Quick Answer

Use form routing and payout holds as the first control. In tax withholding international contractors w-8 operations, collect W-8BEN only for foreign individuals, route entities to W-8BEN-E, and send intermediary or personal-services cases to W-8IMY or Form 8233 review. Approve any treaty reduction only after claim fields and profile facts match, then release funds only when reviewer notes, owner identity, and timestamped decisions are complete.

How to decide which W-8 form applies#

Form W-8BEN is not an IRS filing. The payee gives it to the withholding agent, or payor of the income, and does not send it to the IRS. Treat it as a release control in payer workflows, not a box-checking step.

This article focuses on the decisions payer teams actually own: choosing the correct form path, assessing whether a treaty claim is supportable, deciding when payout setup should pause, recording the evidence behind the decision, and escalating when facts are unclear. A few fundamentals set the baseline:

- Form W-8BEN is for individuals.

- Entities use Form W-8BEN-E.

- Treaty benefits can provide an exemption from, or reduced rate of, withholding for certain income items.

- If the payor knows treaty eligibility is invalid, the treaty rate must not be applied.

- For treaty-claim workflow, income not earned from personal services points to Form W-8BEN, while income earned from personal services points to Form 8233.

That makes payee classification your first high-value check before you configure form collection. If your records indicate an entity, an individual W-8BEN should not satisfy onboarding. If submitted forms conflict with known account facts, treat that as a payout hold and route it for review.

Intake errors create real exposure. IRS requester instructions warn that if a valid W-8 or W-9 is not obtained and withholding fails, the withholding agent may be assessed tax at 30% under chapter 3 or 4, or 24% backup withholding under section 3406. The practical response is consistent gating. If status, form type, or treaty position does not align, stop, document, and escalate before release.

Publication 515 is written for withholding agents paying foreign persons, and that is the operating lens here. This article does not provide country-by-country treaty outcomes or legal advice. Where facts are ambiguous, preserve evidence, keep the payout decision pending, and escalate to specialist review.

Build the right mental model before collecting any form#

Start from the right premise: W-8BEN is evidence for a withholding decision, not paperwork for its own sake. A foreign individual gives it to the payer, acting as the withholding agent, so your team can decide withholding and reporting before funds are released.

What the form is really for#

Treat W-8BEN as decision evidence, not as a filing receipt. The form goes to the withholding agent or payer, not the IRS, so your control should show who received it, when a reviewer checked it, and which payout decision it supported. We recommend making that trail visible in your release workflow. Without that trail, you have stored paperwork, not an operational compliance control.

One failure mode is handling W-8BEN as a one-time onboarding attachment. A team may accept a signed form, release funds, and only later find that payee type, income type, or treaty position did not match account facts.

Foreign status is not the same as treaty relief#

Foreign-status certification and treaty-rate eligibility are separate checks. A payee can certify foreign status on W-8BEN even if they are not claiming a reduced rate or exemption under a treaty.

| Concept | What it means | Operational note |

|---|---|---|

| Foreign-status certification | A payee can certify foreign status on W-8BEN even when they are not claiming a reduced rate or exemption under a treaty | Separate from treaty-rate eligibility |

| Treaty-rate eligibility | Reduced withholding depends on additional conditions, including TIN requirements in some cases | Do not rely on signature alone |

| Beneficial owner status | Matters to treaty claims | Does not establish treaty eligibility on its own |

Beneficial owner status matters to treaty claims, but it does not establish treaty eligibility on its own. If a treaty rate is claimed, do not rely on signature alone. Reduced withholding depends on additional conditions, including TIN requirements in some cases.

One control inside a bigger withholding decision#

W-8 documentation sits inside broader U.S. withholding and reporting obligations. Do not treat form collection as a substitute for the withholding determination itself.

If documentation is missing, inconsistent, or not reliable, pause release, document the issue, and resolve status before payment. That same mindset carries into the next step: choosing the right form path before payout setup begins.

Related: Cross-Border Invoicing: How to Handle VAT GST and Withholding Tax on International Invoices.

Choose the correct W-8 path before payout setup#

Choose the form before activation, not after payouts start. If payee type or claim type is unclear, pause activation and route to specialist review instead of defaulting to Form W-8BEN. We recommend treating that fork as your activation gate, not a cleanup task for later.

The routing logic is simple: first identify who the payee is, then identify what they are claiming. IRS form instructions split W-8BEN to individuals and W-8BEN-E to entities, so a wrong first fork creates downstream withholding and reporting risk.

Use this decision tree first#

Start with two checks: is the payee a U.S. person, and if not, what claim is being made? Before you accept any form, confirm your account record matches both the selected payee type and claim type.

- U.S. person (including resident alien): use Form W-9. This is the TIN request path for U.S.-person information reporting.

- Foreign individual beneficial owner: use Form W-8BEN. It is for individuals and can apply whether or not a treaty rate is claimed.

- Foreign entity beneficial owner: use Form W-8BEN-E. This is the entity path for chapter 3 and chapter 4 status documentation.

- Foreign person claiming income is effectively connected with a U.S. trade or business: use Form W-8ECI. This is a distinct claim path, not a BEN or BEN-E substitute.

- Foreign intermediary, foreign flow-through entity, or certain U.S. branch: use Form W-8IMY.

- Foreign government or other eligible foreign organization claiming special withholding treatment: use Form W-8EXP.

- Nonresident alien individual claiming exemption on compensation for independent personal services: assess Form 8233. It is provided to the withholding agent for that exemption claim.

| Form | Who uses it | What claim it supports | Common misroute | When to escalate |

|---|---|---|---|---|

| W-8BEN | Foreign individuals | Foreign status, and possibly treaty benefits | Used for a foreign entity | If beneficial-owner individual status is unclear |

| W-8BEN-E | Foreign entities | Entity status for chapter 3/chapter 4 | Routed to an individual payee | If entity classification or role is unclear |

| W-8ECI | Foreign beneficial owner | Income is effectively connected with a U.S. trade or business | Treated as routine BEN or BEN-E intake | If ECI is claimed but account facts do not clearly support it |

| W-8IMY | Foreign intermediaries, foreign flow-through entities, certain U.S. branches | Intermediary or flow-through documentation; may establish foreign status for sections 1441, 1442, and 1446 | Forced into BEN or BEN-E for speed | Always escalate when intermediary role is not clear |

| W-8EXP | Foreign governments and certain foreign organizations | Reduced rate or exemption from withholding for specified categories | Sent to ordinary commercial entities | If eligibility category is not clearly established |

| W-9 | U.S. person, including resident alien | Correct TIN for information reporting | Requested from foreign payees | If U.S.-person status conflicts with residency or entity facts |

Where teams get tripped up#

A common rework point is W-8BEN vs W-8BEN-E. The deciding fact is whether the legal payee is an individual or an entity, not who handles the account.

Another decision point is BEN or BEN-E vs W-8ECI. W-8ECI is for an effectively connected income claim, not a general foreign-status form.

Form 8233 has a narrower use case. It is for nonresident alien individual personal-services exemption claims and does not replace W-8BEN or W-8BEN-E as a universal form.

The operator rule that saves rework#

Use IRS W-8 requester guidance as the routing baseline, and stop when the facts stop being clear. If intermediary, flow-through, certain U.S. branch, or ECI elements appear, require specialist review notes before activation.

Do not use a collect-any-W-8-and-activate approach. Accept only the form variant that matches both the payee's status and the claim it is designed to support.

Decide whether a treaty claim is operationally supportable#

Approve treaty relief only when the reduced-rate claim is complete, consistent, and not contradicted by facts you already hold as the withholding agent. A valid W-8 can establish foreign status, but treaty relief is a separate step, and your team should rely on it only when the treaty claim itself is supportable.

That distinction matters operationally. Form W-8 is given to the payer or withholding agent, and treaty treatment applies only if the claim is properly made and eligible. If payer-side information indicates ineligibility, do not apply the treaty rate.

What an operationally supportable treaty claim looks like#

At minimum, the payee must represent residency in a treaty country, and the form must be complete for the claim being made. If required reduced-rate information is missing, inconsistent, or conflicts with the payee profile, treat the treaty claim as unreliable even if the foreign-status certification may still be usable. We recommend checking that against your payer-side profile, not just the signed form.

For individuals, run a Publication 519 conflict check before you approve. If your records suggest resident-alien treatment, dual-resident complexity, or another status conflict, stop auto-approval and escalate.

| Review point | Approve when | Escalate when |

|---|---|---|

| Documentation sufficiency | Treaty-relevant fields are complete and include what is needed to establish reduced-rate entitlement | The form is incomplete for the claim or lacks information needed for reduced-rate entitlement |

| Consistency with payee profile | Legal name, country, payee type, and claimed status align with account records and selected W-8 path | The W-8 information conflicts with the payee profile or prior records |

| Publication 519 conflict check | Nothing in your file suggests resident-alien treatment | Facts point to resident-alien treatment, dual-resident complexity, or another status conflict |

When to require deeper review#

Use a clear internal rule: escalate unusual or contradictory treaty positions for specialist review before you release payout at a reduced rate. We recommend keeping that stop rule in your reviewer playbook when facts are hard to reconcile.

Treat Form 8833 as an escalation signal. Treaty-based return positions that reduce U.S. tax are generally disclosed on Form 8833 attached to the return, and failure to disclose can carry a stated penalty of $1,000 ($10,000 for a C corporation). You do not file this as payer, but potential disclosure obligations should trigger documented reviewer notes on why the treaty claim was or was not relied on.

What remains unknown without country-specific analysis#

A clean W-8 alone does not determine the final withholding outcome. You still need country-specific treaty article and income-type analysis, plus any applicable limitation on benefits review, before stating that a reduced treaty rate is available.

Keep that discipline in operations. If the claim does not pass completeness, consistency, and Publication 519 conflict checks, do not auto-approve treaty relief. Once that standard is clear, you can define the minimum intake package needed to support it.

Related reading: Tax Residency in Ireland for Digital Nomads and Tech Contractors.

Define the minimum intake package for onboarding#

Set an internal release gate: the payee is not payout-eligible until the intake package is complete, validated, and tied to a documented payer-side decision. At minimum, link these four artifacts to the payee record:

- Selected form path: Form W-8BEN for an individual, Form W-8BEN-E for an entity, or the correct exception lane when facts call for Form W-8IMY or Form 8233.

- Payee legal identity record from onboarding, so form data can be matched to the account.

- Beneficial-owner representation on the form, checked against the payee type on file.

- Payer-side decision outcome, approved, rejected, or escalated, with decision owner and timestamp.

This record needs to stand on its own because Forms W-8 are kept in withholding-agent records and are not sent to the IRS by default.

Validate fields, not just uploads#

Treat upload-only as incomplete. Validate required fields against the selected form instructions before payable status is allowed.

For Form W-8BEN, confirm the beneficial owner name, country of citizenship, and permanent residence address are present and consistent with the payee profile. Because the form includes a penalties-of-perjury certification, an unsigned or uncertified form is incomplete.

For Form W-8BEN-E, validate Part I identity fields and enforce chapter 3 status selection logic with one entity-type box. If classification is missing, unclear, or contradictory, stop payable activation. Block these routing errors early:

- Treating all foreign payees as W-8BEN. W-8BEN is for individuals, while entities use W-8BEN-E.

- Keeping intermediary or flow-through fact patterns on the wrong lane instead of routing to W-8IMY.

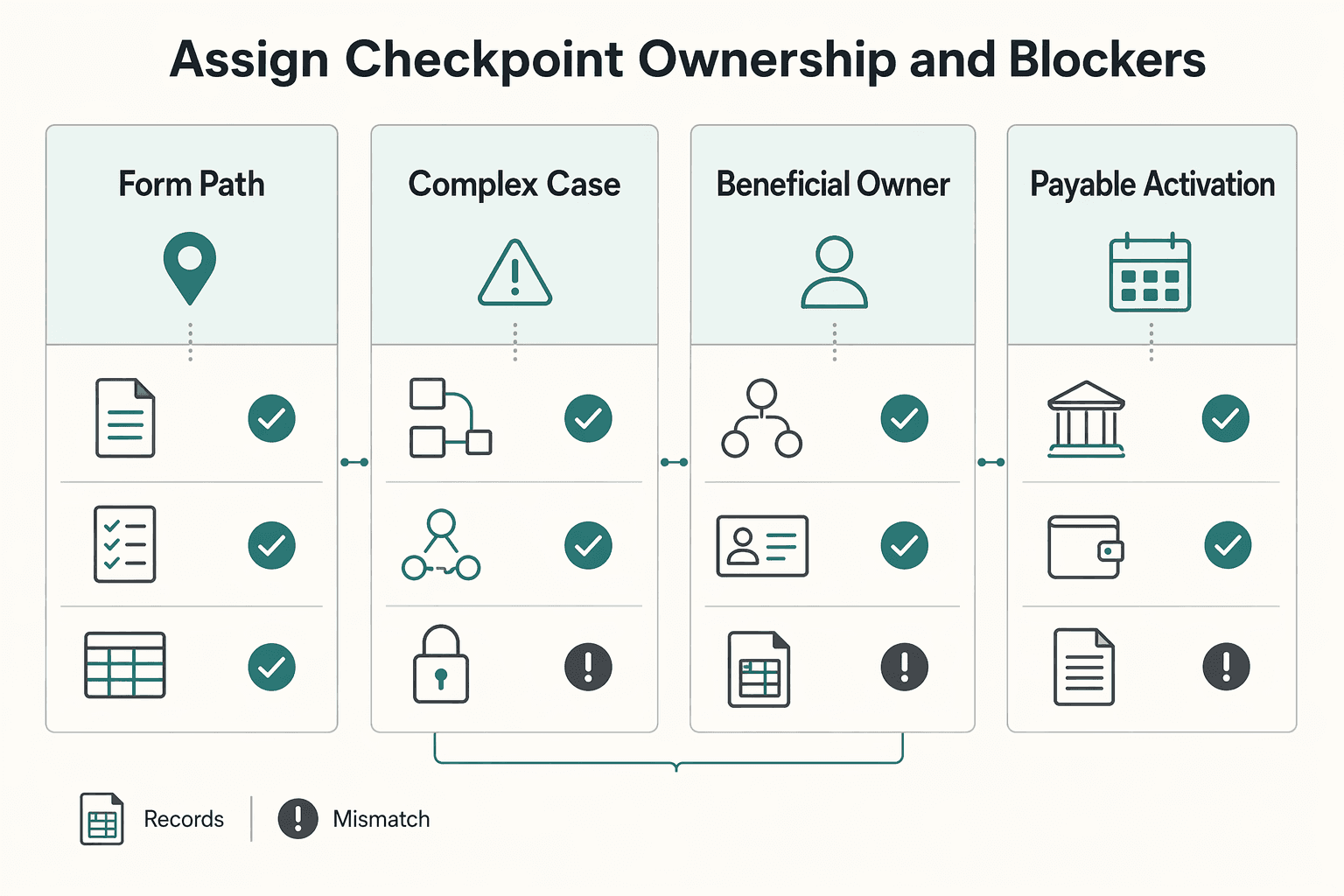

Assign checkpoint ownership and blockers#

The IRS defines withholding-agent responsibility functionally. Assign internal owners clearly so gaps do not appear between intake, review, and release.

| Checkpoint | What must be true | Owner (example) | Release blocker |

|---|---|---|---|

| Form path selection | Individual, entity, intermediary, or personal-services exception routed correctly | Designated tax owner | Wrong or unclear form path |

| Identity match | Form identity data matches onboarding record | Designated compliance/KYC owner | Unresolved mismatch |

| Beneficial-owner check | Claimed status matches payee facts and selected form | Designated tax owner | Facts indicate conflicting status |

| Payable activation | Final decision, decision owner, and timestamp attached to record | Designated payments owner | Missing decision trail |

Keep payable status as a control gate#

If the package is incomplete, field validation fails, or decision traceability is missing, keep the account off the payout rail.

This is a risk control, not paperwork hygiene. A withholding agent or payor that fails to obtain a valid Form W-8 or W-9 and fails to withhold as required may be assessed at 30% under chapter 3 or 4, or 24% backup withholding. Preserve the submitted form version, validation result, decision owner, and decision timestamp from day one.

For the full breakdown, read International Inheritance Tax Guide for Digital Nomads.

If you want a cleaner first-pass intake before reviewer sign-off, use the W-8 form generator to standardize collected fields.

Validate and route exceptions before releasing funds#

Do not release funds just because a form was uploaded. If a reasonably prudent reviewer would question the claim, place a hold and require corrected documentation or escalation before payout.

That is a withholding-agent control, not just a fraud control. The withholding agent is directly liable for withholding decisions. Under chapter 3, the baseline can be 30 percent when payment to a foreign person is not reliably documented for reduced treatment.

Use a fixed decision sequence#

| Step | What to do |

|---|---|

| Intake validation | Confirm the selected form path still matches payee facts, required fields are complete, and the beneficial-owner claim matches onboarding records |

| Exception scoring | Score by release risk, not ease of remediation; wrong-form routing and unsupported or unreviewed treaty claims are release blockers |

| Compliance hold decision | Apply a payable hold with a specific reason and assign the next action, corrected documents or specialist review |

| Payout release | Release only after the blocker is resolved and the reviewer decision is documented on the payee record |

| Post-release monitoring | Monitor profile changes, document updates, and downstream reporting impacts on Forms 1042-S and 1042 |

Treat these exceptions as high risk#

| Exception | Why it is high risk | Required action |

|---|---|---|

| Individual profile paired with Form W-8IMY | Form W-8IMY is for intermediaries, flow-through entities, or certain U.S. branches, not a general individual beneficial-owner certification | Hold payout, stop the lane, and route to tax or legal review |

| Missing or unsupported beneficial-owner claim | The form claim conflicts with payee, ownership, or entity facts | Hold payout and require corrected documentation before reliance |

| Treaty claim with no review notes | Treaty-claim defects are common, and an unchecked treaty claim is not enough | Keep hold until review notes show what was checked and the claim is approved or rejected |

Conflict is a critical red flag, not just missing data. A signed form can still be unreliable if it conflicts with profile facts or points to the wrong form lane. If documentation is unreliable or incorrect, obtain new documentation before relying on the claim.

Make hold and escalation rules explicit#

- If mismatch persists after first review: hold payout and require corrected documents.

- If corrected documents still leave ambiguity: escalate to tax or legal review.

- If ambiguity remains unresolved: do not release.

Treaty outcomes need the same discipline. A favorable treaty result does not, by itself, remove reporting obligations, so release should stay blocked when treaty review support is missing.

Build controls that survive retries and audits#

Design the hold and release path so retries do not create duplicate financial effects. Store the idempotency key with the payout decision record, and account for provider limits such as key length and retention windows.

In practice, maintain a clear event trail by recording distinct events like exception_scored, hold_applied, document_replaced, review_approved, and payout_released, with tamper-evident integrity checks.

Return clear machine-readable and human-readable hold reasons, for example wrong_form_path, beneficial_owner_conflict, treaty_review_missing, and new_document_required, so ops and client systems can distinguish compliance holds from transient payment errors.

For creator platform edge cases, see Tax Reporting for Creator Platforms: 1099s W-8s and International Withholding.

Keep records current with refresh and change-event controls#

Old documentation that still looks approved can become a control failure, so treat W-8 records as time-bound and change-sensitive, not one-time onboarding artifacts.

A Form W-8BEN is generally valid through the last day of the third succeeding calendar year, unless a change in circumstances makes information on the form incorrect. For entities using Form W-8BEN-E, change events require a new form within 30 days when correctness is affected. If you are the withholding agent, this is a direct liability issue. Without valid documentation and correct withholding, the IRS may assess 30% tax under chapter 3 or 4, or 24% backup withholding.

Define triggers that force review, not just reminders#

Use a simple rule: if an update could affect form correctness or the withholding outcome, open a refresh case. Common triggers include:

| Trigger | Why it matters | Minimum action |

|---|---|---|

| Legal entity change | Information on the signed form may no longer be correct | Hold for re-documentation and reviewer approval |

| Ownership or profile update | Information supporting status on the form may have changed | Re-validate form path and supporting profile data |

| Jurisdiction change | Country information can affect withholding and reporting treatment | Require reviewer check before continued reliance |

| Internal revalidation cycle | Policy may require periodic re-check before legal expiry | Request refreshed certification or documented reconfirmation |

Use alerts for upcoming expiry, but treat expired records and known change-in-circumstances events as decision points, not passive queue items.

Separate document status from payout status#

Keep document refresh status and payout eligibility as separate controls so stale records cannot pass silently into payouts.

In practice, track a document state, for example current, expiring_soon, expired, change_pending, replaced, and a payout state, for example payable, hold_refresh_required, hold_specialist_review. expiring_soon may still be payable under policy, but expired or change_pending generally should not remain payable unless a reviewer approves an exception and records why. Avoid updating profile data against an old W-8 while leaving payout eligibility untouched.

Make the log useful in an audit#

Use append-style event logging tied to the payee, document version, reviewer, and withholding decision, instead of editing prior records in place.

At minimum, capture event type, timestamp, actor, old value, new value, linked document, and approval outcome. Events such as profile_country_changed, document_marked_expired, refresh_requested, review_approved, and payout_hold_applied are more defensible than one mutable status field. If a hold is cleared, the record should show who approved continued reliance and what was reviewed.

Add a separate escalation for adjacent reporting issues#

When a change event suggests obligations outside withholding, open a separate escalation path instead of trying to force it through W-8 review.

That separation matters for Form 8938 and FBAR. Form 8938 is attached to an annual income tax return, while FBAR is FinCEN Form 114 and is not filed with the IRS. One does not replace the other, and each uses its own thresholds. IRS comparison guidance includes Form 8938 thresholds such as $50,000 or $75,000 for certain unmarried or married filing separately individuals living in the U.S., while FBAR uses a $10,000 aggregate account threshold. Route those issues to the tax reporting owner, and keep withholding decisions and adjacent-reporting escalations as distinct records.

Maintain an evidence pack that survives audit scrutiny#

Your evidence pack is most defensible when a second reviewer can reconstruct the reliance decision from the record alone.

Preserve the exact artifact you relied on, not just metadata. In practice, keep the submitted form, form variant and revision, validation results, reviewer notes, decision timestamp, and payout-impact status at that time. If you relied on Form W-8BEN, retain that exact version and capture the form revision, for example Rev. October 2021, where shown. Apply the same version-tracking standard to Form W-8BEN-E, Form W-8ECI, and Form W-8IMY.

Record validation evidence at a level that shows what was actually checked. Capture required-field checks, signature acceptance, whether an electronic signature indicated an authorized signer, whether the form was treated as valid for chapter 3, and whether chapter 4 validity was evaluated separately when relevant. A pass or fail flag alone is weak support if a withholding decision is challenged.

Tie each decision artifact to the controlling reference used at review time. In practice, that means the Instructions for Form W-8BEN, the IRS requester instructions for the W-8 series, and any internal policy interpretation your team applied. Also ensure intake records reflect that W-8 forms are furnished to the payer or withholding agent, not filed with the IRS as part of intake. This is a liability control. Withholding agents can be personally liable for tax that should have been withheld, including potential 30% chapter 3 or 4 assessments or 24% backup withholding when documentation is not valid.

For exportable retention outputs, a practical set is three views:

| Export | Minimum fields | PII approach |

|---|---|---|

| Reliance register | Payee ID, form type, form revision, decision date, reviewer, payout status | Mask tax IDs and exclude raw document images |

| Exception log | Payee ID, failed check, override or hold outcome, notes reference, approver | Keep reasons and approvals, not full identity packets |

| Reporting tie-out | Payee ID, withholding outcome, linked Form 1042-S record, Form 1042 batch or filing reference | Use internal IDs and reporting references instead of full profile data |

Retention timing is context-specific: keep Form 1042 copies for the applicable statute of limitations on assessment and collection, and in section 1446 contexts retain withholding certificates, statements, and related information for as long as they may be relevant.

This gives auditors and risk owners enough to test decisions without circulating unnecessary raw documents or signatures.

Fix the mistakes that repeatedly create withholding risk#

Withholding and reporting risk often comes from form misclassification and unsupported reliance, not just missing files.

Complete files alone do not fix a bad form decision. A common pattern is relying on the wrong form or continuing to rely on a form after facts changed.

The first mistake is routing every non-U.S. payee to Form W-8BEN. That form is for a foreign individual beneficial owner. Entities belong on Form W-8BEN-E. Intermediary or flow-through cases may require Form W-8IMY, and that form needs accompanying payee-association information. For personal-services income, the IRS points to Form 8233 instead of defaulting to a standard W-8BEN treaty path.

The second mistake is treating Form W-8BEN-E like a longer W-8BEN. Form W-8BEN-E is the entity form, and confusing the two is a sign that core facts still need confirmation: who the beneficial owner is, whether an intermediary is involved, and whether the claimant is the right party.

The third mistake is treating treaty eligibility as approved just because a W-8 is on file. If you have reason to know the claim is wrong, or the form lacks information needed to support a reduced rate, the payor must not apply the treaty rate.

Why collect once and forget breaks#

W-8 documentation is not one-and-done. A form is generally valid until the last day of the third succeeding calendar year from signature, unless a change in circumstances makes it incorrect earlier. The Instructions for Form W-8BEN also require notification within 30 days of a relevant change, followed by a new W-8BEN or other appropriate form.

If documentation becomes unreliable or incorrect, obtain new documentation and apply presumption-rule handling as required. Also, facts known by your onboarding or verification agent are treated as known by the withholding agent.

What to do when you discover an error#

If you find a misroute or unsupported treaty treatment, remediate in order:

- Pause reduced-rate treatment on affected future payouts. Do not keep applying treaty rates while documentation conflicts are unresolved.

- Re-collect the correct documentation. Reconfirm payee type and income facts first, then request the appropriate form.

- Document the remediation trail. Record what failed, when it was detected, what was put on hold, and who approved the corrected posture.

- Reassess withholding. If prior documentation was unreliable, evaluate whether presumption-rule treatment should have applied and whether escalation is needed.

Red flags to catch before month-end close#

Run a short exception sweep before close:

| Red flag | What to do before close |

|---|---|

| Individual profile paired with Form W-8BEN-E, or entity profile paired with Form W-8BEN | Treat the documentation as unreliable, collect updated forms, and apply presumption-rule handling before close |

| Form W-8IMY without the required payee-association details | Treat the documentation as unreliable, collect updated forms, and apply presumption-rule handling before close |

| Treaty rate requested, but relevant fields are incomplete | Treat the documentation as unreliable, collect updated forms, and apply presumption-rule handling before close |

| Form details inconsistent with payee profile or account data | Treat the documentation as unreliable, collect updated forms, and apply presumption-rule handling before close |

| Reduced rate claimed, but the file lacks information needed to establish entitlement | Treat the documentation as unreliable, collect updated forms, and apply presumption-rule handling before close |

| Form nearing expiry at the last day of the third succeeding calendar year | Treat the documentation as unreliable, collect updated forms, and apply presumption-rule handling before close |

| Known change in circumstances with no refreshed form inside the 30 days window | Treat the documentation as unreliable, collect updated forms, and apply presumption-rule handling before close |

If any red flag appears, treat the documentation as unreliable, collect updated forms, and apply presumption-rule handling before close.

For the payment ops side, see How to Pay International Contractors With Fewer Delays and Disputes.

Map controls to Gruv product operations without overbuilding#

In Gruv, keep the core control simple: documentation should determine payout release, and the release decision should be traceable for finance. If a payee can move to payable status before the correct W-8 or W-9 is collected and reviewed, you create avoidable withholding risk at the point withholding is triggered. That point is when payment is made.

Put the gate at payout release#

Treat W-8 or W-9 intake as a pre-release compliance gate, not just an onboarding checklist. For foreign individuals, generally use Form W-8BEN. For U.S. payees, use Form W-9. For foreign entities, generally use Form W-8BEN-E. Route W-8IMY cases to exception review when allocation support is incomplete. Before funds move, confirm that form type, payee type, and profile facts are consistent.

If your program supports masked tax-document handling and reviewer/timestamp audit fields, use them. Avoid a generic approved status with no reviewer identity, no decision note, and no clear record of what was validated.

Make finance able to follow the decision#

Connect release decisions to your payout status and reconciliation workflow so finance can trace intake, hold or release, payment, and reporting. This matters because withholding applies at payment release, and Form 1042-S may still be required even when no tax is withheld. If finance cannot tie hold or release reasons to payment records, close becomes manual reconstruction.

Roll out in modules#

Start with W-8 or W-9 collection, form-type validation, and exception routing for mismatches. Add deeper automation only after repeated error patterns justify it, such as entity payees being routed to W-8BEN or incomplete W-8IMY allocation packages.

Keep market and program caveats explicit. Coverage and withholding or reporting handling can vary by jurisdiction, chapter 3 or chapter 4 context, and IGA-dependent program configuration.

For a step-by-step walkthrough, see Competitive Benefits for International Contractors Without Misclassification Risk.

Conclusion#

The defensible approach here is payer-side control, not one-time form collection. If you are the withholding agent, meaning the party with control, custody, receipt, disposal, or payment authority over the income, you are responsible for the withholding decision and documenting the basis for it.

Use one operating rule before release: do not pay until the documentation path is supportable. For a foreign individual beneficial owner, Form W-8BEN should be furnished to the payer or withholding agent before income is paid or credited, and it is not sent by the payee to the IRS. If the facts point to a different documentation path, route accordingly and hold for review instead of forcing a mismatch.

Treat each W-8 as time-bound, not permanent. A Form W-8 is generally valid through the last day of the third succeeding calendar year, but validity can end earlier if a change in circumstances makes the form incorrect. Form W-8BEN instructions also require notice of relevant changes within 30 days.

This is a control obligation, not a formality. IRS instructions state that if a withholding agent or payor fails to obtain a valid Form W-8 or Form W-9 and fails to withhold as required, assessment exposure can include 30% under chapter 3 or 4, or 24% backup withholding in the relevant case. Treaty claims are conditional, so apply a reduced rate only when the claim aligns with the documented facts.

Keep an auditable evidence pack per decision, such as the submitted form version, validation results, reviewer identity, decision timestamp, review notes, and payout-impact status. That record can support both the original payment decision and ongoing obligations, including annual Form 1042 filing unless an exception applies.

If you want one closing rule for tax withholding international contractors w-8, use this: proceed only when form type, payee facts, and withholding outcome align. When any one of those three breaks, hold and escalate.

When you're ready to implement these controls in production workflows, review the Gruv docs and map the checklist to your payout gates. ---

Frequently Asked Questions

Do contractors send Form W-8BEN to the Internal Revenue Service (IRS) or to the payer?

Contractors give Form W-8BEN to the payer or withholding agent, not directly to the IRS.

Is Form W-8BEN only for claiming tax treaty benefits?

No. Form W-8BEN is also used to certify foreign status even when no reduced treaty rate or exemption is claimed. Treat foreign-status documentation and treaty eligibility as separate checks.

Who should act as the withholding agent in a platform payout model?

The withholding agent is the U.S. or foreign person with control, custody, or payment authority over amounts subject to withholding. In platform payouts, this is a facts-and-flow determination, not a label by preference. If responsibility is split across entities, map the payment chain before launch.

How do teams choose between Form W-8BEN, Form W-8BEN-E, and Form W-8IMY?

Use Form W-8BEN for a foreign individual beneficial owner and Form W-8BEN-E for a foreign entity documenting chapter 3 or chapter 4 status. Use Form W-8IMY for foreign intermediaries or flow-through entities rather than beneficial owners. If a W-8IMY is missing the information needed to associate payments to payees, do not treat that form alone as sufficient for release.

What is the minimum checklist before releasing an international contractor payout?

At minimum, confirm the correct W-8 form type and that documentation can be reliably associated with the payee. For W-8IMY cases, confirm the accompanying association or allocation information is present. If documentation cannot be reliably associated, amounts subject to withholding may default to 30 percent withholding.

When should a treaty claim be escalated instead of auto-approved?

Escalate when treaty eligibility is unclear based on the submitted documentation. If eligibility is in doubt, the payor must not apply the treaty rate. For treaty-based return positions, Form 8833 can be relevant, but it is not automatically required for every treaty claim.

How long should W-8 decision evidence be retained for audit defense?

Do not apply a blanket fixed-year rule to all W-8 decision evidence. Retain records as long as their contents may become material to administering Internal Revenue law. Also separate validity from retention: Form W-8BEN is generally valid through the last day of the third succeeding calendar year unless a change in circumstances makes it incorrect.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

How to Pay US Subcontractors from Canada

Engaging U.S. talent can be a strong growth move for a Canadian business. The challenge is making the cross-border mechanics feel routine on your side and invisible on theirs. If payments, compliance, and reporting are sloppy, you create financial risk, waste time, and look less credible to the people you want to keep. When they are handled well, your back office starts to work in your favor.

Cross-Border Invoicing: VAT, GST, and Withholding Tax

Treat cross-border invoicing as three linked decisions, not one: where indirect tax is due, whether withholding applies, and what evidence supports both positions. In workflows that touch VAT, GST, and withholding tax, the most expensive mistakes usually start with a narrow question such as, "What should appear on the invoice?" That is not enough. The invoice is only the visible output. The real control point is the decision you make before the invoice exists.

Creator Platform Tax Reporting for 1099 and W-8 Expansion Decisions

Tax form routing is an operating decision, not a creator support task. When it goes wrong, you see payout delays, avoidable withholding, and reporting risk. For creator platforms, the core job is to classify payees before the first payout and keep that logic defensible as volume grows.