Quick Answer

Build a gated decision path before issuing any no-VAT invoice: classify the transaction, validate buyer taxable-person evidence, lock invoice wording, and map reporting to the legal entity that files. Use Article 194 references as review anchors, not automatic outcomes. Keep proof at decision time with the VAT ID result, timestamp, invoice version, and rules log, then reconcile to regular VAT returns and any OSS filings in scope. If country treatment is unclear, pause automation and escalate.

Why Reverse Charge Requires an Owned Control Decision, Not a Default#

For cross-border B2B platforms, a common risk is not just recognizing the phrase "reverse charge." It is being able to show why a treatment was used, who owned the decision, and what happens when the facts do not fit the default path. This guide focuses on those controls so decisions can hold up at invoice, filing, and audit time.

It is written for compliance, legal, finance, and risk owners in multi-market platforms that control tax determination, invoice logic, record keeping, and audit response across jurisdictions. It is not aimed at one-country, single-entity setups with no cross-border exposure, where this level of control may be unnecessary.

Who should keep reading#

Keep reading if your platform sits between business buyers, sellers, contractors, or service providers and your team has to make repeatable VAT decisions at scale, because role mapping matters.

In some cases, a marketplace can be treated as a deemed supplier. Even where it is not, platforms can still have record-keeping requirements for supplies of goods and services.

That makes evidence the key checkpoint, not just the outcome. If your current logic only asks, "do we charge VAT or not?", it likely misses the documentation layer that audit reviews depend on.

What the list will optimize for#

The controls in the next sections are ranked against four practical tests:

- legal defensibility under EU VAT rules and local implementation, especially where cross-border facts are messy

- operational effort to build and maintain the control, not just design effort

- failure impact on VAT return accuracy and related reporting

- clarity of ownership across tax, product, finance operations, and legal

The list therefore favors controls you can enforce, verify, and escalate. A technically clever position that operations cannot execute consistently is not a reliable control.

The scope limits that matter#

EU platform VAT discussions are often shaped by the 1 July 2021 B2C e-commerce changes and OSS. That context matters, but it does not answer every cross-border VAT decision.

| Scheme | Filing cadence | Return status |

|---|---|---|

| Union | quarterly | OSS returns are additional and do not replace the regular VAT return |

| Non-Union | quarterly | OSS returns are additional and do not replace the regular VAT return |

| Import | monthly | OSS returns are additional and do not replace the regular VAT return |

OSS is optional. Registration is in one Member State of identification. OSS returns are additional and do not replace the regular VAT return. Filing cadence differs by scheme: quarterly for Union and non-Union, monthly for import.

Use that as an immediate control check: if someone says "we are covered because we use OSS," confirm which scheme they mean. Confirm which legal entity is registered and whether they still account for the regular VAT return alongside OSS.

For genuinely complex cross-border transactions involving two or more participating EU countries, VAT Cross-border Rulings are an escalation path. A taxable person can request an advance VAT ruling. The request must follow the national VAT-ruling conditions in the filing country. Where multiple companies are involved, one company should submit on behalf of the others.

The rest of the guide turns those points into practical decision checkpoints, reporting checks, and escalation triggers for cases where VAT treatment is still unclear.

