Quick Answer

Start with a send-or-hold rule: do not issue the invoice until customer identity, jurisdiction, and your VAT basis are verified against current HMRC and GOV.UK guidance. Keep UTR, account reactivation status (if relevant), and records such as bank statements or receipts in the same file. When any decisive fact is missing, keep the draft on hold instead of guessing wording, then update only after verification.

Start here and remove VAT guesswork before you send#

Treat this as a send gate, not background reading. It gives you one decision tree and one reusable checklist to help you prepare post-Brexit invoices for UK clients while verifying VAT points before you send.

This guide is for freelancers and small teams. It focuses on services first and treats goods as edge cases. It does not confirm specific post-Brexit VAT invoicing outcomes; verify VAT points against current HMRC and GOV.UK guidance. It covers practical invoicing operations, not custom legal advice for partnerships, complex group structures, or other unusual setups.

Before you start#

Set these basics first:

| Check | What to confirm | Note |

|---|---|---|

| Invoice issuer | Whether the invoice is being issued by a sole trader or a company | A sole trader is the simplest structure to set up and keep records for, but you are personally responsible for business debts; for companies, owners are responsible only up to their financial investment. |

| HMRC filing access | If you file Self Assessment online, your HMRC access is active and your UTR is ready | First-time filers must register before using the online service. |

| Records folder | Create the records folder before sending invoices | Keep records such as bank statements or receipts so you can complete your return correctly. |

| Timing | Filing can start on or after 6 April following the end of the tax year; the example shown uses 5 October 2025 and 31 January | These are not VAT Return deadlines, but missed admin timing can lead to delays and possible penalties. |

- Confirm who is issuing the invoice: sole trader or company. GOV.UK describes a sole trader as the simplest structure to set up and keep records for, but you are personally responsible for business debts. For companies, owners are responsible only up to their financial investment.

- If you file Self Assessment online, make sure your HMRC access is active and your UTR is ready. First-time filers must register before using the online service.

- Create your records folder before sending invoices. HMRC says to keep records such as bank statements or receipts so you can complete your return correctly.

Use HMRC and GOV.UK as your checkpoint. Decide the tax position before you choose invoice wording. Do not start from an old template and work backward. That can lead to reissues, client confusion, and slower approvals.

Verify your own filing readiness. Before you check client-side facts, make sure your own admin is in order. If you use Self Assessment, you can file on or after 6 April following the end of the tax year, and you need your UTR to sign in. If you already have an account and do not reactivate it when required, HMRC says your return may be delayed.

Timing still matters. In the GOV.UK example for the previous tax year, 6 April 2024 to 5 April 2025, you must tell HMRC by 5 October 2025, and the tax bill is due by 31 January. These are not VAT Return deadlines, but they show how missed admin timing can lead to delays and possible penalties.

Keep the scope tight. Use this article for standard operating decisions: service invoices, small-team invoicing, and cross-border checks with clear records. Treat goods, mixed arrangements, and unusual structures as stop points that need separate verification before you send anything.

A finished invoice should pass four checks: the VAT treatment is decided on a verified basis, reissue risk is low, the client has enough clarity to pay, and the file will support later return work.

Apply a pass/fail check before sending. Only send when you can answer, without guessing, who is billing, what records you are keeping, and what HMRC or GOV.UK basis you used for the tax decision. If any answer is unclear, pause and verify first.

That habit prevents avoidable back-and-forth. Once that gate is in place, route the scenario before you draft line items. Related: A Guide to VAT for UK Freelancers.

Map your invoice scenario in 60 seconds#

Use this as a quick routing note, not a tax rule engine. Capture the admin facts first, then finalize wording.

Capture four admin facts before you finalize invoice text.

- Confirm your business structure, because it affects tax and legal responsibilities.

- Confirm whether Self Assessment registration is complete, or whether an existing account needs reactivation.

- Check UTR status if registration follow-up is still pending.

- Confirm records are ready, for example bank statements or receipts, and note any applicable HMRC deadlines.

If any of these are unclear, stop there and mark the case as unconfirmed.

Keep HMRC admin status as a verification gate. This section does not define VAT outcomes. It sets a pre-send control: if registration, reactivation, or records are not verified, keep the invoice in draft.

Use a simple routing table.

| Scenario label | What to record now | Send/hold decision |

|---|---|---|

| First-time filer or new sole trader | Self Assessment registration status and UTR progress | Hold until registration is confirmed |

| Existing filer with inactive account | Whether account reactivation is complete | Hold until reactivation is confirmed |

| Previous tax-year obligation may apply | Whether HMRC was notified by the relevant 5 October deadline | Hold until deadline status is verified |

| Records incomplete | Missing bank statements, receipts, or other return evidence | Hold until records are complete |

Apply a hard stop for unclear cases. Stop and verify if business structure, registration status, deadline status, or records are uncertain. Late notification can lead to penalties, and filing without reactivating an existing account may delay your return. For a step-by-step walkthrough, see How to Invoice a US Client from Mexico as a Temporary Resident.

Gather the minimum compliance pack before drafting#

Build the file before you draft wording. Keep the records you rely on organized so your return can be completed accurately.

Capture the core records first. Before you draft, gather the tax records you will rely on, such as bank statements or receipts. Keep those records together and consistent so you can use them when completing your return.

Add a short internal note. Explain what is confirmed and what is still open. If part of the position is not verified yet, mark it as pending instead of guessing. Keep this note with the tax records you already need to retain so the file is usable later if reviewed.

Verify in order. Confirm whether you need to complete a return for the previous tax year, then confirm your filing setup is active. First-time filers must register for Self Assessment before using online filing, existing accounts may need reactivation, and filing without reactivating an existing account can delay your return. Online filing also requires sign-in details and your UTR.

If you need to complete a return for the previous year, tell HMRC by 5 October and plan for the 31 January payment deadline.

Flag edge cases for manual review. If registration status, account status, or required records are unclear, pause before final wording. Do not force a template answer when the basis is unclear. Keep the draft on hold until that point is verified.

Set VAT treatment before you write line items#

Set a clear decision status before you draft tax lines: either confirmed or on hold. If customer status, jurisdiction, or service classification is unclear, keep the draft on hold and verify before sending.

Specific post-Brexit VAT outcomes are not confirmed here. The goal is to keep confirmed treatment separate from unconfirmed treatment and keep a file that stands up later.

Mark the draft status before you write line items.

- Confirmed: you have enough verified information to document one treatment decision consistently across internal notes and the invoice.

- On hold: one decisive fact is still open, for example customer status, jurisdiction, or service classification.

If you have only an email trading name, or an unverified tax ID from a signature block, pause until those details match your customer records.

Use a decision table so treatment labels never rest on assumptions.

| Draft treatment label | Use only when you have separately verified | Keep in the file | Action if any item is missing |

|---|---|---|---|

| Treatment confirmed | Core customer facts and the treatment basis are verified from appropriate guidance or adviser input | Customer legal name, billing jurisdiction, service description, internal treatment note, retained invoice copy | Hold draft and verify before issuing |

| Treatment on hold | One key fact is still unverified | Open questions list, date of follow-up, internal note, retained draft copy | Keep the invoice unsent until verified |

| HMRC admin readiness checked | You know your filing route and account status for Self Assessment | UTR, reactivation status (if applicable), filing method note | Complete missing admin steps before filing |

| Confirm with accountant or HMRC | You still cannot verify the treatment decision | Copy of the question asked, date sent, reply received, updated treatment note | Keep the invoice unsent until you have an answer |

Keep HMRC admin checks separate from the VAT label. The supported checkpoints here are administrative: registration timing, filing access, account status, and recordkeeping.

Check HMRC filing readiness in parallel. HMRC says you must tell HMRC by 5 October if you need to complete a tax return for the previous year in the listed first-time or reactivation cases. Online filing needs your UTR, filing without reactivating an existing account may delay the return, and some users must use commercial software or other forms. If you are a sole trader and earn more than £1,000 in a tax year, register for Self Assessment. Plan for the 31 January payment deadline.

If classification is uncertain, hold and verify. If you replace a draft, keep the withdrawn version, the replacement, and a short note explaining what changed. Keep records needed to complete your return accurately, for example bank statements or receipts.

Build the invoice with the right fields and wording#

Once key details are confirmed, build the invoice from verified records only. If a fact is still unverified, the draft is not ready to send.

Use a fixed build order so the invoice and your file stay aligned.

| Field | What to enter | Check before send |

|---|---|---|

| Supplier details | Legal trading name and contact details used in your records | Matches the contracting entity |

| Customer details | Customer legal name and billing details from the verified file | Not just a brand name or email signature |

| Service period | Dates or billing period covered | Matches delivered work or agreed milestone |

| Line items | Clear descriptions tied to agreed scope | No vague catch-all labels |

| Total due | Amount due in invoice currency | Arithmetic and staged billing logic checked |

| Due date | Specific agreed date | Matches contract or quote terms |

| Payment instructions | Payee, rail, and reference details | Reference can be matched later in your records |

If the invoice and customer file do not match cleanly on names, dates, scope, and totals, pause before issuing.

Carry invoice details only from verified records. If a key detail is unverified, keep the invoice on hold until your file is complete.

Treat filing prerequisites as internal controls, not assumptions.

- If you are filing for the first time, register for Self Assessment before using the online filing service.

- If you already have an account, reactivate it before filing to reduce the risk of delays.

- Keep your UTR available for online filing.

- Confirm your case can use HMRC's online service, since some cases must use other forms or software.

The control is consistency between your records, your issued invoice, and your filing workflow.

Run a final QA check before sending. The invoice should be traceable later for tax return work and recordkeeping.

- Customer identity and core invoice details match the verification file exactly.

- The invoice copy is stored with the supporting record set.

- The file can be reconciled to records such as bank statements or receipts.

- Filing prerequisites are in place before you submit a return.

Keep this standard high because HMRC recordkeeping expectations still matter when you complete tax returns.

Choose payment terms that protect cashflow and reduce disputes#

Set payment terms as a commercial policy, then document them the same way everywhere. The HMRC and GOV.UK material here supports recordkeeping and filing checkpoints, but it does not prescribe deposit percentages, milestone structures, or late-fee wording for a post-Brexit UK invoice.

Define your terms before you invoice. Put them in the quote, contract, or statement of work, and use the same wording across documents for:

- amount basis

- due date

- any late-payment handling you choose to include

If the signed commercial document and invoice do not match, pause and fix the source document first.

Separate internal policy from VAT rules. If you use stricter terms for higher-risk work, label that clearly as your internal policy. Do not present it as a VAT requirement from the guidance.

Keep each billable line tied to your records. A practical record set is:

- issued invoice copy

- payment evidence, for example bank statements or receipts

- any other documents you rely on when filing your return

This lines up with GOV.UK's expectation that you keep records for tax return work.

Run one final pre-send check. Confirm your record set is complete, your Self Assessment account is active before filing, your UTR is ready for online filing, and your filing route is valid, for example partnerships cannot use the standard online filing service. Keep HMRC deadlines in view, including 5 October 2025 for telling HMRC in the stated first-time/reactivation cases and 31 January for paying the tax bill.

Send through a traceable payment rail and monitor status#

Pick a payment setup you can prove later, not just one that is convenient today. Each receipt should map cleanly to the right invoice and payment record.

Choose a consistent receiving method. Make the payment reference clear on the invoice and use the same receiving method consistently.

Treat this as an operational choice, not an HMRC requirement. The control is whether you can match the payer, amount, date, and reference to one issued invoice without ambiguity.

Track status in one place. Do not rely on inbox memory. A spreadsheet or accounting system is fine if you use clear states consistently, for example sent, due, and paid.

This supports recordkeeping discipline. GOV.UK says you need records such as bank statements or receipts to complete your tax return correctly, and to work out profit or loss once you start trading.

Predefine your failure path. If a payment does not match an invoice in your records, open an investigation note in the same invoice record and capture:

- date identified

- mismatch detail

- who checked the payment evidence

- what you asked the client to confirm

- final resolution

A short written trail is much easier to reconcile and review than scattered messages.

Keep close-cycle support together. At each close cycle, keep the invoice copy, payment evidence, and a status snapshot in one place. Retain enough support to tie receipts back to invoices and to compare your records with your HMRC online view when you check how much you owe or print your tax calculation.

Related reading: How to Conduct a Client Post-Mortem and Gather Feedback.

Handle Great Britain and Northern Ireland differences without rework#

Record whether the client paperwork refers to Great Britain (England, Scotland and Wales) or Northern Ireland before you finalize invoice wording. This guide does not confirm exact VAT treatment differences, so do not treat a single "UK client" label as a final tax decision.

Make billing jurisdiction a required field. If the paperwork only says "UK," pause and confirm the client's legal entity and billing jurisdiction. Also record whether the work is for services, goods, or a mix so your internal review stays consistent.

Keep one layout, but run a final guidance check. Reuse structure and process, not VAT wording copied from old invoices. Before sending, check the latest HMRC and GOV.UK guidance for your specific scenario.

Separate lines where that helps review. If a deal includes mixed or unclear elements, separate invoice lines where that helps your internal review and later reconciliation. Keep the client confirmation, your treatment note, the final invoice, and payment evidence together. GOV.UK expects records such as bank statements or receipts, and this keeps your decision trail in one file.

Treat digital services and B2C edge cases as separate paths#

Treat digital work and B2C edge cases as a separate review path. This section does not establish digital-services VAT outcomes, so keep invoice wording in draft until the facts are confirmed.

| Check | What to record or verify | Article note |

|---|---|---|

| Sale classification | Classify the sale before drafting final wording and record what is confirmed and what is still unclear | If the scope is unclear, keep the invoice in draft and document what still needs to be confirmed. |

| Customer type | Separate business-customer and consumer-customer cases in your file | Do not infer treatment from labels alone; if customer status is uncertain, stop and verify before sending. |

| Legacy VAT terms | Review old templates or emails that may create uncertainty | Pause and confirm current treatment with current guidance or adviser input before finalizing the invoice. |

| Records pack | Build the records pack before sending, including records such as bank statements or receipts | If required records are incomplete, do not finalize the invoice. |

| Filing readiness | If the invoice connects to Self Assessment workflow, keep registration, reactivation, and UTR readiness in view | First-time filers must register before using the online filing service, existing users may need to reactivate an account, and filing uses your UTR. |

Classify the sale before drafting final wording. Record what is confirmed and what is still unclear. If the scope is unclear, keep the invoice in draft and document what still needs to be confirmed.

Separate business-customer and consumer-customer cases in your file. Do not infer treatment from labels alone. If customer status is uncertain, stop and verify before sending.

Treat legacy VAT terms as a re-check trigger. If terms in old templates or emails create uncertainty, pause and confirm current treatment with current guidance or adviser input before finalizing the invoice.

Build the records pack before sending. Keep records such as bank statements or receipts, since GOV.UK says records are needed to complete returns correctly.

If this invoice later connects to Self Assessment workflow, keep filing readiness in view. First-time filers must register before using the online filing service, existing users may need to reactivate an account, and filing uses your UTR. Hard boundary: if required records are incomplete, do not finalize the invoice.

Avoid the mistakes that trigger delayed payment and reissued invoices#

If records need correction, reduce rework first: fix the record and confirm your HMRC admin status before filing. This section focuses on HMRC process controls for records, registration, reactivation, and filing readiness.

Pause filing work when records are incomplete. Verify your core records before doing anything else. HMRC guidance says you'll need to keep records, for example bank statements or receipts, so returns can be completed correctly. Use that as your minimum control before moving forward.

Keep a clear record trail. If you need to correct and resend documents, avoid parallel versions in your working files. Keep related records and correspondence together so the history is easier to follow during later reporting.

Run the HMRC readiness checks before filing season pressure hits. Check whether you need to send a tax return before registering, register for Self Assessment if filing for the first time, reactivate an existing account where required to avoid delays, and confirm your UTR is available for online filing.

Document the root cause and run a monthly control. Track deadline-sensitive admin points in your review cycle, including the 5 October HMRC notification deadline in the stated guidance context, online filing availability on or after 6 April, and the 31 January payment deadline.

| Symptom | Likely cause | Immediate fix | Prevention control (HMRC-aligned) |

|---|---|---|---|

| Return preparation stalls | Supporting records are incomplete | Complete the record set before continuing | Monthly sample check for complete records, for example bank statements or receipts |

| Filing preparation is blocked for a new filer | Self Assessment registration not completed | Register before using the online filing service | Monthly check: confirm whether a return is required, then register early |

| Return processing is delayed | Existing Self Assessment account was not reactivated | Reactivate the account before filing | Pre-filing admin review of account status |

| Penalty risk appears during year-end admin | HMRC notification timing was missed in the guidance context | Notify HMRC as required for your case | Deadline tracker covering 5 October, on or after 6 April filing start, and 31 January payment |

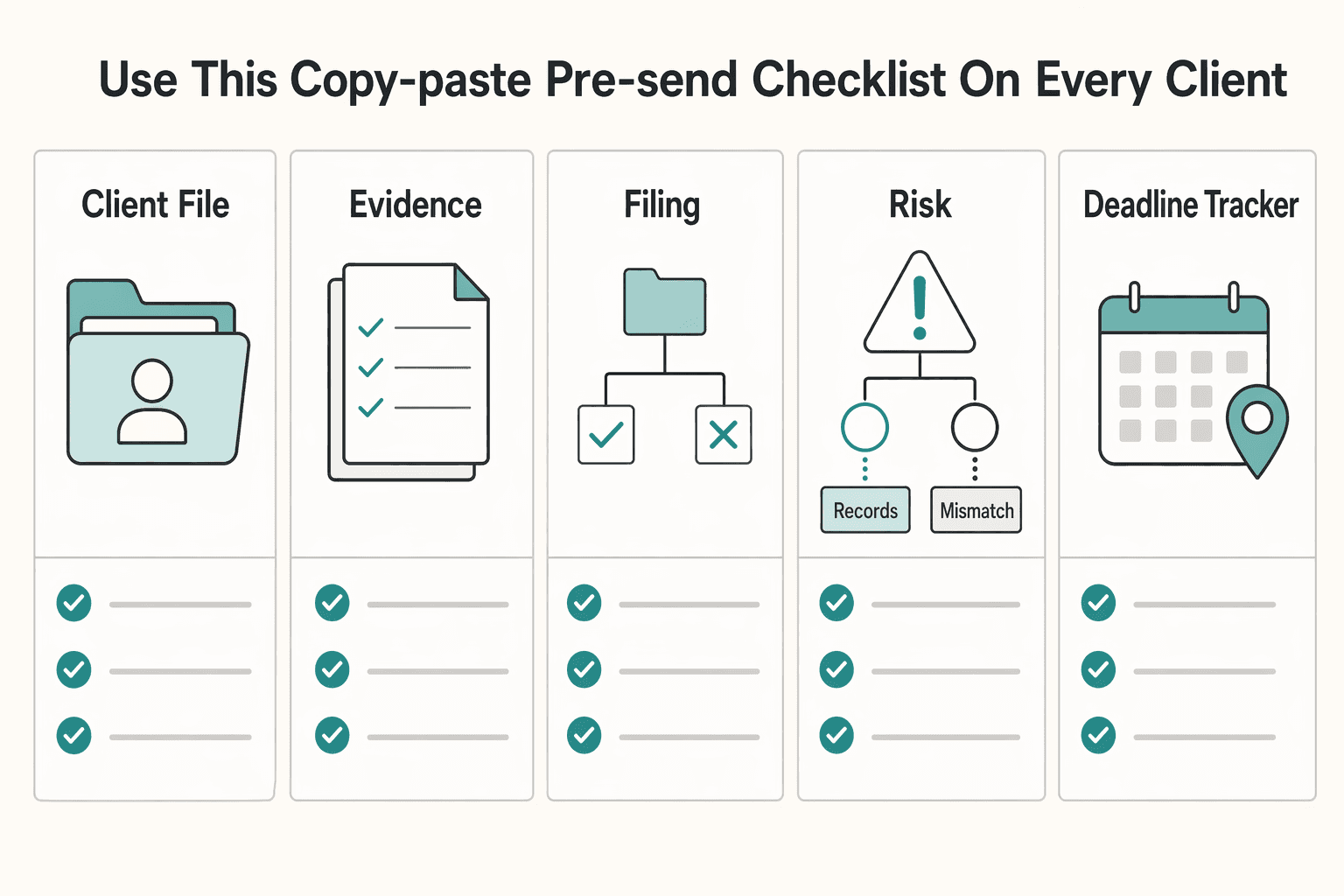

Use this copy-paste pre-send checklist on every client#

Treat this as a send-or-hold gate. If you cannot evidence each point in your file, hold the invoice.

| Check | What the file should show | If missing |

|---|---|---|

| Client file complete | The core client and invoice details you rely on are stored together | Hold the invoice. |

| Record trail complete | Supporting records for return preparation, for example bank statements or receipts | Hold the invoice. |

| Self Assessment admin ready (if relevant) | Your Unique Taxpayer Reference (UTR) is available, and any existing Self Assessment account is reactivated before filing | Hold the invoice. |

| Registration risk checked (if relevant) | If you need to register, have a National Insurance number ready and complete registration on time | Hold the invoice. |

| Filing route confirmed | If your case cannot use the online filing service, use the alternative submission routes HMRC provides | Hold the invoice. |

| Deadline tracker current | Your workflow is aligned to the 5 October notification point and the 31 January payment deadline where they apply | Hold the invoice. |

| VAT treatment handled separately | VAT decisions stay in your specialist VAT process and the rationale is in the file | Hold the invoice. |

- Client file complete: keep the core client and invoice details you rely on stored together.

- Record trail complete: keep supporting records HMRC expects for return preparation, for example bank statements or receipts.

- Self Assessment admin ready (if relevant): your Unique Taxpayer Reference (UTR) is available, and any existing Self Assessment account is reactivated before filing.

- Registration risk checked (if relevant): if you need to register, for example as a sole trader, have a National Insurance number ready and complete registration on time, because late or missed registration may lead to a penalty.

- Filing route confirmed: if your case cannot use the online filing service, use the alternative submission routes HMRC provides.

- Deadline tracker current: HMRC guidance includes a 5 October notification point for telling HMRC you need to complete a return for the previous tax year, in the cited guidance context, and a 31 January payment deadline, so keep your workflow aligned to the periods that apply to you.

- VAT treatment handled separately: this Self Assessment checklist does not confirm VAT invoicing treatment, so keep VAT decisions in your specialist VAT process and do not send when that rationale is missing from the file.

Run your final VAT process check before sending: Use the VAT Reverse Charge Checker.

Final takeaway and next action#

Use the same order every time: decide whether a return is required first, confirm the filing route second, prepare records third, then run the pre-submit checklist. Starting from an old template before those steps can create avoidable rework.

Turn this into a one-page SOP you use before every filing. Keep it short and operational:

- Confirm whether you need to send a tax return before registering.

- Confirm the filing route from current HMRC or GOV.UK guidance: register before first-time online filing, reactivate an existing account before filing, and keep your UTR ready.

- Prepare the records needed to complete the return correctly.

- Run the final checklist before submitting.

Apply a strict hold rule: if key facts are unclear, stop and verify before filing. Build the evidence into the same SOP. Keep the client file, return copy, filing rationale, and supporting records together. HMRC examples include bank statements or receipts for completing returns correctly. Add one last check: if someone else cannot understand the filing decision from the file alone, it is not ready.

Include annual admin checks in the SOP as well. Keep date checks current from GOV.UK each year. This guide shows a 5 October 2025 notification example for that prior year and a 31 January payment date, so do not roll the 2025 date forward unchanged.

Before you scale recurring templates, have a qualified adviser validate the decision points and evidence requirements for complex cases. Also confirm whether the online service applies, since some taxpayers must use commercial software or other forms instead.

If you want cleaner reconciliation for incoming client transfers, review Virtual Accounts.

Frequently Asked Questions

Do I charge VAT when invoicing a UK client after Brexit?

This guide does not support a yes-or-no VAT answer for that scenario. Check current HMRC or GOV.UK VAT guidance, or confirm with a qualified adviser before issuing the invoice. If your file cannot show why you chose the treatment, hold the invoice.

When should I use reverse charge wording on an invoice?

Use it only when you have current support for the exact facts and keep that support with the invoice record. This guide does not establish when reverse charge wording applies. If the support is missing, pause before sending.

What must appear on a post-Brexit invoice to avoid reissue risk?

This section cannot verify exact VAT wording requirements. Keep the invoice aligned with your client file and retain supporting records needed for return preparation, such as bank statements or receipts. Consider keeping corrected-version history and related correspondence together as well.

Do I still need an EC Sales List for services to EU business clients?

This guide does not support an EC Sales List answer for that case. Do not assume an older process is still valid without checking current guidance. If you cannot verify the current position, pause before filing or sending.

How do rules differ between Great Britain and Northern Ireland?

This guide does not provide those VAT differences. Treat jurisdiction as a check item before you reuse a template. Keep your location and treatment rationale in the file.

What changes if I sell digital services to B2C customers in the EU?

This guide does not support the EU VAT treatment for digital B2C sales. Handle that as a separate verification step instead of treating it as a minor variation of a standard service invoice. If customer-location evidence is unclear, stop and resolve it first.

What should I do first if I already sent an invoice with the wrong VAT treatment?

First, preserve the sent invoice, correspondence, and the records behind the original decision. Then confirm the correct treatment from current HMRC VAT guidance or a qualified adviser before issuing any correction, since this section does not support a specific correction method. Keep Self Assessment admin current where relevant: HMRC says to tell them by 5 October when that rule applies, keep your UTR ready, and note that filing without reactivating an existing account may delay the return, with payment due by 31 January where applicable.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

Educational content only. Not legal, tax, or financial advice.

Related Posts

Stop Freelance Profit Margin Erosion Before It Hits Cashflow

Revenue can hold steady while the business underneath it gets weaker. What comes in matters, but what you keep after the work is delivered is the clearer signal of health.

Understanding the UK's Statutory Residence Test (SRT)

Treat SRT like ops, not folklore. You want a repeatable workflow you can run monthly so your tax-year answer is boring, documented, and easy to defend.

VAT for UK Freelancers Without Filing Surprises

If you want a low-stress approach to **vat for uk freelancers**, start with an HMRC-first baseline. Think of compliance as a series of decisions backed by records, not a setting inside your invoicing tool.