Quick Answer

Use a for further credit wire transfer only when instructions name a receiving institution and a separate final beneficiary. Enter account owner and routing values exactly as provided, including memo text when no dedicated FFC field exists. Pause release if your form cannot represent both legs without truncation or guesswork. Also confirm provider support before submission: Wise states it does not process FFC wires.

What to Verify Before Releasing an FFC Wire#

A wire can reach the first receiving institution and still need additional instructions to reach the intended final account. In a for further credit wire transfer, funds may first land in an organization's main receiving account, sometimes through an intermediary or correspondent bank, and then rely on final-credit instructions for allocation to the ultimate beneficiary.

You will see this when the recipient collects incoming wires into a central account and then splits funds to individual accounts. Brokerage funding is a common example, and FFC can also apply to international wires. In practice, bank-level routing can look successful while final beneficiary crediting is still pending.

The real decision is operational. You need to know whether FFC is needed, where each identity and account detail belongs, and how to keep a traceable record when bank forms and recipient instructions may label fields differently. This guide stays focused on those decisions so finance, ops, and product teams can reduce avoidable exceptions and explain payments end to end.

Treat FFC as an instruction layered onto a wire, not a separate payment rail. You are still sending a wire. FFC tells the receiving organization where funds should land after initial receipt.

Exact FFC requirements vary by destination account and institution workflow. This guide stays narrow: what is generally reliable in operations, what is institution-specific, and what to verify before release. For related payment-operations context, we covered this in detail in SEPA Instant Credit Transfer for Euro Payouts.

FFC means a two-step routing instruction, not a payment type#

FFC is a routing instruction layered onto a wire, not a separate payment type. You still send a standard wire transfer, and the FFC details tell the receiving organization where funds should land after initial receipt.

A typical chain looks like this: sender bank -> intermediary/correspondent bank, when used -> organization's main receiving account -> ultimate beneficiary allocation. The important point is that the wire can arrive at the top-level account first, and the FFC instruction indicates where funds should in the end end up.

Required fields can vary by receiving account context, so follow the recipient's written instructions exactly.

Your operating checkpoint is exact matching. If instructions provide an account name and account number, enter them exactly. If there is no dedicated FFC field, keep the memo or description pending until the account number, account name, and requested wording are verified against the recipient instruction packet or an approved, tested template; then use only those verified details.

A practical limitation is provider support: not every provider processes FFC wires, and Wise says it does not. For a related breakdown, see FFC Account Number Explained: When and Why Wire Transfers Need Further Credit Instructions.

Where FFC is required in real platform payment flows#

Use FFC-style routing when the recipient's own instructions show a two-step destination, not just because the payment is a wire. That helps you avoid adding complexity where none is needed.

| Context | Signal | Risk | Control |

|---|---|---|---|

| Brokerage and custody funding | A second allocation step appears after initial receipt | The wire can arrive correctly at the institution while final allocation still depends on complete downstream beneficiary details | Confirm the top-level receiving institution and account details, confirm downstream beneficiary details exactly as provided, and pause if the form cannot carry second-step details cleanly |

| Omnibus receiving accounts | Instructions include For final credit to, For credit to, or For the benefit of | The institution can receive funds before final beneficiary credit is completed | Treat those lines as routing-critical until the recipient or receiving institution confirms otherwise, and keep the full instruction packet with the outbound field mapping |

| Cross-border paths | One institution is named to receive the wire and a different beneficiary is named for final credit | Multi-institution routing increases operational complexity and downstream fields need tighter validation | Validate all downstream fields before release; if there is no dedicated field for second-leg routing details, escalate before sending |

Brokerage and custody funding#

Some brokerage and custody flows separate the receiving institution from the final beneficiary. In that setup, a wire can arrive correctly at the institution while final allocation still depends on complete downstream beneficiary details.

Names such as National Financial Services LLC or Fidelity Group of Funds are not proof that FFC routing is always required. They are a signal to verify whether the instruction packet includes a second allocation step after initial receipt. Before you approve the payment, check three things:

- Confirm the top-level receiving institution and account details.

- Confirm the downstream beneficiary details exactly as provided.

- Pause the payment if your form cannot carry second-step details cleanly.

Omnibus receiving accounts#

Omnibus or pooled receiving accounts can raise allocation risk because the institution can receive funds before final beneficiary credit is completed. If recipient instructions include lines like "For final credit to," "For credit to," or "For the benefit of," treat them as routing-critical until the recipient or receiving institution confirms otherwise.

Keep the full instruction packet and your outbound field mapping together so operations can reconcile quickly if allocation questions arise.

Cross-border paths need extra caution#

Cross-border transfers are more likely to involve multi-institution routing, including correspondent relationships, so operational complexity increases. That does not mean FFC is required for every international wire. It does mean layered routing is more common and downstream fields need tighter validation.

Use a simple rule:

- If one institution is named to receive the wire and a different beneficiary is named for final credit, validate all downstream fields before release.

- If your tool has no dedicated field for second-leg routing details, escalate before sending instead of compressing instructions into fragile free text.

A common risk is successful arrival at the receiving institution followed by delayed final allocation.

For a step-by-step walkthrough, see FFC vs FBO vs FAO Wire Transfer Instructions for Platform Teams.

How to map wire fields correctly the first time#

Map the recipient's instruction packet to your form line by line before release. One misplaced field can still allow a wire to be sent while delaying final allocation.

Use labels as clues, then verify against the packet#

Label text can vary across banks and portals, so treat phrases as routing clues rather than fixed definitions. Use each label to narrow the likely role, then verify it against the recipient packet and your bank's field guidance before you send.

| Label on the form/instructions | Treat as a possible role | Verify before send |

|---|---|---|

For credit to | An account in the routing path (bank-dependent) | Which institution and account details this field expects in your specific flow |

For final credit to | Final allocation details (bank-dependent) | Whether this field expects final account details, beneficiary details, or both |

For the benefit of | Beneficiary-identifying details (bank-dependent) | Legal name and any associated account reference exactly as provided |

Payment reference | Supporting free-text field | Whether it is supplemental only or required for downstream allocation |

If two or more of these appear together, assume a layered path and confirm which details belong to initial receipt versus final allocation.

Expect form-label variance, especially after ISO migration#

Field names can change while routing intent stays the same, so keep an internal mapping template that places recipient-provided details consistently even when portal labels differ.

This matters more after the Federal Reserve's ISO 20022 migration. Wires sent on or after July 14, 2025 must use ISO format, and banks have flagged significant field and label changes. In that shift, older terms like Beneficiary may appear as Creditor, so teams should map meaning, not just familiar wording.

Add one release checkpoint#

Before you approve the wire, run one clean match pass against the recipient instructions:

- Confirm receiving-account details exactly as written.

- Confirm final-allocation details exactly as written.

- Confirm beneficiary-identifying details exactly as written.

- For cross-border instructions, check whether intermediary or correspondent routing details are required and captured in the correct place.

For recurring wires, approved templates can reduce re-entry risk. They help standardize entry, but copied payments can still carry stale values when some fields are locked, so final review is still required.

What breaks when one field is wrong#

A common failure mode is partial success: funds reach a central receiving account, but final allocation is delayed because downstream details were misplaced or incomplete. That can create manual repair work and slower resolution. If your form cannot clearly carry both the receiving leg and the final-credit leg, pause and escalate before release.

For a related operations comparison, see Same-Day ACH for Platforms: How to Speed Up Contractor Payments Without Wire Transfer Fees.

The minimum instruction pack your team should collect before sending#

Use one approved instruction record before release. Treat this packet as an internal control and preserve recipient-provided wording.

What to store in the packet#

Keep these items together in one versioned record:

- The original recipient instructions, captured exactly as written.

- Any downstream allocation text, captured exactly as written when provided.

- Any beneficiary-identifying text exactly as provided.

- Your internal field-mapping note showing where each provided value will be entered in your payment form, or flagged as unmapped.

- An exception note for instructions that do not fit available fields, with escalation instead of guessed formatting.

- An escalation contact tied to the instruction source, plus the final approve/hold/reject decision.

If routing details appear in the recipient instructions, store those values exactly as provided. Route them for second review instead of filling gaps from memory.

Make inclusion and ownership explicit#

Do not rely on operator memory. Define an internal split and make it auditable.

| Owner | Responsibility | Retained evidence |

|---|---|---|

| Intake owner | Collects the instruction packet and escalation contact | Original instructions and intake record |

| Review owner | Validates mapping and final entry text against the instructions | Approval notes and entered values |

| System owner | Maintains templates and version history | Template revisions and mapping notes |

That keeps review and repair grounded in one record instead of scattered messages. If you want a deeper dive, read A Guide to the 'For Further Credit' (FFC) Instruction in Wire Transfers.

Choosing FFC versus other rails in your payout architecture#

Choose the rail based on routing certainty first, then optimize operations. If recipient instructions include an intermediary path and a separate final-credit destination, treat a wire with FFC-style handling as an option to validate with the receiving institutions. If not, use the simplest direct rail your program supports that still preserves traceability.

| Situation | Practical default | Why teams pick it | Main caution |

|---|---|---|---|

Recipient provides explicit intermediary routing plus distinct For credit to / For final credit to details | Wire transfer with validated FFC-style instructions | Preserves the institution-provided path without substituting an unconfirmed route | Field mapping should be reviewed with each institution |

| Recipient can receive on a supported direct local rail or virtual-account flow, with no downstream final-credit leg | Direct local rail or virtual-account flow | May reduce handling when your ledger and reconciliation model already match that destination pattern | Do not assume reconciliation is automatically simpler |

| Instructions are incomplete or conflicting | Pause and resolve before sending | Prevents avoidable exceptions and rework | A payment can look sent before funds are actually usable, and availability can still take several days |

The decision rule that holds up#

These sources do not establish a universal FFC routing rule. When intermediary and final-credit instructions are explicit and complete, FFC-style wire routing can be a conservative choice to validate. That is not a universal rule that FFC is always correct.

When those downstream details are not explicit, default to the least complex direct rail you already operate with clear audit data. Complexity should be justified by recipient routing requirements, not habit.

Tradeoffs teams should evaluate#

The tradeoff is straightforward: preserving explicit recipient routing can improve operational certainty, but it can also increase formatting variability. It also demands tighter mapping discipline because field patterns should be treated as institution-specific until confirmed.

Exception workload and reconciliation effort depend on your controls, not the rail label. Faster-looking payment movement also does not guarantee faster usable funds, so finance and support workflows should rely on confirmed posting logic, not status optics.

Policy controls still govern the choice. Rail preference does not replace compliance obligations. Compliance treatment is fact-specific and tied to your business model, and existing BSA obligations may still apply even when a model is not explicitly listed in guidance.

Before release, document the payout-pattern risk assessment and show how oversight and monitoring fit into your AML program. A common failure mode here is hidden exposure. Teams route payments without fully understanding where risk actually sits.

What to mark as unknown up front. Set expectations early: treat SLA, fee, and field-format assumptions as unknown until confirmed by counterparties. The recommendation is narrower: preserve explicit institution-driven routing when provided and validated. Otherwise, prefer the simplest traceable direct rail inside your controls.

If your decision table points to simpler direct routing, compare whether dedicated receiving details change FFC handoffs and exception volume in your flow: Explore Virtual Accounts.

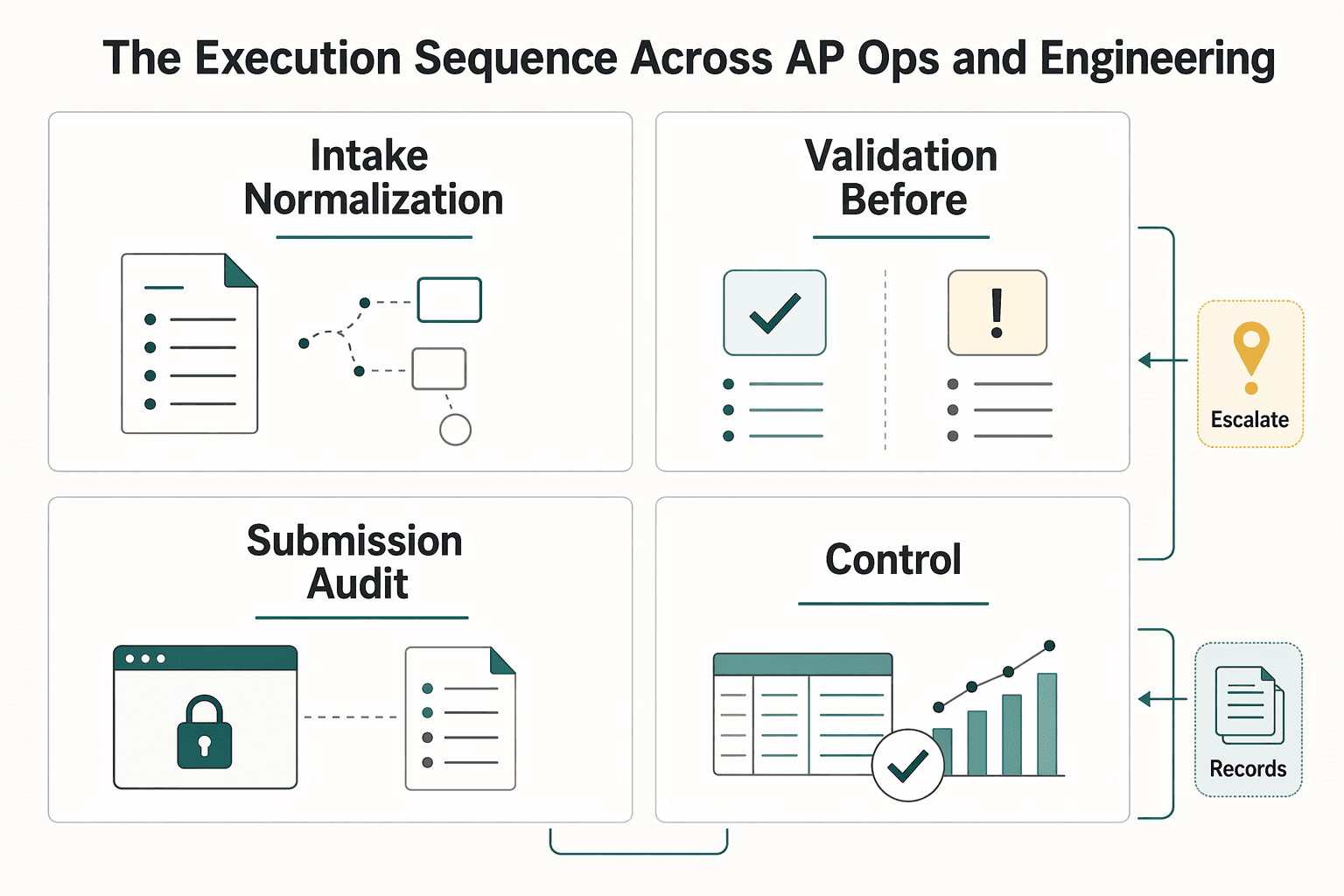

The execution sequence across AP, ops, and engineering#

A workable control sequence keeps payment facts intact from intake to closure: capture the instruction set, validate known versus unknown data, submit with a preserved record, then reconcile to final posting.

| Stage | What happens | Key control |

|---|---|---|

| Intake and normalization | Normalize the recipient packet into one internal record before submission | Keep the original source artifact and the normalized fields together, and separate unknown from accidental blank |

| Validation before release | Run a second review on the normalized record and the release payload before send | Confirm the data still matches the source packet and flag unresolved items instead of guessing; for non-critical items, leaving a field blank is better than inventing certainty |

| Submission and audit capture | Store the released payment as a control artifact | Retain the submitted payload snapshot, timestamp, and associated reference identifiers |

| Post-send controls and closure | Track the payment through reconciliation and close only when records align from initiation to posting | Keep evidence attached at each control point and preserve exception history intact |

Intake and normalization#

Start with the recipient packet as received and normalize it into one internal record before submission. Keep the original source artifact and the normalized fields together so teams are not retyping or reinterpreting details later.

At intake, separate unknown from accidental blank. A useful discipline from FinCEN SAR guidance is to complete items when relevant information exists, and to mark unknown explicitly for critical items in that filing context.

Validation before release#

Run a second review on the normalized record and the release payload before send. The goal is simple: confirm the data still matches the source packet and that unresolved items are flagged, not guessed.

For non-critical items, use the most complete information available. If information is not readily available, leaving a field blank is better than inventing certainty.

Submission and audit capture#

Once you release the payment, store the submitted payload snapshot, timestamp, and associated reference identifiers. Treat this as a control artifact, not just an operational log.

If your software cannot include pertinent known information in a non-critical field, FinCEN's filing guidance points to a discrete filing approach until systems are updated. Operationally, apply the same principle: use a controlled fallback instead of silently dropping known data.

Post-send controls and closure#

Track the payment through reconciliation with evidence attached at each control point, and close only when records align from initiation to posting. Keep exception history intact so management reporting and internal audit can reconstruct what happened.

This fits the OCC view of wire processing as a distinct transaction-and-settlement flow, with governance anchored in internal controls and auditable checkpoints.

Common failure modes and the fastest recovery path#

Treat FFC exceptions as data-integrity incidents first. Most stuck international wires trace back to missing or mismatched beneficiary details, and recovery is limited once a wire is processed and settled.

Where these wires usually break#

The breakpoints are usually predictable:

- Missing or unclear reference text that forces manual repair or rejection.

- Mismatched beneficiary data, including wrong or mistyped account or SWIFT details.

- Currency and account mismatches that trigger manual repair or rejection.

- Transfers that enter a compliance review queue and pause until information is resolved.

Fastest recovery path#

Do not edit facts mid-case. Escalate with the exact approved instructions and the exact submitted payload so support can trace the original message.

| Evidence item | What to include |

|---|---|

| Original recipient instructions | Full original recipient instructions, including all beneficiary and reference text provided |

| Submitted payload snapshot | Submitted payload snapshot, provider reference, and send timestamp |

| Observed symptom | The exact symptom, such as unclear reference, suspected SWIFT or account mismatch, or funds not posted to the intended beneficiary |

| Beneficiary confirmation | Any confirmation needed to validate intended account-owner details |

Bundle those items into one evidence pack.

If a routing error is suspected, contact the bank or provider within minutes for the best, still slim, recall chance. After settlement, reversal is generally not a path you should rely on.

Decision rules under pressure#

Under pressure, keep the decision tree simple. If the issue is unclear or missing reference data, push for repair tracing against the original provider reference instead of sending a duplicate transfer. If the issue is account or SWIFT mismatch, expect delay or rejection and prepare corrected instructions separately while the original case is investigated. If funds reached the institution but not the intended recipient, anchor support on the exact beneficiary details submitted and keep the first payment record intact until status is clear.

Related reading: Wire Transfer Fees for Platforms and How to Minimize Outbound Costs.

Reconciliation and audit evidence after the wire is sent#

After a wire is sent, the close standard is straightforward. Your team should be able to prove what was sent, how it was approved, and how it was reconciled from records alone.

Build one evidence pack per outbound wire#

Keep a compact record set for each outbound wire:

- initiation record on the approved request form, including electronic forms

- records required by your wire procedures for the submitted payment

- reconciliation records: wire log entry and settlement account statement match

- exception notes and follow-up actions

The wire transfer log is the anchor. If you cannot tie the settlement posting back to the log entry, treat the payment as an open exception.

Reconcile in a practical sequence#

Use a practical check set to isolate where a payment may have stopped:

- Sent wire event

Confirm submission and recording. Match the initiation record and key transaction details to the wire log.

- Settlement-side confirmation

Reconcile the settlement account statement against the wire log to confirm settlement on your side.

- Downstream confirmation (where available)

If downstream posting evidence is available, attach it. If it is not, state that limit clearly instead of assuming final allocation.

Fedwire settlement is immediate, final, and irrevocable once settled, so settlement confirmation may not prove downstream allocation in every routing path.

When wires are originated through a correspondent or other third party, keep party roles clear in internal records so exception review is easier.

Add controls that survive turnover. Keep separation of duties between initiators, approvers, and reconcilers, and make the reconciliation record independently verifiable. A second reviewer should be able to trace approved request -> wire log -> settlement account statement without relying on side-channel context.

During reconciliation, flag unusual wire amounts or volumes as exception signals and document the review outcome. Weak internal controls increase risk of loss from fraud or employee error. This pairs well with our guide on ACH vs Wire Transfer for Contractor Payouts When Platform Teams Should Use Each.

Cross-border and compliance caveats to confirm early#

Confirm cross-border behavior with the exact bank, jurisdiction, and program you will use before launch. For any International wire transfer flow, required message content and fields can vary by institution and corridor, so a domestic Wire transfer setup may not carry over cleanly.

Before go-live, verify these points in one test case and review the retained record or payload snapshot, not just the confirmation screen:

- core message data is present, including date, amount, transaction reference, and institution-chain details

- involved institutions in the payment chain can be captured separately from the Ultimate beneficiary when those roles exist

- your process is still usable when a bank form does not expose a dedicated field for one of those parties

Apply controls corridor by corridor, not as one global policy gate. Treat Anti-Money Laundering (AML) review and sanctions-related checks as market- and partner-specific program controls. This matters especially in fragmented payment chains, where weak originator or beneficiary data can make suspicious activity harder to detect and sanctions obligations harder to meet. If multiple institutions are involved, confirm early that your provider preserves the identity data your team needs for review and investigation.

Confirm recordkeeping early as well. In U.S. programs, the Bank Secrecy Act (BSA) focuses on records and reports that let institutions reconstruct customer-account transaction activity and maintain a paper and audit trail. Ask what cross-border wire records you will retain, in what format, and whether your team can interpret them without bank-side help.

Write implementation docs with restraint: "where supported," "when enabled," and "coverage varies by market/program." That language keeps teams from treating bank-specific behavior as a universal rule.

Managing bank-by-bank variance without creating chaos#

The cleanest way to manage variance is to treat each recurring destination instruction set as an approved internal pattern and require teams to use that pattern as written.

Define each pattern at the level you can verify from your own retained records. Do not infer Fidelity, Charles Schwab, Citibank UK, or other bank-specific routing behavior from these sources.

Freeze the approved template#

Capture and lock only what you can document from verified records:

- retained records, for example bank statements or receipts

- sanitized payload snapshot, approval date, and last verified date

- explicit status checks for any account that may need reactivation before use

Track template and mapping changes in version control so unverified assumptions stay visible and reviewable.

Put a real gate in front of first use#

Put real go-live controls in front of first use of any bank pattern. One clear failure mode to guard against: delayed processing when an existing account is not reactivated.

If your team cannot point to retained records, account-status checks, and an approved template version, treat the pattern as unapproved.

Conclusion#

FFC outcomes are operational. Success depends on exact instructions, consistent field mapping, and clean handoffs. Once a wire is initiated, errors are often hard to reverse.

That matters even more when multiple institutions are involved. Funds transfers move through a chain of interbank messages; complexity rises as more institutions are added, especially in cross-border flows that rely on correspondent relationships.

Before you scale volume, standardize three controls:

- Define a minimum instruction pack. Collect the beneficiary and routing details needed to initiate, trace, and reconcile the payment, including any corridor-specific routing code when required.

- Lock field mapping by approved destination pattern. Keep a tested mapping so each instruction element is placed consistently before release.

- Set an exception protocol. For delays or crediting issues, pull the original instruction packet, submitted payload snapshot, and provider or bank reference immediately.

Use a final pre-send check: compare the outbound payload against the approved instruction pack line by line, especially beneficiary and routing details. Fast processing is not a substitute for correct final crediting, and fees can vary by provider, destination, and amount, so confirm routing and cost before release.

Next step: implement the minimum instruction pack, mapping standard, and exception protocol before adding destinations or payout programs. If you need traceable cross-border payout operations with policy gates and clearer reconciliation, confirm coverage for your program and markets first.

When you are ready to run this with policy gates, idempotent retries, and audit-ready status tracking, review the operational fit: See Gruv Payouts.

Frequently Asked Questions

What is a For Further Credit wire transfer in plain terms?

A For Further Credit wire transfer tells the receiving side to route funds to one account first, then credit the intended recipient. In practice, a wire can reach the right institution and still need that second crediting step, so exact field mapping matters.

When is FFC required instead of optional?

There is no universal bank rule, so treat FFC as required only when the recipient instructions explicitly call for it. If the packet includes FFC language, follow that mapping exactly. If instructions are unclear, pause and verify before release.

Is FFC used for international wires or only domestic flows?

That depends on the provider and instruction set for the payment route. For international wires, required fields can expand based on the recipient country, so routing and beneficiary details usually need closer review.

Where do I enter FFC details if the bank form has no dedicated FFC field?

There is no universal fallback field for FFC text. Use the recipient instruction packet and your approved, tested template for that destination pattern. If you do not have a verified template, hold the payment and confirm placement first, or use a bank-specific guide such as How to Add For Further Credit Instructions to Bank Wires: Bank-by-Bank Guide.

What is the difference between `For credit to` and `For final credit to`?

Treat them as institution-specific instructions and follow the full instruction set and your tested mapping for that bank pattern.

What are the minimum details I should collect before sending an FFC wire?

Collect the receiving institution details, beneficiary details, and the exact approved placement for FFC instructions. For international flows, also capture any additional details requested for the recipient country. Keep the instruction packet and any supporting records your provider requires together in the same approved record.

What should I do first if an FFC wire is sent but not allocated to the final beneficiary?

Start a trace case with the original instruction packet, provider confirmation, and intended beneficiary details. Ask for the wire tracking reference if available (such as a Fed wire reference number when applicable), and confirm whether the wire has actually been released before treating it as an allocation failure.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- consumerfinance.gov/compliance/compliance-resources/deposit-acco...trusted

- consumerfinance.gov/rules-policy/regulations/1005/30trusted

- dir.ca.gov/dwc/sb1160-ab1244/Other-Consolidations/Mesa-...trusted

- fdic.gov/risk-management-manual-examination-policies/...trusted

- federalregister.gov/documents/2016/05/11/2016-10567/customer-due...trusted

- fincen.gov/resources/frequently-asked-questions-regardi...trusted

- fincen.gov/system/files/shared/CBFTFS_Complete.pdftrusted

- ftc.gov/system/files/warning-letters/covid-19-letter...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How to Send an FFC Wire Transfer With Fewer Errors

When a client asks for an **FFC transfer**, treat it as an accuracy-sensitive request, not a speed task. The request itself does not prove payment reliability, so your safest move is to confirm one current instruction source before you enter anything.

How to Enter For Further Credit Instructions on Bank Wires

The goal is first-pass accuracy: enter FFC wire instructions so funds reach the final account after the initial routing leg without avoidable rework.

FFC Account Number Meaning for Wire Transfers and Further Credit Instructions

FFC confusion is often a source-status problem, not just a wording problem. If teams act on instructions from the wrong place, execution risk increases.