Quick Answer

Start by mapping your flows as receive, hold, convert, and payout, then select the account model that matches the required capability. A business foreign currency account is usually the right fit when you need cross-border currency operations but not full local-bank services. Use an in-country structure only when local rails or domestic tax-payment functions are mandatory. Before go-live, verify KYB/KYC completion, quote-expiry handling, webhook status reliability, and Finance sign-off on ledger reconciliation.

Choose the account model before comparing providers#

If you are setting up contractor, creator, or marketplace payouts, decide the account type before you compare providers. That choice affects FX cost, onboarding speed, and how much work Finance, Ops, and Engineering inherit later.

The three options sound similar, but they do different jobs. A business foreign currency account is built to make, receive, and convert payments in foreign currencies. A multi-currency account lets you hold, manage, and transact in multiple currencies from one account. An in-country bank account is the heavier option when you need true local banking overseas, such as branch deposit handling or the ability to initiate tax payments electronically. If you blur those lines and buy off homepage language alone, you can end up rebuilding your payout flow around limits you should have caught at the start.

| Account path | Usually fits when | Verify first | Main tradeoff |

|---|---|---|---|

| Foreign-currency account | You need to make, receive, and convert payments across borders without full local banking operations | Which currencies you must actually receive and pay out, and where FX conversion happens | Good for currency operations, but not the same as local banking depth |

| Multi-currency account | You want one account structure that supports several currencies and may reduce the need for separate foreign-country accounts | Whether your real corridors, collections, and payout routes are supported, not just listed | Flexible structure, but you still need to confirm local capability gaps |

| In-country bank account | You need true local-bank services in a market | Whether local branch deposits or electronic tax-payment initiation are required | More local depth, but setup can be much slower |

The timeline difference alone is enough to make this decision early. U.S. Bank says opening a foreign currency account in the U.S. typically takes a week or less, while opening an in-country account can take months, sometimes six or more. That does not make one path universally better. It means the cost of being wrong is not just pricing. It may also include delayed launch timing, extra engineering workarounds, and controls that Finance and Ops never wanted to own.

Before you start#

Use one quick checkpoint before you compare providers. Write down each money flow as receive, hold, convert, or payout, then ask a hard question: do you need currency access, or do you need local banking services in a specific country? If the answer is local tax payments or branch-level banking, keep in-country banking in scope. If not, focus on foreign-currency and multi-currency options first.

This guide is intentionally narrow: help you make one defensible choice, move into onboarding faster, and launch with controls that Finance, Ops, and Engineering can actually run. The next step is to choose the account type before you worry about who offers it.

Pick the account type before you pick a provider#

Pick the capability first, then the provider. If you do not need in-country banking services, start with foreign-currency or multi-currency options and only move to a local bank structure when a country requirement is explicit.

Step 1 Choose a foreign-currency account for cross-border money movement#

Choose a business foreign currency account when you mainly need to receive, hold, convert, and send funds across borders without full in-country banking services.

Map each flow as receive, hold, convert, or payout, then check whether any step requires a local branch, local tax-payment initiation, or another domestic banking function. Currency access and local banking depth are not the same thing.

Step 2 Choose a multi-currency account when flexibility matters more than local-bank depth#

Choose a multi-currency account when you need to manage several currencies in one setup. A multi-currency account holds multiple currencies in one account, while a foreign-currency account typically holds one.

Before committing, verify the currencies you can actually hold and whether local rails are available in your real corridors. A long supported-currency list is not enough if you need domestic collection or payout behavior in a specific market.

Step 3 Choose an in-country bank account only when a local requirement is real#

Use an in-country bank account when local rails, domestic tax payments, or country-native operations are mandatory. In Singapore, GIRO must be set up with an SGD savings or current account at a GIRO-participating bank, and hard-copy GIRO applications can take up to 21 working days.

The main tradeoff is time: a U.S.-based foreign currency account may open in a week or less, while an in-country account can take months, sometimes six or more. If no local requirement is explicit, avoid taking that delay by default.

If you want a deeper dive, read How to Set Up a Business Bank Account in Singapore as a Foreigner.

Gather the evidence pack before onboarding starts#

Build the evidence pack before you contact providers so onboarding decisions are based on verified documents, tax handling, and real flow coverage, not assumptions. Keep one shared folder and a short operating note covering who the entity is, who controls it, who can sign, which tax forms apply, and which money flows you need to run.

Step 1 Assemble entity, ownership, and signer documents#

Start with incorporation records, beneficial ownership details for KYB, and signer identity documents for KYC. For legal-entity onboarding, beneficial-owner collection and identity verification are required at account opening under risk-based procedures.

Use a practical check before submission: entity records and ownership details are current, and signer names match the IDs you will upload.

Step 2 Define tax handling before the first payment flow#

Decide upfront which counterparties provide Form W-8BEN and which provide Form W-9, then confirm your records can support Form 1099-NEC where needed. W-8BEN is provided by a foreign beneficial owner to a payer or withholding agent, and W-9 is used to provide a correct TIN for IRS information returns.

| Item | When it applies | Key detail |

|---|---|---|

| Form W-8BEN | Provided by a foreign beneficial owner to a payer or withholding agent | Decide upfront which counterparties provide it |

| Form W-9 | Used to provide a correct TIN for IRS information returns | Decide upfront which counterparties provide it |

| FBAR | Can apply when aggregate foreign account value exceeds $10,000 at any point in the calendar year | Due April 15 with an automatic extension to October 15 |

Make an explicit FBAR call and document it. FBAR reporting can apply when aggregate foreign account value exceeds $10,000 at any point in the calendar year; the due date is April 15 with an automatic extension to October 15.

Step 3 Map flows by corridor, currency, and rail#

Validate coverage at the flow level: collection, conversion, and payout by exact corridor and currency pair. Headline country and currency counts do not confirm that your required route and rail behavior are available for your use case.

Your check is simple: can you collect in the needed currency, hold or convert it as planned, and send it on the required rail in the destination corridor?

Step 4 Assign owners for policy, exceptions, and status ingestion#

Assign owners before submission so failures and status changes are not orphaned at launch. A practical split is Finance for policy gates and document completeness, Ops for exception handling, and Engineering for webhook ingestion and internal status mapping.

Treat status ingestion as a launch requirement, not a later task. Providers expose transfer-status webhook events, so you should confirm event destination, retry handling, and internal state mapping before going live.

For a step-by-step walkthrough, see How to Determine the Maximum Value of a Foreign Bank Account for FBAR.

Compare bank-led and fintech-led options with a decision matrix#

Choose based on verified execution, not headline pricing. If you cannot verify corridor coverage, status granularity, and exception handling before signing, treat that provider as high implementation risk.

Step 1 Build the matrix with verified facts first#

Use the evidence pack from the last section. Mark anything unverified as unknown.

| Provider | Eligibility | Supported corridors and payout reach | Conversion model | Operational visibility | Known vs unknown | Main implementation risks |

|---|---|---|---|---|---|---|

| U.S. Bank | Positions a U.S.-based foreign currency account as a fit when you do not need in-country banking services. Published setup contrast: U.S.-based opening is typically a week or less; in-country accounts can take months. | Confirm corridor, currency, and payout-method coverage directly with the provider. | Foreign-currency holding is clear; quote mechanics and spread detail are not verified here. | No webhook or payment-status evidence was captured in this review. | Known: U.S.-domiciled option, faster setup framing. Unknown: exact corridor support, payout event data, exception tooling. | FX exposure if conversion happens outside a controlled policy point. Timing risk remains until corridor behavior is confirmed. Ledger mapping may depend on statement or file formats unless richer integration is available. |

| HSBC USA | Global Money has explicit eligibility: you can apply if you have Premier checking. | Hold up to 8 currencies; send in 60+ currencies to 200 countries and regions. | Hold and convert multiple currencies in one account. This review does not support like-for-like spread comparisons. | HSBC developer materials show a payment status enquiry API for treasury payment initiation; confirm your product path has equivalent access. | Known: clear eligibility and broad transfer footprint. Unknown: whether your account path exposes the same status depth and exception data. | FX exposure depends on hold-versus-convert choices. Settlement timing still varies by corridor. Reconciliation quality depends on whether references and statuses map cleanly into your ledger. |

| Wise | Wise Business shows business coverage in 80+ countries. | Hold 40+ currencies and get receiving account details in 8+ currencies. | Hold, convert, and send money. Precise pricing and spread comparisons are not verified from this review alone. | No status or webhook source for Wise is included in this section pack, so treat visibility as unverified until shown. | Known: strong multi-currency hold and receive footprint. Unknown: event model, exception workflow, corridor-specific settlement detail. | FX risk appears when balances sit unconverted or are converted ad hoc. Timing depends on route. Ledger mapping needs a field-level export check, not only a dashboard demo. |

| Airwallex | Public pages support business-account positioning, but precise eligibility rules were not fully captured in this reviewed set. | Local bank details in 60+ countries; send money to 150+ countries; 120+ countries use local payment rails. | Public pages support a multi-currency model, but detailed conversion mechanics were not fully captured here. | Transfer and batch transfer webhook events for status changes are documented. | Known: local account-detail reach, payout breadth, webhook status surface. Unknown: exact eligibility for your entity and corridor-level exception behavior. | FX exposure depends on when you convert relative to payout. Local rails can improve timing, but not every corridor behaves the same way. Ledger mapping should use webhook event IDs plus transfer references. |

Step 2 Treat unknowns as delivery risk#

Unknown cells are not neutral. They usually surface later, when Finance expects close-ready data and Ops is handling payout failures.

Prioritize these checks:

- Coverage at flow level

Confirm one real route end to end: receive in currency X, hold it, convert it, and pay out in country Y on the rail you need.

- Status depth, not just status existence

Ask for sample webhook payloads or status enquiry responses with more than "completed" and "failed," including pending, returned, cancelled, and review states where available.

- Reconciliation fields that map to your ledger

Ask for sample export or API output with stable IDs, amount, currency, fees, rate or conversion reference (where applicable), beneficiary details, and remittance/internal reference fields.

Reconciliation quality should carry real weight. HSBC publishes a virtual accounts case reporting a 75% reduction in weekly reconciliation time. That is not a product-wide promise, but it is a practical signal that clean references and status data can outweigh a slightly lower apparent FX line item.

Step 3 Apply a simple implementation rule#

If you need faster setup and do not need in-country banking depth, a U.S.-based option may fit. If you need broader multi-currency holding, receiving details, and stronger payout visibility, fintech-led options may fit better, but only after corridor and exception-path verification for your real flows.

The common failure mode is the same across banks and fintechs: one missing route, one thin status model, or one export Finance cannot reconcile. Before signing, require one proof pack for your highest-volume flow plus one failure scenario. If a provider cannot show both, classify it as high implementation risk and keep comparing.

Related: Wise Business vs. Revolut Business: A Head-to-Head Comparison. For a practical next step, try the free invoice generator.

Open and activate the account in seven execution steps#

Treat account activation as a controlled launch. If you cannot verify identity status, permissions, receiving coverage, quote-expiry handling, and reconciliation output before the first live payout, delay go-live.

- Submit onboarding data and complete KYC and KYB checks.

Provide the required entity and identity information, then track review states until approval is explicit. If available, enable KYC review-state webhooks early so Ops can monitor status changes without manual chasing.

- Confirm the approved entity, users, and role permissions.

Verify which entity was approved and test who can do what before operational use. Role-based access should match real responsibilities so the right people can act and see what they need.

- Configure receiving details and Virtual Accounts where supported.

Set up the first receive routes you plan to use, then confirm currency and account-detail coverage on those exact flows. Do not assume virtual/global receiving coverage in every corridor, and confirm transaction details are usable for reconciliation.

- Enable payout destinations and compliance policy gates.

Add only initial payout destinations and confirm what controls can still hold release. KYC/KYB completion alone does not guarantee immediate payout enablement.

- Test FX conversions with quote-expiry handling built in.

Use live quote data and enforce the provider validity window instead of relying on copied rates. In one documented Wise flow, quotes expire after 30 minutes; reject stale quotes by design and request a fresh one.

- Run small-value end-to-end tests for receive, convert, and payout.

Start in sandbox or simulation where supported, then run a small live transaction. Validate statuses, references, and amounts across the full chain, including one non-happy-path test if simulation supports it.

- Get Finance sign-off on reconciliation exports against your ledger.

Before launch, validate a real export or API payload with Finance. They should be able to match transaction ID, amount, currency, fee, conversion or quote reference (where applicable), and internal reference cleanly.

We covered this in detail in How to Open a Stripe Account for a Non-US Business.

Set day-one controls for FX, compliance, and reconciliation#

After your first live tests pass, lock the operating rules before volume arrives. The goal is simple: conversions, release checks, and event tracing should run on policy, not payout-day judgment.

| Control area | Rule | Evidence or trigger |

|---|---|---|

| FX conversion | Set a default rule for each flow: instant convert, threshold-based convert, or scheduled convert; restrict overrides | Each conversion record should include flow type, rate or quote reference, approver, and timestamp |

| Compliance release | Make AML and KYC status a release gate with states such as hold, in review, cleared, and refused | Where EU VAT status is relevant, validate with VIES and store the result used for the decision |

| References | Store both the provider reference and your internal journal reference on every receipt, conversion, and payout | Example pattern: Wise data.action.id to referenceNumber |

| Events and exceptions | Treat failed webhooks, unmatched deposits, and payout returns as incidents | Model statuses including refused, failed, and credited; if status events are missing, route to active investigation immediately |

- Define conversion rules by flow, then restrict overrides.

Set a default conversion rule for each flow: instant convert, threshold-based convert, or scheduled convert. Then define who can override, which reason codes are allowed, and where that reason is recorded. As a control check, each conversion record should include flow type, rate or quote reference (where available), approver, and timestamp.

- Block release on explicit compliance states.

Make AML and KYC status a release gate with clear states such as hold, in review, cleared, and refused. Keep identity checks risk-based, not document-only, since CIP is part of AML compliance controls. Where EU VAT status is relevant, validate with VIES before release and store the result used for the decision; treat VIES as an EU cross-border check tool, not a global VAT database.

- Require provider and internal references on every money movement.

For every receipt, conversion, and payout, store both the provider reference and your internal journal reference. This is what makes ledger tracing and audit follow-through practical. A concrete pattern is matching notification IDs to statement reference fields, for example Wise data.action.id to referenceNumber, so every movement can be reconciled.

- Treat missing events and exception statuses as incidents.

Failed webhooks, unmatched deposits, and payout returns should trigger incident handling, not back-office cleanup. Build for asynchronous recovery windows and bounded replay history, for example retry and retrieval limits, and model payout lifecycle statuses explicitly, including refused, failed, and credited. If status events are missing, route to active investigation immediately.

Related reading: Setting Up a Business Bank Account for a New LLC.

Align Finance, Ops, and Engineering on operating ownership#

Set operating ownership before go-live so approvals, exceptions, and retries do not stall in shared queues.

| Team | Primary ownership | Named responsibilities |

|---|---|---|

| Finance | Approvals, tax artifacts, and close | Own Form W-9 collection and review, Form W-8BEN handling when requested by the payer or withholding agent, and 1099 threshold and calendar logic |

| Ops | Investigations and payout exception queues | Investigate failed payouts, unresolved holds, and missing status events; run a weekly control review for the first 90 days |

| Engineering | Idempotency behavior, webhooks, and provider-event mapping into your internal ledger | Implement idempotent requests so retries do not create duplicate operations, handle duplicate webhook deliveries, and test replay and retry paths before launch |

- Assign clear owners for each production lane.

Use a simple split: Finance owns approvals, tax artifacts, and close; Ops owns investigations and payout exception queues; Engineering owns idempotency behavior, webhooks, and provider-event mapping into your internal ledger. Name a primary owner, backup, and escalation path for each lane before launch.

- Put Finance in charge of tax evidence and payout gates.

Finance should own Form W-9 collection and review when payer reporting obligations apply, and Form W-8BEN handling when requested by the payer or withholding agent. If 1099 reporting is in scope, Finance should also own threshold and calendar logic, including the IRS FAQ language showing $600 and $2,000 (for certain payments made after December 31, 2025). Track tax-form status, approver, and payout rule when forms are missing.

- Make Engineering accountable for retry and event integrity.

Engineering should implement idempotent requests so retries do not create duplicate operations, and webhook consumers should handle duplicate event deliveries. Before launch, test replay and retry paths and confirm they produce one intended business outcome and one correct ledger effect.

- Make Ops accountable for investigations and control review cadence.

Ops should run the payout exception queue, investigate failed payouts, unresolved holds, and missing status events, and escalate through the documented path. For the first 90 days, run a weekly control review on conversion outcomes, failed payouts, unresolved holds, and reconciliation breaks. Include payout-to-transaction linkage evidence in that review where your provider preserves that association, and keep breaks open until references map cleanly.

This pairs well with our guide on How to Handle Realized and Unrealized Gains/Losses on Foreign Currency.

Avoid the five rollout mistakes that cause costly rework#

Costly rework usually starts when teams go live with unresolved provider and control assumptions. The fix is to treat unknowns as launch blockers before the first payout.

- Choosing by marketing copy instead of a structured matrix.

Compare U.S. Bank, HSBC USA, Airwallex, and Wise in one operating matrix: entity eligibility, receive/payout corridors, conversion behavior, reconciliation exports, and exception visibility. Public positioning is useful but not sufficient: U.S. Bank emphasizes minimizing conversions, HSBC Global Wallet markets multi-currency flows from one US-domiciled account, Airwallex markets local accounts in 20+ currencies and receiving from 70+ countries, and Wise states businesses can hold 40+ currencies. If your exact corridors or status outputs are not confirmed in writing, mark the row unresolved.

- Deferring compliance design until after onboarding.

Map KYC/KYB/AML gates before funds move. Beneficial-owner identification and verification procedures are part of AML program obligations, so define controls at account opening, beneficiary setup, fund release, and hold/review handling.

- Using wallet balances as system truth.

Treat wallet or account balances as operational views, but reconcile from your internal ledger and event history. In manual payout models, you are responsible for matching payouts to transaction history; if a payout cannot be tied to both provider references and journal entries, keep it open as a reconciliation break.

- Separating provider choice from implementation design.

Provider selection and go-live design are the same decision stream: corridor fit, status granularity, failure states, and reconciliation outputs. If those details appear only after contract signature, risk discovery is happening too late.

- Logging unknowns as post-launch tasks.

Unverified pricing, unclear eligibility, missing corridor confirmation, and vague failure statuses are launch blockers, not backlog items, when this account model sits at the center of collections, conversion, and payouts.

Need the full breakdown? Read How to Set Up a Business Bank Account in the UK as a Non-Resident.

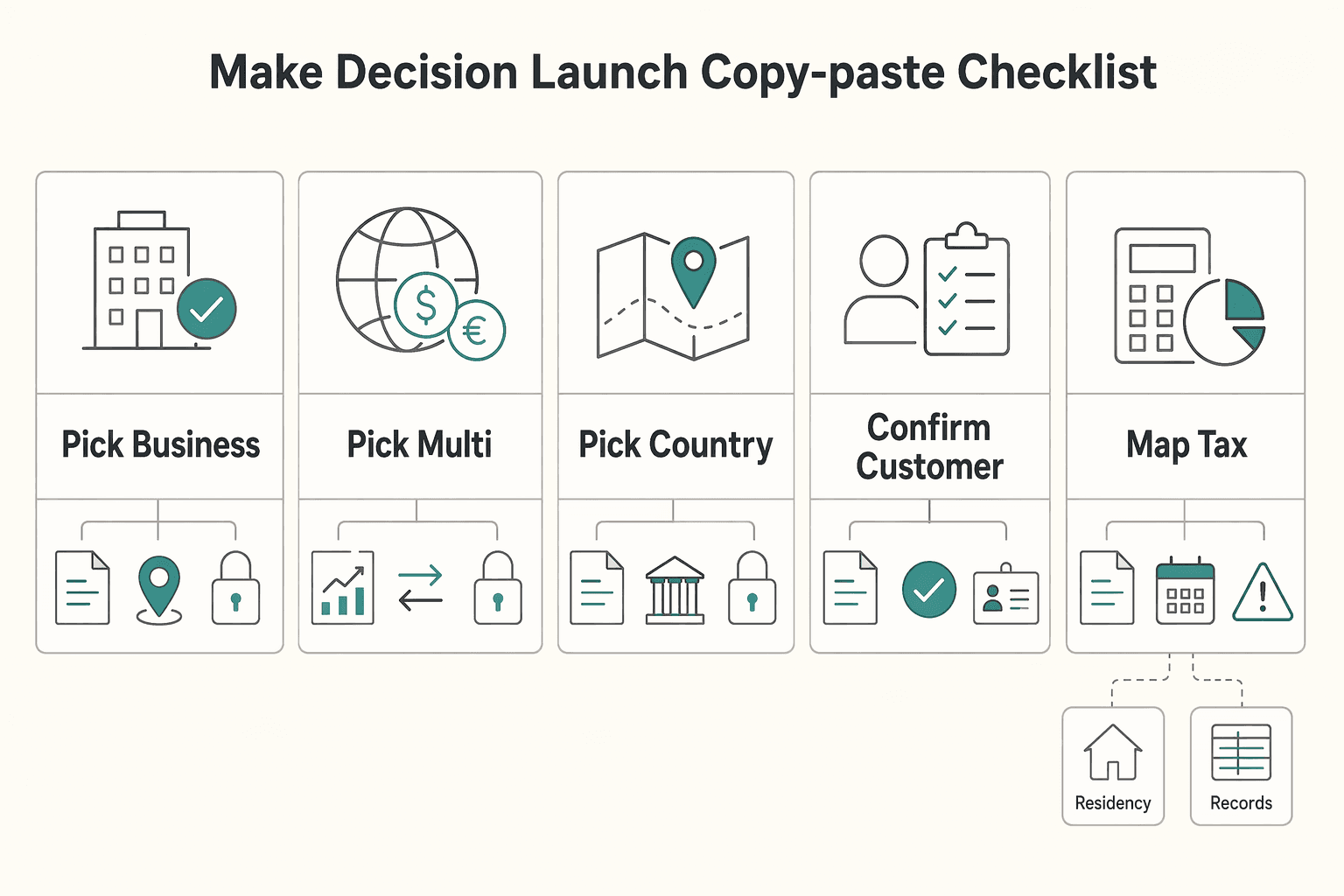

Make the decision and launch with a copy-paste checklist#

Choose the account path now, then treat everything else as launch readiness.

Step 1. Choose the account path by the local capability you actually need.

- Pick a business foreign currency account for routine foreign-currency business flows.

- Pick a multi-currency account when you need flexibility across currencies and want to reduce opening foreign-bank accounts.

- Pick an in-country bank account only when local rails or country-native banking tasks are required.

Verification point: write one sentence that starts with "We need local capability for...". If you cannot name that requirement, do not default to an in-country account.

Step 2. Lock the evidence pack before onboarding.

- Confirm customer identifying information and beneficial-owner verification are complete before account opening.

- Map tax forms by counterparty: use Form W-9 for TIN information reporting, and submit Form W-8BEN when requested by the payer or withholding agent.

- Finalize your corridor list and policy owners so reviews do not stall in email threads.

Verification point: for each payout counterparty type, answer "W-9, W-8BEN, or neither?" immediately.

Step 3. Validate minimum go-live controls.

- Define your

FXrule set: when conversion happens and who can approve exceptions. - Define

AMLhold handling so Ops knows when release stops and who reviews the case. - Treat webhooks as real-time but potentially duplicated, and implement duplicate-event handling.

- Require reconciliation checks that match transaction records against accounting records and ledger entries.

Step 4. Run a controlled pilot, then scale payouts. Run small live flows across real corridors, review failures, and fix repeat issue classes before expanding volume or geography. Scale only after Finance, Ops, and Engineering all confirm reconciliation, exception handling, and event monitoring are working as expected. For country- or program-specific support, Talk to Gruv.

Frequently Asked Questions

What is a business foreign currency account, and how is it different from a multi-currency account?

A business foreign currency account is usually a domestic, bank-based setup for holding funds in a non-home currency when you do not need local in-country banking services. A multi-currency account is broader. It uses one account model to hold, send, and receive multiple currencies without opening separate foreign bank accounts. In practice, the first question is not branding but scope: do you need one foreign currency at your home bank, or operating flexibility across multiple currencies?

When do I need an in-country bank account instead of a domestic foreign-currency setup?

You usually need an in-country account when local banking services are actually required, not just nice to have. If your flows rely on services that require local banking capability, a U.S.-based foreign-currency setup may be too limited. A good checkpoint is simple: ask the provider to confirm in writing whether your exact local receive and payout flows work without a local account.

What are the main FX risks during account setup and first production payouts?

The core risk is financial loss from exchange-rate movements between currencies. During setup and early payouts, that can show up when there is a delay between receipt, conversion, and payout. If you want a practical control, run small live tests first and verify the booked conversion rate, payout currency, and final ledger entry all match what Finance expects.

Which compliance checks should block payouts: KYC, KYB, AML, or all three?

At minimum, treat customer identification and beneficial-owner verification as blocking checks where applicable. Under 31 CFR 1020.220, customer identification procedures are part of the AML program, and under 31 CFR 1010.230, legal-entity onboarding must identify and verify beneficial owners. If signer identity, entity details, or beneficial-owner data is incomplete, payouts should generally stay on hold until the required information is complete.

What should Engineering validate first: webhooks, idempotency, or ledger reconciliation?

There is no universal first step, because the right order depends on how your money state changes are triggered. If provider events drive internal updates, test webhook delivery for duplicates, delays, and misses, but do not trust those events unless idempotency and ledger mapping are also proven. A practical checkpoint is that every movement can be tied back to both a provider reference and your internal journal reference.

How do I compare providers when fee and spread details are unclear in public materials?

Do not guess from homepage copy or partial pricing pages. Build a matrix with known and unknown fields for corridor coverage, conversion behavior, receive and payout support, exception visibility, and reconciliation exports, then ask for written confirmation on the missing items. Public claims like holding 40 currencies can be useful context, but if spread logic, payout fees, or status outputs stay unclear, treat that provider as higher implementation risk rather than cheaper by default.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- docs.stripe.com/webhookstrusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- europa.eu/youreurope/business/taxation/vat/check-vat-n...trusted

- iras.gov.sg/quick-links/payments/giro-individual-income-taxtrusted

- irs.gov/forms-pubs/about-form-w-9trusted

- irs.gov/forms-pubs/about-form-w-8-bentrusted

- stripe.com/resources/more/multicurrency-accounts-101trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How to Set Up a Business Bank Account in Singapore as a Foreigner

Treat this as an operations system - compliance, receiving rails, and reconciliation, not a one-time application form. It's part of your money ops stack. The real win is predictable cashflow: clients can pay you cleanly, you can explain every inflow, and you avoid unnecessary compliance back-and-forth.

Wise Business vs Revolut Business for Cashflow Reliability

Cashflow reliability should drive this choice before brand familiarity or feature sprawl. For freelancers, creators, and small teams, the real question is not which provider feels more established, but whether you can get paid predictably, understand the full cost of each settled invoice, and recover quickly when a payment path stalls.

Opening a Hong Kong Bank Account as a Foreigner With Fewer Delays

Opening a Hong Kong account as a foreigner is possible in some cases, but success usually comes down to eligibility and routing, not form filling. Access, document checks, and whether you can start remotely all depend on the provider you choose.