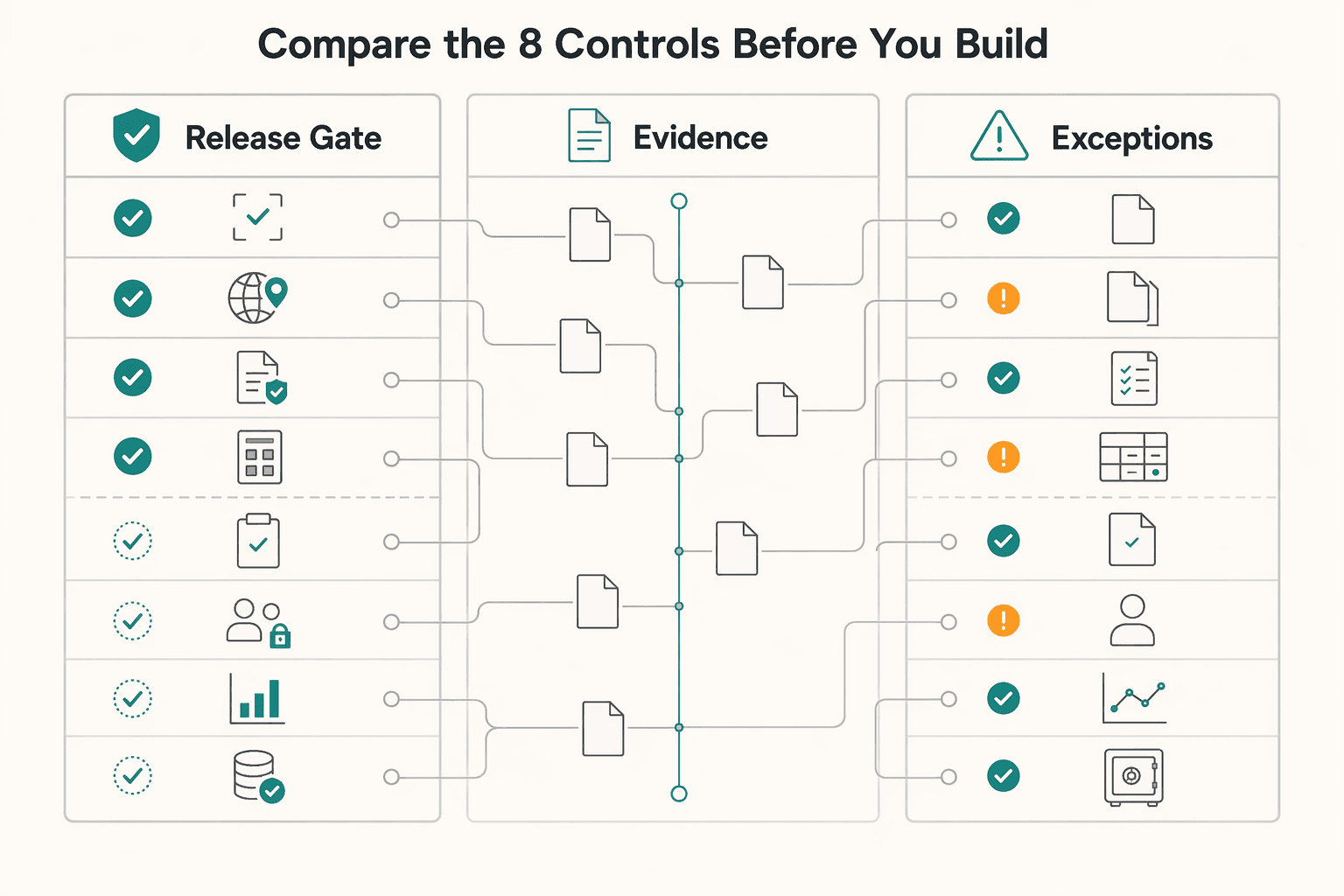

The 8 controls that matter most for B2B marketplace VAT#

If you only build five controls first, start with these. They address a common failure pattern: treating a no-VAT outcome as a default instead of a decision your platform has to classify, evidence, invoice, report, and escalate.

This shortlist is grounded in EU checkpoints; detailed B2B reverse-charge eligibility, invoice wording, and listing duties still need jurisdiction-specific legal confirmation.

1. Supply classification gate#

Start here whenever you run mixed B2B and B2C flows. This gate stops the wrong tax path from being chosen at source, before invoice and reporting logic are applied.

The control only works if classification is structured. From 1 July 2021, B2C e-commerce VAT rules changed, and in certain circumstances a marketplace can be treated as a deemed supplier for goods. Record-keeping requirements can still apply even where it is not deemed supplier. Make supply type an explicit setup field with ownership and approval, because one miscoded flow can spread quickly.

2. Taxable-person validation gate#

For high-volume onboarding, this is an evidence control more than a technical check. Validation outputs can support your decision record, but they are not a substitute for legal classification.

Set one process to capture buyer taxable-person evidence and validation output before invoicing, and define clear recheck triggers in your operating model. The risk is relying on old validation results after key buyer details change. For team process detail, use How to verify a European VAT number using the 'VIES' system.

3. Invoice wording and data gate#

At scale, invoice consistency is part of audit defense. If invoice content does not match the treatment you chose, the evidence chain weakens even when the underlying decision was reasonable.

Lock approved templates and required buyer and treatment fields in the invoicing layer, and block release when required evidence is missing. For cases with non-standard VAT treatment, keep wording aligned to the jurisdictional position your legal analysis supports rather than letting templates drift by entity.

4. Return and listing gate#

Reporting controls have to follow the entity and filing channel that actually owns the obligation. Do not assume commercial flow equals reporting ownership.

Keep OSS in scope without stretching it too far. OSS returns are additional and do not replace the regular VAT return. Filing cadence differs by scheme: quarterly for Union and non-Union, monthly for import. Reconcile invoice populations and treatment flags against filed returns and OSS scheme scope.

5. Jurisdiction exception gate#

Legal uncertainty should stop a launch, not trail behind it. This control prevents expansion-by-template risk.

For non-EU markets, route cases to explicit legal review instead of assuming EU-style logic carries over. For complex EU transactions involving two or more participating countries, VAT Cross-border Rulings are an escalation path. Requests are made in the participating EU country where the requester is VAT-registered and must follow that country's national VAT-ruling conditions.

These five controls come first because every later control depends on the facts they capture. If you want a deeper dive, read How to Handle VAT when a UK LTD invoices an EU business client post-Brexit.

Compare the 8 controls before you build#

Build in sequence, not all at once. Controls 1-4 usually determine whether a potential no-VAT or exempt path is defensible and whether filings can be reconciled. Controls 5-8 mainly reduce exception, ownership, and audit risk.

The legal-anchor column below is a planning label, not legal advice. For EU outcomes, treat EU law and local law as binding. Filing impact is operational: D = can directly change reporting path or VAT return population, S = mainly supports evidence or reconciliation. This table does not resolve article-level reverse-charge rules, mandatory invoice wording, or EC Sales List applicability.

| Control | Legal anchor | Owner | Best for / key pros-cons / concrete use case | Failure mode | Detection checkpoint | Escalation trigger | Filing impact (Reporting / Evidence / Return) | Complexity | Audit evidence |

|---|---|---|---|---|---|---|---|---|---|

| Supply classification gate | EU and local law; apply OSS and deemed-supplier rules where relevant | Product + Tax | Best for mixed B2B/B2C flows. Pro: prevents early routing errors. Con: taxonomy upkeep. Use when goods and services logic can split by flow, including deemed-supplier uncertainty in some marketplace cases. | Wrong supply type sends transactions into the wrong tax path | Taxonomy approval review and spot checks on new flows, including where post-1 July 2021 B2C changes may affect classification boundaries | New supply type, goods flow, or deemed-supplier uncertainty | D / S / D | Context-specific | Approved taxonomy, supply flags, decision log, owner signoff |

| Taxable-person validation gate | Same | Ops + Tax | Best for high-volume onboarding before no-VAT invoicing. Pro: strong evidence trail. Con: stale checks create false confidence. Use where buyer entity details can change after onboarding. | Missing or outdated buyer taxable-person proof | Validate before invoice release; recheck after buyer legal-entity or profile change | Failed validation, key-detail change, repeated invoice failures | D / S / D | Context-specific | VAT ID input, validation snapshot, timestamp, source, recheck history |

| Invoice wording and data gate | Same | Finance Ops | Best for multi-entity invoicing at scale. Pro: consistent, auditable invoice output. Con: tighter release controls can slow operations. Use where template drift has appeared before. | Missing required fields or invoice content that cannot be supported by documented treatment | Release block when required buyer or treatment fields are missing | Manual override request or out-of-process template change | D / S / D | Context-specific | Template version history, invoice copy, field-completeness log |

| Return reporting gate | Same | Tax + Finance | Best for multi-entity filing with OSS coexistence. Pro: clearer reporting ownership. Con: higher reconciliation load. Use when one flow can touch regular returns plus OSS channels. | Supplies mapped to wrong entity or wrong return | Reconcile invoice population to the regular VAT return; confirm OSS return cadence (quarterly Union and non-Union, monthly import) and that OSS returns are additional (not replacements) | Unreconciled differences or scheme-ownership confusion | S / S / D | Context-specific | Return-mapping matrix, reconciliation file, entity-ownership notes |

| Jurisdiction exception gate | Same | Tax + Legal | Best for non-EU expansion or complex EU chains. Pro: blocks risky template reuse. Con: legal review time. Use when local treatment confidence is low. | EU-style assumptions reused where local treatment differs; registration timelines can slip when anti-evasion investigations are required | Country watchlist and legal signoff before go-live; for cross-border SME exemption flows, confirm turnover is within EUR 100 000 and EX-number confirmation before exempt treatment starts | Low-confidence jurisdiction, delays beyond expected processing windows (up to 35 working days), or need for a VAT Cross-border Ruling (filed in the participating Member State where VAT-registered, under national ruling conditions; if multiple companies are involved, one company submits) | D / S / D | Context-specific | Country matrix, legal memo, CBR request or response |

| Responsibility map gate | Same | Legal + Product + Tax | Best for mixed facilitation, payout, and invoicing roles. Pro: clarifies obligation ownership early. Con: cross-team alignment burden. Use when invoice issuer, payout controller, and contractual supplier can differ. | Unclear VAT obligation owner across platform, seller, and buyer | Contract and flow signoff before automation | Role ambiguity or deeper transaction control than planned | D / S / D | Context-specific | Contract extracts, role matrix, transaction-flow diagram |

| Audit evidence pack gate | Same | Tax Ops + Finance | Best when logic exists but proof is fragmented. Pro: stronger audit defense. Con: storage and process discipline needed. Use where evidence sits across multiple systems. | Evidence exists but cannot be reconstructed by legal entity or transaction | Retrieval test by entity and transaction sample | Missing proof chain or missing change log | S / S / S | Context-specific | Validation proof, invoice version, rule log, return map, exception notes |

| Escalation and handoff gate | Same | Tax + Legal + Ops | Best for exception-heavy launches. Pro: stops unresolved cases before filing. Con: requires active queue governance. Use when validation or entity conflicts and return mismatches recur. | Gray-zone transactions continue without decision | Queue-aging review tied to filing cycle | Failed status checks, conflicting entity data, repeated return mismatch | S / S / S | Context-specific | Ticket trail, approval log, hold or release record |

If you have one filing cycle before launch, implement 1-4 first, then add a thin but enforced 8 so uncertain cases stop instead of auto-processing. Add 5-7 before expansion, entity growth, or audit pressure forces rushed implementation.

Before implementation, run your highest-volume corridors through the VAT reverse charge checker as an initial screen before invoice and filing logic is locked.

Classify the transaction before any VAT decision#

Classification has to come before tax calculation. If you skip that step, every later control is weaker.

-

Set the order upfront. If a transaction is a cross-border B2B service, do not assume reverse charge; test whether it may apply before running VAT amount logic. Set a first-pass label at creation: service or goods-related, B2B or B2C, domestic or cross-border, and contracting legal entity. This prevents a common failure mode: mixed platform flows routed through one generic tax branch.

-

Keep cross-border services and goods in separate branches. OSS content is explicit that, from 1 July 2021, the rule change is about cross-border B2C e-commerce, not a general B2B reverse-charge rulebook. For goods flows, keep a dedicated check because, in certain circumstances, a marketplace can be treated as a deemed supplier for VAT purposes. If treatment changes by product line or flow type, do not force one shared rule.

-

Use legal anchors as decision labels, not auto-results. You can map branches to EU VAT Directive anchors and note Article 194 where your tax team confirms relevance, but do not hard-code it as an automatic outcome. Record the anchor plus jurisdiction-specific confirmation in the decision log. For complex cross-border cases, use VAT Cross Border Rulings (CBR): file in the participating EU country where the requester is VAT-registered, and if multiple companies are involved, one group company can submit for the others.

-

Treat mixed models as an ongoing control risk. Platforms that combine multiple transaction types do not have one supply type, so recheck classification when new SKUs, service codes, corridors, or contract structures are introduced. Also flag early if a seller relies on the cross-border SME scheme. It requires prior notification in the Member State of establishment and is subject to the EUR 100 000 Union turnover cap.

Validate buyer status and keep proof current#

Buyer-status checks can serve as a release gate before invoicing, but the EU excerpts here do not prescribe one mandatory VIES sequence for reverse-charge decisions. What matters is that your process is consistent and reconstructable.

- Set an internal order and apply it consistently

For cross-border EU B2B service flows, collect the buyer VAT ID and legal-entity details before invoice issue, then run your validation step and store proof at decision time. Treat this as your control design, not as a legal sequence.

- Keep a usable audit trail, not just a pass or fail flag

Store a snapshot tied to the invoice decision so your team can show what was checked and when. A practical record can include the VAT ID used, outcome, timestamp, and whether the check was system-run or operator-run. That is an operational standard, not a legal minimum listed in the sources. If helpful, link your internal SOP to How to verify a European VAT number using the 'VIES' system.

- Re-check when risk signals change

A one-time validation at onboarding is often not enough for an ongoing control. Revalidation on material buyer-data changes or repeated invoice failures is a risk-based policy choice, not a requirement stated in the excerpts.

- Separate VAT-number checks from other status determinations

VAT-number validation does not answer every scheme question. In the cross-border SME scheme, a business files prior notification in its Member State of establishment, and exemption starts only from the date that state grants the EX number. The process should not exceed 35 working days, but may take longer when additional investigations are needed.

Do not use OSS B2C logic to fill B2B buyer-status gaps. The cited 1 July 2021 change is explicitly for cross-border B2C e-commerce, and OSS returns are additional to regular VAT returns. If status is unclear in a high-value or unusual case, pause automation and escalate. For complex cross-border treatment questions, consider requesting a VAT Cross-border Ruling in a participating EU country where the requester is VAT-registered.

Lock invoice content so reverse charge is enforceable#

A correct tax decision can still fail in practice if invoice text or fields drift after the decision. Once buyer status is set, lock invoice content with the same discipline.

- Standardize templates by national rule, not one EU default.

Use controlled reverse-charge templates with local overrides owned by tax or finance. EU invoicing explanatory notes are practical, informal guidance, not legally binding law, and they are not complete. Each Member State is responsible for transposing Directive 2010/45/EU, and national tax administrations are the principal source for local interpretation and application. Treat reverse-charge wording and VAT display as jurisdiction-specific controls, not one universal template.

- Design invoice fields for control and operations, not display alone.

Keep key invoice attributes as structured data, for example issuing entity, buyer legal name, buyer VAT ID, country, date, invoice number, and reverse-charge flag, so finance and compliance can reconcile decisions later. A visually correct PDF is not enough if core decision data sits in free text.

- Block release when key evidence or local elements are missing.

Add a QA gate that stops invoice issue when template version, buyer-status evidence, or locally expected wording/fields are missing for that flow. Keep the invoice version ID with the earlier validation snapshot and the national guidance reference used for the template rule. If UK and EU invoicing run through one queue, link this control to your local guidance, such as How to Invoice a UK Client to Avoid VAT Complications Post-Brexit.

Map reporting duties to entities, not assumptions#

Reporting failures in a reverse-charge setup often come from entity confusion, not the first tax decision. After invoice content is locked, map each reporting duty to the legal entity that issued, received, or must account for the supply.

- Assign supplier-side reporting to the legal issuer

Keep the invoice issuer as the owner of source records, return mapping, and filing evidence. Follow the sequence in HMRC guidance: determine place of supply first, then VAT liability. If place of supply is outside the UK, no UK VAT is chargeable. Tie the evidence pack to that entity: invoice number, buyer legal name, buyer VAT ID, country, reverse-charge flag, and place-of-supply decision snapshot.

- Record buyer self-accounting as counterparty duty

Where reverse charge applies, record who is expected to self-account, but do not treat that as automatic proof of your own filing duty. For supplies received from outside the UK, Section 8 of the VAT Act 1994 covers the reverse-charge accounting mechanism. Keep buyer-side accounting paths in buyer or local-finance review, with entity-level signoff before any VAT return posting.

- Separate cross-border services from UK domestic reverse charge

Do not route all reverse-charge invoices into one reporting bucket. Keep cross-border services reverse charge and UK domestic reverse charge in separate review paths by entity. Notice 735 says the domestic regime applies to specified goods and services and is not the same as cross-border services reverse charge.

- Reconcile to filed outputs, not invoice volume alone

Reconcile by legal entity across invoice population, reverse-charge flags, and filed reporting outputs. Use this checkpoint to catch mapping drift after entity launches, template edits, or master-data changes. For UK domestic reverse-charge cases, document whether Reverse Charge Sales List (RCSL) review was considered and whether it applied. Sections 65 and 66 of the VAT Act 1994 and regulations 23A-23D of the VAT Regulations 1995 tie controls and penalties to that artifact. If a non VAT-registered business receives specified domestic reverse-charge supplies, escalate for VAT-registration exposure review.

Handle countries where reverse charge may not protect you#

Reverse charge can be correct on a B2B invoice and still leave local VAT-registration exposure in some countries. Treat non-EU expansion as a separate control decision, not as a copy of your EU template.

1. Build a two-track jurisdiction matrix#

Use two outcomes per country and corridor: reverse charge expected and possible Non-resident VAT registration required. For each row, capture seller entity, supply type, buyer status, invoice treatment, filing owner, confidence level, legal basis, and review date. No corridor should go live with an incomplete row or without a named approver.

| Country or bucket | What the current evidence supports | What you should not assume | Required next action |

|---|---|---|---|

| Participating EU countries | VAT Cross-border Rulings (CBR) can be used for complex cross-border VAT transactions between participating EU countries | That EU mechanisms decide non-EU treatment | If EU treatment is unclear, consider CBR before scaling |

| Philippines | The materials here do not establish an EU-style reverse-charge outcome or local non-resident VAT registration triggers | That B2B status alone removes local VAT obligations | Keep on watchlist; require local review before go-live |

| South Africa | The materials here do not establish an EU-style reverse-charge outcome or local non-resident VAT registration triggers | That EU invoice logic applies unchanged | Keep on watchlist; require local review before go-live |

2. Keep EU tools in their lane#

Use EU tools for EU ambiguity, not for non-EU conclusions. CBR is an EU mechanism for complex cross-border transactions between participating EU countries, filed in the participating country where the applicant is VAT-registered. When multiple companies are involved, one can file on behalf of the others.

Apply the same boundary to OSS. OSS is optional. Registration is in one Member State of identification. OSS returns are additional to regular VAT returns. Filing cadence differs by scheme: quarterly for Union and non-Union schemes, monthly for the import scheme. Those features help with administration, but they do not prove non-EU B2B reverse-charge treatment.

