Quick Answer

Start by mapping churn to operational stages, then prove each suspected cause with one evidence chain: API event, webhook record, and matching Ledger or payout reconciliation output. Triage in order: payout and payout-batch failures, then KYC/KYB/AML gates, then fee or packaging changes. If the stage signal cannot be rebuilt for the same cohort and analysis window, mark the cause unknown and fix visibility before funding roadmap work.

Why Freelancers Leave Platforms#

Treat churn as an economics question#

Contractor churn is not just another retention metric. On a freelancer platform, it is a business model decision because every dropout can affect activity volume, support cost, and the quality of the growth you keep.

Churn analysis asks when and why people stop using a product. On a platform serving freelancers, that answer rarely lives in one number. You need evidence across behavior, billing, support, and the operating experience around onboarding, activation, payment, and communication. Unit economics is the right lens because it shows whether the model is sustainably profitable on a per-unit basis, not just whether signups still look healthy.

Focus on losses that change growth quality#

This guide helps founders, revenue leaders, product teams, and finance operators figure out why freelancers leave, what that churn costs, and which fixes are worth funding first. The key is separating noise from the losses that actually weaken margin or future revenue quality.

Before you debate solutions, ask two questions. Which cohort is leaving, and at what stage? Does that exit reduce profitable activity from existing users, delay activation, or simply trim low-value volume? If you cannot answer both from the same analysis window, you are not ready to call the cause. Treat it as unknown, not insight.

This is where teams often go wrong. When churn rises, it is easy to jump to discounts, promo credits, or a broad product rebuild before validating the cause. If the issue is onboarding friction or payment experience, pricing changes may increase activity without fixing why people leave. If the problem is concentrated in a high-value repeat cohort, the right response may look very different from what a top-line retention chart suggests.

Use an operator standard for evidence#

Use a simple standard throughout this guide: can you tie the observed drop-off to an operational event you can verify, then estimate whether fixing it improves unit economics?

In practice, that means clear definitions, a sequence for diagnosis, and evidence checks before you approve work. A good early outcome is not a perfect answer. It is an agreed shortlist of likely causes, a list of unknowns, and a rule for what gets escalated to product, finance, or operations. Net revenue retention is a useful reminder here. Sustainable growth comes from what existing cohorts keep doing over time, not from replacing churn with more acquisition.

The rest of this guide is about making those calls with enough proof to act, and enough restraint to avoid fixing the wrong problem. For a deeper look, read Contractor Onboarding Optimization: How to Reduce KYC Drop-Off and Get to First Payout Faster.

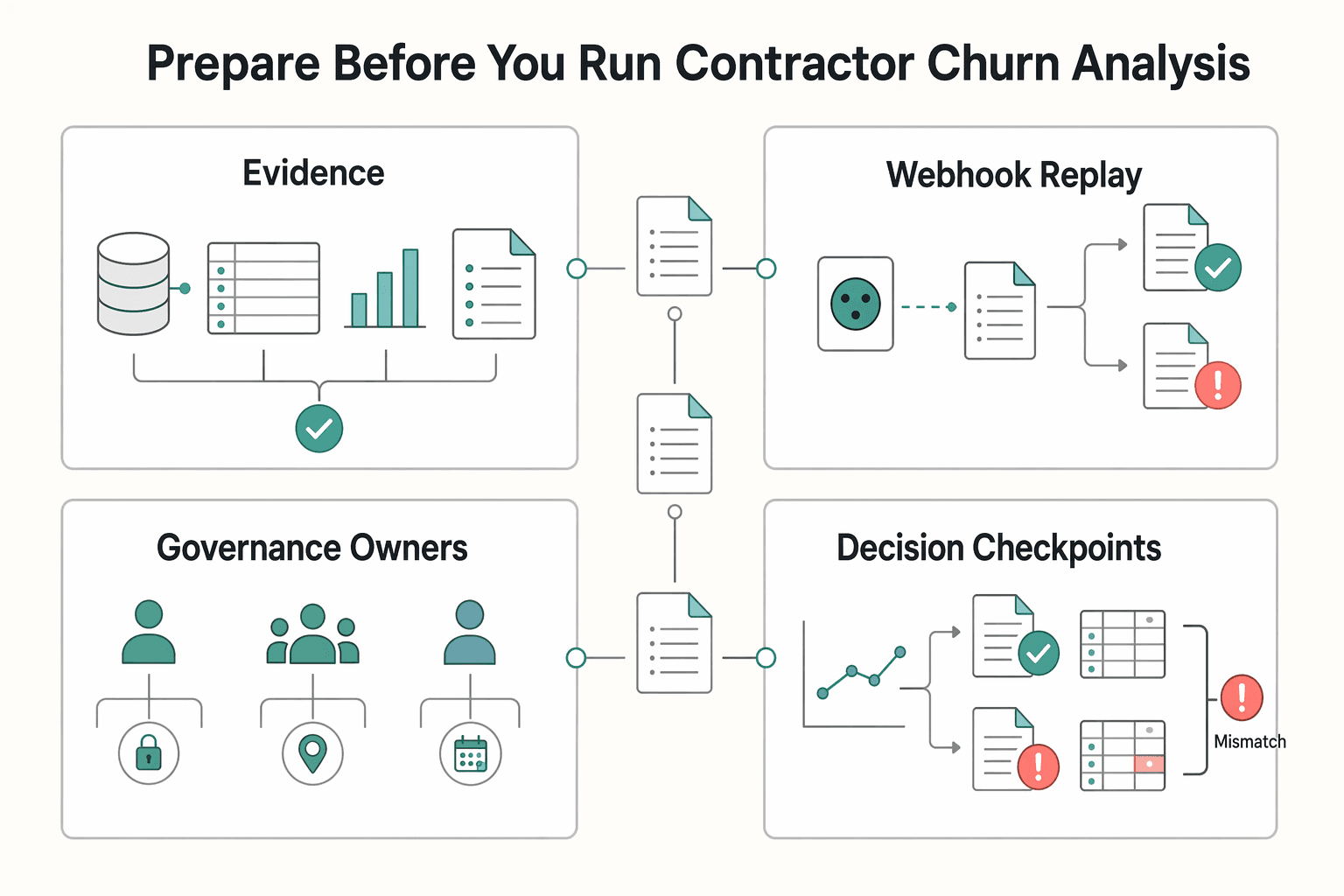

What to prepare before you run contractor churn analysis#

Before you start, prepare one evidence pack and assign decision ownership. Otherwise, you will see where activity dropped without being able to defend why.

| Preparation | What to pull or confirm | Checkpoint |

|---|---|---|

| One evidence pack for one analysis window | Retention output, customer journey stages, payout status logs, and Ledger or payout reconciliation exports for the exact same date range; keep the itemized payout reconciliation export and the Failed payouts section | You can trace one freelancer from journey stage to payout outcome without changing dates |

| API and webhook visibility | Verify coverage for onboarding, payout attempts, transfer reversals, and account state changes | If retention shows drop-off but the event trail is missing, treat it as an observability gap until proven otherwise |

| Governance owners | Make ownership explicit for each gate and exception path; name who can approve pricing model changes | Otherwise, you can diagnose correctly and still stall because no one has authority to change policy, messaging, or fees |

| Decision checkpoints | Escalate to product when stage drop-off in retention is supported by event evidence; escalate to finance or operations when reconciliation data shows failed payouts, reversals, or payout-batch issues tied to the same cohort and window | If the chain breaks between journey stage, event data, and reconciliation, label it unknown and fix data visibility first |

-

Build one evidence pack for one analysis window. Pull retention output, customer journey stages, payout status logs, and Ledger or payout reconciliation exports for the exact same date range. Keep the itemized payout reconciliation export and the Failed payouts section, not just dashboard summaries. Check that you can trace one freelancer from journey stage to payout outcome without changing dates.

-

Confirm API and webhook visibility before analysis. Webhooks are HTTP endpoints that receive events, and they cover payment events that can happen outside the immediate payment flow. Verify coverage for onboarding, payout attempts, transfer reversals, and account state changes. If retention shows drop-off but the event trail is missing, treat it as an observability gap until proven otherwise.

-

Assign governance owners up front. KYC requirements for payouts are country-specific, and KYB checks can sit inside AML/CFT programs, so ownership for each gate and exception path must be explicit. Name who can approve pricing model changes as well. Otherwise, you can diagnose correctly and still stall because no one has authority to change policy, messaging, or fees.

-

Set decision checkpoints before debate. Escalate to product when stage drop-off in retention is supported by event evidence. Escalate to finance or operations when reconciliation data shows failed payouts, reversals, or payout-batch issues tied to the same cohort and window. If the chain breaks between journey stage, event data, and reconciliation, label it unknown and fix data visibility first.

Map freelancer journey stages to churn events that actually hurt revenue#

Use only stages and churn signals you can reconstruct from operational systems. If a signal cannot be rebuilt from Ledger plus Webhooks without manual interpretation, treat it as non-decision-grade until visibility is fixed.

Split the journey into operational stages#

Map stages to how freelancers actually move through your product: sign-up, verification, first earnings, first withdrawal, repeat payout, and tax-document readiness only if tax paperwork is a real gate in your flow.

| Stage | What to track in platform terms | Why it matters commercially |

|---|---|---|

| Sign-up | Account created, profile started, onboarding initiated | Shows whether acquisition is producing usable supply |

| Verification | KYC requirements requested, submitted, approved, or stalled | Verification gates charges and payouts |

| First earnings | First completed job or first funds attributed | Distinguishes activated supply from casual sign-ups |

| First withdrawal | First payout requested, attempted, succeeded, or returned | Core payout trust moment |

| Repeat payout | Inclusion in recurring payout batches and success/failure pattern | Shows whether earnings behavior is durable |

| Tax-document readiness | Required tax form requested and completed, if applicable | Tracks readiness when tax documentation is a platform gate |

Keep stage names tied to emitted events. For example, "stalled verification" is operationally useful because verification requirements vary by location, business type, and requested capabilities.

Define churn events in platform language#

Use event-level churn definitions, not vanity inactivity windows. Strong examples are stalled KYC, repeated payout failure, unresolved AML holds when linked to observed drop-off, and abandonment before repeat payout batches.

Define exact boundaries for each event. "Repeated payout failure" is practical because you can validate it in payout status logs plus reconciliation data. Also check batch-level behavior for repeat payouts, since automatic payouts can include multiple transactions. Returned payouts should be reviewed directly, especially where destination details are incorrect.

Tie each churn event to a monetization consequence#

For each event, ask: what revenue quality is lost at this stage? Stalled KYC usually delays activation, first-withdrawal failures reduce payout volume, and drop-off before repeat payouts removes freelancers who already reached earnings.

Before escalating fixes, run one checkpoint: can this churn signal be reconstructed from Ledger plus Webhooks without manual interpretation? A single ledger should be your financial source of truth, and connected-account webhook coverage is required for asynchronous state changes.

If the answer is no, classify the cause as unknown and fix observability first. Without that chain, you cannot reliably separate compliance friction, payout operations issues, and missing data coverage.

We covered this in detail in Involuntary vs Voluntary Churn on Platforms and How to Attack Each.

Segment churn by cohort before you decide what to fix#

After you can reconstruct a churn event, segment it before choosing a fix. Averaging unlike freelancers into one headline churn rate usually hides the operational cause.

Build cohorts around monetization, not demographics#

Use cohorts that change revenue quality or operating cost: geography, payout rail, pricing model exposure, compliance path, and lifecycle stage. Cohorts are groups that share properties or event sequences, and they can be compared directly over time in retention analysis.

Geography and payout rail are operational, not cosmetic. Payout availability varies by country and industry, local payment-method fit is market-specific, and cross-border payout coverage varies by country and method footprint, including documented coverage in more than 50 countries for one global payouts footprint. Compliance path is also cohort-worthy because verification requirements vary by country, capabilities, and account setup.

Before analysis, run one data-quality check: can you reproduce cohort membership from stored properties and event history, without analyst interpretation? If not, fix tagging first.

Separate new freelancer churn from mature freelancer churn#

Do not combine first-stage drop-off with repeat-earner attrition. New and mature cohorts can show the same churn event for very different commercial reasons.

A practical split is before first successful payout versus after repeat payout behavior starts. That boundary is observable in platform events and aligns to monetization. It also accounts for timing differences, including an initial payout schedule that is typically 7-14 days after the first successful payment.

| Churn trigger | Affected cohort | Unit economics impact | Operational owner | Reversibility |

|---|---|---|---|---|

| Stalled KYC before first earnings | New freelancers in stricter verification paths by country or capability | Delayed activation and slower payback | Compliance and onboarding product | Usually medium if document flow and messaging improve |

| First payout delay or failure | New freelancers on specific payout rails or cross-border routes | Lower trust before repeat earnings | Payments ops | Often high if routing, destination details, or status visibility improves |

| Repeated payout failure after repeat earnings | Mature freelancers with proven earning history | Higher loss of durable payout volume | Payments ops and finance | Medium, but typically high-priority if impact is concentrated |

| Churn after fee or pricing exposure change | Cohorts exposed to a different pricing model | Margin and retention tradeoff | Finance and growth or product | Medium, after cause is verified |

Pick the fix that matches the cohort signal#

Match the intervention to the cohort pattern. If one compliance-path cohort shows high KYC/AML fallout but strong post-activation retention, prioritize verification flow, document prompts, and status messaging before broad discounting.

If payout friction is concentrated in mature cohorts and the lost payout volume is materially larger than expected top-of-funnel gains, move payout reliability ahead of additional acquisition spend. For a step-by-step walkthrough, see FMLA for Freelancers: Why It Doesn't Apply and How to Build Your Own Leave Plan.

Quantify the economics before approving retention work#

Approve retention work only when the economics are credible by cohort: lost contribution, likely recovery, intervention cost, and payback period, with a clear split between observed data and assumptions.

Once cohorts are clean, turn each into a simple investment case so budget follows expected impact, not just a high churn headline.

Build a cohort impact model from contribution, not just churn rate#

Start from contribution margin, not gross volume. Contribution margin (sales revenue minus variable costs) is the clearest base for estimating what a churned cohort costs.

| Component | What it covers | Decision note |

|---|---|---|

| Lost contribution | Contribution margin per active freelancer or payout-active account, multiplied by churned accounts in that cohort | Finance should be able to reproduce it from Ledger exports for the same time window used in retention analysis |

| Recovery value | Contribution you expect to preserve or recover if the intervention works | Keep observed loss and modeled recovery separate; projected recovery is a hypothesis unless supported by prior experiments, recovery analytics, or holdout results |

| Intervention cost | Engineering time, operations headcount, vendor cost, refunds or credits, and ongoing support cost | If product, ops, and finance cannot reconcile the core numbers, do not approve the fix |

| Payback period | Time required to recover the intervention cost | Lets alternatives be compared on the same basis |

For each cohort, calculate:

- Lost contribution

Contribution margin per active freelancer or payout-active account, multiplied by churned accounts in that cohort.

- Recovery value

Contribution you expect to preserve or recover if the intervention works. If churn appears payment-failure-driven, anchor this to observed recovery analytics where available.

- Intervention cost

Engineering time, operations headcount, vendor cost, refunds or credits, and ongoing support cost.

- Payback period

Time required to recover the intervention cost, so alternatives can be compared on the same basis.

Verification gate: finance should be able to reproduce lost contribution from Ledger exports for the same time window used in retention analysis. If product, ops, and finance cannot reconcile the core numbers, do not approve the fix.

Keep observed loss and modeled recovery separate. Lost contribution can be observed; projected recovery is a hypothesis unless supported by prior experiments, recovery analytics, or holdout results.

Compare intervention classes on economic path and evidence strength#

Put intervention classes side by side before roadmap decisions:

| Intervention class | Primary economic path | Best fit signal | Confidence source | Common risk |

|---|---|---|---|---|

| Pricing model change | Improves retention by changing fee fairness or packaging | Churn spike follows fee or packaging exposure | Retention analysis by pricing exposure, Ledger margin view | Correlation is misread and price changes miss the real driver |

| Payout-speed improvement | Reduces involuntary churn tied to payment failures or banking issues | Churn clusters before first successful payout or after failed payout attempts | Ledger payout outcomes, recovery analytics, retry results | Speed improves, but destination or routing errors remain |

| Merchant of Record simplification | May reduce operational or compliance friction blocking activation or payout readiness | Drop-off clusters around entity, tax, or cross-border operating complexity | Activation funnel, compliance fallout, cost model assumptions | Simplification is funded before cohort size or impact is proven |

| Support-ops escalation | Recovers at-risk accounts through faster exception handling | Small high-value cohort with repeated unresolved payout or verification issues | Ticket resolution data, cohort contribution, prior save rates | Cost scales faster than retained contribution |

Use an if-then rule: if churn is concentrated before first successful payout, prioritize payout reliability first. If churn spikes after fee changes, test pricing and packaging first, while checking for concurrent product or ops changes in the same window.

Score confidence and set a kill rule before launch#

Add confidence scoring to each estimate: High for direct Ledger or observed retention data, Medium for one modeled assumption, Low for mostly directional estimates.

Use a holdout as the effectiveness gate where possible, and run long enough to detect signal, typically 1 to 3 months. For payment-recovery assumptions, document operational defaults you are using, for example 8 tries within 2 weeks, so defaults are not mistaken for observed platform performance.

Set a kill rule before launch: if holdout performance is better than exposed performance, or measured recovery cannot repay intervention cost in your model, stop and reallocate.

This pairs well with our guide on The Gig Economy Gender Gap and Why Female Freelancers Face More Late Payments.

Diagnose root causes in payouts, compliance, and pricing friction#

After you have the economic case, run root-cause triage in this order: payout failures and payout batch behavior, compliance gates, then pricing and fee fairness. That sequence prevents false pricing conclusions when a cohort was never payout-eligible.

| Diagnostic area | What to verify | If unclear |

|---|---|---|

| Payout-stage churn | Trace sampled accounts from application action to API request identifier, related Webhooks, and Ledger linkage through balance-transaction records; preserve transaction-to-payout associations for automatic payouts | Pause the root-cause claim; mismatched request IDs, incomplete Webhooks chains, or missing Ledger links indicate observability debt, not proven payout-driven churn |

| KYC, KYB, and AML gates | Check requirement state changes, document-submission timestamps, and support contact timing near abandonment | If timing is unclear, label the conclusion as uncertain instead of defaulting to a pricing narrative |

| Tax-document friction and fee fairness | Evaluate pricing only after payouts and compliance are ruled in or out; use sequence evidence for W-8BEN, W-9, or tax-readiness prompts shortly before abandonment | If data is thin, state the cause as unknown and list the missing evidence |

Reconstruct payout-stage churn before you blame pricing#

Start by proving payout failure for the highest-loss cohort that churns before first successful payout or soon after a failed withdrawal. Use an evidence chain for sampled accounts: API request identifier, related Webhooks, and Ledger linkage through balance-transaction records.

If you use automatic payouts, preserve transaction-to-payout associations so you can verify what actually happened. The checkpoint is simple: for one churned account, can you trace the path from application action to event history to ledger-style transaction outcome? If not, pause the root-cause claim. Mismatched request IDs, incomplete Webhooks chains, or missing Ledger links indicate observability debt, not proven payout-driven churn.

Test KYC, KYB, and AML gates as payout blockers#

If payout reconstruction does not show a clear payment failure, test compliance next. KYC and KYB requirements can block payout eligibility, and AML/CFT controls can introduce review states that stall payout readiness even when product activity looks normal.

Check requirement state changes, document-submission timestamps, and support contact timing near abandonment. Then ask: did an unmet KYC or KYB requirement appear before the user stopped returning, and was it resolved? If timing is unclear, label the conclusion as uncertain instead of defaulting to a pricing narrative.

Audit tax-document friction and fee fairness, then write the caveats#

Only evaluate pricing and perceived fee fairness after you rule payouts and compliance in or out. A pricing hypothesis is stronger when churn aligns with fee or packaging exposure and the same cohort does not show payout or compliance blockers.

Audit tax/document prompts separately because this friction often appears as abandonment, not clean errors. W-8BEN is used by a foreign individual to establish foreign status, and Form W-9 is used to provide a correct TIN to payers filing information returns; in nonemployee flows, 1099-NEC handling can be part of document readiness. In cross-border cohorts, unclear FEIE guidance or uncertainty around FBAR (FinCEN Form 114, including the $10,000 aggregate foreign-account trigger) can add friction, but do not present these obligations as universal.

Use sequence evidence here too: did a W-8, W-9, or tax-readiness prompt appear shortly before abandonment, and is there support or UI evidence of confusion? If data is thin, do not claim you know why freelancers leave. State the cause as unknown and list the missing evidence. Related: How to Pay US-Based Freelancers from the UK.

Choose fixes with explicit decision rules and ownership#

Turn diagnosis into execution by assigning one ranked fix per owner, each with a deadline, a success metric, and a rollback condition. Keep the decision stage-specific: activation churn needs activation fixes, while repeat-stage churn needs repeat-stage fixes.

| Owner | Apply this fix when... | Success check | Rollback condition |

|---|---|---|---|

| Product | Drop-off happens before first successful payout, with evidence of onboarding/KYC/document UX friction | Sign-up to verification completion, then first successful payout | Verification completion rises but first successful payout does not |

| Payments ops | Churn starts after earnings or around failed withdrawals | Repeat payout success and exception resolution by payout cycle | Support load rises and repeat cohorts do not return |

| Finance | Payout/compliance blockers are ruled out for that cohort | Retained payout volume and margin | Volume increases without payback |

| Compliance | Abandonment follows an unmet requirement | Completion of required checks before payout eligibility | Review queues or unresolved holds expand |

Use scenario contrast to avoid blunt fixes. Cohort analysis should separate activation problems from retention problems before you ship.

Choose rails by friction source, not by preference:

- Use Merchant of Record (MoR) when the core issue is seller liability and payment-processing responsibility, for example refunds, chargebacks, tax handling, and audit burden.

- Use Virtual Accounts when the issue is inbound bank-transfer handling and reconciliation.

- In both cases, confirm market/program coverage before rollout.

Require proof before scaling. Run a holdout with 2 groups (treatment and control), and treat pre/post as supporting context, not causal proof.

- Operational checkpoint (Webhooks): verify the intended event path fired, was delivered, and matched the expected account or payout-state change.

- Financial checkpoint (Ledger): verify the same cohort produced the expected downstream result, for example more first successful payouts, fewer failed repeats, or recovered payout volume.

If either checkpoint fails, stop expansion and keep the change local.

Common mistakes and how to recover without burning roadmap time#

Most wasted retention work comes from fixing the wrong thing. If your evidence is thin, narrow the test, rebuild the event map, and pause broad roadmap changes until the operational trace is clean.

Mistake: using a generic churn template as freelancer truth. Recovery: rebuild the map around freelancer-platform stages and contractor-specific churn events. If the event cannot be reconstructed for the same cohort across API records, Webhooks, and ledger outcomes, treat it as unproven.

Mistake: cutting pricing before proving cause. Recovery: run a constrained holdout on the affected cohort and judge results on retained payout volume or recovered margin. If churn persists, shift the investigation to payout reliability and compliance timing instead of expanding discounts.

Mistake: approving strategy without an evidence chain. Recovery: require traceability from API request identifier to webhook event to ledger result before scaling a fix. Include idempotent request handling in your checks so retries do not create false signals, and use the webhook redelivery window (up to three days) to recover missing events before calling behavior "real."

Mistake: delaying tax and compliance communication until late stage. Recovery: set expectations early. Explain that U.S. payees may need Form W-9 to provide a correct TIN for information return reporting, and define a clear trigger for Form W-8BEN when requested by the payer or withholding agent; then match that with plain account-verification language.

As one finance operator put it, fragmented processes mean reporting becomes reactive and scaling gets harder under tighter regulation.

Conclusion and copy-paste execution checklist#

If you take one rule from this guide, make it this: do not treat freelancer exits like generic customer attrition. Define the exit where it happens in the journey, prove it with traceable evidence, and only then choose a fix.

- Define churn by stage, not by a generic "left" label.

Map your freelancer journey into operational stages such as sign-up, verification, first earnings, first payout, and repeat payout. Then name the churn event in platform terms: stalled verification, failed payout, unresolved hold, or no return after first successful payout. Verification point: for each stage, ask whether the event can be reconstructed from your product data plus financial records without manual guesswork. If not, your definition is too vague to act on.

- Validate the evidence chain before you approve a fix.

Pull the same analysis window across API data, Webhooks, and payout reconciliation exports. The evidence pack should show the account or payment event, the payment lifecycle or balance-state change, and the related financial movement such as payments, payouts, fees, and balance changes. Failure mode to watch: missing webhook acknowledgements can create false silence. One published webhook pattern retries failed deliveries up to 8 times at 5m, 10m, 15m, 30m, 1h, 4h, 12h, and 12h. If your app record and financial records disagree, treat that as observability debt first, not proof of user intent.

- Segment cohorts before intervention.

Cohort retention analysis matters because aggregate metrics blend different groups and hide where the real loss sits. Split cohorts by start time first, then by factors tied to monetization and operations, such as payout rail, geography, compliance path, pricing exposure, and lifecycle stage. Decision rule: if new freelancers are dropping before first payout, do not average them together with mature freelancers who churn after payout friction. Those are different problems with different owners.

- Rank fixes by unit economics and ownership.

Put each proposed fix next to its expected impact on contribution, recovery cost, margin sensitivity, and time to payback. Also assign a named owner and cross-functional partner set, because churn analysis is used across multiple teams and vague ownership slows execution. Recommendation: if the loss clusters before first successful payout, fund payout reliability first. If churn starts after a fee change, test pricing or packaging before rebuilding onboarding.

- Test with explicit success and kill rules, then log unknowns.

Use a holdout group so you can judge incremental impact instead of declaring victory from noisy pre/post movement. Write the success rule, the rollback condition, and the unknowns before launch, including market, program, seasonality, and external campaign constraints. Credibility check: do not claim root cause or ROI uplift when confounders remain. A disciplined note that says "evidence points to payout friction, but market effects are still unresolved" is far more useful than a confident guess.

Related reading: How to Build a Trust and Safety Program for Your Contractor Marketplace.

Frequently Asked Questions

What is contractor churn analysis and how is it different from customer churn analysis?

Customer churn analysis looks for why customers cancel, not just how many leave. Contractor churn analysis uses the same logic, but the causes are often tied to onboarding, activation, payment, and communication events rather than a simple subscription cancel. For a marketplace, that means reading churn through journey stages like first earnings and first successful payout, not only account closure.

Why do freelancers leave platforms even when demand for work is stable?

Demand is only one part of the experience. Contractors often leave when onboarding, activation, payment, and communication break down. The draft figures are a useful reminder of the scale: 33% of contingent workers leave within six months, with up to 44% leaving in the first 60 days. Late payment is a practical red flag too: a Q1 2024 survey found 32% of freelancers had experienced delayed payment in the prior 12 months.

Which metrics should a marketplace track first for customer retention in freelancer cohorts?

Start with cohort retention, because grouped start cohorts show who returns over time instead of flattening everyone into one rate. Then track stage conversion tied to revenue risk: activation to first earnings, first earnings to first payout, and first payout to repeat payout. If one cohort stalls before repeat payout while another does not, you have something operational to inspect instead of a vague attrition story.

How do payout experience and payout batches influence churn risk?

Payout experience can create involuntary churn when banking or payment issues interrupt the freelancer’s ability to get paid. If churn clusters after failed or delayed payout batches, treat that as an operations problem first and confirm it by checking whether the payout state change appears in both your application records and webhook payloads. A common failure mode is assuming the user chose to leave when the real cause was a payment failure or bank issue outside their control.

When should a team change the pricing model versus fixing compliance and payout operations first?

Change pricing when a churn spike clearly lines up with a fee or package change and a constrained test shows recovery. Fix payout operations first when losses are concentrated around payment failures or delayed payouts, because those exits may be recoverable without broad fee cuts. If compliance is a suspected driver, treat it as a hypothesis and verify it with stage-level cohort and event data before making broad pricing changes.

How can API and Webhooks instrumentation improve retention analysis confidence?

Webhooks help because payment platforms can push real-time event data when account events happen, which is especially useful for asynchronous payment-state tracking. Your checkpoint is not “we have logs,” but “we can match the cohort event in application records to the webhook event that confirms it happened.” That improves confidence, but it still does not prove causality on its own.

What should leaders do when evidence is incomplete but churn is rising?

Slow the decision, not the investigation. Report the churn as observed behavior, separate known operational events from unknown causes, and fund the smallest fix that also improves visibility, such as better webhook coverage for payment and account-state events. If the evidence is thin, avoid broad roadmap changes or pricing resets until the retention analysis has context behind the numbers.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 4 external sources outside the trusted-domain allowlist.

- docs.stripe.com/webhookstrusted

- docs.stripe.com/webhooks/handling-payment-eventstrusted

- irs.gov/forms-pubs/about-form-w-9trusted

- irs.gov/forms-pubs/about-form-w-8-bentrusted

- amplitude.com/explore/analytics/churn-analysisexternal

- corporatefinanceinstitute.com/resources/valuation/nrr-meaning-calculation-...external

- fatf-gafi.org/en/publications/Fatfgeneral/Effectiveness.htmlexternal

- mercury.com/blog/understanding-unit-economicsexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

Streaming Platform Churn Analysis: Why Subscribers Leave OTT Services and How to Win Them Back

If you are doing **streaming platform churn analysis OTT**, your first move is not a discount or a copy of whatever a major platform just tried. First separate temporary churn from structural churn, then choose the retention lever that fits the exit pattern before you scale into another market.

How to Pay US-Based Freelancers from the UK

Your ability to attract and keep strong US freelance talent depends less on budget than on how you operate. Strong freelancers often work like serious one-person businesses, and they start evaluating you from the first interaction. Compliance and payment handling are not back-office details. They are early proof that you will be easy to work with, careful with details, and worth prioritizing.

How to Pay US-Based Contractors from Australia

Engaging U.S. talent can be a smart growth move for an Australian business. But paying a cross-border contractor is not just an admin task. If you handle it reactively, you create compliance risk, unnecessary cost, and record gaps that are hard to repair later.