Quick Answer

Start by classifying the payee, then enforce a release hold until the right form is accepted. Route U.S. persons to Form W-9, foreign individuals to Form W-8BEN, and foreign entities to Form W-8BEN-E. Approve only a properly completed, signed artifact that matches the payee record and is retrievable in your retention system. If facts conflict or status is unclear, keep payout blocked and escalate to the exception owner; treaty personal-services and ECI claims need specialist routing.

Why W-8BEN Controls Matter for Platform Payouts#

Before you start#

Treat Form W-8BEN as a decision input, not a document collection task. The Internal Revenue Service frames Form W-8BEN as the "Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding and Reporting (Individuals)." That matters because a platform paying foreign contractors may need more than a file on record. If you are on the payer side, you need a process that supports a withholding and reporting position you can explain later.

Step 1#

Anchor your process to the form's actual purpose. A foreign beneficial owner provides Form W-8BEN to the withholding agent or payer when requested. In practice, that means the form sits inside a payer decision, not next to it. Your onboarding question is not just "Did the contractor upload something?" It is "Does this form match an individual foreign payee we can reasonably treat under our U.S. tax withholding and reporting process?"

A useful first checkpoint is simple: confirm the payee is both a foreign person and an individual before you route them into a W-8BEN path. If the facts point to a U.S. person or a business entity, the right answer is usually a different form, not a faster approval.

Step 2#

Define what gets validated before money moves. This guide focuses on operator choices: when to collect, what to validate, when to pause payouts, and when to send a case for escalation. The IRS does not prescribe that line by line, but it is where most avoidable risk shows up.

The failure mode to avoid is treating file presence as approval. A saved PDF with no reviewer check, no clear payee classification, and no retrievable audit trail is weak evidence if someone later asks why payment was released or why reporting was prepared a certain way. At minimum, confirm the form artifact is signed, tied to the correct payee record, and stored where finance or compliance can retrieve it.

Step 3#

Keep the build tight and focused on reliance. The IRS requester instructions address certain requirements of brokers and other withholding agents that rely on Forms W-8. That is the right level to design for. You do not need an oversized tax program on day one, but you do need clear release rules, a named owner for exceptions, and records that link onboarding facts to payout treatment.

By the end of this guide, you should be able to do three things without guesswork: route contractors to the right form family, decide when a payout can proceed or should pause for review, and preserve enough evidence to support later withholding and reporting decisions. That standard holds up much better than "form collected."

Related reading: How Platforms Are Reshaping Foreign Exchange in 2026.

What to prepare before you collect any tax form#

Build ownership before the intake form goes live. If nobody clearly owns approval, payout holds, and exceptions, the process turns into file storage with no real decision control behind it.

Step 1 Assign control owners#

Name three owners up front: one for tax profile collection approval, one for releasing or holding payouts, and one for the exception queue when the payee facts do not fit the selected form. The IRS forms tell you where the form goes, to the withholding agent or payer, but they do not define your internal governance. For any contractor record, you should be able to say who can approve the form, who can stop payment, and who must review conflicts.

Step 2 Define the minimum evidence pack#

Keep the evidence pack small but usable: payee legal name, payee type, country, signed form artifact, and an audit trail reference that links the review to the payee record. Those fields map to the forms' real purpose. Form W-9 is used to request the TIN of a U.S. person, Form W-8BEN is for individuals, and Form W-8BEN-E is for entities. A signed artifact matters because Form W-8BEN includes a penalties of perjury certification. One early failure mode is a record marked "individual" with a Form W-8BEN-E upload. That should go to review, not payout.

Step 3 Set the payout release rule#

Before launch, choose one release rule and enforce it consistently. One workable rule is no first payout in the standard lane until the required form is accepted. That is a platform control choice, not a universal IRS rule, but it is a clean way to avoid preventable withholding and reporting problems. Your checkpoint is binary: every payee in the standard lanes is either cleared with Form W-9, Form W-8BEN, or Form W-8BEN-E on file, or the case stays on hold until someone with authority resolves it.

For a step-by-step walkthrough, see How to Fill Out Form W-8BEN-E for a Foreign Company.

Classify each payee correctly before first invoice#

With the release rule in place, the next control is straightforward: classify the payee before the first invoice and do not guess. Start with U.S. person status versus foreign person status, then check whether the payee is an individual or an entity. If either answer is unclear, keep the payout on hold and send the record to the exception queue.

Step 1 Route by U.S. person status first#

Your first gate is not treaty eligibility, tax rate, or document upload quality. It is whether the payee is being onboarded as a U.S. person or a foreign person. That single choice determines whether the record goes into the Form W-9 path or the W-8 path.

The reason to make this gate explicit is practical. Form W-9 is used to provide a correct TIN to payers or brokers required to file information returns with the IRS. Form W-8 series documents sit on the foreign side of that fork. If your onboarding flow lets people skip this gate, you will end up trying to interpret forms after money is already moving.

Keep the verification point easy to audit: each payee record should show one status choice, one matching form family, and one reviewer or automated rule that made that routing decision. A common failure mode is a record marked with a non-U.S. country but sent into a W-9 collection path, or a U.S. person path paired with a W-8 upload. Either conflict should stop release.

Step 2 Check individual versus entity before assigning the W-8 form#

Once a payee is on the foreign path, the next question is whether the beneficial owner is an individual or an entity. The form instructions are direct on this point: Form W-8BEN is for individuals, and entities must use Form W-8BEN-E. The reverse is also true. An entity should not move through an individual-only intake, and an individual should not be parked on the entity form.

This is where mismatches usually show up. Your evidence pack from the last step matters here: legal name, payee type, country, signed form artifact, and audit trail reference. If the payee type says individual but the uploaded document is Form W-8BEN-E, pause the record. If the payee type says business entity but someone selected Form W-8BEN, pause it again. The right move is review, not correction by assumption.

You do not need an exhaustive list of entity signals to run this control well. You do need one checkpoint: the selected payee type and the uploaded form must agree. If they do not, route the case to the compliance owner named for exceptions.

| Payee profile | Default form lane | Payout status | Evidence required | Escalation owner |

|---|---|---|---|---|

| U.S. person | Form W-9 | Hold until accepted | Legal name, payee type, signed form artifact, audit trail reference | Tax profile approver |

| Foreign individual | Form W-8BEN in the standard lane | Hold until accepted | Legal name, country, payee type marked individual, signed form artifact, audit trail reference | Tax profile approver |

| Foreign entity | Form W-8BEN-E | Hold until accepted | Legal name, country, payee type marked entity, signed form artifact, audit trail reference | Compliance owner |

| Status unresolved or form conflicts with payee type | Do not assign by guess | Payout hold | Record of mismatch, supporting onboarding data, review note in exception queue | Compliance owner |

Step 3 Escalate uncertainty instead of forcing a form#

This is where real operations usually get tested. If you cannot determine whether a payment should be treated as made to a U.S. person or a foreign person, the IRS instructions say you must apply the presumption rules. For a platform control, that means unresolved status is not a form-selection problem. It is an exception case.

Set one operating rule: uncertain classification stays blocked until the exception queue owner resolves it. You may choose your own internal SLA, but do not present it as an IRS rule. What matters is that a named person can review the facts, document the decision, and release or continue the hold.

The checkpoint before first payment should be blunt and useful: can you show, for this payee, why they are on the W-9 path, the Form W-8BEN path, or the Form W-8BEN-E path? If the answer depends on guesswork, the record is not ready.

Validate Form W-8BEN before payout release#

Once a payee has been classified onto the foreign individual path, the next decision is not whether a file exists. It is whether the Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding and Reporting is complete enough that you can rely on it for payout release. IRS instructions are clear that a withholding agent or payer may rely on a properly completed Form W-8BEN, so your control should be pass or fail, not "uploaded somewhere."

Step 1 Check the form for operational completeness#

Start with the artifact itself. You want one readable, final form linked to the payee record, not a screenshot, partial upload, or unsigned draft. The pass condition is simple: the form is complete for the facts you are relying on, the certification is present, and the signed artifact is stored in a retrievable record-retention location.

The certification matters because Part III is not window dressing. It is the section where the individual certifies, under penalties of perjury, that they have examined the information on the form. If that attestation is missing from the version in your file, you do not have the document you think you have.

Make the verification point easy to test later: can a reviewer open the exact accepted form from the payee profile, see who approved it, and trace that approval to the payout release decision? A common failure mode is a valid-looking PDF saved in email or chat while the platform record only shows "tax form received." If the retained location is not linked and retrievable, treat the record as not ready for release.

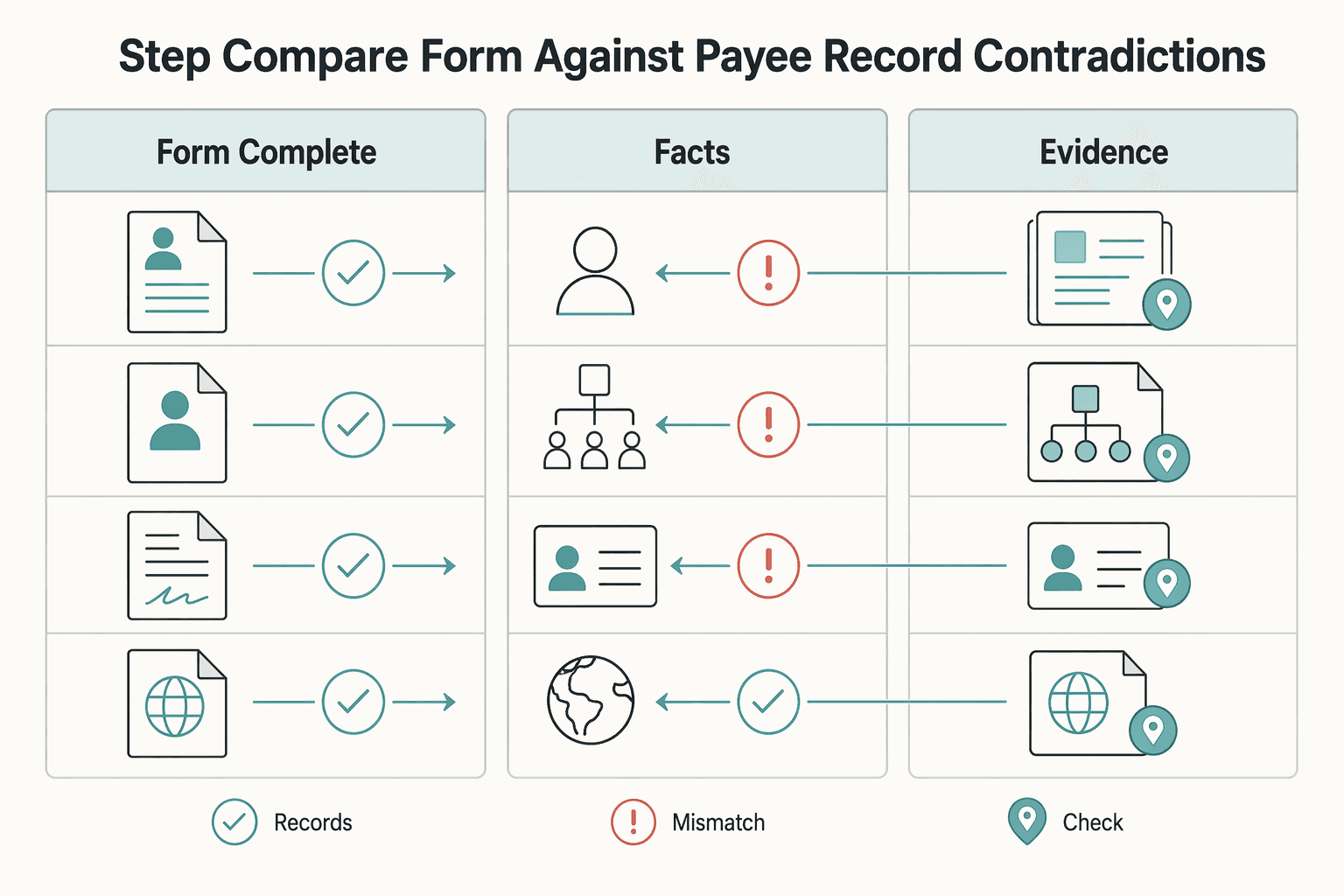

Step 2 Compare the form against the payee record for contradictions#

A complete form can still fail validation if it conflicts with your onboarding record. Before release, compare the accepted W-8BEN against the classified payee profile you set earlier: foreign person path, individual status, legal name, and country. This is where teams usually break down in practice, because they accept a document without checking whether it matches the payee they are about to pay.

