the U.S., instant-payment services are accessed through participating financial institutions rather than directly from the central bank, and participating institutions and service providers are expected to meet availability and service-level requirements.

For cross-border rollout, keep expectations tighter than domestic rollout. Fast payment systems now exist in over 70 countries, but cost, speed, access, and transparency remain core friction points, and interoperability across domestic fast-payment systems is still difficult in practice. FATF’s regulatory-heterogeneity point is the practical constraint: AML and CFT controls are not identical across jurisdictions, so one country’s controls do not automatically transfer to another.

Scale with measurable checkpoints. Confirm you can track payout status from initiation to funds availability, assign ownership for exceptions, and reconcile events without ambiguity. A corridor is not production-ready because the happy path is fast. It is ready when exception handling is visible, owned, and recoverable.

Define settlement terms precisely across product, operations, and support. Document when funds are final, how rejects or timeouts behave, and how delays tied to compliance review are communicated so external promises match what your rail and providers can actually support.

Before broader expansion, create three artifacts:

- build a first market comparison table with country, currency, rail access, compliance burden, and near-instant feasibility

- define written settlement terms covering finality, funds-availability wording, reject windows, and required evidence

- validate one corridor end to end with timestamped status events, reconciliation output, and exception reporting

When your comparison table is ready, use it to validate market coverage and operating constraints with Gruv.

Frequently Asked Questions

What does `instant settlement` actually mean in contractor payments?

It means funds transfer is final, not just fast status movement. In U.S. instant-payment documentation, RTP settlement is described as final and irrevocable, and FedNow describes immediate funds availability to receivers. If a vendor only shows quick initiation or same-day processing, that is faster operations, not settlement finality.

How does `contractor payment automation` reduce delays from `manual approvals` and disconnected systems?

Mainly by reducing handoffs before payout creation, not by making every rail faster. Nacha notes that many back-office workflows still rely on manual intervention for exception handling, returns, and reconciliation, so delays often persist unless those paths are explicitly managed. A practical test is whether you can see where a payment is waiting, who owns the next action, and whether the hold is policy, data, or rail related.

What usually breaks first when scaling `cross-border contractor payments`?

Data consistency and exception handling are common breakpoints before the happy-path API call. CPMI notes that non-harmonized cross-border message data reduces straight-through processing and automated reconciliation, which can increase manual work. You should also expect first-mile and last-mile dependencies, because those legs are typically processed in domestic payment systems.

How should founders compare domestic and cross-border rollout constraints before market entry?

Start by separating domestic instant-rail behavior from cross-border reality. Some domestic rails support always-on processing (for example, 24/7/365 on RTP). FedNow sample flows show core steps completing within seconds and no more than 20 seconds in that sample flow, but that does not automatically carry into international contractor payouts. For cross-border entry, compare corridors on cost, speed, access, and transparency first, since the FSB still identifies those as core frictions and says global progress is unlikely to meet the end-2027 timetable.

Which `service-level agreements (SLAs)` matter most when evaluating payout partners?

Prioritize SLAs that define finality, funds availability, timeout behavior, and exception handling, not uptime alone. A useful minimum set is the exact point funds become irrevocable, the timeout or reject window, and how rejects, returns, and investigations are communicated. If an SLA cannot state when a payment must settle or be rejected within a specified period, contractor-facing expectations will be hard to manage.

How do `AI agents` improve operations without creating compliance risk?

Use AI agents for exception classification, routing, reconciliation prep, and surfacing missing information for review. Nacha points to machine learning reducing manual decisioning in exception routing, where many payment operations still rely on manual intervention. Keep compliance-gate authority and independent critical review with humans, especially as regulators like the FCA rely on existing governance frameworks rather than AI-specific rules.

What proof should operators request when vendors claim faster or “real-time” payment performance?

Ask for corridor-level evidence that separates initiation speed from funds availability and settlement finality. The proof pack should include country and currency scope, rail used, timestamped status events, timeout or reject definitions, exception rates, and reconciliation outputs for the same corridor mix you plan to launch. Treat objective speed claims as claims that should already have a reasonable basis and prior substantiation, especially when large automation gains are also being advertised.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bsaaml.ffiec.gov/manual/OfficeOfForeignAssetsControl/01trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- federalreserve.gov/paymentsystems/fednow_about.htmtrusted

- federalreserve.gov/paymentsystems/files/interest_on_rtp_joint_b...trusted

- ftc.gov/sites/default/files/attachments/training-mat...trusted

- ftc.gov/legal-library/browse/ftc-policy-statement-re...trusted

- irs.gov/businesses/small-businesses-self-employed/mo...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: