Quick Answer

Track each foreign account’s highest balance in its own currency, convert each peak using Treasury’s last-day-of-year reporting rate, then add the USD results to test whether your combined accounts crossed $10,000. File only after that combined check, using FinCEN Form 114. This prevents low December balances from masking short-lived spikes that still count toward FBAR reporting.

Why 'Checking Your Statements' Is a Flawed Strategy for a Business-of-One#

If you rely on December statements alone, you can miss the number FBAR actually cares about: each account's maximum value during the year. The filing test is based on whether the aggregate value of your foreign financial accounts exceeded $10,000 at any time during the calendar year, not on whether year-end balances look low.

For a business-of-one, risk often comes from money moving across systems. You might move funds between foreign bank accounts, brokerage accounts, and mutual funds over the year. The problem is visibility across separate timelines and statements, not just account count. Whether an account produced taxable income also does not determine FBAR relevance.

The common failure pattern is simple. Money comes in, money moves out quickly, year-end balances look modest, and the true peak gets missed. For example, a client payment lands on Monday, you distribute most of it by Wednesday, and by December the balance is small. That December balance may be accurate, but it may not be the maximum value you need for reporting. It can also hide aggregate exposure across your other accounts.

Guidance allows reliance on periodic statements issued at least quarterly for maximum-value determination, but only when those statements fairly reflect the true maximum. In fast-moving accounts, peaks can happen between statement dates. A practical rule is to record the peak balance in the account's native currency whenever a large inflow lands or you make a major transfer sweep, then keep the supporting record.

| Approach | What you track | What it often misses | Operational outcome |

|---|---|---|---|

| Statement-only approach | Year-end or occasional statements across providers | Short-lived in-year peaks and combined exposure across accounts | You reconstruct balances later from scattered records |

| Ongoing peak-tracking approach | Highest observed balance for each account as activity happens | Fewer missed peaks because you log when movement occurs | You already have core values and support when filing FinCEN Form 114 |

The tradeoff is straightforward. Spend a few minutes tracking during the year, or spend much longer reconstructing later. Ongoing tracking gives you a cleaner record of maximum values and a clearer view of whether your aggregate exposure crossed the FBAR line.

If you want a deeper dive, read Portugal's NHR Regime vs. Spain's Beckham Law: A 2025 Tax Analysis for High-Earning US Expats.

Step 1: Establish Your Proactive FBAR Monitoring System#

Treat FBAR tracking as part of your operating routine, not a year-end cleanup. The goal is simple: track each account separately and keep its highest value in that account's own currency during the year.

Build your tracker once#

Use one row per account. That gives you a simple audit trail and keeps each peak tied to one place.

| Account identifier | Institution country | Account type/platform | Base currency | Highest observed balance | Evidence note |

|---|

These are working fields for your records, not required FBAR form fields.

Run a repeatable cadence#

The right cadence is the one you can actually sustain. Match it to account activity so you catch new highs without turning this into busywork.

- Review activity in each foreign account.

- If you see a new high, update

Highest observed balance. - Record where that value came from in

Evidence note(statement, transaction view, export, or screenshot). - If there is no new high, leave the row unchanged.

Periodic statements are acceptable only when they fairly reflect the true yearly maximum. In fast-moving accounts, statement-only review can miss short-lived peaks.

| Approach | Effort | Potential error risk | Visibility across accounts |

|---|---|---|---|

| Reactive statement review | Low now, higher at filing | Can be higher | Fragmented |

| Early tracker | Small recurring effort | Can be lower | Centralized |

Keep values in native currency until filing prep#

Do not convert balances while you are monitoring. Track them in each account's base currency during the year, then convert at filing prep using the Treasury Financial Management Service rate under the year-end conversion rules. If that rate is unavailable, use another verifiable rate and document its source. Add this note at the top of your tracker: Year-end conversion source: document the source and access date during filing prep.

Add threshold labels and an early-warning buffer#

A small setup step here saves hesitation later. Put the filing threshold and your own buffer in plain view so you are not guessing when activity picks up. At the top of your sheet, add:

- Filing trigger: confirm current-year threshold before filing

- Internal early-warning buffer: set by your team

Current guidance says FBAR filing is required when aggregate maximum account values exceed $10,000 at any point in the year. Your internal buffer is there for earlier visibility before you reach that line.

You might also find this useful: Choosing a US Bank Account Path as a Foreign Founder.

Step 2: The Bulletproof Method for Calculating Maximum Value#

Follow the same order every time. Lock each account's highest in-period balance in its own currency. Then convert each peak to USD with one year-end Treasury method, and test filing at the combined-account level.

If you start with USD statements, mixed exchange-rate methods, or a running grand total, you can miss true peaks and make the conversion trail harder to defend later. Once your monitoring is in place, this valuation step becomes mechanical.

1. Lock the highest balance for each account#

Work one account at a time. Determine the maximum value in that account's own currency first, using a reasonable approximation of its highest value during the year, not a year-end snapshot.

Treat short-lived spikes as real peaks when your records show them. Example: EUR 14,500 lands in your foreign platform balance mid-day, then you convert or transfer most of it a few hours later. Even if month-end shows much less, that temporary high can still be your maximum value.

For each tracker row, keep one clear proof point for the peak. Periodic statements can work if they fairly reflect the year's high and are issued at least quarterly. Fast-moving accounts may need transaction exports, balance-history views, or screenshots to support the true maximum.

2. Convert each peak with one year-end Treasury source#

After you lock native-currency peaks, convert each one to USD using the exchange rate on the last day of the calendar year. Use Treasury Reporting Rates of Exchange as your standard method.

| Method or source | How to use it | Note |

|---|---|---|

| Treasury Reporting Rates of Exchange | Use as the standard method | Use the last-day-of-calendar-year rate and record the source table and access date |

| Another verifiable rate | Use only if a Treasury rate is unavailable | Document the source |

| Transaction-date rates | Do not combine with Treasury year-end reporting rates in the same calculation | Do not mix methods |

| Income-tax average-rate methods | Do not combine with Treasury year-end reporting rates in the same calculation | Do not mix methods |

To keep it consistent:

- Pull the reporting-year Treasury rate for each relevant currency.

- Apply that year-end rate to every account maximum for that filing year.

- Record the exact source table and access date in your tracker.

Do not mix methods. If you use Treasury year-end reporting rates for FBAR conversion, do not combine that with transaction-date rates or income-tax average-rate methods in the same calculation.

3. Test filing at the combined-account level#

The filing call comes only after all account peaks are in USD. Add the maximum values and compare the total against the FBAR aggregate filing trigger: $10,000 at any time during the calendar year. Make one combined-account determination. Do not make isolated pass/fail calls by account and stop there.

Keep this boundary clear too. Whether an account produced taxable income does not determine whether it is a foreign financial account for FBAR purposes.

4. Classify edge-case accounts before including or excluding them#

Edge cases are where people tend to over-assume or under-report. Use a two-part check: first account location, then financial interest or signature or other authority.

| Account type | Likely reportable | Why | What to verify |

|---|---|---|---|

| Traditional foreign bank or brokerage account | Usually yes | Foreign bank, brokerage, and mutual-fund type accounts are standard FBAR examples when the institution is outside the U.S. | Institution location, legal account holder, account classification in provider records |

| Fintech wallet or multi-currency platform balance | Depends | Reportability turns on where the financial institution is located and how the account is structured | Provider entity, account location, named holder vs pooled structure, current product terms |

| Employer or payments-platform balance | Depends | Scope can include signature or other authority, not only ownership | Your authority to direct funds, account owner, whether access is payout-only or true account control |

| Foreign exchange or multi-currency account | Depends | Location matters, but treatment can depend on legal account structure | Single account vs sub-account structure, provider documentation, treatment to confirm against current guidance |

For modern scenarios, use this checklist:

- If the institution is outside the U.S., treat that as a reportability signal worth verifying.

- If you can direct transfers or control disposition of funds, do not assume "not my account" ends the analysis.

- For a virtual-currency-only foreign account, current IRS reference text says it is not reportable at this time, but verify current-year guidance before deciding treatment.

- If that same foreign account also holds other reportable assets, do not apply a virtual-currency-only assumption.

By filing time, you want a clean chain: a documented peak for each account, matching evidence, one year-end Treasury conversion method, and one combined USD total.

Related: A Guide to the 'Foreign Bank Account Reporting' (FBAR) for a US LLC with a foreign owner. Before you move to filing, you can also use the FBAR Calculator.

Step 3: Execute Your Calm and Confident Filing Plan#

At this point, filing should mostly be a transfer of validated numbers into the form, not a fresh round of calculations. If your monitoring and valuation work is solid, the filing step stays orderly.

1. Submit through the right channel#

Your FBAR is FinCEN Form 114, filed through the FinCEN BSA E-Filing system. Before you submit, check:

- Confirm you entered each account separately, even when the filing trigger came from the combined total exceeding $10,000.

- Confirm each maximum value is in whole U.S. dollars. Example: $15,265.25 becomes $15,266. If a computed value is negative, enter 0 in Item 15.

- Confirm your exchange-rate source is documented, including any alternate verifiable rate used when a Treasury rate was unavailable.

- Confirm required fields are complete before submitting. Missing required elements can cause rejection.

If you have fewer than 25 accounts and truly cannot determine whether aggregate maximum values exceeded the threshold, FinCEN instructions allow the "amount unknown" box in Item 15a.

2. Work backward from the verified deadline#

Do not wait until the due date to discover you are missing a value, a source note, or a rejected submission. Verify live filing timing first, then set your internal schedule.

| Checkpoint | What to verify | Note |

|---|---|---|

| Standard due date | April 15 following the calendar year reported | Verify live filing timing first |

| Automatic extension | October 15 | No separate extension request required |

| Disaster relief review | Check whether current disaster relief notices provide any further extension | Verify current timing before setting your internal schedule |

Use these checkpoints in your checklist:

- Standard FBAR due date: April 15 following the calendar year reported.

- Automatic extension: October 15 (no separate extension request required).

- Check whether current disaster relief notices provide any further extension.

After you verify current timing, set three internal milestones. Lock accounts and USD values first. Review entries against your tracker next. Then submit early enough to fix any rejection without deadline pressure. After filing, keep the submission confirmation. If you do not have confirmation, treat the filing as incomplete.

3. Keep penalties in context#

Penalty discussion matters, but it helps only if it changes how you work. The practical point is that a consistent process helps you explain good-faith compliance.

| Violation type | General meaning | Current civil penalty reference | What your records help show |

|---|---|---|---|

| Non-willful | Generally used for failures without intentional concealment | Verify the current non-willful penalty amount or rule | A consistent process for account tracking, peak-value calculation, and conversion |

| Willful | Generally used for intentional non-filing or reckless disregard | Verify the current willful penalty amount or rule | That you had a documented process and can explain what you reported and why |

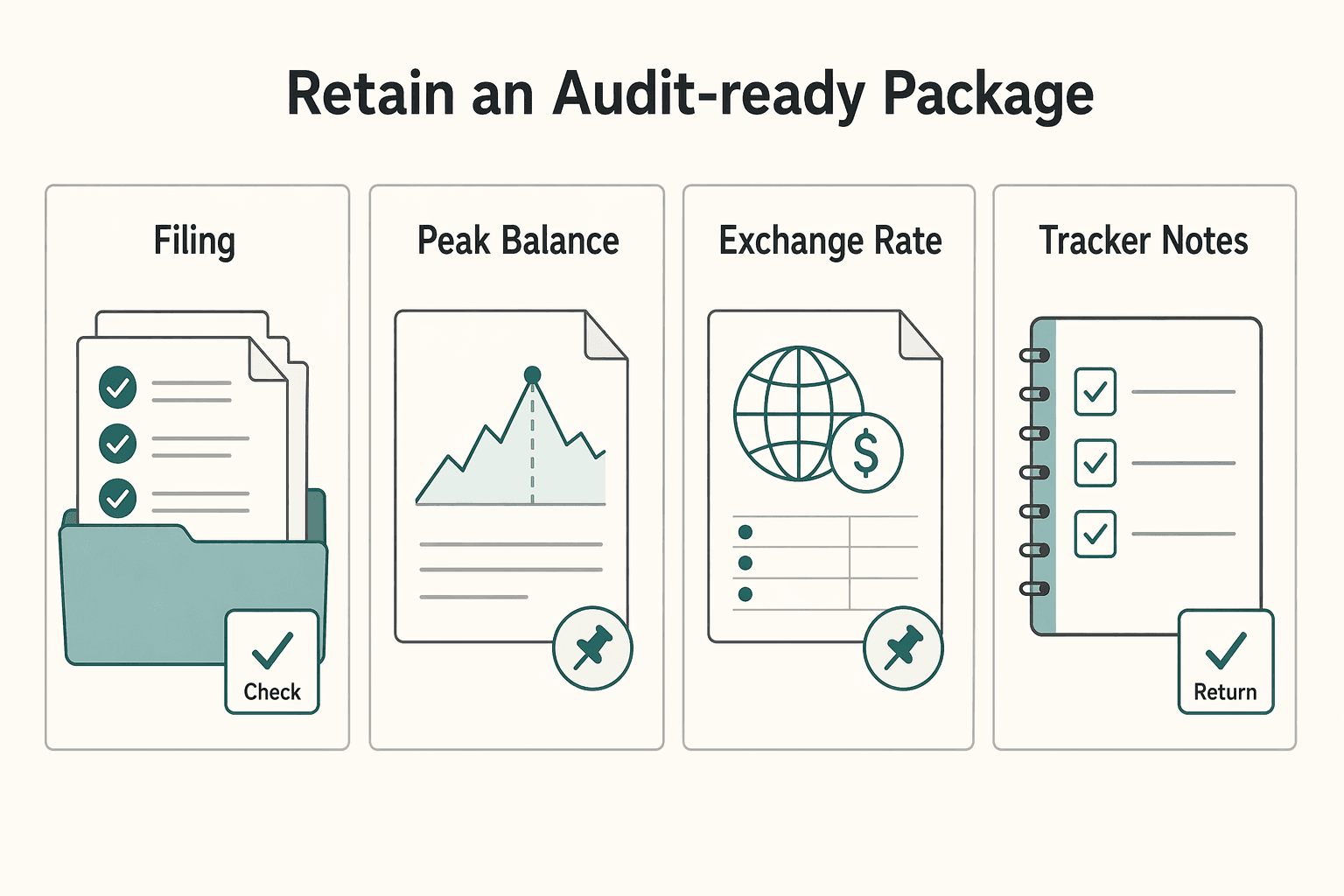

4. Retain an audit-ready package#

Do not scatter support across inboxes, screenshot folders, and old exports. Keep one organized filing-year package for reported accounts.

| Package item | What to keep |

|---|---|

| Account identifiers and institution details | The identifiers and institution details used in your filing |

| Peak-balance support | Statements, exports, and screenshots |

| Exchange-rate support | Exchange-rate support and source notes |

| Tracker notes | How you selected each maximum value |

| Submission confirmation | Final BSA E-Filing submission confirmation |

Your package can include:

- account identifiers and institution details used in your filing

- peak-balance support (statements, exports, screenshots)

- exchange-rate support and source notes

- tracker notes for how you selected each maximum value

- final BSA E-Filing submission confirmation

This is the package that lets you show exactly how the filing was prepared. If you want a field-by-field walkthrough next, use A Step-by-Step Guide to Filling Out the FBAR (FinCEN Form 114).

We covered this in detail in A guide to the Foreign Account Tax Compliance Act (FATCA) for individuals.

From Compliance Anxiety to Financial Control#

The point of this process is not paperwork for its own sake. It gives you better visibility, fewer deadline surprises, and a filing record you can explain without rebuilding your year from scratch.

Run this as a repeatable control loop, not a year-end memory exercise. When you follow Monitor, Value, File consistently, you reduce the chance of missing a peak balance. You also reduce the odds of a last-minute correction scramble that disrupts client work and cashflow planning.

Step 1. Monitor#

Use a review rhythm that matches account activity as an operational choice. Weekly may fit high-activity accounts, while monthly may be enough for lower-activity ones. Track each foreign financial account separately in its own currency, and record the highest balance you can verify since your last check. Use statements only when they fairly reflect the calendar-year high. If they do not, pull transaction history or exports so short-lived spikes are captured.

Step 2. Value#

Before filing, confirm each account's maximum account value as a reasonable approximation of its greatest value during the calendar year. Convert that peak to U.S. dollars using the Treasury rate for the last day of the calendar year, then round up to the next whole U.S. dollar. If no Treasury rate is available, use another verifiable rate and keep the source.

Step 3. File#

Apply the threshold test after each account is valued separately. If the aggregate maximum value exceeded $10,000 at any time during the calendar year, file FBAR on FinCEN Form 114. The due date is April 15 with an automatic extension to October 15. Keep peak-balance support, exchange-rate support, calculation notes, and filing confirmation together. If you have fewer than 25 accounts and genuinely cannot determine whether the aggregate exceeded the threshold, use Item 15a.

| Habit | Reactive scramble | Controlled system |

|---|---|---|

| Peak capture | Relies on memory or year-end snapshots | Uses recurring checks and pulls history when statements miss spikes |

| Threshold check | Done late after balances are mixed together | Done after each account is valued separately |

| Filing prep | Rebuilds support under deadline pressure | Maintains support as you go |

This is the operational payoff: fewer deadline disruptions, steadier cashflow decisions, and more confidence in your reporting process. For execution details, use the filing section above, and verify current filing rules, relief notices, and penalty details before submission.

For related reading, see The Best Debit Cards with No Foreign Transaction Fees.

If you want one workflow for getting paid globally with traceable records and compliance gates where supported, talk to Gruv to confirm fit for your setup.

Frequently Asked Questions

How do I calculate the maximum value when I have accounts in different currencies?

Calculate each account separately in its native currency first. Identify a reasonable approximation of that account’s highest value during the calendar year, then convert that single peak to U.S. dollars using Treasury’s rate for the last day of the calendar year and round up to the next whole U.S. dollar. If no Treasury rate is available, use another verifiable rate and keep the source.

Does a temporary balance spike count if it only lasted a day or less?

Yes. Your maximum value is the highest point reached during the year, not just month-end or year-end balances. You can rely on periodic statements only if they fairly reflect the true maximum, so use records that capture the true peak when they do not.

Do I have to file if no single account was over $10,000?

Maybe. Run the aggregate test after valuing each account separately. If the combined maximum values exceed $10,000 at any time during the calendar year, you must file. If you have fewer than 25 accounts and genuinely cannot determine whether the aggregate exceeded the threshold, use Item 15a (“amount unknown”) as the fallback path.

What happens if I make an accidental FBAR mistake?

This grounding does not establish specific penalty amounts or detailed correction procedures. Verify current IRS/FinCEN correction instructions before you act. For filing timing, FBAR is due April 15, with an automatic extension to October 15.

What types of accounts are considered foreign financial accounts for FBAR purposes?

Start with location. Accounts at financial institutions outside the United States are generally foreign financial accounts for FBAR purposes. Do not use taxable-income status as your exclusion test. The IRS exception list also includes accounts held in an IRA of which you are an owner or beneficiary. If you are still unsure, verify the current rule for that account type.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- apps.irs.gov/pub/epostcard/cor/331025119_201912_990_20210...trusted

- bsaefiling.fincen.gov/docs/XMLUserGuide_FinCENFBAR.pdftrusted

- congress.gov/115/chrg/CHRG-115hhrg30893/CHRG-115hhrg30893...trusted

- fincen.gov/reporting-maximum-account-valuetrusted

- fincen.gov/report-foreign-bank-and-financial-accountstrusted

- fiscaldata.treasury.gov/datasets/treasury-reporting-rates-exchangetrusted

- irs.gov/businesses/small-businesses-self-employed/re...trusted

- irs.gov/newsroom/details-on-reporting-foreign-bank-a...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Portugal NHR vs Spain Beckham Law for High-Earning US Expats in 2026

Start with documentation, not tax projections. In the portugal nhr vs spain beckham law decision, the safer first move is to choose the path you can prove from end to end before you optimize for headline outcomes.

How to Fill Out FBAR (FinCEN Form 114) Step by Step

The cleanest way to handle FBAR is to decide whether it applies, then file through the right channel with the right records in hand. Treat it as a separate annual compliance task, not as part of your income tax return process.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.