Do not correct contradictions by assumption. If the profile says entity but the form is Form W-8BEN, or if the payee was routed to a Form W-9 path and someone uploads a W-8BEN to "fix it fast," keep the payout on hold and route the case to the named reviewer. The failure is not just clerical. It weakens your reliance position.

| Validation check | Failure mode | Payout action | Escalation path | Remediation evidence |

|---|---|---|---|---|

| Form is complete and readable | Partial upload, unreadable file, draft copy | Hold release | Tax profile approver | Corrected full form stored in record-retention location |

| Signed certification artifact is present | Missing signed certification or attestation not captured | Hold release | Tax profile approver | Signed replacement form and approval note |

| Form matches classified payee facts | W-8BEN conflicts with entity status, W-9 path, or onboarding record | Hold release | Compliance owner | Reclassified payee record or replacement form |

| Accepted form is retrievable from retained record | File exists in email or chat but not in linked archive | Hold release | Compliance owner or records owner | Archived form link, audit trail reference, reviewer sign-off |

Step 3 Route missing or invalid forms to withholding review#

If the form is missing or invalid, do not let operations treat it as a minor onboarding defect. Route it to withholding review before any payout moves. IRS instructions warn that if a withholding agent fails to obtain a valid Form W-8 or Form W-9 and also fails to withhold as required under the presumption rules, assessment exposure can follow. Depending on the facts, that can mean tax at the 30% rate under chapter 3 or 4, or the 24% backup withholding rate.

That is why the escalation owner here should not just be customer support. Missed validation issues can create underwithholding exposure, plus penalties and interest. Your evidence pack for release should therefore include the accepted form artifact, the reviewer decision, the retention link, and any remediation note showing how an earlier defect was resolved. If you cannot assemble that packet quickly, the payout should stay blocked.

If you want a deeper dive, read W-8BEN-E Explained for Platforms: How to Handle Tax Forms from Foreign Business Entities.

Route edge cases to the right form and specialist#

Once the W-8BEN itself looks complete, the next question is whether it is the right form at all. If the payee's facts point to treaty-exempt personal services, effectively connected income, or entity status, stop automation and move the case out of the standard individual flow before payment.

| Scenario | Route | Action |

|---|---|---|

| Personal-services income claimed exempt under a treaty | Form 8233 review | Place payout on hold and route for tax review |

| Income claimed effectively connected with a U.S. trade or business | Form W-8ECI review | Keep payout blocked and require tax or legal review before release |

| Payee facts indicate entity status | Form W-8BEN-E | Pause the case, reclassify the payee, and require the replacement form plus an approval note before payout |

Step 1 Flag treaty-based compensation claims for Form 8233 review#

Do not treat every mention of a tax treaty as a routine W-8BEN acceptance. For qualifying compensation for personal services, IRS instructions for Form 8233 say the payee should complete and give that form to the withholding agent if some or all compensation is exempt from withholding. The same instructions also warn that you must know the terms of the treaty between the United States and the treaty country to complete Form 8233 properly.

Your operating rule should be simple: if a contractor says their personal services income is exempt under a treaty, place the payout on hold and route the case for tax review instead of forcing it through the ordinary W-8BEN lane.

The verification point is not just "treaty claim mentioned." It is whether the record shows what income is being paid, what treaty country is being claimed, and whether the reviewer decided that Form 8233 is the correct path. If you need deeper treatment rules, this is the point to use your specialist queue or a dedicated reference like IRS Form 8233: When Foreign Contractors Claim Treaty Exemptions and What Platforms Must Verify.

A common failure mode is accepting a W-8BEN with a treaty box completed and assuming that settles a personal-services exemption claim on its own. When the claim depends on treaty-specific treatment, keep the reviewer note, the payee's written claim, and the final accepted form in one retrievable packet.

Step 2 Route effectively connected income to Form W-8ECI review#

If the payee indicates the income is effectively connected with a U.S. trade or business, do not push them back into Form W-8BEN just because they are a foreign individual. The IRS labels Form W-8ECI as the certificate for a foreign person's claim that income is effectively connected with the conduct of a trade or business in the United States.

Here the checkpoint is factual consistency. Does the payee actually state that the income is effectively connected, or is your team inferring that from vague comments about U.S. clients or U.S. work? If the form intent and the payee's explanation do not line up, keep the payout blocked and require tax or legal review before release. The bad outcome is not only a wrong upload. It is building a file that shows you saw an ECI signal and ignored it.

Step 3 Keep individual and entity paths separate#

The form boundary is explicit, so your intake should be too. Form W-8BEN is "for use by individuals," while Form W-8BEN-E is "for use by entities." That means a foreign company, partnership, or other entity should never clear an individual-only review path just because someone uploaded something quickly to unblock payment.

This is where teams often fail in practice: they fix missing data by swapping forms instead of rechecking payee type. Your red flag is any record where the legal name, contracting party, or tax form scope suggests an entity while the profile is coded as an individual. If that happens, pause the case, reclassify the payee, and require the replacement form plus an approval note before any payout moves.

Related: W-8ECI Explained for Platforms: When Foreign Contractors Have Effectively Connected US Income.

Tie form outcomes to withholding and reporting operations#

Once you have routed edge cases correctly, the next control is making form status change what finance actually does. An accepted form should feed U.S. tax withholding and Form 1042-S preparation, while a rejected or unresolved form should keep the payment in review or on hold. Form status is an input, not the whole tax conclusion.

Step 1 Map form status to a payment action#

Do not leave accepted or rejected tax forms sitting only in onboarding. The payment record needs the same outcome so the withholding agent can show why a payout was released, held, or sent for tax review. For foreign payees, that matters because Form 1042-S is the return used to report income and amounts withheld that fall within its scope.

Your verification point is simple: for any paid foreign-person record, you should be able to pull one chain that shows form type, acceptance status, decision date, reviewer or ruleset, and the withholding treatment applied. If the file shows "accepted Form W-8BEN" but nothing connects that acceptance to the actual payout decision, finance will have to reconstruct the record later, usually at the worst time.

Step 2 Store the evidence pack that explains the withholding treatment#

Keep the signed form artifact, the acceptance or rejection reason, the payee classification, any escalation notes, and the payout hold or release decision together. If a case moved out of the standard lane to Form 8233, Form W-8ECI, or Form W-8BEN-E review, store that routing note in the same packet. The party acting as the withholding agent, meaning the person with control, receipt, or custody of the amounts, needs to be able to prove why the treatment was applied.

One exact field matters more than teams expect: if tax withheld is less than 30%, the Form 1042-S instructions require a chapter 3 exemption code. That means a reduced or zero-withholding outcome cannot live only as a free-text reviewer note. Capture the reporting code requirement when the decision is made, not when year-end reporting starts.

A common failure mode is relying on a pre-filing validator or export check and assuming that fixes recordkeeping. It does not. The IRS makes clear that the withholding agent still has to correct the data in its own system of record before filing.

Step 3 Run a monthly control check for reporting readiness#

A monthly review is an internal control choice, not an IRS-mandated cadence, but it catches drift before year-end. Review these items together so missing documentation, unresolved exceptions, and reporting gaps surface in one pass:

- accepted forms on file and retrievable

- blocked payouts waiting on form acceptance or specialist review

- unresolved exceptions involving Form 8233, Form W-8ECI, or payee-type conflicts

- records expected to flow to Form 1042-S

- records with withholding below 30% that still lack a chapter 3 exemption code flag

The outcome you want is not just a clean dashboard. You want every paid foreign-person record to be reporting-ready, every blocked case to have an owner and next date, and every exception to have a document trail finance can hand over without rebuilding the file from scratch.

You might also find this useful: How to Fill Out Form W-8BEN for a Foreign Freelancer.

Keep an audit-ready record set without overcollecting data#

Keep less, but tie it together better. For Forms W-8, the right file is not the biggest file. It is the smallest record set that can prove why you released or held a payment, what withholding treatment you applied, and how that decision supports Form 1042-S reporting.

Step 1 Retain only liability-relevant records#

Start with the records that actually support your liability position: the signed Form W-8BEN or other required tax form artifact, the payee's classification, the acceptance or rejection outcome, the decision date, and the payout or withholding action taken. IRS requester guidance is clear on two points that matter operationally: "Do not send Forms W-8 to the IRS," and keep them in your records "for as long as they may be relevant to the determination of your liability."

That is the retention rule that matters most. Do not invent a fixed calendar rule if your facts do not support it, and do not turn tax recordkeeping into broad collection of unrelated sensitive data. If a passport copy, utility bill, or extra banking document is not needed for your onboarding or sanctions controls, do not attach it to the tax file just because it is available.

Your verification point is practical: pick one paid foreign contractor and confirm that one record shows the form artifact, the payee type, the approval result, and the payment outcome without pulling from five tools. A common failure mode is storing copies in email, ticket comments, and shared drives, which spreads sensitive data while still leaving gaps in the actual audit trail.

Step 2 Link each tax form to the payment it supported#

The document set has to be payment-traceable, not just onboarding-complete. For each payout or payout batch, keep a link to the exact form version relied on, the acceptance status at the time of payment, the decision date, and the withholding treatment applied. If a case was overridden or manually released, add internal notes showing who approved it, what evidence was reviewed, and any planned follow-up.

The IRS does not prescribe those exact note fields for your internal process, but you still need a clear record. If you cannot reliably associate a payment with valid documentation, presumption rules apply, and that can leave you liable for tax, interest, and penalties. One red flag to watch for is a later-uploaded form with no version history, leaving finance unable to prove which document supported an earlier payout.

Step 3 Label adjacent filing features so teams do not confuse scope#

If your platform or a nearby compliance tool also tracks FBAR, FinCEN, FATCA, or Form 8938 items, label that scope plainly. Form 8938 is used to report specified foreign financial assets. FBAR, meaning FinCEN Form 114, is not filed with the IRS, and the Form 8938 filing requirement does not replace a taxpayer's FBAR obligation. FATCA generally concerns reporting by foreign financial institutions and certain other entities about foreign assets held by U.S. account holders.

Your recommendation here is simple: keep those features out of payout release logic unless you have a separate legal basis to use them. If you surface reference thresholds such as the $10,000 FBAR trigger or the $50,000 / $75,000 Form 8938 example for specified individuals living in the U.S., mark them as personal filing references, not platform withholding controls.

Common failures that trigger penalties and how to recover fast#

Once your records are linked, speed matters. If a payment cannot be reliably associated with valid documentation, the Internal Revenue Service says a withholding agent generally must withhold 30% from the gross amount paid to a foreign payee unless valid documentation supports different treatment. Failed collection can also create 24% backup withholding exposure in relevant cases, plus interest and penalties.

Step 1 Fix missing or late documentation first#

If the form was missing when a payment was evaluated, do not treat a later upload as if it automatically solved the earlier gap. First identify which payments were made without documentation you could reliably associate to the payee. Then route those payments for withholding review before additional releases.

A practical recovery step is to pause additional releases while the case is reviewed. The goal is not to invent a platform-wide IRS cure deadline. It is to rebuild a defensible record: what was paid, what documentation was missing, what form was later collected, and what withholding decision applies now.

Step 2 Replace the wrong form family, not just the file#

Some of the fastest failures are form-family errors. A foreign entity should not be documented on Form W-8BEN, and an individual should not be parked on Form W-8BEN-E. IRS instructions are explicit that foreign entities use W-8BEN-E, while individuals use W-8BEN.

When you find this error, reclassify the payee, collect the correct form, and keep the correction note with the payment record. Do not mark the old upload "accepted" just to clear the queue. The real fix is a corrected payee classification plus the right form in the record you rely on.

Step 3 Escalate treaty and ECI conflicts before more payments move#

Two edge cases deserve fast escalation. For compensation for personal services that is claimed exempt from withholding under a treaty, Form 8233 may be the right route. And if the income is effectively connected with a U.S. trade or business, the IRS says Form W-8BEN is no longer valid for that income and Form W-8ECI must be filed instead.

The fastest practical recovery is to pause automated approval, route the record to a tax reviewer, and document the replacement form and final treatment in the same system of record you use for withholding and reporting. That gives finance something usable later and lowers the chance that the same payee is paid again under the wrong assumption.

Conclusion#

A workable W-8BEN control framework is not complicated, but it does have to be explicit:

- collect Form W-9 for U.S.-person TIN reporting

- route foreign entities to Form W-8BEN-E

- send treaty-based personal-services exemption cases to Form 8233 review

- route effectively connected income cases to Form W-8ECI review

- keep withholding decisions and reporting decisions linked, but separate

- stay ready for Form 1042-S reporting when reportable payments exist, even if chapter 3 withholding is zero because the income was exempt

That last point matters. No withholding is not the same as no reporting. And if valid Form W-8 or W-9 documentation is missing, exposure can include tax at 30% or 24%, plus interest and penalties, depending on the facts.

If your team can show the right form path, the accepted document, the reason a payment was released or held, and the reporting treatment that followed, you are operating from a much stronger position than "form collected."

Frequently Asked Questions

When should you collect Form W-8BEN?

Collect it when requested by the withholding agent or payer. Operationally, many teams collect it before relying on it for payout release so payment and documentation do not drift apart.

What if the payee is a U.S. person or a foreign entity?

Route U.S. persons to Form W-9 for TIN collection. Route foreign entities to Form W-8BEN-E. Form W-8BEN is for foreign individuals, not entities.

Is an uploaded W-8BEN enough on its own?

No. Validation should cover proper completion and the signed certification, not just file presence. A withholding agent or payer may rely on a properly completed Form W-8BEN.

What if the form is missing?

If Form W-8BEN is not provided, the withholding agent may have to withhold at the 30% rate. Missing or invalid documentation can also create other withholding exposure depending on the facts.

When do treaty cases go to Form 8233?

Route compensation for personal services that is claimed exempt from withholding for Form 8233 review. The right outcome depends on the income type and the facts, so do not treat every treaty mention as the same case.

When do you use Form W-8ECI?

Use Form W-8ECI handling when a foreign person claims the income is effectively connected with a U.S. trade or business.

How long does a W-8BEN stay valid?

Generally, it remains in effect starting on the date signed and ending on the last day of the third succeeding calendar year, unless a change in circumstances makes the information incorrect sooner.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

IRS Form 8233: When Foreign Contractors Claim Treaty Exemptions and What Platforms Must Verify

Form 8233 is used by nonresident alien individuals to claim exemption from withholding on compensation for personal services, but for platform operators the key exposure is often operational: scope decisions, review quality, recordkeeping, and escalation. When you pay nonresident individuals for U.S.-source personal services income, the real risk is often not whether a form exists, but whether your team can show why a claim was accepted.

How Platforms Should Collect and Validate Form W-8BEN-E for Foreign Entities

Treat Form W-8BEN-E collection as a payout control, not a paperwork task. If you are the withholding agent, you generally must obtain valid documentation before payment. Without it, IRS guidance says you generally must withhold 30% from the gross amount paid to a foreign payee.

W-8ECI for Platforms Handling Foreign Contractors With Effectively Connected US Income

Start with a simple checkpoint. Verify that the payee is actually claiming foreign status and using the right form for that claim. Then confirm that the record ties the form to U.S.-source income and an ECI position. A common failure mode is accepting the document because it is signed and looks current, while never capturing the business facts that explain why W-8ECI was used instead of W-8BEN. Where source detail is limited, such as exact refresh cadence, this article flags legal-tax escalation points instead of pretending the IRS gives platforms one clean decision matrix. Related reading: [How Platforms Are Reshaping Foreign Exchange in 2026](/blog/platforms-reshaping-foreign-exchange-landscape).