Quick Answer

Expect the cost of using an eor to be more than the monthly per-employee line item. Published examples range from lower starting prices to much higher tiers depending on country, scope, and pricing model, and real contracts may add setup, FX, renewal, or offboarding charges. The practical answer is to compare providers with a normalized fee table and signed scope boundaries, not a headline number alone.

What drives EOR cost#

The biggest mistake when evaluating the cost of using an EOR is treating the monthly fee as the whole decision. It usually is not. The real risk is signing on a clean headline number, then learning later that setup fees, offboarding charges, country-specific compliance work, or scope exclusions were sitting in the fine print all along.

An Employer of Record is the legal-employer service used when you want to hire in a country where you do not have your own local entity. In practice, that service can cover compliance, payroll, taxes, and often onboarding and benefits administration. That sounds straightforward until you compare quotes: pricing can vary widely by country, included services, and benefits. Published ranges can run from $99 to $2,000 per employee per month, which tells you the sticker price alone is not a reliable comparison tool.

This article takes a buyer-side approach. Instead of asking which provider looks cheapest, you will compare quotes line by line, separate one-time charges from recurring charges, and check whether each quote actually includes the work you need done. For a small team, creator business, or freelancer-led company, surprise costs can strain cashflow quickly.

Start with a simple checkpoint. Ask for the fee schedule in writing and verify whether employee onboarding, payroll processing, tax withholding, and benefits administration are included in the base price or treated as extras. If a provider cannot make those boundaries clear early, treat the quote as incomplete. Some buyers only learn about surprise costs after committing, and public examples include a USD 1,000 setup fee and a USD 6,000 offboarding fee. Those are examples, not standard market fees, but they show how fast vague scope can turn into budget shock.

Country of employment changes the math too. One market can look straightforward and low cost, while another carries more compliance obligations and a heavier service burden. If you are comparing providers for cross-border hiring, do not assume a quote in one jurisdiction tells you much about another. The country assumption should be visible on every quote you review.

The goal here is practical: help you choose an EOR with predictable monthly outflow, fewer exceptions, and less contract ambiguity. By the end, you should be able to tell the difference between a quote that is truly cheaper and one that only looks cheaper until the first non-standard event. If you want a provider comparison from the freelancer side, see Deel vs. Remote: A Comparison from the Freelancer's Perspective.

Start with the full cost stack, not the headline fee#

Start by splitting each quote into one-time, recurring, and periodic costs, or you risk mistaking first-year spend for steady-state spend.

Most EOR quotes start with a per-employee monthly fee, but published benchmarks differ: $199 to $650 per employee monthly in one source and $300 to $1,000 per employee per month in another. Some providers use a flat fee model, often cited around $200 to $600, while others use a percentage of salary model. If the quote does not clearly name the pricing model, do not treat it as comparable.

| Cost layer | What it usually means | What to verify in writing |

|---|---|---|

| One-time | setup fee, registration fee, implementation work | when it is charged and what triggers it |

| Recurring | monthly EOR service fee for payroll, compliance, contracts, taxes, and benefits scope | exact monthly amount, pricing model, and country/salary sensitivity |

| Periodic | annual renewal fee or other ongoing admin charges | renewal timing and how changes are communicated |

Define terms early so scope stays clear. Global payroll is the recurring operating layer: payroll, compliance, contracts, taxes, and benefits administration. Entity incorporation is the legal setup route under your own legal entity, with separate setup and maintenance obligations.

Before comparing providers, request a fee schedule that explicitly marks employee onboarding, tax withholding, and employee benefits administration as included or excluded. If those items are unclear, treat the quote as incomplete.

