Quick Answer

Start by matching your legal setup across invoices, website details, and application data, then screen providers by eligibility, GBP receiving details, and review handling. For a uk business bank account non-resident setup, use a strict sequence: prepare an evidence pack, activate one workable route, and test a real payment flow immediately. After approval, document fallback rails, reconciliation checks, and export quality before holding meaningful balances.

Opening a UK business bank account as a non-resident director is one of the harder early operating tasks for a global founder. The process is full of inconsistent eligibility rules, preventable rejections, and risks you often only see after approval. The way through is not a loophole. It is a disciplined sequence.

This is not another bank list. It gives you a three-tier method for making the decision in the right order. First get paid, then protect your cash, then build something you can scale. We move from Tier 1, securing your first working UK payment route, to Tier 2, protecting capital and reducing review risk, to Tier 3, building a financial setup that can grow with the business. Follow that sequence and you stop searching for any account that opens. You start acting like the person responsible for the company's financial core.

Tier 1: The Foundation - Securing Your First UK Payment#

Your goal in this first tier is simple. Set up a payment route you can actually use, for the exact business setup you invoice from, with documents ready for review.

If you are searching for a uk business bank account non-resident, use this order: match your entity, screen providers, prepare evidence, then test the rail. A mismatch between those four can cause delays.

Step 1. Match the application to your real business setup#

Get the legal identity right first. Avoidable friction can start when your entity, invoices, and application do not describe the same business.

A sole trader is owned and run by one person, while a private limited company is a separate legal entity. Your invoices, website details, and account application should all reflect the same setup.

If you operate through a UK limited company, use the company's legal name and Companies House details consistently. Limited companies must file annual accounts and statements with Companies House. Those filings are published online, and the company is subject to stricter operating and record-keeping rules. If you are operating as a sole trader, do not present yourself as a limited company in your invoices or application.

Quick alignment check before you apply:

- Invoice header name

- Website footer business identity

- Companies House details, if applicable

- Application legal name

Tax registration still matters for clean operations. If you need to complete a Self Assessment return for the previous year and you are newly filing, or returning after not needing to file, you must notify HMRC by 5 October. You can submit returns after 5 April, and payment is due by 31 January. Missing the 5 October notification deadline can lead to a penalty.

Step 2. Screen providers before you submit any application#

Do not apply blind. For non-resident applicants, requirements can differ by provider, so confirm current guidance before you submit.

Before applying, confirm these points from the provider's own guidance:

- Whether your country of residence and business setup are eligible.

- Which business details and documents are required.

- How GBP receiving details are presented and whether they fit your invoicing setup.

- What happens if the application is paused for additional review.

Use your operating model, not brand familiarity, to shortlist options:

| Business model | Inbound payment route to verify | Currency handling question | Payout need | Integration and escalation check |

|---|---|---|---|---|

| UK client services, consulting, contractor work | Can clients pay in GBP to details that match your invoicing entity? | Do you need to hold or convert non-GBP income? | Lower-volume supplier or owner payouts | Can you export statements cleanly, and is there a support path if onboarding stalls? |

| Cross-border freelancer or small agency | Can overseas clients pay without confusion or extra friction? | Can you receive and hold the currencies you bill in? | Regular international payouts | Check accounting integrations and how account reviews are handled |

| Marketplace or online seller | Does the account support your platform settlement routes? | Are settlement currencies forcing unwanted conversions? | Frequent supplier, logistics, or refund payouts | Confirm the process if transaction patterns change |

Step 3. Prepare a pre-application evidence pack#

Submit only after you can support the story your application tells. A clean evidence folder can reduce back-and-forth. Keep one folder with current, readable files and a short business description.

| Evidence type | What to include |

|---|---|

| Identity evidence | Identity and address documents requested during verification |

| Company evidence | Company registration details, if using a UK company, plus ownership or director details you may be asked to confirm |

| Business-activity evidence | Sample invoices, signed contracts or proposals, website, and a plain-language summary of what you sell, who pays you, and where payments come from |

| Records for tax readiness | Bank statements or receipts |

- Identity evidence: identity and address documents requested during verification.

- Company evidence: company registration details, if using a UK company, plus ownership or director details you may be asked to confirm.

- Business-activity evidence: sample invoices, signed contracts or proposals, website, and a plain-language summary of what you sell, who pays you, and where payments come from.

- Records for tax readiness: bank statements or receipts, because you need records like these to complete tax returns correctly.

Common mismatches that can cause avoidable delays:

- Company name on invoices does not match the application.

- Address on ID does not match uploaded proof of address.

- Website description does not match the business activity entered in the form.

Step 4. Test the payment rail immediately after approval#

Approval does not automatically prove the route works for your real payment flow. Run a low-risk test: issue a small invoice or receive a small payment, then confirm references post correctly, statement exports work, and bookkeeping maps the payment to the right entity.

If onboarding is paused, respond with the specific evidence requested. Keep your business description, invoices, and account details consistent so your payment details and records flow match how you actually trade.

If you want a deeper dive, read Automating Your Freelance Finances: A Zapier Workflow for Connecting Stripe.

Tier 2: The Shield - Protecting Your Business from Catastrophic Risk#

Once your first payment route works, the next job is risk control: keep balances deliberate, keep records clean, and stay ready for reviews and tax admin.

Step 1. Verify account terms and fallback steps before you hold meaningful balances#

Before you leave real money in the account, verify what can happen if access is interrupted and what your fallback is. Rely on provider legal terms and support policies, not marketing shorthand, when you document this. Match your account setup to your highest likely balance, not your average day.

| Your cash-balance behavior | Account-terms check | Access-risk check during review | Support-path check | Suitability signal |

|---|---|---|---|---|

| Money in, money out quickly | What do the account terms say about access controls and account use? | What access limits can apply during review? | Is there a clear path to urgent support? | Usually easier to operate if you avoid large idle balances |

| You hold 1-2 months of operating cash | Do the terms fit the balances you actually hold? | Can you still run core payouts if a payment is reviewed? | What evidence may be requested, and how fast can you provide it? | Acceptable only if temporary friction is operationally manageable |

| You hold tax reserves or large client advances | Have you documented the terms that apply to long-held balances? | What is your fallback if access is restricted? | Do you know the escalation route in advance? | Use stricter controls on where cash sits and for how long |

Step 2. Reduce restriction risk with transaction hygiene and response discipline#

Transactions that are hard to explain after the fact can create review friction. Your job is to make each payment legible before anyone asks.

- Keep business identity consistent across invoices, website footer, application details, and Companies House records, if you trade through a limited company.

- Use clear payment references, for example invoice IDs, and confirm those references appear in exported records.

- Keep a live evidence folder with invoices, contracts or proposals, proof of delivery, and records such as bank statements or receipts.

- Screen counterparties at a basic level: who is paying, why, from where, and under which contract.

- If access is restricted, stop retrying transactions. Send only the documents tied to the flagged payment, then pause non-essential payouts until the review is clarified.

Step 3. Choose for audit-trail quality, not onboarding speed#

Fast onboarding is nice. Usable records at month-end and year-end matter more. If you lived abroad as a non-resident, HMRC says there are cases where you may not be able to use its online Self Assessment filing service. That makes export quality and reconciliation readiness non-negotiable.

Before committing, test whether you can produce records your accountant can use quickly:

- Monthly and year-end statements

- Readable statement files plus structured exports

- Clear fee line items

- Preserved payment or payout references

- Clean matching from payments to invoices or bills

Run a small in-and-out transaction test, export the records, and confirm you can answer from the file alone: who paid, what for, what fee applied, and what each payout relates to.

Step 4. Keep tax-compliance admin from becoming a cashflow risk#

Tax admin becomes a cashflow problem when you leave it until filing season. For sole traders, HMRC says you need a National Insurance number to register for Self Assessment, and registration is required if you earn more than £1,000 in a tax year. In the HMRC excerpt, you must tell HMRC by 5 October 2025 for the previous tax year (6 April 2024 to 5 April 2025), and payment is due by 31 January.

| Self Assessment point | Article detail |

|---|---|

| National Insurance number | HMRC says you need a National Insurance number to register for Self Assessment |

| Registration threshold | Registration is required if you earn more than £1,000 in a tax year |

| Notify HMRC deadline | 5 October 2025 for the previous tax year (6 April 2024 to 5 April 2025) |

| Payment deadline | Payment is due by 31 January |

| Existing account status | If you registered before but did not file last year, check whether your Self Assessment account needs reactivation |

If you registered before but did not file last year, check whether your Self Assessment account needs reactivation. HMRC says you may need to reactivate it, and filing without reactivation can delay your return.

You might also find this useful: How to Host a Webinar to Generate Freelance Leads.

Before you lock your account setup, run your typical client payment mix through this payment fee comparison tool to pressure-test fees and FX drag.

Tier 3: The Engine - Building a Financial Infrastructure, Not Just an Account#

Once your first route is stable and your protection checks are done, stop treating this as a single account choice. Treat it as an operating setup. The goal is faster cash application, cleaner reconciliation, and fewer manual handoffs before month-end.

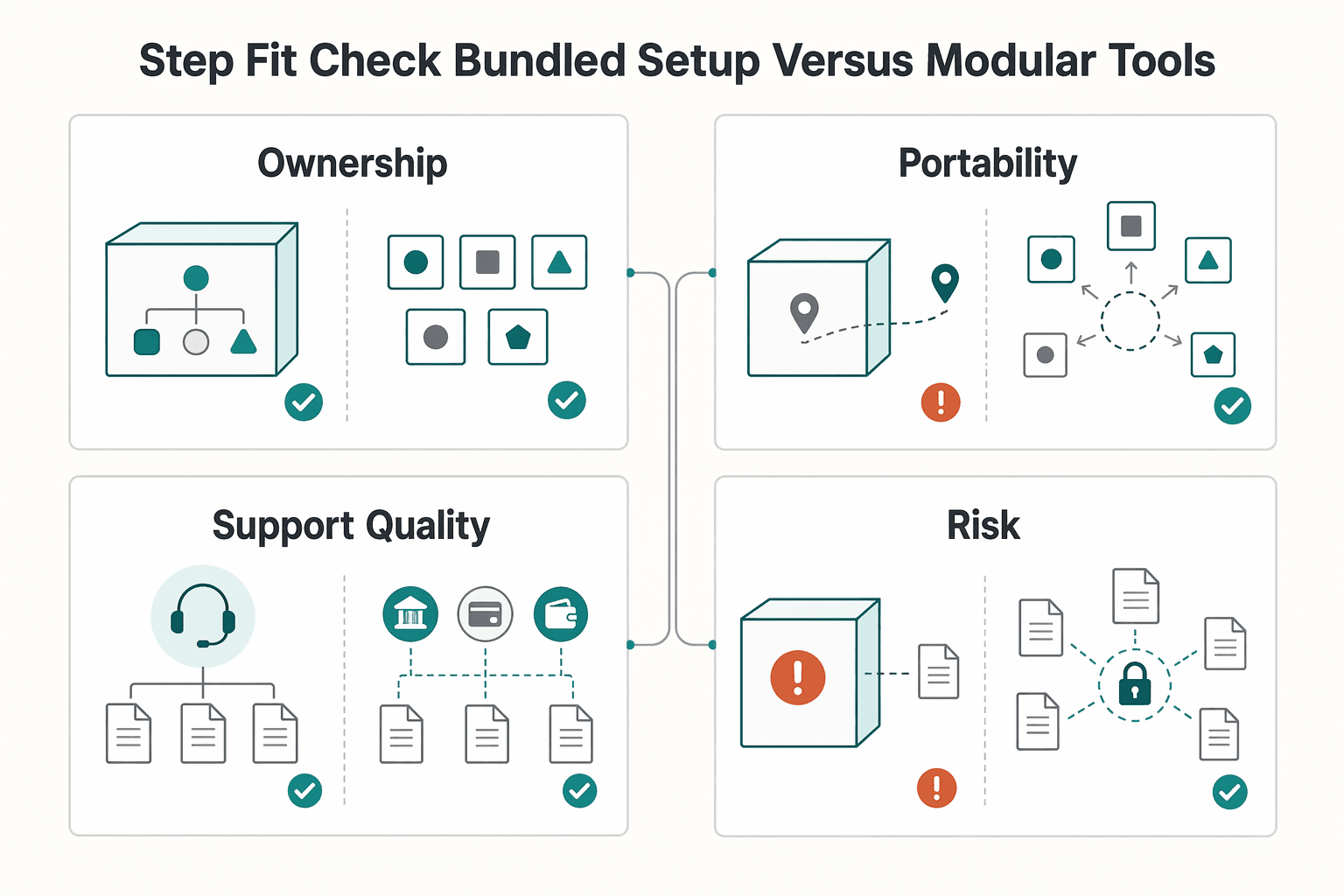

Step 1. Fit check bundled setup versus modular tools#

Convenience is real, but so is concentration risk. A bundled setup can be the right call when speed matters most. A modular setup can be better when control, portability, and component-level choice matter more.

| Factor | What to compare |

|---|---|

| Ownership | Who controls account access, invoice flow, and payout settings, and what happens if one user loses access |

| Portability | Whether you can export statements, transaction history, and beneficiary data cleanly enough to move |

| Support quality | Whether urgent payment-review support is clear and reachable |

| Lock-in risk | How hard it is to replace one component without rebuilding the full setup |

Use a bundled "business in a box" setup when launch speed matters most and you want one application and one support queue. Use a modular stack when ownership, portability, and component-level control matter more than convenience.

If one provider controls too many layers, one review, outage, or support bottleneck can disrupt invoicing, collections, and payouts together. Compare this before you commit:

- Ownership: who controls account access, invoice flow, and payout settings, and what happens if one user loses access

- Portability: whether you can export statements, transaction history, and beneficiary data cleanly enough to move

- Support quality: whether urgent payment-review support is clear and reachable

- Lock-in risk: how hard it is to replace one component without rebuilding the full setup

If you cannot explain how you would exit quickly with records intact, the setup is too tightly coupled.

Step 2. Connect the payment, accounting, and payout layers#

The handoff between payments, accounting, and payouts is where many setups break. Validate that flow before volume arrives. Your setup works only if incoming payments, accounting records, and payout flows line up.

| Task | Native route | Manual fallback | Verification point |

|---|---|---|---|

| Bank data into Xero | Direct feed if supported | Import a CSV bank statement | Confirm references, fees, and dates survive import |

| Bank data into QuickBooks | Direct connection if supported | Manually upload transactions | Confirm duplicate handling and opening-balance treatment |

| Gateway payouts into your books | Automatic sync if available | Export payout data and match to bank credits manually | Confirm each payout maps back to invoices or charges |

Run one live test end to end: take one payment, wait for payout, and confirm your books show gross, fees, and net settlement clearly. For Stripe, monitor payout states such as processing, posted, failed, returned, and canceled. Treat non-standard payout destinations as accounts that can carry higher payout-failure risk.

Step 3. Tighten the client-facing payment instructions#

Small naming mismatches create real payment friction. Clean instructions reduce failed payments and credibility issues at the same time. Credibility is operational consistency. Your invoice needs a unique identification number, and if you trade through a limited company, use the full registered company name exactly as shown on the certificate of incorporation.

Keep your receiving details consistent across invoices and payment instructions. Revolut Business UK states that GBP local sort code and account number are available. Wise says you can receive GBP with your own sort code and account number, while also stating this is not a bank account. Keep that distinction clear if a client procurement team asks what they are paying into.

Use a test payee setup with a trusted client or colleague. In UK flows where Confirmation of Payee is used, a name, sort code, and account number check can reduce misdirected payments. If a mismatch appears, correct the account name in your invoice and payment instructions before the next billing run.

Step 4. Define your backup-route trigger before you need it#

A backup route is only useful if you define the trigger before something goes wrong. Trigger it if the first gateway payout has not landed within the expected first payout window after the first successful live payment (for Stripe, the initial payout is typically 7-14 days), if payouts show failed, returned, or canceled, or if repeated client payments stall because of payee-name mismatch issues.

Prepare onboarding evidence in advance: identity documents, certificate of incorporation, operating address evidence, ownership information, and any business-address proof the backup provider requires. Wise states the trading address must be a physical location, and Revolut Business lists ID, incorporation, operating address, and ownership data among core onboarding items.

If the backup route depends on another jurisdiction or institution, add that local requirement to your checklist and verify it before you need it. The objective is simple. Keep one active route and one ready route.

For a step-by-step walkthrough, see Opening a Business Bank Account in Australia as a Non-Resident.

Beyond the Bank Account: Your Next Step to Financial Control#

Once you know your operating options, the next step is operating discipline. This is where the account becomes part of a reliable records, bookkeeping, and tax-control setup.

| Business model | Setup path | Receiving details choice | First controls to document |

|---|---|---|---|

| Service freelancer | Accounting records + invoicing + one primary collection route | Confirm with your provider which receiving details are available, and use only options you can reconcile cleanly | Weekly reconciliation, invoice-reference check, record retention (bank statements or receipts) |

| E-commerce seller | Accounting records + payout records from each sales channel | Match your enabled payment details to how each channel settles, and keep routes documented | Daily payout check, clearing-account review, record retention (bank statements or receipts) |

| Multi-currency team | Accounting records that track balances by currency | Treat detail and currency setup as provider-dependent; document the exact setup you run | Monthly close checklist, conversion approval rule, named incident owner |

-

Connect your accounting setup. Choose the setup that gives you a clean audit trail. Keep your legal structure consistent in your records: a limited company is a separate legal entity, while a sole trader is one person and is personally responsible for business debts. Done means you can trace each invoice, fee, payout, and ending balance without guesswork.

-

Connect your payment collection routes. Map each route to its own ledger path so receipts and payouts stay auditable. Done means each route can be reconciled from payment to payout to ledger entry, and any fallback route is documented internally.

-

Update invoices and client payment instructions. Update templates, saved billing details, and client-facing instructions together. Use payment details that match how you bill and reconcile. Done means payee name, account details, and invoice currency match exactly.

-

Write control procedures before volume grows. Assign who can view balances, initiate payouts, and approve payment-detail changes. Document your reconciliation cadence and incident checklist, and retain records such as bank statements or receipts. If you need Self Assessment, tell HMRC by 5 October following the relevant tax year, keep your UTR ready, and plan to pay your tax bill by 31 January. If you previously filed, reactivate your existing account before filing to avoid delays. If you lived abroad as a non-resident and cannot use the standard GOV.UK online filing service, use commercial software or other forms.

Related: The Best Bank Accounts for Freelancers in the UK.

If you are evaluating this route, review how Virtual Accounts fit your operating model.

Frequently Asked Questions

Can you legally open a UK business account if you do not live in the UK?

Yes. You can be a non-resident director of a UK private limited company, which means you live outside the UK while serving as a director. Directors do not have to live in the UK, but the company must have a UK registered office address. Approval by a bank or payment firm is still a separate onboarding decision.

Do you need a UK residential address to apply?

Not as a blanket rule. Your company needs a registered office that is a physical UK address in the same UK country as incorporation, but that is different from your personal home address. You still provide your usual residential address to Companies House, while your service address can be different and is the one shown publicly. If you are unclear on this split, revisit Tier 1 before applying.

What exactly counts as a non-resident director, and why do people confuse the addresses?

A non-resident director is a director who lives outside the UK. Most confusion comes from mixing up three different addresses: the company’s registered office, your public service address, and your usual residential address. Treat them as separate compliance fields, not interchangeable labels. Tier 1 gives the deeper setup context.

What documents should you expect to provide?

Use a required-versus-commonly-requested checklist so you do not over- or under-prepare. Required baseline usually includes proof of UK company registration, proof of UK business address, personal details, proof of identity, and current Companies House identity-verification requirements. Commonly requested items include ownership details, identification for shareholders over 10%, and any extra jurisdiction-specific items the provider requests. Individual provider requirements vary. Identity verification is now a legal requirement for people setting up, running, owning, or controlling a UK company, and there is a transition period.

How should you choose between providers for this setup?

Choose based on regulatory fit and operating pattern, not brand familiarity. | Priority | What to prioritize | What to verify before applying | | --- | --- | --- | | Regulatory status | Authorised or registered provider status | The legal operating company name on the FCA register | | Protection model | How customer money is protected (bank deposit protection vs safeguarding) | Firm type (bank, EMI/API, or SPI) and the protection model that applies | | Onboarding path | Realistic setup requirements and timelines | Current checklist, including company/address/identity items and whether in-person steps may apply | | Company details readiness | Accurate address and director information | Registered office, service address, and residential details are correctly recorded | If the fit is not clear against your real cashflow, keep comparing. This decision spans Tier 1 and Tier 3.

Are these accounts protected the same way as bank accounts?

No, not always. Many non-bank providers are EMIs or other payment firms, where customer money protection is typically safeguarding rather than standard FSCS deposit protection. SPIs are a separate category and do not have the same safeguarding requirement. Eligible bank deposits may be covered by FSCS up to the current limit, depending on the institution and account. Use Tier 2 to decide how much balance you are comfortable holding in each type of account.

How do you check whether a provider is real and properly regulated?

Check the FCA register before onboarding. Verify the legal operating company name, not just the consumer-facing brand, because brand names may differ from registered entities. Also confirm the firm type, since protection differs across banks, EMIs or APIs, and SPIs. In practice, do not assume every payment firm safeguards funds the same way.

How long does approval usually take, and what should you do if it stalls?

There is no universal approval timeline you can rely on. Delays can happen while documents and ownership details are reviewed. If progress stalls, monitor your email for additional document requests, respond promptly with what was requested, and keep your backup route ready from Tier 3 so receivables are not blocked. This keeps your payment operations moving even if one application slows down.

Watch

How Non-Residents Can Set Up UK Business Banking

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- assets.publishing.service.gov.uk/media/6912f907663088df8f54f4d6/AP01_v9.0-FIN...trusted

- business.gov.uk/support/business-structures-governance-and-e...trusted

- business.gov.uk/invest-in-uk/expand-your-business-in-the-uk/...trusted

- changestoukcompanylaw.campaign.gov.uk/identity-verificationtrusted

- docs.stripe.com/global-payouts/manage-payoutstrusted

- docs.stripe.com/payoutstrusted

- wise.com/help/articles/2935927/how-do-i-receive-money...trusted

- central.xero.com/s/article/Import-a-CSV-bank-statementexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

Automating Your Freelance Finances: A Zapier Workflow for Connecting Stripe, QuickBooks, and Wise

Cleaner books and fewer month-end fire drills come from sequence, not software. Run this in the right order: structure, compliance, accounting architecture, then automation.

The Best Bank Accounts for Freelancers in the UK

Confirm with each provider directly, as UK bank product details and eligibility requirements can change. Always verify the current terms on official provider pages before applying.

How to Host a Webinar to Generate Freelance Leads

**Treat your webinar as a repeatable pipeline system (capture, qualify, route, follow up), not a one-off event you hope generates leads.** If you run a business-of-one, you're the CEO. Your webinar should behave like an asset you can operate, not a performance you have to reinvent.