Also keep B2C context separate from this B2B decision. The 1 July 2021 e-commerce change and the EUR 10,000 threshold are B2C context, not a non-EU B2B shortcut.

3. Put Philippines and South Africa on a named watchlist#

Make Philippines and South Africa explicit exception entries. Until local analysis is complete, keep both in manual review. Do not allow an automatic no-VAT invoicing path, and do not assume buyer self-accounting fully closes the issue.

4. Escalate low-confidence countries before go-live#

If confidence is low, stop launch. Typical signs are EU-only support for a non-EU decision, mixed platform and seller roles not covered in your file, or a blank or stale legal basis in the matrix.

For EU ambiguity, CBR is an escalation route documented here. For non-EU ambiguity, escalate to local advice before go-live. Keep a reconstructable evidence set for approval: matrix row, dated legal advice, seller entity, supply description, buyer type, intended invoice treatment, filing owner, and signoff.

Related: When OSS VAT Applies and When Reverse Charge Handles EU Work.

Decide platform vs seller vs buyer responsibility early#

Do not launch invoicing or payouts until each transaction pattern has clear ownership for supplier role, invoice issuance, and filing duty. When roles stay vague, the practical result can be wrong invoice treatment, wrong return ownership, and audit gaps.

1. Lock the responsibility map before automation#

Treat each scenario as not ready until platform, seller, and buyer responsibilities are each explicitly assigned. At minimum, map the contracting entity, invoice issuer, funds-flow owner, payout trigger owner, tax-treatment decision owner, and reporting owner.

Use a hard go-live check. For every row, confirm the invoicing entity, supply description, buyer type, intended VAT treatment, and filing owner. If any field is TBD, split between two owners, or unclear in the VAT return path, hold automation.

2. Separate facilitation from deeper transaction control#

Do not use one role label for all marketplace patterns. Keep "platform-only facilitation" separate from "platform with deeper transaction control." Platforms are part of the VAT e-commerce supply chain and, in certain goods cases, can be treated as having received and supplied the goods, as deemed supplier.

That is not a blanket rule for all marketplace flows or all services. It is a signal to run separate analysis where control is deeper instead of reusing a default "seller liable" assumption.

A practical split for your map is below:

| Scenario row | What to decide before rollout |

|---|---|

| Platform-only facilitation | Who contracts, who invoices, who files, and where tax-treatment logic is applied |

| Deeper platform control | Whether the platform's role changes VAT ownership analysis, plus who files in practice |

Do not treat B2C context as a shortcut for B2B role allocation. The 1 July 2021 e-commerce changes and the EUR 10 000 threshold are B2C context.

3. Escalate unresolved role ambiguity and pause rollout#

If responsibility is still unclear after review, escalate before go-live and keep affected jurisdictions on manual handling. For complex EU cross-border ambiguity, use VAT Cross Border Rulings (CBR) as the formal path described here.

Operational checkpoints:

- If multiple companies are involved, submit one CBR request on behalf of the others.

- File in the participating EU country where the requester is VAT-registered.

- Block automated no-VAT invoicing and payout logic that depends on unresolved liability.

Also, do not treat OSS as a substitute for responsibility mapping. OSS returns are additional and do not replace regular VAT returns, so assign filing ownership by entity for both domestic and OSS obligations where relevant.

If platform, seller, and buyer responsibilities cannot be explained clearly on one page for a scenario, do not automate that scenario yet.

This pairs well with our guide on MoR vs. PayFac vs. Marketplace Model for Platform Teams.

Build the minimum audit evidence pack#

Once responsibility is fixed, evidence becomes the next control. A defensible position is not just that the rule was applied. It is that the decision can be reconstructed by legal entity, invoice, and filing period.

| Record | Keep | Why |

|---|---|---|

| Tax-status input evidence | buyer tax-status inputs relied on, the result used at decision time, the timestamp, and whether the check came from an API, batch job, or manual review | enough context to explain later why the VAT treatment was selected |

| Invoice actually issued | rendered invoice, invoice number, issue date, supplier legal entity, buyer legal entity, currency, and the template or rules version in effect at issuance | archive the invoice actually issued, not just template metadata |

| VAT treatment decision logic | transaction attributes used, the resulting VAT treatment, the ruleset version, and any manual override reason | a final tax outcome without decision inputs is weak evidence |

| Return mapping by legal entity | regular VAT return, OSS return where relevant, or manual hold pending review; Member State of identification and filing period where relevant | ties each invoice or credit note to its reporting path |

| Exception and escalation notes | date, approver, issue raised, and supporting memo | keeps the history for blocked, manually approved, or escalated transactions |

Keep five records for each in-scope transaction#

- Tax-status input evidence

Keep the buyer tax-status inputs your team relied on, the result used at decision time, the timestamp, and whether the check came from an API, batch job, or manual review. Keep enough context to explain later why the VAT treatment was selected.

- The invoice version actually issued

Archive the rendered invoice, not only template metadata. Keep invoice number, issue date, supplier legal entity, buyer legal entity, currency, and the template or rules version in effect at issuance.

- VAT treatment decision logic

Store the transaction attributes used, the resulting VAT treatment, the ruleset version, and any manual override reason. A final tax outcome without decision inputs is weak evidence.

- Return mapping by legal entity

Tie each invoice or credit note to its reporting path: regular VAT return, OSS return where relevant, or manual hold pending review. OSS returns are additional and do not replace regular VAT returns, and if you use an OSS scheme, supplies in scope for that scheme should be declared through OSS. Where relevant, keep the Member State of identification and filing period in the record chain.

- Exception and escalation notes

Keep notes for blocked, manually approved, or escalated transactions, including date, approver, issue raised, and supporting memo. For complex cross-border uncertainty, keep the CBR-related escalation trail if an advance treatment ruling is considered.

Keep retention usable for later reclaim support#

Do not design retention only for invoice issuance. Where reclaim or cross-border recovery may matter, keep records organized so they can support later claim preparation. Do not assume this section defines those claim requirements.

Make the evidence chain reconstructable#

A common failure mode is fragmented evidence across billing, ERP, tax engine, ticketing, and email. Use a simple test: for one audited entity and period, can operations produce tax-status input evidence, issued invoice, tax decision trail, filing destination, and exception history in one chain?

Use stable identifiers across systems: customer account, invoice number, transaction ID, legal entity, and filing period. The standard is not "evidence exists somewhere." It is "the file is reconstructable on demand."

Set escalation triggers and ownership handoffs#

Automation should flag cases whenever the legal basis or evidence chain is incomplete. At that point, route the treatment decision to a named owner before final VAT treatment is applied.

| Trigger | Article detail | Response |

|---|---|---|

| Missing chain-transaction facts | cannot show who arranged transport and which VAT number the intermediary used | trigger review |

| Missing acquisition evidence | cannot evidence that the acquisition was declared in the Member State of arrival | trigger review |

| Wrong VAT-ID signal | where VAT-ID usage appears incorrect; in the Article 41 context this can create exposure where output VAT is due without a corresponding input VAT deduction right | escalate promptly |

| Aging or recurring control failure | a repeated or long-running exception is a control risk, not just backlog | escalate beyond operations |

- Use evidence-based escalation triggers

Trigger review when a chain transaction cannot show who arranged transport and which VAT number the intermediary used. Also escalate when you cannot evidence that the acquisition was declared in the Member State of arrival. These are core facts for VAT treatment, and missing them makes automated decisions unreliable.

- Treat wrong VAT-ID signals as high severity

Where VAT-ID usage appears incorrect, escalate promptly. In the Article 41 context, this can create exposure where output VAT is due without a corresponding input VAT deduction right.

- Separate case handling from final sign-off

Keep operations focused on collecting facts, but route the treatment decision to a clearly designated owner outside day-to-day execution. That helps prevent gray-zone cases from being handled as routine.

- Escalate aging or recurring control failures

A repeated or long-running exception is a control risk, not just backlog. Audits can surface multi-year VAT-ID and control failures, and disputed treatment may need formal escalation beyond operations.

Roll out in phases without overbuilding#

Roll out narrowly first, then widen. Start with your highest-volume B2B corridors in the EU, prove evidence and filing quality, and only then expand into exception-heavy markets.

- Phase corridors, not the whole product

Limit the first release to a small set of EU corridors and only the core controls: classification, VAT validation, invoicing, and reporting mapping. Keep B2C logic out of this pilot so you can test B2B treatment cleanly.

- Ship controls in a filing-safe sequence

Use a practical order: classification, VAT validation, invoicing, reporting, then jurisdiction exceptions. Treat this as a control design choice, not a legal mandate, and require each step to produce usable evidence for the next.

- Gate scale-up on real reporting cycles

Do not scale until at least one full filing cycle reconciles invoice data, reverse-charge flags, and filed returns. For separate flows such as cross-border B2C e-commerce, keep One Stop Shop handling in its own lane. OSS is optional; if you use a scheme, all supplies covered by that scheme must be declared via the OSS return. OSS returns are additional and do not replace the regular VAT return, and filing cadence differs by scheme: quarterly for Union and non-Union, monthly for import.

- Escalate uncertainty early and keep claims narrow

For complex cross-border cases, consider VAT Cross-border Rulings (CBR) to seek advance VAT treatment. Where multiple companies are involved, one company should file on behalf of the others. Keep coverage claims scoped by market and program, and confirm local treatment with specialist advice before declaring automation complete.

Conclusion#

The practical win here is not more theory. It is a short, enforced set of controls: eligibility, invoice and reporting alignment, and early escalation when the legal basis is unclear.

- Gate eligibility before tax logic runs

Start from the core rule: reverse charge shifts VAT reporting responsibility from seller to buyer. Do not treat that as a blanket EU outcome. Reverse-charge use in the current EU system is not fully generalized, implementation differs by country, and Article 194 (EU VAT Directive) is described as giving member states multiple options. Your first control should therefore block invoicing until transaction type, buyer status, and jurisdiction are validated. If your team cannot point to the local basis, do not automate the treatment.

- Keep invoice treatment and return treatment on the same facts

Where reverse charge applies, the supplier invoices without VAT and the buyer accounts for VAT on its VAT return. Test that link directly. If invoice language, return mapping, and buyer evidence do not match, treat it as a control failure. Keep one evidence chain per legal entity with at least these artifacts: who is responsible for charging and collecting VAT, whether reverse charge was applied, what invoice mention is required, and how the transaction maps to the return.

- Escalate uncertainty early and expand in narrow steps

Precision matters because reverse-charge policy is often framed around fraud-risk contexts, including missing-trader and carousel patterns. Roll out first in your highest-risk, highest-volume corridors, confirm invoice and filing reconciliation for at least one cycle, then expand. Route cases to manual review before go-live when jurisdiction treatment is non-standard, invoice failures repeat, entity data conflicts, or the legal basis cannot be explained clearly. Also avoid reusing the €10 000 figure as a universal trigger. In these materials, that figure appears in a proposed, conditional domestic B2B context and does not operate as a general B2B rule.

If you implement only one next step, make ownership explicit: one owner for eligibility, one for invoice and return alignment, and one for escalation. That structure reduces surprises without adding process you cannot maintain.

If your rollout spans EU and exception-prone markets, contact Gruv to confirm market coverage, compliance gating, and audit-trace expectations before go-live.

Frequently Asked Questions

When can a B2B marketplace apply the reverse charge mechanism?

Confirm the exact legal test for marketplace reverse-charge scenarios with the relevant authority for the jurisdiction in scope. Apply reverse charge only when the specific jurisdiction confirms it for the transaction in scope. For complex cross-border fact patterns, a taxable person can request a VAT Cross Border Ruling (CBR) in a participating EU country where it is VAT-registered.

Who reports VAT under reverse charge in cross-border B2B transactions?

Confirm who reports output tax and input tax in each reverse-charge scenario with the relevant authority for each jurisdiction. Do not apply one reporting rule across all entities and countries without local confirmation. The cited OSS rules are for cross-border B2C e-commerce, and OSS returns are additional and do not replace regular VAT returns.

What must appear on a reverse-charge invoice for EU transactions?

These materials do not provide mandatory EU reverse-charge invoice wording. Keep invoice templates flexible until local invoicing requirements are confirmed in each jurisdiction. If legal basis and invoice text are not aligned, pause changes rather than hard-coding uncertain wording.

When is non-resident VAT registration still required even in B2B?

Do not assume reverse charge removes all non-resident VAT registration exposure. The cited OSS changes from 1 July 2021 relate to cross-border B2C e-commerce, not a direct B2B reverse-charge rule. Separately, the SME cross-border scheme has its own conditions, including the EUR 100 000 Union turnover ceiling, one prior notification in the Member State of establishment, and EX-number confirmation before exemption starts.

How should teams handle Philippines and South Africa in a multi-country setup?

Keep Philippines and South Africa outside EU-only automation logic and route them through country-specific tax review.

What evidence should be retained to defend reverse-charge treatment in an audit?

Retain records that show the transaction facts and the legal basis used for treatment. Where relevant, keep CBR records, since CBR is described as a mechanism for advance rulings on complex cross-border VAT transactions. For SME cross-border use, retain the prior notification, EX-number confirmation, and quarterly reporting trail.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- common.usembassy.gov/wp-content/uploads/sites/124/2023/06/2018-Na...trusted

- consilium.europa.eu/en/policies/vat-reverse-chargetrusted

- sme-vat-rules.ec.europa.eu/sme-scheme/cross-border-sme-scheme_entrusted

- taxation-customs.ec.europa.eu/archives/taxable-persons/vat-cross-border-ru...trusted

- taxation-customs.ec.europa.eu/document/download/12dc566c-9f43-49d9-a306-b7...trusted

- ustr.gov/sites/default/files/2019_National_Trade_Esti...trusted

- vat-one-stop-shop.ec.europa.eu/one-stop-shop_entrusted

- vat-one-stop-shop.ec.europa.eu/index_entrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: