Quick Answer

Add FFC instructions by entering both the first receiving account and the final credit destination exactly as the recipient's written wire instructions show. There is no universal bank field layout, so confirm label mapping, any intermediary or correspondent details, and route requirements in writing. If any account path or beneficiary wording is unclear, pause and confirm before submission.

Add FFC Instructions Right the First Time#

The goal is first-pass accuracy: enter FFC wire instructions so funds reach the final account after the initial routing leg without avoidable rework.

Confirm that you are handling an FFC routing flow. FFC means funds go to an organization's central account first, then get allocated to the intended person or sub-account. That main account may sit at an intermediary or correspondent bank. The FFC instruction tells the receiving side where the money should finally land.

Because FFC includes a final credit destination, entering only the first account is not enough. Brokerage funding is one common example of this pattern.

Use this guide as an execution checklist. Focus on accurate field entry and resolving unclear details before submission. International wires are in scope, so do not treat FFC as domestic-only.

Collect complete instructions before entry. Before you enter anything, gather the full payment details from the receiving organization. You should be able to clearly identify both:

- The initial receiving account

- The ultimate credit destination

If the instructions include handling details, such as conversion to USD before final deposit, keep that instruction attached to the payment request. Reviewers should be able to validate each entered value against the source. If any account path or beneficiary wording is unclear, pause and confirm before submission.

Account for bank and rail limits early. Bank UI labels and required fields vary by institution and account type, so do not assume there is one universal FFC field layout. If details are unclear or unavailable, treat that as an unknown to resolve, not something to guess.

Also confirm that your rail supports FFC before you begin. Wise states that it does not process FFC wires, even though it supports transfers to 80+ countries in 50+ currencies through other routes.

If you want a deeper dive, read A Guide to the 'For Further Credit' (FFC) Instruction in Wire Transfers.

FFC in One Minute for Payments Operators#

Use this as a validation gate, not a field-entry recipe.

| Reference | Context | Grounded detail |

|---|---|---|

| Wire instructions | Payment-field entry | Confirm the document is actually about wire instructions before release |

| FFC Bucks | Services at FFC | Two days processing; 30-day expiration |

| FFC Connect | Plan pricing | $109.95/month |

Confirm the document is actually about wire instructions. "FFC" can refer to unrelated items here, including FFC Bucks, used for services at FFC with two days processing and a 30-day expiration, and FFC Connect, listed at $109.95/month. If the document is discussing service purchases, plan pricing, or expiration rules, stop and do not use it for payment-field entry.

Require written, exact instruction text before release. Do not infer meaning from acronym familiarity, memory, or prior payouts. If labels are present, require the receiving side to provide the exact wording to use and a clear mapping for each value before submission.

Treat low-authority sources as a risk signal. A community forum may indicate confusion, but it is not an institutional operations manual. Use it as a warning that acronym collisions happen, not as authority for mapping, controls, or validation logic.

One-minute takeaway: first verify that "FFC" is being used in a true wire-instruction context. Then verify each required label and value mapping from current written instructions from the receiving side. If that evidence is missing, hold and escalate instead of guessing.

We covered this in detail in FFC Account Number Meaning for Wire Transfers and Further Credit Instructions.

Decide Whether This Transfer Should Use FFC at All#

Use an FFC-style setup only when the written instructions explicitly require that pattern and your selected wire route can carry it without assumptions.

First, classify the instruction pattern before anyone enters fields. If the instructions show a single beneficiary account and name path, treat it as a one-leg beneficiary wire and do not add extra crediting fields. If they show separate institution-level and beneficiary details, pause and get explicit written mapping for each value.

Next, treat SWIFT Code and IBAN as routing identifiers, not proof that an intermediary leg is required. Release only when the receiving instructions explicitly confirm whether an intermediary or correspondent step is part of the payment path.

For Wise, separate confirmed wire context from unconfirmed field behavior. Wise distinguishes "Receiving domestic payments (non-Swift / non-wire)" from "Receiving USD wire and Swift payments." Its send flow includes "Paying with Wire transfer," and it lists fixed receiving fees such as 6.11 USD for USD wire/Swift payments. It also warns that additional Swift fees may apply when sending euros outside the SEPA region. That confirms wire and Swift usage, but require written confirmation if your payout depends on FFC-specific field capture.

Hold if the instruction labels, names, or account references do not line up cleanly in the same document. Submit only when each value has an unambiguous destination in the provided instruction format.

For a step-by-step walkthrough, see FFC vs FBO vs FAO Wire Transfer Instructions for Platform Teams.

Gather the Exact Inputs Before Opening Your Bank Portal#

Get the source under control before anyone touches the portal. If a wire detail is missing, treat it as unknown until it is confirmed in writing.

Use one controlling source document for entry. Do not key from chat, memory, or mixed snippets. If details conflict across documents, pause and request one reconciled written version before proceeding. If you start from an informational posting, for example FederalRegister.gov, verify against the linked official govinfo PDF before treating it as controlling.

Build one intake packet from that source document only. Include only the exact instruction text you plan to submit. A raw copy plus an entry-ready copy can help keep preparation and entry separate. Bank-specific wire field requirements are not established here, so treat portal-specific fields as unknown unless your official instructions cover them.

Flag unknowns before submission, not during entry. If your portal asks for a value the instructions do not provide, hold the transfer and get written clarification instead of inferring what belongs there.

Set clear internal ownership. If your team uses review controls, separate preparation, approval, and technical validation where practical. This is an internal control choice, not a universal banking rule.

Enter Wire Fields in the Order Banks Actually Validate Them#

Treat wire entry as a party chain, not a set of disconnected boxes, and keep For Credit To and For Final Credit To distinct when both appear in the instructions.

Map the payment chain before you type#

Before opening the portal, restate the payment path from your approved source document. For U.S.-dollar cross-border Fedwire examples, routing data covers three entities: intermediary financial institution, if any, beneficiary's financial institution, and beneficiary.

Use this as an entry discipline when your instructions include an FFC-style flow. It is a practical checklist, not a universal bank validation order.

| Checklist step | Canonical field | What belongs here | Pattern references only | Validation checkpoint |

|---|---|---|---|---|

| 1 | Intermediary FI (if any) | Intermediary institution details in the payment path | Use only if your instructions include an intermediary leg | Party match: intermediary details match source exactly. ID match: required identifier type matches the route. Route match: intermediary leg aligns with stated currency/corridor. |

| 2 | Beneficiary's FI | Beneficiary institution details | Core receiving FI details from the instruction set | Party match: FI name and identifiers align. ID match: no mixed identifier types in one field. Route match: FI details fit the stated corridor. |

| 3 | Beneficiary | Final beneficiary party details | End beneficiary details exactly as instructed | Party match: beneficiary name/account align with source. Format match: keep name and account values in their intended fields. Route match: beneficiary details fit the payment route. |

| 4 | For Credit To (when present) | First receiving account in an FFC-style chain | Use when funds are directed to a central account first | Party match: first receiving account holder matches instructions. Format match: account value entered exactly as provided. Route match: account is valid for the stated route. |

| 5 | For Final Credit To (when present) | Downstream account that receives final allocation | Use when instructions provide a final-credit account | Party match: final account owner aligns with beneficiary details. Format match: enter only the instructed final account value. Route match: final credit target matches the stated route/purpose. |

| 6 | SWIFT/BIC or other required ID code | Route-required institution identifier | Include only when your corridor, correspondent path, or portal requires it | Party match: identifier belongs to the named institution. Format match: code only, no free text. Route match: identifier type matches route requirements. |

Enter the institution leg first#

Start by confirming the full party chain, then enter the institution-level details before account-level details. Treat each payment's routing context as payment-specific, not reusable by default.