Why two EOR quotes for the same hire can differ so much#

If two EOR quotes look similar, choose the one with clearer operating boundaries, not just the lower sticker price. For the same hire, price gaps usually come from country context, included scope, and how compliance work is allocated.

| Scope item | What to verify |

|---|---|

| Onboarding | Included, excluded, or separately priced |

| Payroll | Included, excluded, or separately priced |

| Benefits administration | Included, excluded, or separately priced |

| Terminations | Included, excluded, or separately priced |

| Tax withholding | Who owns it |

| Non-standard compliance requirements | Who handles them |

Published starting prices are not portable across jurisdictions. Providers use different pricing models, and local labor-law compliance work can vary by country, so monthly fees can vary widely. In market examples, some providers start around $199 per employee/month, while others start at $599 per employee/month or more.

Scope is the next major separator. One quote may include onboarding, payroll, benefits administration, and termination support in the base fee. Another may show a similar monthly number but move some of those items into separate charges or exceptions. Even providers that advertise reach across 110+ countries can still price by country and service level within that footprint.

Use a quick comparison check before deciding:

- Mark onboarding, payroll, benefits, and terminations as included, excluded, or separately priced.

- Confirm who owns tax withholding.

- Confirm who handles non-standard compliance requirements.

If those boundaries are vague, treat the quote as incomplete. When prices are in the same range, operational clarity usually beats a slightly lower monthly fee. For a related cost signal, see What is the 'Withdrawal Penalty' on EOR Platforms?.

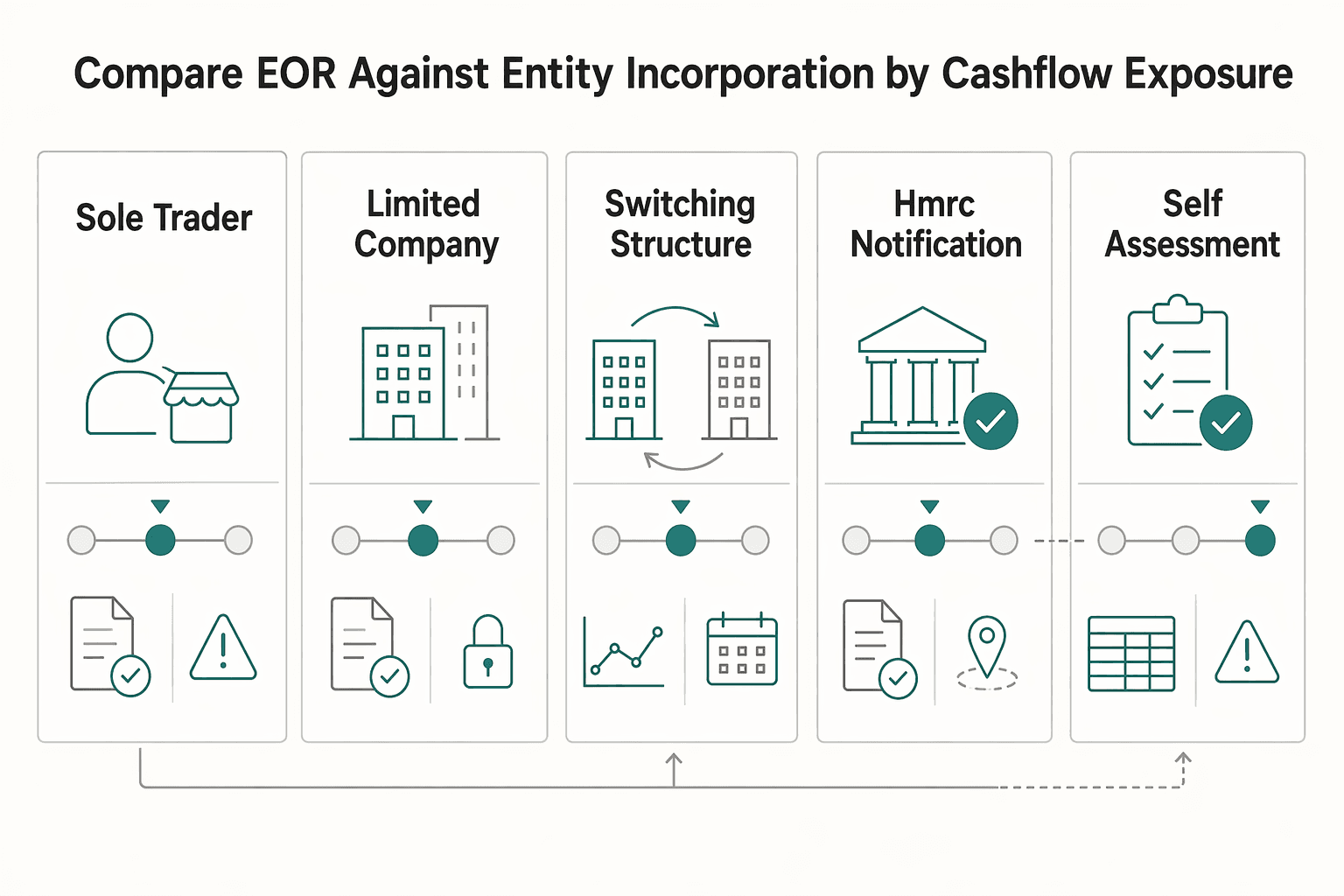

Compare EOR against entity incorporation by cashflow exposure#

If your main constraint is cashflow risk, compare EOR versus entity setup as an exposure tradeoff: an EOR is often easier to budget early, while your own entity can become more efficient later if headcount is stable and you can run local compliance reliably.

| UK checkpoint | Grounded detail |

|---|---|

| Sole trader | Simplest structure to set up and keep records for; personally responsible for business debts |

| Limited company | Legally separate from its owners |

| Switching structure | Moving from sole trader to limited company is usually easier than the reverse |

| HMRC notification deadline | Tell HMRC by 5 October 2025 if you need to file for the tax year 6 April 2024 to 5 April 2025 |

| Self Assessment tax bills | Due by 31 January |

| Sole trader registration threshold | Register if you earn more than £1,000 in a tax year |

| Path | First-year cash exposure | Ongoing cash exposure | Delay and rework risk | Internal admin burden |

|---|---|---|---|---|

| EOR | Provider setup and recurring service charges defined in the contract | Recurring service charges and scoped add-ons | Lower when scope and ownership are explicit in writing | Lower when provider boundaries are clear |

| Your own legal entity | Incorporation/registration work, local advice, and internal setup time | Ongoing filings, payroll operations, and entity maintenance | Higher if structure or deadline assumptions are wrong | Higher because your team owns more of the process |

| Decision check | Useful when you need speed and lower upfront commitment | May still be worth it if predictable monthly spend is the priority | Entity path can improve later if operations are stable in one market | Only compare after pricing time, compliance support, and error recovery |

Use one jurisdiction as a proof test before generalizing globally. In the UK, the business structure you choose affects tax treatment and legal responsibilities. A sole trader is described as the simplest structure to set up and keep records for, while a limited company is legally separate from its owners. A sole trader is also personally responsible for business debts, and UK guidance says moving from sole trader to limited company is usually easier than the reverse.

Deadlines are where failure costs become concrete. UK guidance says you must tell HMRC by 5 October 2025 if you need to file for the tax year 6 April 2024 to 5 April 2025; notifying late could trigger a penalty. It also states Self Assessment tax bills are due by 31 January, and late filing can trigger penalties. UK guidance also says you must register as a sole trader if you earn more than £1,000 in a tax year.

So keep the operating rule simple: if you choose the entity route, assign named owners for registration, filing, payment deadlines, and record retention before launch. If those owners and dates are not clear in writing, your entity-vs-EOR comparison is not complete. For a step-by-step walkthrough, see How to Choose an Employer of Record (EOR) Provider.

Spot hidden fees and contract terms before signing#

Before you sign, assume the quoted monthly rate is incomplete until scope and fee triggers are explicit in writing. Hidden costs usually come from add-ons, exceptions, and vague contract language, not the headline number.

Get the fee schedule in writing#

Do not approve an EOR off a sales deck alone. Require a written fee schedule that covers onboarding, amendments, monthly administration, offboarding, and any recurring charges tied to an annual renewal fee or compliance updates. If a provider says "no hidden fees," verify that against the full contract set, including country-specific terms.

Use one pre-approval bundle:

- formal quote

- full fee schedule

- services included and excluded

- country-by-country assumptions sheet

- sample invoice

- contract language on fee changes and renewals

This is a practical control, not paperwork. Some teams only discover extra charges after committing, including cited scenarios like a USD 1,000 setup fee and a USD 6,000 offboarding fee. Those figures are examples, not standard benchmarks, but they are enough to justify asking exactly what can be billed at entry and exit.

Define triggers before you accept "custom pricing"#

"Custom pricing" can work, but only when trigger conditions are clear. Get explicit boundaries for when extra billing applies to tax withholding, employee benefits administration, and non-standard local labor law cases.

Ask the provider to separate standard service from exception handling in writing. For example, confirm what is included in routine payroll and benefits operations versus what is billed as a correction, manual change, or exception. The workflow may look similar across countries, but country-level details still change cost assumptions, so the country-by-country assumptions sheet should be mandatory.

If a provider cannot map one target country's assumptions and exception triggers clearly, pause and re-quote.

Cover contractor risk explicitly#

If contractors are part of your model now or later, add a clause covering independent contractor misclassification support and remediation responsibility. The goal is not a blanket legal guarantee. It is clear ownership of who handles what, what support is included, and what becomes billable extra work.

Without this, teams can discover too late that support ends at initial paperwork while remediation or conversion work is charged separately. If contractors are in scope, put that allocation in writing before signing. If needed, point your team to What to Do If You've Been Misclassified as an Independent Contractor.

Build an apples-to-apples quote comparison table#

Build one normalized table for every quote, and reject any provider you cannot map in one review cycle. That is a pricing control, not admin overhead: unresolved ambiguity is spend risk.

Normalize the pricing model before comparing price#

Compare pricing logic first, then price. The pricing examples here support three model types: flat fee per employee, percentage of salary, and hybrid custom packages. That is why a lower-looking base number can mislead; for some profiles, a $199 monthly flat fee can still cost more than a 12% model.

| Hiring path | Quoted price |

|---|---|

| Contractor Management | From $49 per contractor/month |

| Global Payroll | $29 per employee/month plus $1,000 per-entity setup |

| EOR | From $599 per employee/month |

Use the same first columns for each provider: pricing model, billing unit, one-time fees, recurring fees, and hiring path (EOR, contractor management, or global payroll). In the grounded Deel excerpt, pricing is workflow-specific, with separate lines for Contractor Management from $49 per contractor/month, Global Payroll at $29 per employee/month plus $1,000 per-entity setup, and EOR from $599 per employee/month.

Weight sources before trusting entries#

Not all pricing inputs carry equal confidence. Keep a source-confidence column so documented provider terms outrank sponsored or anecdotal inputs.

| Provider | Pricing evidence on hand | Included services | Excluded services | Contract term | Support model | Source confidence |

|---|---|---|---|---|---|---|

| Deel | Third-party excerpt with product lines: Contractor Management $49 per contractor/month, Global Payroll $29 per employee/month plus $1,000 per-entity setup, EOR from $599 per employee/month | Not fully verified from provider terms in current pack | Not fully verified from provider terms in current pack | Not established in current materials | Not established in current materials | Medium until matched to provider documents |

| RemoFirst | No grounded quote or contract detail in current pack | Pending direct provider documentation | Pending direct provider documentation | Pending | Pending | Not enough evidence |

| Remote | No grounded quote or contract detail in current pack | Pending direct provider documentation | Pending direct provider documentation | Pending | Pending | Not enough evidence |

| Omnipresent | No grounded quote or contract detail in current pack | Pending direct provider documentation | Pending direct provider documentation | Pending | Pending | Not enough evidence |

A partially filled table is still useful because it shows where the evidence is thin. Do not treat sponsored comparison cards or anecdotal posts as quote-grade proof.

Map fees to the same workflow stages#

Require each provider to map fees to the same stages: pre-hire, employee onboarding, monthly global payroll, change requests, and exit. Then mark each line item as included, excluded, or billable-on-request.

Use a hard decision rule: if a provider cannot normalize the quote to these stages in one review cycle, stop and re-quote.

Country rules and compliance gates that change your real cost#

Your real EOR cost is country-dependent, not just provider-dependent. Compliance requirements and labor law obligations vary by jurisdiction, so give each target country its own cost profile instead of copying assumptions from your last hire.

Use one hard check in every country: confirm in writing what the quoted "standard handling" actually covers. Cross-border hiring can include payroll tax registration, labor law compliance, and other local steps, so ask whether routine tax withholding administration and legally required benefits handling are included, and where that scope is documented, for example in the order form or country appendix.

If a provider cannot document that scope, treat the quote as incomplete. Headline monthly pricing may not reflect true cost, and paperwork or misclassification errors can lead to fines, legal disputes, or hiring delays. Avoid broad claims like "global compliance coverage" unless country-specific terms support them.

For multi-country selection, compare providers country by country, not brand by brand. There is no single best EOR for every case. Fit depends on where you hire, what obligations apply there, and how clearly those assumptions are documented before you sign.

Use this 30-minute pre-sign checklist to avoid cashflow surprises#

Before you sign, require written clarity on scope, exclusions, fee-change triggers, and one real exception scenario. If a provider cannot explain what changes the bill in writing, pause and re-quote.

Build the evidence pack first#

Start with the documents that control money: the formal quote, full service scope, exclusions, contract term, fee-change policy, and jurisdiction assumptions. Your checkpoint is simple: every cost-related statement should appear in the binding document, not only in calls or email.

Run the order of operations in sequence#

- Validate included services against your target country and hiring plan.

- Map total first-year cost, separating one-time charges from recurring charges.

- Test one change-order scenario and ask how pricing is recalculated.

- Stress-test one offboarding scenario and ask what billing continues after notice.

Verify operational controls before signature#

Confirm who owns exception handling, how onboarding or timing delays are reported, and how billing disputes are escalated. Ask for named roles, or clear role owners, expected response windows, and the escalation path when work stalls.

Also treat live payment-behavior signals as part of pre-sign risk. Credit signals are historical and can miss current operating stress; warning signs often appear earlier as complaints about terms, vague downstream-delay explanations, and extension requests. If previously workable terms, for example Net 30, suddenly become a problem without clear documentation, treat that as a cashflow warning and tighten terms before signing.

If the provider cannot explain the cost impact of one compliance edge case in writing, do not sign yet. For adjacent pricing risk, see How EOR Platforms Use FX Spreads to Make Money. If you want a quick next step for cost of using an EOR, try the free invoice generator.

Conclusion#

Choose the quote you can explain end to end, not the one with the lowest monthly sticker price. The practical win is predictability: a provider you can budget, verify, and operate without finding new charges after onboarding or the first payroll cycle.

The clearest number in the research is still only a rough anchor, not a benchmark to copy into your model. One source published on May 5, 2025 says Employer of Record services "typically cost between $200 and $650 monthly" per hired employee. That same source immediately qualifies it as a general estimate that varies based on your company's needs. That is useful for a sanity check. It is not strong enough to decide a vendor on its own.

That caution matters because source quality was uneven. One cited Omnipresent page returned "Page not found," and some retrieved documents were unrelated municipal materials rather than EOR pricing guidance. If you cannot trace a number back to an actual provider page, formal quote, or contract language, do not let it drive your decision. A made-up average is worse than no average because it can make a vague quote look reasonable when it is not.

Your operating rule is simple: normalize every provider into the same comparison table, then test the parts most likely to move cashflow. The research specifically flags EOR setup and currency exchange fees as distinct cost components, so those are not details to wave away in procurement. Ask in writing whether either charge applies to your case, what triggers it, whether it is one-time or recurring, and where it appears in the contract or quote.

A practical failure mode is signing on a "cheap" monthly rate, then discovering that setup, FX, or another scoped-out admin charge pushes the first-year total above what finance expected. Before signature, make the provider map each fee to a stage of the relationship such as onboarding, monthly payroll, changes, and exit. Then confirm which charges are optional, conditional, or standard for your hire.

If you do that consistently, you can better protect margin and payment reliability from day one. Use the checklist from this article as your repeatable standard for each new market and hiring cycle. When a quote cannot be fully explained, verified, and compared on the same basis as the others, treat that ambiguity itself as a cost signal and pause until the provider makes it legible.

Frequently Asked Questions

How much does an EOR usually cost per employee?

Published pricing examples vary a lot, so do not anchor on one number. Some provider materials show starting prices as low as $199 per employee/month. Others start at $599 per employee/month or more, and another guide puts a typical range at $299 to $800 per employee per month depending on country and included services. If you are estimating the cost of using an eor, treat any headline rate as a starting point, not a final budget.

Are setup fees standard in EOR pricing or only charged by some providers?

They are charged by some providers, not universally included. One grounded source explicitly warns that setup charges and FX fees can materially increase the total budget. So the check is simple: ask whether one-time charges sit outside the monthly fee. A common failure mode is assuming an item is included when the contract prices it separately.

Is an EOR cheaper than opening a legal entity in every case?

No. Vendor material argues that EOR services can reduce upfront and ongoing expansion cost versus entity setup, but that does not make EOR cheaper in every country, team size, or hiring horizon. If your priority is lower upfront spend, EOR can compare well. If you expect stable headcount in one market, you should price the entity path separately rather than assume.

What costs are commonly excluded from the base EOR fee?

The most commonly cited extra-cost categories in the source guidance are setup charges and FX fees. Scope gaps can also appear around services that are not clearly listed in the contract. Your checkpoint is to match every billed line to the order form or service agreement, especially for payroll, taxes, benefits administration, and any custom services. If a provider describes something as “custom” without a trigger or rate, expect budget drift later.

How should freelancers and small teams compare EOR quotes fairly?

Normalize every quote into the same buckets: one-time fees, monthly service fees, country assumptions, and anything that depends on payroll amount or exceptions. EOR pricing models can be flat fee, percentage of payroll, or hybrid, so you need to convert them into a first-year total and a steady-state monthly total before comparing. If one quote cannot be mapped cleanly because the scope is vague, that quote is not cheaper yet, just less legible.

Which country-level compliance requirements most often change total EOR cost?

The big drivers are the country-specific obligations tied to payroll, taxes, benefits, and local labor-law compliance. That is why sources stress there is no single universal EOR cost answer and why the same hire can price differently across jurisdictions. Before you sign, verify that the quoted price for your target country includes standard handling for those local requirements, because this is where the real cost of using an EOR usually shifts.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- acquisition.gov/node/56401/printable/printtrusted

- catalog.misericordia.edu/content.phptrusted

- docs.legis.wisconsin.gov/document/statutes/1949/66.pdftrusted

- icc.illinois.gov/downloads/public/2%20TEC%20Attachment%20A.pdftrusted

- labor.ca.gov/wp-content/uploads/sites/338/2024/08/AB2849-...trusted

- lakewalesfl.gov/DocumentCenter/View/4943trusted

- scappoose.gov/sites/default/files/fileattachments/city_cou...trusted

- bectran.com/post/early-warning-signs-customer-cash-flow-...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

What to Do If You've Been Misclassified as an Independent Contractor

Treat this as a protection problem first, not a label debate. If your work was treated as an independent contractor arrangement even though the relationship functioned differently, your first goal is to protect pay, rights, and records while you choose the least risky escalation path. You can do that without making accusations on day one, which often keeps communication open while you document what happened.

When to Use an Employer of Record for International Hiring

An Employer of Record lets you hire in another country through a third party, without setting up your own local entity first. The provider handles key compliance mechanics, but it does not hand off every employment risk.

Deel vs Remote for Freelancers Who Need a Clear First-Payout Decision

Choose the platform that makes your first payout cycle predictable and your contracts easier to defend. This is an operating decision, not a brand contest.