Quick Answer

Build your employer cost by country benchmark from a full employer-paid stack, not headline pay. Include wages or salary, payroll taxes, social security, mandatory health insurance, mandatory pension contributions, and clearly labeled overhead, then normalize unit, period, worker type, currency, and FX basis across rows. Use explicit Unknown values for missing fields, and only treat rows as planning-ready when source links, version dates, and inclusion boundaries are documented.

Salary-only comparisons fall apart as soon as you try to tie them to real employer spend#

Salary-only comparisons fall apart as soon as you try to tie them to real employer spend. A usable employer cost by country benchmark has to include the full cost stack: wages or salary, benefits, payroll taxes, social security, and any employer-paid health insurance or pension contributions that apply in that jurisdiction.

| Component | Value | Context |

|---|---|---|

| Total compensation | $46.15 per hour | BLS private industry, 4th quarter 2025 |

| Wages and salaries | $32.36 | December 2025 split |

| Benefits | $13.79 | December 2025 split |

This is not just a modeling preference. The World Bank's labor cost definition includes wages paid to employees, the cost of employee benefits, and payroll taxes paid by an employer. If a benchmark stops at headline pay and leaves the rest to assumption, it can fail in practice. The gap can show up later in budget variance, ledger mismatches, and country comparisons that looked clean only because major cost categories were missing.

The United States shows why this matters. The Bureau of Labor Statistics tracks Employer Costs for Employee Compensation, or ECEC, as an employer cost per employee hour worked for total compensation, wages and salaries, and benefits. In the latest BLS snapshot for private industry, total compensation was $46.15 per hour in 4th quarter 2025. The December 2025 split was $32.36 for wages and salaries and $13.79 for benefits. If your benchmark uses only the wage line, you are dropping a material share of employer cost before you even start cross-country comparisons.

The same issue shows up inside the benefits bucket. BLS treats legally required benefits as employer obligations paid through payroll tax or compulsory insurance premiums, and the U.S. examples are concrete: Social Security, Medicare, federal and state unemployment insurance, and workers' compensation. That is the level of posting reality finance teams care about.

Two countries can show similar salaries while producing very different employer cost outcomes once statutory charges and compulsory programs are included. The goal is to build a benchmark you can defend. That means a country model with comparability rules, clear inclusion boundaries, and evidence attached to each row so finance, ops, and product are looking at the same cost object. One simple checkpoint helps: if a benchmark row cannot tell you the period, jurisdiction, and which employer-paid components are included, treat it as directional rather than planning-grade.

The rest of this guide is practical. You will see how to normalize country inputs, what evidence to require before a row is production-ready, and how to map benchmark assumptions into ledger and payout behavior. The standard is straightforward: a benchmark that is comparable enough for decisions and documented enough to hold up under audit.

Define the employer cost benchmark you can actually use#

Use this rule first: if a source cannot state scope and method, treat it as directional, not planning-grade. Cross-country benchmarking fails fast when one row is hourly labour cost, another is annual salary plus taxes, and another is average earnings only.

Use these terms the same way in every row:

| Term | Use it for | Minimum comparability check |

|---|---|---|

| Labour cost | Usually an hourly employer-cost measure | Same unit and period across countries |

| Total employment cost | Planning view: salary plus employer-paid add-ons | Same inclusion boundaries for employer-paid components |

| Benchmark comparability | Decision-ready comparison standard | Same scope, same period, same conversion basis |

For hourly labour cost context, Eurostat reports country variation (for example, an EU range of EUR11 to EUR55 in 2024) and splits labour costs into wages/salaries and non-wage costs. BLS also warns that compensation-based measures are more comparable than average-earnings-only data, because earnings definitions vary and can omit major labour-cost items.

Make the minimum component stack explicit in each country row:

- salary or wages

- payroll taxes

- statutory social security

- mandatory health insurance (if applicable)

- mandatory pension contributions (if applicable)

- clearly labeled employer overhead

If an item is unknown, mark it as unknown instead of blending it into a single rate. A row is planning-ready only if each component is clearly included, excluded, or estimated.

Keep a bright line between manufacturing labour-cost signals and platform hiring assumptions. BLS manufacturing hourly compensation is built for manufacturing comparisons and includes direct pay plus employer social insurance and labour-related taxes; that is not automatically the same decision object as knowledge-work hiring assumptions in the United States, United Kingdom, or Germany. If you use signals from China, India, or Mexico, keep them in manufacturing context unless you normalize them to the same employment-cost definition.

For a step-by-step walkthrough, see The Cost of Using an Employer of Record (EOR).

Normalize country data before you compare countries#

Do not compare or rank countries until each row is normalized to the same unit, period, and conversion method. Even with a solid cost stack, the benchmark is not decision-ready if those bases differ across rows.

Build a comparability table before any ranking. Treat it as a control layer: if a row cannot state worker type, sector, period, currency, foreign exchange method, and included contribution categories, it is incomplete.

Build the comparability table first#

Use these columns as mandatory, even if some cells are blank:

| Jurisdiction | Worker type | Sector | Period | Currency | Foreign exchange method | Contribution categories included |

|---|---|---|---|---|---|---|

| United States | Unknown | Unknown | Unknown | USD | Unknown | Unknown |

| Canada | Unknown | Unknown | Unknown | CAD | Unknown | Unknown |

| United Kingdom | Unknown | Unknown | Unknown | GBP | Unknown | Unknown |

| Germany | Unknown | Unknown | Unknown | EUR | Unknown | Unknown |

| EMEA representative market | Unknown | Unknown | Unknown | Unknown | Unknown | Unknown |

Use Unknown explicitly instead of relying on silent assumptions. Two fields need extra scrutiny: worker type (some datasets cover employees and self-employed workers) and foreign exchange method (period-average and end-of-period rates can produce different outputs).

Before a row is usable, confirm that you can point to the source line for each included contribution category and that the conversion basis is written down.

Do not rank mixed units#

If sources mix hourly labour cost and annual total employment cost, stop and normalize before ranking. Annual comparisons can also inherit non-comparable hours-worked assumptions, which makes cross-country level rankings unreliable.

Use one unit across all rows:

- hourly employer cost with matched scope and period, or

- annual total employment cost with matched worker type, sector, and contribution coverage

If you are between those states, keep the table unranked.

Add a recency check before every review#

Before every review, add a named recency checkpoint per region. For U.S. context, use the Employment Cost Index (ECI), which tracks change in employer hourly labor cost over time; for example, civilian workers showed 0.7% in 4th Qtr 2025. For European rows such as Germany, use Eurostat's Labour Cost Index (LCI), updated quarterly, with a 70 days post-period submission window.

Flag rows for review when period labels are missing or when the row is older than the latest available update.

PPPs can improve cross-country comparability, but they answer a different question than settlement or budgeting FX. Use PPPs for purchasing-power comparisons, not for ledger-impacting employer-spend estimates in payment currency.

Related: Average Freelance Rates by Country and Profession: Global Benchmarks 2026.

Build the country evidence pack before modeling#

A country row is not planning-ready until its evidence pack clearly shows the rule source, tax treatment, and what is included or excluded.

| Item | Article fact |

|---|---|

| W-9 | Supports TIN collection for information returns; page review date: 30-Mar-2026 |

| W-8 BEN | Submitted when requested by the withholding agent or payer |

| Form 1099-NEC | Nonemployee compensation of $600 or more is reported on Form 1099-NEC; page review date: 23-Jan-2026 |

| FBAR | Can apply when foreign financial accounts exceed the $10,000 aggregate threshold condition |

For each jurisdiction, build one source bundle that answers three questions: which statutory employer-cost components apply, how tax and social-security effects are treated, and which benefits or employer-paid items are inside or outside the number. Keep wages/salaries separate from non-wage costs such as employers' social contributions and taxes on wages, and state whether treatment is before or after cash benefits.

| Evidence item | What to capture | Why it matters |

|---|---|---|

| Statutory cost rules | Source links for wages/salaries, employers' social contributions, taxes on wages, and other mandatory employer-paid items | Prevents salary-only rows from being treated as total employment cost |

| Tax treatment notes | Whether the row reflects tax and social-security effects before or after cash benefits, plus country-specific inclusions | Avoids comparing totals built on different tax treatment |

| Inclusion/exclusion proof | Evidence for benefits, allowances, insurance, pension, or other employer-paid items included or excluded | Lets finance reconcile the modeled number to policy and ledger behavior |

Add compliance context when it is in scope for your program. AML controls can affect execution timing because customer identification procedures are part of AML compliance requirements, and legal-entity onboarding may require beneficial-owner identification and verification.

Make tax-document dependencies explicit where applicable. A W-9 supports TIN collection for information returns, W-8 BEN is submitted when requested by the withholding agent or payer, nonemployee compensation of $600 or more is reported on Form 1099-NEC, and FBAR can apply when foreign financial accounts exceed the $10,000 aggregate threshold condition.

Before marking any row production-ready, record the source links and version date, and assign clear refresh responsibility in your workflow. Page review dates are useful checkpoints, such as 30-Mar-2026 for W-9 and 23-Jan-2026 for Form 1099-NEC. For a deeper dive, read Global Contractor Payout Benchmarks by Country.

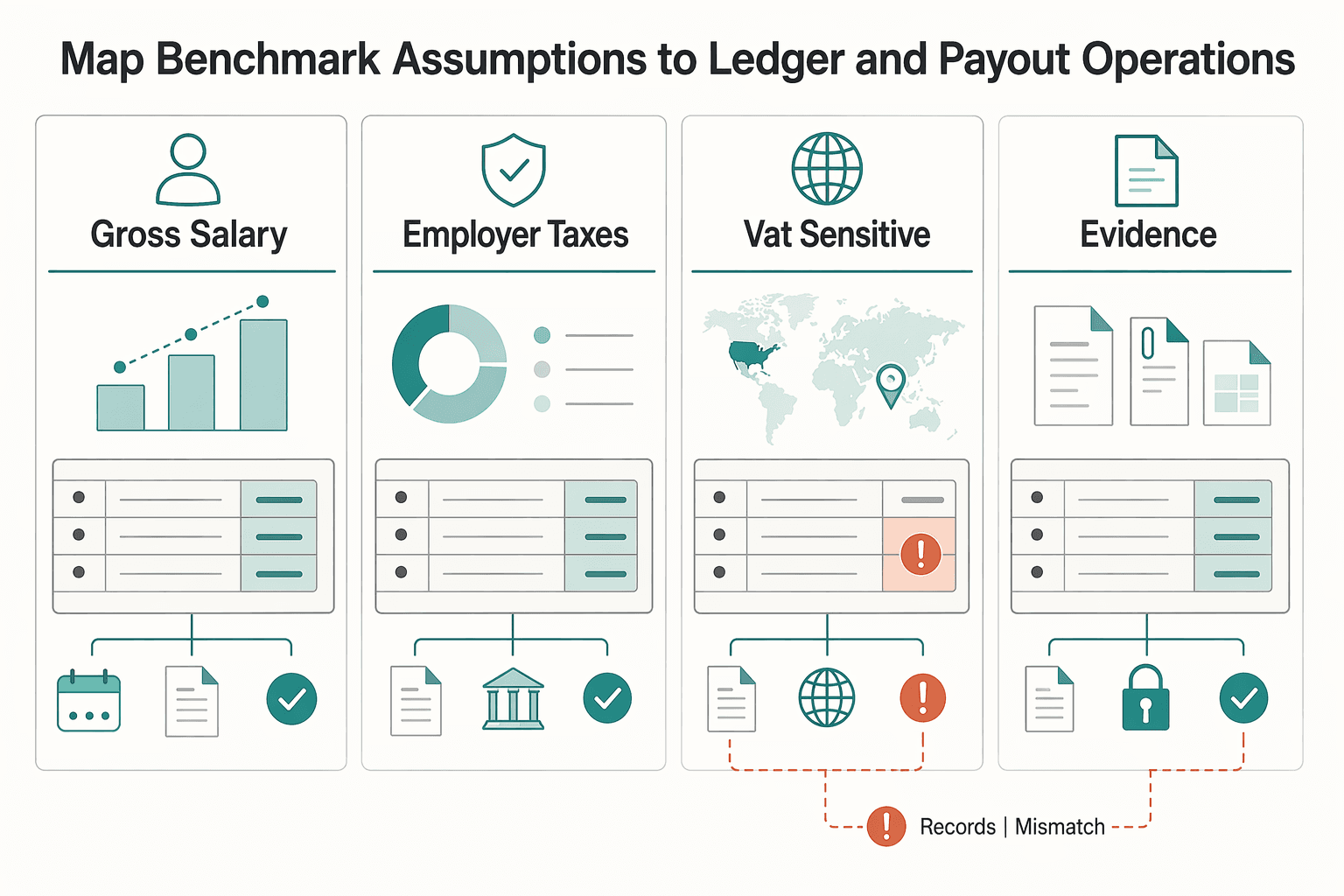

Map benchmark assumptions to ledger and payout operations#

Treat ledger postings as the accounting source of truth, and the benchmark dashboard as a derived view. If a modeled cost cannot be traced to a journal entry, payout event, and supporting document, it is still a planning estimate.

Map each benchmark assumption to expected system behavior so variance can be explained quickly and consistently.

| Benchmark component | Estimate input | Ledger journal expectation | Payout impact | Reconciliation artifact |

|---|---|---|---|---|

| Gross salary or wage | Approved gross amount for the worker and period | Compensation expense with matching payable or cash movement | Drives core payroll or payout amount | Payroll register, payout file, posted journal |

| Employer taxes or social contributions | Country rule set applied to the gross basis | Employer tax expense and related liability posting | May create remittance timing separate from worker pay | Tax calculation support, remittance record, GL detail |

| VAT-sensitive employer-paid service or benefit invoice | Invoice amount and local tax-treatment assumption | Expense plus VAT treatment based on invoice handling | Usually no change to worker net pay, but changes reporting pack | VAT invoice proof supporting deduction where allowed |

| U.S. tax-document status | W-9 or W-8BEN status where a U.S. payer or withholding context exists | Reporting classification can change even when expense is similar | Can alter withholding or information-return path | Collected form, TIN or foreign-status record, reporting support |

Use a consistent internal sequence for execution risk: ingest assumptions, apply country rules, clear compliance gates that can block execution, then run payout simulation and reconciliation checks. This is an operating default, not a universal legal sequence across jurisdictions.

Keep VAT and U.S. tax-document logic explicit in the map, even when gross salary assumptions look the same. VAT treatment depends on whether invoice evidence supports the deduction path, and W-9 versus W-8BEN status can change U.S. withholding or information-return handling.

Call out FX assumptions as a separate variance class. If the model used one rate basis and settlement used another timing basis, classify that gap as FX variance before escalating it as an operating failure.

Related: Payout Failure Benchmark Report: Success Rates by Rail, Country, and Error Code.

Use explicit decision rules when choosing country scenarios#

Use one rule set per objective: for budget planning, compare total employment cost; for labor-market or manufacturing context, compare labor rates only. Do not reuse one view to answer the other question.

This is a scope-and-unit control, not a style preference. OECD wage-tax analysis includes employer payroll taxes and social security contributions, while Eurostat labor-cost levels and the U.S. Employment Cost Index are hourly-oriented, and ECI includes benefits as well as wages and salaries. If one row is hourly labor cost and another is annual salary plus employer add-ons, do not rank yet.

| Decision objective | What to compare | What must match before ranking | No-go sign |

|---|---|---|---|

| Annual budget planning | Total employment cost | Period, worker type, currency basis, employer contribution categories | Salary-only row beside a row that includes taxes/benefits |

| Labor-market or manufacturing context | Hourly labor cost | Same hourly basis and sector coverage | Using hourly rates to pick a hiring-budget country |

| Scenario tie-break | Operational friction | Match cost scope first, then compare compliance/reporting burden | Calling a cheaper row "better" before execution checks |

Before sharing any ranking, label each row with period definition and inclusion set. If a United States row uses an hourly measure with benefits and a Germany row uses headline annual salary, freeze the comparison until both rows are normalized. No-go rule: never pick a "lowest cost country" when contribution categories or period definitions do not match.

Break ties with operational friction, not instinct#

If two countries are close on cost, break ties with execution burden. Start with compliance effort: beneficial-owner identification and verification requirements can add onboarding work for legal-entity flows.

Then check reporting only where it applies. In U.S. payer workflows, Form 1099-NEC may be required for qualifying nonemployee compensation. For U.S. persons with foreign financial accounts, FBAR filing is triggered if aggregate value exceeds $10,000 at any time during the calendar year. These are context-dependent, but they are real tie-break costs when U.S. payer or U.S. person exposure is in scope.

Use United States versus Germany as a scope test#

United States versus Germany is a useful scope test because headline salary can hide bigger differences. In practice, the larger gap may come from employer contributions and reporting complexity rather than nominal pay.

Apply the same sequence every time: match contribution scope and period basis first, then compare operational friction. That order prevents false "cheap country" decisions built on mixed definitions.

Related: Convenience of the Employer Rule for New York and Other Sticky States.

Catch benchmark errors before they hit reconciliation#

Most reconciliation failures start with mismatched assumptions, not with a country being expensive. Use this fail-fast rule: if a row does not document worker class, contribution scope, and FX timing, keep it out of close.

Mixed worker classes are the first red flag. Worker status is evidence-based, not label-based, so a contractor assumption in one country and an employee stack in another is not comparable. If a United Kingdom or Canada row mixes class logic, freeze the comparison until class treatment is aligned.

Incomplete labour-cost scope is the second red flag. Labour cost definitions include wage and non-wage employer costs, so a salary-only row is incomplete unless exclusions are explicit. This is a common breakpoint in reconciliation because statutory employer items are what post into payroll and the ledger.

FX timing is the third red flag. If exchange rates move between transaction date and settlement date, you should expect an exchange difference. Check both the FX rate source and the timing rule; otherwise, normal settlement variance gets misread as an exception.

Pre-close checks worth enforcing#

Use a short checklist every close:

| Check | What to verify | Article example |

|---|---|---|

| Source freshness | Verify release dates and next scheduled updates for each source series | ECI: 0.7% in 4th Qtr of 2025 (3-month) and 3.4% in 4th Qtr of 2025 (12-month); ONS Release date: 17 February 2026; Next release: 19 May 2026 |

| Method consistency | Ensure each row uses the same unit and inclusion set; record FX basis and conversion timing beside the amount | Annual total employment cost or hourly labour cost, not both |

| Contribution completeness | Confirm local employer-paid items or explicit exclusions | Canada: CPP contributions, EI premiums, and income tax to deduct; United Kingdom: employer National Insurance; selected EMEA markets: employer social contributions and taxes on wages |

- Source freshness

Verify release dates and next scheduled updates for each source series. For U.S. recency checks, ECI tracks change in hourly labor cost over time, with recent reference points of 0.7% in 4th Qtr of 2025 (3-month) and 3.4% in 4th Qtr of 2025 (12-month). For UK source control, the ONS labour-cost dataset shows Release date: 17 February 2026 and Next release: 19 May 2026.

- Method consistency

Ensure each row uses the same unit and inclusion set: annual total employment cost or hourly labour cost, not both. Record FX basis and conversion timing beside the amount.

- Contribution completeness

For Canada, confirm assumptions address CPP contributions, EI premiums, and income tax to deduct. For the United Kingdom, confirm employer National Insurance treatment. For selected EMEA markets, confirm non-wage items like employer social contributions and taxes on wages are included, or explicitly excluded with a reason.

For each country row, keep a compact evidence pack with source link, release date or version, owner, worker class, and included employer-paid items. If UK and Canada rows reuse the same salary-only pattern without local caveats, treat that as a pending reconciliation issue, not a usable benchmark.

Related: Can I Claim the Foreign Tax Credit for Taxes Paid to a 'Blacklisted' Country?.

Run an operating cadence that keeps benchmarks trustworthy#

Run this as a risk-based control process, not a static reference sheet: higher-risk rows get tighter reviews, and every change needs clear ownership, measurable status, and visible caveats.

Higher-risk jurisdictions or thinner-evidence assumptions should be reviewed first and more often. Lower-risk rows can follow a standard cycle, but still need a dated review record. If you cannot explain why one row is reviewed more often than another, the cadence is probably habit-based instead of risk-based.

Assign owners across three functions so traceability survives pressure: data updates, variance review, and audit evidence. Each country row should show who last refreshed it, who accepted unresolved variances, and who maintains the evidence pack (source link, release date, inclusion notes).

Use a short scorecard to detect drift before close:

- refresh completion against schedule

- unresolved variance count

- percent of country rows with complete evidence packs

Tie each checkpoint to a pre-defined action when quality drops. Completeness and timeliness are especially useful checkpoints, and data quality should be treated as multi-dimensional rather than a single pass/fail signal.

Keep caveats directly in each row, not buried in commentary. Coverage can exclude sectors in some benchmark series, so scope limits must stay visible. For U.S. rows tied to BLS ECEC, monitor the release schedule at least a week before publication; if you are relying on the database through September 2025 without a detailed news release, mark the row as provisional until reviewed.

Need the full breakdown? Read How to Manage a Multi-Country European Tour and Stay Schengen Compliant.

Conclusion#

A useful employer cost by country benchmark is not a slide artifact. It is a controlled planning input that earns trust when it is built from the full employer cost stack, checked for comparability, and tied back to clear reporting assumptions.

The core judgment is simple: standardize the components first, then compare. The underlying labor-cost definitions support that discipline. World Bank scope points to wages, employee benefits, and employer payroll taxes, and BLS international labor-cost notes make the same distinction by separating direct pay from employer social insurance expenditures and labor-related taxes. That is why earnings-only views are weak decision inputs. They omit cost items and often hide definition differences that can make country rankings look cleaner than they are.

You do not need a huge model to get this right. You need evidence and consistency. A good checkpoint is to refuse production use of any country row that does not show jurisdiction, worker type, period, currency, FX method, included contribution categories, source link, version date, and owner. If a source cannot tell you what is in the number, treat it as directional only. If two rows mix hourly compensation with annual totals, do not rank countries yet.

A concrete example helps. In the United States, BLS reported civilian employer compensation at $48.78 per hour worked in December 2025, split into $33.45 wages and salaries and $15.33 benefits, released March 20, 2026 at 10:00 a.m. ET. That kind of component split is what makes a benchmark usable. It also shows why source notes matter: BLS country-note methodology calls out a minimum ten employees coverage constraint. If your other country sources do not match that coverage, your comparison may still be useful, but only with the caveat attached.

The main failure mode is simple. Teams reuse salary-only assumptions, ignore coverage notes, or let stale inputs sit in the model past their useful life. At that point, the benchmark has not failed because benchmarking is useless. It has failed because the method was inconsistent or the evidence pack was incomplete. Current data matters for the same reason: old assumptions can drift away from current market conditions without any operational change on your side.

So the next move should be narrow and practical. Build the comparability table and the benchmark-to-reporting mapping first. Use those two controls to prove that each country row can be explained, refreshed, and checked before you expand into more countries. That is the version of benchmarking that supports decisions without pretending to be more certain than the underlying data.

Related reading: Cost of Living vs. Quality of Life When Choosing Your Next Nomad Hub.

Frequently Asked Questions

What must be included in an employer cost benchmark by country to make it decision-ready?

At minimum, your employer cost by country benchmark should include wages or salary, employer-paid benefits, and payroll taxes. It also needs the comparison basis attached to each row: jurisdiction, time period, unit of measure, currency, and the foreign exchange method used. If a row does not show what is included, when it applies, and which method was used, treat it as not planning-grade.

Why can’t salary alone be used to compare employer cost across countries?

Because labor cost is not salary alone. The World Bank definition includes wages paid to employees, the cost of employee benefits, and payroll taxes paid by an employer. If you compare salary only, you can understate employer spend and mis-rank countries.

What makes two country benchmarks non-comparable even when both look detailed?

Detailed does not mean aligned. One source may be a per-hour employer compensation measure, like U.S. BLS ECEC, while another may be a calendar-year average or a dataset with country-specific coverage differences documented in technical notes. If scope, worker coverage, period, or unit differ, treat the comparison as directional until normalized.

Should we compare hourly labor cost or annual total employment cost for platform finance planning?

For budget planning, annual total employment cost is often easier to align with headcount plans and ledgers. Hourly measures are still useful, but only if you convert everything to the same unit first and keep the source method visible. If one country is using ECEC per hour worked and another is using annual totals, do not rank them yet.

How should foreign exchange be handled so benchmark variance is not mistaken for operational failure?

Pick one FX rule and label it in every row. A transaction-date exchange rate ties measurement to the date the transaction is recognized, while a weighted-average exchange rate can be acceptable for some income statement measurement contexts. The key failure mode is simple: cash paid at settlement in your functional currency can move with FX even when local employer cost did not, so split FX variance from operating variance in your review.

How often should benchmark assumptions be refreshed and reapproved?

Do not use a universal refresh rule. Use the release cadence of the underlying series and reapprove when the source updates, the method changes, or a caveat is resolved. For example, U.S. ECI for March 2026 is scheduled for April 30, 2026, U.S. ECEC for March 2026 for June 12, 2026, and Eurostat updates labour cost data quarterly, with countries transmitting within 70 days after the reference period.

What is the safest way to answer “which country is cheapest” without misleading stakeholders?

Answer only within a matched scope: same worker type, same period, same unit, same included cost categories, and same FX basis. A safer phrasing is, “Under this normalized method, Country A is currently lower on measured employer cost than Country B.” If those conditions are not met, the right answer is that the current benchmark does not support a credible ranking.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bls.gov/ecitrusted

- bls.gov/ilc/ichcctn.pdftrusted

- data.europa.eu/data/datasets/vqq1et0yey58xqvwcpfcwtrusted

- ec.europa.eu/eurostat/web/labour-market/information-data/...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- fdic.gov/risk-management-manual-examination-policies/...trusted

- irs.gov/forms-pubs/about-form-w-9trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Global Contractor Payout Benchmarks by Country

Treat most country ranking pages as inputs, not answers. If you are evaluating **country-level contractor payout inputs**, the first mistake is assuming every page measures the same thing. Many do not.

Payout Failure Benchmark Report for Platform Teams

A useful **payout failure benchmark report** is not a prettier exception export. It is the operating document that tells your platform team which payout failures are real rail problems, which ones are recipient-data problems, which ones were held before release, and which ones were later recovered.

Average Freelance Rates by Country and Profession in 2026

If you are using **average freelance rates country profession 2026** data for budgeting or payout approvals, start by normalizing the benchmarks into one payout unit, then gate them by source confidence and approval controls. This is not another prettier list of freelancer benchmarks. It is a practical way to turn fragmented 2026 rate inputs into a rate policy that finance and ops teams can actually run without constant exceptions.