Do not reuse routing details from memory. Confirm that institution details, routing identifiers, and corridor are consistent in the same instruction set. If the portal requests SWIFT but your source provides only domestic routing, stop and get written clarification.

Enter the credit chain without swapping account targets#

When both fields are present, verify from the written instructions which account receives funds first and which account receives final credit before entry.

This distinction matters in FFC structures, where funds first land in a central account and then get allocated to an individual destination account.

Checkpoint by party, not by digits: who receives first, and who should be credited finally. If your source puts both values on one line, split them into separate entry-ready lines in your packet and keep the raw source attached.

Add SWIFT only when the route requires it#

Do not force SWIFT into every wire. Use it when the route calls for it.

For foreign-currency transfers in this Fedwire cross-border context, confirm the correspondent-bank path before release, because those transfers must run through a correspondent bank. If an intermediary or correspondent appears unexpectedly, escalate before submission, since routing through a particular intermediary can have legal or compliance consequences. Include the original instructions, your field mapping, and a portal draft or screenshot so a reviewer can verify intermediary FI (if any), beneficiary's FI, and beneficiary alignment.

Translate Bank Labels Without Guessing#

Unclear portal labels are a routing issue, not a wording problem you can solve by intuition. Do not map fields by label alone.

Anchor labels to function, not wording#

Use the canonical chain from the prior step only if it is explicitly documented in your payment instructions: receiving bank, routing or SWIFT code, For Credit To, For The Benefit Of, and For Final Credit To. Then test each portal field against the written instructions line by line. Confirm, where the instructions are explicit, who receives funds first, who is the beneficiary, and which account should receive final credit.

Do not assume a field labeled "beneficiary institution account" means For Credit To, or that "recipient account" means For Final Credit To. If the instructions do not make order of receipt explicit, the mapping is unverified.

Treat free-text placement as unverified#

If the only apparent option is a memo, note, or reference box, do not treat that as confirmed routing placement. The current evidence does not establish where banks expect FFC details when dedicated fields are missing, and it does not support bank-by-bank placement rules.

If mapping remains unverified, pause release and request written clarification through your bank or receiving institution workflow before submission. If you obtain clarification, keep it with the source instructions and a screenshot of the portal field labels in the payment record.

Record unknowns directly#

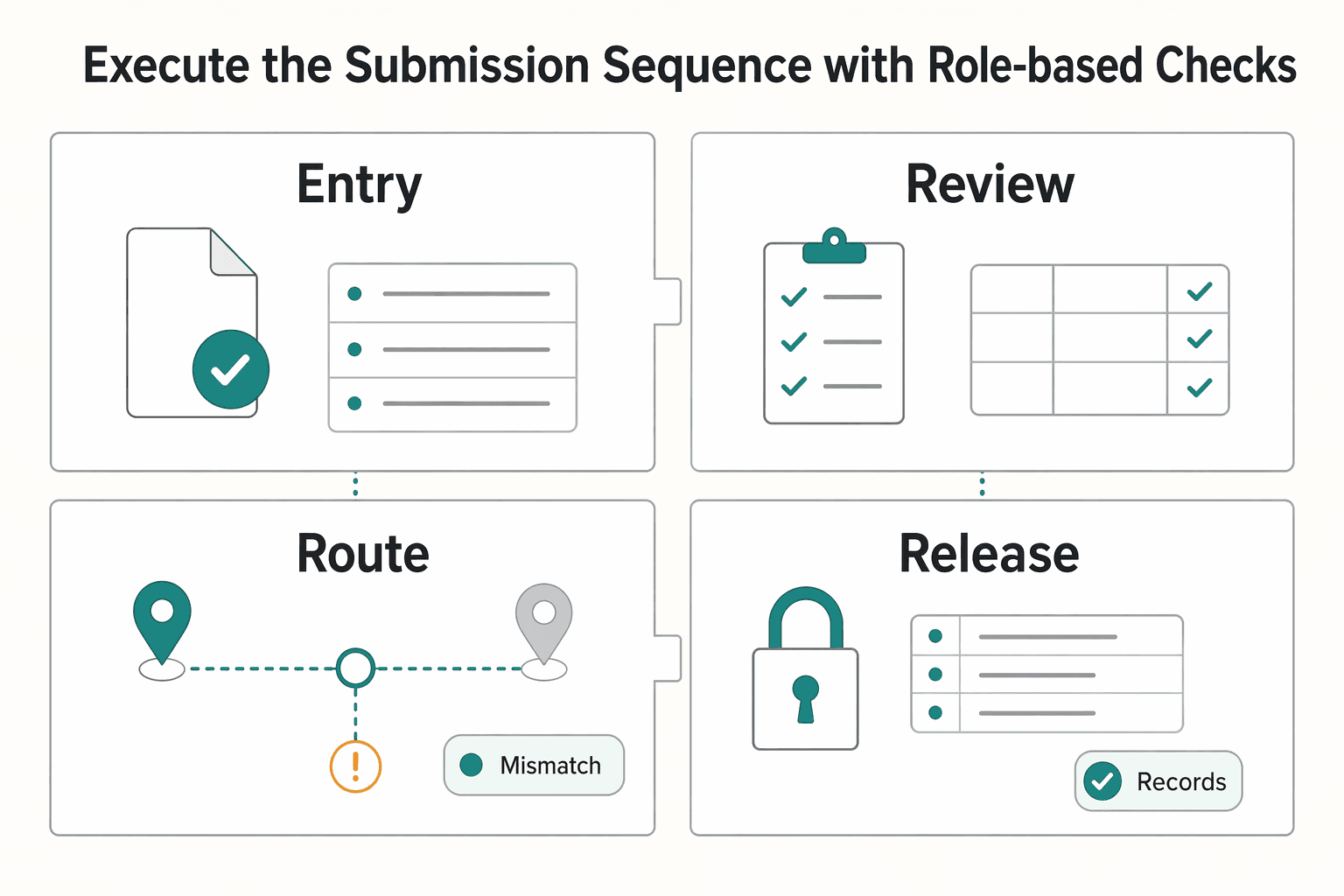

Execute the Submission Sequence With Role-Based Checks#

Once field mapping is verified, reduce execution risk by separating entry, review, route check, and release.

| Stage | What the section says | Example or note |

|---|---|---|

| Entry | Enter wire details from the approved instruction record, not from rewrites or old templates | Use ABA/Routing 123000848 or SWIFT Code IRVTUS3N exactly as shown |

| Review | Compare the FFC recipient details directly against the approved instructions, character for character | Hold release if anything does not match |

| Route check | Confirm that the selected route and portal fields match the instruction set | Use My Account -> Fund Transfers when that path is specified; ACH transfers initiated through the customer's bank are explicitly rejected |

| Release | If your process uses dual control, release only after both roles complete sign-off in your payment record | Attach the instruction artifact and log any reference ID returned at submission |

Enter only from the approved intake packet. Your ops team should enter wire details from the approved instruction record, not from rewrites or old templates. Input receiving or intermediary details and the routing identifier exactly as provided, then complete beneficiary identifiers without edits.

For domestic routing, use the listed ABA/Routing value, for example 123000848, exactly as shown. For international routing, use the listed SWIFT Code, for example IRVTUS3N, exactly as shown. If the instructions include account-format rules, such as account-type suffixes, preserve that formatting exactly.

Review beneficiary fields character for character. Finance review should focus on beneficiary-chain accuracy, not just bank and route fields. Compare the For Further Credit to (FFC) recipient details directly against the approved instructions, character for character, and hold release if anything does not match.

Verify submission path and route fit before release. Before submission, confirm that the selected route and portal fields match the instruction set you are executing. If the provider specifies an initiation path, use that path exactly, for example My Account -> Fund Transfers in the provided workflow.

Do not switch channels and assume instructions will carry over unchanged. In the provided example, ACH transfers initiated through the customer's bank are explicitly rejected.

Release with documented internal sign-off and trace data. If your process uses dual control, release only after both roles complete sign-off in your payment record. Attach the instruction artifact and entry evidence, then log any reference ID returned at submission so reconciliation and tracing start from a recorded reference.

Run a Pre-Submit Control Block Before Releasing Funds#

Put one final gate in front of release. If the record does not match your approved instruction artifact, pause the release.

Validate against the approved instruction artifact. Use the attached instructions as the source of truth for what must be present in the payment record. Your control should enforce only the fields explicitly listed in your approved instructions.

Handle ambiguous or altered formatting as a review stop. If values are merged, padded, broken across lines, or otherwise changed from the source artifact, stop and verify against the approved instructions before release.

Require documentation evidence in-system. Release only when the payment record includes the underlying instructions and the policy documentation your team requires. This keeps the release decision tied to the record and aligns with providers that publish formal policy artifacts and dedicated funding-instructions areas.

Treat duplicate-submit protection as an internal control choice. If retries are common, you can add an internal duplicate-submit guard before release.

If your wire process needs policy gates, idempotent retry safety, and end-to-end status visibility, see how Gruv Payouts can fit that operating model.

Diagnose and Recover Returned FFC Wires Fast#

Treat a returned wire as an evidence problem first, not a speed problem. Do not resend until you can prove what was submitted and what changed.

| Evidence item | What the section says |

|---|---|

| Return notice | Collect it in the return evidence pack and keep artifacts in their native format where possible |

| Sender or provider reference | Collect it in the return evidence pack and keep artifacts in their native format where possible |

| Approved instructions | Use them to compare the approved instruction artifact against the submitted payment record |

| Submitted record export | Collect it so another reviewer can reconstruct the failed submission without extra chat or email context |

| System audit trail showing post-approval edits | Collect it in the return evidence pack |

Freeze the failed payment and define what is known. Lock the failed transaction record before anyone edits it. Then compare the approved instruction artifact against the submitted payment record and mark only mismatches you can verify directly. If you cannot show a concrete mismatch or omission from those two records, keep the case in investigation status.

Build the return evidence pack in original form. Collect the return notice, sender or provider reference, the approved instructions, the submitted record export, and any system audit trail showing post-approval edits. Keep artifacts in their native format where possible so another reviewer can reconstruct the failed submission without extra chat or email context.

Run a requirement-by-requirement review. Verify each required item is completed, and flag blanks or incomplete entries before any resend decision. Classify gaps as MOD when a minor modification or tool-based workaround is needed, or NO when functionality is unsupported and only a process workaround exists. If the team cannot prove where the mismatch occurred, keep the case in investigation status.

Resend only after peer-reviewed correction, or escalate with full evidence. Resend only after the corrected record is peer-reviewed against both the original instructions and the failed submission. If the cause is still unproven, escalate with the full evidence pack to avoid repeated trial-and-error resubmits.

Standardize FFC Across ERP and Payout Rails#

Standardize what you can actually prove first: secure handling of sensitive instructions. Avoid forcing one canonical mapping across banks, ERPs, or payout rails.

Require official, secure channels for sensitive updates. When handling sensitive payment details, use only official, secure websites. If a government counterparty is involved, verify the .gov domain and confirm HTTPS before sharing or confirming information. If either is unclear, pause and request a secure official channel.

For Gruv-connected payout operations, keep the flow compliance-first with policy gates and audit-ready records, where enabled.

Related reading: How to Pay Contractors in India: FEMA Compliance TDS Deduction and Bank Transfer Mechanics.

Mistakes That Cause Avoidable Returns#

Bank-specific FFC return reasons are not established here, so do not treat any single field pattern as a universal cause. In this excerpt, the clearest avoidable risks are handling gaps: unclear records, vague error labeling, and weak escalation discipline.

- Turning review into guesswork instead of record-backed handling. If a reviewer cannot reconstruct what was received, what changed, and why, do not infer a return cause.

- Using vague failure notes instead of explicit categories. The grounded examples are Lost Case (LC) and Wrong Pulls in Screening (WP).

- Escalating without the named assistance artifact. The grounded escalation checkpoint is Operations Assistance Request (OAR), Form 12412.

- Applying unsupported bank-wire assumptions as policy. If written evidence is missing, pause and request clarification rather than inferring return rules.

Final Takeaway and Copy/Paste Launch Checklist#

The safest release pattern is simple: use a consistent internal field checklist, verify every entered value against written instructions, and release only after your internal approval controls are complete.

- Use one internal checklist for beneficiary and routing fields across intake, approval, and bank-entry notes.

- Check that checklist against the payee's written wire instructions every time. Do not treat UI labels as authoritative on their own.

- Compare entered values to the original instruction artifact, whether PDF or email. Treat that artifact as part of the effective payment order record.

- Verify all route fields listed in the written instructions before release.

- Attach source instruction evidence to the payment record and apply two-person approval where your policy requires it.

- Treat unexpected payment-related calls, emails, or messages as suspicious until confirmed through a known channel.

- Log the provider reference immediately after dispatch. On delays or returns, request the provider's trace or proof record right away, such as MT103 for international-wire tracing where available, or the provider's current equivalent.

- After any return, run a short postmortem on field entry, evidence handling, and approval checks, then update your internal notes before resubmitting.

If you need a quick refresher on tracing records, see What is a SWIFT MT103 and How to Use It to Trace a Wire Transfer.

When you want to pressure-test your FFC workflow against your market and program requirements, contact Gruv.

Frequently Asked Questions

What does For Further Credit (FFC) mean in a wire transfer?

FFC means funds first go to an organization's main receiving account, then get allocated to the ultimate destination account. When instructions use this structure, entering only the first account is not enough.

Where exactly do I place For Credit To versus For Final Credit To?

There is no universal field mapping across every bank or portal. Use the recipient's written instructions to confirm which account receives funds first and which account receives final credit before you submit.

Can I use FFC on an International Wire Transfer?

Yes, FFC can be used on international wires. In cross-border routes, an intermediary or correspondent bank may be part of the path, so verify the full route in writing.

Why do FFC wires get returned even when both account numbers are present?

Both account numbers may still be insufficient if required details, label mapping, or route instructions do not line up cleanly.

Can I send an FFC wire with Wise?

No. Wise states that it does not process FFC wires. If your payee requires FFC, use a provider that supports that structure.

What documents should I collect before submitting an FFC wire?

Collect the payee's written wire instructions and use one controlling source document for entry. If details conflict or a required value is missing, pause and get one reconciled written version before submission.

What is SWIFT MT103 and when should I request it?

This article does not provide a reliable definition or universal timing rule for MT103 requests. For transfer tracking, ask your sending bank what record they can provide.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- archive.legmt.gov/content/Publications/MEPA/1990/dsl0601_19900...trusted

- citydocs.dublin.ca.gov/WebLink/DocView.aspxtrusted

- dhcs.ca.gov/services/medi-cal/eligibility/Documents/Arti...trusted

- dhs.gov/termstrusted

- fcc.gov/Bureaus/Wireless/Orders/2000/fcc00366.pdftrusted

- federalregister.gov/documents/2025/11/10/2025-19815/national-emi...trusted

- federalregister.gov/documents/2024/02/15/2024-02448/corps-of-eng...trusted

- govinfo.gov/content/pkg/CHRG-112shrg73401/html/CHRG-112s...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: