Quick Answer

Treat the FFC account number meaning as a verification task, not a guess. In operations, it usually points to onward crediting details inside a further-credit flow, but labels vary by bank and program. Release only after confirming the latest official receiving instructions, capturing both intermediary settlement fields and final-recipient crediting fields, and approving ownership evidence. If instructions are stale, copied from non-authoritative channels, or unclear, stop and verify before sending.

Why FFC Account Number Confusion Causes Expensive Wire Errors#

FFC confusion is often a source-status problem, not just a wording problem. If teams act on instructions from the wrong place, execution risk increases.

If you came here for the meaning of an FFC account number, start with a cautious default: treat copied instructions as unverified until they are matched to the current official source.

Teams get into trouble when product, ops, finance, and support each interpret the same bank details differently. One person copies from an email, another from a help article, another from a portal screenshot, and nobody stops to ask which source is authoritative.

That source-status problem matters more than teams expect. A useful example comes from regulated publishing: a Federal Register page describes itself as an "unofficial informational resource," says readers "should verify their results against an official edition," and states it is "not an official legal edition." The same page (published 01/19/2024) also points to a newer item from 01/17/2025 labeled "Proposed rule; withdrawal."

Apply the same discipline to payment instructions. Before releasing a wire transfer, set one hard checkpoint: confirm the latest instructions against the official bank or program source, record where they came from, and retain the date or version you approved.

Everything below follows from that checkpoint. It focuses on verification steps before using FFC-related instructions, the minimum data to confirm before release, and how to reduce avoidable failures without turning every payout into a manual review.

One limit is worth keeping in mind from the start. These are operational defaults, not universal rules that apply the same way everywhere. Field labels and required details can vary across institutions and programs.

The recommendation is simple: standardize your internal intake and release checks, but do not assume one customer-facing template will work across every case. If the instructions are unclear, stale, or copied from anything other than the current official source, stop and verify before sending.

For related reading, see Virtual Account Numbers for Freelancers: How to Protect Your Bank Details. If you want a quick next step on FFC questions, try the free invoice generator.

Define FFC Account Number in Operational Terms#

In payment ops, the practical FFC account number meaning is simple: treat it as an ambiguous label until you confirm exactly what it refers to in the official instructions for that payout.

That caution is operational, not academic. "FFC" is used in unrelated contexts, including Fair Factories Clearinghouse and Fitness Formula Clubs. So if a request, ticket, or spreadsheet only says "send to FFC account number," do not infer the meaning from the acronym alone.

Use a field-by-field verification step before release. Match each required field to the current official source, keep the same structure in your payout form, and retain the approved source file or screenshot with the date.

The clearest red flag is any template that treats "FFC account number" as self-explanatory free text. If the wording is unclear, stop and request corrected instructions before funds move.

You might also find this useful: How to Send an FFC Wire Transfer With Fewer Errors.

Choose Between FFC Routing and Direct Beneficiary Routing#

Treat any FFC-vs-direct routing decision as unverified until you confirm it from official receiving-bank instructions.

Use this operating standard: do not release a transfer based on assumptions, account type, or institution name alone. Route only from the latest documented inbound instructions, and pause if the path is unclear.

If you are validating payment identifiers while reviewing those instructions, this guide on IBAN and SWIFT differences can help with field interpretation.

This pairs well with our guide on How to Get a National Insurance Number (NINO) in the UK.

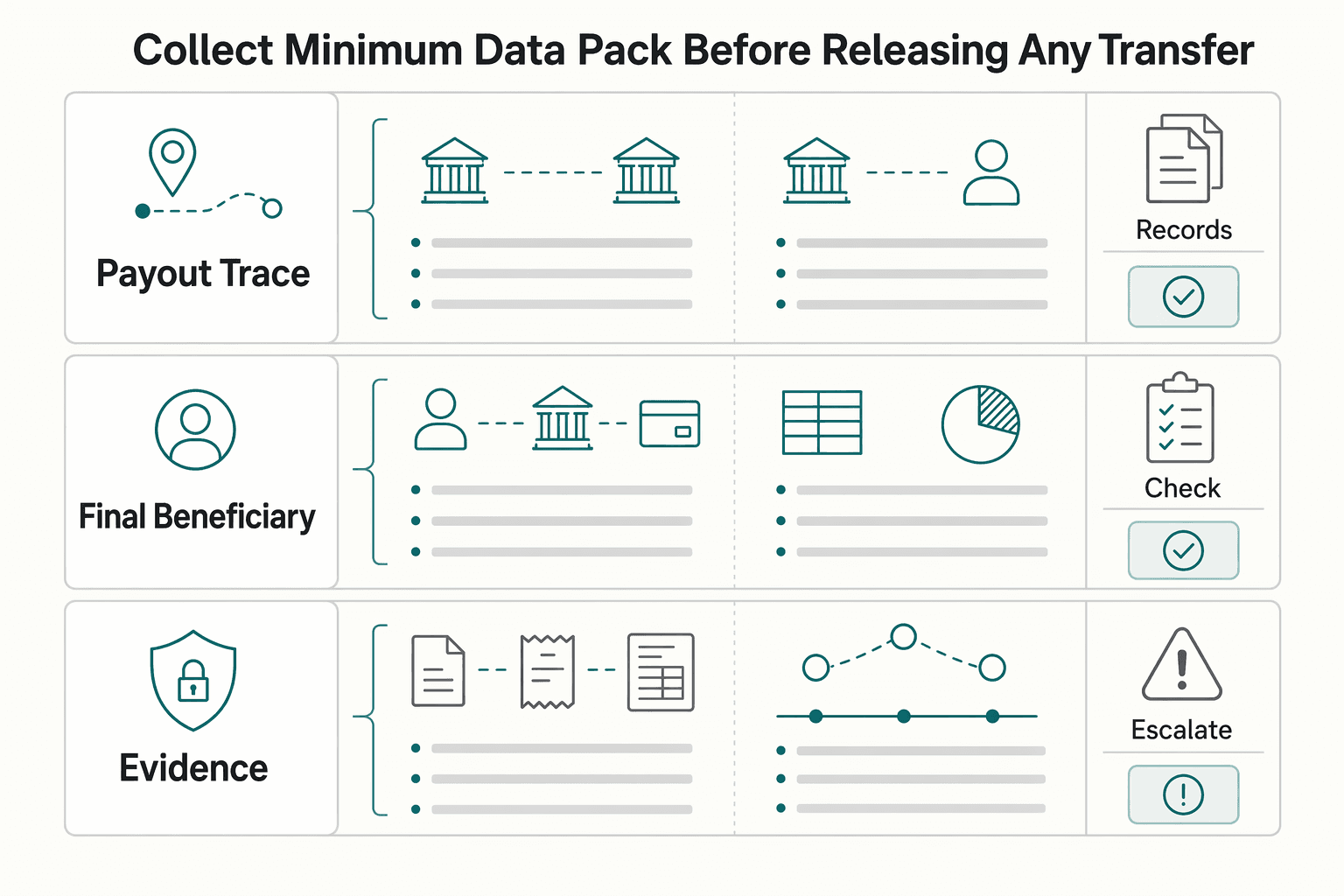

Collect the Minimum Data Pack Before Releasing Any Transfer#

When FFC routing is required, treat release as a two-layer data check: intermediary settlement details and final-beneficiary crediting details should both be complete before a transfer leaves the queue.

Do not collapse these layers into one free-text field. Keep settlement entities and account-specific items in separate structured fields so you can validate them and check downstream posting.

| Layer | Minimum data to capture | Release check |

|---|---|---|

| Intermediary settlement | Receiving institution name, routing identifier as provided (for example SWIFT/BIC), settlement account details, and any named account title | Matches current inbound instructions exactly and is clearly separate from beneficiary crediting data |

| Final beneficiary crediting | Beneficiary legal name, final account or crediting reference, and any required further-credit instruction text | Distinct from settlement account data and mapped to the intended recipient record |

| Ownership evidence | Internal evidence that ties the recipient record to the destination account | Approved per your payout policy before release (or explicitly escalated/approved as an exception) |

If you maintain standing settlement instructions, follow the same structure there: represent settlement entities with BIC codes where applicable, and populate account-specific items at the account level. In Fedwire-oriented setups, use the U.S./FEDWIRE market configuration so market-specific labels and validation rules are available.

Set release gates that block guessing#

No transfer should leave the queue until all of the following are true:

- Current receiving instructions are attached or otherwise preserved.

- Mandatory fields for both layers are present.

- Field-level format and validation checks pass for the identifiers collected.

- Ownership evidence is approved, or an exception is formally reviewed.

Treat the FFC account number as a structured crediting instruction, not a memo field. If your intake form cannot cleanly separate settlement routing from beneficiary crediting, fix intake before you scale volume.

For a step-by-step walkthrough, see How to Determine the Maximum Value of a Foreign Bank Account for FBAR.

Add Ownership and Compliance Controls Before Scale#

Before you scale, turn ownership and compliance into explicit pre-release controls, not after-the-fact cleanup. The source material for this section does not define wire-transfer For Further Credit routing rules, so use it as a governance signal, not a payment-format specification.

Treat this as an operating standard: define what must be true before release, what triggers review, and what evidence must be attached to the case. Keep those rules stable enough that different reviewers reach the same decision on the same facts.

Stop on identity divergence#

If your own policy requires ownership alignment, treat a beneficiary-to-account-owner divergence as a review case, not an auto-release case. Route it with the full case context attached so the decision is explainable later.

Make system behavior match policy#

Your retry and blocking behavior should follow policy boundaries, not ad hoc judgment. In practice, that means clearly separating operational failures from policy/control failures and handling each path consistently.

Keep the audit trail tied together#

Keep one decision trail that links the payout request, review outcome, provider response identifiers, and final posting status. That matches the governance pattern reflected in the source material: formal oversight (including a Financial Audit Committee), independent external financial audit, and documented regulatory filing discipline.

Handle Failures Without Creating Duplicate or Orphaned Funds#

When a payment outcome is unclear, treat the case as an investigation and pause retries until status is confirmed. The fastest way to create duplicates is to resend before you can prove what happened to the first transfer.

The available source material does not provide wire-specific failure codes, root-cause rules, or a mandated retry sequence, so treat this section as an internal control pattern, not a legal or network standard. Use it to keep decisions traceable and defensible.

Run a documented close process before any resend#

| Step | Required action |

|---|---|

| 1 | Freeze retries as soon as a case is ambiguous |

| 2 | Confirm status from authoritative records, not convenience views |

| 3 | Compare what was approved with what was actually transmitted |

| 4 | Decide next action only after evidence is complete: investigate further, return, or reissue |

If records conflict or remain incomplete, keep the case open and assigned. Do not treat uncertainty as permission to resend.

Use authoritative records to close the case#

The sources reinforce one operating principle: non-official views are not substitutes for official records, and results should be verified against the authoritative edition. Apply that same discipline in payments operations: close cases from system-of-record evidence and a defined closing procedure, not from partial status labels or fragmented screenshots.

Related reading: How to verify a European VAT number using the VIES system.

Assign Clear Ownership Across Product Ops and Engineering#

In FFC workflows, unclear ownership is usually what slows resolution when a wire fails between initial receipt and final beneficiary credit. The practical fix is to assign one accountable owner to each operational artifact and each failure queue, with a clear escalation path if ownership is disputed.

Split ownership by decision type#

You do not need a universal Product/Ops/Engineering model, but you do need a deliberate one.

| Function | Responsibility |

|---|---|

| Product | Defines the payout data contract, including required vs optional fields before release |

| Ops | Validates real-world bank instructions for the specific For Further Credit flow |

| Engineering | Enforces schema validation, queue and retry behavior, and controlled change management for wire configuration |

Assign one owner per critical artifact#

| Artifact | Primary accountability | What to verify |

|---|---|---|

| Intake form schema | Field requirements and validation rules | IBAN format checks use a current country reference, and BIC/SWIFT is constrained to 8 to 11 characters |

| Exception queue | Triage, escalation, and case state discipline | Each case has one owner, a current status, and an ongoing mitigation record |

| Reconciliation report | End-to-end outcome visibility | You can trace request, provider response, and whether funds were credited, held, returned, or still under investigation |

If your team cannot quickly name who approves schema changes and who clears bank-instruction exceptions, ownership is still too diffuse.

Add launch checkpoints before scale#

Run UAT in a simulated operational setting with realistic international wire scenarios, including failure simulations, so users validate the workflow before volume arrives. Then confirm support sign-off on the runbook so teams know what evidence to collect, who to escalate to, and when a case stays in investigation instead of being resent.

We covered this in detail in How to Get a CPF Number in Brazil as a Foreigner.

Confirm Country and Program Variance Before You Publish Instructions#

Publish FFC instructions as market- and program-specific guidance, not one global template. Treat the instructions as versioned operational content tied to a defined country scope, program setup, and account configuration.

| Check | What to confirm |

|---|---|

| Country and program | Confirm the exact country and program where the instruction is supported |

| Legal entity | Verify which legal entity owns the main or intermediary account in that market |

| Canada flows | Check whether your ownership evidence pack should include the correct entity records, including a Business Number (BN), where relevant |

| Field labels | Confirm customer-facing field labels match the enabled product variant, not a reused generic label |

| Effective date and approver | Record the effective date and approver for the published instruction set |

This is a control issue, not paperwork. Governance documents in other regulated programs use explicit roles, controls, and versioned guidance, and those versions change over time. If guidance can move from Version 1 (April 1, 2024) to Version 2 (September 30, 2025), your own published instructions can drift too.

Before launch, run one shared verification pass using that checklist so Ops, Compliance, and Engineering are working from the same current instruction set.

Also review adjacent architecture options. Where supported and when enabled, assess whether Virtual Account Numbers change how much manual FFC handling you need for inbound flows; coverage varies by market/program.

Use cautious customer-facing language: "where supported," "when enabled," and "coverage varies by market/program." For Canada entity-record context, see How to Register for a Business Number (BN) in Canada.

Use FFC Only When It Solves a Real Routing Constraint#

Given the approved sources for this section, the safe takeaway is narrow: do not treat acronym matches as payment-routing guidance. In these sources, "FFC" appears in non-payments contexts (network failure recovery), and the other excerpt is about microgrid feeder flow control.

So for payment implementation decisions, pause before you lock field design, ops rules, or launch checklists based on secondary sources alone. Use payment-specific, current written instructions from the receiving provider or bank as the deciding input, not generic search hits.

Use this quick gate before launch discussions:

- Confirm your evidence is payment-routing documentation, not unrelated technical material.

- Reject acronym-only matches as a basis for product or ops requirements.

- Align product, ops, and engineering only after you have live payment instructions that clearly support the flow.

Need the full breakdown? Read How to Get a SIREN/SIRET Number as a Freelancer in France.

Frequently Asked Questions

Is an FFC account number the same thing as a final beneficiary account number?

Not always. In an FFC flow, funds are routed to a primary or intermediary account first and then credited to the final recipient, so the final beneficiary account identifier is often part of that further-credit instruction. The catch is labeling: one bank or platform may call it an FFC field, while another frames it as final beneficiary details. Always verify against the recipient’s current written instructions.

What details are required to send a wire transfer with For Further Credit instructions?

You need enough information for both stages of the route: the bank or intermediary receiving the wire first, and the final recipient details used for onward crediting. In one contractor-withdrawal flow, the required setup includes the recipient’s full name, country, and currency, plus documentation such as a statement or confirmation letter showing the funds will be credited to an account under the contractor’s name. If you cannot produce that ownership evidence, do not release the transfer yet.

When is FFC mandatory, and when should we use direct beneficiary routing instead?

Treat FFC as required when the recipient’s setup centralizes incoming transfers to a primary account before distributing them to individual accounts. If the recipient can accept direct beneficiary credit and their instructions do not require an intermediary account, use direct routing.

Can we use FFC on an international wire transfer in all countries?

FFC can be used on international wire transfers, but support depends on the recipient’s routing setup and can vary by country, provider, and program. Treat “where supported” as the rule, and confirm the live instruction set before publishing or initiating payments.

Why do FFC transfers fail even when bank details look correct?

A transfer can reach the primary account and still fail to post onward if the further-credit instruction is incomplete or does not match the final-recipient details required for posting. Your checkpoint is not just “did the wire move,” but “did the intermediary have enough exact beneficiary data to map it correctly.” If posting is unclear, treat it as a trace case rather than resending and risking duplicates.

Are third-party account payouts allowed in FFC contractor withdrawal flows?

Do not assume they are. In Deel’s contractor withdrawal flow, withdrawals to third-party accounts are not supported, and the user must upload proof that the destination account is under the contractor’s own name. Deel also states its team will verify ownership and respond within 24 hours. That is a useful reminder to build a manual review step before approval.

Which identifier should we prioritize for cross-border routing, IBAN or SWIFT code?

There is no universal winner. Use the identifiers the receiving institution asks for, and collect both where applicable rather than guessing which one matters more for a given corridor. If your team needs a quick refresher on the difference, see What is an IBAN and How is it Different from a SWIFT Code?.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- congress.gov/118/chrg/CHRG-118hhrg55834/CHRG-118hhrg55834...trusted

- csrc.nist.gov/csrc/media/Projects/cryptographic-module-val...trusted

- energy.gov/sites/default/files/2023-07/cwh-ecs-fr_2.pdftrusted

- energy.gov/sites/default/files/2022-06/res-furnaces-ecs...trusted

- federalregister.gov/documents/2024/01/19/2023-28976/energy-conse...trusted

- federalregister.gov/documents/2022/07/07/2022-13108/energy-conse...trusted

- fema.gov/sites/default/files/documents/fema_iappg-1.1...trusted

- fresno.courts.ca.gov/system/files/local-rules/january-2024-040824...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

What is an IBAN and How is it Different from a SWIFT Code?

For people handling high-stakes international payments, uncertainty is expensive. Not knowing whether a wire will arrive on time, or at all, pulls attention away from the work and adds avoidable risk. The fix is not another generic template. It is a repeatable process that tells you which details matter, where to get them, and how to check them before money moves.

How to Register for a Business Number (BN) in Canada

--- Getting control of your operation starts with the right question: not whether you might eventually need a Canadian Business Number, but when it becomes worth setting up. This is less about bureaucracy than about operating cleanly, reducing onboarding friction, and avoiding rushed compliance work later.

When Virtual Account Numbers Protect Freelancer Bank Details

If your goal is to protect freelancer payout bank details, focus on the receiving bank detail, not card-masking tools. In practice, the question is whether to give payers a purpose-built receiving detail, often a virtual bank account number, instead of exposing the underlying account behind your payout setup.