Quick Answer

Classify the sale before you write any VAT wording. For a uk ltd invoice eu business vat case, confirm the contracting entity, whether each line is goods or services, and the buyer’s business status, then run a member-state check in TIC. Issue only when invoice fields, your treatment note, and the evidence pack support the same position. If one legal point is still unproven, keep the invoice in draft and escalate through current HMRC guidance or adviser review.

You can invoice EU clients without VAT guesswork if you decide in this order#

You can reduce VAT guesswork by establishing the facts first, then applying the treatment. This guide is for a UK limited company invoicing an EU business client after Brexit. It starts by separating confirmed facts from working assumptions. The goal is practical: choose a supportable VAT treatment, issue a compliant invoice, and know when to pause for current HMRC guidance or adviser input.

First, define the transaction before you touch the VAT box. Confirm what is being supplied, who the contracting entities are, and whether the customer is acting as a business in this transaction. If any of that is unclear, stop and resolve it before you draft invoice wording.

To reduce errors, draft the invoice around who is actually buying this supply, not around who usually pays you. If the contract counterparty, delivery setup, and billing contact do not all point to the same customer entity, resolve that mismatch first.

Next, build an invoice that is defensible, not just payable. As a baseline, include the issue date, sequential number, supplier identity, customer identity, and a clear description of the goods or services. Before sending, make sure those details match your contract and records so your treatment can be reconstructed later if someone reviews it.

Use this checklist as a structure, not as a full post-Brexit VAT authority. The referenced EU invoice report is dated 23 August 1999.

Finally, escalate early when your legal basis is uncertain. If your VAT decision depends on assumptions you cannot document clearly, stop and get current HMRC guidance or adviser input. Keep your records together from day one so the treatment can be explained from documents, not memory.

That matters most when the pressure is commercial. A client asking for a quick invoice is not evidence that your treatment is right. If the tax basis is still only a working assumption, keep the invoice in draft until you test that assumption.

Gather these facts before drafting the invoice#

Do not draft until you have confirmed buyer status and whether an invoice is required for this supply. Under EU rules, invoices are required for most B2B supplies, and for some B2C transactions. If core facts are missing, pause and verify them first.

| Check | What to confirm |

|---|---|

| Invoice requirement | Whether an invoice is required for this supply |

| Supplier entity | Exact legal entity issuing the invoice, its VAT registration status, and the establishment details tracked internally |

| Customer entity | Customer legal name and registered address matching the contract counterparty |

| Supply classification | Whether the supply is goods or services |

| Buyer status | Whether the buyer is a business or non-taxable legal entity for this deal, plus the VAT registration details relied on |

| Evidence pack | Customer legal details, VAT registration details, contract or SOW scope, delivery location, and payment terms |

| Member-state and special-case checks | Member state invoicing provisions in the Tax Information Communication database and local rules if the supply may be exempt financial or insurance services |

Confirm both legal entities for this transaction and record them consistently.

- Record the exact legal entity issuing the invoice, your UK LTD, its VAT registration status, and the establishment details you track internally.

- Record the customer's legal name and registered address, and make sure they match the contract counterparty.

If your sales file uses a trading name, contact name, or group brand that differs from the contract entity, do not carry that mismatch into the invoice unchecked. Clean up the record first so the invoice, contract, and ledger all point to the same parties.

Classify the supply and confirm B2B status before you draft.

- Separate goods and services before drafting, even if the same client buys both.

- Confirm the buyer is a business or non-taxable legal entity for this deal, then capture the VAT registration details you rely on in your file.

Do not let the payment pattern decide the classification. A retained client relationship, monthly billing, or one purchase order does not turn goods into services or services into goods. The classification has to come from what was actually supplied.

Run a pre-send verification check and keep the file together.

- Keep one evidence pack with customer legal details, VAT registration details, contract or SOW scope, delivery location, and payment terms.

- Check member state invoicing provisions in the Tax Information Communication database before issuing the invoice.

- If the supply may be exempt financial or insurance services, pause and verify local rules. EU-level guidance includes cases where no invoice is required for services supplied in another EU Member State, while Member States may still require an invoice when supplied in their own territory or outside the EU.

A useful test is whether someone else in your business could pick up the file and explain the basic VAT position without asking you what happened. If the answer is no, your pre-send file is probably still too thin.

Classify the sale correctly before you touch VAT fields#

Treat VAT fields as the last step, not the first. Put the transaction into a provisional category, keep tax treatment pending, and only finalize once your records and checks support the choice.

Most problems start with structure. If key facts are unclear, invoice wording, VAT shown, and return handling can all drift out of sync.

Build a provisional worksheet and treat it as a sorting tool, not a VAT answer.

| Provisional check | Facts to confirm before finalizing | Keep pending until verified |

|---|---|---|

| What is being supplied | Scope of work or goods, customer legal entity, destination context | Invoice wording, whether UK VAT appears, VAT Return handling |

| What evidence is on file | Contract or SOW, customer details, and supporting records | Final treatment decision |

| What still needs confirmation | Any unresolved rule or filing point from official guidance | Final invoice release |

If you cannot classify the transaction confidently, do not issue a final invoice. The point of the worksheet is to slow down the moment where people usually guess. A provisional category gives your team a shared starting point, but it does not settle treatment by itself. Mark it as pending until the file supports the result.

Once you have a provisional category, verify before release. If key rule details are still unclear, use official guidance, your records, or a qualified adviser before finalizing.

Do not rely on informal signals. Keep the customer legal details and contract or SOW together so the file supports your decision. Good record-keeping is part of getting the return right later.

If one key point is still unresolved, keep the whole decision unresolved. It is better to hold a draft invoice for one more check than to issue it, post it, and then unwind the wording and ledger treatment later.

Before release, settle three outputs and make sure they agree.

- Invoice wording that matches your verified position.

- A clear decision on whether UK VAT appears.

- A short internal note on expected VAT Return handling.

If any of those is still unclear, keep the invoice in draft. The internal note does not need to be long. It only needs to record the path you followed clearly enough that the same result can be defended later without recreating the whole decision from memory.

Use a hard stop when classification is unclear. If classification is uncertain, pause and verify through official guidance, your records, or a qualified adviser before sending a final invoice.

Separately, keep HMRC basics on track: register for Self Assessment before first-time online filing, reactivate an existing account before filing if needed, keep records, have your UTR available for filing, and meet the relevant HMRC deadlines for notification and payment. Related: Understanding the UK's Statutory Residence Test (SRT).

If your provisional category is clear but final wording is still uncertain, run a quick pre-send check with the VAT reverse charge checker.

Apply the services path for UK to EU B2B work#

For UK-to-EU B2B services, do not let the client's country drive the answer by itself. Set invoice wording only after you have documented the invoice rule path and checked any member-state invoice requirements.

Start with the EU baseline, then check member-state specifics. Record the baseline EU invoicing position first, then confirm whether member-state provisions change what must appear on the invoice.

Treat it as a sequence, not two parallel thoughts. Start with the base rule path, record it, then test member-state provisions before final wording. If you skip straight to wording because the client says they usually receive a certain invoice format, you lose the audit trail for why this invoice was treated that way.

Build an evidence file that shows how you reached the result. Keep the contract or SOW, customer legal entity details, and business-status evidence together so a reviewer can follow what was supplied, to whom, and how you decided the invoice treatment.

At minimum, the file should let a reviewer answer three basic questions quickly: what the service was, who bought it, and what evidence you used to support the customer status for this transaction. If those answers sit in different systems, pull them together before issue.

Draft from the verified treatment, not from a recycled template. Under EU rules, invoices are required for most B2B supplies, and national rules may still add invoice-specific requirements.

Before sending, check the Tax Information Communication database for the customer's member-state provisions. Add invoice wording only when your verified treatment supports it.

A recycled template is risky because it often carries forward old wording that was right for a different client or a different supply. Review the service description line by line and make sure it still matches the contract scope you are actually billing.

Save a short plain-language rationale note with the invoice. Include:

- which EU and member-state invoicing rules you tested

- the customer status and evidence you relied on

- why that invoice treatment was selected

If the service falls into an exempt financial or insurance category, document with extra care. EU rules include no-invoice cases for services supplied in another EU Member State, including contexts tied to Article 135(1)(a)-(g). Member-state exceptions can still apply, including contexts tied to Article 135(1)(h)-(l).

A plain-language note helps when someone outside the tax team has to review the file later. It should read like a brief explanation of the decision, not copied legislation. If the wording is so compressed that only the original preparer understands it, expand it while the facts are still fresh.

Apply the goods path without mixing it with services logic#

For physical goods, do not borrow the services logic from the previous section. Start with what moved, the shipment trail, and the customs record, then build the invoice treatment from that file.

| Goods file item | What to keep |

|---|---|

| Shipment and delivery facts | What left, where it started, and where it was delivered |

| Customer record | Customer legal entity details |

| Customs paperwork | Paperwork tied to the movement, if applicable |

| Import-side responsibility | Internal notes on who handles import-side costs and filings |

| Bookkeeping support | Records such as bank statements or receipts |

First, confirm that this is a goods transaction before drafting the invoice. If something physical crosses a border, treat it as goods and document it from shipment facts, not from a reused services template.

Use this quick check. If your file only has a proposal, a generic invoice draft, and a VAT number, it is not complete enough for a goods decision.

For goods, the file should tell the movement story. You should be able to see what left, where it started, where it was delivered, and what documents tie that movement back to the customer and invoice.

Match the invoice to the import and customs reality before you send it. Verify UK VAT display requirements, import VAT handling, and EORI obligations against current HMRC guidance before finalizing.

Keep one working file with:

- shipping and delivery facts

- customer legal entity details

- customs paperwork tied to the movement, if applicable

- internal notes on who handles import-side costs and filings

- bookkeeping records, for example bank statements or receipts

Do not leave customs paperwork sitting separately from the sales record. If the invoice says one thing and the shipment or customs entry shows something else, fix the mismatch before the invoice goes out, not when you are already reconciling the period.

Treat import-side documents as core accounting records. Confirm the correct treatment for import VAT documents with your accountant or HMRC before filing.

The key control here is traceability. A reviewer should be able to follow the shipment, invoice, customs entry, and payment from start to finish.

That traceability should work in both directions. Starting from the invoice, you should be able to find the shipment and customs evidence. Starting from the customs record, you should be able to find the matching invoice and ledger entry. If either direction fails, the file needs work.

If the same client buys goods and services, keep the documentation clear and verify treatment before issue. Confirm how each part should be handled before sending the final invoice.

If any goods-specific point is unclear, pause and verify before issuing the final invoice. The practical failure mode here is combining everything into one vague commercial description. Once that happens, it becomes harder to prove which part of the invoice relates to physical movement and which part relates to service work around it. Keep those records clean from the start.

Build an invoice that can survive review in any EU member state#

Draft for review, not convenience. Your invoice should make the VAT logic clear and stay consistent with the transaction file behind it.

| Treatment note case | What to do before issue |

|---|---|

| Reverse charge | If classification points to reverse charge, consider including a reverse-charge note, then verify any required wording against current official guidance before issuing |

| UK VAT is not shown | State the treatment basis clearly rather than leaving the tax position blank |

| Exemption or other special treatment | Verify current notation requirements before sending |

Start from your classified transaction and evidence file, not an old template. The legal backdrop is VAT Directive 2006/112; check current HMRC guidance for a definitive 2026 invoice-field checklist before finalizing.

Treat the referenced reverse-charge material as context only. It is a November 2014 study report. It says its views do not necessarily reflect the European Commission's official opinion, and it states that the Commission does not guarantee the data's accuracy.

That means your draft should be built around verified current checks, not around historic invoice language someone saved in a shared folder. Historic wording can be useful as a comparison point, but not as authority.

Write the VAT treatment note so a third party can follow your logic without guessing.

- If your classification points to reverse charge, consider including a reverse-charge note, then verify any required wording against current official guidance before issuing.

- If UK VAT is not shown, state the treatment basis clearly rather than leaving the tax position blank.

- If you rely on an exemption or other special treatment, verify current notation requirements with official guidance before sending.

Aim for wording that explains the position without overclaiming. The invoice should not imply certainty that your records do not support, but it also should not leave the customer or a reviewer guessing why the tax line looks the way it does.

Run one live check against current official material relevant to the invoice before issuing. Do not rely on historic summaries.

That matters because reverse-charge provisions under Articles 199, 199a, 394, and 395 may be relevant. Confirm current invoice content requirements against up-to-date official guidance rather than relying solely on older study documents.

A live check is also a discipline tool. It forces you to confirm that the wording you are about to use still fits the jurisdiction context you are billing into, rather than assuming that last quarter's answer still applies unchanged.

Do a final consistency pass against your evidence pack before issuing the invoice.

Confirm that the legal entities match your records, the line descriptions match the classified transaction, and the VAT note matches your documented rationale. If any part is unclear, pause and verify before sending.

This last pass should be mechanical. Compare the invoice against the contract, the customer record, and the treatment note one item at a time. Fast reviews tend to miss small identity or wording mismatches that later create outsized questions.

Related reading: How a UK Creative Director Should Invoice a US Client from their LTD Company to Optimize for Taxes.

Separate invoice content from filing obligations#

Treat the invoice as one part of compliance, not the whole job. For most B2B supplies, an invoice is required, but additional checks can still sit outside the invoice itself.

Separate what belongs on the invoice from what has to be checked or administered later.

| What appears on invoice | What must be checked or administered later |

|---|---|

| The invoice for the B2B supply (paper or electronic) | Confirm member-state-specific invoicing provisions in the Tax Information Communication database (TIC) before finalizing your workflow |

| Clear transaction information under your applicable invoicing rules | Verify whether national rules add requirements beyond the EU baseline |

| Final invoice file sent to the customer | Keep invoices stored in a retrievable format and location |

If information helps the customer understand the charge, keep it on the invoice. If it exists for follow-through checks, keep it in your records and process.

A common mistake is treating EU-level guidance as the full rule set. The invoice should explain the billed transaction clearly, while your process handles country-specific checks that apply outside invoice wording.

Map the invoice to later obligations, but do not infer all compliance outcomes from invoice wording alone. Run a live check in TIC for the member state involved, then handle country-specific checks separately.

Use the EU baseline as a starting point, then verify member-state invoice specifics in the Tax Information Communication database. EU-wide rules exist, but national rules can still apply in some areas.

In practice, this means your period-end review should revisit the member-state check, the issued invoice, and the stored records together. If those items no longer align, correct the record before filing rather than after.

Keep one audit folder per client with the invoicing decision trail. Include the issued invoice and the notes used to confirm applicable member-state invoicing rules. The goal is quick retrieval, not extra formatting.

Electronic invoices are equivalent to paper invoices, and storage is generally flexible in format and location. Choose the setup that lets you retrieve records quickly.

The folder works best when it is predictable. Store the same document types in the same order each time so a reviewer can find key records quickly.

If you use invoicing, payment, or marketplace platforms, keep traceable records that reconcile to your ledger. Preserve the invoice file plus exports that can be matched back to the same transaction.

Before filing, reconcile material transactions so invoice records and ledger records align. If core details do not match, fix that before reporting.

Where possible, attach reconciliation evidence to the same client file. That reduces the risk that the invoice looks complete on its own while the underlying record trail says something else.

Handle reverse charge carefully where it is actually applicable#

Use reverse-charge wording only when your classification and checked guidance clearly support it. If support is unclear, pause the invoice and escalate to a qualified adviser before proceeding.

Tie your wording to your classification note and keep records aligned. The available HMRC excerpts stress keeping records so returns can be completed correctly, so keep your note and draft invoice consistent before issue.

Run a final consistency check on the draft invoice and your internal note. If the treatment in one place does not match the other, fix it before sending.

This is where small copy-and-paste errors matter. If one part of the file says one treatment and another says something else, treat that as unresolved and pause for review.

Once the wording is validated for the scenario, keep the format consistent. Changing statement style between similar invoices can make later checks harder.

Keep the language clear and repeatable so later reviews stay straightforward. When similar cases are described in noticeably different ways, it becomes harder to tell whether the treatment changed for a real reason or only because a different person prepared the invoice.

Use a hard stop when sources conflict or are incomplete. If official guidance, customer instructions, and prior treatment point in different directions, do not guess the wording.

Escalate before issuing, and keep a small evidence pack with the classification note, draft invoice, and the guidance you relied on. Uncertain wording is a pause signal, not an editing task.

That small evidence pack should be enough for the reviewer to understand the conflict quickly. The goal is not a long memo. It is a concise file that shows the facts, the draft position, and the point that still needs confirmation. For a step-by-step walkthrough, see How a US graphic designer should handle VAT when invoicing multiple EU clients.

Fix common VAT mistakes fast#

Errors here can start with a decision mismatch, not just a formatting problem. Fix the decision first, then make the invoice, internal note, and ledger entry reflect that same decision.

Stop repeat errors before you correct any single invoice. If your current treatment is not clearly supported by the facts and current GOV.UK guidance, pause and escalate instead of guessing.

Use one consistency check before issuing anything: customer record, internal classification note, invoice text, and ledger tax code should all tell the same story. If they do not, fix that first and keep the original and corrected records together.

When you correct an invoice, also check whether the same reasoning error affected other invoices built from the same template or workflow. Fixing one document may not be enough if the underlying process still points the team toward the wrong result.

Do not force one treatment across every line when a job includes different supply types. Split the line items and review each one against its own supporting documents.

The checkpoint is simple: map each line back to a contract, statement of work, or order detail. If that mapping is unclear, pause and rebuild it before reissuing.

This is one place where teams can save time in the moment and create extra work later. A cleaner reissue often starts by rebuilding line support properly, not by trying to edit one mixed-description invoice into compliance.

Rebuild your evidence pack if you cannot explain the treatment decision. Keep it in company records, since a limited company is legally separate from its owners.

A practical pack can include:

- signed commercial documents, such as the contract, proposal, or scope

- customer legal details used on the invoice

- the issued invoice and any correction record

- ledger entries and supporting records, for example bank statements or receipts

- filing notes that explain what was reported and why

If you are correcting after issue, add a brief note explaining what changed and what triggered the correction. That keeps the file intelligible later, especially when the original invoice and replacement invoice both remain in the record set.

Treat old assumptions as untrusted until they are rechecked against current facts and current GOV.UK guidance. Reusing past treatment without revalidation can repeat the same mistake.

If you are also fixing related filing records, recheck core HMRC process points early. First-time filers must register for Self Assessment before using the online filing service. Previously registered users may need account reactivation, and filing without reactivating an existing account may delay the return. Missed HMRC notification deadlines can trigger penalties.

The broader lesson is simple. Historical practice is useful background, not proof. Use it to identify what needs review, not to skip the review.

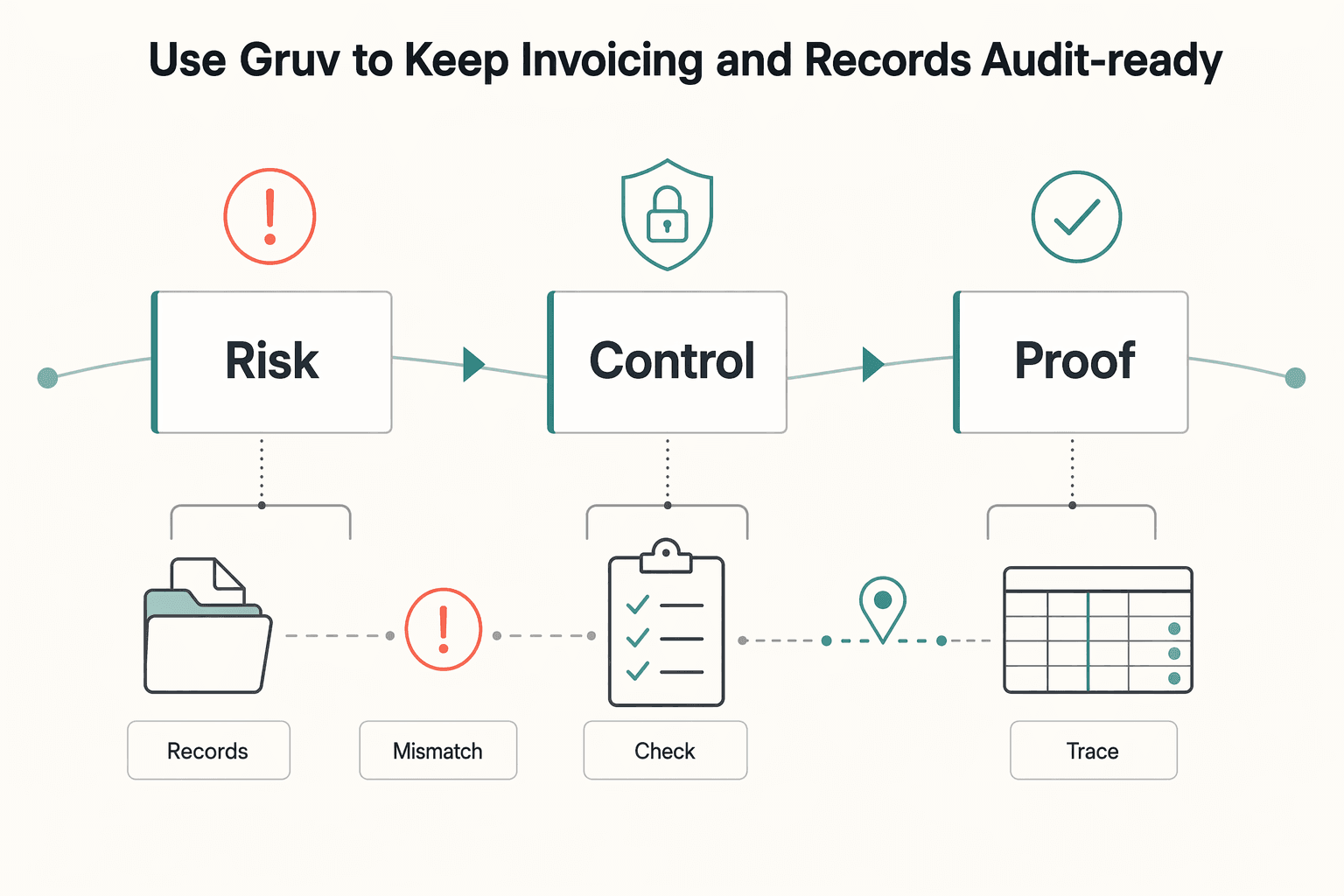

Use Gruv to keep invoicing and records audit-ready#

Use Gruv as your control and record layer, not as the tool that decides tax treatment. For a limited company, the practical goal is a traceable file where the invoice, payment evidence, and accounting treatment all support the same decision.

Keep one continuous transaction trail from invoice issue to payment to ledger entry. Tie it to the same record and internal treatment note. At a minimum, the invoice, payment evidence, and accounting entry should all match one transaction and one rationale.

HMRC expects records such as bank statements or receipts so returns can be completed correctly. If your filing or account tools show prior returns or status history, use that as an internal traceability check, but do not treat timeline visibility alone as proof of compliance.

A good control here is to make sure the person reviewing the ledger can access the invoice and payment evidence from the same transaction file. The easier that path is, the more likely your team will actually follow it.

Verify what is actually enabled in your setup before you rely on it at month end or in filing work. For any process you plan to use, test one real case and keep that output with your period-close records.

The pass or fail test is simple: exported data should match the invoice record and ledger entry without manual rekeying. If it does not, fix the process before filing.

If a platform field is optional, treat that as a control risk until you decide how your team will handle it. Optional data often becomes missing data under deadline pressure, and that is usually where the audit trail starts to thin out.

When treatment is uncertain, require a review gate and document the exception before relying on the final record. Keep a short note on what is unclear, who reviewed it, what was issued, and what still needs checking against current GOV.UK guidance or professional advice.

Apply the same boundary logic HMRC uses online. Some cases fall outside service scope and need commercial software or other forms. If your process does not clearly support the case, pause, document it, and resolve it outside the platform first.

The practical value of that review gate is consistency. It stops edge cases from being forced through a normal workflow that was only built for straightforward invoices.

Copy-paste closing checklist for your next EU invoice#

Do not send the invoice until every checkpoint below is complete.

- Confirm the lane first.

Record the core facts in one place: relevant EU Member State, goods or services, and B2B status. If those facts are split across tools or still unclear, pause and complete the file before issuing.

- Apply the rule set you actually checked.

Decide treatment only after checking the EU-wide VAT invoicing basics and any member-state-specific provisions that apply. Do not assume one template fits every case. If rules conflict or remain unclear, pause and get professional advice before issuing.

- Build the invoice to the verified rule set.

For most B2B supplies, an invoice is generally required, but EU invoicing has both EU-wide basics and member-state-specific rules in some areas. Before sending, check the member-state provisions in the Tax Information Communication database (TIC), and if issuing electronically, confirm the recipient accepts electronic invoices.

- Store evidence with the invoice, then complete follow-through.

Keep the final invoice, treatment note, and supporting commercial documents together so your records stay aligned. After sending, keep a clear record of what you issued and why so reconciliation is traceable later.

- Escalate early on edge cases.

If classification is uncertain, facts are mixed, or the outcome is still unclear after your checks, stop and escalate before billing. Also flag specialist financial or insurance scenarios for review, since some exempt financial or insurance services supplied in another EU Member State may not require an invoice, including scenarios referenced in Article 135(1)(a)-(g) and Article 135(1)(h)-(l).

If you want a compliance-first workflow with traceable invoice and payout records where supported, review the Gruv docs.

Frequently Asked Questions

Do I charge UK VAT when my UK LTD invoices an EU business client?

Treat the VAT position as unconfirmed until you verify it against current HMRC guidance for your exact transaction facts before issuing the invoice.

Is reverse charge still relevant after Brexit?

Do not add reverse-charge wording by default. Confirm whether reverse charge applies, when it applies, and what wording is required against your checked scenario before issuing the invoice.

Do I still need an EC Sales List for UK to EU services?

This guide does not state the current EC Sales List position for UK-to-EU services. Treat this as a separate reporting check and document what HMRC guidance or professional advice you relied on.

What must be on a UK invoice to an EU business?

Before sending, confirm the required VAT invoice fields for this case with current HMRC guidance. Make sure the invoice, accounting entry, and supporting records all reflect the same treatment and explanation, including records such as bank statements or receipts.

Can I invoice an EU client in euros?

Invoice currency and VAT treatment are separate questions. Verify euro invoicing rules and tax handling for your specific VAT scenario against current HMRC guidance before issuing.

What changes if my business is in Northern Ireland instead of Great Britain?

The VAT differences for businesses in Northern Ireland versus Great Britain in this EU invoicing scenario require separate verification. Settle the correct path before issuing the invoice so you do not have to unwind invoice and reporting decisions later.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Understanding the UK's Statutory Residence Test (SRT)

Treat SRT like ops, not folklore. You want a repeatable workflow you can run monthly so your tax-year answer is boring, documented, and easy to defend.

How to Invoice a UK Client Post-Brexit Without VAT Rework

Treat this as a send gate, not background reading. It gives you one decision tree and one reusable checklist to help you prepare post-Brexit invoices for UK clients while verifying VAT points before you send.