Quick Answer

Start by opening a business bank account for new llc as soon as your EIN is ready, then set controls before the first client payment lands. Keep all company inflows and spending inside the LLC account, confirm whether you need merchant services for card payments, and compare fee categories instead of only monthly charges. Before applying, align formation documents, EIN proof, signer ID, and beneficial-owner details to reduce review delays. After approval, create cash buckets, test accounting connections with live data, and update every payment channel.

Beyond the Basics: Why Your LLC's Bank Account is Your Most Critical Business Decision#

Choosing a business bank account for new llc is more than setup admin. It is a risk-control decision. Treat it that way from day one, and you will run payments, records, and fund separation with less friction.

Three practical checkpoints will help frame the rest of this guide:

- Open a business account as soon as your business starts accepting or spending money, once you have your federal EIN.

- Keep business and personal funds separate to support liability protection and cleaner records.

- Compare providers because rates, fees, and options vary from bank to bank.

A compact risk map#

| Risk area | Business impact | Control point |

|---|---|---|

| Incoming payments | Limited ways to accept customer payments | Confirm whether bank transfers are enough or if you also need card acceptance |

| Account opening readiness | Delays opening the account | Have your federal EIN ready before applying |

| Fund separation | Harder bookkeeping and weaker separation | Route business income and spending through the LLC account |

Basic account selection vs risk-first account selection#

| Approach | What you compare | What you may miss |

|---|---|---|

| Basic account selection | Monthly fee, ATM or branch convenience | Whether the account matches how you actually get paid |

| Risk-first account selection | EIN readiness, fund separation, payment method fit, fee categories | Fewer surprises once transactions start |

One early check matters more than many founders expect: if you need to accept cards, you may need a merchant services account. The SBA advises shopping around because rates, fees, and options vary by provider, and fee categories can include discount rate, transaction fees, ACH daily batch fees, and monthly minimum fees when required transaction minimums are not met.

The rest of the decision follows a simple order. First, get EIN readiness and fund separation in place. Then compare banks against that reality instead of against marketing copy.

If you want a deeper dive, read Sole Proprietorship vs. LLC: The Definitive Guide for Global Freelancers.

The Non-Negotiables: Securing Your Corporate Veil & Assembling Your Documents#

Before you compare features, get your LLC documentation application-ready. The first job is to prove legal separation and clear signer authority so the bank can verify you without avoidable follow-up.

In practical terms, the corporate veil is your LLC liability shield, and piercing the veil is when a court sets that shield aside and reaches owners or managers personally in serious-misconduct cases. Authority to act for the LLC means the signer is allowed to bind the company for account opening and control. In Delaware, members and managers have that authority by default unless the operating agreement says otherwise.

Banks have to verify all of this. Under CIP rules, they must use risk-based identity checks, and for legal-entity accounts they must identify beneficial owners and control persons. So expect both entity documents and personal identity review, with requirements that can differ by bank and by online versus in-person opening.

Your preflight document kit#

The easiest way to stay organized is to separate true baseline documents from items that depend on bank policy, channel, and ownership or residency profile.

| Document or detail | Status |

|---|---|

| Articles of Organization, or the equivalent formation document | Usually required |

| EIN confirmation evidence | Usually required |

| Personal identity documentation for the signer and other required individuals | Usually required |

| Ownership and control details for beneficial owners and control persons | Usually required |

| Operating agreement | Bank- or channel-dependent |

| Additional address proof if records do not verify cleanly | Bank- or channel-dependent |

| Additional signer documents | Bank- or channel-dependent |

| Non-resident support documents and eligibility checks | Bank- or channel-dependent |

Usually required

- Articles of Organization, or the equivalent formation document

- EIN confirmation evidence

- Personal identity documentation for the signer and other required individuals

- Ownership and control details for beneficial owners and control persons

Bank- or channel-dependent

- Operating agreement

- Additional address proof if records do not verify cleanly

- Additional signer documents, since some in-person openings require all authorized signers present

- Non-resident support documents and eligibility checks, because provider rules are not uniform

If you are a non-U.S. resident, verify eligibility first. Some providers limit applications to U.S.-resident or U.S.-based applicants, while others accept international founders with U.S.-entity and operations constraints. If that is your case, this follow-up guide is the direct path: The Best Bank Accounts for US LLCs Owned by Non-Residents.

| Document | Why the bank requests it | Common rejection reason | What to prepare instead |

|---|---|---|---|

| Articles of Organization | Confirms legal existence and exact entity name | Entity details do not match other application records | Use the exact filed legal name, including suffix and punctuation |

| EIN confirmation | Confirms federal tax identity | CP 575 missing or IRS record mismatch | If CP 575 is unavailable, request IRS Letter 147C; some providers may also accept a returned SS-4 |

| Operating agreement | Confirms ownership and signer authority | Authority language is unclear or conflicts with application | Make signer authority, member or manager names, and ownership clear and consistent |

| Government ID | Verifies the human signer | ID details do not match application records | Use current ID and match the application name exactly |

| Address evidence | Supports CIP and address verification | Address mismatch across records | Prepare backup address documentation before applying |

The two records that cause the most rework#

Two common friction points are the operating agreement and the EIN record.

Your operating agreement should make one decision easy for the reviewer: who owns the LLC and who is authorized to open and manage bank accounts. Keep member or manager names, ownership, and signer authority consistent across the operating agreement, state filing, and application.

Your EIN record must match what you submit. Name matching against IRS records is used in verification, so keep the legal name and address aligned across EIN records and the application. If the original CP 575 is unavailable, IRS Letter 147C is the official IRS fallback to confirm the EIN. Confirm each provider's accepted EIN proof before you apply.

Final application-ready check#

Before you submit, do one clean consistency check:

- LLC legal name matches state filing, IRS record, and application exactly

- Business address is consistent across records, or backup proof is ready

- Signer name matches government ID exactly

- Ownership and control details are complete for all persons the bank may treat as beneficial owners or control persons

- Opening method requirements are confirmed, including whether all authorized signers must be present in person

This step is simple, but it cuts avoidable rework and manual-review delay. Once your documents are tight, you can judge providers on how they will actually perform.

Related: Hiring Your First Subcontractor: Legal and Financial Steps.

The 'Central Nervous System' Framework: 3 Pillars for Choosing a Global-Ready Bank#

Once your documents are ready, evaluate each provider against three pillars and flag any bank that fails one. The practical question is straightforward: can this bank onboard you remotely, handle your cross-border payment flow, keep your books reliable, and give you controls and records you can defend later?

Weak fits often show up in operations rather than marketing copy. Common failure modes include delayed payment reviews, broken accounting feeds, or month-end records that need cleanup for bookkeeping and compliance.

Pillar 1: Global-readiness#

A provider should only pass this pillar if onboarding, payment rails, review behavior, and total transfer cost are all operationally clear.

| Check | Mercury | Relay |

|---|---|---|

| Remote onboarding and eligibility | Company must be formed and registered in the U.S. or a U.S. territory; founders do not need to live in the U.S. or be U.S. citizens | Account opening is entirely online; supports businesses registered and operating in the U.S. |

| Cross-border handling | Can send payments to 40+ countries in local currencies | Two outbound paths: Local Network and SWIFT |

| Compliance-review behavior | Funds may be held, returned, or unavailable based on regulatory obligations | Reports temporary onboarding restrictions for receiving international wires |

| Transparent total cost | No Mercury fee for USD international wires; 1% currency conversion fee for non-USD international wires | International-wire fees are plan-based and daily or monthly limits apply; current wire limits pending provider verification |

- Remote onboarding and eligibility: Relay describes account opening as entirely online and states support for businesses registered and operating in the U.S. Mercury states the company must be formed and registered in the U.S. or a U.S. territory, and also states founders do not need to live in the U.S. or be U.S. citizens.

- Cross-border handling: Mercury states it can send payments to 40+ countries in local currencies. Relay states two outbound paths, Local Network and SWIFT. A SWIFT payment is an international wire over the SWIFT network, so rail choice can affect cost and operational handling.

- Compliance-review behavior: Mercury states funds may be held, returned, or unavailable based on regulatory obligations. Relay reports temporary onboarding restrictions for receiving international wires. If review behavior is unclear, treat that as operating risk.

- Transparent total cost: Compare bank fees, FX pricing against mid-market, and transfer path. Mercury states no Mercury fee for USD international wires, and a 1% currency conversion fee for non-USD international wires. Relay states international-wire fees are plan-based and daily or monthly limits apply, so current wire limits must be verified from provider records before use.

Pillar 2: Integration and automation#

This pillar matters once the account becomes part of your close process, not just your payments setup. Pass it only if accounting sync, export fallback, and sync-recovery steps are usable in real work.

- Native accounting sync quality: Mercury lists direct integrations with QuickBooks Online, NetSuite, and Xero. Relay documents Xero feeds that sync settled transactions every few hours.

- Sync cadence and ledger impact: If feeds post settled transactions on a cadence, your operational cash view and booked cash view can temporarily diverge. Plan your close process around that behavior.

- Data export reliability: Relay supports PDF, CSV, and OFX exports. Mercury provides CSV fallback exports alongside native integrations.

- Exception handling: Relay documents recovery steps for duplicates or mismatches, including manually triggering sync. If recovery steps are undocumented, expect avoidable manual cleanup and support dependency.

Pillar 3: Compliance and control#

This is where weak setups become expensive later. Pass this pillar only if records are audit-ready and cash controls are enforced by rules, not memory.

| Control area | Grounded example | Operational implication |

|---|---|---|

| Statement quality and audit trail | Mercury states monthly statements are generated between the 1st and 3rd of each month and include account and routing details plus transaction activity for the date range; Relay offers statement exports in PDF, CSV, and OFX | Pass only if records are audit-ready |

| Approval-rule controls | Mercury documents configurable amount-based approval thresholds for payments | Cash controls should be enforced by rules, not memory |

| Cash segregation workflow | Relay states support for up to 20 real checking accounts and supports automated allocation rules, for example allocating 30% of income to a tax account | Weak setups become expensive later |

| CDD caution in 2026 | Do not assume beneficial-owner collection is universally unchanged or removed; Mercury states identification is needed for owners at or above 25% ownership | Collection practice is not uniform |

- Statement quality and audit trail: Mercury states monthly statements are generated between the 1st and 3rd of each month and include account and routing details plus transaction activity for the date range. Relay offers statement exports in PDF, CSV, and OFX.

- Approval-rule controls: Mercury documents configurable amount-based approval thresholds for payments.

- Cash segregation workflow: Relay states support for up to 20 real checking accounts and supports automated allocation rules, for example allocating 30% of income to a tax account.

- CDD caution in 2026: Do not assume beneficial-owner collection is universally unchanged or removed. There are reported 2026 change signals for some institutions, but collection practice is not uniform. Mercury states identification is needed for owners at or above 25% ownership.

| Pillar | Required checks (must be explicit) | Score 0 | Score 1 | Score 2 |

|---|---|---|---|---|

| Global-readiness | Remote onboarding + eligibility fit + wire rails + review behavior + total-cost transparency | Missing or unclear on any critical check | Most checks documented, with some policy gaps | All checks documented and operationally clear |

| Integration and automation | Native sync + known cadence + export fallback + documented sync recovery | No reliable sync or no fallback or recovery path | Works, but requires regular manual intervention | Reliable sync plus clear fallback and recovery steps |

| Compliance and control | Complete statements + approval thresholds + account segmentation + allocation rules | Weak records and weak controls | Partial controls or incomplete record or export coverage | Audit-ready records and enforceable control model |

Use this table to score your shortlist consistently. Then test those scores against actual providers and see where the tradeoffs are real.

You might also find this useful: The Best Business Bank Accounts for Freelancers.

Putting it to the Test: Analyzing Top Banks for the Global Professional#

Use this section as a fit test, not a brand ranking. The right choice is the provider that matches your ownership setup, supports your payment routes, and gives you records your bookkeeping and compliance process can defend.

Digital-first providers#

If your LLC is U.S.-formed and you run cross-border payments, Mercury and Relay are strong examples of the digital-first profile to evaluate. Mercury states your company must be formed and registered in the U.S. or a U.S. territory, and it accepts international founders with country-based exceptions. Relay states it supports businesses registered and operating in the U.S., and that non-U.S. owners can qualify when the business is U.S.-registered with a U.S. operating presence.

The useful comparison is operational, not cosmetic. Mercury states support for payments to 40+ countries in local currencies and direct integrations with QuickBooks Online, NetSuite, and Xero. Relay documents Local Network and SWIFT wire paths, and also states some countries are unavailable for international wires and that policy lists can change.

Modern fintech profiles#

For other online providers, evaluate the profile rather than the label. What matters is whether non-U.S. owner eligibility is explicit, whether international payments are clearly documented, whether accounting sync reflects real bank activity, and whether support coverage is clearly published.

If policy details are vague, treat that as risk. A polished interface does not make up for unclear eligibility, unclear country coverage, or unclear review behavior.

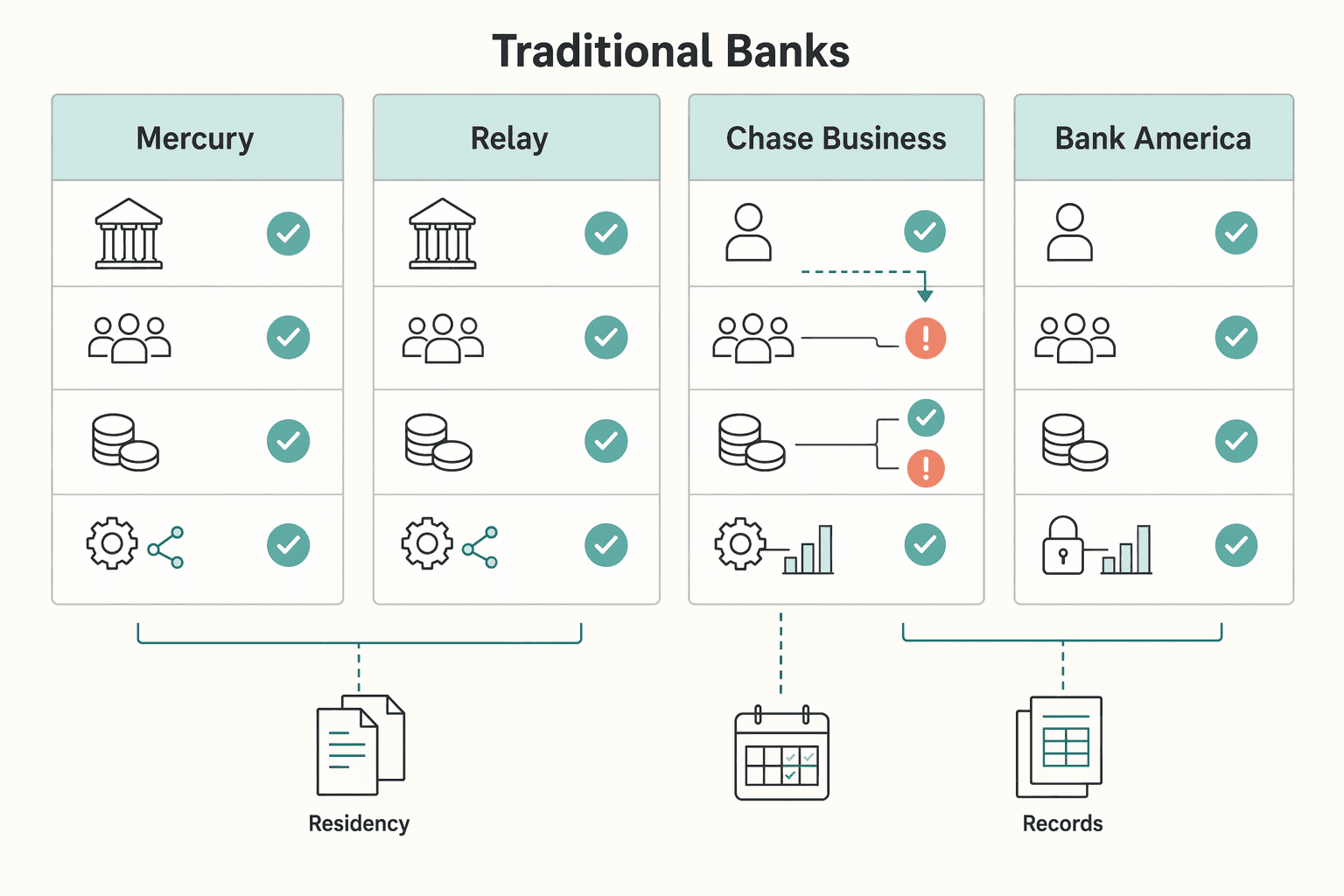

Traditional banks#

Traditional banks can still fit, but onboarding structure matters early. Chase states only single-member or single-manager LLCs with one authorizing representative can apply online, while multi-member or multi-manager LLCs are directed to open in branch.

It also helps to separate fee marketing from workflow fit. Chase Business Complete Banking shows a monthly fee that can move from $15 to $0, including a $2,000 minimum daily ending balance path, but that does not change ownership-structure constraints. Its QuickBooks integration page in this context describes payment-processing data sharing, which keeps the focus on payment-processing data scope. For Bank of America, different debit-spend waiver thresholds appeared across surfaced materials in this run, so you should verify the live, account-specific disclosure before applying.

| Provider | Best fit | Key strengths | Known tradeoffs | Verification needed before applying |

|---|---|---|---|---|

| Mercury | U.S.-formed companies, including eligible international founders, that want cross-border payments and accounting integrations | Clear U.S. entity eligibility; payments to 40+ countries in local currencies; direct integrations with QuickBooks Online, NetSuite, and Xero; support target within 5 minutes during business hours | Country-based founder restrictions can apply; policy fit still depends on your payment destinations and risk profile | Confirm founder residency eligibility, destination-country fit, onboarding document set, and current fee details pending provider verification |

| Relay | U.S.-registered businesses with a real U.S. operating presence that want clear wire-path choices and accounting sync | Eligibility rules for U.S. registration and operations are explicit; transaction sync to QuickBooks Online and Xero; documented Local Network versus SWIFT behavior; live chat target under 60 seconds during business hours | Some countries are unavailable for international wires and lists can change; non-U.S. ownership alone is not sufficient without U.S. operating presence | Confirm U.S. operating presence fit, destination-country availability, required beneficial-owner or control-person details, and current plan and wire fee details pending provider verification |

| Chase Business Complete Banking | Simpler LLC structures, especially where online eligibility rules are already met | Online path exists for some LLCs; published fee-reduction paths from $15 to $0, including a $2,000 minimum daily ending balance option | Multi-member or multi-manager LLCs are directed to branch; cited QuickBooks page focuses on payment-processing data scope | Confirm whether your LLC can open online or must open in branch, confirm current fee-waiver route, and confirm integration scope for your bookkeeping workflow |

| Bank of America Business Advantage Fundamentals | Traditional-bank comparison shoppers willing to validate live disclosures before applying | Public fee disclosures are available; surfaced fee table showed a $16 monthly fee (effective March 25, 2026) | Different debit-spend waiver thresholds appeared across surfaced materials in this run | Confirm the exact applicable disclosure for your account, current waiver threshold, and any ownership or branch onboarding requirements |

Use this short workflow to decide:

- Shortlist two options that pass your pillar score: one primary and one backup.

- Validate policy fit against your exact facts: U.S. formation, EIN, ownership and control structure, residency, U.S. operating presence, industry restrictions, and wire destinations.

- Choose your primary for incoming payments and accounting sync, and keep the backup available before you move to Day 1 configuration.

We covered this in detail in The Best Business Bank Accounts for Australian Sole Traders.

Before you choose an account, run your expected client payment mix through this payment fee comparison tool so you can compare real landed costs, not just headline fees.

Your Day 1 Blueprint: How to Configure Your New Account for Maximum Control#

A good account choice can still create messy records if you configure it poorly. Set this up before your first client payment arrives. Day 1 configuration determines where cash lands, how clean your records stay, and how much cleanup you create later.

Build your cash allocation buckets#

Start with a simple bucket structure: income, tax reserve, owner pay, and operating expenses. If your provider offers multiple accounts or internal buckets, create them now. If not, use scheduled internal transfers with consistent names so the same control still exists.

| Bucket | Purpose | Automation rule | What to review monthly |

|---|---|---|---|

| Income | First landing account for all incoming revenue | Route deposits here first based on your setup policy | Unexpected deposit sources, missing payouts, holds, reversals |

| Tax reserve | Funds set aside for tax obligations | Move funds on a schedule based on your allocation policy | Reserve balance versus expected obligations, missed transfers |

| Owner pay | Funds earmarked for owner compensation transfers | Move funds only through scheduled transfers with clear memos | Irregular transfers, duplicates, personal spending bypassing process |

| Operating expenses | Budget for day-to-day business spend | Fund this after reserve and owner-pay allocations | Vendor creep, recurring charges, spend pace versus current revenue |

Do not copy someone else's percentages. Set your allocation policy with your advisor based on your margins, tax profile, and revenue timing.

Connect only tools you can verify#

Only connect accounting and payment tools after a low-risk live test. Check whether the record that lands in your accounting system is clear enough for your books: date, label, amount, and transfer direction. If a tool creates unclear or duplicate entries, leave it disconnected for now.

Set your owner pay protocol#

Treat owner compensation as a controlled transfer process, and align your method with your advisor before you automate anything. On Day 1, enforce transfer discipline: schedule transfers, use clear memos such as Owner transfer Apr 2026, and keep personal and business flows separate.

Audit every revenue channel#

Once the account is open, update every channel that sends you money:

- Invoices and invoicing software

- Payment processors

- Marketplaces or platforms

- Client procurement or vendor portals

After the first live deposits, run a verification pass. Confirm deposits land where you expect, confirm transfer rules run as expected, and confirm no channel still points to an old account.

If you chose an account partly for an opening offer, track those terms on Day 1. For example, American Express Business Checking presents its welcome-offer conditions as cumulative with "AND": deposit a total of $5,000 or more in eligible deposits within 30 days of opening your first account, maintain an average account balance of $5,000 for the next 60 days, and make 5 or more qualifying transactions within 60 days. Its terms also state that Business Debit Card transactions and deposits using Redeem for Deposits are not qualifying transactions.

This pairs well with our guide on The Best Business Bank Accounts for Canadian Sole Proprietors.

Your Bank Account Isn't a Chore; It's Your Foundation#

Your account setup determines four outcomes you can verify every month: payment reliability, fee visibility, clean reconciliation, and separation of business and personal funds. The SBA baseline is straightforward: open the account when your business starts accepting or spending money, because that separation supports limited personal liability framing and cleaner records.

You should also treat the account as the operational layer of your LLC documents. Your EIN is the business's federal tax ID and is commonly used in setup, an operating agreement may be requested as part of formation documents, and banks may verify owners or the person with significant management responsibility. This is not legal advice, and the account is not a liability shield by itself, but matching account setup to real ownership and payment flows makes your records easier to support.

Choose your bank on criteria, not branding. If you run cross-border payments, confirm the exact route you will use: currencies, cutoff times, intermediary-fee risk, and realistic delivery windows. Some banks disclose international wires in a 1 to 5 business day range, and some outgoing wires may be delayed by internal review, so validate the live path instead of relying on a generic "international wires supported" label.

Keep recordkeeping standards inside the bank decision, not as an afterthought. The IRS requires a system that clearly shows income and expenses, and for many small businesses the checking account is the main source for bookkeeping entries. Confirm statement access, an accounting integration where available, and a manual export option so you can still reconcile with supporting documents like invoices, receipts, deposit slips, and paid bills.

Use this short control checklist after opening your account:

- Review each incoming payment route and test your primary path

- Confirm accounting sync accuracy against actual deposits and fees

- Validate owner-draw, reserve, and operating-spend workflows

- Monitor policy, fee, and verification requirement changes early

For a step-by-step walkthrough, see Choosing a US Bank Account Path as a Foreign Founder.

If you want a single workflow to collect client payments and run payouts with clearer status tracking, review Gruv for freelancers.

Frequently Asked Questions

When should you open the account?

Open it when you start accepting or spending money as your business. The SBA also gives a practical checkpoint: you can open a business account once you have your federal EIN. This matters because separating business and personal funds supports liability protection and cleaner records. Next check: confirm your EIN is ready, then compare bank options before you apply.

Which account type fits your use case?

Choose the account type based on how money moves through your business, not on branding. The SBA lists checking, savings, credit card, and merchant services as common business account types. This matters because a mismatch can create avoidable fees. Next check: map your main workflow to the table, then confirm the bank’s fee schedule for that account type. | Use case | Account type to start with | Required capabilities to confirm | |---|---|---| | Day-to-day business spending and deposits | Business checking | Transaction fees, minimum account balance fees, early termination fees | | Holding business reserves | Business savings | Transaction fees, minimum account balance fees, early termination fees | | Business purchases and expense separation | Business credit card account | Account terms and fees | | Accepting customer card payments | Merchant services account | Discount rate, per-transaction fees, ACH daily batch fees, monthly minimum fees |

Do you need an EIN to apply?

Treat your federal EIN as a core readiness checkpoint. The SBA says you can open a business bank account once you have your federal EIN. This matters because it marks when you can move from setup to application. Next check: confirm the bank’s requirements page shows whether EIN is required or requested.

What is the difference between your identity and the business’s identity, and where does an ITIN fit?

This SBA guidance does not spell out ITIN-specific rules or detailed identity-field requirements. If this is relevant to your case, confirm the bank’s exact application requirements before you submit.

Can you open the account while living overseas or using a nonstandard address?

This SBA guidance does not provide bank-by-bank rules for overseas residence, remote onboarding, or nonstandard addresses. Next check: confirm your exact residency and address scenario directly with the bank before applying.

What fees matter most when comparing accounts?

Look beyond the headline monthly fee. The SBA says to compare transaction fees, minimum account balance fees, and early termination fees. For merchant services, also review discount rate, per-transaction fees, ACH daily batch fees, and monthly minimum fees. This matters because the real cost usually appears only after live payment volume starts. Next check: mark each fee on the schedule against your expected monthly activity.

What is a merchant services account, and do you need one?

If you want to accept customer credit or debit card payments, the SBA identifies merchant services as the account type tied to that function. Before signing, review the discount rate, transaction fees, ACH daily batch fees, and monthly minimum fees. This matters because card acceptance costs depend on fee terms and volume. Next check: confirm the full fee schedule before you enroll.

How should you think about multi-currency accounts, API integration, and virtual cards?

This SBA guidance does not cover multi-currency accounts, API integrations, or virtual cards. Treat these as optional, bank-specific features and verify details directly with the bank.

How do you choose an account that makes compliance and filings easier?

Start with separation: SBA guidance emphasizes keeping business and personal funds separate. Then shop around, since rates, fees, and options vary by bank. Next check: compare account types and fee schedules side by side before choosing.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- congress.gov/crs_external_products/R/HTML/R45518.web.htmltrusted

- delcode.delaware.gov/title6/c018/sc04/index.htmltrusted

- dos.ny.gov/september-5-2018vol-xl-issue-36trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- fdic.gov/resources/deposit-insurance/understanding-de...trusted

- fdic.gov/financial-institution-employees-guide-deposi...trusted

- irs.gov/businesses/employer-identification-numbertrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Sole Proprietorship vs LLC for Global Freelancers in 2026

For most freelancers in 2026, the practical default is still simple: use the simplest structure you can run cleanly, then formalize when risk actually rises. If your work is still in validation mode and the downside is contained, a sole proprietorship is often the practical starting point. When contract exposure, delivery stakes, or dispute risk starts climbing, forming an LLC deserves earlier attention.

Hiring a Subcontractor for the First Time Without Costly Surprises

**Start with a risk-control sequence, not an ad hoc handoff.** As the Contractor, your goal is simple: deliver cleanly, control scope, and release payment only when the work and file are complete.

The Best Bank Accounts for US LLCs Owned by Non-Residents

**You can bank in the US without a US passport, Green Card, or flight. The real requirement is an operating setup that passes review on day one and stays clean months later.**